Abstract

With the ending of the operational first year of the American Affordable Care Act, health insurance premiums were accessed online. For a US$50,000 income, the lowest premiums ranged from US$805 annually (age 20 years) to US$3802 (age 64 years), while the highest ranged from US$2186 (age 20 years) to US$10,326 (age 64 years). The lowest premiums at age 50 years were higher in rural areas in contrast to the highest premiums that were less expensive rurally. At age 64 years, the lowest premiums were 9–12.6% of a US$50,000 income, while the most expensive varied between 16.5 and 39%. Access to gynecologic oncologists was variable in different networks. Medicaid enrollment nationally was ∼6x higher than paid enrollment. Eligible participation in Affordable Care Act coverage exceeded expectations by >190%. Performance of four healthcare exchange traded funds indicated that investor confidence is high in the American healthcare sector.

On 31 December 2014 the first operational year of the American Affordable Care Act (ACA) ended while second year enrollments were underway for new and existing participants [1–4], so that it became possible to tabulate first year enrollment and premium prices of ACA health insurance for the second year of operation. The healthcare insurance system in the USA prior to the ACA was cumbersome and complicated stretching the comprehension of individuals and their caregivers, and while the ACA has introduced significant changes designed to extend coverage to many more Americans, it too seems cumbersome and complicated with its own vexations [5–7].

Legislation for the ACA (Patient Protection And ACA) was created at the onset of the Great American Recession in 2008, which involved government bailouts of American banks and the American auto industry. The legislation for ACA service provisions received amendments and was coupled to budgetary reconciliation in separate legislation [8–10]. Year 1 enrollments in various ACA health insurance plans began in November of 2013 with availability of coverage beginning 1 January 2014. This availability of coverage coincided with a major economic recovery in the USA. ACA health insurance coverage was designed to have a closing date for enrollment and annual re-enrollments so that insurance exchanges would not be open to enrollments for most of each year, except for certain special circumstances. The 31 December 2014 closing enrollment date received 4–6 week extensions by the President. For year 2, the ACA health insurance exchanges re-opened for additional new and changed enrollments on 15 November 2014 and closed on 15 February 2015. Certain extenuating circumstances allowed for enrollment in ACA coverage beyond this point. To begin to understand the access to health insurance in the USA, one must realize that most individuals in the USA consider healthcare to be local, thinking in terms of nearby doctors and healthcare facilities. Consequently, arranging healthcare insurance coverage by long distance using telephone, fax or internet can seem discordant with local access. This report focuses on the local aspect of access to health insurance, especially premium costs and participation. This presentation is not comprehensive, but tailored to bring to world readers a cross-sectional street-view of the initial year of operation of this new American healthcare program.

Methods

The authors explored the range of premiums on exchange-based qualifying health plans (QHPs) for Kentucky [11], California [12], Minnesota [13], Alabama [14], Nebraska [14], South Carolina [14] and Utah [14]. The costs of insurance in four cities of each state were obtained. The two largest cities were included, as well as two rural cities with the widest geographical separation, chosen at random.

Information on overall enrollments in exchange QHPs and Medicaid was obtained as cited from state, federal and foundation sources.

Because Kentucky has been highly successful in ACA initiation, leading the nation in enrollments [15], it has been featured in this report.

Visited sites were abstracted by four of the authors and checked for concurrence. Nonconcurrent summaries were re-examined and adjusted for accuracy. In making observations to evaluate the usable quality related different exchange web sites, the following criteria were employed:

The site used all parameters on which premium price would be based (applicant age, dependent age and income);

The site used a locating zip code to determine premium cost for different locations;

The site determined tax credits and premium cost to distinguish the actual cost;

The site returned multiple premium results that could be compared.

Exchange web sites that met all of these criteria were designated as excellent and straightforward for the purposes of this report.

Results

Entry point for the purchase of health insurance coverage

Individuals in the state of Kentucky purchase health insurance through the Kentucky Health Insurance Exchange. Accessibility to the exchange is through multiple means, including internet, telephone and in person at enrollment centers with the aid of certified financial assistors called ‘kynectors’.

A snapshot view of the Kentucky Health Insurance Exchange (KY-Nect) [11], the web-based access and purchase point is as follows: the online user progresses through several screens that collect information to determine the scope of an individual's eligibility for various health insurance plans. The spectrum of available plans includes different premium costs and different potential levels of payment reduction through a government tax credit. A summary screen informs the applicants of what plans they are eligible for. The coverage to be considered is fine-tuned for certain options (i.e., medical alone or medical and dental), and then further fine-tuned for personal cost, deductibles and out-of-pocket limits with slider filters. Finally, the user is advanced to an array of health insurance purchase choices that include premium costs.

