Abstract

This article examines the impact of Greece retroactively, via legislation, changing the terms in hundreds of billions of euros worth of Greek government bonds governed by domestic Greek law. As the abrogation of gold clauses in US government bonds by the US Congress in 1933 had been, the Greek action was decried as violative of the rule of law and sure to negatively impact the future ability of Euro area sovereigns to borrow. We test whether the Greek action had negative spillovers on European government debt markets. We find no evidence of increased borrowing for even the most peripheral European economies from the Greek action.

Introduction

In February 2012, the Greek legislature retroactively inserted “collective action clauses” in close to 200 billion euros worth of local law governed sovereign bonds (the “Greek retrofit”). These new clauses allowed for a super majority of creditors to agree to restructuring the debt and bind all non consenting creditors (Weidemaier & Gulati, 2013). These clauses were then used to drive a restructuring of the Greek debt, with creditors taking net present value (NPV) haircuts in the range of 55–65%, some of the biggest in history (Zettelmeyer et al., 2013). The actions of the Greek government, done with the approval and support of European authorities, were widely decried as violative of the rule of law and sure to increase borrowing costs for other European borrowers. We examine that claim.

The condemnation of the Greek action was loud and widespread. Bill Gross, chief investment officer of the giant bond fund, PIMCO, declared that Greece’s actions constituted a “gross violation” of the “sanctity” of contract rights (Goff, 2012). Other titles in the financial press and blogs included, “Greece Kills the Rule of Law”, “Why the Greek Bondholder Law is ‘Too Awful to Think About’”, and “Greece’s Disgraceful Debt Default”.

1

One market commentator wrote: This Greek government . . . retroactively inserted provisions in a debt contract and then imposed them. No sovereign-debt contract is now immune from the same action. All sovereign-debt contracts will carry a risk premium. Buyers of European sovereign debt now act at their own peril… Legal jurisdictions are important . . . At Cumberland, we did not own and we will not own debt where a legal system can rewrite a contract, unless disputes (bankruptcy) can be adjudicated by a neutral court (Ritholtz, 2012).

An eminent UK debt lawyer, explained: Retroactive legislation of this sort runs counter to one of the most fundamental cornerstones of any civilized, free society – namely the rule of law. Investors acquired bonds in the belief that whatever contractual rights were embodied in them would be upheld by the courts and could only be altered with their agreement. So, when the debtor altered those rights unilaterally and to its own advantage . . . it is hardly surprising that the confidence of investors was badly shaken. And the fact that the perpetrator of this act was a European sovereign, and part of the European Union, who might be expected above all others to understand and uphold the principal of the rule of law, made the shock all the more palpable. It is easy to protest . . . that this was an isolated incident, and would not be repeated. Dogs that bite once tend to do so again (Burn, 2013).

There is also, however, a more benign perspective. Under this view, there are a set of conditions under which blindly following contractual rules is calamitous. This is so when contracts specify terms that are not adapted to circumstances and when welfare would be enhanced by bypassing them. When certain contingencies could not be adequately contracted for ahead of time, it may be best for the state to step in to fill the contractual gaps ex post (Bolton & Rosenthal, 2002). Here, assuming the market understands what has happened, there should not be a market penalty following the intervention in contracts.

In what follows, we assess the alternative views by testing whether the Greek retrofit had negative spillovers on European government debt markets that shared vulnerability to a similar use of this legal technique. 2 The Euro area is, because of the economic and political interconnectedness of the member nations, particularly vulnerable to financial contagion (Capasso et al., 2023; Clancy et al., 2022). Hence, to the extent the Greek restructuring was violative of rule of law notions and called into question the viability of all debt of vulnerable Euro area nations, we should readily see effects. However, we find no evidence that the Greek retrofit increased the borrowing cost of other peripheral European economies. These results are consistent with the findings of Krozsner (1998) and Edwards (2018), who examined the 1933 abrogation of gold clauses in US public debt by the US Congress – an action that produced howls of outrage that the rule of law had been trampled and dire predictions that borrowing costs would skyrocket, none of which materialized (Magliocca, 2012; Vanberg & Gulati, 2019). To the contrary, US government borrowing thrived.

In the next section, we provide an account of how and when Greece decided on the retrofit strategy. Our focus is the question of the degree to which the final form of the retrofit, with its legislatively imposed aggregation across debt issues, quorum, and 66.67% vote features, and the subsequent legal decisions about its legality, was extraordinary. This “surprise” aspect of the story is important to setting up the empirical analysis that follows, with the market reacting to unexpected novel features of the retrofit. An examination of that response to the retrofit event then provides a measure of spillover effects.

The Greek debt crisis began in late 2009 and spread to other parts of Europe by early 2010. The retrofit strategy though did not get serious consideration until late 2011. Indeed, for much of the first year and a half of the crisis, European policy makers repeatedly stated that any debt restructuring was off the table. And if a restructuring was ever done, policy makers kept insisting, it would be a “voluntary” one.

The reason for the aversion to even the use of the word “restructuring” in European policy circles and particularly at the highest levels of the European Central Bank was, first and foremost, the fear that a Greek restructuring would lead investors to be concerned about not just Greek debt, but all peripheral Euro area debt. That, in turn, would cause borrowing costs to rise across Europe, thereby deepening the crisis. Indeed, there were multiple points during the crisis when senior European policy makers seemed to prefer the outcome of Greece leaving the European Union to it restructuring even one euro of its government debt under a plan to keep Greece in the union.

In hindsight, it is easier to see that Greece had little choice but to do a massive restructuring of its government debt in March 2012. And to engineer it, Greece had to retroactively pass legislation to introduce collective action clauses into its debt contracts, that would provide a mechanism for creditors to voluntarily restructure Greek debt (Zettelmeyer et al., 2013).

We ask two basic questions at the outset, before reporting empirical tests: How did the concerns of European policy makers who resisted the restructuring manifest themselves? And, how much of a surprise jolt was the actual makeup of the retrofit and the extent of the proposed write-down?

The public record does not provide answers to the surprise question, particularly with respect to the Greek Bondholder Act of March 2012. Hence, as a precursor to our empirical analysis, we dig into the background discussions that preceded the Act to try and unearth both the surprise element of the Act and the concerns voiced by the engineers of the restructuring strategy regarding possible market responses and future legal challenges.

