Abstract

Recent efforts by the Federal Government of Canada have devoted resources to mitigating disaster risk and identifying sustainable solutions for post-disaster housing reconstruction financing. In 2023, Canada committed funding to set up its National Flood Insurance Program. In parallel, the Department of Finance and Public Safety Canada plans industry engagement on solutions to earthquake insurance. In anticipation of the need to rethink post-earthquake housing reconstruction financing for single-family homes, the present study evaluates the feasibility of implementing three novel financing mechanisms in Canada, drawing inspiration from existing US and New Zealand programs. The proposed mechanisms include a grants program targeting low-to-moderate-income households, a low-interest loan program, and an affordable insurance program. Simulations of the impacts of M7 earthquake in the Strait of Georgia, British Columbia, are used to compare the post-earthquake uninsured losses in the status quo and if each new mechanism was in place before the event. Benefits are assessed through the reduction in uninsured losses, while opportunity losses measure the costs of each program. Results indicate that a loan program with an interest rate above 3.5% could offer benefits surpassing its opportunity cost, albeit with substantial initial expenses. In addition, introducing an affordable insurance program and a disaster fund shows promise but requires robust capitalization in its initial years. A combination of affordable insurance and low-interest loans could alleviate long-term debt for homeowners, particularly for earthquakes causing moderate losses.

Introduction

Insufficient financing strongly predicts deficient recovery processes (Comerio, 2023; Greer and Trainor, 2021; Smith, 2011). However, due to the scale of the losses, financing post-earthquake recovery is challenging, especially for uninsured or underinsured households (Alisjahbana et al., 2022). The interplay between inadequate insurance coverage, limited access to credit, governmental budget constraints, and price increases due to demand surges further complicates recovery efforts and can exacerbate long-term disparities in recovery outcomes (Peacock et al., 2018). Addressing these challenges requires innovative financing mechanisms and enhanced risk-reduction strategies. Aligned with this idea, the Federal Government of Canada is rethinking its disaster recovery financing mechanisms. In March 2022, Public Safety Canada assembled an Expert Advisory Panel to redesign the main programs used by the Federal Government to assist Provinces and Territories (Denlinger, 2022). In 2023, Finance Canada committed seed funding to set up Canada’s first National Flood Insurance Program (Public Safety Canada (PSC), 2022, 2023). The next stage of this initiative will evaluate the implementation of an affordable national earthquake insurance program in Canada (Department of Finance Canada, 2023; DiSabatino, 2024). This study contributes to identifying economically viable post-earthquake recovery financing mechanisms for Canada by evaluating the benefits and costs of adapting programs from other countries to the Canadian context.

Despite the potential, Canada has not experienced an earthquake causing significant loss recently. However, experiences from other developed economies shed light on potential issues Canada may face after such an event. For example, on January 17, 1994, the Northridge earthquake struck the San Fernando Valley region of Los Angeles, damaging about 12,500 homes and resulting in an estimated US$20 billion in losses at the time (Kamel and Loukaitou-Sideris, 2004). The insurance industry faced an unprecedented challenge due to the magnitude of claims because, at the time, insurance providers were required to offer earthquake coverage with homeowners insurance. Fearing bankruptcy in the event of another earthquake, insurance providers chose not to write any new homeowners’ policies in California. To stabilize the market, in 1996, the California Earthquake Authority (CEA) (2023) was created as a privately funded, publicly managed nonprofit organization to standardize earthquake insurance coverage and assume most of the financial risk. Still, earthquake insurance takeup rates dropped by more than 50% in comparison to before the 1994 Northridge earthquake (Pothon et al., 2019; Worldwide, 2014).

A similar stress to the insurance market was observed in the aftermath of the 2010–2011 Canterbury earthquake sequence in New Zealand. The earthquake sequence damaged around 167,000 houses (Greater Christchurch Group, 2016). The extent of loss failed an insurance company responsible for about 30% of the local market (King et al., 2014). New Zealand’s long-term commitment to disaster risk management mitigated the consequences of these losses. Since 1946, the Toka Tū Ake Earthquake Commission (EQC) has built the Natural Disaster Fund using levies collected from home insurance policies and investment returns. In 2010, before the Canterbury earthquakes, the Fund had over NZ$6.1 billion in accumulated funds, allowing the Fund to absorb a significant portion of the housing recovery costs. However, in 2016, another earthquake struck New Zealand. Although less damaging, the 2016 Kaikoura Earthquake compounded the Canterbury earthquake sequence impacts. It led to the depletion of the Natural Disaster Fund and the dual call on their NZ$2.5 billion reinsurance coverage. The EQC was forced to call on the Government guarantee of the Fund (King et al., 2014).

The Northridge and Canterbury earthquakes caused financing challenges despite the robustness of the financing mechanisms in each country at the time. Comparatively, Canada could face a direr scenario after a similarly large earthquake. In Canada, disaster financing mechanisms are primarily structured around a combination of optional, private insurance coverage and Federal, Provincial, and Territorial assistance programs. The penetration rate for earthquake home insurance in Canada varies from more than 65% near Vancouver to less than 5% in other regions, especially outside British Columbia (Goda et al., 2020). Despite British Columbia’s high takeup rate, an investigation of the impacts of a large earthquake in the province highlighted that if insured losses were CA$ 30 billion, 26 (out of 30) insurance companies would be distressed, and up to 11 could fail (Kelly et al., 2020b). A recent study by the Geological Survey of Canada indicates that a magnitude 7.0 earthquake in the Strait of Georgia in British Columbia could lead to losses exceeding CA$30 billion (Hobbs et al., 2021). Beyond insurance, the Disaster Financial Assistance Arrangements (DFAA) are the main way for the Federal government to assist Provinces and Territories after disasters. In turn, Provinces and Territories can assist households. However, DFAA only compensates for losses due to uninsurable perils. Hence, it does not apply to earthquake-induced losses.

