Abstract

Quantum games, like quantum algorithms, exploit quantum entanglement to establish strong correlations between strategic player actions. This paper introduces quantum game-theoretic models applied to trading and demonstrates their implementation on an ion-trap quantum computer. The results showcase a quantum advantage, previously known only theoretically, realized as higher-paying market Nash equilibria. This advantage could help uncover alpha in trading strategies, defined as excess returns compared to established benchmarks. These findings suggest that quantum computing could significantly influence the development of financial strategies.

Keywords

1. Introduction

The nature of trading has consistently been shaped by advancements in information delivery and technology. From the introduction of the telegraph in the 1850s to the development of the stock ticker by Edward Calahan in 1867, real-time reporting of stock prices and market news revolutionized the trading landscape. These innovations allowed brokers and traders to access information more rapidly than ever before, fostering a more dynamic and competitive market environment.

The digital era brought a paradigm shift with the advent of online trading platforms. The launch of digiTRADE in 1994 and Ameritrade’s pioneering online brokerage services enabled traders to place orders instantaneously with minimal or even no commissions. The internet introduced unprecedented speed and accessibility while offering tools like data integration, dashboards, and business intelligence for more informed decision-making. This transition to electronic trading also marked the decline of traditional floor traders and brokers, as algorithmic trading took center stage. Automated systems capable of analyzing market conditions and executing trades underscored the growing reliance on technology in the trading ecosystem.

Building on these developments, a key question involves the potential advantages of a quantum computing-based “quantum trading” platform. Current advancements in quantum computing suggest increased speed and efficiency in data processing (Dong et al., 2024; Herman et al., 2023); however, it is the proven ability of quantum computers to deliver higher-quality solutions to competitive interaction problems that offers unique value to traders (Hanauske et al., 2010; Khan et al., 2021). This can be particularly relevant for mission-critical markets such as carbon trading and other green markets. This paper examines game-theoretic trading models using the games Chicken and Prisoner’s Dilemma as prominent examples to implement on a quantum trading platform.

2. Core Trading Strategies: Long and Short

Trading fundamentally revolves around the actions of buying and selling. When directed toward achieving specific objectives, these actions evolve into strategies designed to meet those goals. In this strategic context, buying is termed “going long,” and selling is referred to as “going short.” However, these terms are not merely catchy labels; their meaning and execution vary depending on the market in which the trading takes place.

For instance, in futures trading, going long entails purchasing a futures contract with the expectation that the price of the underlying asset—such as a commodity, stock index, or cryptocurrency—will rise. Conversely, going short involves selling a futures contract with the anticipation that the price of the underlying asset will fall.

In contrast, within the equity market, the focus of this discussion, going short involves borrowing shares of a company from a broker and selling them at the current market price, expecting a subsequent price drop due to increased supply. If the price falls as predicted, the trader repurchases the shares at the lower price, returns them to the broker (along with any applicable fees), and retains the difference as profit. Here, going long signifies buying first and selling later, while going short reverses the order: selling first and buying later. While short trading can aid in price discovery, its excessive use may contribute to financial crises like the one that occurred in 2008 (Cruttenden, n.d).

Regardless of the specific market, these trading actions hold strategic significance only when driven by an underlying “game” or competitive dynamic. Depending on the nature of this game, the outcomes of these strategies can vary significantly. For example, consider a simple scenario in the equity market where two traders—perhaps large fund managers—engage in a game of “Chicken,” facing off with payoffs that include not just monetary gains or losses but also intangible stakes like bragging rights or reputation. Let us formalize both the game Chicken and its manifestation in trading.

2.1. Trading as Chicken

The classic narrative of the game Chicken involves two drivers speeding toward each other on a narrow road. At some point, they must decide how to navigate the impending encounter. The road is so narrow that both cannot pass simultaneously at full speed; at least one driver must slow down to avoid a collision. In this scenario, each driver faces two strategies: either to “go slow” or to “speed up.” The former represents a cautious, safety-first approach, but comes with the social cost of appearing to yield, or losing face. The latter strategy embodies taking a bold risk, with the potential reward of earning bragging rights if the other driver backs down. To emphasize the physics, and ultimately quantum physics, underlying game theory, the players will signal their strategic choice using coins: heads (H) for going slow and tails (T) for speeding up.

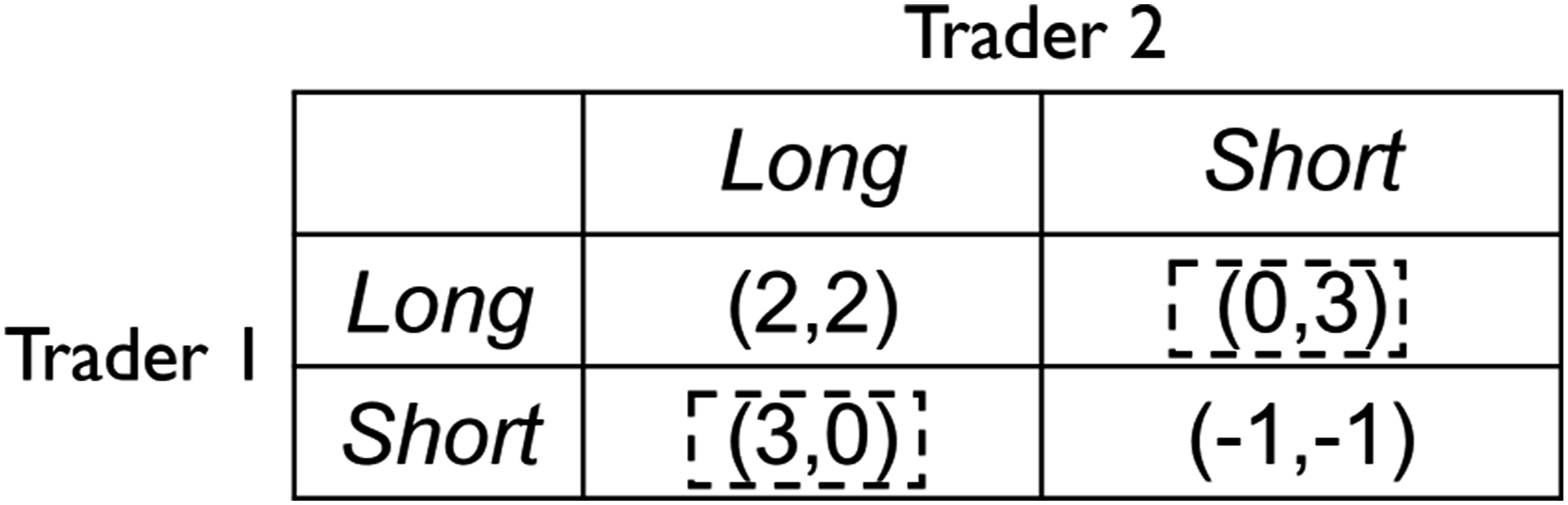

In the context of trading, these strategies can be reframed: going slow corresponds to going long, while speeding up aligns with going short. To clarify the dynamics of this interaction, we can assign specific payoffs to the players based on the strategies they choose, creating a payoff matrix that reflects the outcomes of the game. The matrix shown in Figure 1, as taken from (Binmore, 2007), represents the strategic options in this scenario, Long or Short, and the resulting payoff to the players. The first number in a tuple is the payoff to the row player (Trader 1) and the second number is the payoff to the column player (Trader 2). Trading as the game Chicken with payoff determined by the strategies Long versus Short. The dashed outcomes, along with their corresponding strategy pairs, represent Nash equilibria.

A fundamental assumption in game theory is that all players are rational, meaning they consistently act to maximize only their individual payoffs. Consequently, a key solution concept in understanding competitive interactions is the Nash equilibrium: a collection of strategies—one for each player—where each strategy is a best response to all others. Put differently, it is an outcome where no player would benefit from changing their strategy unilaterally. In the game Chicken, there are two Nash equilibria, (Long, Short) and (Short, Long). Additionally, there exists a “mixed” strategy Nash equilibrium, which arises when players randomize between their original “pure” strategies. This randomization can be affected by the players tossing their coins and deciding to play the strategy corresponding to the resulting face. For mixed strategy equilibrium to exist, the probabilities determined by the coin toss should make the other player indifferent about which strategy to choose as a best response. In Chicken, the mixed strategy Nash equilibrium is achieved when both players choose Long 50% of the time and Short 50% of the time. This results in an expected payoff of 1 for each player. Although this payoff is lower than the pure strategy payoff of 3, the advantage of the mixed strategy Nash equilibrium is that it ensures no player receives a payoff of 0, offering a measure of risk mitigation in the game.