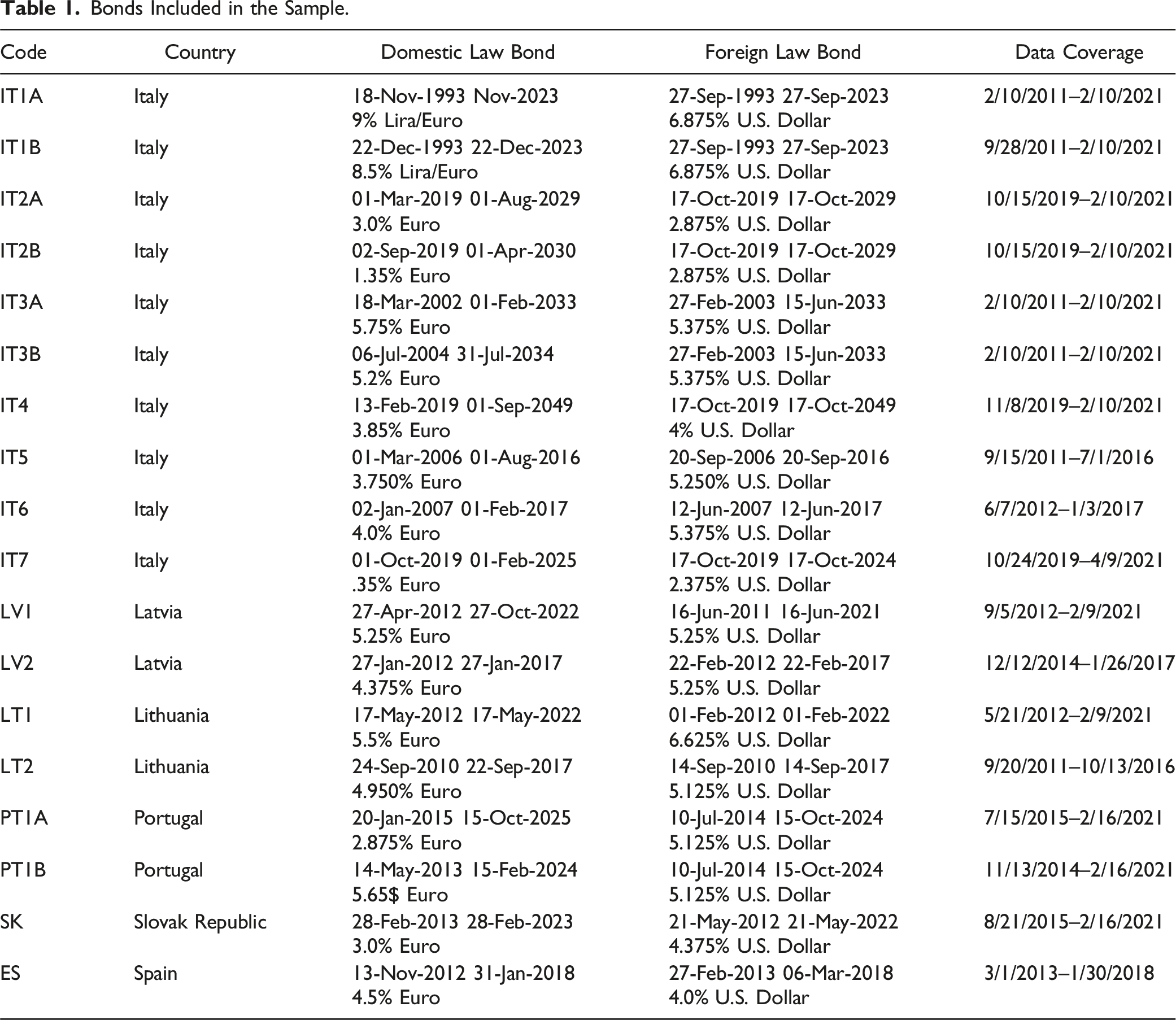

In the following section, we focus on a series of legal decisions and use event study analysis to examine how the Greek retrofit affected the borrowing costs of Italy, Portugal, Spain, Latvia, Lithuania, and the Slovak Republic. To conduct these tests, we match bonds issued under national or EU jurisdiction with bonds by the same country and with similar maturity but issued under New York or English law. We then use these matched bonds to explore how the Greek retrofit and various court decisions that rejected challenges to the Greek Bondholder Act affected the yields of bonds issued under national legislation relative to similar bonds issued under New York or English law.

The Backstory

To reconstruct what happened, we talked with forty-one lawyers, bankers, policy makers and journalists who were either involved in the decisions or were reporting on them at the time (based on their own interviews with some of the protagonists). We structured our interviews around an initial narrative that we had put together as best we could based on what we ourselves had read and heard during that time. We used that skeleton as the basis to ask our respondents to help correct errors and fill in gaps. Below, is the story that has emerged from these exchanges.

The Origins of the Retrofit

The idea of the retrofit was first floated in May 2010 by Lee Buchheit, a New York sovereign debt lawyer, in a draft paper posted on the social science research network (ssrn.com). Buchheit was a legendary figure in the world of sovereign debt, known for his creative restructuring techniques. But his work had almost all been in the emerging market space and with debt governed by New York law. Greece, with its debt under European laws, was not talking to him. And his law firm, Cleary Gottlieb, was at best likely to represent some of Greece’s creditors. Greece’s long-time lawyers, Allen & Overy, were in London and there was little reason to think that Buchheit would play a role in an eventual Greek restructuring.

When first floated in May 2010, Buchheit’s retrofit idea was not taken seriously by anyone. Indeed, he had played out it as a thought experiment for a Spring 2010 class on International Debt at Duke Law School. The view taken in European officialdom at the time was that the crisis would be fixed with a rescue package that would enable Greece to continue paying its bondholders on time and in full. No serious thought was given to a restructuring with bondholders taking a real hit. To the contrary, when the EUR 110 billion rescue package for Greece was introduced in May 2010, the holders of maturing Greek Government Bonds continued to be paid in full with the proceeds of official sector (EU/IMF) loans. The same standard policy response was followed in the cases of Ireland and Portugal.

Alongside these interventions, senior policy makers, such as Jean Claude Trichet and Lorenzo Bini Smaghi of the European Central Bank, were giving speeches assuring everyone that a sovereign debt default and restructuring in Europe would never, ever be permitted. When the official sector tells investors that a debt instrument will never be allowed to default, it is implicitly telling them that the sovereign debtor will be bailed out with official sector money before the payment falls due. That was the state of affairs through 2010 and into mid-2011.

In 2010 and into mid-2011, the general view in European policy circles was that debt restructurings with haircuts only happened in emerging market nations. The expertise of restructurers like Buchheit and their suggestions were not relevant to a Euro area member nation such as Greece. As the Euro crisis worsened though, some policy makers began to march to a different drummer – particularly at the IMF, where there were many who had experience with emerging market restructurings that could see that the Greek situation was looking more and more like an emerging market sovereign debt crisis. Eventually, a combination of voices at the IMF and some European policy makers with experience from the Paris Club persuaded Greece to switch lawyers to Buchheit and his team at Cleary Gottlieb, the emerging market restructuring specialists.

On July 24, 2011, Buchheit was invited to go to Washington DC to meet with the then Greek finance minister, Evangelos Venizelos. At the meeting, Venizelos handed Buchheit a term sheet put together a few days prior with the Institute of International Finance (IIF), acting as the representative for some of the bondholders and a subset of banks. This blueprint became known as “PSI 1” (standing for “private sector involvement 1”).

It was modelled on a restructuring technique used during the Latin American crisis, where as part of the Brady plan, investors were offered a “menu of options”. Specifically, it contained a par bond option, a discount bond option, and a couple of other options. One would have thought that the hiring of Buchheit and his team from Cleary Gottlieb would lead to a change of tack, and that they would be given discretion to do something radical. But that was not so. They were told that their task was to execute that modest term sheet, not question it. Although in hindsight it seems palpable that Buchheit would ultimately be asked to implement his May 2010 plan, no one we have spoken to suggested that they saw this coming as early as mid-2011. One respondent explained: Until Trichet retired, there was no question of a restructuring. He would not even allow talk of it anywhere near him. And Trichet was not retiring until the end of October 2011. So, we had to wait.

An all hands meeting took place in Athens in early August. The IIF team, led by sovereign debt veteran Charles Dallara, insisted that there had to be a preliminary canvass of all Greek government bondholders to see which menu option they might favour, before the preliminaries to a deal could be launched. One of our respondents explained what followed: I never understood the logic of [the IIF’s strategy to want to first canvas the creditors] but was happy to adhere to their wishes. That process was to be conducted by the Ministries of Finance in the 50 some countries where the bondholders resided. It was a nightmare to administer. This process burned up August and September. It probably saved Greece because it became clear that most holders were going to take the par bond option.

3

But while this was unfolding the situation in Greece was getting worse, further eroding any hope that Greece could escape without a savage debt restructuring. The only question was whether that restructuring would be visited upon the commercial creditors of the EUR 209 billion of Greek government bonds left in private hands, or upon the EU/IMF, if the policy of a total bailout that began in May 2010 were to continue.

The Decision to Restructure

Somebody (we have heard from multiple sources that it was the IMF staff) with support from a couple of Northern European finance ministries (both the Netherlands and Finland were mentioned) swayed the French and the Germans in the early fall of 2021 that a Greek government bond restructuring was now unavoidable. Importantly, they persuaded Germany’s Chancellor Angela Merkel and Finance Minister Wolfgang Schäuble that this was coming. Once Schäuble was converted, the game changed. Either Greece was going to do a massive restructuring to get Europe out of the quicksand, or it was going to have to leave the euro. The line in the sand was that the restructuring must involve at least a 50% principal haircut (later raised to 53.5%) and a 90–95% participation from whatever was left of the Greek creditor base.