Aligned with current efforts to identify sustainable disaster recovery financing alternatives for Canada, this study investigates if housing reconstruction financing mechanisms that exist in other countries would be viable in Canada. Three mechanisms for financing post-earthquake single-family housing reconstruction are investigated: (i) a government-managed insurance program and its use to build a disaster fund, (ii) a low-interest loan program, and (iii) a grants program for low-income homeowners. A scenario-based analysis is employed that focuses on the impacts of an M7.0 earthquake on the Strait of Georgia in British Columbia. Data representing the probability of damage to residential buildings due to this earthquake are collected from the Canadian National Earthquake Scenario Catalog (Hobbs et al., 2021). These probabilities are transformed into 1000 probabilistic damage maps using Monte Carlo sampling to estimate the distribution of uninsured losses if the earthquake happened in 2024 with no changes to the financing system. Then, probabilistic models are developed and used to simulate the implementation of the financing mechanisms (i), (ii), and (iii). Each financing alternative is evaluated regarding its potential capacity to reduce uninsured losses and costs. Finally, a brief assessment of homeowner indebtedness under each scenario is presented to understand the financial impact on homeowners.

Housing reconstruction financing in Canada

Before discussing alternatives, understanding the status quo for post-disaster housing reconstruction financing in Canada is important. Home insurance is the primary form of ex-ante risk transfer in Canada. Homeowners pay an annual premium to insure (partially or completely) their buildings in case of a catastrophic event (e.g. earthquake). Insurance payments are only disbursed if damages incur losses above a threshold (i.e. the deductible). The premium is a function of the hazards at the location of the building, the coverage percentage, and the deductible. Higher risk areas, higher coverage, and lower deductibles incur higher premiums. In Canada, residential earthquake insurance takeup rates vary significantly by province, from more than 65% near Vancouver to less than 5% in most other regions (Goda et al., 2020). Thus, high levels of uninsured losses are expected after an earthquake. Another factor contributing to uninsured losses is the deductible, which is often between 5% and 20% of the building replacement costs. Single-family home deductibles are around 12.5% in British Columbia (Kelly et al., 2020a). In this case, a CA$500,000 replacement cost single-family home would not trigger insurance if losses are below CA$62,500. For larger events where insurance is triggered, the deductible must be paid out-of-pocket and will compound other emergency expenses.

Disaster-struck households with uninsured losses may receive financial assistance from Provinces and Territories to restore, replace, or repair their principal residences. Provinces and Territories can partially transfer these costs to the Federal government through the DFAA program. DFAAs are provided to Provinces and Territories when response and recovery costs from an uninsurable peril exceed what they can reasonably bear on their own. However, earthquake is not an uninsurable peril. Consequently, in the aftermath of a major earthquake, Provinces and Territories cannot count on DFAA. They will have limited capacity to assist disaster-struck households in financing home repairs and reconstruction. These households would have to rely on private loans or savings. Households of lower socioeconomic demographic status may not have savings or face difficulties in having a large loan approved, creating a further disparity in disaster outcomes.

The following section presents a brief overview of post-disaster housing reconstruction financing in other countries to identify alternative disaster financing mechanisms to support disaster-struck Canadians.

Alternative housing reconstruction mechanisms

This section discusses selected post-disaster housing reconstruction financing mechanisms that could benefit Canadians. A comprehensive summary of disaster reconstruction financing mechanisms and approaches is presented in Organisation for Economic Co-Operation and Development (OECD) (2020). Here, the focus is on three well-documented programs with diverse goals which can be translated into a computational model. One example of a federally backed insurance program, a low-interest loan program, and a federal grants program are described. The methodology discussed in the next section can be expanded to evaluate the suitability of other programs described in OECD (2020) in the Canadian context, as long as these can be translated into a computational model.

Federally backed insurance programs

Federally backed, affordable insurance programs have been used as a risk-transfer mechanism (see OECD, 2020). New Zealand’s EQC insurance program is one example that applies to earthquakes. It was created in 1945 to provide affordable insurance and help communities recover from earthquakes. The program evolved over the decades, and it is currently called EQCover. In the current iteration, homeowners are automatically enrolled in EQCover if they have a valid private insurance policy for their residential building, including fire insurance (and most do). The EQCover premium is 16 cents per NZ$100 of the EQCover amount, up to a maximum of $480 plus taxes. The deductible is at least NZ$200 and at most 1% of the insured amount. The maximum coverage is NZ$300,000. Homeowners are incentivized to seek private insurance if their home replacement costs exceed this value. In years without disasters, the collected EQCover premiums are paid into New Zealand’s Natural Disaster Fund and re-invested. The Fund allowed the EQC to play a substantial role in cost-sharing the repairs from the Canterbury earthquake sequence. EQCover is Government guaranteed. If EQC has many claims and cannot cover its obligations from the Natural Disaster Fund and its reinsurance, then the Government will pay the shortfall.

Low-interest loan programs

Federally managed, low-interest loan programs present an attractive alternative to assist disaster-struck households sustainably. That is, because loans must be paid back, the costs of such a program are partially recovered over time. One example of a low-interest loan program is the United States Small Business Administration (SBA) Household and Personal Property Loans (HPPL) Program. Successful HPPL applicants may receive up to

Federal grants programs

Grant programs are a common tool for Federal governments to assist the housing reconstruction of socioeconomically disadvantaged households (Australian Department of Home Affairs, 2018; HUD, 2022; Mahul and White, 2012). One example of such a grant program is the Community Development Block Grant for Disaster Recovery (CDBG-DR) administered by the US Department of Housing and Urban Development (HUD, 2022). HUD provides funds to state housing authorities that, in turn, decide how to allocate the funding to aid low-to-moderate-income households. HUD and state housing authorities use the US Census criterion in which a household that earns less than 120% of the regional median income is considered to have low-to-moderate income. State housing authorities define each household’s maximum assistance,

