Abstract

The growing divide in U.S. politics has significantly influenced how states administer their pension funds. Republican-controlled states have introduced laws prohibiting state pension funds from considering non-pecuniary factors. These states primarily cite concerns about potential breaches of fiduciary responsibility as their rationale. Conversely, Democratic-led states have taken the opposite approach, actively promoting or requiring the incorporation of Environmental, Social, and Governance (ESG) factors in pension investment decisions. This stark contrast reflects divergent perspectives on whether pension beneficiaries prioritize financial gains above all else or if they would accept potentially lower returns to support environmental and social objectives. This study empirically evaluates these assumptions with two large U.S. pension plan participant samples, using conjoint analysis—a cutting-edge method for preference measurement—to empirically assess assumptions about pension plan participants’ attitudes towards ESG features and their willingness to sacrifice profits to endorse environmental or social causes. This research is the first comprehensive U.S. effort to apply this method in the context of ESG investing with representative samples of the U.S. The findings show a clear partisan divide in attitudes regarding investment restrictions on firearms and fossil fuels. However, broad support exists for companies addressing child labor, living wages, and gender pay equality when these social goals are presented with specificity. In contrast, when social issues are framed more generally as “labor rights,” Republican participants tended to prioritize profitability. These results indicate that misconceptions about ESG and unawareness of social externalities may influence public support for anti-ESG legislation. They also reveal that neither ESG mandates nor bans may reflect the diverse preferences of pension beneficiaries. Properly addressing fiduciary concerns requires dissecting ESG into its components to match beneficiaries’ investments with their values more effectively.

1. Introduction

In recent years, Environmental, Social, and Governance (ESG) investing has emerged as a pivotal aspect of modern financial management, sparking debates that straddle the domains of economics, ethics, and politics. ESG investing fundamentally involves integrating environmental, social, and governance considerations into investment decisions, a practice born from the growing recognition of how these factors can significantly impact financial performance and societal well-being (see, e.g., Edmans, 2023). 1 With trillions of dollars under management globally, ESG investments have become a major force in the financial world, reshaping how institutions and individuals approach investing.

The ascent of ESG investing has become highly politicized in the U.S., placing major financial entities like BlackRock at the center of heated debates (Schmitt, 2024). 2 This politicization is vividly reflected in the legislative actions taken by several states regarding the management of their public pension funds, which are split along ideological lines. Some states endorse ESG investments under the belief that they align with their constituents’ preferences and best interests. Others vehemently oppose such strategies, arguing that they represent a breach of the fund managers’ duty of loyalty to their beneficiaries.

This contrast highlights a crucial yet understudied issue: To what extent do ESG related pension management laws truly reflect the preferences of pension plan participants? This question is particularly significant for anti-ESG legislation, as the concerns about fiduciary duties hinge on its answer. Despite the growing body of literature on ESG investing, there exists a notable gap in empirical evidence about the representativeness of such legislative actions. This article aims to address this shortfall. It sheds light on the alignment—or lack thereof—between political actions and constituent interests in the arena of ESG investing, offering insights that are crucial for policymakers, investors, and scholars in understanding the complex interplay between finance, politics, and corporate governance.

This study employs a powerful research methodology: conjoint analysis. This innovative approach allows researchers to delve deep into the stakeholders’ attitudes regarding pension fund investment strategies by inferring their preferences from a set of hypothetical choices characterized by unique attributes related to financial returns and ESG considerations. In other words, rather than asking the study participants how much they would be willing to pay for an investment package with environmental or social features, the participants saw different hypothetical investment options with unique features and chose one in each decision task. This methodology’s advantage lies in its ability to simulate real-world trade-offs, decomposing the value of complex products with several attributes, and minimize social desirability bias (Bansak et al., 2021).

Two separate conjoint experiments with large samples of U.S. retirement plan participants provide insightful information about their preferences. The data paint a much more complex picture than the broad generalizations that have dominanted the political debate. Even among individuals identifying as conservatives, there is a clear preference to support companies that combat child labor, advocate for gender pay equality, and pay living wages. However, when social goals are presented indirectly as “labor rights,” conservative participants focus on profitability. These nuanced preferences stress the complexity of people’s values and the critical importance of how asset managers present (or frame) their strategies. The overal consensus for social sustainability suggests that misconceptions about ESG investing and the non-saliency of certain social externalities may explain public support for anti-ESG legislation.

This Article is structured as follows: Section 2 provides background information on fiduciary duties, public pensions management, and the politicization of ESG investing. Section 3 reviews the literature on concessionary investing and presents the main hypotheses this study tests. Section 4 discusses this works’ methodology. It explains conjoint experiments, how the data were collected, and discusses the relevant estimands for the present analysis. Section 5 presents the findings, revealing a widespread agreement among the U.S. population in favor of investments that promote equal pay for men and women, ensure living wages for their employees, and implement actions to prevent child labor. Section 6 discusses the findings and puts them into the context of related studies. Section 7 concludes noting that the heterogeneity and complexity of public retirement fund participants demand a more flexible supply of plans that better match the participants’ values with their investments. Breaking the ESG label into its individual environmental, social, and governance components would be crucial for aligning investors’ values with their investments.

2. Fiduciary Duties and the Politicization of Public Pension Management

A fiduciary duty underpins the relationship between pension fund beneficiaries and their managers, with the latter expected to act in the best interests of the former (Schanzenbach & Sitkoff, 2018). Historically, the primary duty of pension fund managers was to maximize financial returns. However, the emergence of ESG concerns, including climate change and social inequality, has prompted a reassessment of what constitutes prudent investment strategies. While ESG concerns may well be understood as risk management (Edmans, 2023), ESG’s evolution reflects a broader shift in the understanding and application of fiduciary responsibilities in the context of global challenges and stakeholder expectations (see, e.g., Pollman, 2022; Bartlett & Bubb, 2023).

In the U.S., the approach to ESG investing within public pension fund management is characterized by a diverse and evolving set of legislative responses, reflecting the varied political and economic priorities across states. At one end of the spectrum, some states have embraced ESG considerations in their pension fund management. Maine, for example, passed a law in 2021 that requires its public employee retirement system to divest from major fossil fuel companies by 2026. 3 Similarly, the Illinois Sustainable Investing Act, 4 enacted in 2019, mandates that state and local government entities managing public funds incorporate sustainability considerations, including environmental and social factors, into their investment decisions (Ropes & Gray, 2025).

