Abstract

Drawing on the case of Chinese companies’ overseas listings on US stock exchanges, this study unpacks the geography and network structure of China’s integration into global financial networks (GFNs) by taking a city network approach based on inter-firm service and collaboration linkages. The results show that New York and Hong Kong are the dominant international financial centres facilitating this process. The Cayman Islands and British Virgin Islands are the key offshore jurisdictions in which the Chinese companies are incorporated. Beijing, Shanghai, and Shenzhen are more likely to be connected with GFNs than other cities in mainland China. The financial and business service firms involved in the overseas listings are mostly located in these cities. These strategic nodes have varied functions in GFNs. Several key city-dyads within the networks are identified, which further indicates the importance of those strategic nodes mentioned above. Despite the growing importance of Chinese firms and financial centres within GFNs, the continuing integration of China’s economy via overseas listings on US stock exchanges has strengthened rather than challenged the existing global financial order dominated by the west.

Keywords

Introduction

In the past decades, a considerable literature has grown up around the theme of the dynamic interactions between local economies and an increasingly globalised economy (Bathelt et al., 2004; Brenner, 1999; Coe et al., 2004; Yeung, 2009). Meanwhile, beyond the traditional research focus on production issues, finance is endowed with increasingly great significance in such interactions, given its centrality in capitalism as well as its globalised and networked nature (Coe et al., 2014; Lee et al., 2009; Sokol, 2013).

In this context, the global financial network (GFN) framework is coined for analysing the dynamics of regional economies’ integration into the global financial system (Coe et al., 2014; Wójcik, 2018). It argues that via establishing financial linkages with financial centres and offshore jurisdictions around the world, many local economies connect themselves with GFNs. To be specific, the GFN framework has identified the network actors, e.g., financial and business service (FABS) firms, and the associated geographical units, e.g., financial centres and offshore jurisdictions, at the heart of the analysis of global finance and economy.

While the GFN framework provides an analytical tool to map and place finance in the world economy, its theoretical advancement also hinges on the enrichment of related empirical studies (Coe et al., 2014). Established accounts have drawn on the data of global FDI (Haberly and Wójcik, 2015a, 2015b) or some high-end financial transactions (Gemici and Lai, 2020; Wójcik et al., 2021, 2022) to unpack certain structures of GFNs. However, only very few of them could provide fine-grained analysis at the city level (Wójcik et al., 2022). Moreover, such accounts majorly take account of the rather stabilised landscape of global finance as a whole, while being less attentive to the dynamic processes of local economies’ integration into GFNs. Methodologically, limited by the standard data insufficiency, there is not a widely applicable way to quantitatively analyse such processes.

To fill this gap, this paper adopts a new strategy of quantifying the spatial and network structure of GFNs based on the case of overseas listings. Overseas listings refer to the listing and trading of corporate shares on stock markets outside of the home country of the issuer, which represents an important way to integrate local economies into the global financial market (Pan, 2020; Wójcik and Camilleri, 2015). From a GFN perspective, such a critical process is enabled by a global network of FABS, and in turn, shapes a networked landscape of global finance with some interconnected strategic places including international financial centres and offshore jurisdictions. To be specific, varied FABS firms such as investment banks, accounting, and law firms provide crucial services for companies to go public. Geographical units including international financial centres and offshore jurisdictions provide vital financial infrastructures such as stock exchanges and complicated financial vehicles. Following the strategy of converting inter-firm service provision and collaboration relations into spatial linkages (Pan et al., 2017, 2020a), it is possible to majorly draw on valid data sources like company prospectuses to quantitatively analyse overseas listings and the therefore formulated GFNs.

Emerging economies like China have been mobilising overseas listings on leading international stock exchanges as an important strategy in developing their domestic economies (Pan and Brooker, 2014; Peck and Zhang, 2013; Wójcik and Burger, 2010; Zhang and Peck, 2016). Since the 1990s, a growing number of Chinese companies have been successfully listed on international markets (Claessens and Schmukler, 2007; Karreman and van der Knaap, 2012; Yang and Lau, 2006), and New York has been one of the most important destinations (Pan and Brooker, 2014). The two major stock exchanges in New York, NASDAQ and NYSE, are viewed as the most established and globalised stock markets worldwide (Pan, 2020), and hold a privileged central position in global finance (Wójcik, 2013a). As of 2020, over 300 Chinese companies, including many high-profile Chinese companies such as China Mobile, Alibaba, and NIO, were listed on those two stock exchanges in New York. While previous studies foreground the critical role of some transnational FABS firms and financial centre cities in integrating China’s economy into the global financial market (Wójcik and Burger, 2010; Pan et al., 2018), little is known about the geographical trajectory and network structure. In the substantive context of Asia’s recent rise in GFNs (Wójcik, 2013a; Lai et al., 2020), it is necessary to better examine China’s integration and its impact on the global financial landscape. Drawing on the method mentioned above, this study investigates the spatial and network structure of Chinese companies’ overseas listings on US stock exchanges.

This paper contributes to existing literature threefold. First, it introduces a new strategy to quantitatively analyse the city networks formed by local economies’ integration into GFNs. Second, while established accounts mainly take accounts to the geographies of financial markets and financial intermediaries (Faulconbridge, 2019; Haberly et al., 2019; Pažitka and Wójcik, 2019; Gemici and Lai, 2020), this study incorporates the analysis of the recipient ends of financial services, in our case, the Chinese US-listed companies and their located cities/regions. Such an approach connects GFNs with broader regional development issues under financial globalisation (Pan et al., 2020b). Third, this study unpacks the spatial and network structure of GFNs formed by Chinese companies’ US listings, and identifies several strategic nodes and leading city-dyads.

The remaining part of the paper proceeds as follows: the next section reviews the established accounts on GFNs and overseas listings to ground our case study. The third section explains our data sources and the method used for this study. In the fourth section, we present an analysis of the geography of Chinese companies’ US listing, highlighting listed company origins, their incorporation places, and the locations of the associated FABS firms as an important geographical trajectory of China’s global financing. The fifth section maps the service and collaboration networks formed in the process and analyses the therefore formulated GFN structure. The final section concludes and gives an outlook.

Understanding the spatial and network structure of GFNs shaped by overseas listings

Key geographical units

International financial centres: overseas listing destinations

Financial centres are at the geographical intersection of various global financial activities, as well as agglomeration of a broad range of institutions related to finance. From a network perspective, financial centres are those highly connected nodes in GFNs shaped by FABS activities (Wójcik, 2018). In reality, international financial centres are destinations of overseas listings and are at the heart of GFNs formed therefrom (Pan, 2020).

Several leading international financial centres, such as New York, London, and Hong Kong, stand out as the most attractive destinations for overseas listings (Wójcik and Burger, 2010; Pan et al., 2018). On the one hand, these leading centres are well equipped with more sophisticated FABS to garner efficient corporate financing from worldwide investors. On the other hand, going public in leading international financial centres can be attractive for eligible companies, with obvious benefits including good liquidity and enhancement of visibility and reputation, especially for those companies from developing economies (Wójcik and Burger, 2010).

Although there is a preference for geographical and cultural proximity in the choice of overseas listing destinations (Ghadhab and Hellara, 2015; Pan and Brooker, 2014), the listing rules and regulatory policies from the host markets are also key factors (Claessens and Schmukler, 2007; Hornstein, 2014; Pan and Brooker, 2014). International financial centres and stock exchanges are competing to attract potential issuers from overseas, in order to increase profits and enhance their reputation (Wójcik, 2011: 60). Those financial centres hosting more and larger overseas listings usually hold more prominent status in GFNs.