Case study

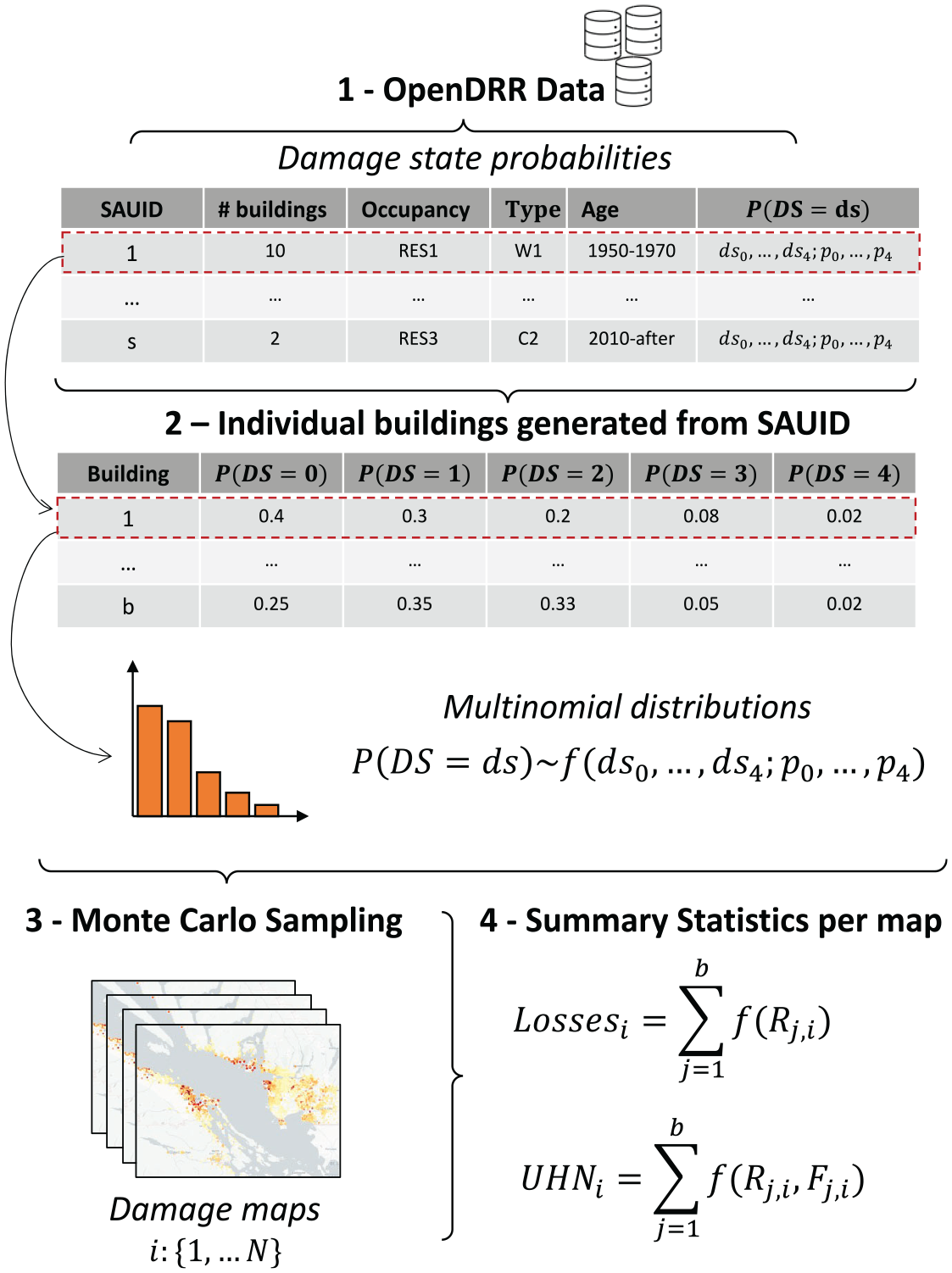

The Geological Survey of Canada recently developed a National Earthquake Scenario Catalog and conducted detailed assessments of potential post-earthquake losses in Canada. These scenarios represent possible earthquakes near main urban centers in Canada, covering a range of magnitudes and epicenter locations to inform regional risk management. The M7.0 Strait of Georgia Earthquake Scenario is selected from this catalog for the subsequent analysis because it is the most similar to the earthquake scenario used by emergency management agencies in Lower Mainland British Columbia for planning activities—that is a M7.3 in the same location (City of Vancouver, 2024). In 1997, a magnitude 4.6 earthquake occurred 3 to 4 km beneath the Strait of Georgia. This scenario, called GSF7 Scenario for short, visualizes the effects of that event if it had a magnitude of 7.0. The data representing this scenario are publicly available via the Open Disaster Risk Reduction Platform (OpenDRR; Hobbs et al., 2021). In the following, these data are referred to as the OpenDRR data. The OpenDRR results indicate that this earthquake could cause CA$30.3 billion in total losses, heavy damage to 10,626 buildings, and displace 345,774 persons. Damage to linear infrastructure and subsequent disruption costs are not accounted for in the loss figures. Moreover, damages from secondary hazards such as aftershocks, liquefaction, tsunami, landslides, and fire following are not included. Hence, loss figures are likely underestimated. Details of this scenario are available at Geological Survey of Canada (2023).

Single-family homes are the focus of the analyses in this study because they represent 77% of residential units and 90% of the exposed value in terms of structural replacement costs in the OpenDRR GSF7 Scenario. In the OpenDRR data, 6.7% of these buildings are unreinforced masonry buildings, and the remainder are wood structures. The OpenDRR data for the GSF7 are provided as tables where each row represents a group of assets with similar properties (e.g. single-family homes built before 1990) in a Settled Area. Each Settled Area has a unique ID (i.e. SAUID). Settled Areas are roughly analogous to the census Dissemination Areas. For example, in these tables, ten similar buildings in the same Settled Area would be listed as a single asset (i.e. one row) comprised of ten buildings (Hobbs et al., 2021). The tables also provide the probability that a building in this collection is in a damaged state

The procedure described in Figure 1 is used to reintroduce variability in the earthquake impacts. The original tables are expanded so that a row representing ten buildings becomes ten identical rows. Then, the damage state probabilities for each building

Overview of analysis.