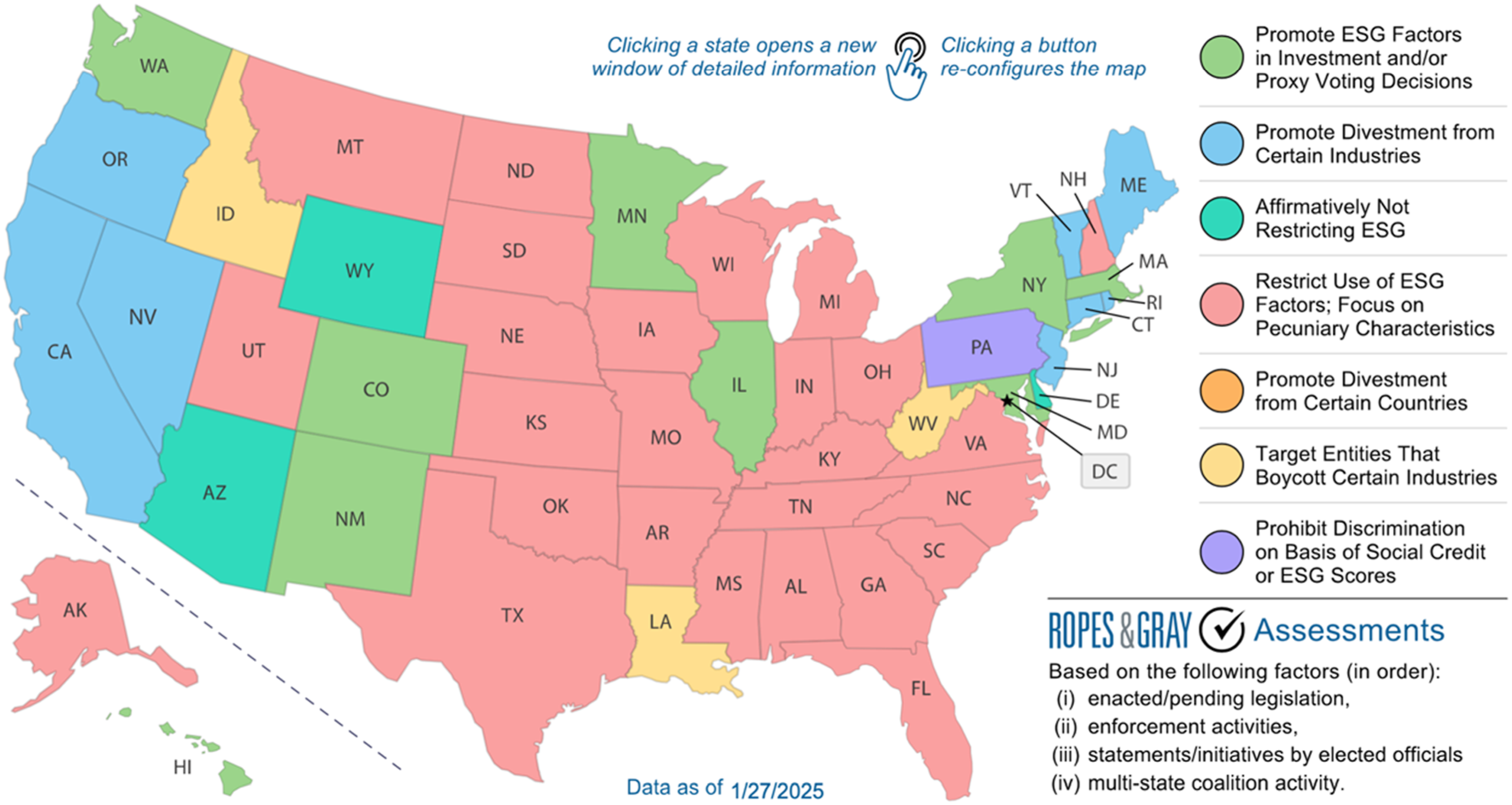

Conversely, several states have taken a critical stance on integrating ESG factors into pension fund management. A particularly striking instance of this was the state of Florida’ decision to actively divest approximately $2 billion from BlackRock, one of the world’s largest investment management firms, specifically citing disagreements with the firm’s ESG policies as the state’s decision trigger (Kerber, 2022). Other notable examples are Texas 5 and West Virginia, 6 which have enacted legislation prohibiting state investment funds, including public pension funds, from investing in companies that boycott fossil fuel industries. Similarly, the Arizona State Board of Investment recently revised its Investment Policy Statement to prohibit the consideration of non-pecuniary factors in state pension investments. 7 Figure 1 shows Ropes and Gray’s simplified summary of the state laws passed until January 2025 (Ropes & Gray, 2025).

The federal viewpoint on this matter—regulated by the Employee Retirement Income Security Act of 1974 (ERISA)—has been markedly affected by political dynamics as well, showcasing distinct fluctuations alongside transitions in presidential administrations. The Department of Labor’s 2022 rule, promulgated under the Biden administration, represents a notable pivot from the previous administration’s policies by adopting a more flexible stance towards the inclusion of ESG criteria in investment considerations. Esg legislation in U.S. States (2025).

This diverse landscape of legislative actions across the U.S. stresses the politicization surrounding ESG investing in pension fund management. A critical aspect yet to be fully explored is the actual preferences of fund beneficiaries for ESG-aligned investment options. Comprehensive evidence that maps these attitudes across the broader U.S. population remains sparse. This gap in the literature is precisely what the present study aims to address.

3. Literature Review

This study delves into various strands of literature, primarily focusing on people’s preferences for socially responsible pension funds and the broader context of altruism and socially responsible investing. ESG investing is only one channel how people express their philanthropy. Simpson and Willer (2015) conduct a thorough review of the causes of altruism, and conclude emphasizing the importance of social norms, rules, and reputations in fostering cooperation and prosocial behavior. Bennett and Einolf (2017) observe that religiosity, minority religion membership, and religious diversity correlate with a higher propensity to assist strangers. This finding contrasts with Wiepking et al. (2014), who find no direct link between country-level devoutness in Europe and charitable giving, but note an increased likelihood of religious giving in religiously heterogeneous countries.

On concessionary investing, Barber et al. (2021) study the trade-off between expected financial returns and the nonpecuniary benefits of impact investing, using data from approximately 24,000 venture capital and growth equity investments made by around 3,500 investors between 1995 and 2014. They find that certain investor groups, including development organizations, foundations, financial institutions, public pension funds, and investors from Europe, Latin America, and Africa, exhibit a discernible willingness to accept lower financial returns for the sake of achieving positive societal impacts. This result varies significantly across investor types and is influenced by factors such as mission objectives and regulatory pressures. In a similar vein, Biong and Silkoset (2017) conduct a conjoint experiment among 276 Norwegian small and medium sized companies to examine to what extent managers emphasize social responsibility versus expected returns when choosing investment managers for their employees’ pension funds. The authors note that employers prioritize suppliers that offer funds committed to socially responsible investment (SRI) practices. Other factors, such as the supplier’s corporate brand reputation, expected returns, and management fees, also impact the managers’ choices but less than SRI commitments. Interestingly, employers with investment expertise prioritize expected returns more highly and place less emphasis on SRI, while employers with defined CSR strategies focus more on social responsibility and less on expected returns.

Heeb et al. (2022) investigate how investors’ WTP for sustainable investments responds to the social impact of those investments, using a framed field experiment. They find that while investors exhibit a substantial WTP for sustainable financial commitments, it does not significantly increase for greater impact investments, suggesting an emotional rather than calculative valuation of impact. Zytnick (2024) empirically assesses whether mutual fund votes reflect their investor preferences, finding that they do not, except for small, ideologically aligned ESG funds. The author suggests that limited investor attention may explain this minimal ideological sorting, as investors select investments based on broad rather than subtle ideological features.

In the pension management domain, several studies have shown a strong preference for socially responsible alternatives. Most of the strong evidence in this respect, however, comes from Northern European countries—especially the Netherlands. Apostolakis et al. (2016) report that over half of their Dutch respondents prefer socially responsible investment portfolios, with a significant portion willing to incur additional costs for this choice. Similarly, Delsen and Lehr (2019) find that a majority of Dutch pension plan participants aged 40 and above are inclined towards sustainable investments, even if it means higher premiums or lower benefits. However, Borgers and Pownall (2014) add that Dutch citizens often struggle to balance financial decisions with non-financial preferences, a dilemma partly attributed to limited financial sophistication.

Studies in the U.S. reveal more nuanced attitudes towards socially responsible investments. Hirst et al., (2023) find that American investors are willing to sacrifice monetary gains for social causes, but to a lesser extent compared to their consumer or philanthropic behaviors. Additionally, a considerable segment of their sample showed reluctance to make financial sacrifices for pro-social initiatives. Echoing this sentiment, Haber et al. (2022) stress significant differences in ESG preferences across various age and wealth demographics, with older and less wealthy investors being more resistant to sacrificing retirement savings for ESG causes.

Based on the literature reviewed, the main hypotheses this study tests are the following:

A sustainable investment package will have a higher likelihood of being chosen. And, relatedly, such likelihood increases the more sustainable the investment package is.

There will be a clear partisan split of preferences for ESG investing. Given the prevalence of anti-ESG legislation in most Republican-led U.S. states, this work will mostly compare the responses of participants who identify as Republicans with the rest.

Religious people will tend to be more altruist than non-religious people.

4. Methods

4.1. Conjoint Analysis

Since the early seventies, the term “conjoint analysis” has primarily been used to refer to a class of survey-experimental methods that estimate respondents’ preferences based on their overall evaluations of alternative profiles that vary across multiple attributes Bansak et al. (2021). The general idea behind conjoint analysis is that features or attributes embodied in objects (or people) drive consumers’ preferences for that option. For instance, two job opportunities usually involve different salaries, commute times, and benefits packages. Since there is more than one variable—or “dimension”—to consider when choosing what job offer to accept, such a choice is multidimensional. Features or attributes are product or people’s characteristics, such as the screen size of a tablet, its memory, and battery life; or a candidate’s education, work-experience, gender, among others.

The notion that product-specific attributes influence choices is consistent with economic and consumer-behavior utility maximization theories (M. Ben-Akiva et al., 2019). 8 Conjoint analysis allows for estimating the relative importance of each attribute or feature on people’s decision making. In the example above, it allows determining how important each of the attributes (i.e., salary, commute time, and benefit package) is for job applicants, and how changes in attribute levels affect the probability of accepting an offer.

Conjoint analysis can take many forms but in any of them the study participants compare at least two options. Each comparison is a “choice-set,” and each participant makes several choices per study. The two most common forms of conjoint experiments are rating-based and choice-based surveys (see, e.g., Green & Srinivasan, 1990). The former asks the study participants to rank each option presented to them. The latter, to choose the option they prefer in each choice-set. The method infers people’s preferences from the profiles (i.e., options available to choose with randomly assigned levels of each attribute) people choose and/or ranked.

Conjoint experiments have many advantages over traditional A/B tests (Hainmueller et al., 2014). In addition to controlling for several potential confounders at once, conjoint experiments are better at minimizing social-desirability bias. Because multiple features change in each task, respondents are less likely to focus on a single feature. By avoiding such a focus, conjoint analysis reduces the possibility of induced demand artifacts. In this sense, a multi-feature conjoint analysis task is more likely to be reliable and valid than a contingent valuation task in which the consumer trades off only one feature.