When the health insurance suitable to the user is found and selected, a process of user vetting is begun that involves submission of documents to qualify for subsidized discounted rates, the issuing of an application ID, insurance plan selection with the insurance company, receipt of the bill from the company and processing of payment for the initial coverage period. In the first year of operation, delays in this enrollment process extended 2–4 weeks [16]. Time to start of coverage was shorter in Kentucky, but the kynect exchange currently states that applications would take two weeks to begin coverage [17]. All coverage began as of 1 January 2015, and applications submitted later in the year were the most likely to have delayed coverage. No coverage was issued without completion of the payment process. Some individuals did not submit their first monthly payment and consequently did not complete the enrollment process. In contrast to the online purchase of automobile insurance [18], a delay to coverage was routine to both the online and telephone enrollment process when qualification for a subsidy was an issue. Individuals with incomes above subsidy levels could obtain next day coverage using a bankcard both online and by telephone.

Consumer cost issues of health insurance for fiscal year 2015

We have structured this report to deal with the lowest bronze premiums and the highest platinum premiums. We have not dealt with every plan, nor every family size, nor every income and consequently have not dealt with silver plans (lying between lowest bronze and highest platinum). The mother–daughter family illustration that we present allows them to take advantage of the lowest premiums available with the subsidized bronze plan and also explores what a top-tier platinum plan would cost in the event that they would anticipate heavy use of the healthcare system. Any consideration, for example, of the silver plan cost sharing neither conserves income with low premiums nor presents any advantage for heavy use of the healthcare system in the mother-daughter family illustrated in this report.

Financial factors for a woman purchasing health insurance in Louisville, Kentucky.

Note that premiums are highest at age 64 years with eligibility ending at age 65 years.

All $ currency is in US$.

Must sign up before February 15 to avoid penalty, extended to 30 April 2015. Filling single not as head of household.

FPL: Federal poverty level; MAGI: Modified adjusted gross income.

The premium subsidy threshold is based on 400% of the federal poverty level that changes with family size. MAGI is determined from US Federal Income Tax Forms and other information [22]. In

The penalty for failing to enroll in health insurance before February 15 was estimated at 1% of income above the income filing limit of US$10,150 for 2014 and at 2% for 2015. A woman with a dependent child receives a tax credit discount to her monthly premium because together they are below the family-size dependent premium subsidy threshold and the premiums shown have had the discount applied (case B,

Cost of health insurance in Kentucky for a single woman.