2.2. Trading as Prisoner’s Dilemma

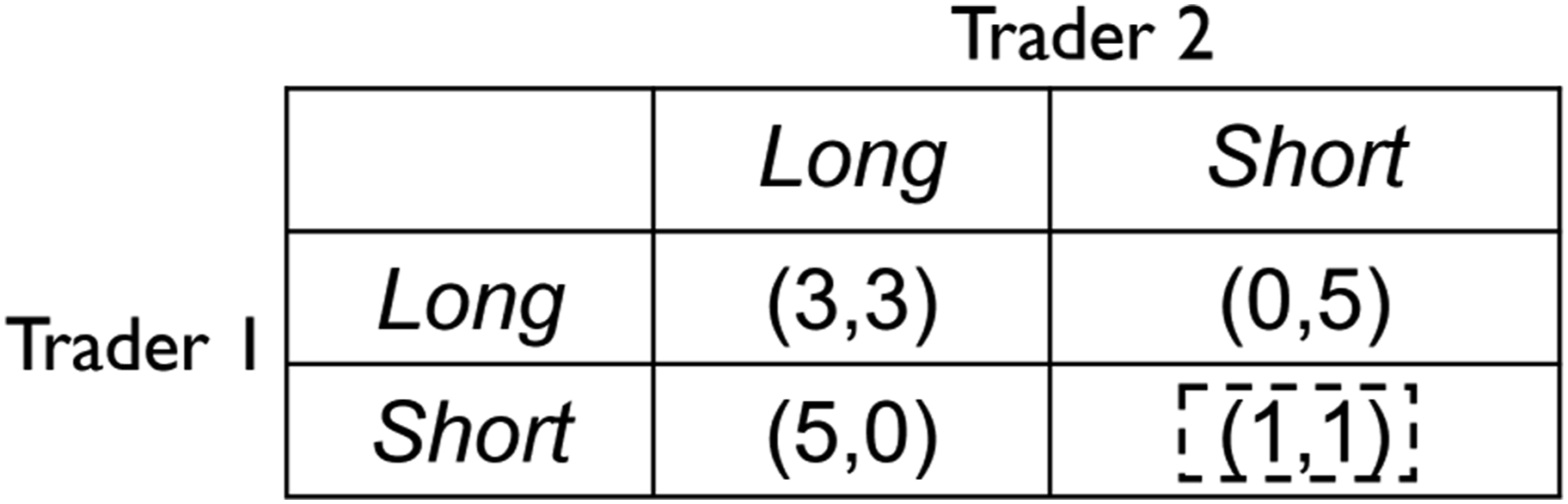

Prisoner’s Dilemma illustrates how individually rational strategies can lead to outcomes that are suboptimal for the group. This scenario is reflected in a trading context, as shown in Figure 2 (also sourced from (Binmore, 2007)), where the strategy of Short consistently offers a higher expected payoff for each trader: 5 or 1, compared to 3 or 0 when playing Long. Trading as the game Prisoner’s Dilemma with payoffs determined by the strategies Long versus Short. The unique Nash equilibrium is at the dashed outcome (1,1) corresponding to the strategy pair (Short, Short).

Imagine a two-trader market snapshot, where both traders are seeking to profit from equity market investments. If both choose to go long, the market remains relatively stable, and each trader can expect a steady profit of 3. However, the temptation to go short is strong: if one trader shorts while the other goes long, the shorting trader can secure a substantial profit of 5, while the long trader makes no profit.

Shorting, however, comes with significant risk. If both traders decide to play Short, their profits are limited to 1 each due to the heightened risk of a short squeeze—a situation where rising market prices force short sellers to cover their positions, driving prices even higher. However, when these rational choices are played out, the resulting Nash equilibrium is exactly (Short, Short) where each trader only gets a payoff of 1.

3. Refereed Trading

In his Nobel Prize winning work (Aumann, 1974), Aumann showed how it is possible to enhance the quality of Nash equilibria by introducing correlation into the players’ strategic actions. For example, in the game of Chicken, traders may correlate their actions by connecting their coins with a flexible wire or cable, creating a system we call a referee. This referee establishes a publicly known probability distribution over the four possible outcomes of the game, determined by the properties of the coins and the connecting wire. After tossing their individual coins, each player observes his own outcome. However, because of the wire connection, these outcomes are no longer independent and the player also has to take into account the correlation between the coin tosses. This is done by assessing the probabilities with which his opponent will play her strategies, conditional on the result of his coin toss.

This process can be conceptualized as the referee providing advice to each player on what strategy to play (the individual coin toss outcome). The players then decide whether to follow this advice by predicting what advice was given to their opponent. This prediction process involves computing conditional probabilities, where the conditioning event is a player’s own coin toss outcome, and evaluating the expected payoffs of agreeing or disagreeing with the referee’s suggestion. When both players always follow the referee’s advice, the resulting outcome is referred to as a correlated equilibrium.

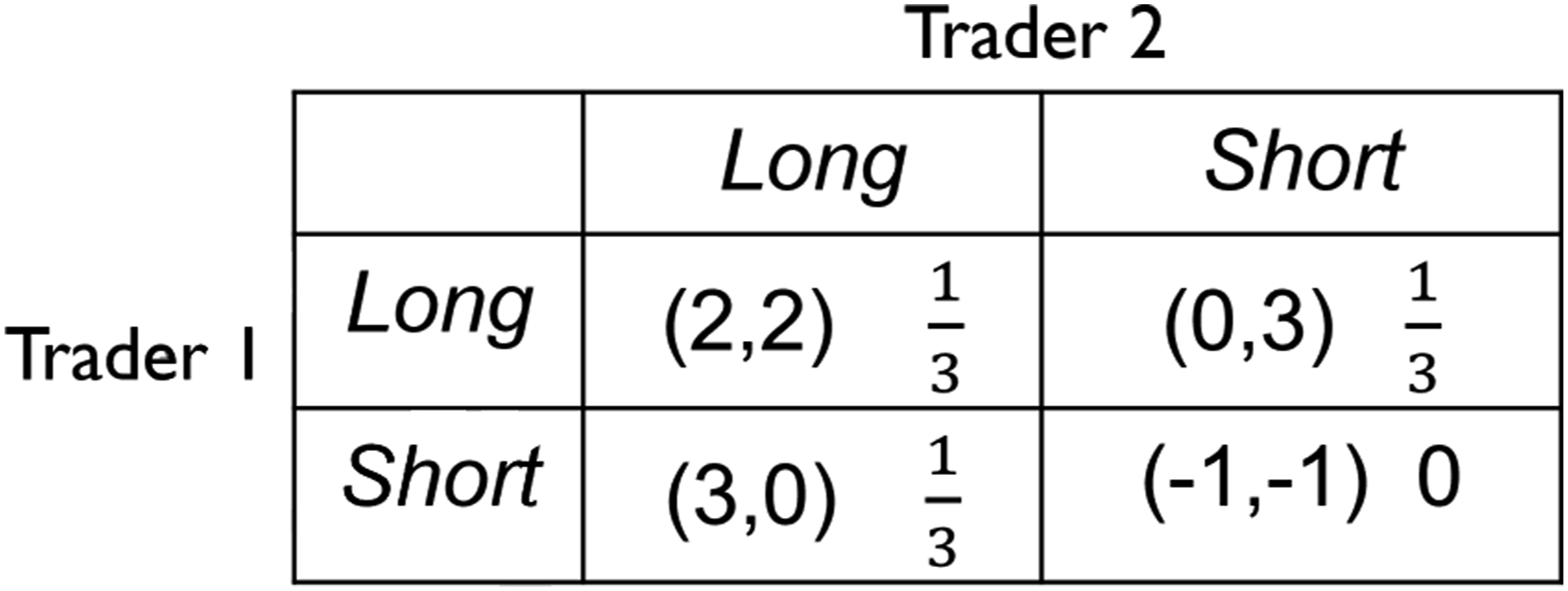

In the game of Chicken, for example, if the referee is characterized by the probability distribution (1/3, 1/3, 1/3, 0) over the game’s outcomes as given in Figure 3, both players will always agree with the referee’s advice and earn an expected payoff of 5/3 each, an improvement over the mixed strategy Nash equilibrium. To understand how this improvement arises, consider the case where Trader 2 tosses her coin and receives advice to play Long. Let this event be denoted as B. To decide whether to follow the advice or deviate from it, Trader 2 evaluates the following scenarios: • A1: Trader 1 is advised by the referee to play Long. • A2: Trader 1 is advised by the referee to play Short. Trading as the game Chicken with a referee characterized by the probability distribution

The conditional probabilities of these events, given B, are calculated as:

The expected payoff to Trader 2 from agreeing with the referee is therefore 2 ⋅ 1/2 + 0 ⋅ 1/2 = 1, and disagreeing gives her the payoff 3 ⋅ 1/2 + (−1) ⋅ 1/2 = 1. Since the payoffs are the same, Trader 2 is indifferent between the two options and hence agrees with the referee’s advice and plays Long. Her overall expected payoff in the game is 2 ⋅ 1/3 + 0 ⋅ 1/3 + 3 ⋅ 1/3 + (−1) ⋅ 0 = 5/3. Similar reasoning shows that both players will comply with the referee’s advice if it is to play any strategy that is consistent with the probability distribution (1/3, 1/3, 1/3, 0). Consequently, this distribution constitutes a correlated equilibrium in the game of Chicken.