4.2. Study Design

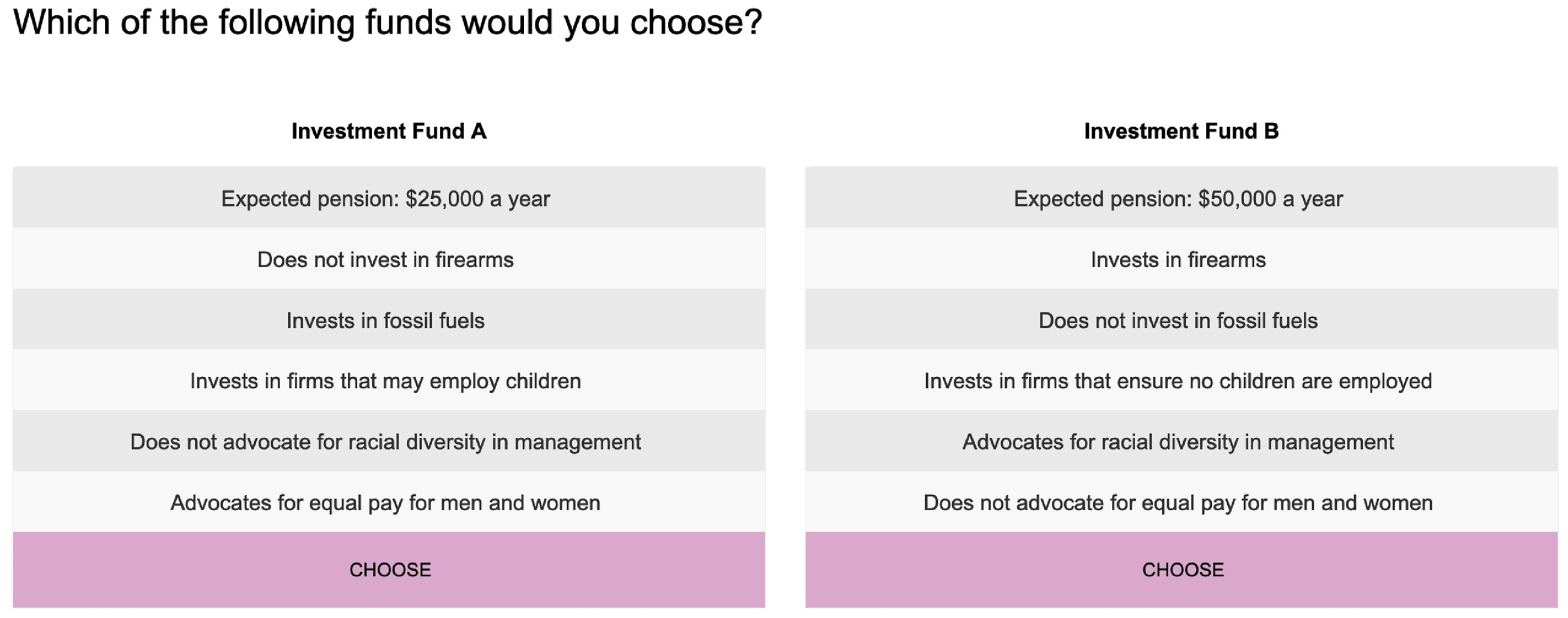

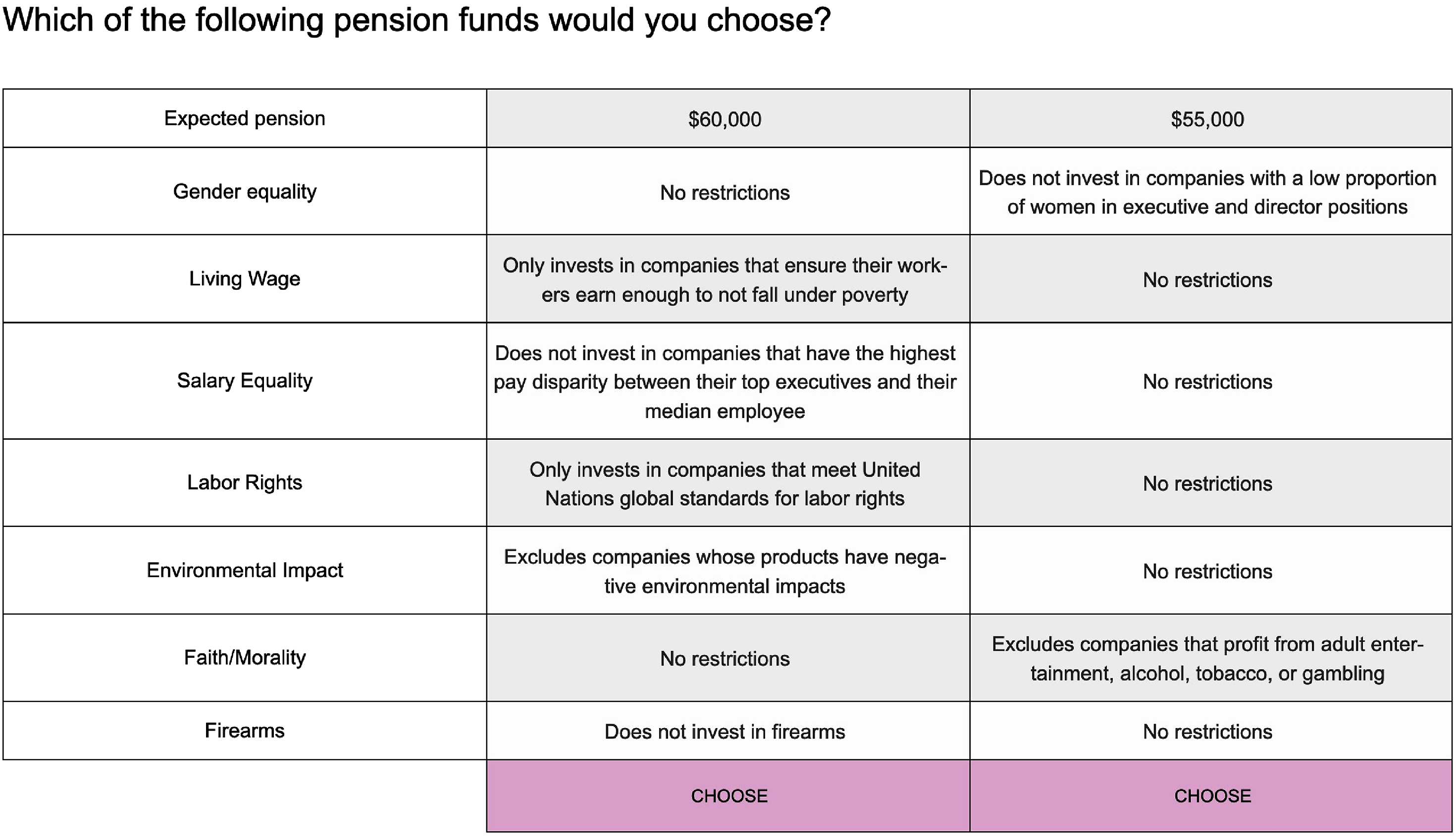

As noted, this work is based on two forced-choice conjoint experiments. Each participant first read the survey instructions, which summarized how investment funds may promote environmental and social causes and described the attributes (i.e., features or variables that influence the decision-makers’ choices) included in the conjoint vignettes. The questionnaires started with socio-demographic questions and both surveys included two attention checks. Subsequently, each participant saw the conjoint vignettes. In both experiments each participant had to make 12 choices, selecting one of two profiles. Twelve choices provide a large amount of data from each respondent and minimize survey satisficing, which is still rare in studies with twenty (Johnson & Orme, 1996) and even thirty choice tasks (Bansak et al., 2018). However, the survey platform Conjointly limits the customization of choice tasks, recommending anything between 8 and 14, yet also allowing (but discouraging) 20 and 30 choice tasks. The second experiment included an additional part between the socio-demographic questions and the conjoint vignettes, which intended to measure general preferences for different combinations of investment packages that included only one ESG attribute. This was to have a benchmark to compare market share simulations based on the estimated choice models. Figures 2 and 3 show examples of the conjoint vignettes from the first and second experiments, respectively. Conjoint vignette first experiment. Conjoint vignette second experiment.

Attributes included in conjoint experiments were carefully selected based on their relevance in prior ESG literature and extensive pre-testing with colleagues from the Laboratory for the Study of American Values to ensure the variables were clear and relevant to respondents. This constraint was what motivated the inclusion of a single expected pension attribute—avoiding references to risk intervals, which only few people understood correctly. In the first experiment, the attributes of the conjoint vignettes were the following: (i) expected pension (from $20,000/year to $60,000/year, by $5,000 increments), and the following types of investment restrictions: (ii) companies that sell firearms, (iii) entities that profit from fossil fuels, (iv) firms that may employ children, (v) companies that do not advocate for racial diversity in management, and (vi) firms that do not advocate for equal pay between men and women. The experiment was not pre-registered because of the lack of similar studies, especially in the U.S., which complicated ex-ante power analyses and precluded the design of a clear analysis plan. However, an important part of this project was to compare responses from Florida and California with the rest of the U.S. The minimum sample size was calculated to have representative samples of each state and the U.S. 9 According to Johnson and Orme’s rule, the minimum sample size to find main effects was 188 responses (Johnson & Orme, 2003). There were no randomization constraints, which made 288 combinations (i.e., profiles) possible (9 × 25).

The second experiment had different variables and reduced the range of the expected pension attribute (7 levels, from $40,000/year to $70,000/year with $5,000 increments). This was to compare the results with those of Hirst et al. (2023) and prevent trade-offs involving a substantially lower pension. The attributes in this second experiment were the following investment restrictions: (i) companies with a low proportion of women in executive positions, (ii) firms that do not pay living wages, (iii) companies with the highest pay disparity between the executives and the median employee, (iv) companies that do not comply with the United Nations (UN) standards for labor rights, (v) entities that produce products with a negative environmental impact, (vi) firms that profit from adult entertainment, alcohol, tobacco, or gambling, and (vii) companies that sell firearms. Each of these variables had two levels (i.e., present or absent). Thus, there were 896 possible combinations (7 × 27). According to Johnson and Orme’s rule, the minimum sample size to find main effects was 146 responses (Johnson & Orme, 2003).