That set the stage for the dramatic events of the night/early morning of October 25/26, 2011. Late night on October 25, the Greek restructuring team was told by the European authorities that it would have to restructure the Greek government bonds that remained in the hands of private investors (roughly EUR 209 billion), with at least a 50% principal haircut. At that point, however, there was reason to believe that a significant number of investors would have called that bluff. After all, Greece and the European authorities were still saying publicly that any restructuring would be “voluntary”. Hearing that message, private investors could be expected to decline to participate and to test whether European officialdom was truly prepared to “bring Argentina to the belly of Europe” (to quote one of our lawyer-respondents). Argentina, at this stage, was in the midst of a decade-long legal battle with holdout creditors – a battle that it was losing and that had essentially shut it out of international financial markets. What is more, Greek government bonds lacked the provisions that might have allowed a forceful use of the existing contractual techniques to bind reluctant creditor participation in a, by all appearances, huge debt write down.

The mandate to restructure Greek government bonds had been given on October 26, 2011, but it was also made clear that there would be no money in the Troika program to pay the EUR 14.4 billion bonds maturing on March 20, 2012. Yet Greek public finances were in such a dire state that if the debt write down was not completed within the next six months, Greece was certain to slip into outright payment default.

By this late stage, Jean Claude Trichet and the European Central Bank (ECB) had reluctantly acquiesced to the plan of a restructuring but their conditions were still that it must be “voluntary” and could not trigger a “credit event” or a “default”.

On its face, this was a mission impossible. One respondent explained: Trichet probably knew it to be an impossible ask. When the yields spiked temporarily after the infamous Deauville walk on the beach, Trichet was crowing like Peter Pan with his “I told you so” speech. I was pretty sure he was dusting off the same speech to give when Greek government bondholders did not “voluntarily” accept a 50 percent haircut with no threat of default if they rejected the offer.

To be sure, for those tasked with designing the restructuring in October 2011, there was nothing in the terms and conditions of a Greek government bond that would have allowed Greece to fashion a coercive exchange offer. And the inability even to threaten a payment default if holders rejected the offer removed the one tool that all sovereign debtors have invariably used to push reluctant creditors into giving debt relief.

How could Trichet’s requirement that neither a “default” on the bonds nor a “credit event” on the credit default swaps be triggered, be met while restructuring Greece’s bonds held by private investors? Eventually though, a combination of voices at the IMF and from Buchheit’s team persuaded policy makers that there could be a way forward by retrofitting Greek bonds with collective action clauses and that if a small number of credit default swaps on Greek bonds were to be triggered in the process, this was a risk worth taking. Indeed, it might make investors who held both bonds and CDS contracts more willing to vote in favor of a restructuring deal. There remained the question of how to do the deal in a voluntary fashion.

The Local Law Escape Route

Greece enjoyed one potential tool that had not been available to emerging market sovereigns in the last 30 years -- the local law escape route. The challenge for the architects of the debt restructuring, however, was how to use that weapon without blowing everything up. The fear was, as a respondent explained: If one accepted that the Greek Parliament had complete dominion over the fate of Greek law-governed Greek government bonds, the local law power was potentially thermonuclear. There were going to be spillover effects to the rest of Europe.

Early discussions explored different ways in which the local law power could be used. Suggestions included imposing a withholding tax on the bonds, or simply legislating a write down. European lawyers quickly raised two objections to these options. The tax solution probably would not be legally kosher unless it was imposed on all bonds, not just the Greek government bonds, and that would cause mayhem in the corporate debt market. As for legislating a direct 50% write down of the Greek government bonds, that would almost certainly have amounted to an unconstitutional “taking”, and would be a violation of Trichet’s “voluntary” requirement.

The challenge was how to make the restructuring with a substantial write off appear voluntary, while being coercive, and yet likely to survive legal challenges. One way to thread the needle was Lee Buchheit’s idea from May 2010, to retrofit a restructuring mechanism that would be subject to a vote within Greek bonds such that the restructuring would be binding on all bondholders, if a super majority of the bondholders agreed to the restructuring terms. This could arguably be portrayed as a voluntary restructuring given that a super majority of creditors had agreed to the deal. In addition, since these collective action super majority vote requirements had just been agreed to for all European sovereign debt starting on January 1, 2013, a court might conceivably not see the retrofit inclusion of these collective action clauses as expropriatory. These arguments were untested long shots, and as one respondent explained to us, would require some “magical thinking” from the judge. But if, by the time the matter got to court, the debt crisis had been successfully resolved, courts would be more open minded and loath to reverse the move for fear of unleashing a global financial crisis.

The fly in the buttermilk was that a set of investors – anticipating that Buchheit might attempt to implement his May 2010 retrofit idea with a common vote requirement for CACs of 75% (in principal amount) – were rumoured to have purchased 25% blocking positions in the bonds coming due in March 2012. And Greece neither had, nor was going to receive from the European authorities, the funds needed to pay those March 2012 maturing bonds in full.

One of our Official Sector respondents explained: It is indeed very important that you focus on the payment that was coming due on March 20, 2012. It was a huge source of concern for both Greece and the IMF. There was no money in the program for that payment to be made – but at the same time there was a very strong desire to avoid a payment default. As noted, in the [IMF] staff [paper that argued] for aggregated CACs, we were concerned that investors were purchasing these bonds with a view to using leverage to be excluded from the restructuring altogether - or getting better terms. Although this is speculation, I think they assumed that the retrofit CAC would be bond-by-bond – meaning that as long as they acquired a controlling position, they would be in the driver’s seat.

4

The Need for a Lower Threshold

Given the concern that holdouts had accumulated blocking positions, the strategy had to be changed at the last minute with a different retrofit than the standard CACs. And it had to be changed quietly so that the speculators who had possibly purchased blocking positions could not respond in time to the change. The problem in moving away from the 75% vote requirement though was that this was the market standard for CACs. And arguing that what Greece had done was nothing more than embracing the market standard was a key supporting argument in Buchheit’s original May 2010 proposal; one that could be invoked by lawyers in court to defend the inevitable lawsuits challenging the legality of the retrofit.

At this point though, Buchheit was no longer actively managing the design of the restructuring. He was undergoing medical treatment for cancer that had been diagnosed a few months prior. The latest that the doctors allowed him to postpone the treatment to was January, so the reigns of the restructuring were handed over to his junior partners, Andrew Shutter and Andres de la Cruz in January 2012. Buchheit was, as Financial Times reporter, Robin Wigglesworth writes, unable to even respond to emails: [Buchheit] admit[ted] the pain was so “incandescent” that at one point he warned his colleagues that there might come a point where he would be under so much medication that he could no longer trust his own judgment. “When that time approaches,” he told them, “I’m going to send you an email and say, from here on out you may get emails from me, but feel free to ignore them because I can’t promise you that I shall be thinking clearly (Wigglesworth, 2019).”

Dealing with the reality of the potential holdouts therefore was left to de la Cruz and Shutter through February and March 2012.

Things get a murky here in our story because we have heard multiple conflicting versions about how the ultimate vote threshold to be inserted through the retrofit was determined and why it was not the 75% bond-by-bond requirement that Buchheit had suggested in 2010.

Ultimately, the decision was made to use a 66.67% required majority vote, via a bankruptcy style class-voting mechanism where all the Greek bonds were put into a single giant class, a radical form of aggregation. One version of the story we heard from some of the Greek participants is that this was what the Greek legislature was comfortable with; it was basically their corporate bankruptcy scheme. Another version, and here the sources were American, was that this was the class voting threshold for approving a plan of reorganization for a corporate entity under Chapter 11 in the US. And the third version was that this was a last-minute decision made without great thought other than to use a mechanism that would ensure that the vote would go through successfully, so that Greece would not face the immediate prospect of being ejected from the Eurozone. Legal risks would be dealt with in the future. One participant in the final decisions explained: The documents essentially had a blank space for the final vote requirements. We used what we had to in order to get the deal done. There was no time to think about whether a court would uphold this in the future. That was not our job to worry about. All of this discussion of borrowing from chapter 11 or the Greek bankruptcy code strikes me as revisionist history. Maybe it was in the heads of some people, but there was little discussion of it that I remember. We did what we had to do – thank heavens it worked.

A couple of our sources suggested that using the vote requirement from the bankruptcy code had a better chance of being upheld than some other random vote threshold. But we are not sure why anyone involved thought that any future European court would care that the threshold in question had been borrowed from the US bankruptcy code for corporations or the Greek one. This was a sovereign, after all, not a corporation – and no judge was going to be confused about that.