On the other hand, unlike Chicken, the Prisoner’s Dilemma has the notable characteristic that the strategy Short strongly dominates Long. Hence, neither mixed strategies nor the introduction of a referee to correlate players’ actions can lead to an improved Nash equilibrium. Regardless of the probability distribution over the game’s outcome that characterizes the referee, both players will always deviate from the referee’s advice to play Long. This rigid structure of the game’s outcomes is part of what makes it both compelling and widely discussed.

The Prisoner’s Dilemma is also a good case to illustrate how quantum computing can reshape strategic interactions. By employing quantum physical principles such as superposition and entanglement, quantum computers can bypass the dilemma’s limitations, offering superior Nash equilibria that are otherwise unattainable. More dramatically, if quantum computing is available to only one player, it can create a clear advantage by enabling the quantum trader to achieve outcomes beyond the reach of their classical counterpart.

4. Quantum-Refereed Trading

Mathematically, incorporating randomization and correlation through mixed strategies and a referee serves to extend the domain and range of the underlying game function. This process can also be applied in the quantum realm, enabling the inclusion of higher-order randomization and correlation. For a detailed exploration of this mathematical framework, refer to (Bleiler, 2008).

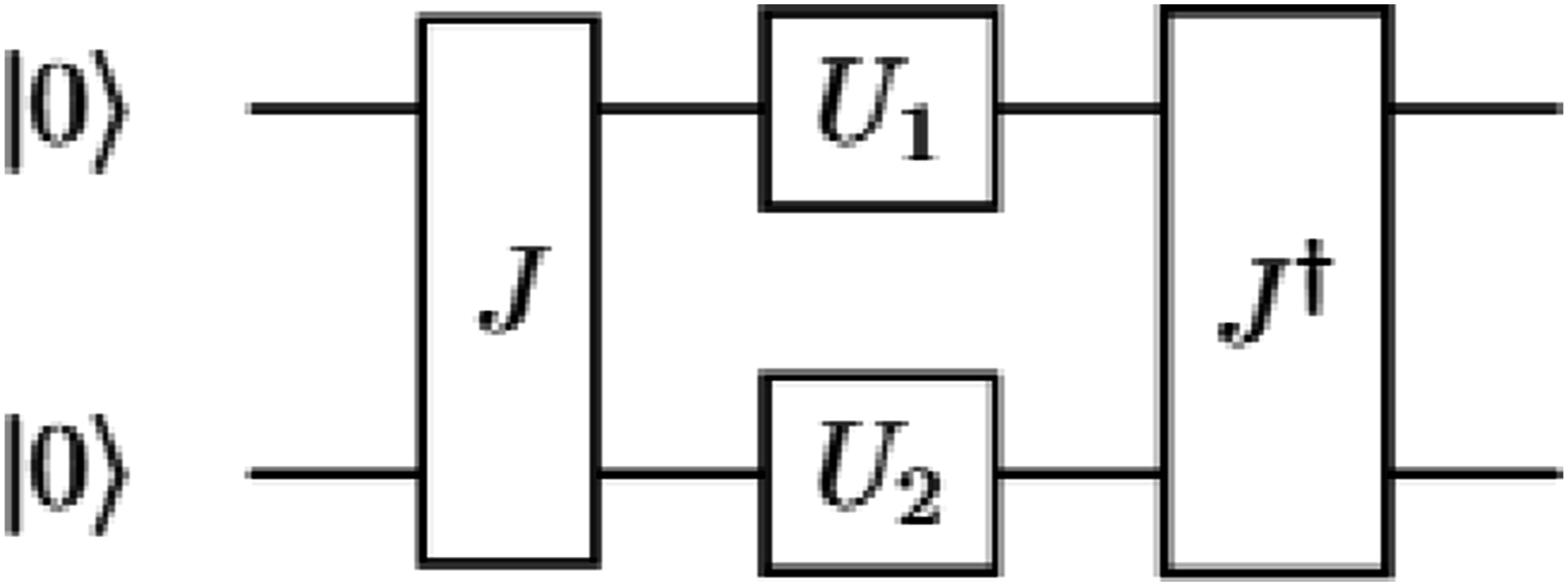

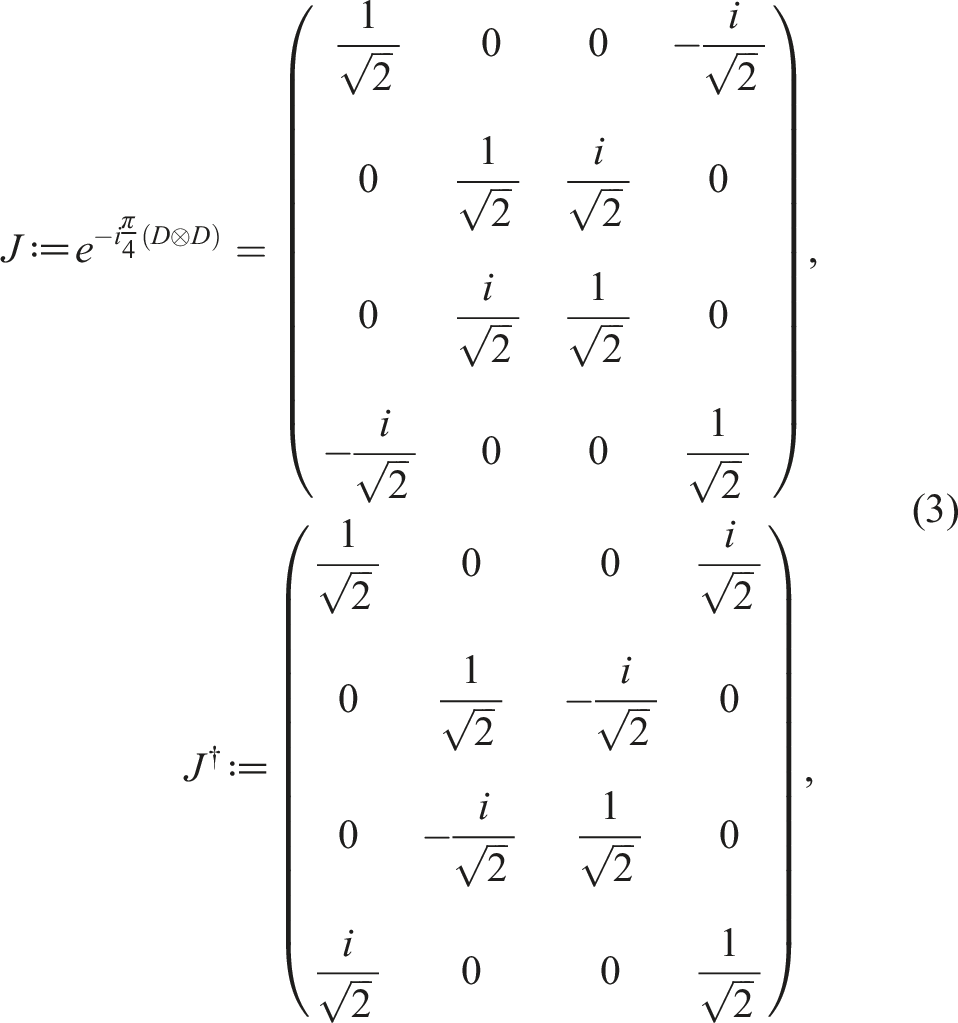

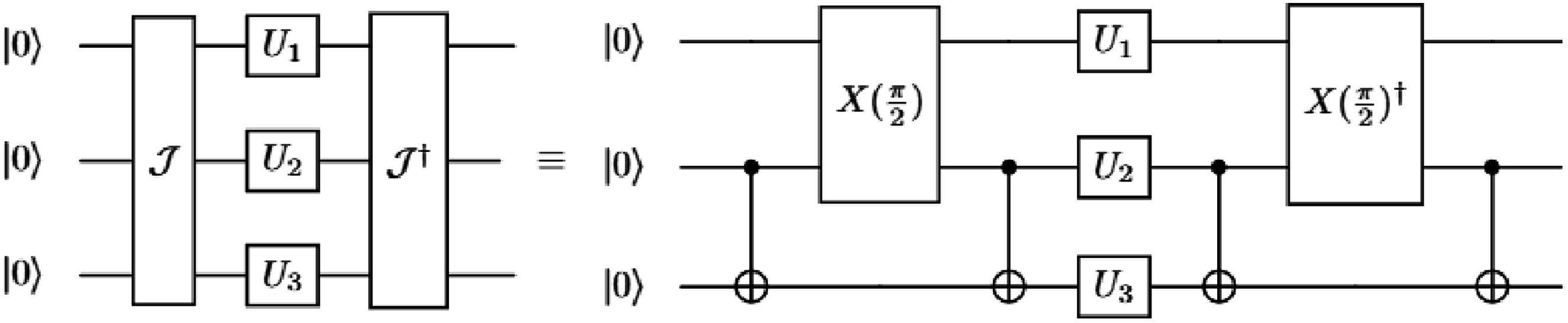

Eisert, Wilkens, and Lewenstein (Eisert et al., 1999), henceforth referred to as EWL, introduced an extension of game theory in the form of a quantum circuit for two-player, two-strategy games. This EWL protocol is illustrated in Figure 4. In this framework, players’ coins are replaced with qubits, and correlations between classical coins are extended to maximal entanglement between qubits. Instead of probability distribution over game outcomes, the quantum referee is characterized by a quantum superposition of outcomes. The EWL game quantization protocol for two-player, two-strategy games. The gate J puts the two qubits |00⟩ into the maximally entangled state

