Abstract

The recent upheavals in content governance at X and Meta have something in common: both were initiated by the platform's controlling shareholders. As the US economy and government become increasingly dominated by hyperrich tech oligarchs, Elon Musk and Mark Zuckerberg embody a newly assertive ideological force in the governance of the digital public sphere: platform ownership. Yet scholarship on content governance has until now had little to say about ownership or its influence. To bridge this gap, this article draws on media ownership research and the study of media moguls to ask: who owns the major public communications platforms, and how do these owners influence content governance outcomes? To map platform ownership, I examine public records including SEC disclosures to distinguish individually-controlled oligarchic firms from diversely-held market-controlled firms. On this basis I argue that Meta and X's ownership structure is distinctly oligarchic, as they are more directly controlled by individuals than other major platform firms such as Bytedance, Apple, and Microsoft, and, to a lesser extent, Google, Reddit and Bluesky. For content governance outcomes, I review evidence of Elon Musk and Mark Zuckerberg controlling content policies at their respective firms, and discuss whether their actions are best explained as ideologically-motivated political instrumentalism, self-interested economic instrumentalism or market-wide commercial logics. I also discuss how ownership influence may be constrained by the professional logics of Trust and Safety management, and point to precedents in media law and policy to constrain owner power and build non-commercial alternatives.

Keywords

“I think what she's saying is that if you do this and you control the publishers and you run for office, that makes you a modern day William Randolph Hearst,” [Facebook VP Elliot Schrage] explains. “You know, with the publishing and the politics and the…”

“Oh,” Mark says softly. “Is that a bad thing?”

—Sarah Wynn-Williams (2025), recounting a conversation with Mark Zuckerberg

Introduction

In recent years, platform owners have become actively and visibly involved in shaping content policies, and, through them, public discourse across the globe. In 2022, Elon Musk, the richest person in the world, acquired Twitter (now “X”) and careened its content moderation policies toward a new far-right course. In early 2025, Mark Zuckerberg announced a similar right-wing turn, stripping away key protections against hate speech and disinformation (Meta, 2025). For both figures, these moves coincide with overtures to the US Republican right and President Donald Trump. Speculation abounds as to whether they are motivated by genuine ideological conviction, a tactical need to mollify the incumbent administration, or some combination thereof (Murphy, 2025). More than ever, the interests and ideologies of a small few “tech oligarchs” (Cohen, 2025) are proving essential to understanding the twists and turns of platform content governance.

These owner-driven upheavals at Meta and X point to a gap in the literature on content moderation, where ownership influence is rarely discussed at all. Whilst content moderation is widely acknowledged to be a “commercial” enterprise (Gillespie, 2019; Roberts, 2019), we lack the tools to discuss how the particular interests and agendas of individual owners can shape platform decision-making, and run up against other contradictory forces within the firm and the market (Narayan, 2024). In a recent contribution, Julie Cohen (2025) warns against an emergent tech oligarchy, in which a handful of platform owners exert power not only through their extreme wealth and control of the state, but through their control of technological infrastructures. This infrastructural platform power is multifaceted—from setting product standards to facilitating police surveillance—but includes the capacity to shape public discourse through their control of public communications.

This article explores how conditions of tech oligarchy can inform the study of online content governance. To this end, it draws on precedents in media ownership research, and parallels between media moguls like Rupert Murdoch and platform oligarchs like Elon Musk. In the 20th century, wealthy individuals could acquire immense power over public over communications through their private ownership of mass media industries. Today, public communications platforms offer a new way for the super-rich to control public discourse at scale. Media ownership research has helped to interrogate how different ownership structures have shaped media performance, and to call attention to the concentrated power of media oligarchs. The goal of this article is to bridge these gaps and investigate how ownership research can inform our understanding of online content regulation.

I begin my analysis by reviewing key contributions in platform content governance and media ownership research. Building on the comparative institutional media sociology of Rodney Benson et al. (2025), I conduct a two-step analysis: mapping platform ownership's institutional forms and then comparing institutional logics related to content governance. First, to map ownership, I review public records including SEC disclosures to compare features like corporate form, shareholder type, ownership concentration, and management composition. On this basis I distinguish individual-owned oligarchic firms from diversely-held market-owned firms, and argue that Meta and X's ownership structures are distinctly oligarchic, compared to other major platform firms such as Bytedance, Apple, and Microsoft, and, to a lesser extent, Google, Reddit and Bluesky. Second, for content governance outcomes, I review evidence of Elon Musk and Mark Zuckerberg pursuing self-interested political instrumentalism at their firms, and the degree to which market forces and professional norms in Trust and Safety may constrain ownership influence as countervailing institutional logics. Overall, I argue that concentrated individual control at X and Meta plausibly accounts for their radical right-wing turn, and propose more sustained comparative analysis to assess the degree of divergence from market-controlled firms and their relationship to Trust and Safety management.

Background: Platform content governance and media ownership

Platform content governance

Online platforms are powerful gatekeepers for public communications, and there is a growing body of scholarship interrogating how platforms exercise this power. Many contributions focus on “content moderation,” or the organized screening of user activity to enforce certain standards for content or behavior (Gillespie, 2019; Roberts, 2019). Other researchers point to a broader set of governance modalities through which platforms shape online media; for Thomas Poell, David Nieborg and Brooke Erin Duffy (2022), in addition to moderation, platforms also govern cultural production through curation (algorithmically ranking or sorting content for discoverability) and regulation (setting legal and technical standards for participation). Platform operators thus have a range of instruments at their disposal to steer public discourse, from relatively fine-grained moderation sanctions to more constitutive and all-encompassing design choices shaping the affordances of platform technologies.

The extent to which platforms actually control their users or public discourse is of course not absolute. Users retain substantial autonomy; platform moderation and curation are error-prone (Gorwa et al., 2020), and users are often able to circumvent or game their detection logics (Steen et al., 2023; Ziewitz, 2019). More broadly, the power of platform gatekeeping in the broader communications system, relative to other actors such as news media, remains debated (e.g. Napoli, 2019; Schlosberg, 2016a; Seipp et al., 2023). A small number of mostly US-based platforms are influential globally, but their relationship to local media and platform markets differs across national contexts (Agarwal, 2025; Khalil and Zayani, 2023). My goal here is not to resolve these questions on the nature and extent of platforms’ infrastructural power; rather, my question of ownership concerns who wields this power, and to what end, at the level of the platform firm.