Regardless of the reason, 66.67% was the final required vote the Greek legislature retrofitted into all the Greek government bonds. And this was a 66.67% vote requirement across all the Greek government bonds, not an individual bond by bond vote requirement as was standard for CACs in other sovereign bonds at the time. There was also a quorum requirement (50%) that ended up not mattering since there was overwhelming participation. What was key was that, given the final choice of strategy by Greece, holding out was in effect impossible now – since none of the relevant hedge funds had the funds required to acquire a blocking position.

One respondent explained: In the Buchheit article [of 2010], he had referred to retrofitting CACs into existing bonds. He had not suggested retrofitting a class voting mechanism on the entire universe of Greek law-governed Greek government bonds since a key element of his argument had been that what he was suggesting was reasonable because it was just using the market standard mechanism, the CAC. But some hedge funds had taken him literally. Those funds purchased positions in the EUR 14.4 billion Greek government bonds maturing on March 20, 2012, that would have allowed them to block the use of a conventional CAC had one been retroactively inserted in that bond. With the class voting mechanism, however, that strategy misfired, expensively, for the hedge funds involved. The Eurogroup (of Eurozone finance ministers) did not approve using this technique until the night before the offer was launched. There were several reasons for their reluctance – a general uneasiness with ex post facto changes to contracts; a question about whether this technique was consistent with the word “voluntary”; and concerns that the technique was open to legal challenge. When the offer was launched, however, the Troika made it clear that holders of at least 90 or maybe 95 percent of the eligible Greek government bonds would need to participate for the latest rescue package for Greece to go forward. That was an impossibly high threshold to reach without the retrofit class voting mechanism.

We asked all our respondents the question of how concerned participants had been about potential legal challenges to the retrofit. We had imagined that this was probably one of their central concerns. Only a handful of them thought that this had been an issue at all, let alone a big concern. Everyone expected that there were likely to be legal challenges, but no studies were commissioned to predict the outcomes of litigation in different European courts and to think about how to modify the original Buchheit plan to minimize legal risk. 5

Best we can tell, legal risk was largely irrelevant to the design of the final details of the Greek retrofit strategy such as the voting thresholds. In contrast to how legal scholars often frame strategy choices in such dramatic situations, where careful consideration is given to the risk that a court could block key parts of a prospective deal, here that risk was essentially out of the equation in the final critical deliberations. This was not because there was no legal risk. Everyone knew there was legal risk; and, if they did not, creditors were making sure they did by promising litigation. It is just that the choice of final parameter values was overdetermined by political dictates – to get the deal done on something that could be articulated as voluntary, and for the amount of debt relief from private creditors that was politically required. The instructions from politicians were to achieve certain immediate goals. Legal risks would materialize in the future and would likely be someone else’s problem. Further, if the deal was a success in rescuing Europe from this existential crisis, perhaps the courts would find it difficult, if not impossible, to reverse.

Were There in Fact Negative Spillovers?

In this section, we report on whether the retroactive modification of local law Greek sovereign bonds by the Greek legislature, with the approval of the European authorities and the IMF, had negative spillovers on the European sovereign debt market. If the authorities were willing to take these actions vis-à-vis Greece, surely they would be willing to do the same for any other European nation that hit a similar crisis in the future. European sovereign bonds after March 2012, one might say, could no longer be viewed as risk free. At least, that was the fear of many senior European policy makers in 2010–2012 and it arguably resulted in their delaying the Greek restructuring long beyond the point at which it was clear that Greece’s debt was unsustainable.

We build on Bolton et al. (2021) and use the event study approach to test whether there is evidence that European governments vulnerable to a similar use of the retrofit technique faced an increase in borrowing costs after the passage of the Greek Bondholders Act and following court decisions that upheld the retroactive modification of the local law Greek sovereign bonds by the Greek legislature. 6 We start by discussing the methodology and data and we then describe our results.

To test for possible spillovers, we match bonds with similar remaining maturity issued by the same sovereign under different legislations. Specifically, we match bonds issued under domestic law with bonds issued under New York or English law. Given that the two types of bonds are subject to the same type of sovereign risk but only local law bonds are subject to the legal risk of a retroactive legal change to its terms, negative spillovers from the Greek restructuring should be reflected in an abnormal increase in the spread of domestic law bonds in the aftermath of unexpected events which are deemed to weaken creditor rights for bonds issued under domestic law.

Bonds Included in the Sample.

We start by defining

In the second step, we use the parameter estimates of equation (1) to obtain excess (“abnormal”) changes in spreads as out-of-sample forecast error (i.e., by subtracting the out-of-sample predicted values from the actual changes during the event window) and compute cumulated abnormal spreads by adding the excess spreads over time during the event window. We conduct this exercise using a 6-day event window, starting one day before the event and ending 4 days after the event. Note that we only retain bond-pairs and episodes for which the estimation of equation (1) gives a good fit (specifically, we drop all pairs for which the F statistics of equation (1) is not significant at the 10% confidence level).

Defining the abnormal change in spread as:

A positive value of

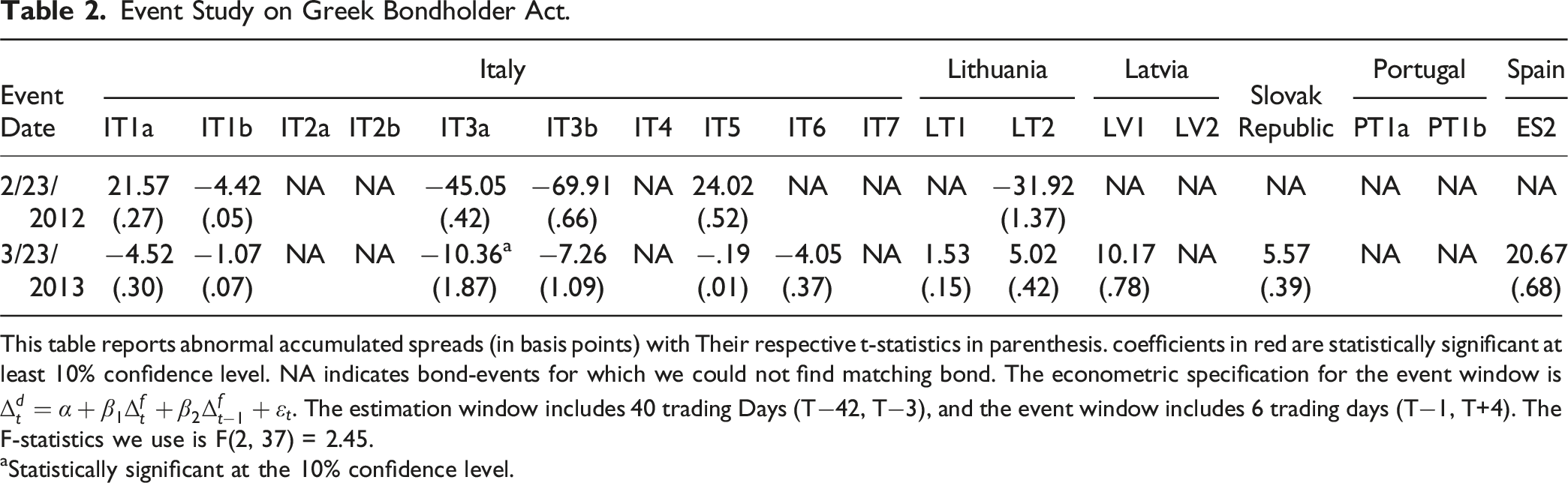

In terms of events, we first study what happened in the aftermath of the approval of the Greek Bondholder Act of March 2012 and then the focus on court decisions which upheld the validity of the Act. The story we tell in Section II suggests that there were elements of surprise in all of these. With the Greek Bondholder Act, the form of the retrofit (using aggregated voting) ended up being more extreme than had been originally planned—a strategy change that had to be made at the last moment to outfox creditors with bonds maturing in March 2012 who were seeking to hold out. With the local Greek courts, in front of whom the next set of cases came, whose decisions some might have expected to be sympathetic to the Greek government, the fact that many Greek citizens and institutions were taking big losses in the 2012 restructuring cut the other way. Finally, there were the cases that were brought in foreign and international courts where there was little reason to expect any special sympathy for the Greek government. In a number of those tribunals, one might have expected some sympathy to run the other way since the creditor-plaintiffs were citizens of the nations in whose courts the cases were being adjudicated.