Offshore jurisdictions: incorporated places for the overseas-listed companies

Several studies point to the importance of offshore jurisdictions in facilitating global finance activities (Haberly and Wójcik, 2015a; Palan et al., 2013; Sigler et al., 2020; Wójcik, 2013b). Transnational companies and financial institutions often use offshore jurisdictions for a variety of purposes including tax avoidance, offshore secrecy, and regulatory evasion (Hudson, 2000; Zoromé, 2014). Some critics argue that offshore jurisdictions are outside the scope of global financial regulation, and have a negative impact on the increasingly globalised world economy (Wójcik, 2013b; Palan and Nesvetailova, 2014). Typical offshore jurisdictions like the Bermuda, the Cayman Islands, and Delaware usually come with low tax rates, light and flexible incorporation regulatory frameworks, and good secrecy (Palan et al., 2013; Wójcik, 2013b). Since the boundary between offshore jurisdictions and traditional financial centres is becoming increasingly blurred (Clark et al., 2015), some international financial centres like Hong Kong and Singapore also perform the similar functions as other typical offshore jurisdictions.

As the incorporation places of many overseas-listed companies, the offshore jurisdictions also house numerous FABS firms that deal with the relevant transactions. In particular, the law firms handling legal issues to comply with the laws in the offshore jurisdictions and relevant regions are critical.

Origins of the overseas-listed companies

Despite that the prevailing accounts on GFNs put much emphasis on the geographies and networks of financial institutions or financial centres, little attention has been paid to the broader geographies of the cities/regions connected with GFNs. This foregrounds our initiative to incorporate the analysis of the regions in need of financing in the empirical analysis of GFNs. First, while the established accounts tend to place a narrow focus on a handful of top financial centres in GFNs such as New York and London, there is a call for investigating of local economies’ integration into GFNs as it could bring other rather peripheral cities and regions into view (Fang et al., 2022). It is noteworthy that in the past 30 year or so, some of these peripheral cities and regions are connected with GFNs via overseas listings (Pan and Brooker, 2014; Wójcik and Burger, 2010) and gaining increasing importance in GFNs’ dynamics. Second, as the receiving ends where international financial capital flows into, the cities and regions integrated into GFNs may benefit by developing new paths to growth. As revealed in a recent study, linking with GFNs via overseas listings creates global capital and knowledge pipelines for Linyi city to achieve local industrial upgrading (Pan et al., 2020b). Finally, the deeper integration of emerging economies into GFNs may stimulate the development of their local FABS industries. Such developments could in turn contribute to the ever-changing dynamics of GFNs. This rationale echoes the call to pay attention to the financial development in emerging economies (Alami, 2018; Boussebaa and Faulconbridge, 2019; Lai et al., 2020). On the one hand, some business opportunities will be generated for local FABS firms in the process. On the other hand, there might exist spillover effects for local counterparts from global FABS firms (Lai, 2011).

The location of FABS firms facilitating overseas listings

The FABS firms are at the heart of the analysis under the GFN framework (Coe et al., 2014; Wójcik, 2013b, 2018). In the process of overseas listings, three categories of FABS firms including the investment banks, the law firms, and the accounting firms, play key roles. Among them, the investment banks are usually in the lead position in launching initial public offerings (IPOs) (Morrison and Wilhelm, 2007; Wójcik, 2013b). The geographies of the FABS firms are crucial to understanding the formation and structure of GFNs.

The geographies of the FABS firms facilitating the overseas listings typically fall into three categories. First, the FABS firms are largely agglomerated in the overseas listing destinations. These destinations themselves are leading international financial centres with advanced FABS industries. Moreover, the host FABS firms own unparalleled advantages over competitors due to their familiarity with the listing destination’s business climate and proximity to the regulatory bodies. Second, the offshore jurisdictions, where the listed companies incorporated their listed entities, are also home to agglomerated FABS firms. The local FABS firms are the expertise of the judicial and taxation system. Finally, the FABS firms could be from the home country of the listed companies, as the eligible national FABS firms are in a privileged position to win over domestic clients.

Besides, some cities beyond the above categories might have unique competitiveness in the specific FABS sectors due to particular locational advantages. For instance, many international FABS firms agglomerate in Hong Kong, which has enabled its critical brokerage role in connecting mainland China with overseas markets (Fang et al., 2022).

The city networks of GFNs shaped by overseas listings

The activities of FABS firms interconnect the key geographical units in GFNs shaped by overseas listings (Pan et al., 2017, 2020a). First, the FABS firms provide services for the listed companies. Consequently, inter-firm service relationships are formed. Second, FABS firms need to collaborate with each other in facilitating overseas listings (Dörry, 2014). These inter-firm service provision and collaboration relations can thus be projected into the urban space, forming the city networks of GFNs (Pan et al., 2017, 2020a). Accordingly, we can map and analyse the city networks of GFNs formed in overseas listings. The results can reflect the collaboration and competition between the geographical units in GFNs.

Data and method

In this study, we explore the geography and network of the GFN shaped by the overseas listings of Chinese companies on the NYSE and NASDAQ. We obtain the basic information of the listed companies including the name, operation location, stock code, year of IPO, and incorporation places from Zero2IPO 1 and Choice. 2 In addition, we collect the prospectuses of the listed companies from the US Securities and Exchange Commission. 3 In the prospectuses, we can get the names and office locations of the key FABS firms, including underwriters, legal consultancies, and accounting experts, that facilitate the IPO. We then double-check the data at hand according to the websites of the listing firms and the relevant FABS firms. Finally, we obtain data of 301 companies listed on the NYSE and NASDAQ from 1994 to 2020 and the related FABS firms.

Following the established methodology (Pan et al., 2017, 2020), we build up two specific types of city networks, namely the service networks and the collaboration networks. The inter-firm services and collaboration relations will be converted into spatial connections based on the location of firms (Liu and Derudder, 2013). Considering that many FABS firms have multiple operation sites, the specific offices that provide services to the IPO as disclosed in the prospectuses are applied in the analysis. In both the service networks and collaboration networks, the strengths of the network links between cities are measured by the frequencies of service provisions or project-based collaborations. In the case that the inter-firm relations occur within the same city, the city connections will also be included in the analysis.