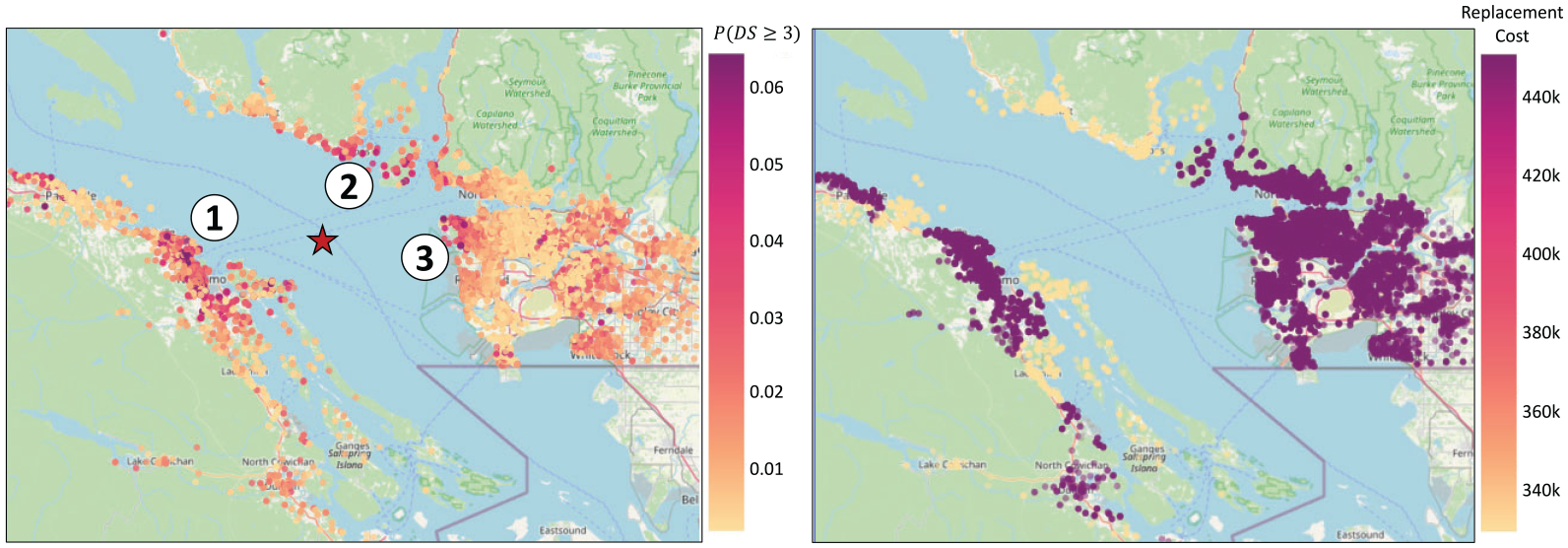

The left-hand side panel in Figure 2 shows the mean probability of severe (i.e. 3) or complete (i.e. 4) damage for each building obtained from 1000 damage maps created using the procedure in Figure 1. The star symbol indicates the epicenter location. Region 1 is the Nanaimo region on the Vancouver Island. Regions 2 and 3 on the Mainland are the Sunshine Coast and Metro Vancouver regions. All else equal, earthquake intensity is a function of distance to the epicenter, which is observed in the probability of damage in the figure. Areas further from the epicenter can experience more damage when soil conditions worsen or buildings age. This study assumes that these factors were properly accounted for in OpenDRR results. The right-hand side panel presents the OpenDRR-estimated replacement cost for a building in each area. Buildings outside the Vancouver and Nanaimo regions are estimated to be nearly CA$100,000 less expensive to replace by the OpenDRR developers. This combination of hazard and exposure indicates that the Nanaimo and Vancouver regions are prone to higher losses.

Hazard and exposure in the Strait of Georgia.

