Abstract

Financial exploitation (FE) is a significant concern for older adults, with annual prevalence rates estimated between 5% and 17%. This study investigates how financial skills, specifically objective numeracy and financial knowledge, relate to scam susceptibility and FE in 672 adults aged 60 and older. Structural equation modeling revealed that higher financial knowledge and numeracy scores were significantly associated with reduced scam susceptibility, which, in turn, was linked to a lower likelihood of experiencing FE. Notably, gender, age, race, education, and income had differential impacts on financial skills and scam susceptibility. Males and minority groups, particularly African American and Hispanic participants, showed higher scam susceptibility, partially mediated by lower numeracy and financial knowledge. Education emerged as a critical protective factor, both directly and through its positive influence on financial skills. These findings underscore the importance of targeted interventions to bolster financial skills among older adults, especially vulnerable groups, to reduce FE risk. The study highlights the need for tailored educational resources and support programs to protect older adults, with particular attention to enhancing numeracy and financial knowledge across diverse demographic groups.

Introduction

Financial exploitation (FE) is a pervasive issue affecting older adults (60+) and costs billions of dollars each year (US Government Accountability Office, 2021). In the present article, we focus on financial exploitation by a stranger (FE), distinct from exploitation by a known and trusted other, which falls under the umbrella of elder mistreatment, comprising elder abuse and neglect (see Burnes et al., 2017 for more detail on this distinction). Financial exploitation by a stranger is referred to by various names in the literature, including consumer financial fraud (Deevy et al., 2012), financial fraud (Beals et al., 2015), consumer fraud (Federal Trade Commission & Anderson, 2013), or exploitation of older adults in a consumer context (Holtfreter et al., 2014). A recent definition of this type of exploitation states FE is “Intentionally and knowingly deceiving the victim by misrepresenting, concealing, or omitting facts about promised goods, services, or other benefits and consequences that are nonexistent, unnecessary, never intended to be provided, or deliberately distorted for monetary gain (Beals et al., 2015).” Prior research on FE among older adults has examined credit card fraud, price misrepresentation, investment scams, lottery scams, and identity theft, among others (see AARP et al., 2011; Deevy et al., 2012; FINRA Investor Education Foundation, 2013; Huff et al., 2010).

Prevalence of Financial Exploitation in Older Adults

Financial exploitation is a significant concern for older adults, with studies reporting varying prevalence rates. Estimates regarding the prevalence rate for FE range have demonstrated a 1-year prevalence between 4% and 17% in older adults, with most studies generally reporting between 10% and 15% (Deevy et al., 2012; Deevy & Beals, 2013; Shadel et al., 2021). A recent systematic review suggests a prevalence of 5.4% in the past year (Burnes et al., 2017). Given these estimates, millions of older adults are impacted by FE annually, underscoring the need for effective interventions. This is highly significant given the impact of FE on independent living, quality of life, and well-being.