A key component of this protocol is the gate J, which generates entanglement between qubits in the following form:

This entanglement is reversed by J†, the inverse of J. Mathematically, J is a unitary matrix, meaning that applying the conjugate transpose operation, denoted by the symbol †, produces its inverses, J†. The use of J and J† ensures that the quantum model can reproduce the original game dynamics, accommodating both pure and mixed strategies. In the quantum setting, players implement their strategies by performing quantum operations—represented as gates U1 and U2—on their qubits. These operations are referred to as quantum strategies. The initial state of each qubit is |0⟩, analogous to the heads (H) state of a coin, indicating the strategic choice Long, while |1⟩ corresponds to tails (T), indicating the strategic choice Short.

The details of operation of the EWL quantum referee are as follows. The entangling and disentangling gates are, respectively,

The symbol ⊗ represents the tensor product of matrices. It is worthwhile to note here that the matrix representation of Short is in fact the ubiquitous Pauli-Y matrix multiplied with the complex number i:

For more details on quantum gates and their unitary matrix representations and operations, see (Nielsen & Chuang, 2000).

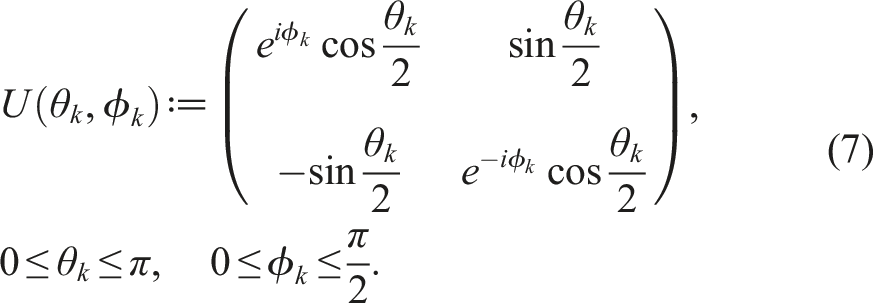

The pure strategy Long is represented as

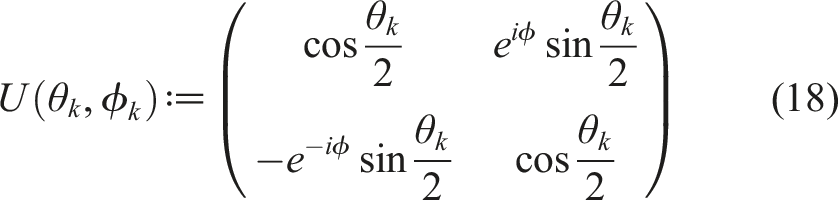

In general, quantum strategies for player k, k = 1, 2, are defined as unitary matrices

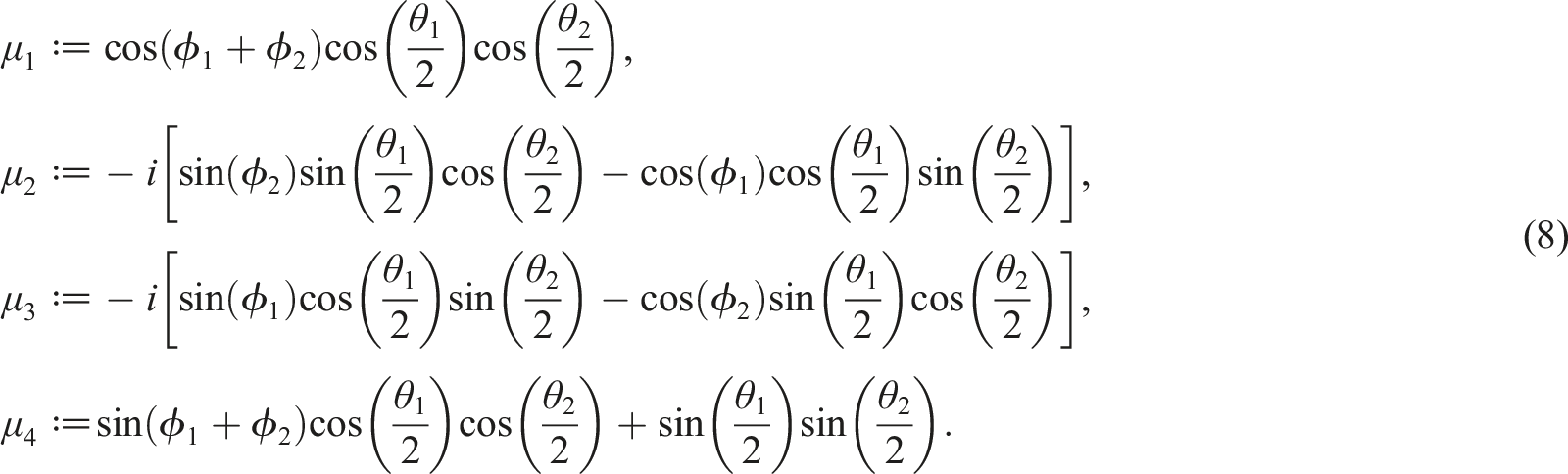

Note that Long occurs when θ = ϕ = 0, while Short occurs when θ = π and ϕ = 0. The EWL quantum referee is then characterized by the quantum superposition (μ1, μ2, μ3, μ4) of the outcomes

The quantum superposition (8) is analogous to the probability distribution that characterizes a classical referee. Indeed, when measured, it gives a probability distribution over the outcomes of the game. Similarly, the quantum strategies can be viewed as the players’ actions of “tossing” their respective qubits within a maximally entangled two-qubit system. These tosses place the qubits into a quantum superposition of |0⟩ and |1⟩, representing the quantum referee’s advice, with which the players may agree or disagree. If both players agree, then the result is a quantum correlated equilibrium, a further refinement of Nash equilibrium.

4.1. Quantum Strategies and Alpha

For the Prisoner’s Dilemma, when the quantum referee advises both players to employ the quantum strategy

In Chicken, the same dynamics give both traders a payoff of 2. More specifically, if one trader plays the conventionally dominant strategy Short against quantum Long, his payoff is 0. This demonstrates the advantage of quantum refereed trading: a trader unaware that the trading environment has shifted to quantum computation will consistently receive a payoff of 0 against the quantum trader who will generate alpha due to his superior strategy.

The correlations that characterize the EWL quantum referee differ fundamentally from those achievable in conventional settings. To illustrate this, consider when Trader 1 is advised by the quantum referee to go long. Assuming a conventional mindset though, Trader 1 deviates from this advice by flipping over his qubit to indicate that he is going short. To his surprise, the qubit remains in the state |0⟩. Even more surprising is that his action flips the qubit of Trader 2, leaving it in the state |1⟩. This is impossible when trades are made under the advice of a conventional, honest referee characterized by coins, especially if the coins were located a great distance apart (Clauser et al., 1969).

The two-player EWL quantum referee has been experimentally implemented, as demonstrated by Solmeyer (Solmeyer et al., 2018). Additionally, alternative quantum referee models have been investigated, including the one introduced by Chappell (Chappell et al., 2012), which was explored within the framework of the Einstein-Podolsky-Rosen (EPR) experiment.

4.2. Mixed Quantum Strategies and Alpha

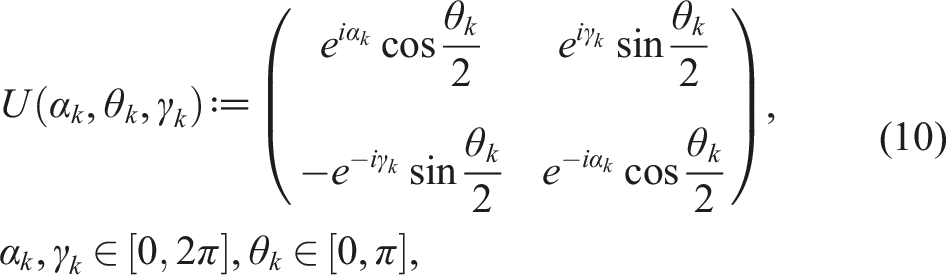

When the set of quantum strategies is expanded to include a full class of gates parametrized by three real parameters, for example,

However, an additional advantage emerges when the players employ their quantum strategies probabilistically, using mixed quantum strategies. In this approach, a player tosses her qubit one way a certain percentage of the time and a different way the remaining percentage of the time. This results in two distinct quantum superpositions of |0⟩ and |1⟩, which can be interpreted as the quantum referee providing probabilistic advice to the players.