Concerning the motives behind content moderation, platform governance scholarship has since its earliest contributions always stressed that platform content decisions are fundamentally commercial in nature (Roberts, 2019). For Tarleton Gillespie (2019), content moderation is at the core of platform services’ value proposition to their users. The commercial logics of content policy are not necessarily predictable, however, but contingent, strategic, and deeply political. As a starting point, profit-seeking platforms try to minimize costs and therefore avoid content moderation where possible. Where they cannot avoid moderating, they limit costs through pervasive outsourcing and automation (Roberts, 2019). Under these resource constraints, content policies must reconcile diverse and often contradictory demands from their end-users (e.g. Myers West, 2018) and advertisers (Griffin, 2023; Joseph and Bishop, 2024). Beyond these market pressures, moderation strategies are shaped in large part by second-order reputational, political and regulatory considerations, which include binding legal frameworks as well as informal pressure from journalists, NGOs, governments, political parties, and so forth (Klonick, 2017). Taken together, these factors give rise to a “networked governance” in which the above stakeholders vie for influence over platform policy—and platforms enter strategic partnerships with and against them to outsource moderation costs and deflect responsibilities (Caplan, 2023). This is of course not a contest amongst equals; the struggle over platform content policies reflects and reinforces structural inequalities including colonialism and imperialism (Siapera et al., 2015), racism (Noble, 2018; Siapera and Viejo-Otero, 2021) and patriarchy (Gerrard and Thornham, 2020).

Over the past decade, the politics of platform regulation have trended toward more restrictive and proactively enforced content standards. In their early years, platforms insisted that they were merely neutral intermediaries without any responsibility for the content they carry—a notion that scholars have questioned since its inception (Gillespie, 2010; Grimmelmann, 2008; Napoli and Caplan, 2017). This pretence of being “just an app” became increasingly difficult to maintain as platforms developed more sophisticated governing capacities to target and curate content and encountered ever-greater societal expectations to address harms on their service (Gillespie, 2019). Platforms may never have been truly neutral, but their media-like functionality in shaping public discourse has steadily become more technically refined, politicized, and institutionalized as a form of speech governance.

This process of politicization has now also reached platform owners, with Mark Zuckerberg and Elon Musk becoming more visibly active in shaping content governance standards for their services (to be explored further in Section “Private logics: Political instrumentalism and partisanship at oligarchic firms”). Around the same time, many wealthy tech founders and CEOs have started to ally themselves more openly with the US government and the Republican party under Donald Trump—culminating in the now-infamous image of influential owners and CEOs with front-row seats at the 2025 inauguration (Swenson, 2025). But the academic literature on public communications platforms and content governance has until now had little to say about ownership. The position of CEO and owner are often conflated, and far more is said about stakeholders than about shareholders.

An exception here is Julie Cohen's (2025) recent account of tech oligarchy, which places platform owners as the center of a new political-economic configuration where “extreme concentrations of material wealth [are] deployed to obtain and protect durable personal advantage.” These tech oligarchs, through their ownership of platform infrastructures, “have played uniquely influential roles in structuring technological development in particular ways that align with their personal beliefs and who now wield unprecedented informational, sociotechnical, and political power” (Cohen, 2025). Tech oligarchs now leverage the power of the state and its laws, as well as platforms and their technologies, to further enrich themselves and to pursue technopolitical vanity projects—such as AI singularity and space colonization—toward “a human future that they alone determine” (Cohen, 2025).

Whereas Cohen's account is concerned with the digital economy in its broadest sense, my inquiry is specific to public communications platforms and their control of the public sphere. It concerns that subset of oligarchs which, in legacy media, have also been referred to as “press barons” or “media moguls”—figures like Rupert Murdoch and Silvio Berlusconi, who leverage their private ownership of communications industries to influence public discourse. What does it mean for public communications industries to be controlled by wealthy individuals? For this answers I now turn to media ownership research.

Media ownership: Moguls, markets and alternatives

Ownership by wealthy individuals or families has historically been common in most Western media systems (Benson et al., 2025). It exists alongside alternative models, including public, non-profit and employee ownership. In recent decades, private or family firms have also been supplanted by ever-larger, publicly-traded corporate conglomerates (E. M. Noam, 2016). Media ownership research has helped to map these diverse ownership forms and their effects on public discourse (Downing, 2011). Below I discuss key contributions in political economy and sociology of the media, and their relevance to platform governance, including anti-capitalist, anti-monopoly and comparative institutional perspectives. The latter are most salient for our inquiry as they contain detailed analyses of different firm structures and the potential contradictions between private and market logics in public communications.

A general problem facing researchers is that ownership influence is typically invisible (Schlosberg, 2016b). Owners tend to deny and obfuscate their influence over media production, especially in news journalism. Acts of interference are occasionally leaked, but these glimpses into the inner workings are occasional and anecdotal. And even without direct interference, owners can still exercise power indirectly; for Graham Murdock, owners more commonly exercise “allocative control,” in determining how resources are distributed—rather than direct “operational” control of day-to-day decisions (Murdock, 1982). Other authors draw on Steven Lukes’ (1974) “three dimensions of power” to argue that media owners exercise an invisible “non-decision-making power” that sets the conditions under which media professionals carry out their work (Benson et al., 2025; Schlosberg, 2016a). The structuralist and comparative theories I review below can be understood as responses to this problem of unobservable influence.

Some of the most influential commentaries on media ownership take a class-based anti-capitalist perspective (Herman and Chomsky, 1988; Schiller, 1970). At the risk of generalizing between competing tendencies in the diverse field of critical political economy (Downing, 2011; Hardy, 2014), these contributions tend to position private media ownership as part of a broader ownership class, which acts as a nexus of capitalist interests and predictably inclines commercial media outputs toward a pro-capitalist, pro-imperialist, anti-worker ideology (Herman and Chomsky, 1988; Murdock and Golding, 1973; Schiller, 1970). Within these parameters, capitalist ownership may permit a broad diversity of viewpoints, but it works alongside other structural factors to police the boundaries of acceptable opinion and foreclose more radical alternatives (Herman and Chomsky, 1988).

Without dismissing the power of these structuralist critiques—which continue to inspire trenchant media criticism to this day (Tasseron, 2023)—they are not directly concerned with the power of individual owners, or accounting for differences in performance between firms (Golding and Murdock, 1991; Schudson, 1989). For platform governance, radical structuralist critiques such as these can help us think through the ways that platform capitalism controls content governance agendas and excludes certain viewpoints or ideologies from the realm of the possible (e.g. Fuchs, 2018). They are less immediately helpful in studying individual agents like Musk or Zuckerberg within these structures.

Another broadly structuralist strain of research concerns the question of ownership concentration. Here the concern is with the number of owners in a given media market (Bagdikian, 1987; Noam, 2009). This research has called attention to waxing and waning trends of concentration across national media markets (Mastrini, 2019; Zhao, 2004), with overall global concentration trending upward due to aggressive mergers-and-acquisitions policies unleashed in the post-Reagan era (Noam, 2009). For liberal theorists, media concentration is considered harmful to democracy as it risks undermining competition between firms as well as pluralism of available viewpoints (Baker, 2006). Platforms now raise comparable concerns about market power, and monopolization (Moore and Tambini, 2018; Napoli, 2019). for Natali Helberger (2020) and Theresa Seipp et al. (2023), these unequal platform markets raise equivalent democratic concerns about concentrated, media-like “opinion power.” However, since platforms are uniquely prone to winner-takes-all dominance (Barwise and Watkins, 2018), reforms to introduce competition or create “counter-power” (Helberger, 2020) remain challenging. Until now these debates in platform governance have largely focused on the relative power of different platforms at the level of the market, rather than the level of the platform firm and the power of individual shareholders like Musk or Zuckerberg within these firms.