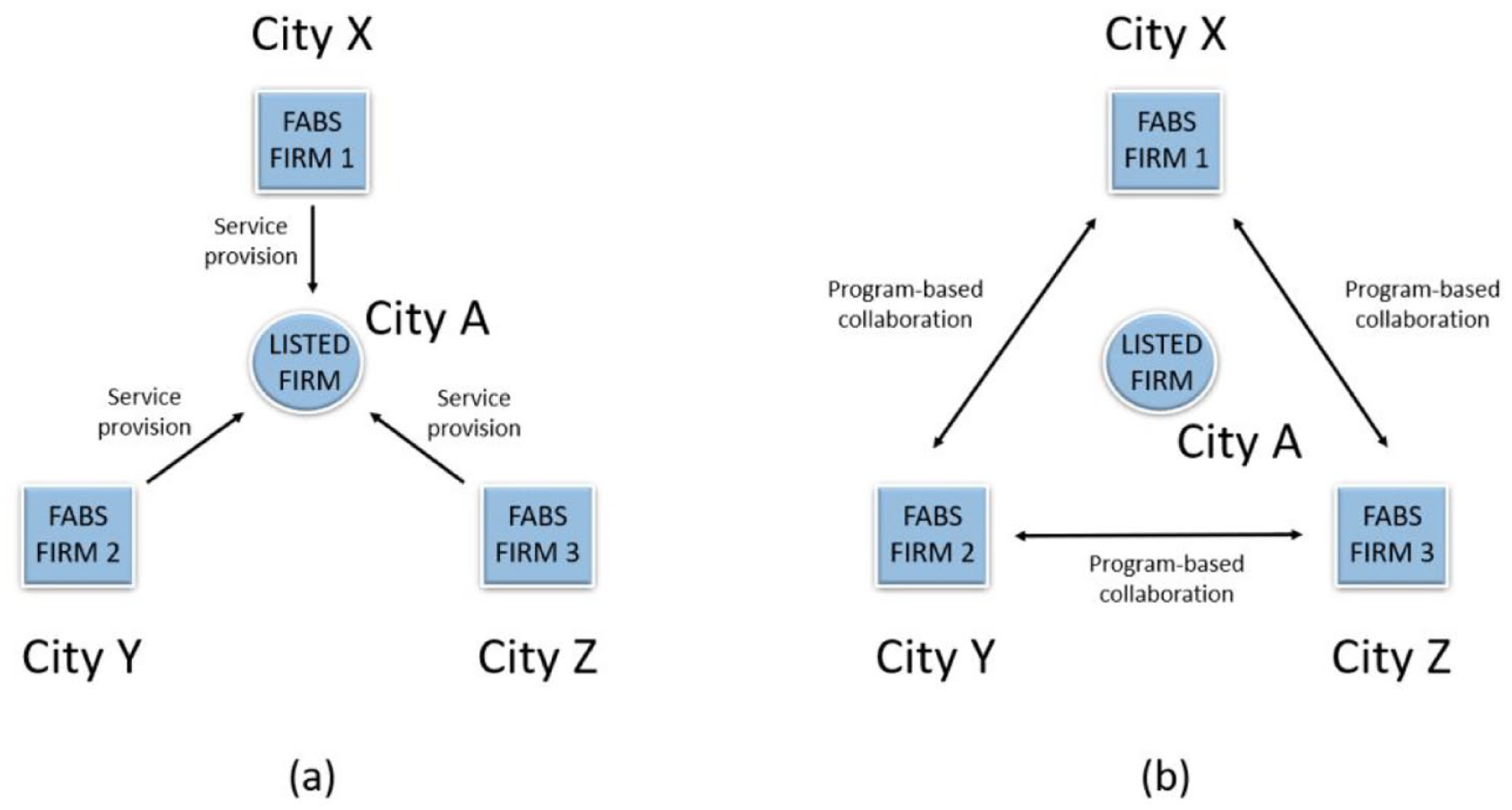

As illustrated in Figure 1(a), the service networks are the spatial projections of the service provision relations between FABS firms and the listed companies in the overseas listing process. Since the service provision relations are directed from the FABS firms to the listed companies, the converted city networks are directed networks. Meanwhile, Figure 1(b) illustrates the collaboration networks as the FABS firms cooperate with each other serving the same client in the IPO process. The collaboration networks are the spatial projections of these project-based collaboration relations, which are undirected networks.

Illustration of the service networks and the collaboration networks.

We use the following indexes to measure the status of different nodes in the city networks. SVi and RVi refer to the prominence of city node i as a service provider and service recipient in the network. Ci refers to the comprehensive importance of the city node i in the network, which measures its total connectivity as both the service provider and recipient. The SVi, RVi, and Ci are calculated as follows:

where fij refers the total frequencies of the service provision from the FABS firms in city i to the listed companies in city j, and N is the number of cities in the network.

Similarly, CVi refers to the status of city node i in the network as a collaborator and CVi is calculated as follows:

where kij is the frequency of the IPO-project-based collaborations between city i and j, and N is the number of the cities in the network.

The geography of Chinese companies’ US listings

Key geographical units in Chinese companies’ US listings

Not surprisingly, the destination of the overseas listings, New York, holds the central position in promoting the process. New York has certain advantages for attracting Chinese companies, and in particular, Chinese high-tech companies have strong preferences to go public on Nasdaq and NYSE (Halling et al., 2007; Pagano et al., 2002; Pan and Brooker, 2014).

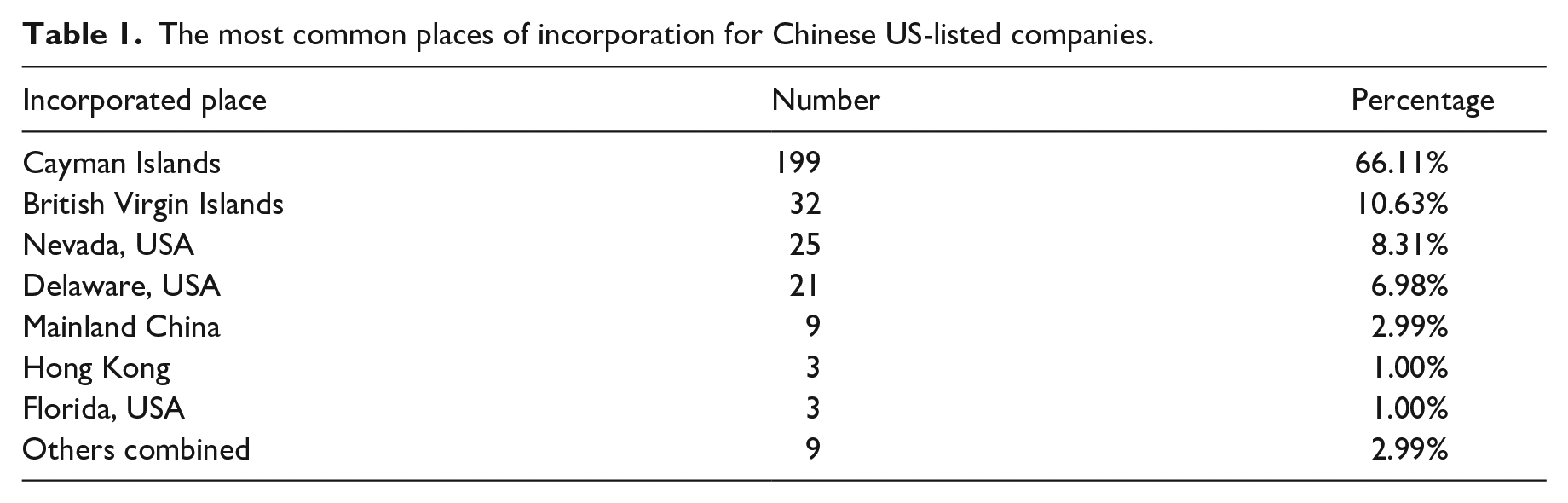

Several offshore jurisdictions stand out in the US listings of Chinese companies. Table 1 shows that most of them are incorporated overseas in offshore jurisdictions such as the Cayman Islands. The major consideration is to use the financial system of offshore jurisdictions to lower the operation cost and avoid the regulations (Buckley et al., 2015; Sigler et al., 2020; Wójcik, 2013b). As stated in the prospectus of Alibaba’s IPO on NASDAQ, incorporating in the Cayman Islands is to enjoy the ‘political and economic stability, an effective judicial system, a favourable tax system, the absence of exchange control or currency restrictions, the availability of professional and support services.’ 4 Similar statements can also be found in other firms’ prospectuses. In this case, the Cayman Islands is in the overwhelmingly lead position followed by the British Virgin Islands. The US offshore jurisdictions, Nevada and Delaware, rank third and fourth respectively.

The most common places of incorporation for Chinese US-listed companies.