For instance, suppose the referee advises Trader 1 to play Long half of the time and the quantum strategy

5. Multiple Traders

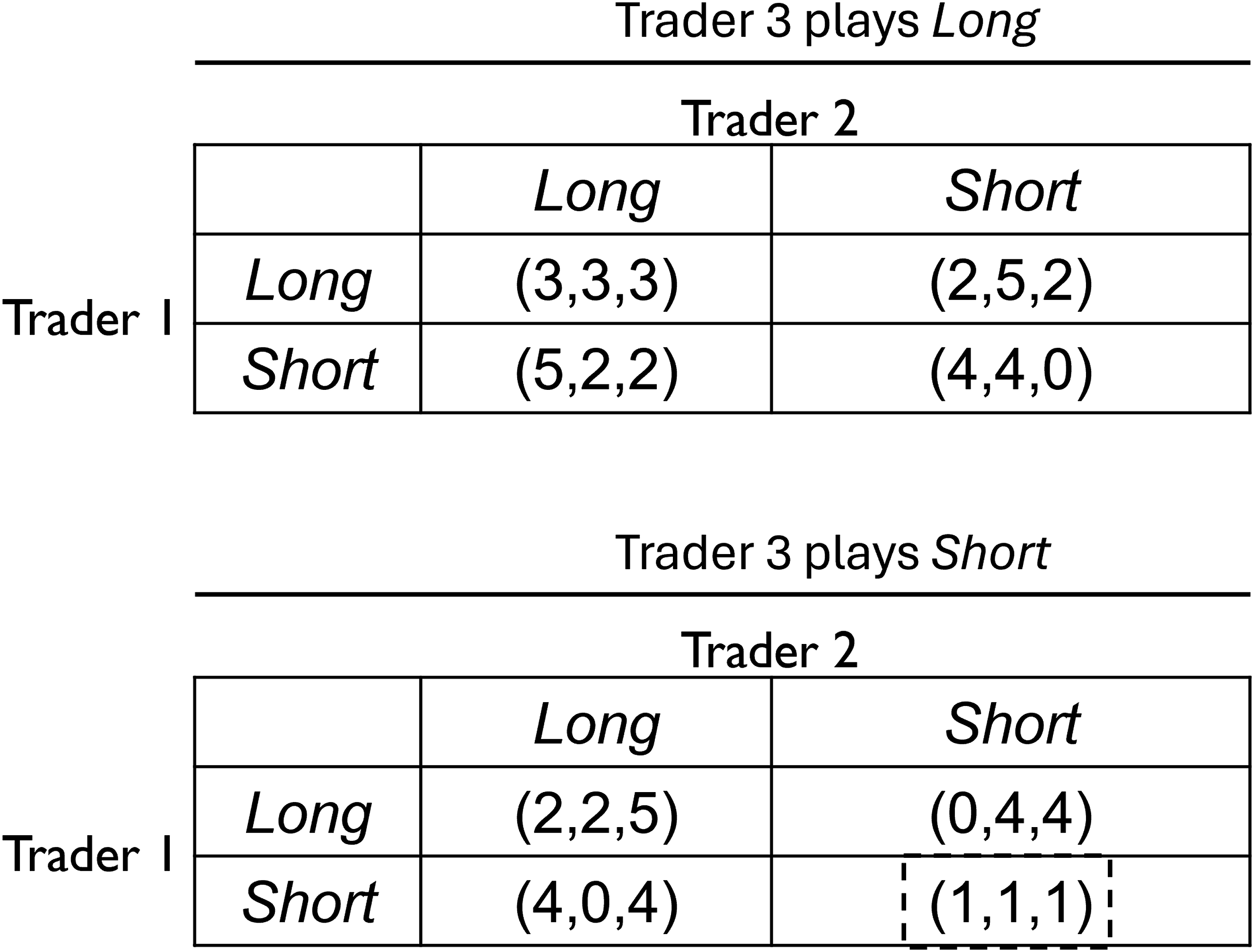

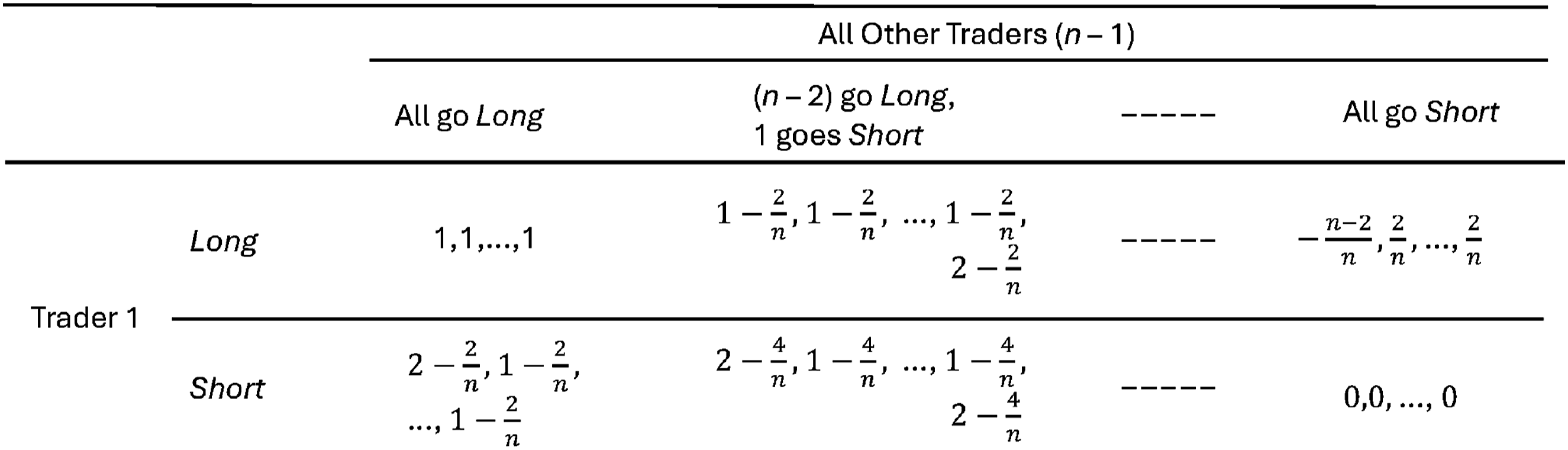

The game-theoretic models of equity trading and their quantum-refereed implementations can be extended to include multiple players. For three-trader Prisoner’s Dilemma, the version depicted in Figure 5 is often used in quantum game theory literature. A best-response analysis of this version reveals that the only pure strategy Nash equilibrium is (Short, Short, Short), highlighted with a dashed box, where each trader only gets 1. A generalized version for n-trader Prisoner’s Dilemma is documented in (Magli et al., 2021) and is replicated in Figure 6. We use this version in our quantum implementation of trading for n = 3, 4, 5, and 6. Note that in this version of the Prisoner’s Dilemma, the Nash equilibrium where everyone goes Short produces a payoff of 0, while a payoff of 1 is made if all traders were to go Long. Three player Prisoner’s Dilemma model of with a unique, suboptimal Nash equilibrium (Short, Short, Short), highlighted in a dashed box, that cannot be improved upon with mixing or the introduction of a referee. A n-trader Prisoner’s Dilemma model for trading.

Even with the introduction of mixed strategies, the traders’ payoffs do not improve. Furthermore, employing a referee to correlate the players’ actions fails to enhance the outcomes, regardless of the probability distribution used to characterize the referee. To illustrate, consider a referee modeled by three coins interconnected via some mechanism (e.g., a wire or cable). The referee’s influence is represented by a probability distribution (p1, p2, …, p8) over the eight possible outcomes of the game.

Assume that Trader 3 tosses her coin and receives advice to play Long. We denote this event as X. To decide whether to follow this advice or instead play Short, Trader 3 considers the following scenarios: • A1: Both Trader 1 and Trader 2 are advised by the referee to play Long. • A2: Trader 1 is advised to play Short, and Trader 2 to play Long. • A3: Trader 1 is advised to play Long, and Trader 2 to play Short. • A4: Both Trader 1 and Trader 2 are advised to play Short.

The conditional probabilities of these events, given X, are calculated as:

Trader 3 then evaluates her expected payoff for two options: agreeing with the referee’s advice or disregarding it. Using the version of Prisoner’s Dilemma in Figure 5, the expected payoff for agreeing is:

On the other hand, the expected payoff for disagreeing and playing Short is:

By comparing these equations, it becomes clear that Trader 3 will always achieve a higher expected payoff by disagreeing with the referee and playing Short. The three-trader Prisoner’s Dilemma also demonstrates the strong dominance of the Short strategy over Long. A similar analysis will show that this result holds for the version of Prisoner’s Dilemma in Figure 6.