As for the role of individual moguls, a more promising line of inquiry can be found in institutionalist approaches, which distinguish in finer detail between different organizational types or forms of ownership. In the critical political economy tradition, comparative researchers have for instance compared performance between commercial and publicly-owned media (Curran and Seaton, 1981; Golding and Murdock, 1991); increasing corporatization of the media in the hands of ever-larger, publicly-traded conglomerates (Murdock, 1982); and its financialization under the sway of institutional investors (McChesney and Pickard, 2011; Winseck, 2010). A recurring point of debate that emerges here is the relative performance of private, family, or individual-controlled news media compared to large corporate conglomerates (e.g. Murdock, 1982; Hanretty, 2014).

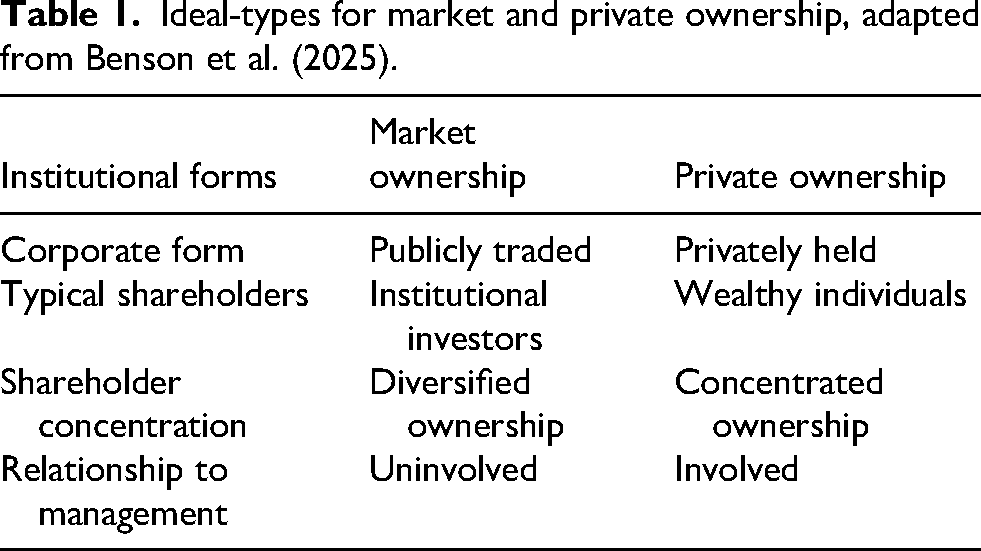

Building on these earlier contributions, Rodney Benson et al. (2025) have developed a more detailed typology of different ownership forms, which are associated with distinct institutional logics for media production. In Benson's framework, private ownership in the hands of wealthy individuals is contrasted with market ownership, where ownership tends to be diversified amongst institutional investors. These ideal-typical institutional forms exhibit the following characteristics: for private ownership, (a) as a legal entity, the firm is typically privately held rather than public listed and traded on the stock exchange; (b) investors are often private individuals or families, and (c) ownership in the firm is relatively concentrated, often with a single beneficial owner holding a controlling share. Additionally, (d) private owners tend be relatively closely involved in day-to-day management decisions. All this can be contrasted with market ownership, in which the firm is (a) typically publicly listed, and thereby attracts a larger amount of (b) institutional investors, which serves to (c) diversify ownership and disperse control. This dispersed ownership tends not to be actively involved in management, leaving executives relatively autonomous (d). Table 1 below summarizes these distinctions.

Benson's model also describes non-profit and public ownership as alternative models; these are discussed in less detail here since they are less germane to the study of (presently existing) platforms. But the market/private-distinction is highly relevant to platforms, as we will see further below.

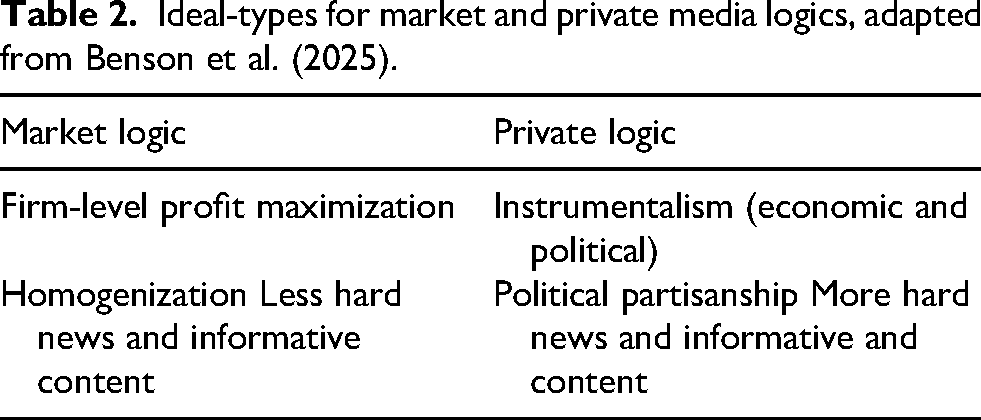

Market ownership and private ownership matter because they are associated with distinct institutional logics, in terms of how the firm is managed and produces content. For market ownership, the market logic entails a stricter insistence on firm-level profit maximization. A defining trend since the 1990s, across markets in general and media in particular, has been their financialization: the growth of the financial sector and financial assets relative to the industrial and other sectors of the economy, leading many firms to attract more institutional investors, such as hedge funds and private equity, and to take on higher levels of debt (Winseck, 2010). For media firms, research shows that financialization tends to drive a stronger emphasis on cost-cutting and on short-term performance, as well as deference to the demands of audiences and advertiser (Winseck, 2010). The private logic, by contrast, is more erratic and driven by the individual whims of the owner; Benson et al. (2025) refer to this as a “instrumentalist” logic, in which the firm is put at the service of the individual's interests. These interests include, but are not limited to, profit within the firm. An owner may also choose to forego firm-level profits in service of their other economic interests—for instance, securing positive coverage for their non-media holdings—or for political or ideological purposes (Table 2).