4.3. Sample

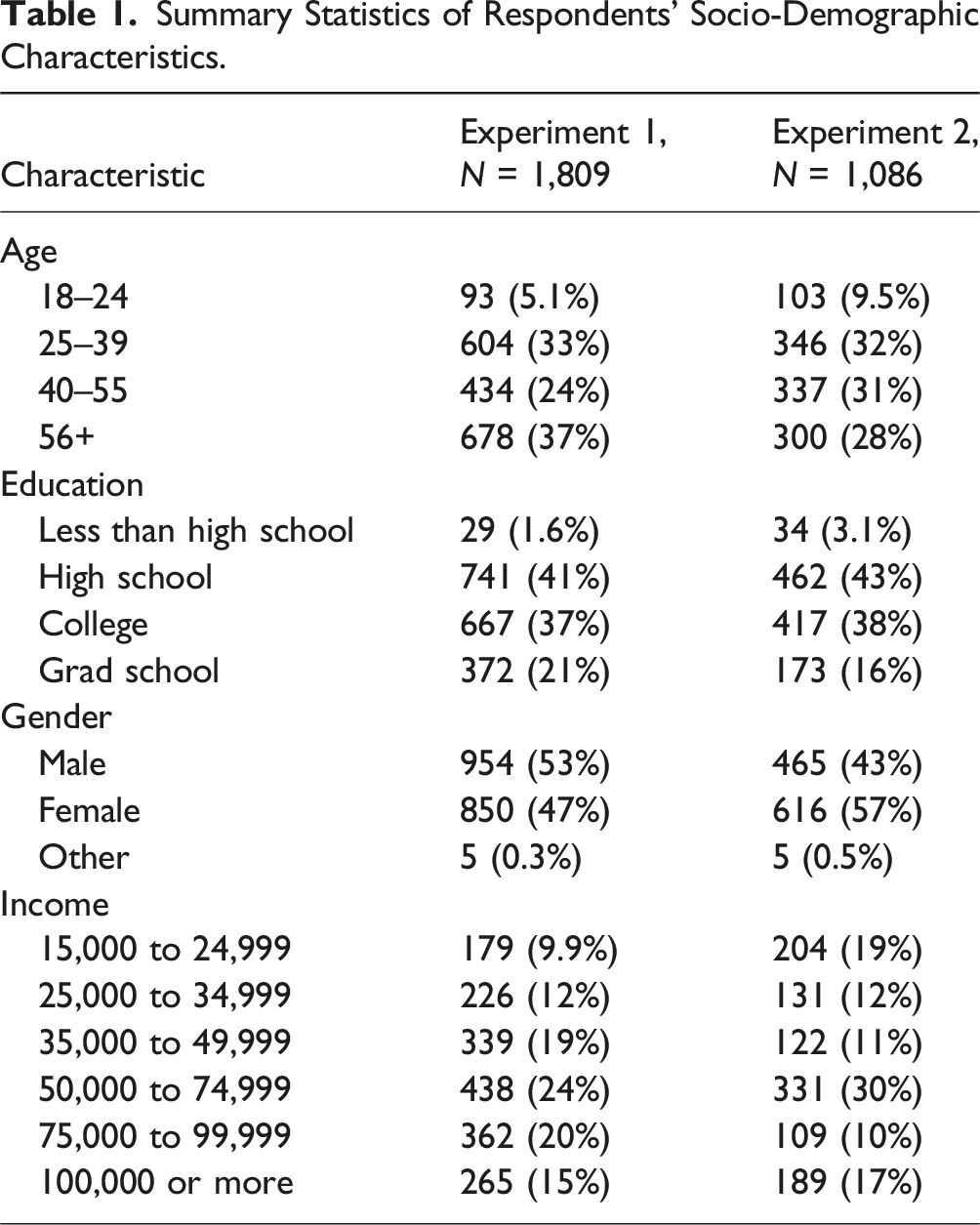

The survey distribution was facilitated by Lucid Theorem. The survey company was asked to obtain a representative sample of the U.S. population regarding gender and age for each experiment. The conjoint analysis questionnaire was hosted on the Conjointly.ly platform, which enhances participant engagement and simplifies the programming of conjoint experiments. An integral feature of the Conjointly.ly system is its automatic filtration mechanism of low-quality data, which screens out responses from participants demonstrating low levels of engagement with the survey. Only responses from participants who successfully cleared two attention checks were considered valid. Furthermore, responses completed in less than half or above twice the median completion time were filtered from the data as well. 10

Summary Statistics of Respondents’ Socio-Demographic Characteristics.

4.4. Estimands of Interest

4.4.1. Average Marginal Components Effect

One of the most widely used estimands in conjoint analysis is the average marginal component effect (AMCE) (Hainmueller et al., 2014). It measures how an attribute change affects the desirability of an option. Going back to the job offers example, if a researcher wants to determine how commute times (let’s assume there are only two levels: “high” or “low”) affect the probability that job candidates accept an offer, the AMCE algorithm will group all the profiles in which commute time was “high” and all the profiles in which commute time was “low.” The difference in outcomes (i.e., offers accepted) between the two groups is the AMCE.

In more technical terms, the AMCE is a difference between “marginal means” (Leeper et al., 2020). It represents the causal effect of changing a profile attribute while averaging over the distribution of the remaining profile attributes. Its simplicity made it one of the most widely used estimands in experimental political science (Bansak et al., 2022) to measure, for instance, whether people’s ethnicity affects the probability they get a visa (Hainmueller & Hopkins, 2015), or whether candidates from minority groups are less likely to be elected for office (Doherty et al., 2019).

Formally, the Average Marginal Component Effect (AMCE) can be expressed as follows:

AMCE a : The Average Marginal Component Effect for attribute level a compared to baseline level a'.

Yi(a): The potential outcome (e.g., vote choice or selection probability) when the attribute is set to level a.

Yi(a'): The potential outcome when the attribute is set to the baseline level a'.

E[·]: Denotes the expectation over the distribution of individuals and other attributes.

This formulation represents the AMCE as the average causal effect of changing an attribute from a baseline level a′ to another level a on the outcome of interest, while averaging over the distribution of other attributes and respondents. It captures the expected difference in outcomes when manipulating a single attribute level, holding all else constant.

A particular advantage of this estimand is its straightforward graphical representation, especially when comparing two groups of respondents. This is one of the reasons why this study mostly reports AMCEs. This work uses Leeper’s “cregg” R package to perform the AMCE calculations (Leeper, 2020). This package estimates AMCEs with multi-variable regression, controlling for all variables included in the conjoint design.

4.4.2. Willingness to Pay (WTP)

Several discrete choice models allow researchers to estimate WTP. Three are particularly relevant for this work: (i) Multinomial Logit, (ii) Mixed Logit, and (iii) Hierarchical Bayes. All of them are rooted in the concept of Random Utility Maximization (RUM) (M. E. Ben-Akiva & Lerman, 1985). According to RUM, when comparing two products, rational consumers will choose the option that provides them with the highest utility. Utility is modeled as having an observed component due to the variation of product features and an unobserved component due to the impact of unobserved variables:

The systematic part of utility

The three models presented in this work estimate these partworths from the respondents’ choices. In the case of Multinomial Logit, this is typically done through Maximum Likelihood Estimation (MLE) (see, e.g., K. E. Train, 2009). The MLE process finds the values of

After calculating the value of each attribute, the model predicts the probability that individuals choose an option within the choice set as a function of its features. The probability

As the formula above clearly illustrates, the MNL output is a set of choice probabilities, which is based on the relative preferences for different levels of the product features. WTP is computed by dividing the utility of each feature by the utility of money (see, e.g., Train & Weeks, 2005). It represents the amount of money a consumer is willing to pay to move from one product (or attribute level) to another while keeping their total utility constant. In other words, WTP reflects how much more a consumer is willing to pay (

From equation (3), the indifference condition may be expressed as follows when subtracting the disutility of price for each option:

MNL assumes that preferences or partworths are homogeneous across all individuals. In other words, it does not account for variation in preferences between different decision-makers. However, interaction MNL models do account for observable heterogeneity, and two notable extensions of MNL, the Mixed Multinomial Logit (MMNL) (McFadden & Train, 2000), and its Hierarchical Bayes (HB) variant (see, e.g., Allenby & Rossi, 2006), allow estimating partworths for each respondent, which is particularly useful for analyzing heterogeneous preferences. Moreover, having individual-level coefficients allows researchers to calculate hypothetical market shares of different profiles.

To estimate the parameters in MMNL, the likelihood function is approximated using simulation techniques (K. E. Train, 2009). Markov Chain Monte Carlo (MCMC) methods are used for estimating parameters in HB models (Allenby & Rossi, 2006). HB will be used for willingness to pay (WTP) and market share simulations because of its advantages handling respondent heterogeneity and outliers (see, e.g., Regier et al., 2009).