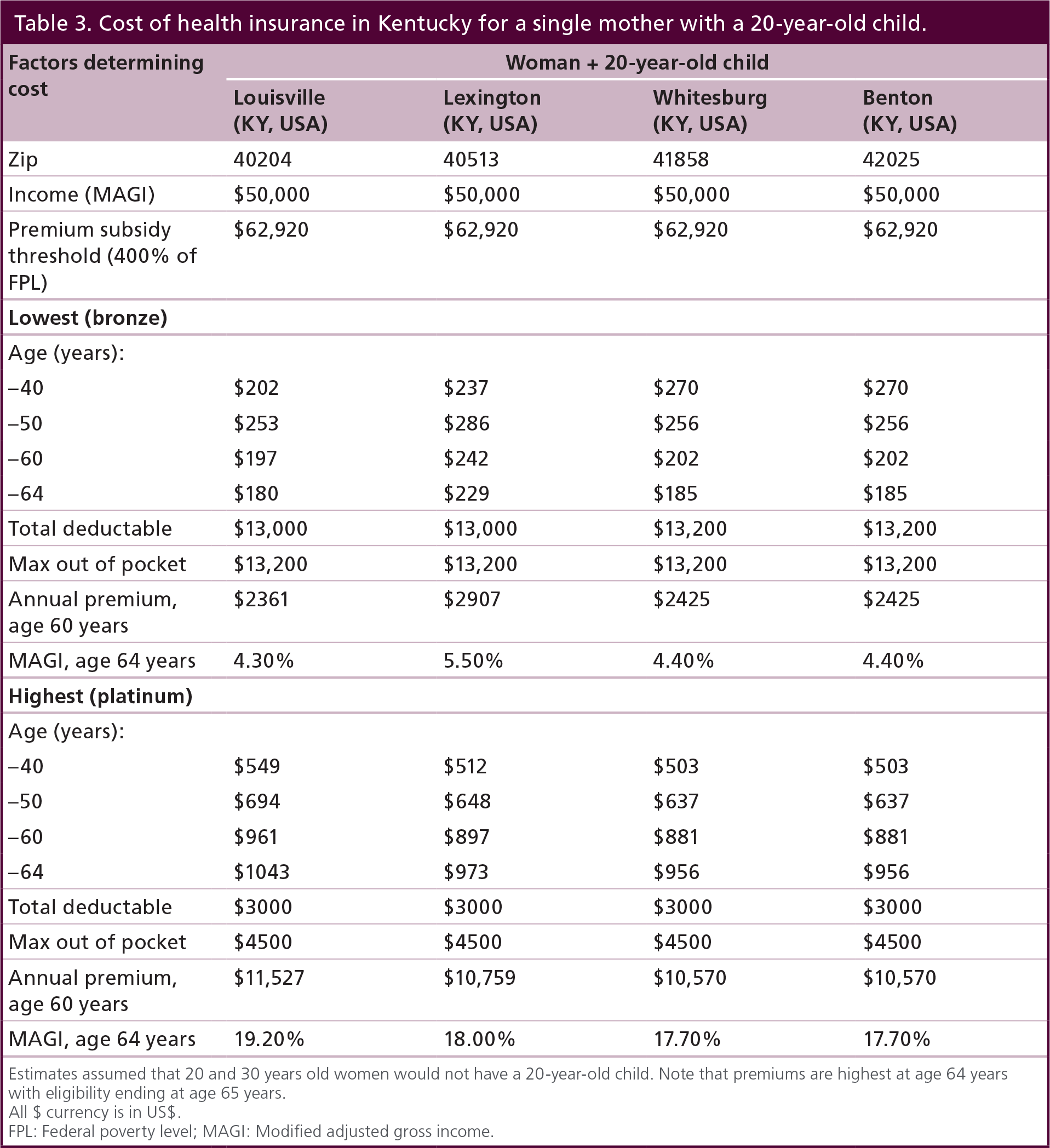

Louisville and Lexington have Kentucky's two largest metropolitan areas. Whitesburg is located in Appalachian eastern Kentucky and Benton is 375 miles away in a low population region of western Kentucky.

Note that premiums are highest at age 64 years with eligibility ending at age 65 years.

All $ currency is in US$.

FPL: Federal poverty level; MAGI: Modified adjusted gross income.

Cost of health insurance in Kentucky for a single mother with a 20-year-old child.

Estimates assumed that 20 and 30 years old women would not have a 20-year-old child. Note that premiums are highest at age 64 years with eligibility ending at age 65 years.

All $ currency is in US$.

FPL: Federal poverty level; MAGI: Modified adjusted gross income.

Penalties at tax time

For a single mother with a 20-year-old child, their family MAGI is under the US$62,920 premiums subsidy threshold, so that they are entitled to an immediate subsidy discount applied each month to their health insurance premiums

Fiscal year tax increase for health insurance tax credits forfeited by increased income from US$50,000 to US$65,000 for a single mother with a 20-year-old child in different regions of Kentucky.

All $ currency is in US$.

Estimation is based on filing single not as head of household. Note that premiums are highest at age 64 years with eligibility ending at age 65 years.