It is important to note that market ownership is not necessarily considered “better” for media or democracy; the literature is deeply divided on this point. On the one hand, individual private owners are more likely to interfere in editorial decision-making and thus jeopardize the media's independence and objectivity. On the other hand, privately-owned firms are also less bound to the dictates of shareholder value and profit maximization and can choose to forego profit in favor of other ideals. Those ideals might include personal, partisan agendas but also commitments to investing in quality journalism. Comparative analysis shows that private ownership is associated with stronger forms of political bias and partisanship, but also with higher levels of informative, educational and public affairs content (Benson et al., 2025; Hanretty, 2014). Market-controlled firms, by contrast, tend to prioritize audience-pleasing entertainment and newsroom cost-cutting to the detriment of public affairs content, as well as standardization and homogenization to the detriment of localism and pluralism (Hanretty, 2014; McChesney and Pickard, 2011).

In sum, individual control over communications industries has a mixed record: it opens the door to oligarchic influences and highly partisan tabloid press, but it can also help to insulate journalistic enterprises from cost-cutting pressures of the market that have worked to commodify public communications and decimate newsrooms across the globe. In the following sections, I will explore how private and market ownership pertain to public communications platforms.

Mapping platform ownership forms

Method

The following section conducts a comparative institutional analysis of the ownership of public communications platforms, including social media platforms and app stores. Social media platforms are understood here as platforms that offer public communications (i.e. between a unrestricted number of users) as a primary functionality of their service (Burgess et al., 2019). This definition includes platforms like YouTube and Instagram, and excludes private communications platforms such as WhatsApp or Signal and non-communications platforms such as Amazon or Airbnb. My analysis centers these public communications platforms because, like media, their governance has a distinct capacity to influence public discourse and cultural production (Poell et al., 2022; Napoli and Caplan, 2017). In addition, I also include the dominant app stores, since these have also played an increasingly active and influential role in content-level standard setting, especially in policing “alternative” platform offerings such as Gab and Parler (Van Dijck et al., 2023). The large social media platforms, together with the large app stores, are some of most important gatekeepers for public communications online.

My analysis focuses on popular platform firms with a large global audience. These are mostly US-based platforms, with the exception of Singapore-based TikTok. Table 1 identifies their parent companies, which will be the targets for the subsequent firm-level ownership analysis. Bluesky boasts a substantially smaller reach than other firms listed here, but is included as a significant new market entrant. The largest platforms missing from this list are Chinese platforms, and to a lesser extent Russian platforms, which form their own alternative ecosystems to the US-led global platform market (Huang and Tsai, 2022; Qi et al., 2024; Rolf and Schindler, 2023). These platforms are excluded from my analysis due to methodological constraints—information about ownership are not as readily available—and due to potential incommensurability: direct comparisons between these diverse jurisdictions are complicated severely by significant differences in corporate governance and public communications (Mancini and Hallin, 2012). TikTok, though based in Singapore, is included in the analysis due to its global reach, which is broadly co-extensive with US platforms—whilst acknowledging potential differences in Singaporean corporate governance that may complicate direct comparisons with its US-based counterparts (Table 3).

Ideal-types for market and private ownership, adapted from Benson et al. (2025).

Ideal-types for market and private media logics, adapted from Benson et al. (2025).

Public communications platforms and their parent companies.

For each of these firms, I aim to map firm-level ownership institutions and the degree of market or private control, corresponding to Benson et al.'s ideal-types outlined in Section “Media ownership: moguls, markets and alternatives.” Hence, I review whether their shareholdership is: (a) publicly traded or privately held, (b) owned by institutional investors or wealthy individuals, (c) concentrated or diversified, and (d) represented in management.

For public firms, the most important data source for this analysis is financial reporting for the US Securities and Exchange Commission (SEC). Under US securities law, firms traded on the stock exchange are required to report the identities of all beneficial owners with an interest exceeding 5% of outstanding equity. Shares held by senior executives are also identified. These reports, which are part of the SEC Schedule 14A form, or “Proxy Statement,” are publicly available online in the SEC's EDGAR database. 1 Data were collected between May and August 2025.

For private firms, mapping ownership is more challenging since they are not obliged to disclose their beneficial owners. Some firms disclose voluntarily, while others remain secretive. Litigation and investigative reporting can also uncover ownership data. For these firms, the below reflects a best-effort review of such publicly available sources.

To measure ownership concentration, I distinguish between diversified and concentrated ownership. In Djankov et al.'s (2003) approach to in-firm ownership concentration, the shareholder with the largest interest can be identified as the beneficial owner, unless the largest shareholder holds less than 20% of shares. In this case, the firm's ownership can be considered diversified. I propose several refinements to this general approach. First, I differentiate between degrees of concentrated versus diversified ownership. In some cases the beneficial owner commands a controlling share of over 50%, and in other cases there are power-sharing arrangements between a small number of joint controllers. Hence I distinguish between sole controller, joint controller, and diversified ownership structures. To capture this, I calculate the minimum number of shareholders needed to attain a >50% voting majority. 2 A minimum voting majority of 1 indicates sole control, 2 or 3 indicates shared control, and 4 or higher indicates diversified control. As we will see below, this approach helps to capture more granular differences in concentrated control between different platform firms.

Second, I also distinguish between economic and voting rights. 3 Many platform firms maintain dual-class stock structures, in which legal control in terms of voting rights is separated from economic ownership or equity. A privileged class of stock (“Class B”) entitles its holders to outsized voting rights, relative to their dollar value, helping them to retain a decisive say in corporate decision-making beyond their economic stake. As described by Julie Cohen (2025), dual-class stock structures have been an essential instrument for Silicon Valley founders to retain voting power in their firms even after their initial public offering (“IPO”) on the stock market. In media research, dual-class stock structures are less common, except for digital-first startups outlets, and remain largely understudied (Benson et al., 2025).

The precise effect of these structures on corporate governance remains debated, and is returned to below (Hossain and Kryzanowski, 2019). For our mapping exercise, these dual-class stock structures are significant because they destabilize the ideal-typical understanding of private versus market ownership as coinciding with the distinction between public versus private incorporation. For big tech, publicly-traded firms with dual-class stock can be under tighter individual control than even certain privately-held firms. As we will see, this is the case for some but not all platform firms, and tracking private versus market control in this market therefore requires a granular case-by-case analysis.

Findings

Table 4 provides an overview of key findings. We see important differences between firms; some are subject to highly concentrated individual control, and others to joint or diversified control. Amongst institutional investors, the largest stakes are almost invariably held by BlackRock and Vanguard—two of the “Big Three” asset managers that together control a substantial portion of the global economy (Bebchuk and Hirst, 2022; Christophers, 2020). However, through dual-class structures, powerful founder-CEOs have retained control over several public firms: Mark Zuckerberg maintains a tight grip over Meta, being its sole controller as well as its CEO. For Alphabet, Larry Page and Sergei Brin share joint controllership. They are no longer directly involved as executives, though they remain involved at arms lengths as board members. Reddit is controlled, via parent company Advance Magazine Publications, by the Newhouse Family, who are also major shareholders in Condé Nast, Charter Communications, and several other media firms (Maier, 1997). Their power is limited to some extent by having granted an irrevocable proxy of their voting rights to Reddit's founder and CEO, Steve Huffman. Microsoft and Apple, by contrast, are closer to the ideal-typical market ownership model, without a dual-class stock structure and without any powerful individual owners besides institutional investors.