5.1. Quantum Referee: Three Traders and Beyond

In (Du et al., 2002), the authors propose an extension of the EWL quantum referee to three or more players (traders) using the payoff table in Figure 5. These author use as the entangling gate

For the case of three traders, the quantum referee is characterized by a quantum superposition of the outcomes of the underlying game that generalizes the quantum supposition in (8). This generalization is the result of adding a qubit, in the state |0⟩, to the quantum referee mechanism together with quantum strategies of the form in (18) for Trader 3. In (Koh et al., 2025), the authors give an analytic expression for the quantum superposition characterizing the EWL quantum referee in an n-player scenario.

The quantum entanglement between the three qubits is given by the phase-adjusted Greenberger-Horne-Zeilinger (GHZ) state

Du et al.’s quantization for three players reaches a quantum correlated equilibrium when the referee advises the traders to play Short. However, this equilibrium results in a payoff of 3 for each trader! The study of mixed quantum correlated equilibria in games involving three or more traders remains an under explored area. Notable progress in this direction is the work of Ahmed in (Ahmed, 2009).

6. Implementation on Ion-Trap Quantum Computer

Building on the work of Du et al., we implemented the quantum-refereed Prisoner’s Dilemma trading model for three or more traders on an ion-trap quantum computer housed at the University of Maryland (Debnath et al., 2016). The system consists of a linear chain of trapped 171Yb+ ions; qubits are encoded in the energy levels the ion. During operation, the qubits are initialized to the |0⟩ state through optical pumping, and quantum gates are performed by turning on laser beams that individually address each ion. Measurement is then done through state-dependent fluorescence (Olmschenk et al., 2007).

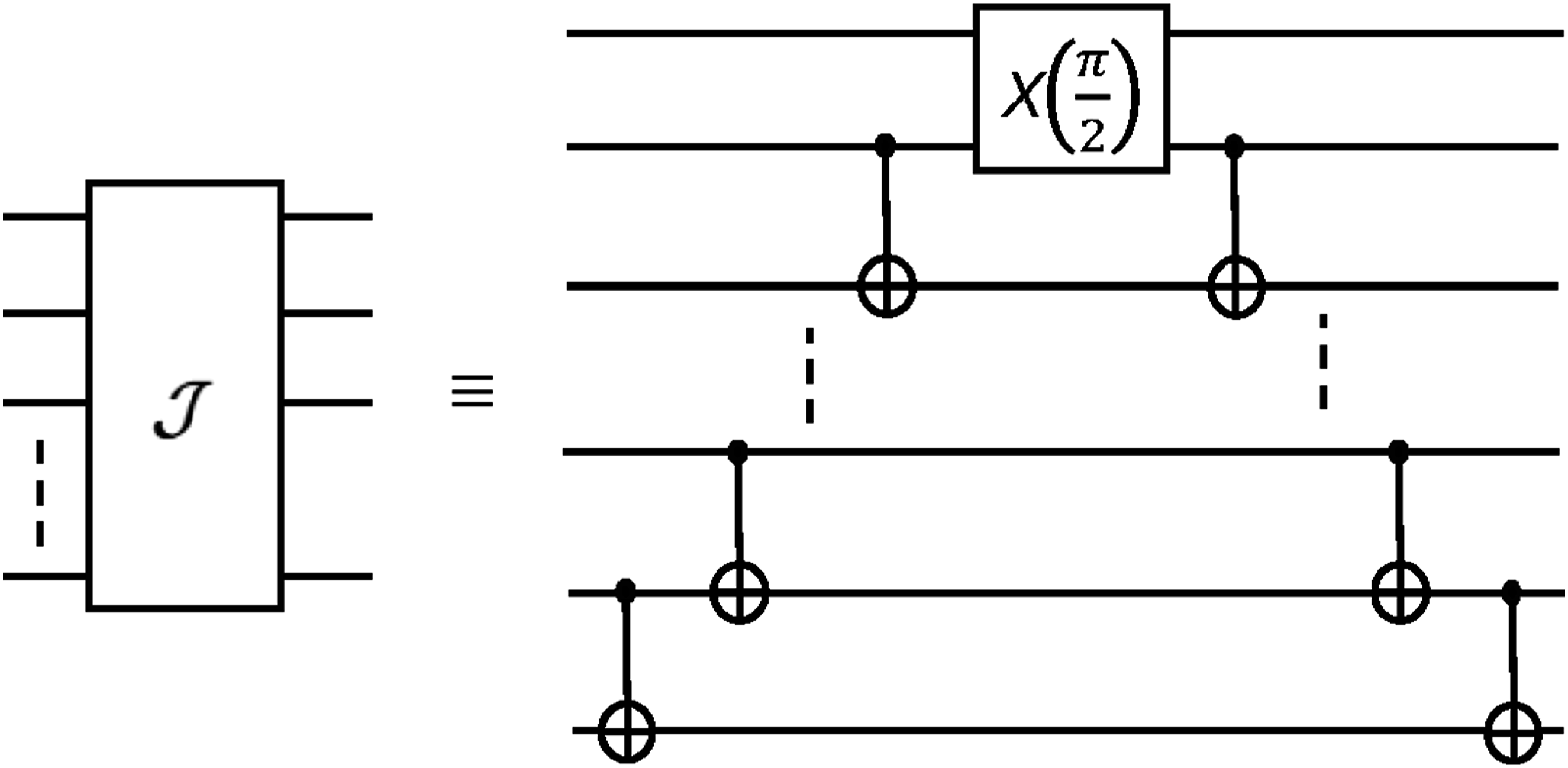

The native operations of the system include a universal gate set of single-qubit rotations and an entangling two-qubit gate The three-trader, two-strategy game quantization (quantum referee) a la Du et al. The gates Decomposition of n qubit entangling operation