Cross-sectional survey of health insurance cost to American consumers

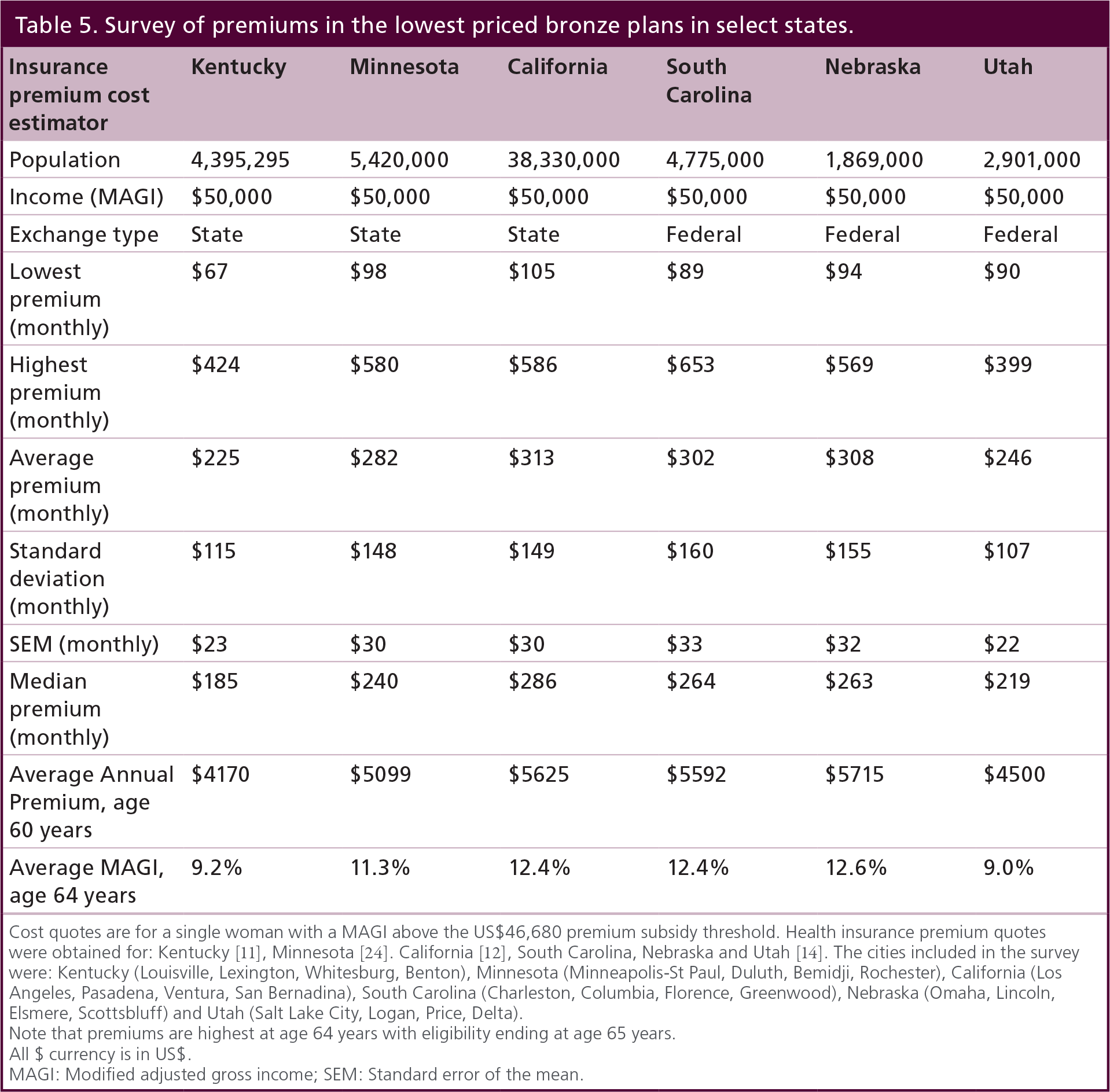

Three states that had state-run health insurances exchanges (Kentucky, Minnesota and California) and three that did not (South Carolina Nebraska, Utah: health insurance purchase on the Federal exchange) were examined. Central measures were determined over all ages and for four cities. Kentucky had the lowest average bronze premiums across all ages

Survey of premiums in the lowest priced bronze plans in select states.

Cost quotes are for a single woman with a MAGI above the US$46,680 premium subsidy threshold. Health insurance premium quotes were obtained for: Kentucky [11], Minnesota [24]. California [12], South Carolina, Nebraska and Utah [14]. The cities included in the survey were: Kentucky (Louisville, Lexington, Whitesburg, Benton), Minnesota (Minneapolis-St Paul, Duluth, Bemidji, Rochester), California (Los Angeles, Pasadena, Ventura, San Bernadina), South Carolina (Charleston, Columbia, Florence, Greenwood), Nebraska (Omaha, Lincoln, Elsmere, Scottsbluff) and Utah (Salt Lake City, Logan, Price, Delta).

Note that premiums are highest at age 64 years with eligibility ending at age 65 years.

All $ currency is in US$.

MAGI: Modified adjusted gross income; SEM: Standard error of the mean.

Survey of premiums in the most expensive platinum plan in select states.

Cost quotes are for a single woman with a MAGI above the $46,680 premium subsidy threshold. Health insurance premium quotes were obtained at: Kentucky [11], Minnesota [24]. California [12], South Carolina, Nebraska and Utah [14].

Note that premiums are highest at age 64 years with eligibility ending at age 65 years.

All $ currency is in US$.

MAGI: Modified adjusted gross income; SEM: Standard error of the mean.