This work implements HB with the “choicetools” R package (Chapman et al., 2023). It performs HB choice modeling through a three-stage framework designed for conjoint analysis and preference estimation. The model specifies individual-level parameters (e.g., part-worth utilities) with normally distributed priors centered on population-level hyperparameters, where the global mean (μ) is assigned a weakly informative normal prior

The first experiment model included 13 parameters across 1,809 respondents, with each respondent completing 12 choice sets (2 alternatives per set). MCMC estimation was performed using 10,000 iterations, with the last 1,000 draws used for inference. The final Root Likelihood (RLH) (an indicator of model fit that measures how accurately the predicted choices align with respondents’ actual choices) was 0.819, with a 71.1% certainty level, suggesting good predictive validity. Posterior distributions were stable across iterations, with no evidence of poor convergence. When limiting the sample to Republican participants, the model estimates the 13 parameters across 674 respondents. The MCMC estimation followed the same procedure (10,000 iterations, last 1,000 draws used for inference). The final RLH reached 0.851, with a 77.6% certainty level, indicating strong model fit. The acceptance rate remained within the optimal range (0.30–0.31), and posterior distributions remained stable, confirming no convergence issues. Finally, when restricting the sample to those with an “anti-ESG” prior, the MCMC estimation followed the same procedure (10,000 iterations, last 1,000 draws used for inference). The final RLH reached 0.853, with a 77.0% certainty level, further confirming the robustness of the HB model. The acceptance rate remained within the optimal range (0.30–0.31), and posterior distributions showed no signs of instability. These findings indicate that the HB model maintains strong predictive validity even when analyzing a more targeted subset of respondents.

The second experiment model included 13 parameters across 1,086 respondents, with each respondent completing 12 choice sets (2 alternatives per set). MCMC estimation was performed using 10,000 iterations, with the last 1,000 draws used for inference. The final Root Likelihood (RLH) was 0.747, with a 58.0% certainty level, indicating a reasonable predictive fit. The acceptance rate remained within the optimal range (0.30–0.31), and posterior distributions appeared stable, suggesting no convergence issues. When limiting the sample to Republican participants, the model estimated the same 13 parameters across 448 respondents. The MCMC estimation followed the same procedure (10,000 iterations, last 1000 draws used for inference). The final RLH reached 0.789, with a 65.8% certainty level, demonstrating a stronger model fit compared to the general sample. The acceptance rate was 0.30–0.31, and posterior distributions remained stable, confirming no convergence issues. Finally, when restricting the sample to those with an “anti-ESG” prior, the MCMC estimation again followed the same procedure (10,000 iterations, last 1,000 draws used for inference). The final RLH reached 0.779, with a 64.0% certainty level, supporting the robustness of the hierarchical Bayesian (HB) model. The acceptance rate remained within the 0.30–0.31 range, and posterior distributions showed no signs of instability. These findings indicate that the HB model maintains predictive validity even when analyzing a more targeted subset of respondents.

The choice-based conjoint assumptions were also tested, with no evidence of violations. Utility maximization was confirmed by high Root Likelihood (RLH) values indicating systematic decision-making. Respondent consistency was strong, with acceptance rates in the optimal range (0.30–0.35). Finally, model fit was validated through high certainty levels and stable posterior distributions. As in the first experiment, the HB model provides robust, reliable estimates of respondent preferences.