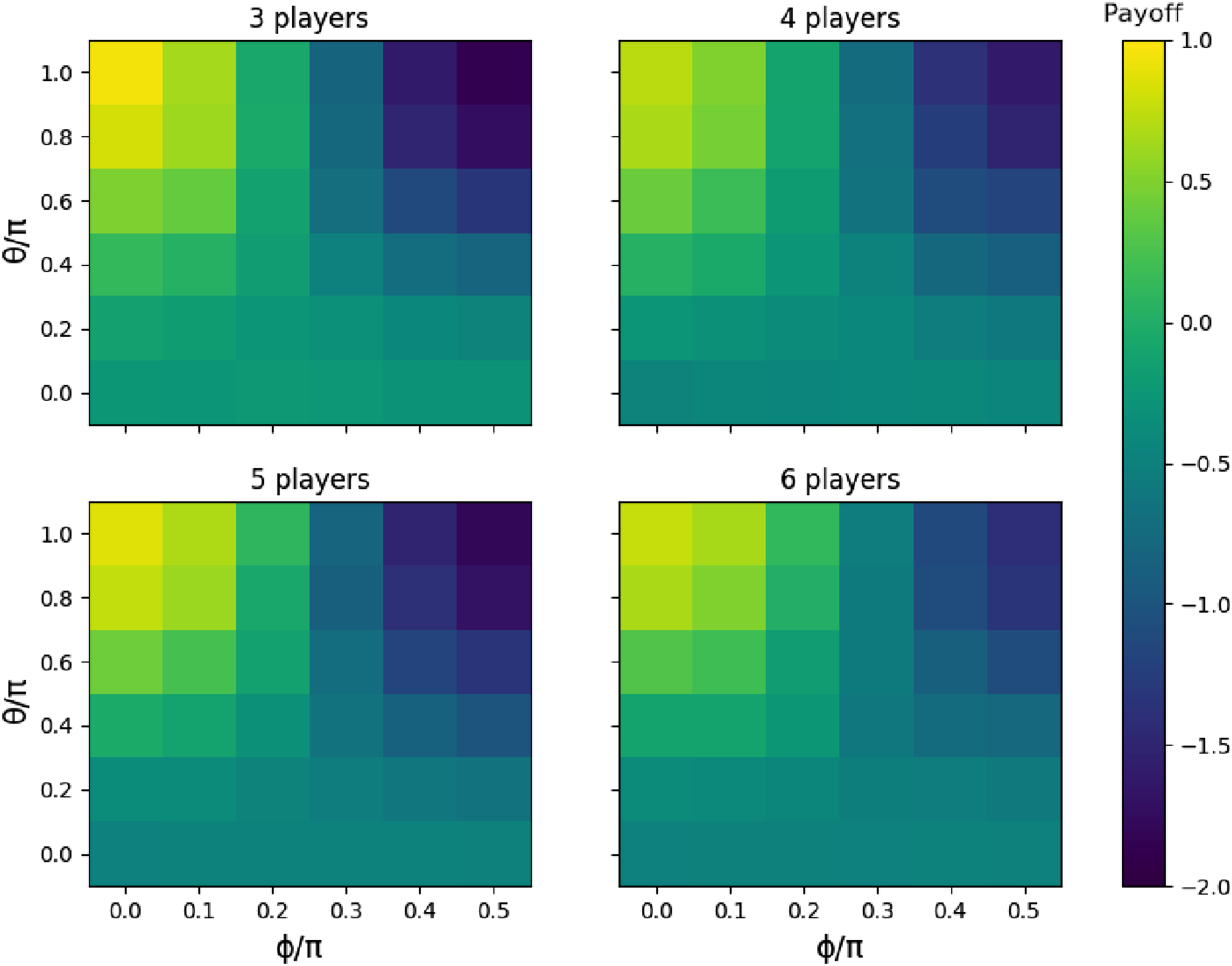

To experimentally demonstrate the Nash equilibrium, we allow Trader 1 to vary his quantum strategy parameters (θ, ϕ) while holding the strategies of the other n − 1 traders fixed at the equilibrium parameters (π, 0). The payoff to Trader 1 is then measured. By symmetry, if the payoff is maximized when Trader 1 adopts the parameters (π, 0), this serves as evidence that the Nash equilibrium has been achieved. We note in our experiments that while the quantum referee proposed by Du et al. generalizes to n traders, for even values of n greater than 2, the quantum correlated equilibrium arises only when the initial state of every qubit is |1⟩ instead of |0⟩. The Nash equilibrium outcomes for the different numbers of players are exhibited in the heat map of Figure 9. For n > 2, our processor required more gates in the decomposition than for when n is odd. For n players, the number of entangling gates used for each circuit to show Nash equilibrium is on the order of 3n. Experimental demonstration of Nash equilibrium for the multiplayer quantum prisoners’ dilemma for n = 3, 4, 5, and 6 players. The maximum payoff of 1 for Trader 1 occurs when they choose the parameters Quantum circuit for Nash equilibrium in two-trader prisoner’s dilemma (or Chicken) when the game is played probabilistically.

6.1. Two-Traders With Mixed Strategies

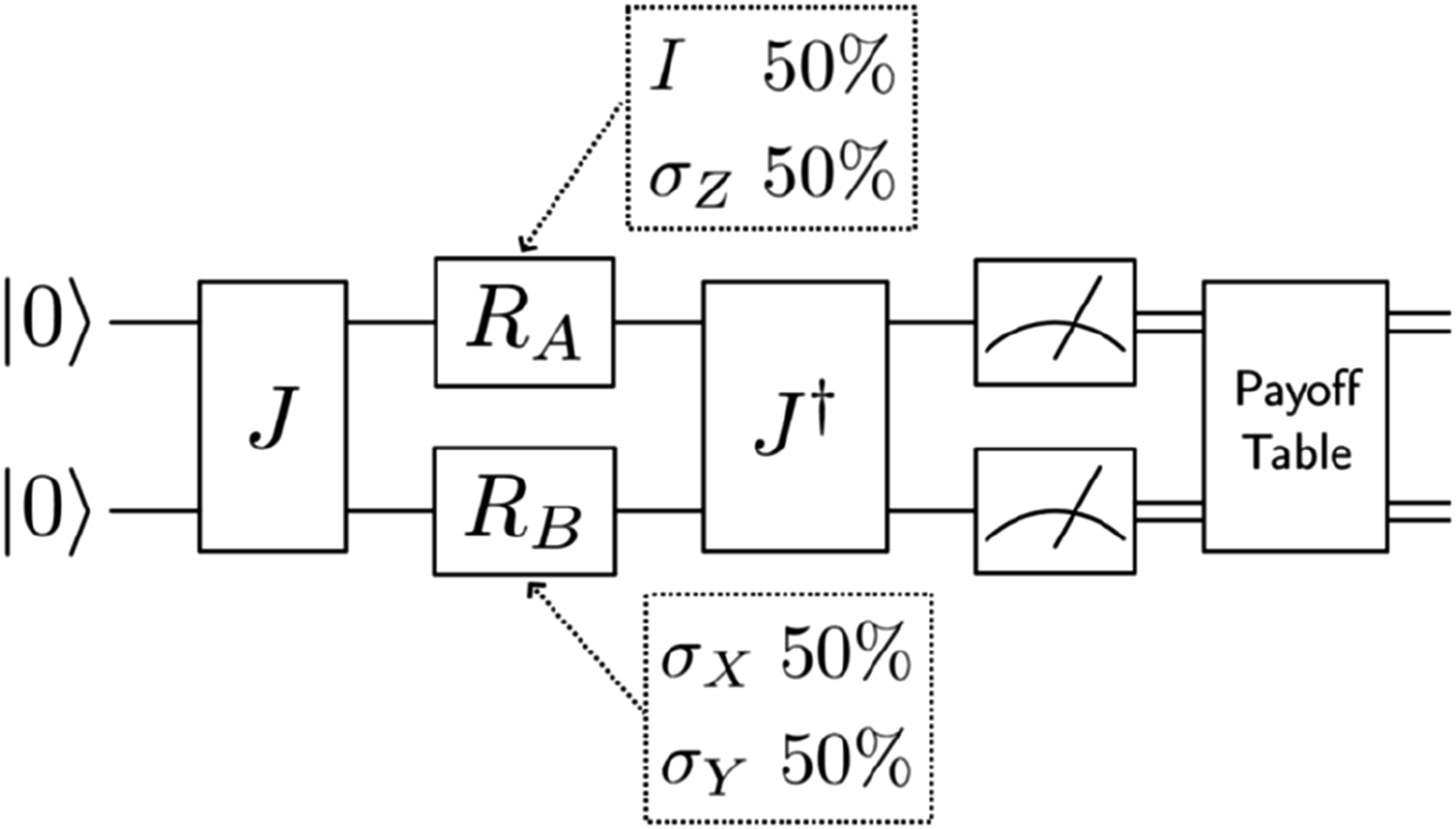

To show Nash equilibrium for randomized strategies, we follow a similar method but repeat the process twice since the equilibrium strategy is no longer symmetric (Figure 10). Explicitly, we fix Trader 2’s strategy and allow Trader 1 to vary his quantum strategy parameters (α, θ, γ). If this is a Nash equilibrium, then Trader 1’s payoff is maximized when adopting the parameters according to his mixed strategy. We then show the same after fixing the other player’s strategy.