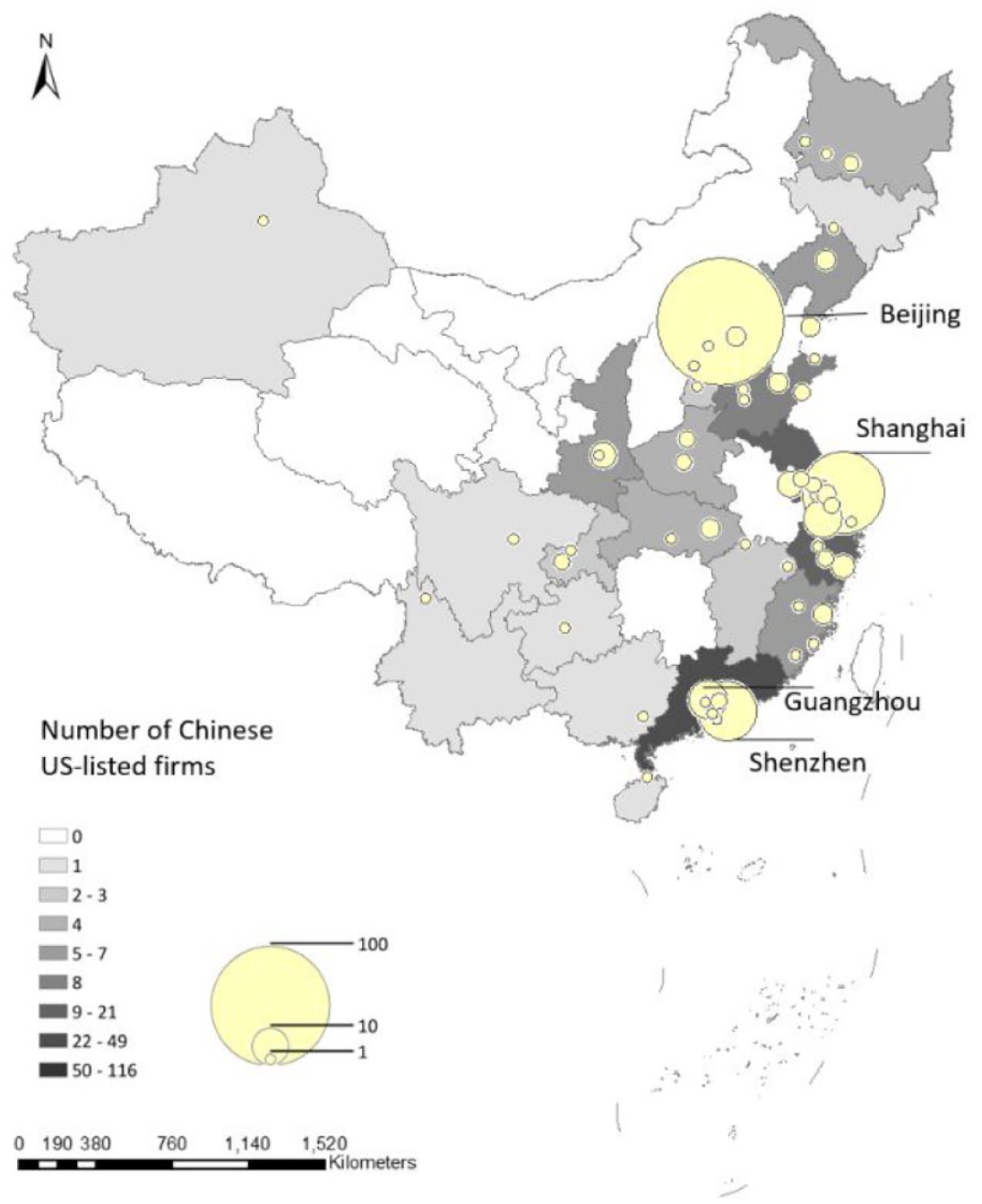

Regarding the origins of the Chinese US-listed companies, our results show that they are unevenly distributed in 55 prefecture-level cities and 23 provincial-level administrative regions 5 – most of them highly agglomerated in the few most developed cities in China. As Figure 2 shows, they are largely distributed in coastal areas, especially the most highly interconnected three urban agglomerations in domestic urban networks, namely, the Beijing-Tianjin-Hebei, Yangtze River Delta, and Pearl River Delta (Zhao et al., 2015). Beijing, Shanghai, and Shenzhen are the top three cities with the largest number of US-listed companies, together accounting for 63.5% of the total. The uneven geography concurs with the findings in previous studies that economically advanced and highly connected regions in China take precedence over others in integration into GFNs (Pan and Brooker, 2014; Wójcik and Burger, 2010).

The geographical distributions of Chinese companies listed on the US stock markets.

The FABS firms and their locations

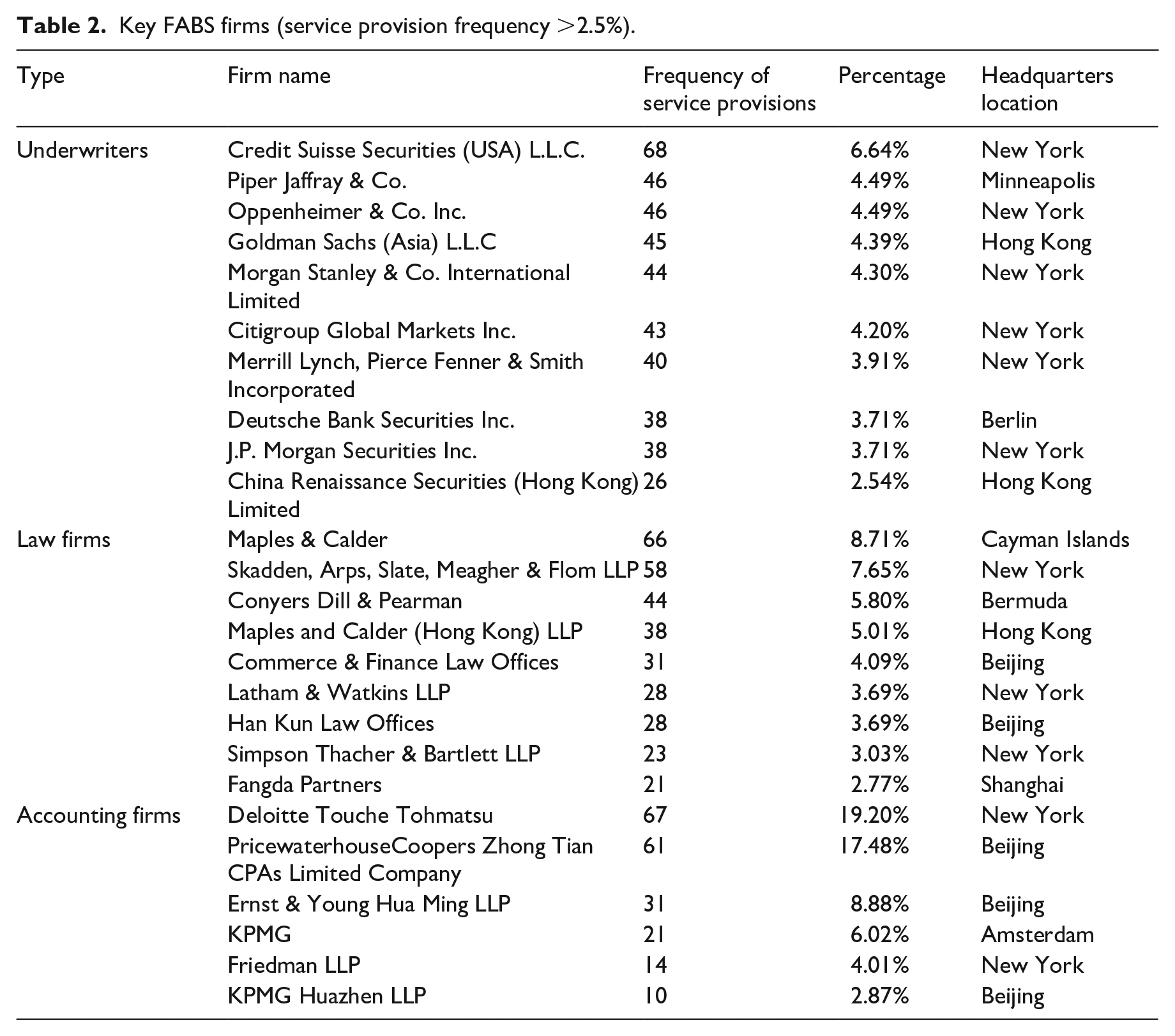

As Table 2 shows, the FABS firms with higher frequencies of service provisions are majorly headquartered in a few leading global financial centres and offshore jurisdictions. The underwriting services are dominated by global investment banks, such as Goldman Sachs (Asia), Credit Suisse Securities (USA), Piper Jaffray & Co., and Oppenheimer & Co. Inc. Since the listing destination is New York, it is not surprising that American investment banks are in a dominant position. Most of these investment banks are headquartered in New York. Hong Kong also houses many important investment banks, which are regional headquarters of investment banks either from the US or mainland China.