5. Results

5.1. General Preference for Social Sustainability

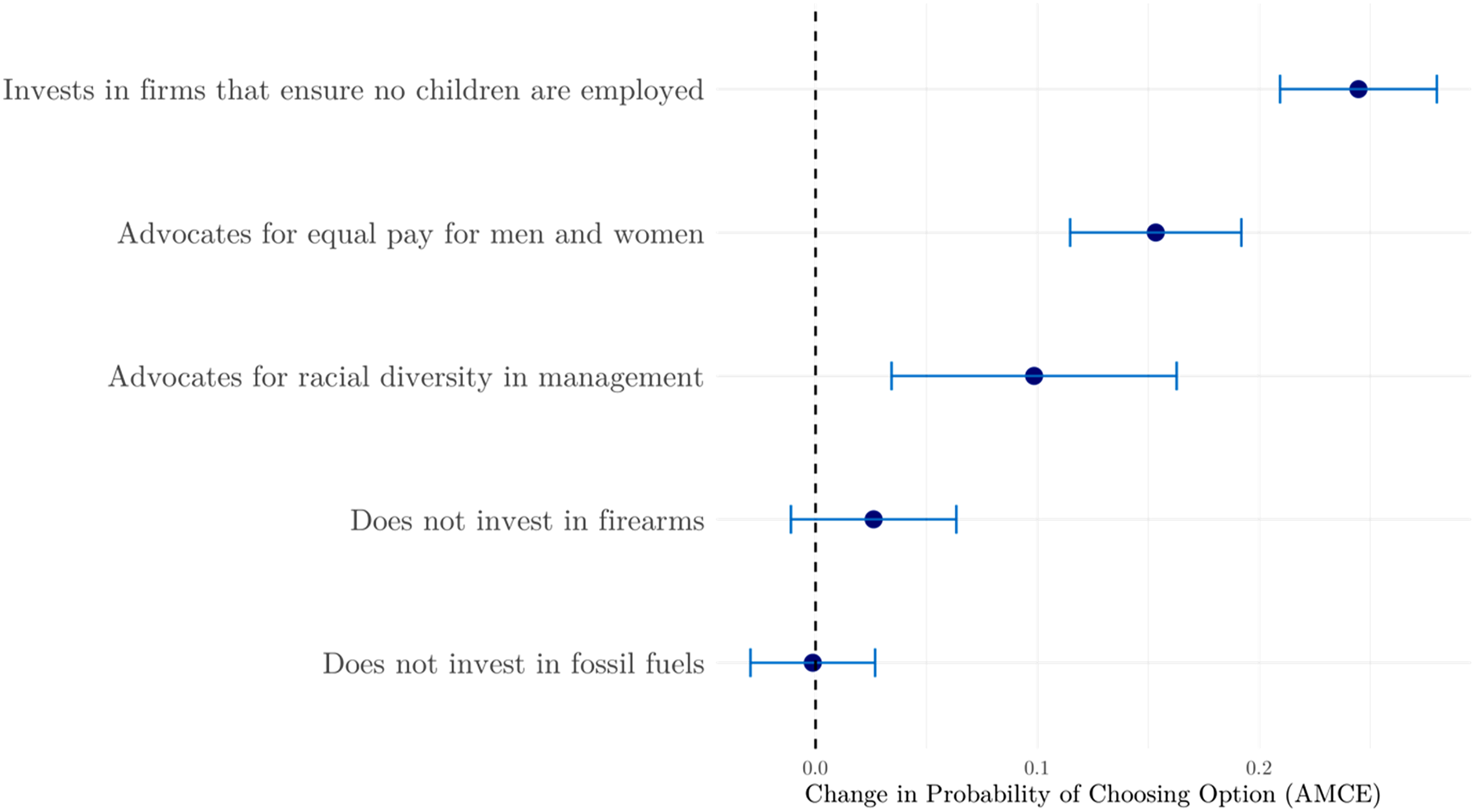

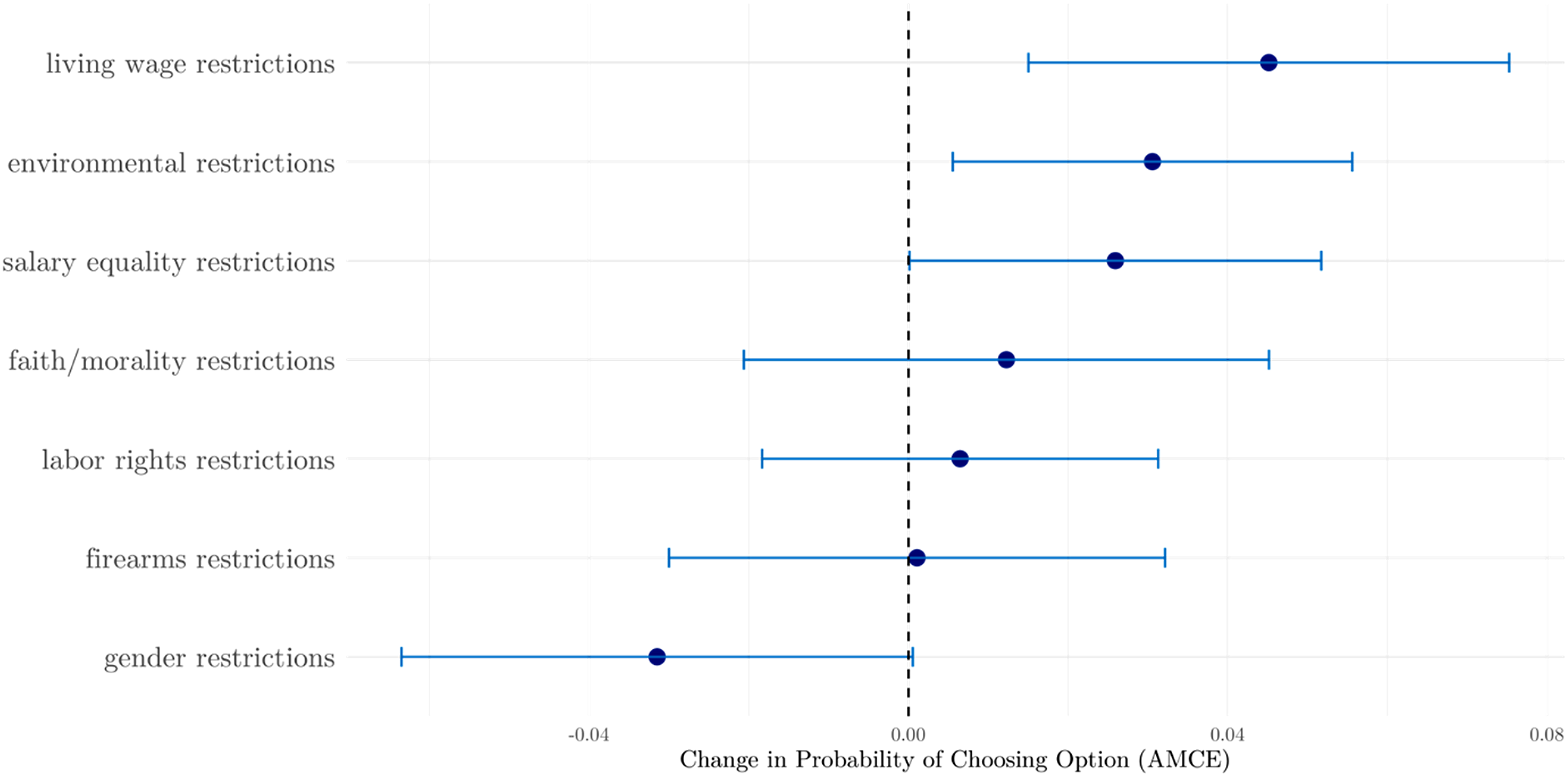

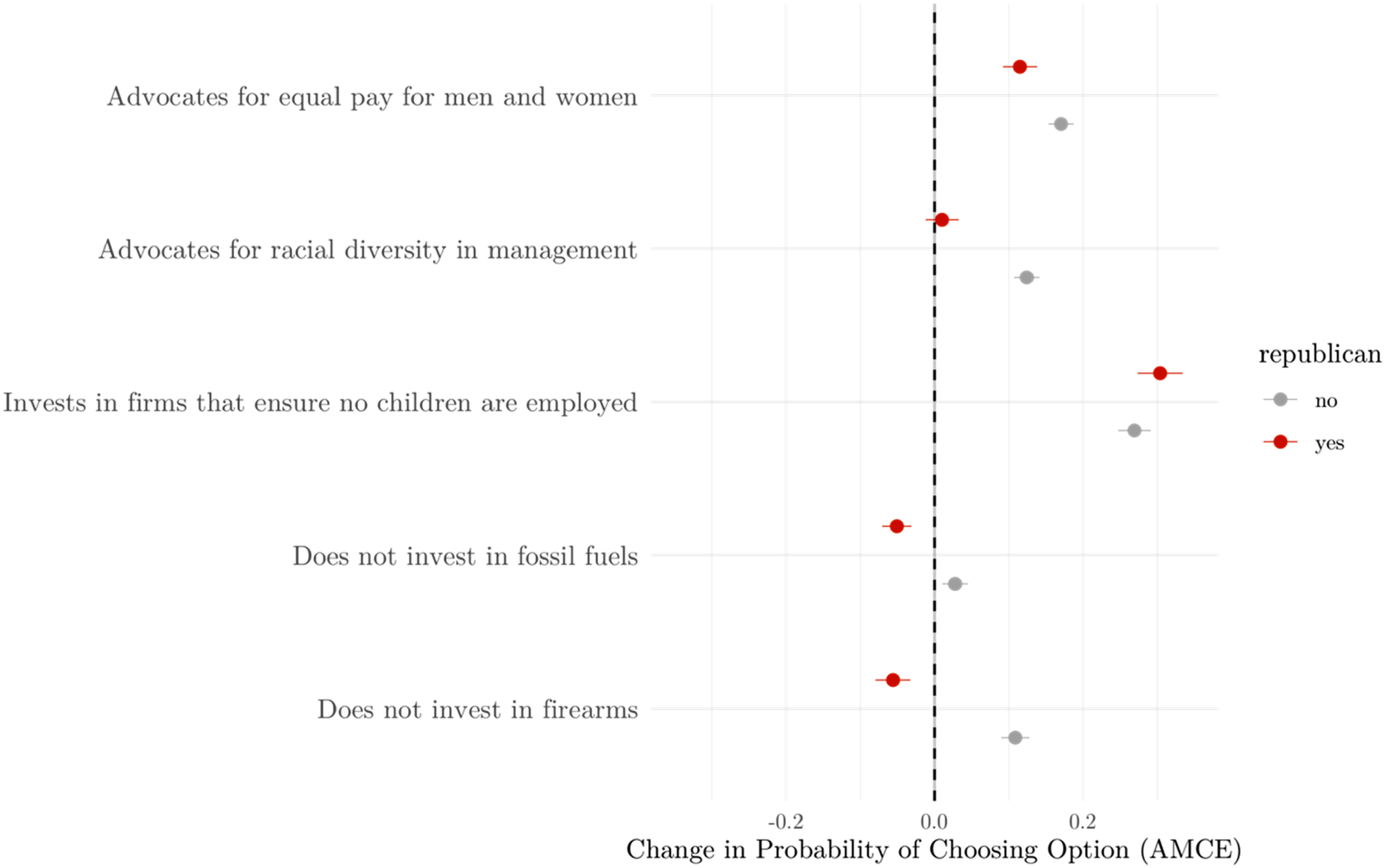

When considering AMCEs for the population as a whole, we find that the respondents had a very strong preference for funds that take affirmative measures against child labor (AMCE = 0.24, s.e. = 0.02, p < .001), favor gender pay parity (AMCE = 0.15, s.e. = 0.01, p < .001), and advocate for racial diversity in management (AMCE = 0.10, s.e. = 0.01, p < .001). Figure 4 shows these results, which represent the main findings of the first conjoint experiment. In the second experiment, the participants showed a general preference for funds that ensure firms pay a living wage (AMCE = 0.05, s.e. = 0.015, p < .004), exclude companies with a large wage disparity between management and the median employee (AMCE = 0.025, s.e. = 0.013, p < .05), and ban firms whose products have a negative environmental impact (AMCE = 0.03, s.e. = 0.012, p < .017). Figure 5 displays these results. Amce first experiment. AMCE second experiment.

The HB model provides similar results. The respondents’ willingness to sacrifice profits were not only statistically significant but also substantial. The median respondent was willing to pay $7,104 for child labor restrictions (95% bootstrapped CI: [$5,892, $8507]), $1,695 to not invest in firearms (95% bootstrapped CI: [$1,199, $2259]), $2,562 to promote racial diversity in management (95% bootstrapped CI: [$2,102, $3109]), and $4,907 to support gender pay parity (95% CI = [$4,270, $5881]).

Market share simulations show that sustainable funds would dominate if people made informed choices about their pension investments. If people had to choose between an investment package with only sustainable features and another with no sustainable characteristics, and both entailed the median expected pension, 85.4% of the participants in the first experiment would choose the sustainable option (95% bootstrapped CI: [83.8%, 86.95%]). In the second experiment, however, only 54.8% of people would choose the sustainable investment package (95% bootstrapped CI: [52.02%, 57.83%]). The additional questions from the second experiment validate this estimation, with 52.3% (95% CI = [48.9%, 55.5%]) of the respondents choosing said investment package.