The losses experienced by building

where

where

where

Baseline earthquake-induced unmet needs

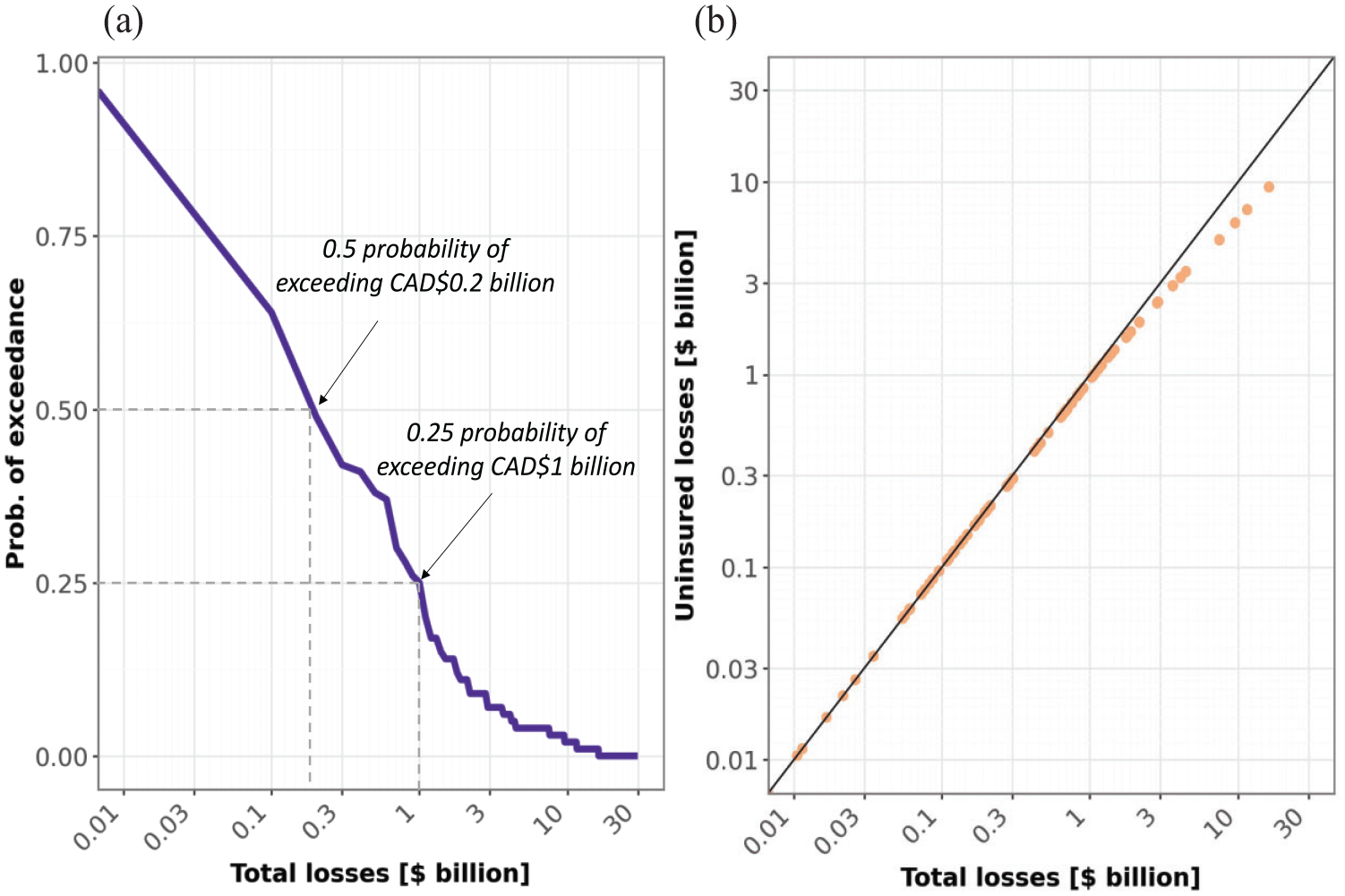

This section evaluates the impacts of the GSF7 if it happens in 2024, with no changes to disaster recovery financing mechanisms available to Canadians. Figure 3 shows the losses estimated from 1000 damage maps. Panel (a) shows that single-family housing-related losses are expected to be below CA$ 0.2 billion (i.e. 0.5 probability of not exceeding) but may be close to CA$15 billion in low-probability cases. The maps with high losses reflect realizations where most buildings are assigned a higher level of damage. Panel (b) shows that in maps where total losses are below CA$ 1 billion, most losses will not be covered by insurance. Losses stem primarily from many buildings experiencing lower levels of damage. The median loss per building for the GSF7 is CA$ 1367, which would not exceed the insurance deductible (i.e. between CA$ 40,000 and CA$ 55,000). These results highlight some limitations of insurance being homeowners’ sole source of post-disaster housing reconstruction financing.

Estimate losses due to the M7 Strait of Georgia earthquake. (a) Probability of excedeence of loss thresholds. (b) Comparison of insured and uninsured losses. Results represent 1000 damage maps. Losses account only for damages to single-family housing. Insurance coverage is estimated based on Equation 3.

In the baseline scenario, the unmet housing needs equal the uninsured losses and must be covered out-of-pocket (e.g. savings or private loans). Four mechanisms for reducing unmet needs after the GSF7 are explored in the following. The subsequent analyses do not evaluate if one mechanism would be generally beneficial to Canada. Rather, “what-if” scenarios are simulated where a certain financing mechanism was implemented before the earthquake, and their benefits and costs are compared. The analysis results must be interpreted in this context. Moreover, the following assumptions underlie the results: (i) The GSF7 earthquake happened. That is, only uncertainties regarding the extent of the losses are evaluated, not uncertainties regarding the event occurrence. (ii) Reductions in unmet housing needs for British Columbians are perceived as a benefit to Canada. The GSF7 earthquake could displace as many as 345,774 British Columbians, severely impacting the province’s economy and causing ripples across the Canadian economy. Yet, the assumption that assisting disaster-struck homeowners in British Columbia benefits Canada is a limitation of the subsequent analysis.

Implementing a federal grants program

This section investigates implementing a federal grants program to assist low-to-moderate-income homeowners (i.e. those who earn less than 120% of the regional median income). This program would be similar to the CBDG-DR program in the United States. To evaluate the efficacy of the grants program, the number of homeowners with unmet needs exceeding a threshold T in each damage map is calculated. If most homeowners have unmet needs below T, a grants program capped at T would be efficient. In Figure 4, the abscissa axis shows the total losses from each damage map, and the ordinate axis shows the percentage of low-to-moderate-income homeowners with unmet needs below

Expected uninsured losses per low-to-moderate-income homeowner.

Introducing a low-interest loan program

This section evaluates the benefits and costs of implementing a low-interest loan program in Canada similar to the Homeowners and Personal Property Loans offered by the SBA HPPL to disaster-struck homeowners. The HPPL loans are limited to a cap of US$500,000. However, the effective loan amount may be lower based on the SBA’s evaluation of the financial status of the applicant (e.g. based on credit score or other debt). In previous work (Costa and Baker, 2024), the author developed a linear relationship between loss and the approved loan based on data from 285,260 SBA-approved HPPL loans provided by Collier and Ellis (2022). Assuming the loan program would follow the same relationship, the maximum loan is:

For a building j in damage map i, the benefits of the low-interest program are estimated as the difference between unmet housing needs with and without the loan program, that is