Need for a Comprehensive Model

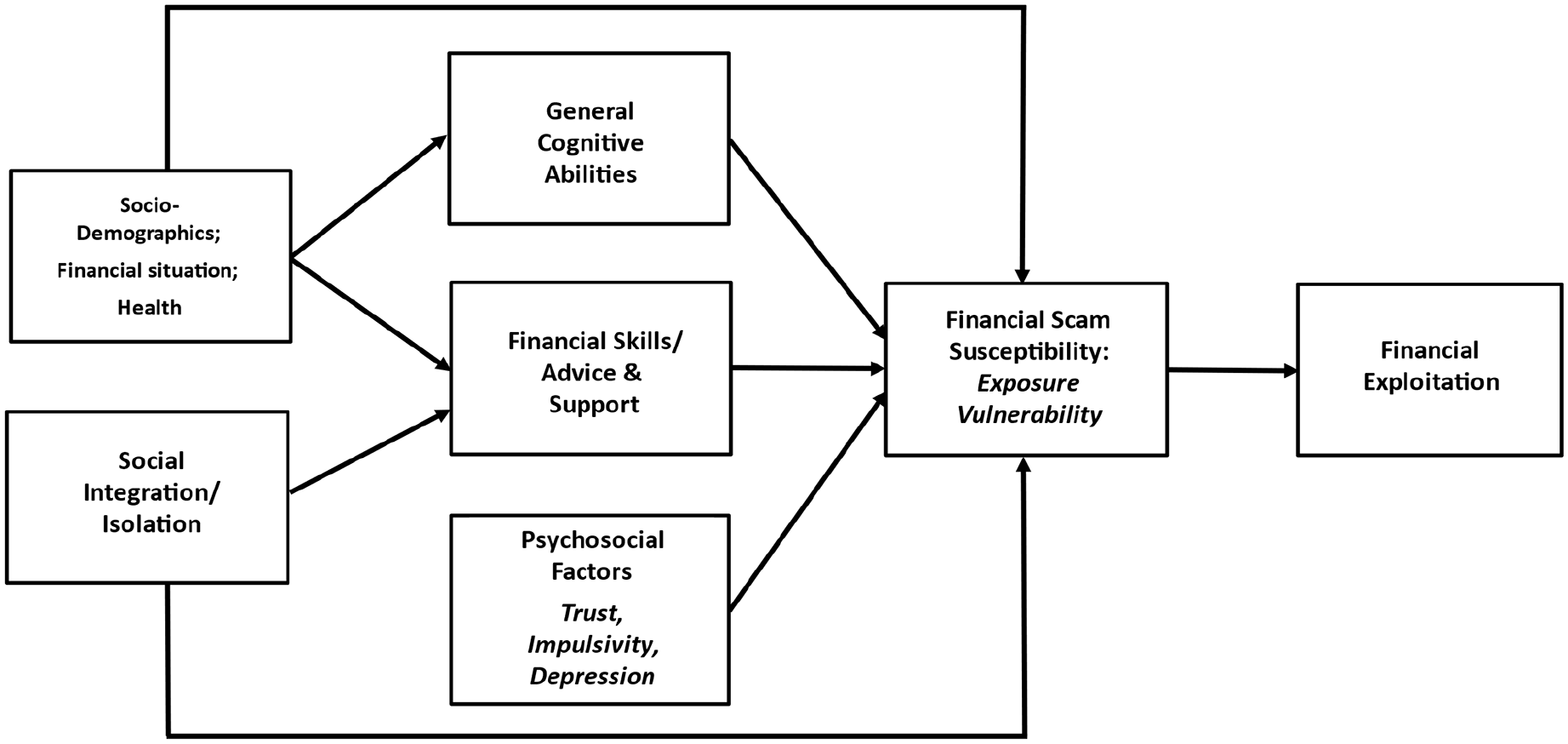

Understanding the risk factors contributing to FE is crucial for developing effective interventions. While research studies, many of which are discussed below, have examined risk factors of FE, they are often in isolation and lack a comprehensive model or theory. A comprehensive model is needed to explore the complex interaction of demographic, cognitive, financial, and psychosocial factors related to FE. Therefore, this study aims to provide a more holistic examination of FE risk factors guided by a comprehensive theoretical model (see Figure 1).

Theoretical Model of Financial Exploitation.

Risk Factors Influencing Financial Exploitation

Various situational, psychological, and behavioral factors influence financial exploitation (Shao et al., 2019). For example, older adult victims of fraud report an element of trust and a promise of financial security as causes of FE (Nguyen et al., 2021). Other research has examined other risk factors associated with FE, including sociodemographic, behavioral/situational, and psychological factors, each of which is discussed in turn.

The research on whether age is a risk factor is mixed. While many studies have found a link between age and FE (AARP et al., 2011; FINRA Investor Education Foundation, 2013; Holtfreter et al., 2014), others have shown the opposite, that older adults are less at risk than their younger counterparts (Titus et al., 1995). Similarly, James et al. (2014) found a link between factors such as income, cognitive function, psychological well-being, social support, financial and health literacy, and age with scam susceptibility (with susceptibility increasing with age) but with no measure of financial exploitation. Income is related to FE risk in complex ways. For example, those with lower incomes are more likely to be at risk for lottery scams, while those with higher incomes are more at risk for investment scams (AARP et al., 2011). The extant data on race is similarly mixed, with many studies finding no difference based on race (Kerley & Copes, 2002; Titus et al., 1995). However, data from the Federal Trade Commission (FTC) revealed that Black older adults are more likely to be victims of FE than non-Hispanic whites (2004). Among a sample of Black older adults, those with lower levels of health and financial literacy, lower semantic memory, and lower psychological well-being were found to be at greater risk of FE (Yu et al., 2021). Other research suggests that Black older adults are less at risk of FE, though no mechanism is given to explain this finding (Han et al., 2021).