Observations on state run exchanges

From the stand-point of usability of state exchange web sites, California, Kentucky and Minnesota were excellent and this defined their prominent use in this report. In addition, Idaho had an excellent, straightforward site. Some issues found at state exchange web sites were as follows.

The site:

Did not accept income to estimate health insurance costs (Colorado);

Did not accept age for calculating estimates (New York, Vermont);

Did not accept the age of a dependent for calculating estimates (Washington);

Did not allow zip code, city or county to be specified (Rhode Island, Vermont);

Did not adjust for or show the tax credit (Colorado, Hawaii);

Made user log in and enroll in order to get all the coverage choices available (Washington, DC);

Had results that could not be sorted by the price of premium and were randomly listed (Washington).

It should be understood that when an individual is participating in an ACA-qualified health insurance plan, they need to receive their care from physicians in that plan's provider network. For individuals with specific needs, determining if certain specialists were in the network and nearby could be important. Our efforts examined physician participation and their proximity by inquiring if the provider network included care from a gynecologic oncologist. The most common problematic issue was finding network information on the exchange web sites. Consequently, our inquiries were performed on the providers Internet sites and involved some persistence to examine provider networks associated with the health insurance plans that we surveyed. The bronze plans with the lowest premiums matched to 15 gynecologic oncologists in Louisville and Lexington that were within 100 miles (closest 1.1–35.9 miles; furthest 11.2–83.7 miles). The platinum plans with the highest premiums matched to three gynecologic oncologists in Louisville and 13 in Lexington that were within 100 miles (closest 3.6–4.2 miles; furthest 3.6–11.8 miles). Distance was a bigger factor in rural Kentucky, so that four matches to gynecologic oncologists for Whitesburg required 25–46 miles of travel, while in Benton 133–210 miles of travel were required and extended out of state. The Whitesburg referral addresses could not confirm practices that included a gynecologic oncologist while the Benton referral addresses did. One provider network serving Lexington listed a referral address that did not include gynecologic oncologists in their practice. While care by a gynecologic oncologist may be achieved through institutional affiliations in these cases, this assumption could not be confirmed by a consumer trying to make an insurance decision based on this availability. Although these inquiries were limited to four Kentucky cities, they demonstrated that there is considerable variability in provider network information about access to care from a gynecologic oncologist.

State-by-state enrollments in ACA healthcare insurance coverage

The basics: The major opportunities provided by the ACA involve enrollments in exchange-based qualified health plans (exchange QHP), Medicaid, and the Children's Health Insurance Program (CHIP). As demonstrated earlier, enrollment in exchange QHPs may or may not be discounted depending on an individual's MAGI and will be either through the federal exchange (Healthcare.gov: 29 states) or through state run exchanges

Enrollment in the Affordable Care Act's qualified health plans, Medicaid and Children's Health Insurance Program.

Summary is current to February–March 2015

ACA: Affordable Care Act; CHIP: Children's Health Insurance Program; QHP: Qualified health plan

Macroparticipation in exchange QHPs & Medicaid/CHIP: all in?

Overall enrollment in Exchange QHPs was 41.4% nationally

Kentucky had the greatest increase in Medicaid/CHIP enrollments over Pre-ACA enrollment (81%:

Enrollment (

Economics & paying for it all!

The original ACA legislation appropriated US $100 billion over the period 2010–2019 in mandatory funding and another US$100 billion in discretionary funding over the same period [36]. Grant funding to individual states of US$4.99 billion [37,38] has been made to implement the ACA with California and New York receiving the most. Kentucky received the fifth most and Minnesota the 13th most. Moving forward in the long-term, Federal spending for Social Security and the government's major healthcare programs – Medicare, Medicaid, the Children's Health Insurance Program, and subsidies for health insurance purchased through the exchanges created under the ACA – would rise sharply, to a total of 14% of gross domestic product (GDP) by 2039, twice the 7% average seen over the past 40 years. That boost in spending is expected to occur because of the aging of the population, growth in per capita spending on healthcare and an expansion of federal healthcare programs [39]. With such a substantial increase, it is reasonable to ask: what will be its effects? No answer exists at present because there are so many moving parts to the assumptions made for healthcare projections involving a strengthening economy, constraints on federal spending, lowering of federal deficits, while unknowns include: pressures from an aging population, rising healthcare costs, expansion of federal subsidies for health insurance, increases in interest rates, and so on. However, the investment market may provide surrogate indicators of where this is all going. Regardless of personal or programmatic politics, the financial sectors independently grow where investors perceive the best rewards and the lowest risks.