Key FABS firms (service provision frequency >2.5%).

Due to the regulatory differences across jurisdictions, the legal services are majorly provided by three groups of law firms headquartered in the destination of the IPOs (New York), offshore jurisdictions (Cayman Islands, Bermuda, and Hong Kong), and mainland Chinese financial centres (Beijing and Shanghai). These law firms located in varied jurisdictions will need to work together to make full compliance with different law systems.

Accounting services are majorly provided by the ‘Big Four’, namely Deloitte, PricewaterhouseCoopers, KPMG, and Ernst & Young, and their joint ventures. 6 The Big Four are headquartered in the lead international financial centres including New York, London, and Amsterdam, while their joint ventures in China are in mainland Chinese financial centres like Beijing.

It is noteworthy that many of these important FABS firms own well-developed branch networks composed of offices all around the world with different functions and market focus. Both headquarters and branch offices might provide services for the IPO process. For example, while headquartered in Berlin, Deutsche Bank Securities Inc. largely relies on its New York office to provide underwriting services to Chinese clients. KPMG, while headquartered in Amsterdam, usually provide accounting service to Chinese companies via its Hong Kong and Beijing offices. Despite the role of control and management played by the headquarters (Taylor and Derudder, 2004), the offices that operate the real business can also be crucial in forging the competitiveness of their located financial centres (Wójcik, 2018). Our analysis in the following section gives more information about this critical geography.

The city networks shaped by Chinese companies’ US listings

Service networks

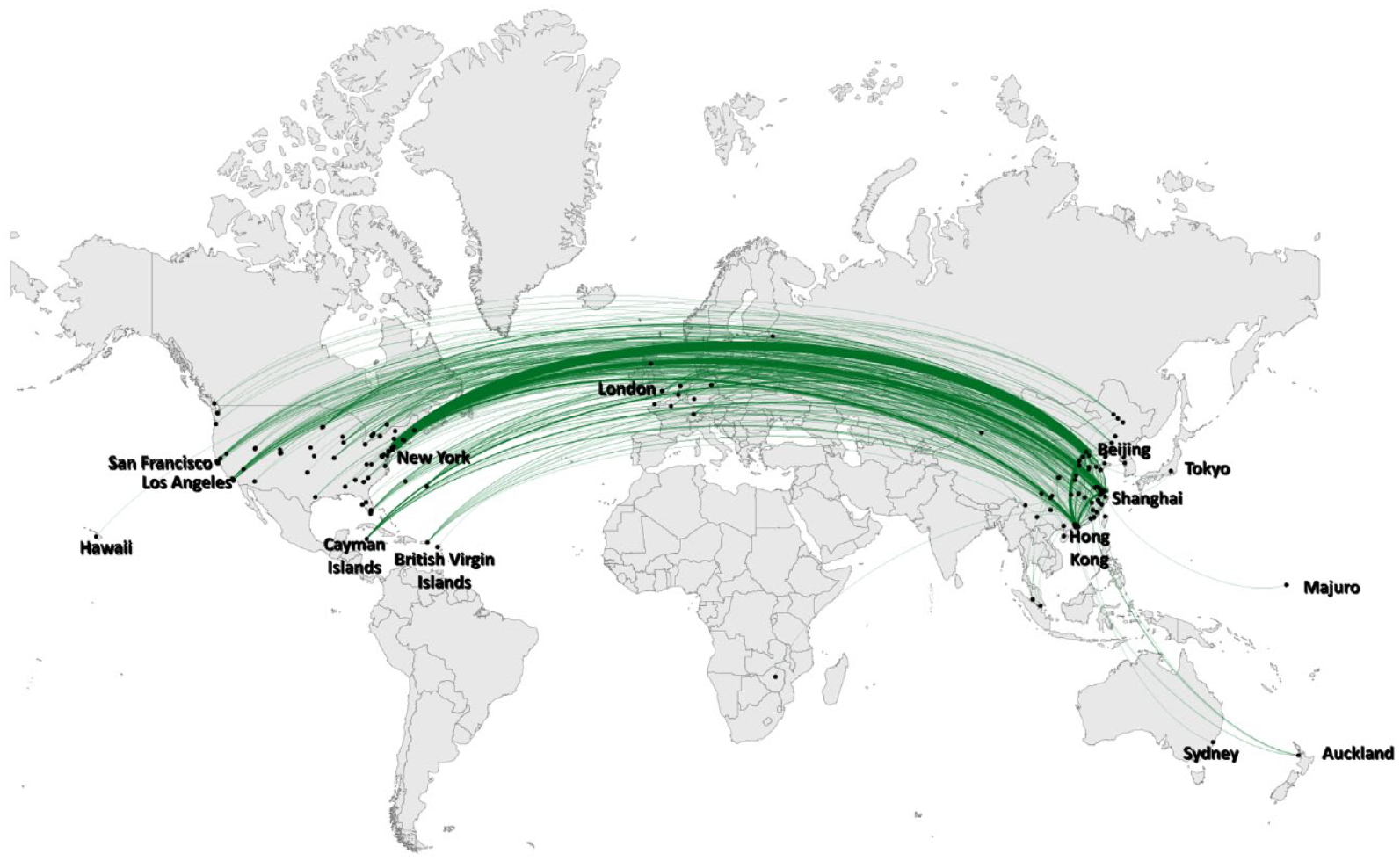

Based on the inter-firm service relationship between FABS firms (the offices in charge of providing the services) and the listed companies, we have mapped different service networks. As shown in Figure 3, the overall service network of all services (underwriting, legal, and accounting) spans a large geographical scale, connecting mainland Chinese cities and other financial centres and offshore jurisdictions around the world.

The overall service network formulated in mainland Chinese companies’ US listings.