5.2. Consensus About Child Labor, Gender Pay Gap, and Living Wage

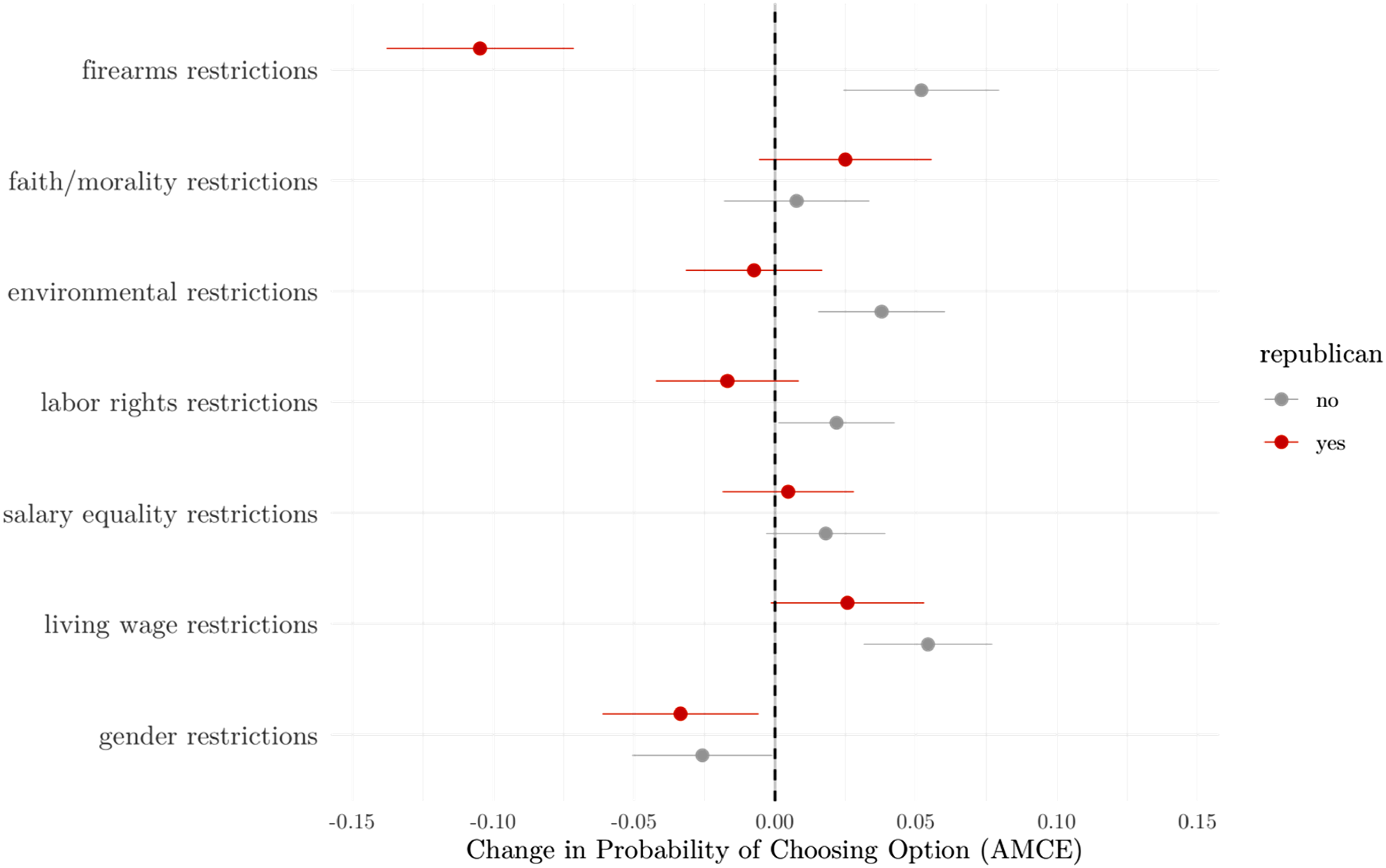

Not surprisingly, there was substantial heterogeneity among the responses of conservative participants and the rest. When comparing the preferences of those that identified as Republicans with those that did not (Independents plus Democrats), it is clear that Republicans were less likely to choose funds that exclude fossil fuels (∆AMCE = −0.08, s.e. = 0.026, p < .001) or firearms (∆AMCE = −0.17, s.e. = 0.03, p < .001) (see Figures 6 and 7 below). However, people from all over the political spectrum tended to favor funds that advocate for gender pay parity and take affirmative measures to prevent child labor. Interestingly, even Republicans were more likely to choose funds that only invested in firms that paid living wages—the HB model shows the median Republican participant was willing to forego $739.40 to limit their investments to firms that paid living wages (95% bootstrapped CI: [$302.94, $1,317.33]) yet the AMCE is only statistically significant at the .1 level (AMCE = 0.025, s.e. = 0.013, p = .06). The HB model shows identical results, estimating that Republicans were willing to forego $5,911 (95% bootstrapped CI = [$3,862; $7,392]) to reward funds that take measures against child labor and $2,809 (95% bootstrapped CI = [$2,091; $3,746]) to support funds that advocate for pay parity between men and women. AMCE first experiment by ideology. AMCE second experiment by ideology.

While Republicans were indifferent to the pursuit of racial diversity in management, Independents and Democrats tended to favor said goal. One of the main aims of the first experiment was to assess whether people in Florida were more conservative than average. Interestingly, there were no statistically significant differences between Florida and the American average. If anything, people in Florida appeared to care more about child labor than the U.S. average. But the difference was too small to pass a significance test.

The HB simulations indicate that in the first experiment 71.51% (95% bootstrapped CI: [68%, 75%]) of Republicans would prefer an investment package with the median pension and only sustainable features and 63.2% (95% bootstrapped CI: [59.8%, 66.7%]) would forego $5,000 to constrain their investments to sustainable features. In the second experiment, the HB simulations suggest 52.57% of Republicans (95% bootstrapped CI: [49.63%, 55.70%]) would prefer the all-sustainable investment package with identical expected profitability, and 27.68% (95% bootstrapped CI: [23.88%, 31.47%]) would be willing to forego $5,000 to invest their money exclusively in sustainable options. These estimates are in line with the results of the WTP questions included in the second experiment.

5.3. The Specificity and Salience of Social Features Have a Large Effect on People’s Choices

One of the main findings of the first experiment was the very substantial effect of the child labor feature on most respondents. Preventing child labor is a core component of the international labor standards established by the UN. This was properly disclosed to the participants when defining each attribute of the conjoint vignette in the introduction of the second experiment. While most of the respondents did prefer options that excluded companies that did not meet the UN labor rights standards, the effect was much lower compared with funds that did not take measures against child labor. Notably, the effect was negative for Republicans. While the negative AMCE was not statistically significant, the HB model indicated the median Republican respondent was willing to sacrifice $1,048.50 (95% bootstrapped CI = [$541.86, $1522.11]) to ensure her investments were not constrained by the UN labor rights standards. This finding, however, should be interpreted with caution since child labor prevention is just a part of the UN international labor standards. It is possible that Republicans dislike the other UN standards and the total utility of the attribute is low or even negative. Future research may well test this hypothesis.

5.4. Misconceptions About the Meaning of ESG Appear to Drive the Support for anti-ESG Legislation

One of the first questions the participants saw in both questionnaires was whether they would prefer their pension funds be managed according to ESG considerations. Conditional on their answers, respondents were categorized as either having a “pro” or “anti” ESG prior.

In both experiments, environmental features did not influence the choices of participants with an anti-ESG prior. However, some social causes did. In the first study, those with an anti-ESG prior preferred funds that advocate for gender pay parity (AMCE = 0.13, s.e. = 0.01, p < .005), support racial diversity in management (AMCE = 0.04, s.e. = 0.01, p < .05), and take measures against child labor (AMCE = 0.27, s.e. = 0.012, p < .005). Moreover, those with an anti-ESG prior were indifferent to fossil fuels exclusions. In the second experiment, only three features were statistically significant. Living wage restrictions had a small positive impact (AMCE = 0.03, s.e., = 0.01, p < .008), and both firearms and gender restrictions had a small negative impact with AMCEs close to zero. The HB model—which is a better tool for handling participant heterogeneity—reports that the median respondent with an anti-ESG prior was willing to pay $2,432 to support gender pay parity (95% bootstrapped CI = [$1,891; $3,314]), $739 to restrict her investments to firms that pay a living wage (95% bootstrapped CI = [$303; $1,317]), and $1,080 to not invest in firms with a negative environmental impact (95% bootstrapped CI = [$813; $1,400]).

5.5. Religion Has Mixed Effects on Altruism

The literature review outlined in Section 2 reveals mixed evidence regarding the influence of religiosity on altruistic behavior. Considering the relevance of this theme to this research and the minimal burden of adding an extra item to the questionnaire, this study explored whether individuals who pray or meditate often are more inclined than their non-religious counterparts to choose investment options with social or environmental constraints. Two caveats are in order. First, prayer or meditation frequency is an imperfect operationalization of religiosity, but it is common in the literature. Second, this is also a reductionist operationalization of altruism, since there are many other possible behavioral channels, such as charitable donations, volunteering work, etc. Thus, this analysis is limited to one of many behavioral channels of altruism.

In the first experiment, there were two significant differences based on individuals’ frequency of prayer or meditation. Those who engaged in these practices almost daily were less likely to select investment portfolios with restrictions on firearms (∆AMCE = −0.06, s.e. = 0.017, p < .005) or fossil fuels (∆AMCE = −0.05, s.e. = 0.01, p < .005). This tendency was also observed when analyzing data exclusively from non-Republican participants.

In contrast, the second experiment presented a unique finding within the entire sample: religious individuals showed a higher propensity for investments with faith/morality constraints. The effect was substantial (∆AMCE = 0.14, s.e. = 0.05, p < .005), and it persisted when excluding Republicans from the analysis. Nonetheless, religiosity affected Republicans’ preferences for salary equality since those who reported praying or meditating often were more likely to opt for investment options that included salary equality restrictions (∆AMCE = 0.27, s.e. = 0.10, p < .006).

6. Discussion

There are several methodologies for measuring people’s preferences. This study merged the analyses used in political science and marketing to provide more understandable and informative results about U.S. pension plan participants’ preferences for ESG investing. An important limitation of this work, however, is that the participants faced no monetary incentives to reveal their preferences. Thus, it is possible that they presented themselves as more generous than they are. The original design of this study intended to account for this possible issue with a lottery, in which the respondents could win $100 to invest in shares that matched their preferences. Unfortunately, because of California regulations, 11 this option was not feasible. Nevertheless, research comparing the validity of incentivized versus non-incentivized surveys shows that non-incentivized surveys still provide valuable data (see, e.g., Charness et al., 2021). Some studies find that incentives make no significant differences (e.g., Hackethal et al., 2023). Others find that incentives lower WTP estimates but make no qualitative differences (e.g., Hernández & Vila, 2014; Liebe et al., 2019). Moreover, this work’s findings show credible trends. This is especially the case with respect to highly-politicized issues, such as environmental and firearms restrictions, in which the respondents split in partisan lines. It is important to emphasize here that people’s utilities were inferred from their choices, not their statements. Thus, any difference in preferences for firearms restrictions between conservatives and liberals stem from the profiles the participants chose. Besides, the WTP estimates are very close to what the 2023 Rock Center Survey of Investors, Retirement Savings, and ESG reports (between 1% and 5% of people’s pension), 12 participants over 55 years old were willing to sacrifice lower amounts than those who were farther from retirement, and, as noted, highly religious people were more likely to choose investment packages with faith/morality restrictions.