Inasmuch as there was uncertainty about the outcomes of these cases, these rulings were a “surprise” for the market and they allow us to conduct multiple event studies that examine the European sovereign debt market reactions to these decisions. That uncertainty about outcome is revealed in the numerous lawsuits that were threatened, and then filed, soon after the restructuring (White and Sassard, 2012; Wilson & Weismann, 2012).

Drawing from the legal literature (Belle, 2020; Grund, 2017; Iverson, 2019; Manuelides, 2019), we focus on the Greek Bond holders act and 10 key rulings on the multiple challenges that investors brought against the Greek government’s actions in Greek and foreign sovereign courts, European courts, and arbitration tribunals. Three of these rulings were rendered by Austrian courts, four by German courts, one by the International Centre for the Settlement of Investment Disputes, one by the European Court of Human Rights, and one by the Greek Council of State. Specifically, we focus on the following events and dates: I. II. III. IV. V. VI. VII. VIII. IX. X. XI.

Event Study on Greek Bondholder Act.

This table reports abnormal accumulated spreads (in basis points) with Their respective t-statistics in parenthesis. coefficients in red are statistically significant at least 10% confidence level. NA indicates bond-events for which we could not find matching bond. The econometric specification for the event window is

aStatistically significant at the 10% confidence level.

It could be claimed that, being decisions by national authorities, the events described in Table 2 were not true surprises suitable for an event study. We do not think that to be case, given the narrative in Part II – and the form of the Greek Bondholder Act itself. Nevertheless, one can make the argument that foreign courts were a lot less likely to show sympathy for the Greek government’s actions than Greek courts and, therefore, their decisions were more surprising. Hence, we now turn to decisions by foreign courts.

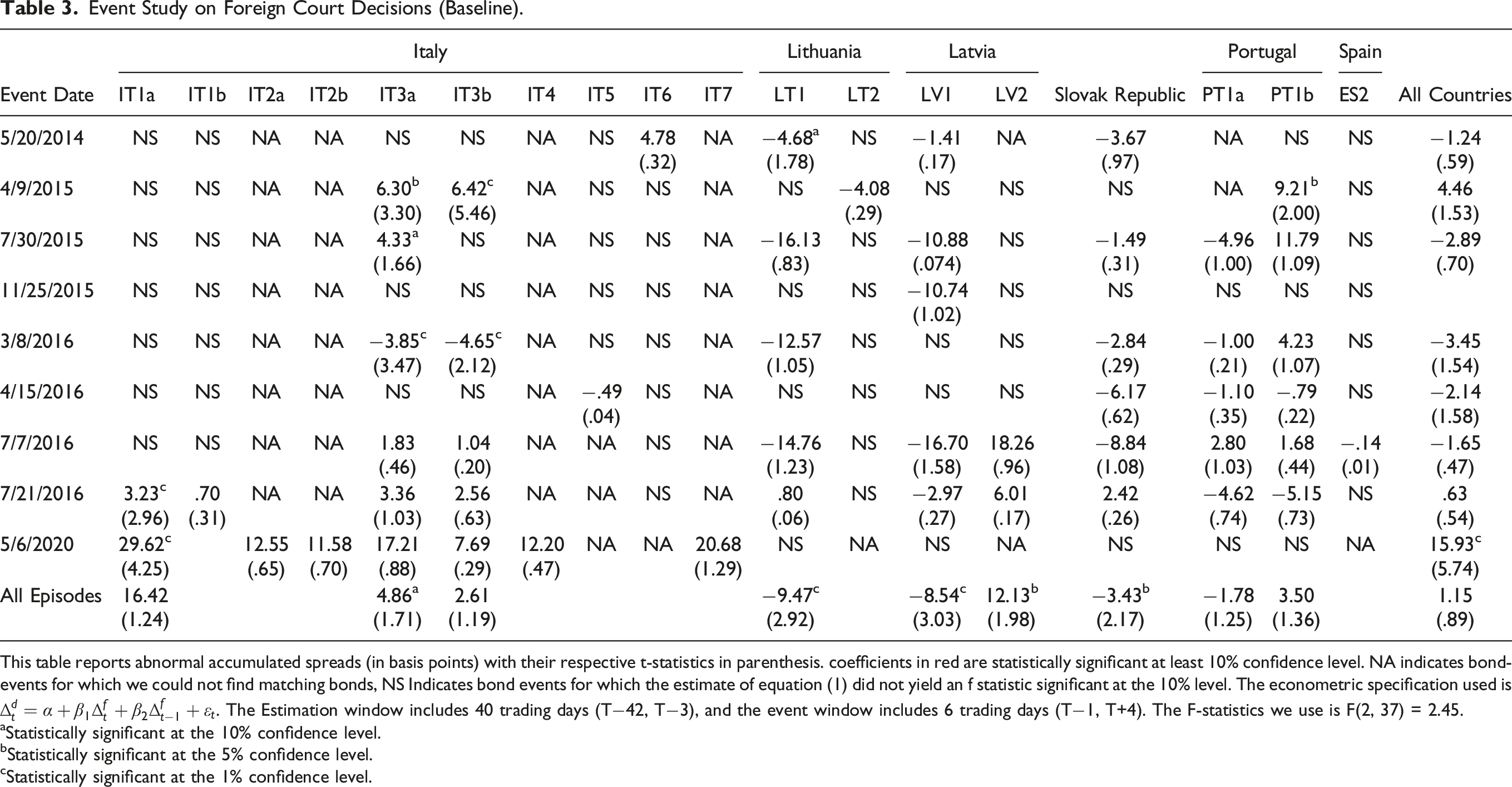

Event Study on Foreign Court Decisions (Baseline).

This table reports abnormal accumulated spreads (in basis points) with their respective t-statistics in parenthesis. coefficients in red are statistically significant at least 10% confidence level. NA indicates bond-events for which we could not find matching bonds, NS Indicates bond events for which the estimate of equation (1) did not yield an f statistic significant at the 10% level. The econometric specification used is

aStatistically significant at the 10% confidence level.

bStatistically significant at the 5% confidence level.

cStatistically significant at the 1% confidence level.