where the amount to be paid back to a lender on a loan with principal

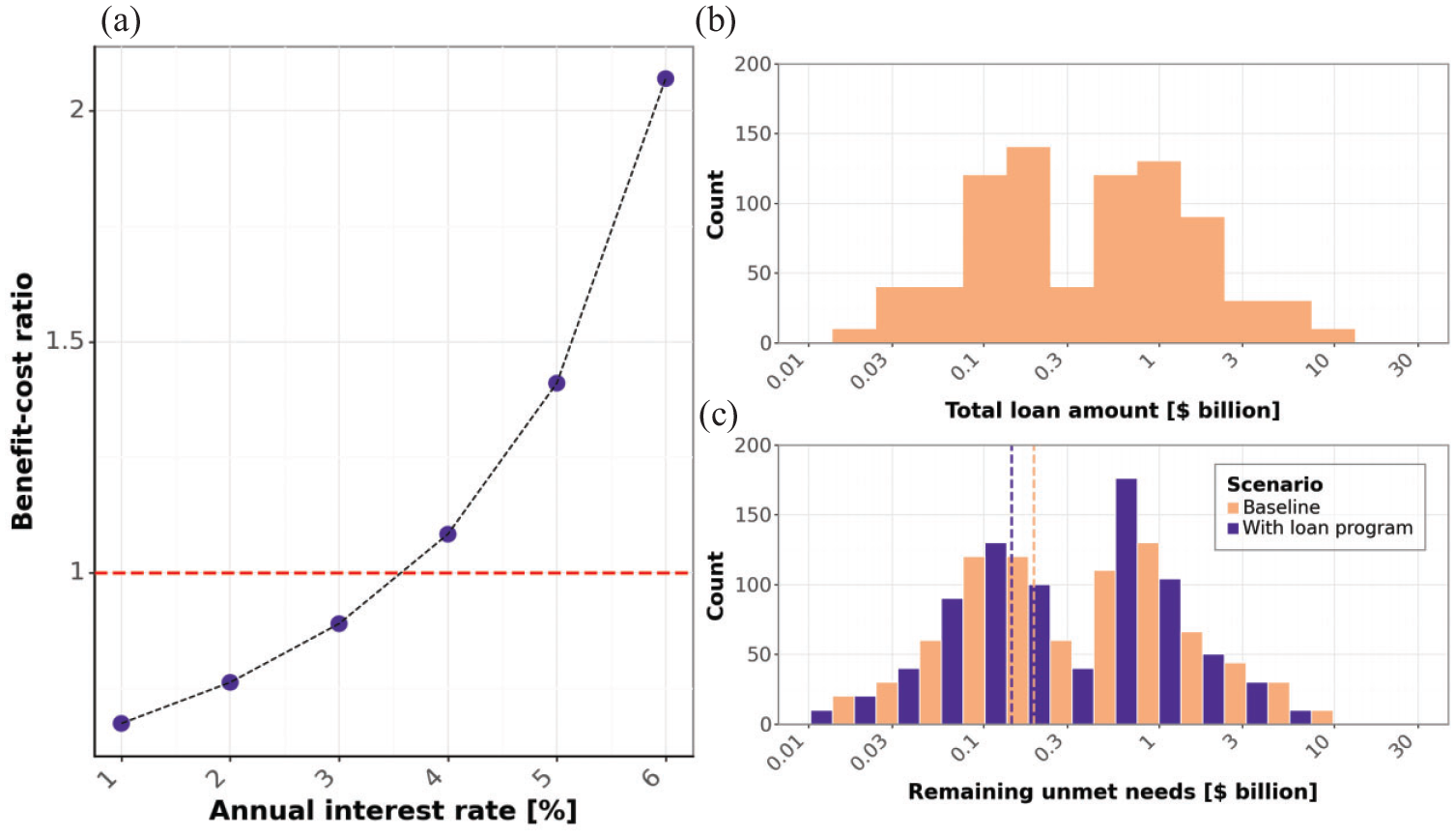

It is assumed that the loan program would employ the same maturity of SBA HPPL loans, that is 30 years (or 360 months). The SBA HPPL offers an annual interest rate of 8% for homeowners they judge would qualify for a private loan. Otherwise, SBA HPPL interest rate does not exceed 4%. To evaluate the benefit–cost ratio of a similar program in Canada, we assume that 8% is the market rate for loans at which the lender would have no opportunity cost loss. We estimate the cost associated with loaning money at an interest rate lower than 8% annually as:

where

Benefitcost analysis for a low-interest housing reconstruction loan program. (a) Benefit-cost ratio as a function of the loan program interest rate. (b) Expected upfront cost of the loan program. (c) Expected reduction in unmet needs from the loan program. The benefit is the reduction in unmet housing needs, and the cost is the difference between loaning funds using market rates and the interest rates on the abscissa axis. The horizontal red dashed line in panel (a) shows the interest rate at which the benefits and costs are equal.