Behavioral and situational variables that are related to FE include risk-taking behavior (Schoepfer & Piquero, 2009), exposure to sales situations (AARP et al., 2011; FINRA Foundation, 2007), remote purchasing (Holtfreter et al., 2014), and adverse life events (Consumer Fraud Research Group, 2006). Psychological traits of low self-control/impulsivity (Holtfreter et al., 2014), openness to outside sources of information (AARP, 2007, 2008), and interest in persuasion messages have also been linked to FE (AARP et al., 2011). Cognitive factors also play a significant role. For example, Lichtenberg et al. (2016) found that decisional abilities are linked to financial exploitation, suggesting that cognitive impairments may lead to poorer financial decision-making, increasing vulnerability.

Finally, financial literacy has been connected to the risk of FE (AARP, 2007, 2008; Consumer Fraud Research Group, 2006). Financial literacy is using knowledge and skills to manage financial resources effectively. As with income, the findings are mixed based on the type of FE; investment fraud is more common among those with higher levels of financial literacy, and lottery scams are more common among those with low financial literacy (James et al., 2014). Additionally, prior research has demonstrated that a decline in cognitive function is associated with decreased financial literacy (Boyle et al., 2013; Gamble et al., 2012). Overconfidence in financial literacy has also been associated with a greater risk of FE (Gamble et al., 2012). The research has found that increasing financial knowledge reduces scam susceptibility (Burke et al., 2022). Finally, Wood et al. (2016) documented that objective numeracy is directly linked to financial exploitation, highlighting that basic numerical skills are critical for protecting oneself against fraud.

Gaps in the Current Research

Despite research examining factors linked to FE in older adults, gaps in our understanding need to be addressed. Although there has been interest in exploring the impact of financial literacy, such as those cited above, models of FE have yet to simultaneously include financial skills, scam susceptibility, and FE. Prior research demonstrates links between financial skills and susceptibility (Engels et al., 2021), between financial skills and exploitation (Wood et al., 2016), and between financial susceptibility and financial exploitation (Hall et al., 2023, referred to as financial exploitation vulnerability). However, the indirect pathways (i.e., mediation analyses) between financial skills and FE have yet to be adequately explored, which limits our understanding of the relationship between these variables and FE. Moreover, though it is widely assumed that financial scam susceptibility is related to financial exploitation, little research has examined this relationship directly, particularly concerning the commonly used scam susceptibility questionnaire (James et al., 2014).