Discussion

What are the innovations that the ACA brings to Americans seeking healthcare coverage?

The consumer-based perspective presented here can be considered in terms of five consumer applications (app) that the ACA brings to Americans as follows:

Consumer App #1 removes access barriers to health insurance and hence healthcare. Previously, the ACA's pre-existing conditions could prevent all coverage for the specific pre-existing condition, premium discrimination could raise premiums for certain conditions on individual policies issued to prevent enrollment of individuals with these conditions, and insurers could change the terms of coverage at any time after enrollment to exclude or limit coverage on certain conditions (rescissions). The ACA has since removed these barriers.

Consumer App #2 implements choices with regard to price and plan benefits. Online access provides what the consumer wants at the price that they decide to pay. Bronze, Silver, Gold and Platinum plans provide step-wise coverage of healthcare costs that are covered (60, 70, 80, 90%, respectively), as well as stepped deductibles and out-of-pocket costs.

Consumer App #3 makes coverage of Essential Health Services [41] universal to all ACA QHPs, as well as to private insurance plans created or purchased after 23 March 2010 [42]. At least 15 free preventive services and one wellness visit are covered by ACA QHPs without copayments (a fixed amount the consumer pays for covered services, typically at the time of the service) and coinsurance (the share of costs of the allowed amount for a covered service after reaching the deductible), regardless of whether the deductible has been met. It does not include premiums, or costs that are not covered by a plan. Once the deductible is met, the plan will pay its share of the plan's coinsurance. These essential health services must be done in-network, and there are costs to the consumer otherwise.

Consumer App #4 provides affordability through federal financial assistance with cost of QHPs to consumers, expansion of Medicaid and consumer selection of their share of covered services payment responsibilities. The ACA provides variable assistance that discounts the cost of QHPs to those with MAGIs that are up to 400% of the federal poverty level and expands Medicaid in participating states to 133% of the federal poverty level. In addition, individuals can decide on QHPs with a monthly premium that is acceptable and in line with their anticipated healthcare needs, which would be least expensive for individuals that will need little or no medical care.

Consumer App #5 mitigates financial ruin by removing caps on annual benefits and on lifetime benefits and by placing maximums on out-of-pocket expenses for covered services. Prior to the ACA QHPs, healthcare bankruptcy loomed when annual or lifetime dollar limits had been exceeded so that coverage no longer applied. In addition, catastrophic illness during the deductible phase could impose extreme out-of–pocket expenses and be financially ruinous [43]. The ACA qualifies out-of-pocket limits based on income and family size. For the healthcare consumer at ground zero, these applications of the ACA have enormous impact.

Is health insurance coverage affordable for Americans?

Affordability is the key promise of the ACA. Delivering this promise has several moving parts, including base price, usage costs (deductibles, out-of-pocket expenses), penalty for incomplete participation, reconciliation on federal income tax and increased cost over time. Cost average reports have placed increases at ∼5% nationally [18–20], but the cost of health insurance premiums for 2015 range from 22% decreases to 35% increases [44]. Notably, average figures result from what is used to compute the average (all policies vs all policies expected to be purchased [i.e., weighted by the distribution that is purchased]), so that the average felt by consumers may differ from reported estimates. While the ACA does provide individual consumers the opportunity to re-enroll in less expensive plans, and more than half (54%) re-enrolling for 2015 switched plans, it is not known if the changes were to higher or lower cost plans [45]. Importantly, individuals will feel an increased cost of premiums due to age so that even in the absence of any increase in the cost of the policy held, the consumer will bear and perceive an increased cost to their health insurance. In the end, affordability is an issue that is personalized to the individual or family. Importantly, preparedness for making decisions related to participation in QHPs does require commitments to self-education and knowledge [46].

What is the greatest complication facing Americans that receive health insurance on ACA exchanges?

Tax implications for the consumer have been enumerated in the case of unanticipated increases in income that will result in a give-back at tax time either through a reduced refund or additional tax due [47,48]. Individuals that qualify for an exemption must use Form 8965 to calculate the Shared Responsibility Payment (SRP) and report any potential exemptions from the SRP. The IRS takes great care to avoid calling the SRP a tax penalty, although it serves the same purpose. In the event that the consumer has an unanticipated decrease in income, the taxpayer receives a reduction in their tax due or an increase of their tax refund through the Premium Tax Credit which essentially compensates for what their healthcare subsidy should have been using their 2014 income information. For taxpayers receiving the healthcare subsidy or claiming the Premium Tax Credit, form 8962 must be used to calculate any additional credit or credit repayment. When filing a tax return for the first year covered by the ACA, Form 8962 [49] must be submitted, which requires information that verifies participation in a QHP in order to avoid non-participation penalties. Verifying information for Form 8962 is provided on forms sent to participating individuals:

Form 1095-A [50] is required to be sent to individuals who have enrolled in a QHP through an exchange and for tax year 2014 must be prepared by 31 January 2015. Only those who go through an exchange qualify for the premium tax credit on QHP premiums.