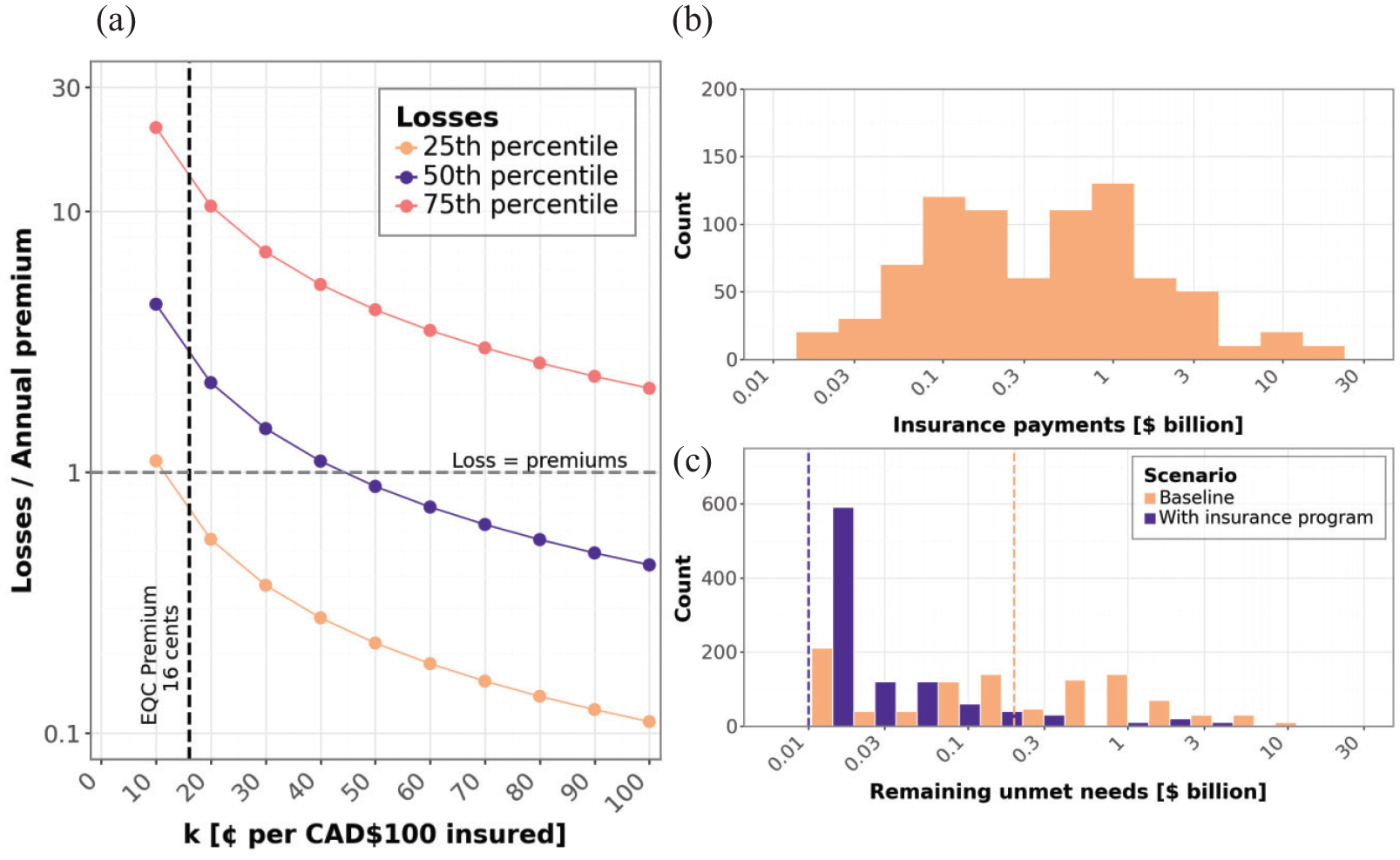

Creating a low-cost insurance program

The last strategy evaluated is implementing a mandatory insurance program inspired by the New Zealand Earthquake EQCover, which insures up to NZ$300,000 in property losses with a minimum deductible of NZ$200 and a maximum of up to 1% of the amount insured. To isolate the effects of this insurance program, it is considered that homeowners would opt out of private insurance. Thus, the unmet needs in the analyses in this section are calculated from Equation 2 setting

where

where

Benefit–cost analysis for a low-cost insurance program in Canada. Panel (a) compares expected losses to anticipated annual premiums. Panels (b) and (c) show the initial costs and remaining unmet needs if the program is in place.

As expected, the loss-to-premium rate is above 1 for all

Impacts to homeowner indebtedness

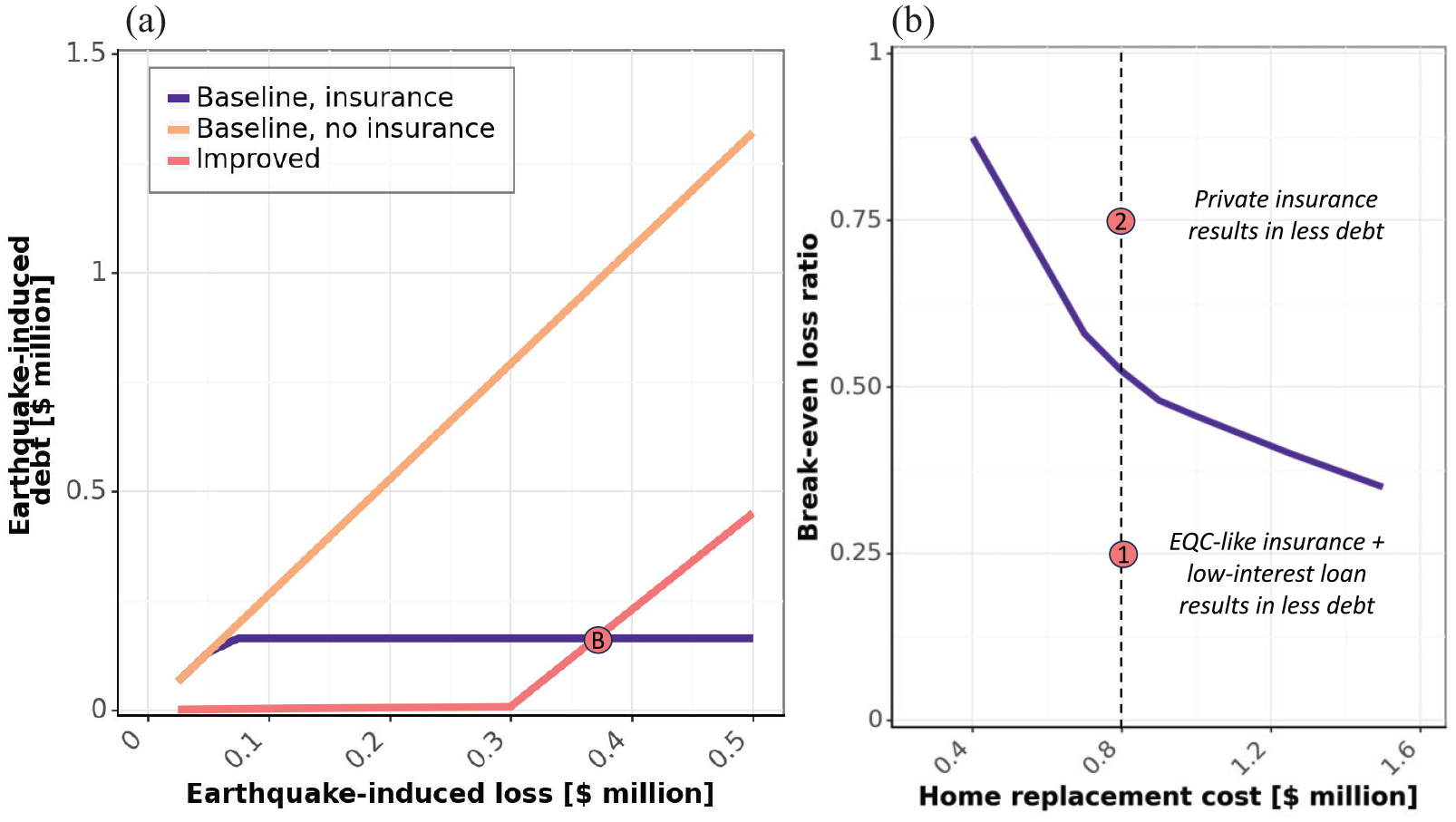

The analyses above consider costs and benefits from the Federal Government’s perspective. Here, the impacts on homeowners in British Columbia are evaluated. To simplify the comparisons, a building with CA$500,000 replacement cost is considered. In the baseline scenario (i.e. no changes from status-quo), it is assumed that unmet housing needs are covered by a market-rate (i.e.