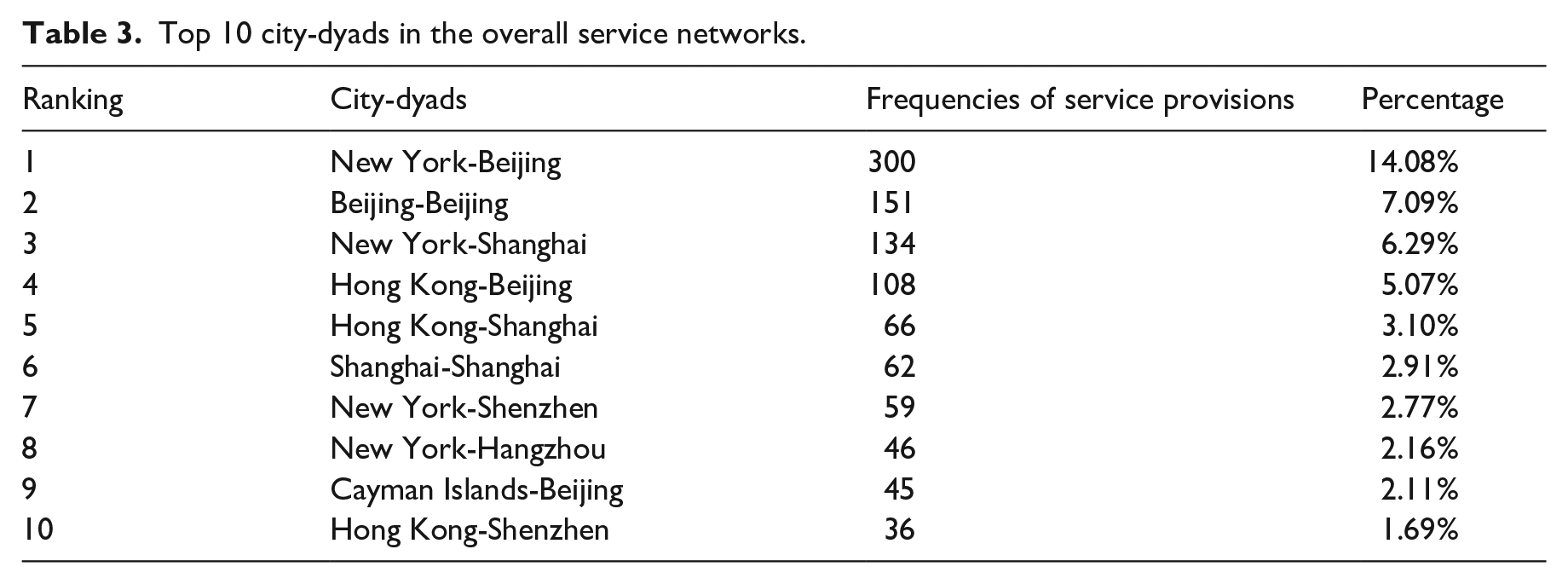

Table 3 lists the top 10 city-dyads measured by service provision. Most prominently, strong ties are observed between mainland Chinese and US cities. New York-Beijing has the largest frequencies of service linkages, and New York-Shanghai, New York-Shenzhen, and New York-Hangzhou are leading city-dyads. Hong Kong-Beijing, Hong Kong-Shanghai, and Hong Kong-Shenzhen respectively rank 4th, 5th, and 10th, demonstrating the prominent bridging role of Hong Kong (Fang et al., 2022; Sigler et al., 2021). Interestingly, Beijing-Beijing ranks 2nd, indicating the growing competitiveness of Beijing as a financial centre. In addition, the offshore jurisdiction of the Cayman Islands has strong connections with Beijing.

Top 10 city-dyads in the overall service networks.

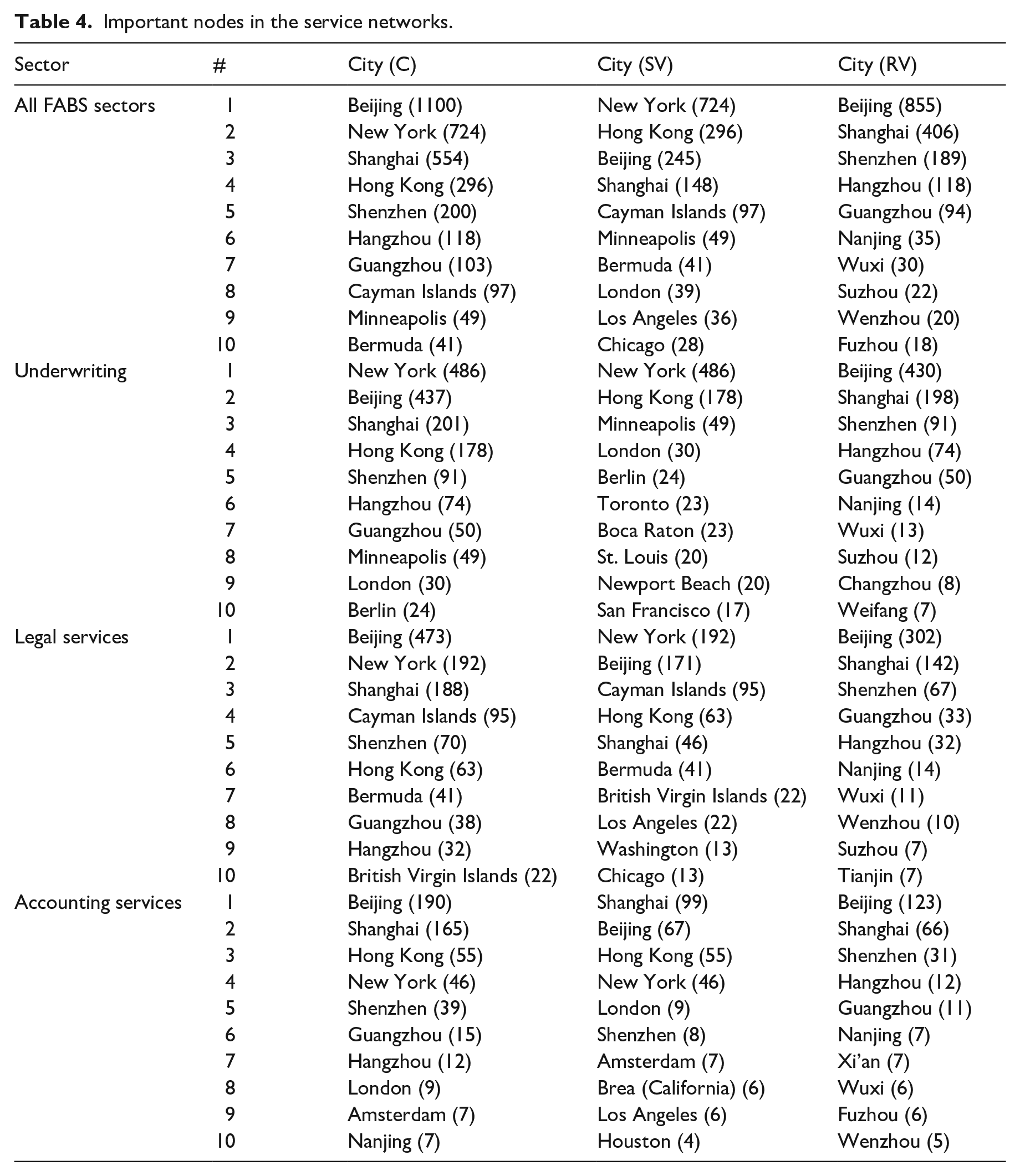

Table 4 presents the top 10 nodes in different service networks in terms of connectivity (C), service provision (SV), and service recipient (RV). The most connected cities fall into three categories. Beijing, Shanghai, Shenzhen, Hangzhou, Guangzhou, etc. are mainland Chinese cities, which are home to headquarters of listed companies; New York, Hong Kong, etc. are international financial centres where FABS firms are agglomerated; The Cayman Islands, Bermuda, etc. are offshore jurisdictions.

Important nodes in the service networks.

Among mainland Chinese cities, Beijing is the most prominent service recipient, while its role as an important provider of legal and accounting services should not be neglected – it ranks 3rd as a FABS provider city only after New York and Hong Kong. Shanghai ranks 4th in service provision and it is particularly competitive in the accounting sector. Shenzhen is also an important accounting service provider. Surprisingly, no mainland Chinese city is a prominent underwriting service provider.

New York, as the destination of the IPOs, is the most important service provider. In addition, it ranks 1st in both underwriting and legal services, and ranks 4th in accounting services. Interestingly, Hong Kong is the pivotal securities centre following New York in providing underwriting services. Hong Kong is also influential in providing legal and accounting services, ranking 4th and 3rd, respectively. London, Berlin, Los Angeles, and a few other international financial centres also appear in Table 4, while much inferior to New York and Hong Kong.