Form 1095-B [51] is to be completed by a small employer insurance provider. It is for individuals who obtain their insurance through a small group employer (<50 employees), as well as individuals that seek insurance on their own but do not get it through an exchange. The preparation of this form is optional for 2014 and is to be phased in for future years.

Form 1095-C [52] – is to be completed by large employers, is also optional for 2014 and is to be phased in for future years.

As these forms are optional for 2014, individuals who are challenged by the IRS to verify participation may not be able to rely on forms 1095-B or C, and may have to resort to more rudimentary methods (receipts, pay stubs, employer statements) until these forms are phased in.

What can be said about the enrollment numbers for participation in insurance plans on ACA exchanges?

Updates in enrollment have been made monthly by state and government reports and consequently would be subject to ebb and flow of accruals governed by approved applications, payment and point of time in the enrollment cycle. Summaries presented here cover participation for the first year of ACA health insurance availability and include new and re-enrollments for 2015. Estimates of eligibility used in the figures reported here were from the original 2014 estimates prior to the start of 2014 and are in line with various agency, government and media reports of successful participation in the ACA healthcare insurance plans. 2015 projections for enrollment of 11.4 million uninsured individuals may have been too optimistic. Nevertheless, a robust number (4.67 million) of previously uninsured individuals enrolled for 2015 on exchanges [43,53].

What is the impact of health insurance coverage made available through the ACA?

It is likely that it is too early to assess the impact of the ACA on healthcare services. However, it has been reported that expansion of Medicaid coverage through the ACA did not result in long waiting times for provider appointments while appointment availability increased 7.7% [54]. Importantly, many states were estimated to have significant shortages of healthcare providers (45,000 primary care physicians and 46,000 specialists by 2020) for expanded healthcare [55]. Kentucky had a shortage assessment of 13,076 healthcare providers of which 3709 (36%) were physicians and 30% were physician assistants [56]. Considering the expansion of near-universal insurance coverage to 94% of the residents in Massachusetts (2002–2010), breast and cervical cancer screening increased 4–5% for mammograms and 6–7% for Pap tests [57]. While these early signs of expanded healthcare are encouraging, it is inevitable that as expansion continues more healthcare providers will be needed to deliver services.

It is impossible to ignore the unpopularity of the ACA [58]. Approval was highest at the time of the 2012 elections and has steadily fallen to an all-time low of 37% approval and 56% disapproval [59]. However, new enrollees and re-enrollees have not abandoned the marketplace exchanges and as already discussed represent successes in reducing the ranks of uninsured Americans. Some explanation for falling popularity could come from those that were forced to buy a more expensive product with coverage that they did not need, especially maternity benefits for individuals beyond reproductive age or of male gender. The perception of a broken promise that those who want to keep their insurance or doctor will be able to do so also may be contributory. To many the ACA is synonymous with ‘Obamacare’ so that the President's plummeting approval ratings [60] can carry over to feelings about the ACA. This is supported by ideology and politic since only 8% of Republicans indicate approval of the ACA, while 74% of Democrats indicate approval. With only 33% of independent voters indicating approval of the ACA, the connection to low Presidential approval is apparent [57] With these factors in mind, it is clear that only efforts to take the ACA away will make it more popular.

Conclusion

Enrollments in the ACA offerings have exceeded projections; however, the greatest enrollments have been in expanded Medicaid, which is premium-free. The concept of affordable premiums is less real to older Americans with low incomes. In addition, information on how Americans who are enrolled in ACA QHPs view their deductible and out-of-pocket expenses when using health insurance has not yet been comprehensively compiled. However, in summary, there can be little doubt that the ACA has brought considerable reform to American healthcare insurance.