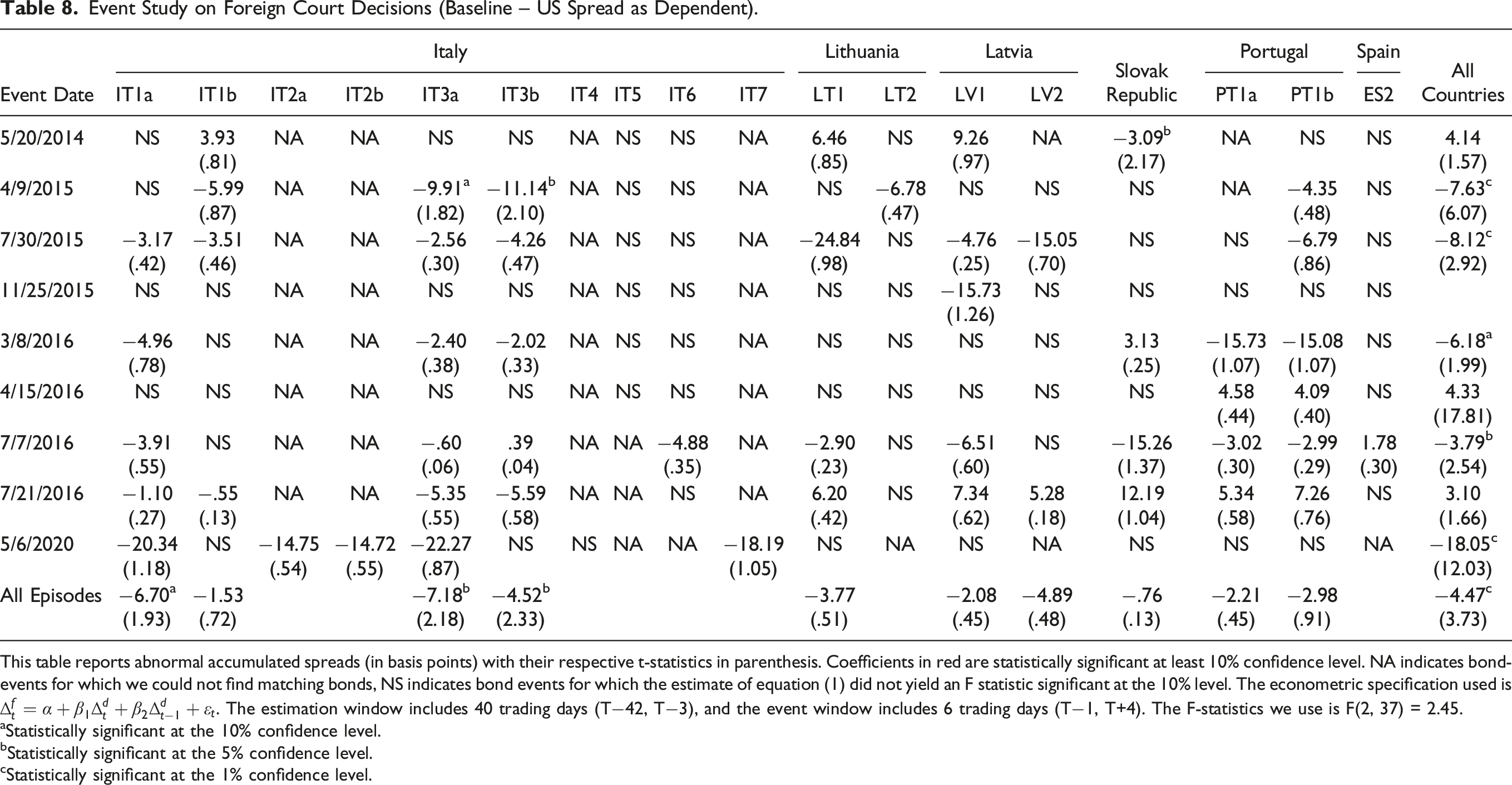

Out of 50 bond-event pairs for which we have data on abnormal spreads, only 6 are positive and statistically significant, while two are statistically significant and negative. These positive coefficients are for the ICSID ruling of April 9, 2015 (two Italian Bonds and one Portuguese bond), the Austrian Supreme Court ruling of July 30, 2015 (one Italian Bond), the European Court of Human Rights of July 21, 2016 (one Italian bond) and the German Federal Constitutional Court of May 6, 2020 (one Italian bond). Note that even for these 6 bond-event pairs with positive and statistically significant abnormal accumulated spreads, the effects tend to be small. In most cases, they range between 3 and 9 basis points, and only in one case they are close to 30 basis points.

The two estimates with negative and statistically significant excess returns (indicating that a specific court decision led to a reduction of borrowing costs) are for Italian bonds and are associated with ruling of March 8, 2016 by the German Federal Court of Justice. In this case, we also find a small effect ranging between 4 and 5 basis points.

Considering the joint tests of the bottom row, we find 5 statistically significant abnormal returns (out of ten for which we have data). In two cases (one for Italy and one for Latvia), our estimates indicate positive abnormal accumulated spreads and in three cases (one for Lithuania, one for Latvia, and one for the Slovak Republic), they indicate negative abnormal accumulated spreads. In all cases, the abnormal accumulated spreads are small, ranging between −9 and 12 basis points.

The last column shows that the only event that had a significant impact on bond spreads was the May 6, 2020 decision by the German Federal Constitutional Court, but the cell at the bottom right corner of the table shows that if we jointly consider all events and bonds for which we have data, we obtain a small (1.1 basis points) and not statistically significant coefficient.

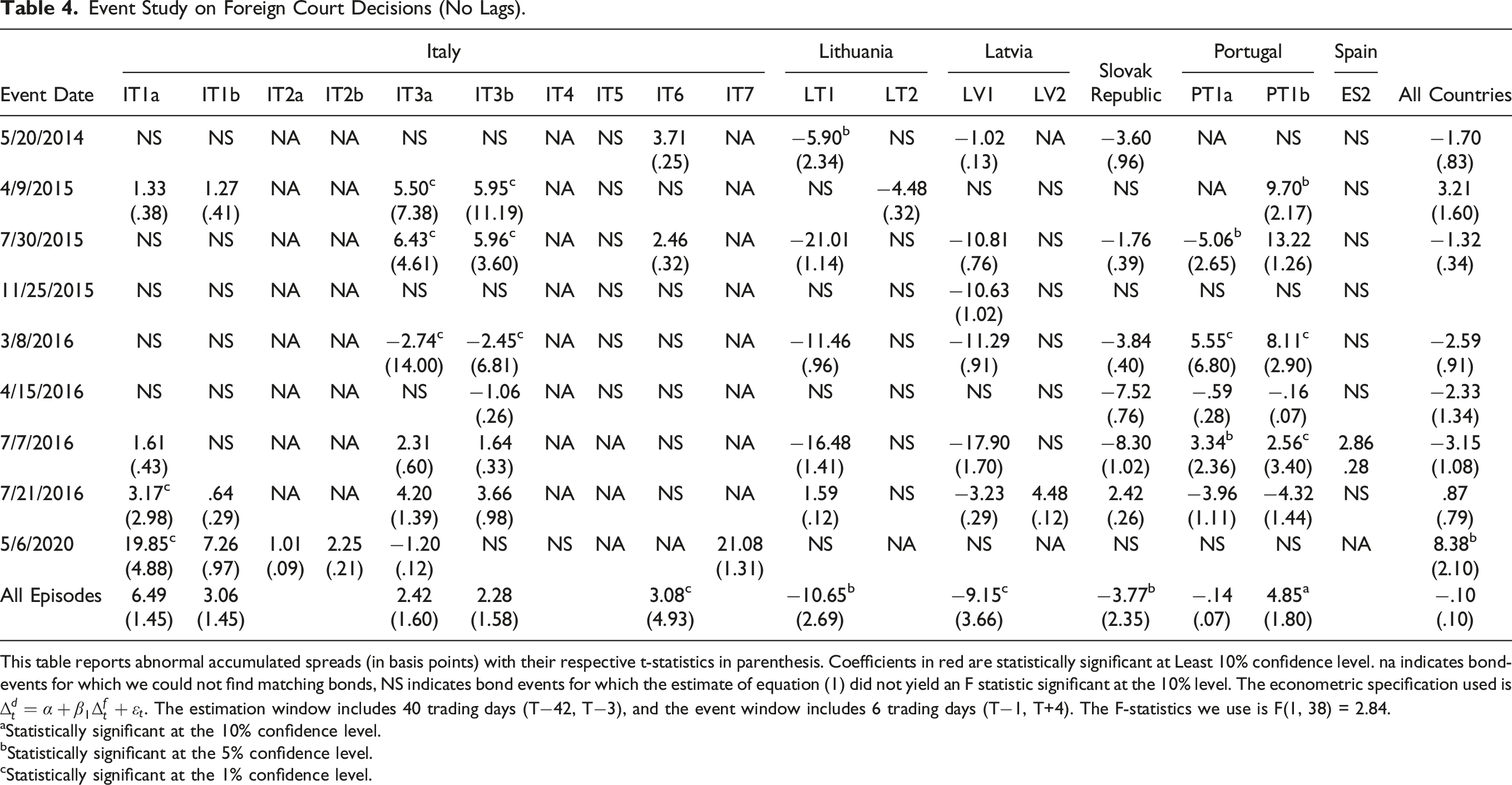

Event Study on Foreign Court Decisions (No Lags).

This table reports abnormal accumulated spreads (in basis points) with their respective t-statistics in parenthesis. Coefficients in red are statistically significant at Least 10% confidence level. na indicates bond-events for which we could not find matching bonds, NS indicates bond events for which the estimate of equation (1) did not yield an F statistic significant at the 10% level. The econometric specification used is

aStatistically significant at the 10% confidence level.

bStatistically significant at the 5% confidence level.

cStatistically significant at the 1% confidence level.