Ownership of public platform firms.

As for private firms, much remains uncertain, and precise concentration ratios cannot be calculated. Still, certain key figures are available. TikTok reports that 60% of Bytedance stock is held by institutional investors, including BlackRock and the Susquehanna Group, and another 20% by the firm's employees (including, the platform stresses, its US employees), and the other 20% by its founders (TikTok, n.d.). In this light, control of Bytedance is notably more diversified than for the dual-class public firms in our sample.

The same cannot be said for X, which appears to conform closely to the ideal-typical private ownership model since its takeover by Elon Musk. A court document listing all X investors was unsealed through litigation in the Summer of 2023, but it does not state the value or percentage of their share (Silverman, 2023). This list may also be outdated, especially since March 2025 when X was acquired by XAI—a holding company that also owns X's associated Artificial Intelligence ventures (Datta, 2025). The available evidence indicates that Elon Musk maintains a controlling share of xAI Holdings Corp, and thus of X. Notably, although Musk has stepped down as CEO of X, he remains the CEO of xAI Holding Corp.

Bluesky, finally, is not so transparent as its idealistic stylings might suggest. Its website states that it is “owned by Jay Graber and the Bluesky team” (Graber, 2022). A BBC report describes Graber as the “primary owner” (Gerken, 2023), but it is not clear whether this entails a controlling (>50%) share, or, for that matter, who the other owners in the “Bluesky team” are. This level of secrecy is not exceptional among private platform firms, but it is arguably in tension with Bluesky's self-professed dedication to openness and transparency (Table 5).

Ownership of private platform firms.

Discussion

The rise of platforms marks a reversal of trends: whereas media markets have tended toward ever more financialized and corporatized control, platforms and their dual-class stock structures have allowed individual owners to maintain decisive influence at key firms. 4 However, the above data show that individual control differs significantly between firms. Important differences remain between platforms, however, which are summarized in Table 6 below. Some firms have diversified corporate ownership (Apple, Microsoft, Bytedance), whilst others remain concentrated with sole (X, Meta, Reddit), joint (Alphabet) or indeterminate (Bluesky) controllership. Among these, X and Meta are arguably the most clearly oligarchic since the sole controller is at once the firm's executive. Between them, Musk's may be the stronger position since he may also have the majority of economic rights (though this is not fully certain due to a lack of transparency), while Zuckerberg only holds a majority of votes and shares economic ownership more widely. Alphabet's structure is comparably oligarchic, but to a lesser extent, since Larry Page and Sergei Brin share control over the firm and since neither occupies an executive position. Reddit, finally, is an interesting edge case, somewhere between Meta and Alphabet, since its controlling shareholder, the Newhouse family, has conferred its voting rights to the CEO and founder, Steve Huffman. With a controlling share by proxy, Huffman occupies a similar position as does Zuckerberg, with the important caveat that Newhouse might revoke the proxy only if certain contractual conditions are met. In this sense, Huffman's operational control remains dependent on Newhouse's allocative control. The following section considers implications at the level of content governance.

Individual versus market control at public and private platform firms.

Also notable in this dataset is the ubiquitous presence of BlackRock and Vanguard. This is not unique to tech: these firms manage highly diversified portfolios across almost the entire US and global stock market, amounting to over $19 trillion USD in assets under management. Technically, these firms do not own the stock represented here; it is merely managed for the benefit of their clients, who are equally diverse and include pension funds, sovereign wealth funds, retail investors, and high-net worth individuals. With their passive and diversified investment strategy, these firms typically do not monitor closely the firms they hold stock in. This being said, Big Tech currently represents a substantial share of the total US stock market – the largest five tech firms collectively account for 23% of the S&P500 – such that even these diversified funds are heavily invested in tech valuations. State Street, the third of the Big Three investment funds, also holds platform stock, but their share apparently does not reach the 5% threshold for SEC disclosure requirements. The following section considers how these institutional investors might shape content governance.

Platform ownership and the institutional logics of content moderation

Media ownership research predicts that different ownership forms yield different institutional logics, or sets of practices and values that act as organizing principles (Friedland and Alford, 1991). As discussed in Section “Media ownership: moguls, markets and alternatives,” Benson et al. associate market ownership with a commercial logic of profit maximization within the firm, and hence cost-cutting and standardization. Private control, by contrast, empowers a more diverse and erratic set of (oligarchic) personal preferences, including political and economic instrumentalism. In a given organization, multiple contradictory logics may be at play; in news media, there are tensions between market and private logics of ownership as well as the professional logics of journalism, with its ideals of objectivity and independence, which may act as countervailing forces to ownership.

How does ownership affect the institutional logics of platform content governance? The following section reviews available evidence, starting with a discussion of private control and political instrumentalism at X and Meta—the two platforms with the most clearly oligarchic ownership structure. I then discuss market ownership, the role of institutional investors and the extent to which X and Meta truly diverge from market standards in content governance. Finally, I discuss the role of Trust and Safety professionals as a potential countervailing logic to both private and market control.

Private logics: Political instrumentalism and partisanship at oligarchic firms

Compared to media, researching ownership influence at platforms has the methodological advantage that some owners are far more overt in their influence on content. As the following section shows, Elon Musk at X and Mark Zuckerberg at Meta are closely involved in content policies at their respective firms. These are also the two platform firms in our sample with the greatest degree of private control: the sole controller as CEO. Less is known about other privately-controlled firms such as Reddit and Google, since their owners have typically been less overt in their stances on content governance. Overall, it seems that individual owners are not necessarily or structurally involved in shaping content policy—these matters may be also be delegated—but that owners do retain the power to assert influence once it attracts their interest. In the known instances that owners have concerned themselves with content policy, they typically pushed for weaker moderation; collaboration with authoritarian governments; and boosted algorithmic visibility for their own personal accounts.

At X, Musk's influence on content policy was immediate and flagrant. Recent work by João Magalhães, Robert Gorwa and Clara Iglesias Keller (Magalhães et al., 2025) reviews Musk's actions in detail through a database of events before, during and after the acquisition. Notable changes for content policy include allowing suspended users to return to the platform, such as Donald Trump and Holocaust-denying white nationalist Nick Fuentes; withdrawing from the Global Internet Forum to Counter Terrorism (GIFCT); suspending access to academic research APIs; ending partnerships with various NGOs (except those aligned with US conservative moral priorities such as CSAM and synthetic drug content); and removing the user block function—though the latter was later reintroduced, seemingly due to requirements imposed by app stores (Magalhães et al., 2025). Musk also forced through changes in staffing and decision-making structures: large portions of the Trust and Safety staff were either fired or pressured to resign. There are also strong indications that Musk enacted changes to the Twitter recommendation algorithm in order to boost the visibility of his personal profile (Graham and Andrejevic, 2024). Version 4.0 of Twitter's AI feature “Grok” also appeared to search for Musk's opinion to answer politically controversial queries, although the firm denies that it was expressly instructed to do so (Zeff, 2025). For Magalhães et al. (2025), Musk's tenure at X represents an “unprecedented fusion of social media and authoritarianism,” in which “[t]he only consistent principle behind his view of free speech is that content moderation should primarily serve his own interests and beliefs.”

