While stock dividends sound glamorous and warm the hearts of uninformed investors, the truth is that they are a wasteful method of reducing surplus, beneficial, perhaps, to marketwise insiders, but costly to stockholders and the firm that declares them. This article analyzes the cost of the average melon.

Get full access to this article

View all access options for this article.

References

1.

One can illustrate from works of the highest quality. For example: “The stock dividend has no real effect on the stockholders.”MoonitzM.StaehlingC. C., Accounting—An Analysis of Its Problems (Brooklyn. 1952), vol. 2, p. 140. “From the stockholder standpoint the stock ‘dividend’ transaction is nothing more nor less than a straight split-up.”PatonW. A.Jr., Corporation Accounts and Statements (N.Y., 1955) p. 128.

2.

WhitakerA. C., “The Stock Dividend Question,”American Economic Review, Mar. 1929, vol. 19, no. I, p. 39.

3.

See note 2, p. 28–29, 32–33.

4.

“Stock Dividends, Investment Trusts, and the Exchange,”American Economic Review, June 1931, vol. 21, no. 2, p. 279.

5.

WilcoxE. B., dissenting to American Institute of Accountants. Accounting Research Bulletin No. 11 (Revised), “Accounting for Stock Dividends and Stock Split-Ups.” (N.Y., 1952), p. 104-A.

6.

Whitaker, “The Stock Dividend Question,”loc. cit., p. 34.

7.

“The surplus is frozen by the stock dividend so that it cannot later be distributed as a cash or property dividend.”LattinN. D., The Law of Corporations (Brooklyn. 1959), p. 467. “A dividend is basically a distribution of corporate assets, and it is nothing short of ridiculous … to label a procedure which ensures the permanent retention … of a specified amount of income funds as a ‘distribution.’” Paton and Paton, note 1, p. 95; see also p. 127. Paton and Paton place quotation marks around “dividends” of stock. Accounting Research Bulletin No. 11 (Revised) suggests that large or repeated issuance of new shares be called a “split-up” or, less desirably, “a split-up effected in the form of a dividend.” Op. cit., p. 102-A.

8.

See DewingA. S., Financial Policy of Corporations, 5th ed. (N.Y., 1953), vol. I, ch. 22.

9.

See note 8, p. 122. This is also called “a strong argument” in WixonR., ed., Accountants Handbook, 4th ed. (N.Y., 1956), p. 21–43.

10.

This is pointed out by Moonitz and Staehling, note 1, vol. 2, p. 141.

11.

MoonitzStaehling, note 1, vol. 2, p. 142. Nevertheless, it must be conceded that precisely because of its misleading implications, “The stock dividend may be very helpful in securing the stockholders' acquiescence in this policy of reinvestment of earnings.” Whitaker, “Stock Dividends,”loc. cit., p. 279.

12.

Op. cit., p. 132.

13.

Dewing remarks, “In making this transfer from surplus to capital stock the directors should realize that the average stockholder values his ownership in the corporation only as a source of cash dividends.” Op. cit., vol. 1, p. 782, fn. ggg.

14.

Letter of 11 February 1960 from GlenneyFrank E., Investment Administrator, Moody's Investors Service.

15.

Historically, a fifth burden was sometimes relevant. Until “the middle [nineteen] thirties, stockholders in our national banks were liable for the bank debts up to the par value of their shares.”Dewing, op. cit., vol. 1, p. 15.

16.

“There is evidence that many financial managements, sensitive to critical attitudes of employees and others with respect to higher dividends, prefer increasing the number of shares … to increasing the amount of cash per share. This is rather silly, as … there should be no necessity either for apologizing for or disguising such an increase.” PatonPaton, op. cit., p. 128.

17.

Studies have yielded positive correlations between payout ratios and share prices per dollar of current earnings. ModiglianiF.MillerM. H. point out that these correlations may reflect, not investors' desire for income or lack of understanding, but merely the fact that dividends are regarded as indications of other things, most notably insiders' views as to the firm's long-run earning power. “The Cost of Capital, Corporation Finance, and the Theory of Investment: Reply,”American Economic Review, Sept. 1959, vol. 49, p. 668. In either event, it pays to have an increase in dividends visible.

18.

PatonPaton, op. cit., p. 115, remark. “About the only excuse one can think of for converting retained earnings into bonds is to develop an interest charge for the sake of increasing tax deductions… . Even this point has its offset in the fact … that the bonds issued are legally income to the recipients, in the amount of their fair market value.”