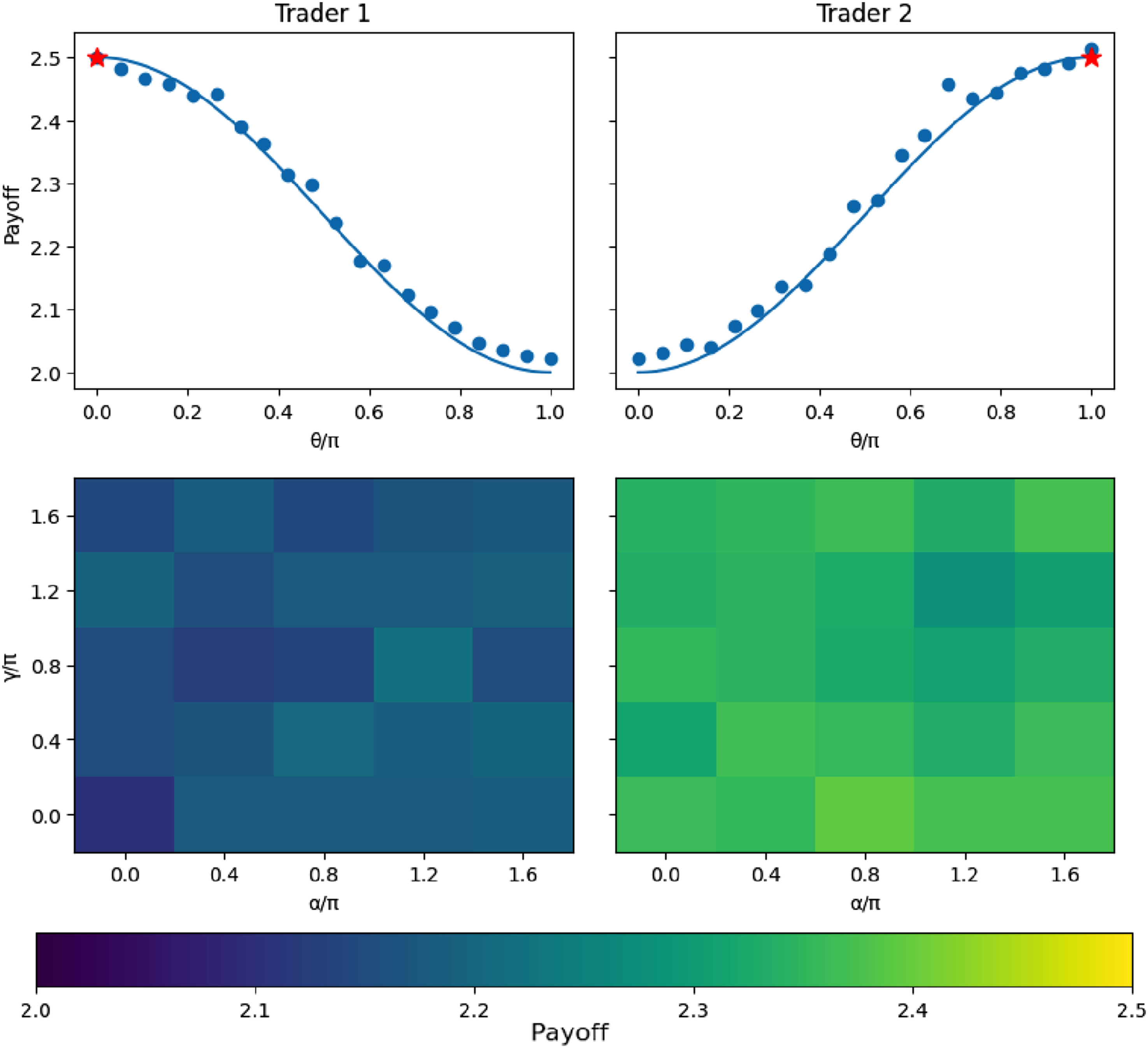

When one player plays their equilibrium strategy, the playoff of both players only depends on the other player’s choice of θ with no dependence on α and γ. As such, when testing the Nash equilibrium, we show that the θ value giving the highest payoff corresponds to that player’s equilibrium strategy. Trader 1 achieves a maximum payoff at θ = 0, and Trader 2 achieves a maximum payoff at θ = π. We successfully demonstrated Nash equilibrium for randomized strategies as shown in Figure 11. Payoffs of players when deviating from the Nash equilibrium strategy for randomized prisoners’ dilemma. Top: Experimentally measured payoffs for different values of θ are shown. The solid blue line shows the simulated payoff, and the blue dots show the payoff obtained in experiment. The red star is the Nash equilibrium strategy. The maximum payoff is obtained at the Nash equilibrium strategy for both players, confirming the Nash equilibrium. Bottom: Experimentally measured payoffs for different values of α and γ at a fixed value of θ. When one player chooses the Nash equilibrium strategy, the simulated payoffs do not have a dependence on α and γ, which is confirmed experimentally.

7. Discussion

We show how the strategic dynamics of Chicken and Prisoner’s Dilemma manifest in trading and explored their implementation on a quantum trading platform. Our results highlight how a quantum referee can create higher-order correlations and deliver a quantum advantage, achieving superior market Nash equilibria. Additionally, we showcase this Nash equilibrium experimentally on an ion-trap quantum processor for up to six traders.

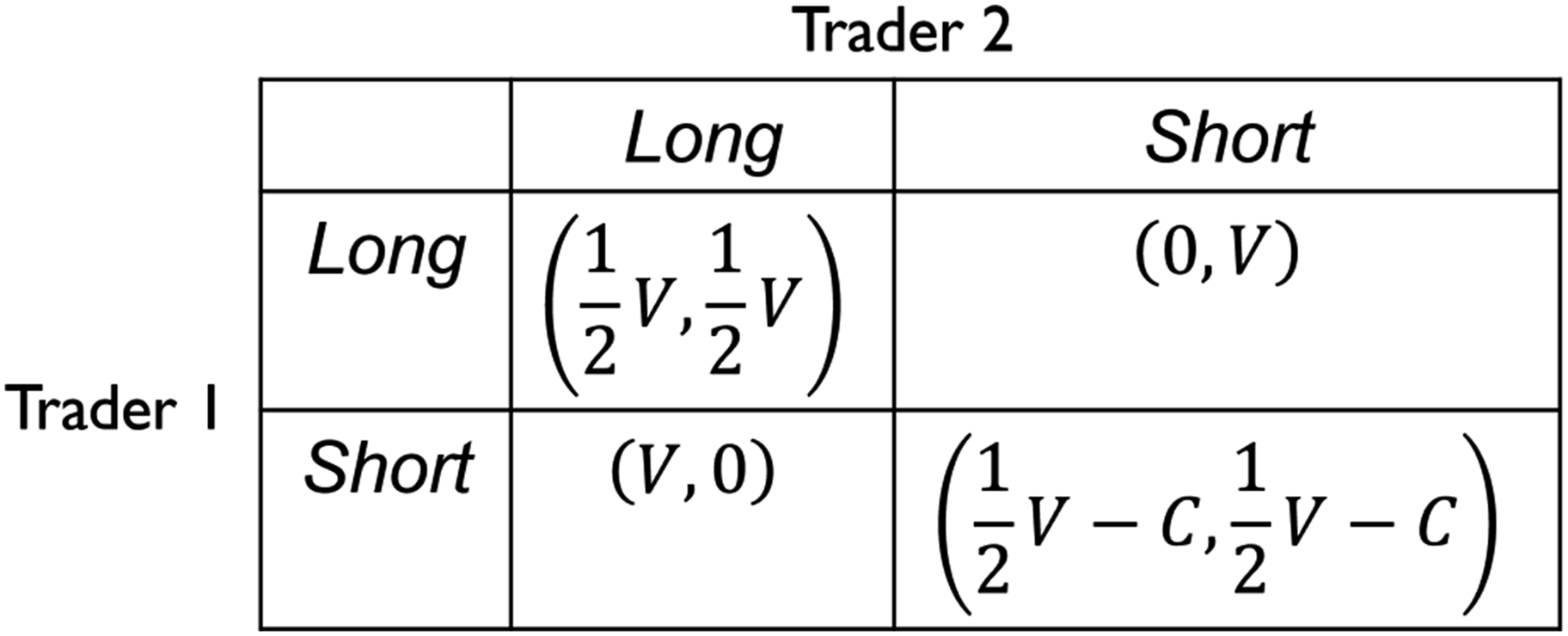

Notably, the quantum referee yields superior Nash equilibria for the entire class of two-player Hawk-Dove games (Binmore, 2007). In these games, each player employs two strategies: Dove, corresponding to the Long position, and Hawk, corresponding to the Short position, as illustrated in Figure 12. The payoff structure ensures that the strategy pairs (Long, Short) and (Short, Long) result in opposite payoffs to the players. Within this framework, Prisoner’s Dilemma and Chicken emerge as special cases with specific parameter values, namely V = 4 and C = 1 or C = 3, respectively. The traders/players heed the advice of a quantum referee even when it is provided probabilistically and realize a better paying Nash equilibrium. In future work, we aim to extend Hawk-Dove games to include additional players and explore more complex game-theoretic scenarios, including mixed quantum strategies. The class of Hawk-Dove game models for equity trading. The variable V represents the value of the asset being traded, which is split when both traders go long, and the variable C represents the cost of both going short.

We also plan to investigate the implementation of these games on quantum computing platforms, exploring in detail the role of quantum entanglement to leverage advantage in financial applications. For instance, this advantage could create win-win scenarios by achieving superior market equilibrium in green markets. Green markets, such as carbon trading, are designed to facilitate the exchange of environmental pollutants under regulatory restrictions (e.g., “cap and trade”) with the primary aim of mitigating pollution by sustaining higher prices. However, if these markets adopt a Prisoner’s Dilemma dynamic, short-selling could become the dominant strategy, resulting in market volatility and potentially lower prices. Quantum trading technology offers a promising solution to address this issue.

In the context of Hawk-Dove games, we emphasize the earlier work of Hanauske et al. (Hanauske et al., 2010), which illustrates that the quantum-entangled version of the hawk-dove game produces “non-aggressive” evolutionary stable strategies that are unattainable within the classical game-theoretic framework. The real-world context of their model is investment banking and the issuance of highly risky investment products with high expected return (aggressive, Hawk strategy) versus investment products of rather low risk and moderate expected return (non-aggressive, Dove strategy). Their findings also suggest that the economic population collectively adopts a non-aggressive quantum strategy, and they suggest potential applications of this toward mitigation of market crashes. The authors interpret quantum entanglement in a non-physical sense, framing it as a shared psychological contract that aligns the strategies of economic agents. Rather than resulting from explicit contract negotiations, they argue that this alignment emerges from broader socioeconomic factors that simultaneously shape individual behavior. These factors include moral standards, values, legal rules, shared experiences, and similar educational backgrounds, which collectively influence decision-making and drive individuals toward coordinated actions, even in the absence of direct communication.

We propose refining this intriguing interpretation of quantum entanglement (the quantum referee) by viewing it as data generated by a network of quantum computers executing trades, which is then made available to traders. This could establish higher-order correlations between traders’ actions, similar to how shared information, such as news, shapes and synchronizes behavior in classical trading environments.

Footnotes

Acknowledgments

The authors thank Alaina Green for experimental support.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: NML acknowledges support from the U.S. Department of Energy (DoE), Office of Science, National Quantum Information Science Research Centers, Quantum Systems Accelerator (DE-FOA-0002253) and the National Science Foundation, Software-Tailored Architecture for Quantum Co-Design (STAQ) Award (PHY-2325080).