Current Study Objectives

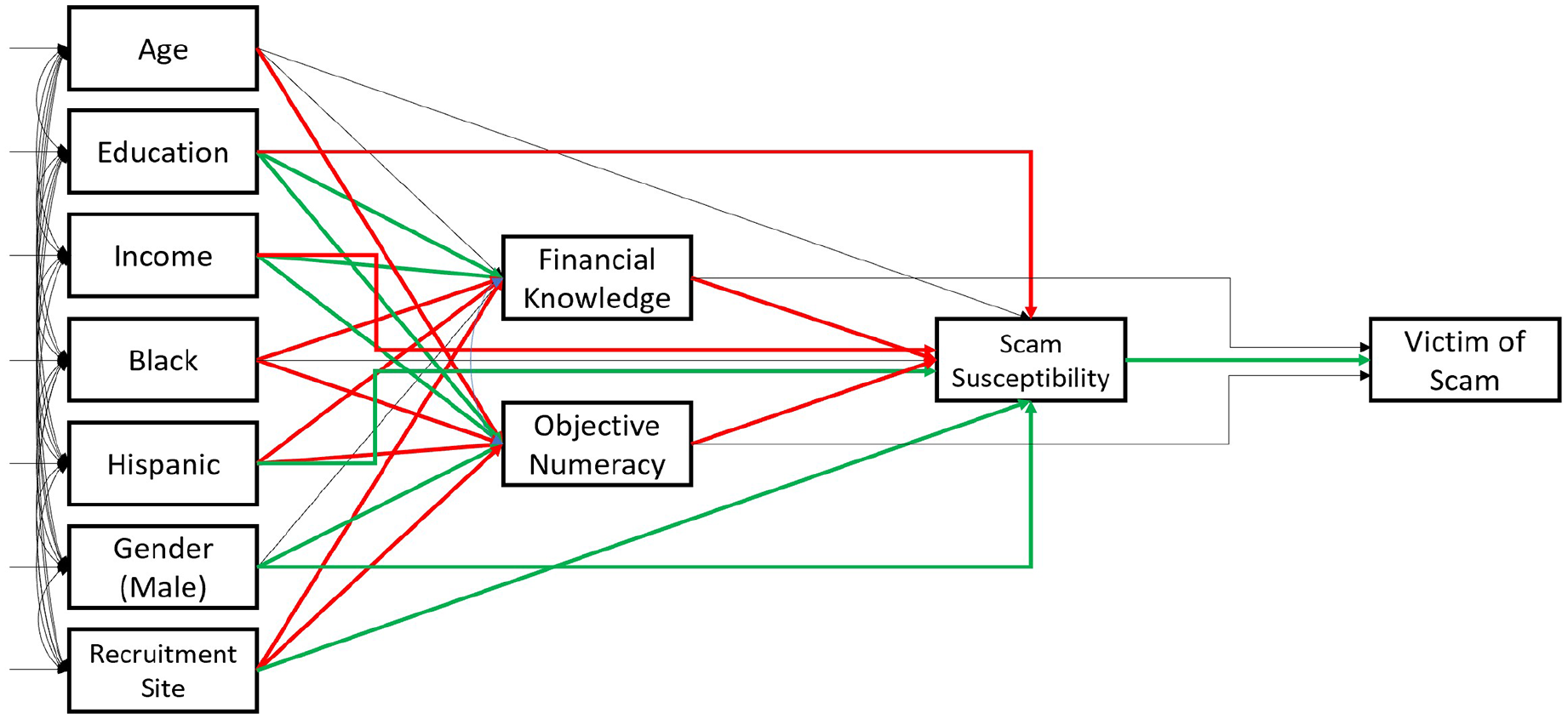

The present study seeks to examine the relationship between financial skills, financial scam susceptibility, and financial exploitation using baseline data from a longitudinal study investigating factors associated with financial exploitation among a diverse sample of older adults. The overarching model guiding the study depicts how the interaction among cultural and situational factors (such as race and current financial status) with personal-level cognitive variables (such as financial skills and knowledge) are linked to risk susceptibility and downstream victimization (see Figure 1). In the present study, we focus on a subset of this model, using two indicators of financial skills, objective numeracy and financial knowledge, and indicators of financial scam susceptibility and financial exploitation (see Figure 2). We hypothesized that higher levels of financial knowledge and objective numeracy would be associated with lower levels of financial scam susceptibility. Moreover, we hypothesized that higher scam susceptibility is associated with higher scam victimization. In addition, we examined the mediating role of financial skills on the relationship between age and education, as well as scam susceptibility. We hypothesized that older adults with less education would have lower financial skills (e.g., financial knowledge and objective numeracy), associated with higher scam susceptibility. Additionally, we hypothesized that higher financial skills would be associated with lower scam susceptibility and a lower risk of scam victimization (mediation). Finally, we include demographic factors, such as age, race, gender, and education, as covariates in our models examining financial skills and financial scam susceptibility.

Path model with significant paths highlighted (green is positive, red is negative).

Methods

Participants

All research was approved by an Institutional Review Board (IRB). Participants (N = 713) from two U.S. cities, Pittsburgh and New York, aged 60 and older, were recruited from the community to participate in a longitudinal study examining factors associated with financial scam susceptibility and financial exploitation. The present analysis uses baseline data from this study (Beach et al., 2023). Participants were excluded from the current analyses if they had missing data on any study variables, leaving an analytic sample of 672. Those with missing data did not differ significantly from those with complete data on the variables included in the model (all p’s > .05).

Measures

Table 1 includes counts and percentages or means and standard deviations for all study variables (as appropriate).

Sample Descriptive Statistics.

Mean (SD); n (%).

Demographics

Multiple demographic variables, including age, race, gender, education, and income, were assessed via a demographic questionnaire administered at baseline and included in our analyses.

Financial Variables

Numeracy

Numeracy was assessed using the numeracy scale (Lipkus et al., 2001).This scale asks the participant to complete 11 tasks, such as converting percentages to proportions and proportions to percentages, and how often a fair die comes up with an even number. The score is the sum of the total number of correct answers. The scale range is 0 to 11.

Financial Knowledge

Financial knowledge was assessed with four items adapted from the Health and Retirement Survey (James et al., 2014). Topics covered include interest rates, inflation, and investing basics. A single total score was computed, with one point for each correct answer. The scale range is 0 to 4.