19.

The popular view is that: A stock dividend is roughly equivalent to a cash dividend because the recipients could realize cash by selling the additional shares. The obvious answer is that a stockholder could sell part of his proportionate interest in the company whether or not there is an increase in the number of shares into which his interest is divided. Hence, if any benefit is obtained, it must be of the sorts mentioned in the text; that is, either it must become more convenient for stockholders to sell part of their holdings, or their holdings must be increased in value because price per share decreases a smaller proportion than the number of shares increases. It is also without merit to argue that a stock dividend conserves cash, avoids underwriting fees, provides cheap capital, or saves on income taxes: There is no reason why a cash dividend of equal bookkeeping amount would otherwise have to be declared. It is misleading to state that. “The alternative to the stock dividend … is the disbursement of a cash dividend followed by issue of privileged subscription rights… . Such procedure would have been very costly … because [of] personal income taxes on dividends and because of the underpricing and underwriters' fees necessary… .” Accountants' Handbook, op. cit., p. 21–43. See also Bothwell, cited in footnote 23.

20.

See especially the study of Burrell, cited in footnote 23 below.

21.

Cf. Dewing, op. cit., vol. 2, p. 1188.

22.

Both parts of this sentence are supported by the studies, cited in footnote 23, of Dolley and of Fogg, Wider distribution of ownership may also be a prerequisite of listing on an exchange. It has also been said that wider distribution of ownership will reduce the chance of capture of control by “pirates,” will lessen price fluctuations “because there is less money invested in the average holding which can be shaken out if a market break occurs,” and will facilitate raising capital because “the added contribution which is asked of each individual stockholder is smaller.” (The quotations are from the article in Barron's cited in footnote 23.) Indeed, according to Dolley, wider ownership is, for management, the primary purpose of splits, despite the higher costs attendant on wider ownership.

23.

The evidence, indeed, is contradictory. And even where the results are positive, as in the study of Myers and Bakey, there are some disconcerting notes. Thus the only attribute that Myers and Bakey found among their 70 stocks that was significantly associated with an increase in value was a low pre-split price (less than $60). Similarly, the article in Barron's asserts that “There also appeared to be only a slight relation between the size of the split and the size of the increase in stockholders.”

24.

See: Barron's Magazine, Sept. 15, 1947, vol. 27, no. 37. BothwellJ. G.Jr.“Periodic Stock Dividends,”Harvard Business Review, Jan. 1950, vol. 28, pp. 89–100. BurrellO. K., “Price Effects of Stock Dividends,”Commercial and Financial Chronicle, Convention Number, Dec. 2, 1948, pp. 10, 68–70. DolleyJ. C., “Common Stock Split-Ups—Motives and Effects.”Harvard Business Review, Oct. 1933, vol. 12, pp. 70–81. FoggP. S., Stock Split-Ups (Harvard Graduate School of Business Administration, 1928). LivermoreS., “The Value of Stock Dividends,”American Economic Review, Dec. 1930, vol. 20, p. 687. MyersJ. H.BakeyA. J., “The Influence of Stock Split-Ups on Market Price,”Harvard Business Review, Mar. 1948, vol. 26, pp. 251–55. SiegelS. N., “Stock Dividends,”Harvard Business Revew, Oct. 1932, vol. 11, pp. 76–87.

25.

Lattin comments, “While the shareholder derives no greater property interest by the issue of another piece of paper, he does find it more convenient, in case he desires to sell, to have these share-dividend units to use instead of splitting his larger units… . The inconvenience does not add up to much.” Op. cit., p. 465.

26.

PorterfieldJ. T. S., “Dividends, Dilution, and Delusion,”Harvard Business Review, Nov.-Dec.1959, vol. 37, no. 6, p. 60.

27.

Op. cit., p. 665.

28.

For exceptions to this and the next point, see footnote 29 below and the text sentence preceding it.

29.

See footnote 42.

30.

Another exception to the nonreduction of surplus applies to the splitting of par-value stock whose par value has reached the minimum (often one dollar, but sometimes less), if there is one, specified by the chartering state for shares with par value. Further split-ups would require either charges to a surplus account or a conversion to no-par stock (which is authorized in all states except Nebraska).

31.

The requirement is unfortunate from an accounting viewpoint. “The preferable accounting procedure … [for a stock dividend is to use] the capital book value per share (either par or stated value or, more logically, average amount received per share from stockholders)… .” PatonPaton, op. cit., p. 125. See also MoonitzStaehling, op. cit. However, the requirement has the sanction of Accounting Research Bulletin No. 11 (Revised), op. cit., p. 101-A—with dissents.