Offshore jurisdictions with the Cayman Islands in the lead, are featured in the service networks. As the incorporation places of the listed companies, the offshore jurisdictions mainly provide legal services.

Collaboration networks

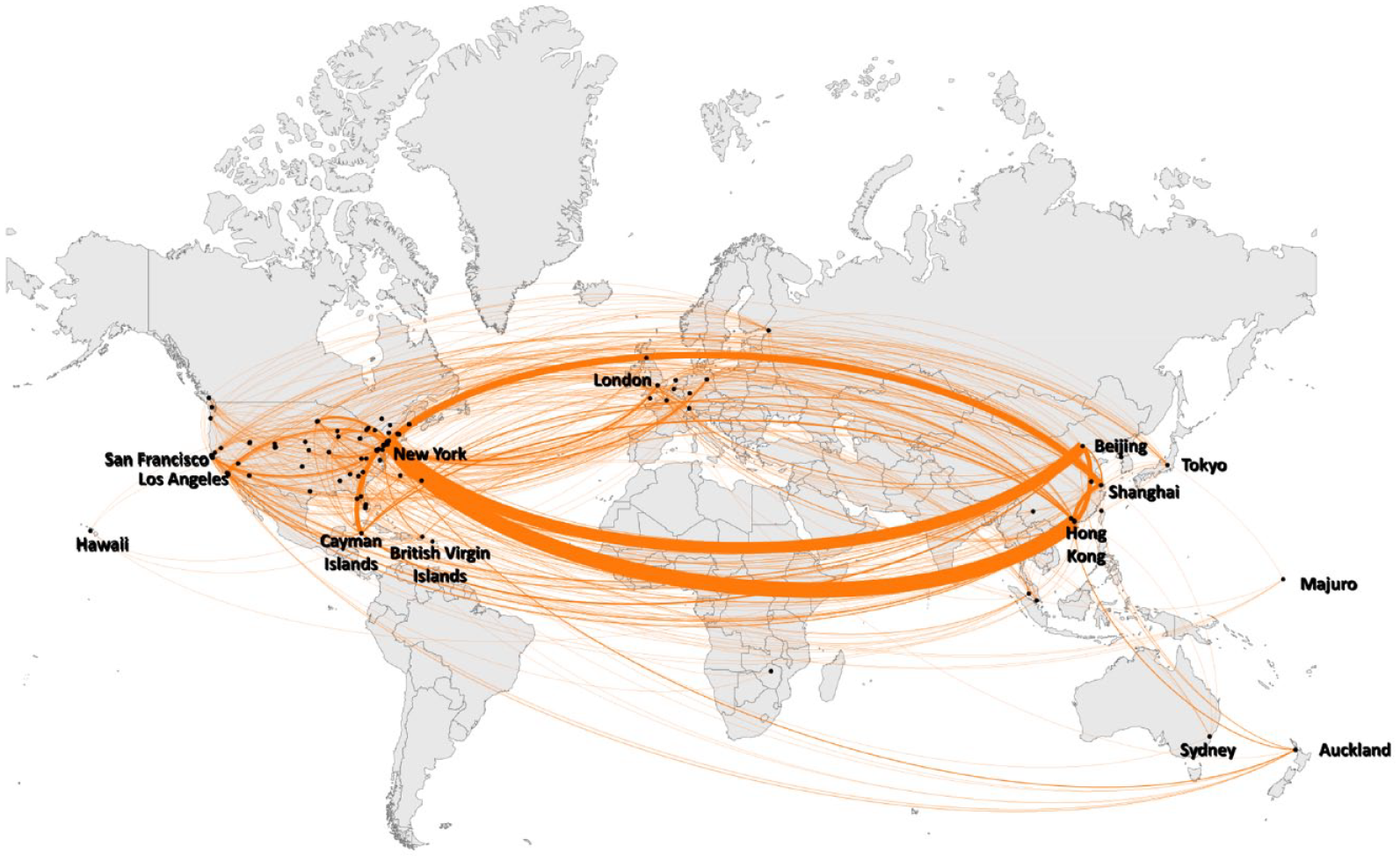

Figure 4 maps the overall network based on FABS collaborations. Not surprisingly, New York, Hong Kong, Beijing, and Shanghai stand out as key nodes within the network.

The overall collaboration network formulated in mainland Chinese companies’ US listings.

Table 5 lists the top 10 city-dyads measured by the frequencies of FABS collaborations. Many strong ties are intra-city self-loops. Most collaborations are between FABS firms in New York, which indicates New York’s critical role in facilitating Chinese companies’ US listings. The intra-city collaborations within Hong Kong, Beijing, and Shanghai also well reflect the competitiveness of these financial centres in GFNs, as the local clusters of FABS firms have formulated advanced networks of financial knowledge and expertise inside the city (Bassens, 2012). In addition to the intra-city self-loops, other strong inter-city ties in the service network are majorly between the four key node cities including New York, Hong Kong, Beijing, and Shanghai.

Top 10 city-dyads in the overall collaboration network.

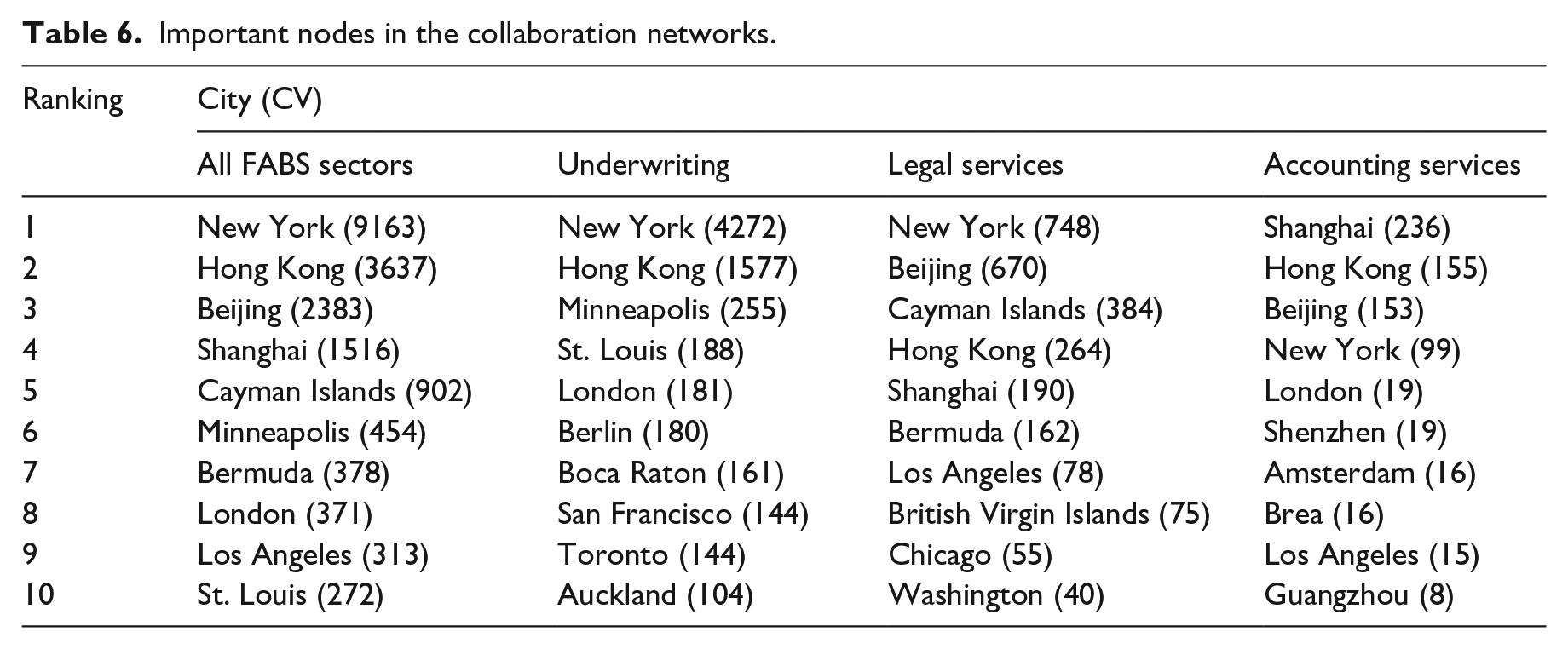

Table 6 lists the top 10 nodes with the highest collaboration values (CV) in different collaboration networks. Likewise, the nodes can be divided into mainland Chinese cities, international financial centres beyond mainland China, and offshore jurisdictions. Only four mainland Chinese cities, Beijing, Shanghai, Shenzhen, and Guangzhou, are featured in the table, and the latter two are in a very marginal position in the networks. As Table 6 shows, Beijing is both an important legal service hub and a prominent accounting service hub. It ranks 2nd in the collaboration network of legal services and 3rd in accounting services. Shanghai is an accounting service hub in the network, ranking 1st in the collaboration network of accounting services.