Financial Scam Susceptibility

Financial scam susceptibility was assessed with the Scam Susceptibility Questionnaire used in the RUSH study (James et al., 2014). The scale assesses aspects of susceptibility, such as the propensity to listen to sales pitches and beliefs about scam targeting. The response scale is a six-point Likert scale with 0 = “Strongly Agree” and 5 = “Strongly Disagree.” Three items are reverse scored. An average score was computed for each participant across the five items. The range of averages was from 0 to 4.4, with higher scores representing more scam susceptibility.

Victim of Financial Scams

A single-item indicator was used to assess whether an individual was a victim of a financial scam, with a binary variable coded 1 for “yes” and 0 for “no.” There are seven different types of financial scams listed: prize, grant, inheritance, or lottery scam; debt or taxes scam; fake charity scam; job or business opportunity scam; investment scam; products/services scam; and trusted other scam (Morgan, 2021).The current data range was from 0 to 5, coded into a binary variable, with yes on any item coded as a 1 and 0 for not being a victim of scams.

Data Analytic Plan

Structural equation modeling was used to test hypothesized relationships between financial skills and knowledge, scam susceptibility, and scam victimization. Demographic factors, including gender, age, race, education, and income, were included in the model as covariates, as was the recruitment site. Further, as noted, we conducted mediation analyses to examine if scam susceptibility mediated the relationship between financial skills and knowledge and scam victimization and if financial skills and knowledge mediated the relationship between age and education and scam susceptibility. In mediation analysis, the total effect represents the overall relationship between the independent variable (X) and the dependent variable (Y), combining both direct and indirect pathways. The direct effect is the portion of this relationship that remains after accounting for the mediator (M), while the indirect effect captures how X influences Y through M. It is possible for the indirect effect to be significant while the total effect is not. This occurs when the direct effect is small or when the mediator fully explains the relationship between X and Y. In such cases, the mediator plays a crucial role in understanding the relationship between X and Y, even when the total effect appears weak or non-significant. All analyses were conducted in RStudio version 2022.12.0, using the lavaan, DiagrammeR, and gtsummary packages. Comparative fit index (CFI), root mean square error of approximation (RMSEA), and standardized root mean square residual were used to assess model fit according to standard conventions (CFI > 0.95, RMSEA < 0.06, SRMR < 0.09, Hu & Bentler, 1999). Additionally, proposed mediation paths were tested with bootstrapped standard errors (n = 10,000). Multiple random seeds were used to examine if the results were consistent across samplings.

Results

Descriptive Statistics

The average age of participants was 72.6 (range: 60–97, median = 71, SD = 8.58). The sample was 63.40% female, 39.88% Black, and 17.86% Hispanic. The sample was generally well educated, with 80.36% indicating that they had completed some college and 25.30% having an income of $70,000 or higher. Since participants were recruited from two cities, all analyses included the site as a covariate. Table 1 presents descriptive statistics for the sample and the variables used in the study.