The debt estimated in Equation 10 is compared with the debts incurred in an improved scenario where the same homeowner has coverage from an EQC-like insurance program and has access to a low-interest (i.e.

where

Benefits to homeowners from different housing reconstruction financing mechanisms. (a) Expected homeowner debt under different financing scenarios. (b) Break-even loss ratios for different home replacement costs. If the loss ratio is below the line (e.g. Point 1), the improved scenario would result in less debt. Conversely, if the loss ratio is above the curve (e.g. Point 2), private insurance would lead to less debt.

Discussions and limitations

Post-disaster financing is a broad subject that goes beyond the scope of this study. This section discusses some of these limitations and provides discussions to inspire future work to expand the scope. First, the National Earthquake Scenario Catalog only provides average replacement costs for buildings (rather than a distribution) leading to a reduction in the variability in the estimated losses. A more detailed model for the replacement costs would be ideal to represent the tails of the loss distribution better. However, this would also add uncertainty to the model and require more damage maps.

Benefits and costs observed for the GSF7 earthquake scenario may not be observed in other events. Insurance takeup rates in British Columbia are more than ten times as high as in other regions despite similar earthquake risks (e.g. measured by 500-year expected earthquake losses; Hobbs et al., 2023). A similar magnitude event in the Ottawa-Montreal area is expected to lead to significantly higher initial costs for implementing alternative financing schemes. Future analyses focusing on the Ottawa-Montreal area are needed to determine if the benefits increase at the same rate.

Other programs may be better suited for Canada and British Columbia. The programs (i.e. low-interest loans, low-cost insurance, and grants) were selected due to the availability of information and the authors’ previous experience in modeling them. Rather than an extensive assessment to identify the best program for Canada, this study provides a framework that can be used to study the suitability of different funding arrangements. Moreover, combining all existing and new programs may yield better results but is outside this study’s scope.

Although Canada is exposed to significant seismic hazards, annual catastrophic losses are driven by water and fire hazards. Consequently, identifying the country’s best post-disaster housing reconstruction financing would require a comprehensive assessment of multiple hazards. Current efforts by Natural Hazards Canada and the Flood Hazard Identification and Mapping Program may provide the data needed to conduct a similar study evaluating the benefits and costs of housing reconstruction financing tools for flood disasters.

Limitations exist in the use of reduction in unmet housing needs as a metric of benefit. This study discusses using Federal funds to support housing reconstruction, and individuals not directly impacted may not perceive a reduction in unmet housing needs as a benefit. Conversely, fostering the successful recovery of an earthquake-struck community may provide an economic boost to the region, reducing the ripple effects of the disaster across the country. The socioeconomic and political implications of introducing the programs evaluated in this study must be considered to guarantee a fair use of public resources.

Conclusions

This study evaluates the viability of introducing three new post-earthquake financing mechanisms in Canada: (i) a grants program targeted at low-to-moderate-income households, (ii) a low-interest loan program, and (iii) an affordable insurance program. Existing programs in the United States and New Zealand inspire the proposed financing mechanisms. The reduction in unmet housing needs measures the benefits of introducing these programs. Opportunity losses measure the costs of each program. Benefits and costs are evaluated in the context of an M7 earthquake in the Strait of Georgia in southwest British Columbia.

Results indicate that a grants program capped at CA$50,000 would be sufficient to cover housing repair costs for low-to-moderate-income households. However, the benefits (as defined above) of such a program would be, at best, equal to its cost. Conversely, it is demonstrated that the benefits of a Federal loan program with an interest rate above 3.5% would exceed the opportunity cost of providing loans at below market rate (assumed 8% annually). However, the loan program would have a substantial upfront cost to the Federal government. Finally, introducing an affordable insurance program and using it to build a disaster fund are another promising alternative. This program would require a robust capitalization scheme in its first year. Still, assuming no earthquake occurs in this period, it could serve a pivotal role in a future earthquake similar to the New Zealand Disaster Fund after the Canterbury earthquake sequence. Although outside of the scope of this study, it is likely that a combination of existing and new financing mechanisms could yield optimal results in terms of the benefit–cost ratio.

Support for implementing these funding mechanisms is ultimately conditioned on how it benefits individuals and households. Results show that a combination of the affordable insurance program and low-interest loans can reduce the long-term debt experienced by homeowners compared to private insurance when damage is not heavy. For a CA$800,000 home, unless losses are more than CA$400,000, private insurance results in more long-term debt than a combination of the affordable insurance program and low-interest loans. This finding is primarily due to the initial cost of the deductible (assumed 12.5% in the case study). While private insurance remains the most competitive alternative for risk-averse homeowners who can afford it, a combination of the affordable insurance program and low-interest loans can be more appealing for the most likely earthquakes, which are expected to cause lesser losses.

This study’s contributions align with Federal-level initiatives to better support Canadian households struck by disasters (PSC, 2023; Denlinger, 2022). The 1994 Northridge and 2013 Christchurch earthquakes were near-misses regarding the collapse of the United States and New Zealand’s disaster recovery financing mechanisms. Canada is taking important steps to mitigate the risk of experiencing the same harsh lessons. This study provides methodological and quantitative contributions to foster the holistic design of post-disaster financing mechanisms for Canada that will minimize the long-term impacts of catastrophes. Future work will expand the scope to evaluate other earthquakes, particularly in the Ottawa-Montreal region, to unveil similar insights and identify programs that may be beneficial across Canada.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author received financial support from his Discovery Grant from the Natural Sciences and Engineering Research Council of Canada (RGPIN-2023-03537).