Future perspective

A new President, a new legislative majority and a Supreme Court decision all could bring change altering the ACA. Political decisions are hard to predict at the individual level, but the reality of the large numbers of Americans now enrolled in an ACA plan make moves of repeal very questionable from the stand point of electability. Candidates in states that have refused Medicaid expansion may realize that they have a substantial constituency that wants participation through expansion. The Supreme Court has agreed to hear King versus Burwell on the question of the IRS ruling that the ACA subsidies could be granted to individuals purchasing health insurance in federally operated exchanges [61]. Provisions that are unpopular with the public may be the most vulnerable targets in the courts, such as the mandate for individuals to obtain health insurance or pay a penalty, the mandate that larger employers offer health insurance coverage to workers or pay a penalty and the tax on medical devices [30]. The Supreme Court has rendered a ruling in mid–2014 that was unfavorable to the ACA, holding that the federal government cannot lawfully mandate that closely held for-profit corporations provide contraception coverage if the exercise of religion is a compelling factor for the business [62].

Fiscal sustainability of the ACA by the government will likely carry through 2020, but may impact affordability by restricting subsidies if the government budget is stressed. In the face of an improving economic recovery where many more employers offer health insurance coverage to their employees, the role of individual participation in purchasing their own coverage could recede, but this would only be of neutral effect on the ACA. Lastly and of great significance will be the voice of Americans, who having taken advantage of the ACA's opportunity for healthcare access, will want this access to remain or widen.

Acknowledgements

The authors appreciate the time and information provided by C Banahan (Executive Director of the Office of the Kentucky Health Benefit Exchange), SK Mayfield (Kentucky Commissioner of Public Health in the Cabinet for Health and Family Services), J Midkiff (Executive Director Communication and Administrative Review in the Office of the Secretary of the Cabinet for Health and Family Services), B Hurley (Staff Assistant to the Kentucky Commissioner of Public Health) and K Cantrell (Cabinet for Health and Family Services Office of Health Policy).

Executive summary

Buying health insurance differs on various state-run exchanges and on the federal exchange.

Obtaining cost estimates is facile from state-run IT platforms or the federal IT platform.

Subsidies that are applied to monthly premiums on a means tested scale are administered as a tax credit.

Penalties for not participating or for increases in income that disqualify some or all subsidization are collected on the annual income tax.

Premiums vary from state to state and from city to city within states, changing with income, age and family size.

Premiums were highest at age 64 years and could vary by more than three-fold between the least expensive bronze plan and the most expensive platinum plan.

Information on network providers was difficult to obtain without going to the provider's website. State-by-state summaries of participation

Organizational differences could be explained by 29 states in the federal exchange, 14 states on exchanges that were state-operated, five states operating as State-Partnership Marketplaces and three states operating as federally-supported state-based market places.

Medicaid enrollment nationally was approximately six-times higher than in qualifying health plans (QHPs), but varied from state to state and was higher in states that expanded Medicaid (10.6x) than in those that did not (4.9x).

Unknowns in affordability are due to cost of premiums, deductibles, out-of-pocket expenses, penalties for incomplete participation and increased premiums over time.

Changes in premiums ranged from a 22% decrease to a 35% increase for year 2.

Age-adjusted premiums cause an annually increased cost even when plans do not increase in cost.

Investors in the healthcare industry indicate confidence due to annual growth appreciation >35%. Questions worthy of discussion

What are the innovations that the Affordable Care Act (ACA) brings?

– There are five innovations: 1 removal of access barriers; 2 implementation of choice of price and plan benefits through online comparisons; 3 universal coverage of essential health services; 4 affordability through financial assistance subsidies and Medicaid expansion; 5 mitigation of financial ruin by removing caps on annual benefits and lifetime benefits and by placing maximums on out-of-pocket expenses for covered services.

Is health insurance coverage affordable for Americans?

– Since premiums are very low for young Americans aged 20–25 years, affordability is achieved; however older Americans in the years just prior to eligibility for Medicare have high premiums and may not feel that health insurance is affordable.

What is the greatest complexity facing users of ACA exchanges?

– Obtaining and providing accurate and precise documentation in order to enroll with subsidies in ways that avoid penalties is daunting.

Has enrollment been good?

– Enrollment for year one was on target, while 4.7 million previously uninsured Americans enrolled for 2015.

What is the impact and future of ACA?

– Political contentiousness is likely to focus on unpopular provisions, but rather than being election issues are likely to be pursued in courts.

Footnotes

The authors have no relevant affiliations or financial involvement with any organization or entity with a financial interest in or financial conflict with the subject matter or materials discussed in the manuscript. This includes employment, consultancies, honoraria, stock ownership or options, expert testimony, grants or patents received or pending, or royalties.

No writing assistance was utilized in the production of this manuscript.