At Meta, it is not the ownership structure that changed in recent years but rather Mark Zuckerberg's personal behavior. According to insiders, he appears to have moved from an initial indifference to content governance, towards relatively close involvement, and now back to a broadly hostile, deregulatory stance. In the memoir Careless People, former Facebook executive Sarah Wynn-Williams (2025) recalls that, in his early years, Zuckerberg was largely disinterested in content governance issues and regulatory politics more broadly, prioritizing commercial and engineering matters instead. Against pressure from staff, Zuckerberg long resisted more proactive moderation policies that would “mov[e] the company closer to the media industry or allo[w] it to assume more media-like functions, such as editing or fact-checking” (Wynn-Williams, 2025: 283).

However, once Zuckerberg began to take an interest in politics during in the early Trump years, he was able to assert control such that, at one point, even individual content governance decisions were escalated to his personal desk; for key moderation actions, Facebook came to act as “an autocracy of one,” with Zuckerberg frequently overruling the firm's own stated content policies, including on controversial issues such as complying with Russian and Chinese censorship and surveillance mandates (Wynn-Williams, 2025). Around 2020, Zuckerberg also appears to have considered running for US president, with close colleagues speculating that he planned to leverage not only his immense wealth but his infrastructural control over public communications (Wynn-Williams, 2025: 284). Notably, to cement his control over social media, Zuckerberg also contemplated purchasing Twitter during this period—several years before Musk ultimately would (Wynn-Williams, 2025: 282). Insiders also believe that, like Musk, Zuckerberg “juiced” his platform's recommender algorithms to grant disproportionate visibility to his personal profile (Wynn-Williams, 2025: 63).

In early 2025, Meta under Zuckerberg became the first major platform to follow Musk's right-wing turn; shortly before Trump's second inauguration, Zuckerberg issued a personal statement announcing that the platform would cease fact-checking, loosen its protections against hate speech, and “work with President Trump to push back on governments around the world,” including the EU and its new platform regulations (Kaplan, 2025). Arguably less radical than Musk, and certainly less flagrantly antagonistic toward his employees and regulators, Zuckerberg nonetheless appears to be following the same blueprint.

What about Sergei Brin and Larry Page, as shared controllers of Alphabet? Unlike Zuckerberg or Musk, they have not been publicly involved in content-related controversies, and this imposes limitations on our analysis. What we do know is that, as board members rather than executives, their influence is limited, at least formally, to high-level strategic decisions. They are not charged with deciding on content policies, let alone individual moderation actions. Whether they have worked behind the scenes to influence content policy or decisions cannot be ruled out, and requires further research. As it stands, the stark disparities in publicity suggest that their influence is more modest than either Zuckerberg's or Musk's, and confined to high-level forms of allocative rather than operational decision-making. These differences might be attributed to in part to personal temperament—Brin and Page may simply not be interested in involving themselves in content governance, or indeed be positively committed to ideals of non-interference. But besides personal temperament, these outcomes are also consistent with our mapping of ownership structures; Page and Brin's shared control, rather than sole control, as well as their non-executive management positions, both place them at greater institutional distance to content governance than their counterparts at Meta and X.

As for Reddit, the unusual proxy-voting arrangement between CEO Steve Huffman and the Newhouse family requires further research. Huffman's views on content governance are somewhat typical amongst platform CEOs in the sense that he oversaw a general expansion of moderation efforts over the past decade, ostensibly in response to broader market and regulatory forces, whilst personally expressing a cyberlibertarian ethics of free speech maximalism and limited government (Guest, 2023). Unlike at Meta, however, there is no evidence of any significant break with past policies during the second Trump presidency. Perhaps more notable is the fact that, since Reddit's IPO in 2024, Huffman's control has come to depend on voting rights delegated to him by the Newhouse family, who also own numerous media outlets such as The New Yorker and Vanity Fair and hold major stakes in Charter Communications and Warner Bros. The recently-deceased patriarch Si Newhouse has been criticized for his interference with independent journalism, though less is known about his recent successors (Maier, 1997).

In sum, there is ample evidence to suggest that private platform ownership exerts ideological pressure on platform content policies, at least for some firms. This makes close study of individual owners—their convictions, their interests and assets, their actions—an important topic of study for our understanding of public communications platforms. A limitation here is that more reclusive owners, such as Brin, Page, and the Newhouse family, may prove difficult to study, although sustained investigation may still bear fruit (e.g. Maier, 1997). Where direct involvement cannot be observed, such research can also be complemented by comparative analysis of content-level outcomes. If individual owners do involve themselves in content governance, this begs the question whether they produce different results than market-owned firms—and to what extent either ownership form is truly able to control content governance professionals.

Private versus market logics: Content governance as private power or commercial calculus

Media research predicts that firms controlled by institutional investors are likely to have a relatively strict focus on profit maximization, with less regard for ulterior ideological or political considerations. This “market logic” aligns with typical accounts of platform content governance as a commercial enterprise (Gillespie, 2019; Roberts, 2019). As discussed in Section “Platform content governance,” there is extensive research on the different commercial pressures shaping platform content policy, including the need for user growth and retention; advertiser preferences and “brand safety”; cost-cutting, automation, outsourcing and scalability; and regulatory, political and reputational risk management. This begs the question: are individually-controlled firms any different? Do moguls moderate differently than markets?

Answering this question is challenging because the commercial logics of content moderation are deeply political and contingent. Like media, platforms act under conditions of deep uncertainty, rapid change, and structural inequality between competing interests. As such, singling out certain firms as departing from market logics requires some caution; there is after all very little consensus on what “ordinary” commercial moderation looks like. The following section discusses whether Musk and Zuckerberg are truly departing from industry standards out of ideological conviction, or instead may represent the most visible outcropping of broader market shifts.

For Musk, the case for political instrumentalism is relatively strong: he undertook his crusade long before his current ally Trump regained power, and persevered despite commercial headwinds. As a private company the financial details are opaque, but industry reporters conclude that the takeover has been a commercial disaster, with advertisers and users alike abandoning the platform en masse (Magalhães et al., 2025). Musk himself has said as much; in a textbook expression of political instrumentalism, he claimed that the takeover was “not a way to make money,” but to create an “inclusive arena for free speech” (Klar, 2022).