Another limitation of this study is that the choice vignettes do not represent how pension funds are chosen in the real world. To begin with, in the case of public pension funds, it is not the beneficiaries themselves but a pension manager who chooses in which funds to invest. Also, pension funds beneficiaries tend to have little room to customize their portfolios in many if not most private pension plans. Even when wealth managers allow beneficiaries to opt into an “ESG” option, it is not clear what restrictions the portfolio entails. And any sustainability goal tends to be presented as vaguely as possible. However, the choice vignettes made the investment restrictions salient and easy to understand. Accordingly, the results may well be understood as a normative benchmark. And one may argue that this would be an ideal benchmark (not this study itself but the type of study), one of a well-informed and engaged “consumer.” In fact, it is extremely challenging—if not impossible—to operationalize said benchmark with observational data. Relatedly, the estimates are certainly at odds with data on charitable donations, portraying a much more altruistic picture of the U.S. population. While it’s common practice in applied economics to consider that people’s behavior reveals their preferences, behavior is the result of a complex mechanism in which the link between attitudes and behavior is mediated by situational factors, some that affect their engagement with a particular choice task (see, e.g., Haddock et al., 2020). In this sense, this study sheds light on people’s attitudes in a setting in which there was little friction to reveal those attitudes with their choices.

This work finds substantial heterogeneity among the preferences of the U.S. population regarding some environmental and social features of ESG investing. However, despite this heterogeneity, there is much more consensus on social sustainability than what conventional wisdom assumes. This is a key difference with the Rock Center surveys, in which most participants tended to express a similar degree of concern for environmental and social issues. And this consensus falsifies the representativeness of anti-ESG legislation, even in Florida.

Despite using a different methodology, the Rock Center surveys show similar results on people’s WTP for social or environmental causes, and that people who are closer to retirement place a higher value on profitability. However, this study’s WTP estimates are much higher than those Hirst et al. (2023) find. WTP estimates are very sensible to the range of prices used in the conjoint vignettes. By using a pension average that is close to the median pension in the U.S. the results of this study should be reasonably informative. However, the estimates are likely to be inflated due to the lack of economic incentives (see, e.g., Ahles et al., 2024; Murphy et al., 2005). It is important to note that Hirst et al. (2023) designed a more complicated decision task (not a conjoint experiment) that always involved a sacrifice between 0.1% and 9% to invest in a sustainable option, and only considered the responses of participants with a positive WTP in the calculation (Hirst et al., 2023, p. 1009). The methodology used in this work and its much larger sample sizes should give it an edge. But, unlike this study, Hirst et al. (2023) did use economic incentives. Future studies may well replicate this work’s research design with economic incentives to appraise whether the results replicate.

As noted, the effect sizes were much larger in the first experiment than in the second. The psychology literature has documented that people are more likely to act ethically when a decision cue increases the saliency of a choice’s moral dimension, which is consistent with a self-concept maintenance theory (see, e.g., Mazar et al., 2008). It is likely that a similar effect occurred in the first experiment, in which the child labor feature had such a large effect. In fact, in some of the open-ended comments, many participants who identified as Republicans referred to child labor as a case in which children’s autonomy was coerced. This finding underscores that the specificity of certain social externalities makes the consequences of choices more tangible and harder to ignore, thereby enhancing their moral saliency and prompting more ethical decision-making.

There was another important difference between the results of the first and the second experiments. While investment exclusions affecting “fossil fuels” split the respondents in partisan lines, exclusions that focused on the “environmental impact” of companies did not affect the choices of conservative respondents. The impact of policy framing on policy popularity is well-documented (see, e.g., Hardisty et al., (2010)). This appears to be a similar case in which the “fossil fuel” label acts as a stronger cue for Republicans. In fact, the median Republican respondent was willing to give up $1,305 to ensure her pension fund managers did not exclude investments in fossil fuels (95% bootstrapped CI = [$954, $1,640]). The preceding paragraphs have important implications for the framing of sustainable investing. Broad categorizations that trigger people’s political identities seem unlikely to nudge people, and especially conservatives, towards more sustainable behavior. For instance, nowadays the “fair-trade” movement appears to be in decay (see, e.g., Subramanian, 2019). And perhaps the movement would be more successful with a different framing that would make it easier for people to understand what types of trade-externalities it addresses. Maybe more than one label would be necessary for appealing to different types of investors and/or consumers.

Child labor was a feature that moved most respondents. However, child labor has soared in the U.S. in recent years (Gurley, 2023). This study suggests that most people would benefit substantially from knowing what products and companies exploit children to invest (and potentially buy) elsewhere. Considering people’s very high WTP to address child labor issues, it is not unreasonable to assume that more informative and effective disclosures would be efficient, even if costly.

Any method aimed at simplifying and condensing information inherently faces challenges (see, e.g., Loewenstein et al., 2014). ESG metrics are compromised by several notable issues: a lack of standardization, insufficient third-party verification, and inconsistent weighting adjustments, among others (Brest & Honigsberg, 2021). For example, Tesla’s situation vividly illustrates the conflicts between governance and environmental considerations, highlighting the limitations of a one-size-fits-all approach to ESG labeling. These nuanced differences in how individuals prioritize environmental versus social issues underscore the need for a more granular approach. Disaggregating ESG into its constituent elements—Environmental, Social, and Governance—could offer substantial benefits. Such a breakdown would enhance transparency and allow for a more customized evaluation of these components, providing investors with the tools to align their investments more closely with their specific values and ethical considerations (see, e.g., Temple-West & Tett, 2022). In fact, if anti-ESG laws were genuinely motivated by potential breaches of fiduciary duties, politicians should prioritize the unbundling of the ESG label.

7. Conclusions

This study assessed the representativeness of existing state laws on public pension fund management, which often homogenize investor attitudes toward sustainability by relying on rigid and oversimplified assumptions about the beneficiaries’ preferences. Republican-led states assume that considering ESG factors in state pension fund investments constitutes a breach of managers’ fiduciary duties to their beneficiaries. Conversely, Democratic-led states assume that their constituencies prefer endorsing environmental or social goals, even if it means lower returns or higher fees.

This work identified a distinct partisan divide in attitudes toward investments in firearms and fossil fuels, yet widespread agreement across the political spectrum supporting companies that address specific social issues like child labor, living wages, and gender pay equality. This consensus is remarkably present across various groups, including those traditionally opposed to ESG investing. This finding suggests that prevailing misconceptions about ESG might be influencing public opinion in conservative states and, consequently, public support for anti-ESG legislation. Indeed, this study only reveals a pronounced partisan division in attitudes toward investment restrictions on firearms and fossil fuels. Many with an anti-ESG prior appear to assume that ESG is just an environmental movement because they do prefer investments with social sustainability features. Nevertheless, the sharp partisan divide indicates that mandatory ESG investing laws also contradict the preferences of a significant segment of the population.

The experimental results further emphasize the critical impact of goal presentation on people’s choices. When environmental goals were framed broadly, Republicans were indifferent to them. However, when framed as a ban on fossil fuels, Republicans were willing to sacrifice a part of their pensions to ensure their investments were not subject to said constraint. While child labor had a very large effect on most respondents in the first experiment, compliance with international labor right standards—which include a ban on child labor—had a much lower effect. This difference suggests that a general label that many associate with a political agenda leads people who truly care about child labor to behave inconsistently with their preferences.

Considering the complexity and heterogeneity of pension plan beneficiaries’ preferences, this study recommends splitting the ESG label into its individual components: Environmental (E), Social (S), and Governance (G). Disaggregating these factors would enable a more precise and faithful alignment with the diverse values of individual investors. Moving away from a one-size-fits-all ESG model not only honors the diversity of investor values but also has the potential to widen the appeal of sustainable investing by offering clearer, more personalized investment options.

Footnotes

Acknowledgments

The author wrote this piece while working at the Stanford Rock Center for Corporate Governance but revised the piece during his NYU Fellowship. Many thanks to Oren Bar-Gill, Robert Bartlett, Joe Grundfest, Colleen Honigsberg, Louis Kaplow, Lewis Kornhauser, Mark Lemley, Rob MacCoun, Rok Spruk, Jeff Strnad, George Triantis, Mike Tomz, Paul Sniderman, Lauren Davenport, the editor, three anonymous reviewers, the members of the Stanford Laboratory for the Study of American Values, and participants at the 2024 American Law and Economics Association Annual Meeting and the 14th Annual Conference of the Spanish Law and Economics Association for their feedback. The author acknowledges the financial support from the Stanford Laboratory for the Study of American Values and the Stanford Olin Program in Law and Economics. The author also acknowledges the academic account Conjointly provided free of charge. IRB approval was obtained through the Stanford Laboratory for the Study of American Values. Data and analysis are available at the author’s ![]() .

.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This was supported by Stanford University.