Important nodes in the collaboration networks.

As for international financial centres, New York owns an incomparable lead position in these networks as a dominant hub in the collaboration networks of underwriters and law firms. Hong Kong is the second most important financial centre following New York, and its advantage is mainly reflected in mediating underwriting and accounting collaborations. Offshore jurisdictions like the Cayman Islands, Bermuda, and the British Virgin Islands are featured in the legal collaboration network. They have maintained close ties with other financial centres.

Strategic nodes

Several strategic nodes stand out in the above city networks. As the listing destination, New York has been the primary city node in facilitating Chinese companies’ US listings. In addition to its globally competitive stock markets, a dense cluster of the world’s leading investment banks, law firms, and accounting firms has ensured New York’s status as a first-tier international financial centre. These FABS firms work closely with their counterparts in other international financial centres and offshore jurisdictions. The city network analysis suggests that New York has strengthened its position in GFNs shaped by Chinese firms’ overseas listings over time.

Some offshore jurisdiction, in particular the Cayman Islands, is a critical conduit for mainland Chinese companies to issue and trade their stocks in the US. By incorporating the listed entities in these offshore jurisdictions, mainland Chinese companies catered to the requirements of overseas listings on the US stock markets, reduced the taxation cost, and escaped from regulatory restrictions in mainland China.

Hong Kong is the key financial centre as well as an offshore jurisdiction bridging mainland China and the global financial market (Lai, 2012; Taylor et al., 2014; Fang et al., 2022). The FABS firms in Hong Kong established by western capital (such as Goldman Sachs (Asia) L.L.C.) provided important service for Chinese companies to enter the global capital market. Meanwhile, the locational strategy of many leading mainland Chinese FABS firms have strengthened Hong Kong’s role as an international financial centre. With the increasing integration of China into GFNs, Hong Kong’s role as the only gateway might be challenged, as mainland Chinese companies increasingly have direct access to international FABS firms and financial markets (Fang et al., 2022; Sigler et al., 2021).

Beijing and Shanghai, two rapidly rising world cities in mainland China (Derudder et al., 2018; Pan et al., 2021), have also been actively engaging in the process of Chinese companies’ US listings. On the one hand, a majority number of Chinese companies that made successful IPOs on the US stock exchanges are from the two cities. On the other hand, the FABS firms from the two cities play important roles in serving the firms listed on US stock exchanges. In the context of China’s pursuit of promoting the development of its own world cities (Timberlake et al., 2014), Beijing and Shanghai might become more influential within GFNs in the future.

Conclusion

Over the past three decades, there have been a growing number of mainland Chinese companies successfully going public in the US. This process represents an increasingly deep integration of China into GFNs since the 1990s, which has brought forth enormous changes to both China and the global finance (Lai et al., 2020; Pan et al., 2020b; Wójcik and Camilleri, 2015). By investigating 301 mainland Chinese companies’ listings on Nasdaq and NYSE from 1994 to 2020, this study unpacks the geography and network structures of GFNs therefore formed.

Deploying the GFN framework, our study analytically focuses on several key geographical units, including international financial centres, offshore jurisdictions, and those cities/regions that received global financial capital, to sketch the trajectory of China’s integration into GFNs. The results show that New York is the key international financial centre as the destination of Chinese companies’ US listings. The Cayman Islands and British Virgin Islands are important offshore jurisdictions in which Chinese listing companies are incorporated. Beijing, Shanghai, and Shenzhen have great advantages over other mainland Chinese cities in connecting with GFNs, as they house the largest number of listing firms’ headquarters. FABS firms involved in the overseas listing process are mostly located in above-mentioned cities, while Hong Kong is found to be an extremely important node where key FABS firms are agglomerated.

By quantifying the city network structures of GFNs shaped by Chinese companies’ US listings, this study discloses the distinctive functions of several strategic nodes. New York, Hong Kong, Beijing, and Shanghai are key nodes in both the service networks and the collaboration networks. New York is the dominant hub in the service and collaboration networks of all FABS sectors – its network position well matches its core role in Anglo-American financial power (Wójcik, 2013a). Hong Kong, Beijing, and Shanghai are also important nodes but with differentiated functional advantages. Hong Kong is more capable of providing underwriting services, and Beijing has strength in providing legal and accounting services. Shanghai is an important node providing accounting services. New York-Beijing is the most important city-dyads in service networks, while New York-Hong Kong is in the lead position in collaboration networks. Besides, offshore jurisdictions including the Cayman Islands, the British Virgin Islands, and Bermuda are key nodes within networks, providing legal services and collaborating with New York, Hong Kong, and other financial centres.

Despite the rapid development of mainland Chinese financial centres (c.f. Lai, 2012; Pan et al., 2021; Timberlake et al., 2014), our results suggest that Chinese companies’ US listings have evidently reinforced the core structure of GFNs dominated by the west (Wójcik, 2013a). The western transnational FABS firms have overwhelming advantages over Chinese FABS firms, while the latter are largely confined to the legal and accounting services related to China’s regulation. The western financial centres are key to Chinese companies’ global financing, while the mainland Chinese financial centres are still in a relatively marginal position. Notwithstanding the ‘Chinese globalisation’ which has been considered one of the three globalisations shaping the 21st century (Derudder and Taylor, 2020), and the rise of China is seen as a potential challenger to the current global financial order (Wójcik, 2013a), our study indicates that by listing firms in the US, China is continuously integrating itself into the current order of GFNs instead of challenging the established structure.

The city network method applied in this study, also named as project-based network building method (Pažitka et al., 2021), provides a new way to quantitatively analyse the geography and network structure of integrations into GFNs at city scale. This method could be applied in investigating varied categories of global financing activities such as global venture capital investments, bond issuing etc. Moreover, such research work on inter-firm networks (Pan et al., 2017) could also provide a fresh perspective in understanding world city networks, in which the city-level analysis of economic networks has been largely relying on the intra-firm linkages without investigating the competition and collaboration between cities (Taylor and Derudder, 2004; Taylor et al., 2014, 2021).

While this study focuses on the thriving US listings of Chinese companies in the past decades, the most recent tensions between Chinese companies and the US regulators have created great uncertainties for this trend. Such developments remind us of the impacts of geopolitics and state power on GFNs (Töpfer, 2018; Lai, 2018), and the necessity of including the analysis of specific institutional contexts (Liu and Dicken, 2006; Wu, 2020; Wu and Zhang, 2022). Future research could draw on such issues to interrogate how GFNs are impacted by the state actors.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China (NSFC) [grant number 42022006; grant number 41871157]; the China Scholarship Council [grant number 202006040044].