And yet, there is a risk in taking these high-minded claims at face value. Around the same time as the X acquisition, mass layoffs affecting Trust and Safety staff took place at most major platform firms. According to industry commentators, these layoffs were primarily driven by rising interest rates and tightening money markets in an inflationary post-Covid economy (Allyn, 2024). What Musk presents as a selfless act of moral conviction could also be seen as standard business strategy for a market in transition, adapting to the end of the long 2010s and the drying up of its endless pools of cheap credit (see also Jia et al., 2023).

Another reason to doubt Musk's bona fides are his other properties: with a combined valuation of over 1.2 trillion, SpaceX and Tesla are together worth at least 30 times as much as X. As several commentators have noted, SpaceX and Tesla are heavily dependent on US subsidies (Lalljee, n.d.). In political-economic terms, Musk's significant stakes in non-media interests can also encourage economic instrumentalism as a mode of power (Benson et al., 2025), in which the owner leverages their control over public discourse to boost their broader investment portfolio. In legacy media, owners might attempt to secure positive coverage for their other ventures, or forge alliances with governments and politicians. As a form of economic instrumentalism, Musk's management of X can be understood as a political-regulatory quid pro quo where he advances the interests and ideologies of the US Republican Party in exchange for secured access to subsidies. Of course, political and economic instrumentalism are not mutually exclusive; Musk's motives may be both political and economic. Crucially, for individually-controlled firms, the point here is that the economic interests of the owner are not the same as those of the firm; whereas the market logic might focus on commercial profit maximization within the firm, the economic instrumentalist logic may sacrifice firm-level profits in favor of the oligarch's cross-ownership of other non-media investments.

In the case of Zuckerberg, the question has already been raised whether his recent “vibe shift” is indeed genuine or rather an opportunistic pandering to current political and cultural sentiments. Those who doubt his conviction point to his previous track record of flip-flopping on content governance issues, whilst others suspect that Zuckerberg has always been a moderation-sceptic cyberlibertarian at heart (Murphy, 2025). Unlike Musk, Zuckerberg only announced his new policies after Trump won re-election, and his outward railing against EU regulation coincided with the US unleashing a global tariff war and more generally taking a more hostile and protectionist stance toward the EU. Notably, Zuckerberg's announcement conflates free speech and content governance with broader regulatory concerns about the EU making it “hard to build anything innovative.” To the Trump administration, this signals not just a push against censorship but against foreign regulation more broadly – including issues that more directly threaten Meta's core business model, such as data protection and antitrust. Wall Street appears to have rewarded Meta for their new course: their stock dipped slightly after first announcing layoffs, but then skyrocketed over 18% by the end of January.

As the alternative to oligarchic private control, further research is also needed to understand the role of financialization and institutional investors in shaping content governance. The analogy to media predicts that, through their insistence on cost-cutting and short-term profit maximization, the main effect of financial institutions on platform governance is to slash budgets and push automation. We have seen that BlackRock, Vanguard and other large investment funds hold stakes in practically all public tech firms, and often the largest stake in diversified firms. As discussed, these passive investors tend not to actively involve themselves in management. Nonetheless, closer study of their voting behavior during shareholder meetings, as well analysis of other Wall Street institutions such as analyst firms, might reveal effects on content policy. Evgeny Morozov notes that financial analysts almost caused Apple to oust their CEO Tim Cook by criticizing his failure to invest in AI (Morozov, 2025). This article has shown that Apple's ownership structure makes it relatively susceptible to such market pressures, compared to owner-controlled firms like Meta or Twitter where the owner-CEO may have more leeway to steer their own course. Another significant development is BlackRock and Vanguard's erstwhile embrace of, and recent retreat from, Environmental, Social and Governance (ESG) frameworks. ESG principles score firms on various metrics, including human rights. After gaining significant momentum in the 2010s and 2020s, with BlackRock CEO Larry Fink as an outspoken advocate, investment firms gradually abandoned ESG in 2025 as Trump's Republican Party railed against “woke capital” (Iacurci, 2025). In the same period, many listed firms have quietly dropped social justice commitments on issues such as staff diversity (Cifrino, 2025). Similar effects in content policy, for instance in the treatment of hate speech, are plausible and worth investigating further. Finally, at non-listed firms, the role of private equity is another area for future research. Consider, for instance, the Susquehanna Group's board position at TikTok and their billionaire director and Republican megadonor Jef Yass’ allegedly important role in brokering a deal with Donald Trump to suspend the enforcement of the US Tiktok ban (Kim and Ibssa, 2024). Platforms and their content governance thus operates in a field of increasingly politicized struggle between various financial actors and institutions, including Silicon Valley's tech moguls but also (broadly Democrat-aligned) banks and investment funds and (broadly Republican-aligned) private equity groups (Merchant, 2025).

In sum, the recent changes at X and Meta are not a simple story of moguls versus markets; there are important agreements, as well as contradictions, between market forces and the owner's political programs. Whilst market-owned firms like Alphabet and Microsoft have not made the same spectacular announcements about new content philosophies, several have shifted incrementally to the right on issues like fact-checking (Datta, 2025) and hate speech enforcement (Grant and Francisco, 2025) in 2025. Ultimately, it remains an empirical question to what extent privately-controlled platforms are diverging from market-owned rivals.

Consequently, there is an urgent need for more sustained comparative analysis between these firms to understand how tech oligarchs shapes platform governance. To this end, it will be important to separate out owners’ public performances from platforms’ underlying practice; there can be major disconnects between platforms’ stated policies and their actual implementation and enforcement. For instance, it is not yet clear to what extent Meta actually enforced the hate speech policies which it has now loudly abolished—nor, for that matter, how other firms handle similar content. A more sustained comparative analysis of moderation performance, at the level of both policy and of practice, is essential to understand whether we are at the start of a great divergence or, instead, a quiet realignment.

Professional logics: “Trust and Safety” as countervailing force?

In Benson et al.'s (2025) framework for media ownership, the professional norms of journalism impose their own institutional logic that can act as “countervailing force” against ownership (whether market or private). Media sociology points to particular management structures and organizational safeguards—such as “firewalls” between editorial and business units—as well as professional norms and workplace cultures, which can socialize professionals toward greater or lesser autonomy from commercial considerations (Cornia et al., 2020). Despite these protections, owners may still influence newsrooms through allocative control over resources and executive appointments (Murdock, 1982). Thus, while journalists are never fully autonomous from ownership, their relationships may still vary significantly between firms. The same question can be asked of platforms: to what extent are owners able to control the actions of workers tasked with content-level decision-making?

Unlike media, most platforms do not maintain even the pretense of independence from ownership. Platform owners like Zuckerberg and Musk assert more direct and overt operational involvement in content-related decisions. Still, their operational control may yet be constrained by other technical and organizational factors.