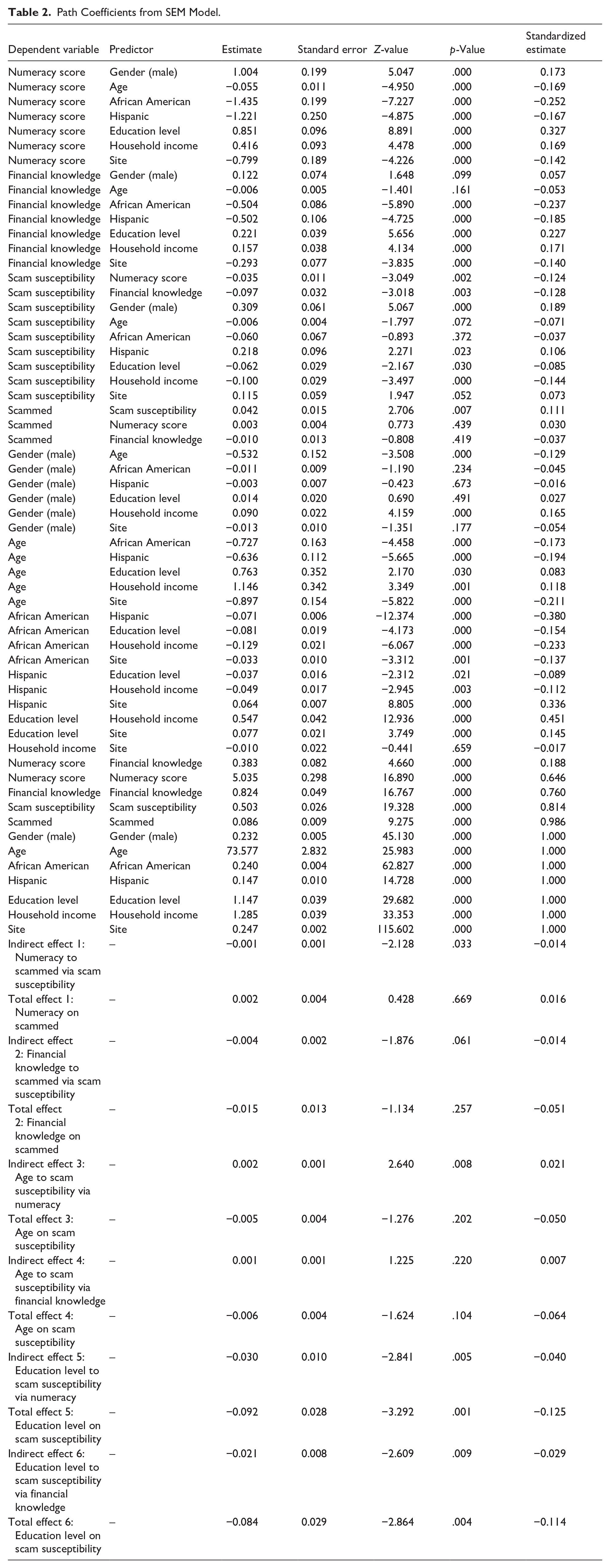

The hypothesized model was robust and demonstrated excellent model fit (CFI = 0.99, TLI = 0.94, RMSEA = 0.043, SRMR = 0.017). See Figure 2 for the path model. Of note, financial knowledge and objective numeracy were both negatively related to scam susceptibility. Individuals with more financial knowledge and higher objective numeracy were less susceptible to scams. Moreover, as predicted, scam susceptibility was positively associated with whether an individual was a victim. Individuals with high scam susceptibility to scams were more likely to be victims of scams.

Regarding demographic factors, individuals who identified as Black or Hispanic generally had lower numeracy and financial knowledge scores than White participants. There was no significant difference in scam susceptibility for Black participants. However, Hispanic participants were generally more likely to be susceptible compared to White participants. Education and income were significantly related to numeracy, financial knowledge, and scam susceptibility in the expected directions. Higher levels of education and higher income were associated with higher numeracy, higher financial knowledge, and lower scam susceptibility.

Three proposed mediational pathways were significant, two pathways showed results that varied depending on the starting seed used for bootstrapping (with p-values fluctuating slightly above and below the 0.05 threshold), and one pathway was consistently non-significant (see Table 2 for path coefficients). As hypothesized, older age was associated with lower numeracy and greater financial scam susceptibility; however, the indirect pathway from age to scam susceptibility through financial knowledge was non-significant. Both indirect effects between education level and financial scam susceptibility through objective numeracy and financial knowledge were significant and in the predicted direction. Higher levels of education were associated with more objective numeracy and financial knowledge, which, in turn, were associated with lower scam susceptibility. The mediation of financial knowledge and objective numeracy on getting scammed via financial scam susceptibility was marginally significant (p’s in the range .04–.07, depending on the starting seed), with the effects aligning with the hypothesis that higher financial knowledge and numeracy indirectly reduce scam susceptibility, thereby decreasing the risk of being scammed.

Path Coefficients from SEM Model.

Discussion

The present study evaluated the relationship between financial skills and knowledge, scam susceptibility, and FE. Our findings largely supported the proposed theoretical model, demonstrating that financial knowledge and objective numeracy were associated with financial scam susceptibility, which in turn was linked to scam victimization. These findings build on prior research highlighting financial literacy as a key factor in fraud risk (AARP, 2007). Furthermore, sociodemographic factors, including age, race, and education, were significantly related to differences in objective numeracy, financial knowledge, and scam susceptibility. Older adults, racial/ethnic minorities, and individuals with lower education had lower numeracy and financial knowledge, increasing their risk of scam susceptibility. These findings align with previous research suggesting that sociodemographic disparities contribute to FE vulnerability (AARP et al., 2011; James et al., 2014).