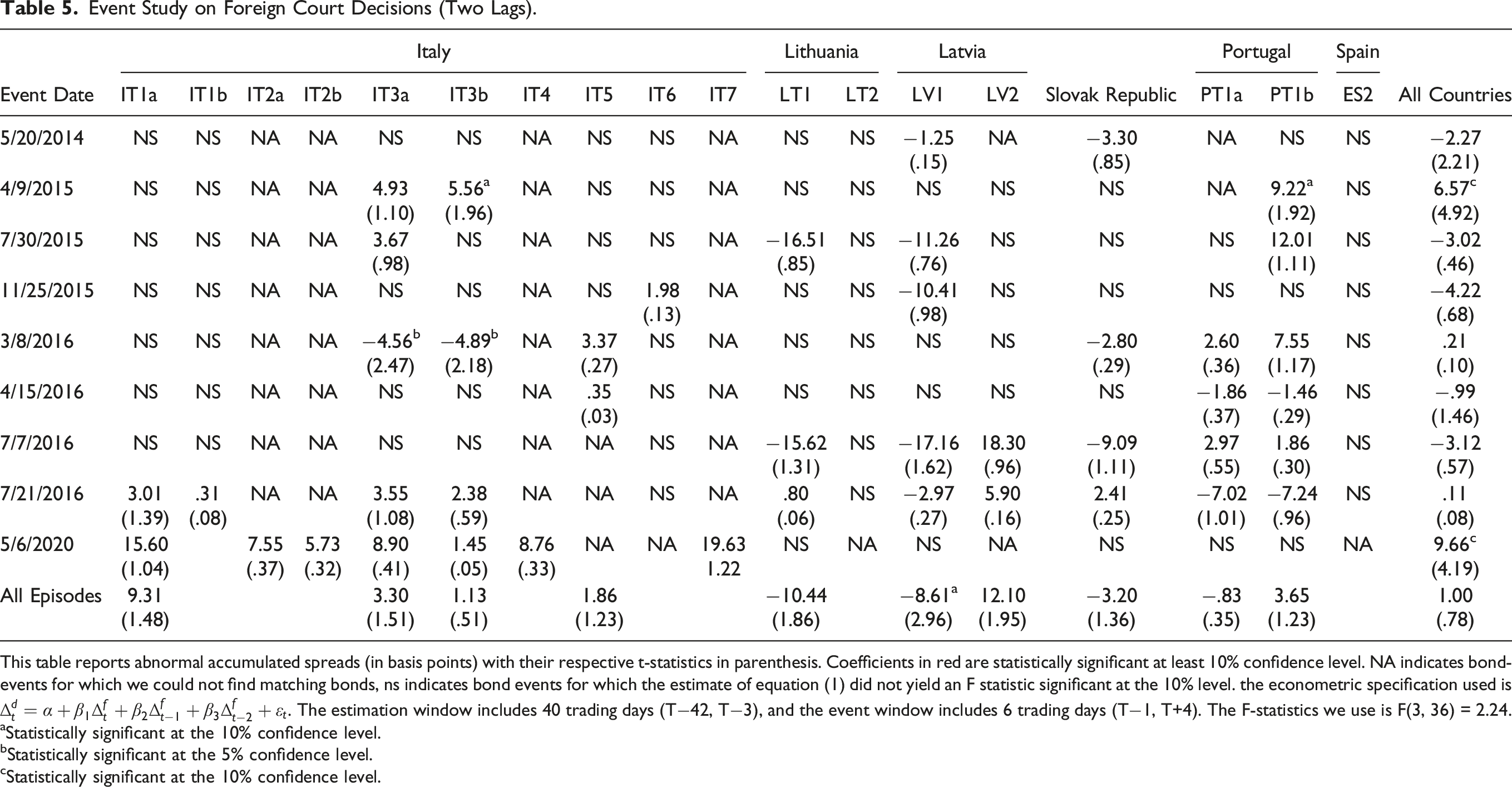

Event Study on Foreign Court Decisions (Two Lags).

This table reports abnormal accumulated spreads (in basis points) with their respective t-statistics in parenthesis. Coefficients in red are statistically significant at least 10% confidence level. NA indicates bond-events for which we could not find matching bonds, ns indicates bond events for which the estimate of equation (1) did not yield an F statistic significant at the 10% level. the econometric specification used is

aStatistically significant at the 10% confidence level.

bStatistically significant at the 5% confidence level.

cStatistically significant at the 10% confidence level.

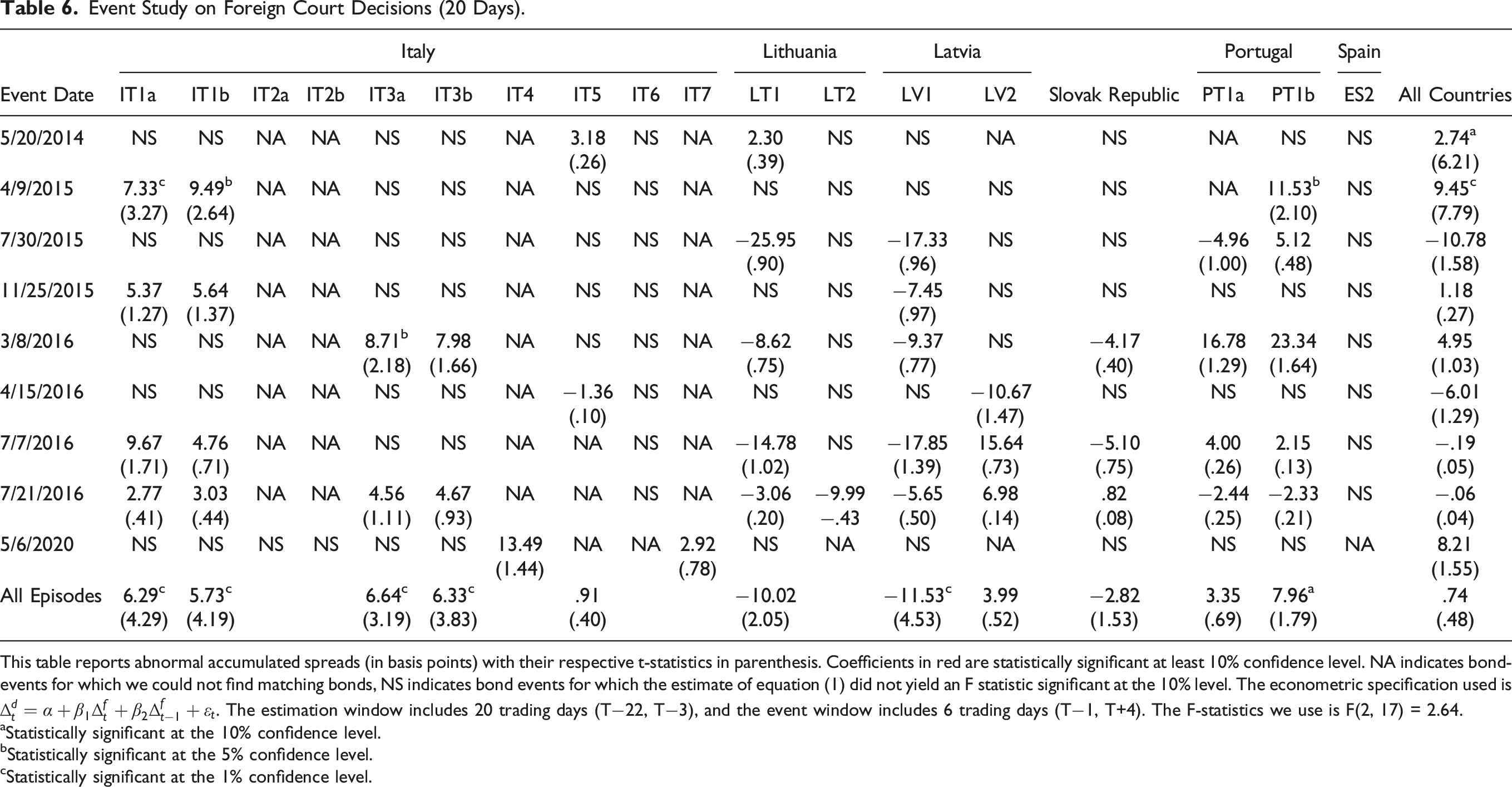

Event Study on Foreign Court Decisions (20 Days).