At a technical level, ownership influence may be limited by the fact that platforms operate with extreme scale and technological complexity; for owners trying to influence content policies, this can create monitoring costs and agency problems. Hence, platform's highly automated enforcement structures, may still leave a degree of autonomy for Trust and Safety workers: the policy experts, engineers, and product managers tasked with designing and implementing policies in detail and at scale. Existing research on moderation labor and management has been chiefly concerned with the fate of front-level workers and issues of their safety and well-being (Roberts, 2019). Whilst significant from a social justice perspective, the status of these frontline workers is less central to questions of media power precisely because their work is highly standardized and, as a consequence, exercises almost no meaningful agency over content-level outcomes (Ahmad and Greb, 2022; Winseck, 2020). Moderation work, for Sana Ahmad, is “outsourced but directly controlled” by lead firms to limit worker discretion and reduce indeterminacy, leaving key decisions in the hands of platform managers and technologists (Ahmad, 2023).

Ownership control over Trust and Safety management can be further constrained by internal managerial structures, which differ significantly between platforms. There has been little sustained research into Trust and Safety management structures, but researchers familiar with industry practice have observed how content policy work is sometimes housed in public policy and government relations units (Roth, 2023), legal compliance (Keller, 2024) or advertising and product teams (Gillespie, 2022). Each of these might suggest a different orientation toward commercial and political pressures, including those from ownership. These arrangements are also dynamic; as discussed in Section “Professional logics: “Trust and Safety” as countervailing force?,” Musk and Zuck both reconfigured moderation workflows at their firms to assert greater day-to-day control over content policy decisions. Relatedly, another potential constraint on ownership influence is the outsourcing of content policy decisions to NGOs, trusted flaggers and other hybrid or networked governance actors (Caplan, 2023; Douek, 2020.). However—as illustrated by Zuckerberg's nixing of fact-checking partnerships, and Musk's withdrawal from GIFCT—powerful owners may still retain allocative control to decide when to enter or exit such partnerships. Given this heterogeneous landscape, further research is need to understand how Trust and Safety management structures across different platforms render them more or less susceptible to pressures from ownership, as well as other political-economic forces such as advertisers and governments.

Private ownership can also clash with workplace cultures and professional norms. Industry reports claim that many platform workers are dissatisfied with the new course at Meta and X (Kolodny, 2025). Musk and Zuckerberg are foisting their agendas on a professional class that is broadly at odds with, if not overtly hostile to, their new radical right-wing experiments (Magalhães et al., 2025). Resistance might be individual or collective, channeled through new professional and labor organizations. Over the past decade or so, content governance has given rise to an increasingly tightly-networked professional field of Trust and Safety work, which is starting to organize itself professionally through associations, conferences, trade journals, and independent consultancies (Hendrix, 2022; Weigl and Bodó, 2025). Tech workers at various firms have also unionized or otherwise engaged in labor activism (Logan, 2023). Over time, these professional and labor institutions could conceivably become a locus of governance and a stabilizing force against ownership influence, much as they do for journalism.

Conclusion

For social media as much as for legacy media, we can follow Michael Schudson (2005) in concluding: “Ownership is important. Ownership is not everything.” But whereas media studies have been occupied with ownership influence since their earliest beginnings, social media research lacks this foundation. Now the issue of ownership is more pressing than ever, as the problem of tech oligarchy deepens and powerful owners begin to instrumentalize content policies to their own ends. In this context, a program of platform ownership research can help us to refine our understanding of platforms’ “commercial” interests, not reducible to mere profit maximization but the contested outcome of contradictory political and economic forces within the platform firm, including powerful individual shareholders.

This article has shown that not all platforms firms are equally subject to individual oligarchic control. There are meaningful differences in incorporation status, ownership concentration, and relationships to management. Compared to media, dual-class structures at platform firms have made individual control more prevalent even amongst massive publicly-listed corporations, reversing the general trend in public communications toward market control and institutional ownership and setting the stage for a new generation of platform oligarchs. There is further descriptive work to be done in mapping ownership of other important platforms not included in this study, such as the large Chinese and Russian platforms as well as small-but-politically-significant alternative platforms like Gab and 4Chan. A complete account of contemporary media moguls would also consider interrelations between the old and the new, such as tech oligarch Jeff Bezos’ acquisition of the Washington Post and the Newhouse media mogul family's acquisition of Reddit.

This article has also examined how oligarchs influence content moderation at the firms they control. Until now, their interventions have typically steered toward cutting Trust and Safety budgets; deal-making with authoritarian governments; and self-preferencing their personal profiles and viewpoints. Recent trends suggest that we may be at the start of a great divergence between market and private ownership, with Musk and Zuckerberg conducting a radical break from default market logics. However, rather than take their high-minded proclamations at face value, what is needed is more sustained comparative analysis to compare market and private firms. In our critique of moguls, there is a risk of normalizing market control as its implied alternative. Here, too, media scholarship can inform a balanced consideration of the effects of stock markets, institutional investment, and financialization on communications industries—and point to alternative models, such as non-profit, worker, and public ownership (Sanders and van Dijck, 2025), which remain largely untested in platform governance.

Finally, this article also identifies Trust and Safety professionals as a potential countervailing force to ownership influence (whether market or private). As a rule, this countervailing force is likely to be weaker than in media, since platforms lack established structures or norms for professional autonomy. But a degree of agency remains plausible at least for some firms, given the heterogeneity of platform management practices, the complexity of their technical infrastructures, and the hostility that Trust and Safety workers have already shown toward recent interferences by Musk and Zuckerberg. As Trust and Safety matures into a fully-fledged professional field with its own networks and institutions, it may prove to be an important site of resistance to ownership influence—though it may also be brought to heel by the merciless budget cuts now being enacted at private and market firms alike. Again, this remains an empirical question in need of sustained comparative research.

Ownership influence also has policy implications. A first demand might be greater ownership transparency, especially at private firms. Who owns and controls firms like X, Bluesky, and TikTok? For legacy media, heightened ownership transparency requirements already exist in many jurisdictions, given this industry's unique importance to democracy (Borges and Christophorou, 2024). Second, managerial safeguards for editorial independence, such as professional codes and organizational “firewalls,” might also provide a blueprint for platform Trust and Safety teams. Third, media's varied landscape of alternative ownership models—public, non-profit, cooperative—can help us imagine a future for the digital public sphere beyond moguls and markets alike

Footnotes

Acknowledgments

The author is grateful to Agustin Ferrari Braun, Rachel Griffin, Charis Papaevangelou, Daphne Keller, David Nieborg, Brenda Dvoskin, Petros Terzis, Julie Cohen, Dwayne Winseck, and Joris van Hoboken for their thoughtful comments on earlier drafts. Special thanks go to Rob Gorwa at WZB, Clara Iglesias Keller at the Weizenbaum Institute, and Rubén García Higuera at CEPC for helping to workshop this article at their respective institutions, and to the organisers and participants of the Bremen AoIR Flashpoint Symposium. Errors remain the author’s own.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Digital Transformation of Decision-Making (DTDM) research initiative of the University of Amsterdam Faculty of Law.

Declaration of conflicting interest

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.