Our study extends prior research by clarifying why racial disparities in scam victimization may exist. Black older adults were at greater risk for financial exploitation, likely due to lower financial knowledge and numeracy, which increased scam susceptibility. This aligns with prior research showing that Black individuals report higher victimization rates (Federal Trade Commission & Anderson, 2004; Yu et al., 2021). Moreover, research suggests that lower financial and health literacy, coupled with psychological vulnerabilities, may contribute to increased FE risk among Black older adults (Yu et al., 2021). The data on Hispanic individuals was more nuanced. While this group also exhibited lower financial knowledge and numeracy, they were not at increased risk of scam susceptibility. Indeed, the opposite was true; they were less likely to be susceptible to financial scams, a finding that warrants further investigation.

Our findings also reinforce prior work linking aging to increased scam susceptibility due to cognitive decline and financial decision-making difficulties (AARP et al., 2011; FINRA Investor Education Foundation, 2013; Holtfreter et al., 2014). In line with previous findings, the oldest older adults were at greater risk for financial scams due to lower objective numeracy, which was associated with a greater risk of scam susceptibility. This is concerning given that cognitive declines in later life are associated with reduced financial literacy and increased FE risk (James et al., 2014; Lichtenberg et al., 2016) Similarly, education played a key role: higher education levels were linked to greater financial knowledge and numeracy, which reduced scam susceptibility. These findings support prior research showing that financial literacy improves with education and is critical for scam prevention (Austin & Arnott-Hill, 2014). Similar findings were demonstrated for income.

Our findings underscore the importance of objective numeracy and financial knowledge as modifiable intervention targets for reducing scam susceptibility. Additionally, our results suggest that minority populations and older adults in later life stages may face a higher risk of financial scams. Addressing these disparities requires increased resources to help protect these at-risk populations from financial exploitation. Financial education programs tailored for older adults, particularly those in racial/ethnic minority groups or with lower formal education, may be an effective preventive strategy.

Objective numeracy and financial knowledge may be amenable to change through targeted educational interventions to increase numeracy and knowledge. For example, a review of financial literacy interventions found a positive correlation between these interventions and financial literacy (Austin & Arnott-Hill, 2014). Moreover, our findings suggest other potential paths for intervention targets, such as providing more significant financial support and community resources in disadvantaged areas, including free financial education, help with taxes, financial consultations, and wealth management services.

The present work has some limitations. One limitation is using a single-item measure to assess whether individuals were victims of a financial scam. While this measure assesses multiple domains of financial scams, it does not allow for examination of how many times an individual fell victim to a single type of scam. Moreover, this was a self-report measure, and individuals may not want to report that they experienced a financial scam because of concerns about social desirability. Further, the data used in the analysis was cross-sectional. Thus, we cannot examine longitudinal changes in factors that may increase or decrease the risk of vulnerability and experience of scams. However, the current study is part of a larger project which aims to address this gap by gathering longitudinal data.

The present study focused on examining the relationship between financial skills (objective numeracy and financial knowledge), scam susceptibility, and financial exploitation (FE) within the context of a broader theoretical framework. While cognitive factors such as decisional abilities and general cognitive function have been linked to financial exploitation risk in prior research (Lichtenberg et al., 2016), our primary aim was to explore the mediating role of financial skills and scam susceptibility. We chose these measures specifically because they are modifiable intervention targets with potential to inform preventive strategies. Additionally, given the cross-sectional nature of our baseline data and the extensive inclusion of demographic and financial skill variables, we opted to prioritize measures that directly addressed our hypothesized relationships.

A strength of the present study is that the indicators of financial skills (objective numeracy and financial knowledge) were assessed with skills-based measures, overcoming some deficits inherent in prior work that relied on self-report measures. Our exploratory analyses revealed no significant relationship between a measure of subjective numeracy and scam susceptibility or financial scam victimization. Individuals may overestimate their numeracy, placing them at risk of being scammed. An additional strength was the large, diverse sample drawn from two locations.

Conclusion

Overall, we provide evidence in support of a model of financial exploitation. Demographic factors interplay with financial skills and knowledge to predict scam vulnerability and risk of being a victim of scams. These processes interact in complex ways, which point to potentially modifiable intervention targets, such as psychoeducational interventions to increase financial knowledge or increase an individual’s skill in numeracy. More resources are needed to help protect at-risk groups, including older adults and other minority populations, so that society does not continue to perpetuate these inequalities through future generations, which is increasingly important as the population continues to age.