This table reports abnormal accumulated spreads (in basis points) with their respective t-statistics in parenthesis. Coefficients in red are statistically significant at least 10% confidence level. NA indicates bond-events for which we could not find matching bonds, NS indicates bond events for which the estimate of equation (1) did not yield an F statistic significant at the 10% level. The econometric specification used is

aStatistically significant at the 10% confidence level.

bStatistically significant at the 5% confidence level.

cStatistically significant at the 1% confidence level.

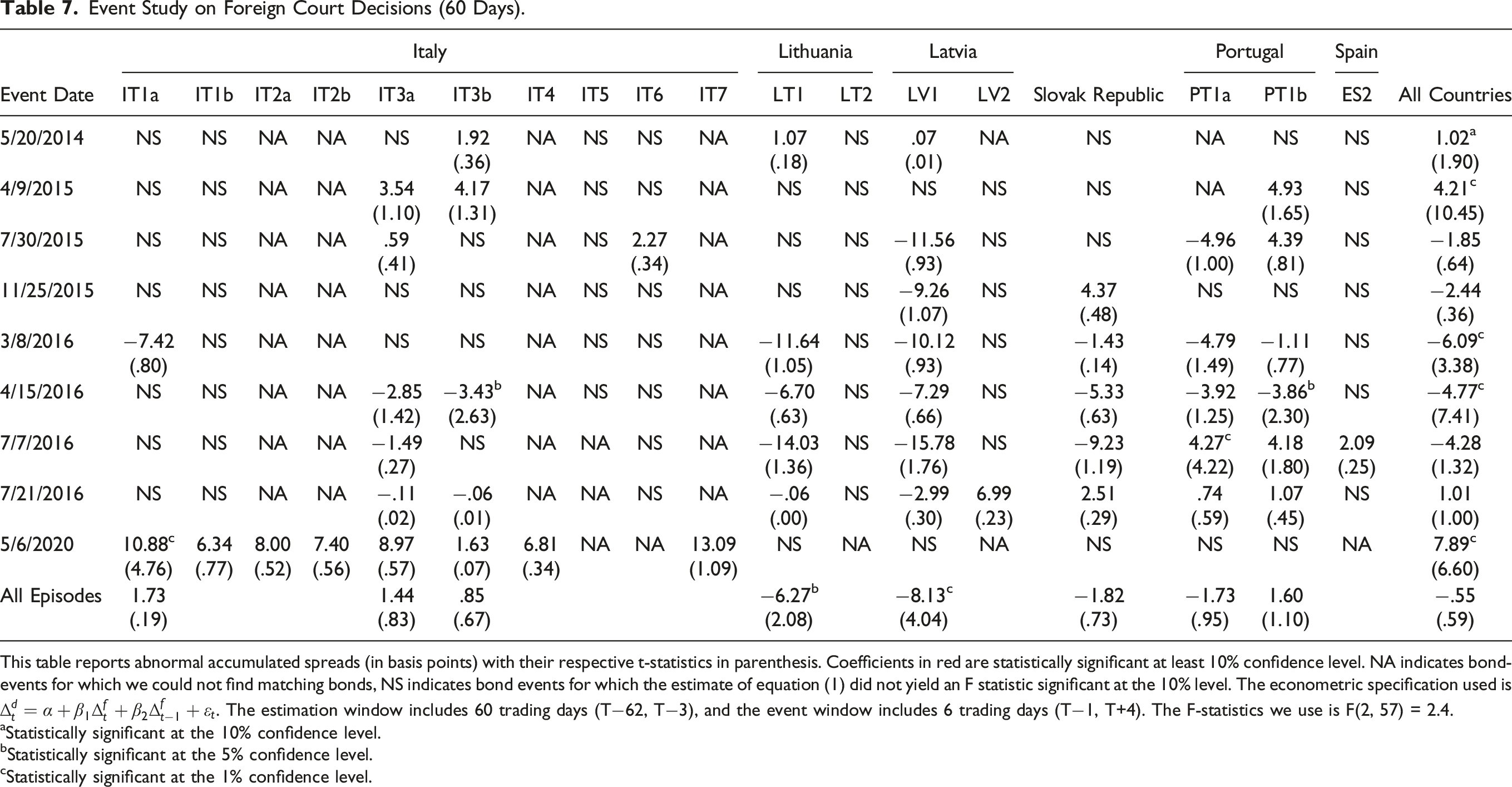

Event Study on Foreign Court Decisions (60 Days).

This table reports abnormal accumulated spreads (in basis points) with their respective t-statistics in parenthesis. Coefficients in red are statistically significant at least 10% confidence level. NA indicates bond-events for which we could not find matching bonds, NS indicates bond events for which the estimate of equation (1) did not yield an F statistic significant at the 10% level. The econometric specification used is

aStatistically significant at the 10% confidence level.

bStatistically significant at the 5% confidence level.

cStatistically significant at the 1% confidence level.

Event Study on Foreign Court Decisions (Baseline – US Spread as Dependent).

This table reports abnormal accumulated spreads (in basis points) with their respective t-statistics in parenthesis. Coefficients in red are statistically significant at least 10% confidence level. NA indicates bond-events for which we could not find matching bonds, NS indicates bond events for which the estimate of equation (1) did not yield an F statistic significant at the 10% level. The econometric specification used is

aStatistically significant at the 10% confidence level.

bStatistically significant at the 5% confidence level.

cStatistically significant at the 1% confidence level.

Conclusions

In the case of the Greek retrofit we find that the incomplete contracts view dominates the creditors’ rights view. That is, the markets did not view the Greek restructuring of 2012 as having fundamentally weakened their contractual rights. Neither what was done by the Greek legislature, nor what the courts decided subsequently, was viewed by the markets as a big negative event as was predicted by many.

The implications are significant, if we think that European policy makers delayed putting in place a debt restructuring for Greece because of a fear of a negative market reaction. If that fear was unjustified, it means that Greece – for almost 2 years – was unnecessarily paying creditors on time and in full with money it did not have and was later going to be extracted from European taxpayers.

More broadly, it is worth reflecting also on similarities between this story from 2012 and the abrogation of the gold clauses by the US in 1933 – the fears of negative spillovers from retroactive legal changes were largely the same (Edwards, 2018; Kroszner, 1998). To the extent those fears caused delays to desperately needed restructurings, those are deadweight losses borne by the populace.

The foregoing is not meant to suggest that there are not cases where the strategies used in restructurings do not constitute such an abrogation of creditor rights that the market does impose a penalty. There surely are (e.g., Colla and Gulati, 2022). The point is that it is not always going to be the case that a retroactive change in law, that abrogates certain creditor rights, will be seen by the market as an unmitigated disaster.

It is worth noting too that the Greek retrofit was not wholeheartedly embraced by investors. In the period between March 2012 and this writing, in August 2023, Greece itself, when it has had to go back to the debt markets in the wake of the 2012 restructuring, has only been able to issue foreign-law bonds. Even though Greek borrowing rates in 2023 are lower than a number of other Euro area nations such as Italy, the market is not been willing to accept Greek local-law sovereigns bonds (McDougall & Arnold, 2023). The point though is that neither the choice of the European authorities and the Greek legislature to use the retrofit strategy to deal with the crisis, nor the choice of the various adjudicatory bodies to uphold the legality of the retrofit, caused an increase in borrowing costs for other vulnerable European countries. 10

To close, a banker, who advises sovereign restructurings, and was one of the last interviews we did in July 2023, mused, as the end of conversation: There might have been a sense, after the success of the Greek retrofit – the use of the “local law advantage” that this would become the standard technique to restructure sovereign debt under local law. But I’ve seen at least two governments resist this option recently. It didn’t even get to the legislature. The Attorney General didn’t like it. Rule of law and domestic constitutional concerns come up. This has not become standard practice.

11

Footnotes

Acknowledgments

Thanks to participants to the 2022 ASSA meetings, John Cochrane, Lee Epstein, Anna Gelpern Jeromin Zettelmeyer, Christoph Trebesch, George Vanberg and Mark Weidemaier for comments, memories and suggestions. We owe a special debt to the forty-one bankers, lawyers, policy makers and journalists who shared with us their memories of the Greek retrofit. Panizza gratefully acknowledges financial support from the Swiss Network for International Studies (SNIS) under the grant “Sovereign Debt in the Aftermath of the Pandemic: Improving Data to Prevent Debt Crises.”

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.