32.

Dilution of participated preferred stock, as well as dilution of convertible bonds and stocks, and stock warrants and options, should be recognized as an additional way in which a stock dividend may benefit the common stockholders. The benefit depends on the existence of these instruments, on the absence of enforceable protective provisions in their contracts, on the decision not to alter their rights proportionately, and on the preservation of the corporation's reputation. If these conditions are met, however, a stock split could also result in dilution (unless the contracts have a loophole only for stock dividends or the corporation is chartered in Nebraska, which (cf. DonaldsonE. F., Corporate Finance, (N.Y., 1957), p. 110, fn. 1) requires that all shares have the same par value). Indeed, as just indicated in the text, dilution by a split can be easier—provided the preferred would not veto the charter amendment, which is required except in the case of “true” no-par shares.

33.

Cf. Donaldson, op. cit., p. 110.

34.

Cf. Donaldson, op. cit., p. 830; BogenJ. I., ed., Financial Handbook.3d. ed. (N.J., 1945), p. 792.

35.

GuthmannH. G.DougallH. E., Corporate Financial Policy, 3d. ed. (Englewood Cliffs, N.J., 1955), p. 47, 48.

36.

Donaldson, op. cit., p. 60.

37.

Delaware Code Annotated, Title 8, sec. 503c.

38.

Letter of 9 May 1960 from BobbR. J., Chief, Excise Tax Branch, Internal Revenue Service, Washington, D.C.

39.

Letter of 20 April 1980 from CallananR. L., Department of Public Information, New York Stock Exchange.

40.

New York Stock Exchange, Department of Stock List, Schedule of Listing Fees (1 March 1950).

41.

Telephone conversation.

42.

Thus, the NYSE initial fee for Dow was in fact $1,775, not $1,330 as in our calculations. The annual fee was in fact $300 per year, not $266.

43.

The rate is one cent per share on shares sold at less than five dollars, two cents for $5.00-$9.99, and three cents for $10.00–19.99, Rates in several other states are given in The Fitch Stock Record:

44.

Donaldson, op. cit., p. 434.

45.

As of 1 January 1959 the federal stock transfer tax became four cents for each $100 (or major fraction thereof) of actual value of the total shares transferred, but in no case less than four cents on the entire transaction or more than eight cents on each share. The eight-cents maximum implies that stock dividends can also increase the federal tax. This would occur if the price per share of the larger number of shares remained above $200. However, publicly held common stocks usually are kept below $200 for “marketability.”

46.

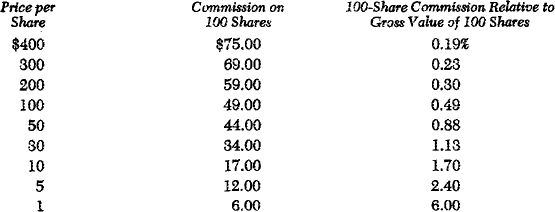

Since April 1959 the following commission rates have been in effect on the country's major stock exchanges for a transaction of 100 shares or less, except that the commission is two dollars less in the case of an odd lot amounting to $100 or more: Notwithstanding the above, when the money value is $100 or more, the commission shall not exceed $1.50 per share or $75 per single transaction, but in any event shall not be less than six dollars per single transaction. In the case of a number of 100-share lots, or of one or more 100-share lots plus an odd lot, each part is regarded as an entirely separate transaction. These rates imply the following relation between selling price and commission:

47.

This and the next point do not apply to shares sold over the counter. There brokers' commissions are supposedly a uniform five percent, the bid-ask spread is apparently about proportional to the selling price, and there is no odd-lot differential.

Notwithstanding the above, when the money value is $100 or more, the commission shall not exceed $1.50 per share or $75 per single transaction, but in any event shall not be less than six dollars per single transaction. In the case of a number of 100-share lots, or of one or more 100-share lots plus an odd lot, each part is regarded as an entirely separate transaction. These rates imply the following relation between selling price and commission:

Notwithstanding the above, when the money value is $100 or more, the commission shall not exceed $1.50 per share or $75 per single transaction, but in any event shall not be less than six dollars per single transaction. In the case of a number of 100-share lots, or of one or more 100-share lots plus an odd lot, each part is regarded as an entirely separate transaction. These rates imply the following relation between selling price and commission: