Abstract

Responding to the call for a greater attention to the inherited variations in housing financialisation, this paper contributes by bringing in a constructivist perspective in exploring how financialisation gradually unfolds in a particular context. Drawing on the case of China, two interrelated arguments are made. First, a structural and temporal distinction is made between three phases of housing commodification, speculation and financialisation 1.0, where significant differences are noticed between the ownership structures, housing rights, markets, returns and motivations from a constructivist perspective. Second, these phases are systemically interrelated as a result of the state-market nexus in China where active state intervention connects these different processes in a continuous cycle of the urbanisation of capital. The case of China adds to the emerging literature on housing financialisation from the global south, and speaks to the largely downplayed temporal variations of housing financialisation in the vigorous literature on financial geography and urbanism.

Introduction

Comparative housing studies tend to record stark similarities between China and its Southeast Asian neighbours (Chiu, 2008), East European transitional economics (Stephens, 2010), and the Western capitalist welfare regimes (Zhou and Ronald, 2017). On the surface, the argument about China’s housing system converging with the global trend of privatisation, neoliberalism and now financialisation seems plausible. Similarities are marked by the fact that over 85% of the Chinese urban residences have achieved homeownership (Research Center for China Household Finance, 2016), market mechanisms dominate housing production and consumption, and severe affordability challenges loom large in many cities (Cao, 2016). However, such a meta-reading of China’s reform direction and consequence needs to be embedded in China’s changing political-economic environment. The latest macro-regulation principle laid down by President Xi in 2017, ‘Housing is for Living, Not for Speculation’, has reiterated housing as a basic right and reemphasised security-based housing provision. The announcement has aroused wide discussions regarding the potential restoration of some of the lost socialist colour of China’s housing system.

Albeit still debatable, most scholars tend to view the re-emphasis on subsidised housing as an ‘intrapreneurial’ adjustment (Miao and Phelps, 2019) of China’s housing market instead of moving back to indiscriminative social goods allocation (Chen et al., 2014; Wang and Murie, 2011). Such intrapreneurism is also reflected in its growing housing finance sector, which has stimulated a heated discussion on the extent, nature and characteristics of Chinese housing financialisation (Chen et al., 2022; Wu, 2020; Wu et al., 2020). While useful in embedding China in the global financialisation literature, emerging studies tend to take a snapshot of current situation at the national level, which provides inadequate explanations of how this phenomenon evolves over time and the underlying factors driving this dynamic. As Aalbers (2019: 377) reminds us, ‘housing financialization. . .is not primarily about showing which place is more financialized; it is about understanding the process by which financial actors, markets, practices, measurements and narratives are increasingly becoming dominant.’

This paper therefore provides an account sensitive to temporal variations of housing financialisaton. The specific questions asked are: how has China’s housing financialisation been developed so far, and what are the key forces driving these processes? Three distinct phases of housing commodification, speculation and financialisation 1.0 are identified. Although seemingly arriving at a similar evolution trajectory to those proposed by Wu et al. (2020) and Chen and Wu (2020), this paper is concerned with the fundamental constructivist features of these phases, and how they compare, and connect, with each other. The generic analytical framework proposed also bears the potential of systematically comparing China’s financialisation process with those of other developing and developed countries internationally. The connections between these phases are explored against the persistent and evolving state-market nexus along the chain of housing and capital production, distribution and consumption. It is argued that embedding financialisation within China’s social and political backgrounds adds to the global financialisation literature in unveiling the complexity of the state-market nexus and its dynamics.

In what follows, this paper begins by reviewing the housing financialisation literature before presenting a constructivist interpretation of it. The third section then scrutinises housing commodification, speculation and financialisation as they were discussed in the Chinese literature. It demonstrates that each of these terminologies actually captures different contingent elements in a progressive fashion. China’s evolving state-market nexus is suggested as the key factor underpinning this dynamic. The united yet diverse political landscape of China (Miao and Phelps, 2022) is likely to play into the unfolding of this nexus at different political unities, but detailed discussions are beyond the scope of this paper. Returning to the broader debate on the nature of housing financialisation, the fourth section of this paper concludes by considering the implications of the relationship between different terminologies as well as the temporal variations for understanding the connections between housing, the state and social and economic development.

A constructivist framework for housing financialisation

Focused studies on the nature of China’s housing sector in general, and market-state relations in particular, have provided meticulous insights on China’s housing system transformation. Housing and social scholars tend to focus on the reform process (Chiu, 1993; Wang and Murie, 1996), tenure changes (Huang, 2004), the transformation of housing welfare system (Chen et al., 2014), housing affordability (Yang and Chen, 2014) and residential inequalities (Logan et al., 2009). Real estate economists are concerned with housing price, market fluctuations (Feng et al., 2011), speculation and real estate financing (Cao, 2015). Geographers and urban scholars have traced the emerging live-work mismatch (Miao et al., 2019), shantytown redevelopment (He et al., 2020) and master-planned suburb estates (Wu and Phelps, 2008). There is now an emerging literature that tries to integrate political, geography, urban and financial perspectives through the lens of financialisation (Chen and Wu, 2020; He et al., 2020; Li et al., 2021; Lin et al., 2019; Wu et al., 2020).

The phenomenon of financialisation, which refers to ‘a pattern of accumulation in which profit making occurs increasingly through financial channels rather than through trade and commodity production’ (Krippner, 2005: 174), has become so profound after the global financial crisis that Aalbers (2019) is ready to propose the advent of a ‘financial geography’. In the same vein as the ‘penetration of commodity relations has been particularly marked. . .in the proliferation of consumer durables in the average dwelling’ (Forrest and Williams, 1984: 1164), financialisation is manifested profoundly in the built environment. Housing, as an essential element of the built environment, has long been a crucial outlet for capital overaccumulation (Gotham, 2009; Harvey, 1978) and has always been capital-intensive (Christophers, 2010). Yet the financialisation of housing denotes an increasing dominance of the financial actors, practices, measurements and narratives, resulting in a structural transformation of housing production, consumption, distribution and investment.

Current studies on housing financialisation could be divided into three strands based on their focus on different housing tenures and related financial structures and characteristics. The first strand focuses on homeownership and associated housing prices and mortgages. Scholars have written about the expanding and pricing of mortgage loans (Newman, 2009; Palomera, 2014; Walks, 2013), credit scoring of potential homeowners (Aalbers, 2008; Shen and Yan, 2009) and mortgage structures and securitisation (Aalbers, 2019; Halawa, 2015; Zhou, 2015). The second strand is concerned with rental market and landlord-tenant-financer relations. Scholars debated on housing rights (Rolnik, 2013) and different forms of rental-finance couplings such as the long-term rental market (Chen et al., 2022), investment-driven rental constructions and the rise of global corporate landlords (Aalbers, 2019). The last and more recent strand unpacks the rental market further by zooming in on the subsidised housing (Chua, 2015; Fields, 2015; Hodkinson, 2011), not-for-profit housing providers (Wijburg et al., 2018), and care homes (Aveline-Dubach, 2022; Horton, 2019) that are typically facilitated by government funding and regulations.

Along with the proliferating of the financialisation literature comes the call for a greater spatial sensitivity to the variegated housing sectors (Aalbers, 2017; Wu et al., 2020). This paper contributes by investigating the temporal variations of the housing financialisaton process. It does so by borrowing insights from Forrest and Williams (1984), Ruonavaara (1993) and Doling (1999) in developing a generic constructivist analytical framework. A constructivist view of housing believes that the properties of a housing system are not pre-defined but are historically and socially constructed (Ruonavaara, 1993). The relative dominance of owner-occupied or social rental housing, for example, is determined by the social relations connected to that form of provision. The structures of social relations in turn, are not immutable but develop through time, shaping the properties of a housing system and shaped by the particular history of the country (Ball, 1986). The rights and duties of an owner-occupier in China, for example, are different from those in Singapore, and similarly being a tenant in China in the 1960s is different from being a tenant in the 1990s. Likewise, the features of housing financialisation in a particular country/place is influenced by the evolving common choices of individuals, the shifting conventions and social relations. A constructivist analytical framework, therefore, is particular useful in unveiling not just the ‘variegated, contingent, fragmented, incomplete and uneven’ terrain of financialisation (Aalbers, 2017: 546), but also the contextualised factors underpinning these variations.

Inspired by Doling (1999), Stephens (2010) and Wang and Murie (2011), some of the key constructivist properties associated with a housing system are: housing rights, ownership, markets, returns and motivations. Housing rights measure the extend of housing accessibility granted on the basis of citizenship rather than consumption capability. A ‘radical housing right regime’, borrowing from Harloe (1995), could be defined as a fully socialised set of arrangements and the removal of any vestige of capitalist market influence over people’s access to decent homes. In reality, a place recognises, protects and legalises people’s housing rights to various degrees, leaving rooms for the influence of financial means. A related yet narrower element is housing ownership, which focuses on the monetary transaction of housing as commodity and the type of possession with legal implications. Saunders (1990) identified some key features associated with housing ownership. These include: the right to indefinite use, to give away or bequeath; the right to modify and dispose; the ability to choose an appropriate price and method of payment; and the advantage of investing in something one controls. The growing investment complexity and multi-scalar governance structures of our modern housing sector (Miao and Maclennan 2017) makes it important to unpack housing ownership in order to understand the scale and scope of financial influence.

Housing markets are where housing-related transactions happen. Although traditional analysis emphasises the intrinsic fixity, durability and construction delay of housing as constraints of its market dynamic, the prevalence of financial engineering in the housing sector, and housing securitisation in particular, has transformed illiquid properties into revenue-generating (quasi)financial assets (Wu et al., 2020). The degree of overlap between housing and financial markets, however, varies between places and along time (Aalbers, 2016, 2019; Fields and Uffer 2016). Housing returns could take variegated formats and could be psychological, social and economical. When housing is transferred on the market not (only) for its use value but for its exchange value, there is normally a minimal monetary return expected from housing owners, not only to compensate for the opportunity cost of money spent on the properties and the transaction costs involved, but also to capture the expected appreciation in the future.

The dominant housing motivation is another important factor shaping a housing system, especially through the price signal (Alexiou et al., 2019). Individuals’ motivations are what they expect to gain in the future, and they choose how to behave now by evaluating among alternative courses of action. Compared to ‘housing returns’ used in this paper that are current, certain and independent, housing motivations are future, flux and subject to peer pressures and market trend. Of course there are multiple stakeholders on the market and each has their motivations. This paper is not concerned with individuals or one particular group’s motivations, but the dominance of one sector’s motivation over others. Consumer motivations are the most divergent yet crucial variables influencing market performance. Tan and Khong (2012) identified four major motivations, including local amenities investment, social capital investment, residential stability and financial benefits. Housing suppliers’ and financiers’ motivations are more interrelated, with the latter exerting increasingly stronger influence over the former (Bruun, 2018). The motivations of housing regulators, traditionally associated with correcting market failures, are also found to be in favour of, and even responsible for creating, the conditions of housing financialisation (Aalbers, 2016).

Examined through this constructivist framework, a highly financialised housing sector might reveal the following key features. First of all, the ‘radical housing right regime’, where housing was treated as a basic human right, and housing finance was heavily subsided and regulated to shelter it from the market volatility (Florida and Feldman, 1998), is replaced by a post-Fordist housing regime that is monetary-based and individualist. Here housing right becomes a privilege associated with landlords, and ‘global corporate landlords’ replace the public sector in the operation and management of most housing assets (Beswick and Penny, 2018). Secondly, housing ownership is ‘there to keep financial markets going, rather than being facilitated by those markets’ (Aalbers, 2017: 548). The lengthy and costly process of achieving ownership is being engineered and reengineered by financial institutions into relatively stable and lucrative financial returns. Households’ desire to make early repayment to mortgage loads is regarded as ‘investment risks’ and discouraged. Thirdly, the housing market, which used to be considered too important to be regulated and controlled solely by market principles (Florida and Feldman, 1998), has now been transformed by, and integrated with, the global capital markets and financial circulations. The sheer size of the global real estate market ($280 trillion USD by the end of 2017), and in particular the residential property market ($220 trillion USD), means that housing is the last, and perhaps most significant, frontier of the global capital exploitation (Leijten and Bel, 2020).

Fourthly, in this market, the exchange value of housing becomes disengaged from its use value as housing takes on the attributes of a financial asset (Coakley, 1994). Corporate investors and financiers set the rules of the game, and they are seeking speculative, profit-driven returns at the expense of the renters and the poor. Lastly, a financialised housing sector exists to fuel the motivations of capturing future returns and/or hedging future volatilities. Here the inherent temporal and spatial characteristics of housing and the housing sector, such as inertia, durability, fixity and heterogeneity, become both the necessary preconditions of, and the obstacles to, such motivations. There is an army of specialised financial agencies and experts being trained to overcome such obstacles and further fuel this process. The prevalent social relationship is, therefore, a financialised one. It is still subject to public interventions, but even these interventions are evaluated on financial principles and logics (Hendrikse, 2015). Parallelly, governments, public authorities and semi-public institutions are proactively cultivating, augmenting and participating in housing financialisation to fulfil their growth and/or political goals.

These simplified features associated with a deeply financialised housing system take time to formulate and will vary geographically. This paper presents the case of China in the next section to illustrate its pathway towards housing financialisation. While theoretically driven, this paper is grounded on key academic and policy discourse and secondary data analysis. The technique followed is the ‘sociology of knowledge approach to discourse analyses’ suggested by Keller et al. (2018), which combines the macro-level theorisation of discourse as institutional production and the micro-level conceptualisation of everyday knowledge to enable the investigation of social relation on multiple levels (see Miao (2021) as an example of this approach). Specifically, national strategic policy documents related to housing sector reforms were thematically analysed to provide a macro canvas of the state-market nexus. Detailed academic case studies and policy review pieces were synthesised to distil the micro properties of China’s housing regime at different stages. Secondary data from key institutions such as the National Bureau of Statistics and the People’s Bank of China were used wherever relevant to illustrate the arguments further.

A Chinese pathway towards housing financialisation

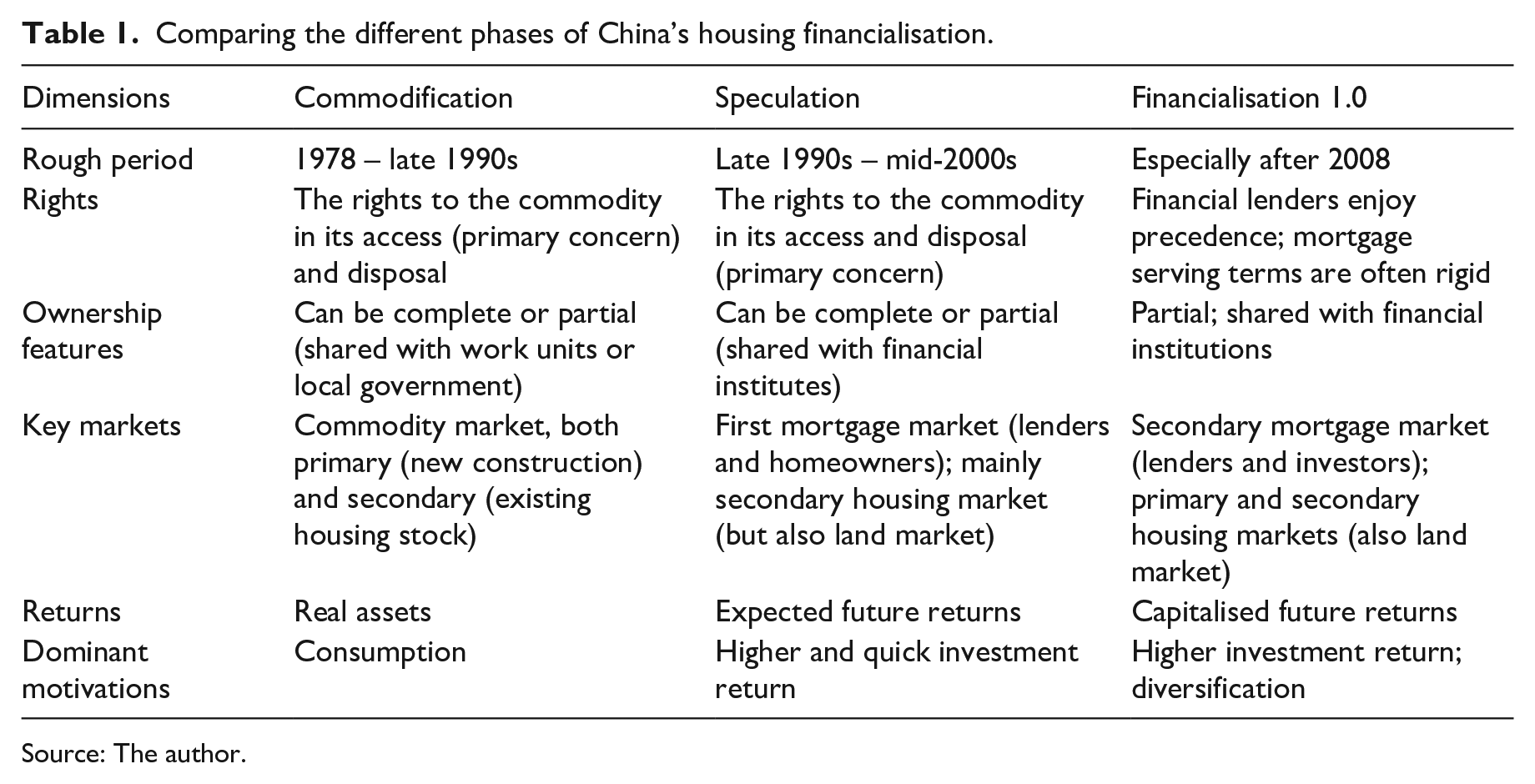

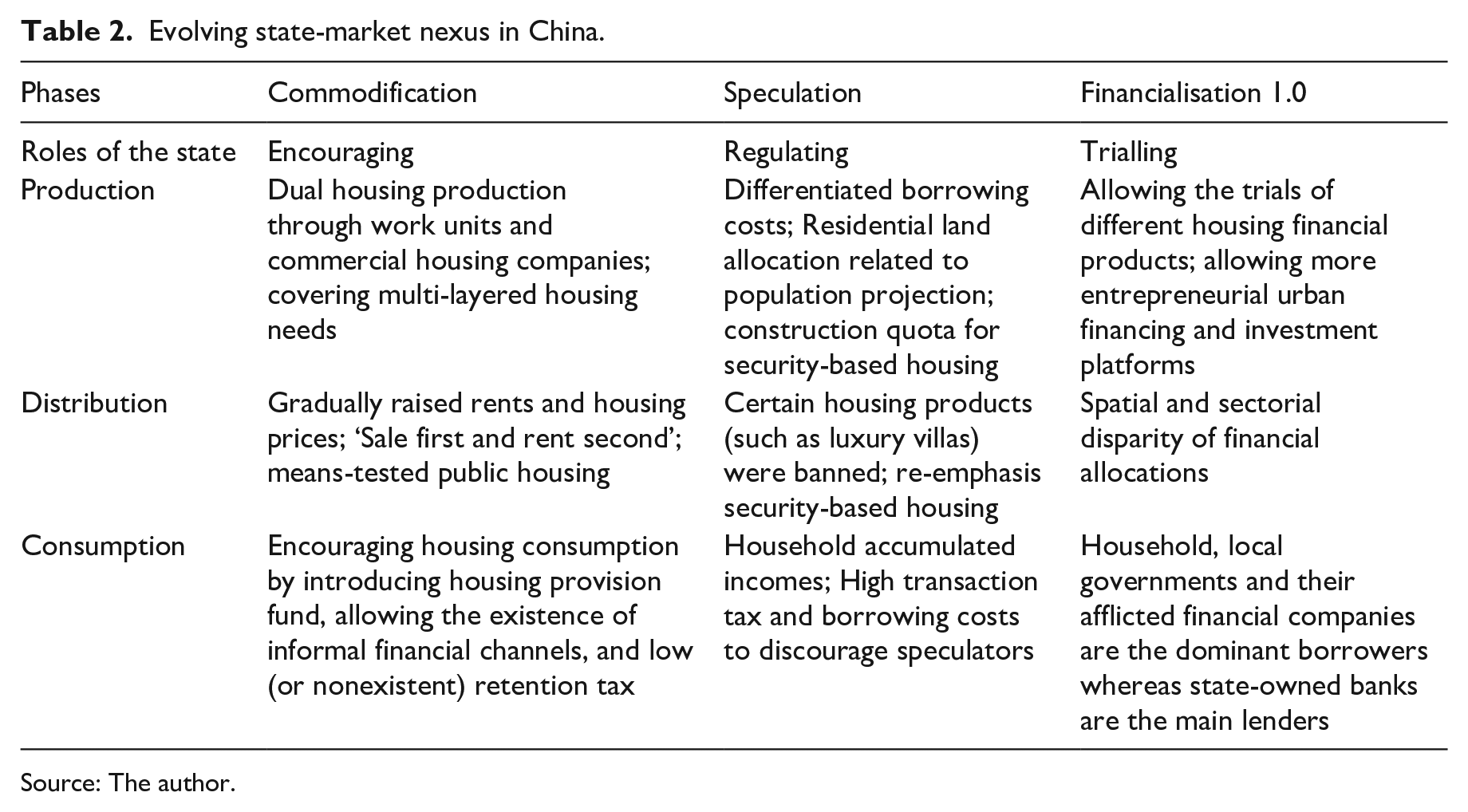

Adopting a constructivist framework in China, three distinct phases of housing commodification, speculation and financialisation 1.0 could be identified, based upon their structural composition, temporal significance and financial maturity (Table 1). Echoing Li et al. (2021), Chen and Wu (2020) and Wu et al. (2019), it is noticed that the Chinese state has been functioning as the driver for the changing system conditions. Lin (2019: 439) summarised how ‘China’s central state and its agents in the banking, financial, and real estate sectors are both owners/sellers and buyers, regulators and developers, rule makers and game players with obvious conflicts of interests, giving rise to peculiar financialisation trajectories’. This section builds upon previous studies by providing a meticulous analysis of how the state-market relations evolve along the housing production, distribution and consumption chain. Adding to the prevalent critics of the financialised regime of accumulation (Lake, 2015) and the speculative state (Chu and He, 2022) in using governance, regulation and even ownership to create financial centrality in order to legitimise and extend its power, this study records a continuous self-adjustment from within the Chinese state in boosting the property market while maintaining a ‘harmonious’ society (Table 2).

Comparing the different phases of China’s housing financialisation.

Source: The author.

Evolving state-market nexus in China.

Source: The author.

Housing commodification (1978 – late 1990s)

Housing commercialisation refers to the process of managing or running the housing sector principally for financial gain (Isaacs, 2016). It starts with housing privatisation and commodification, where housing is treated as a private asset and is primarily for exchange as commodity (Wang and Murie, 1996). In China, the commodity nature of housing was gradually discovered after 1978 along with the economic reform process (see e.g., Chen, 2013; Deng et al., 2009; Wang, 2001). The overall direction between early 1980s and late 1990s was to substitute the state’s role with the market mechanism (Huang, 2004).

Taking an experimental approach, a dual housing production mode was cultivated in this stage (Wang and Murie, 1996). On the one hand, state-owned enterprises or work units still shared some housing provision responsibility by, for example, setting up their special housing funds and even affiliated housing development companies for new constructions (Zhang, 2000). On the other, urban housing authorities started transferring their development responsibilities to commercial housing companies in public or collective ownership. These companies were financially independent, but their profits were shared through negotiation with the city governments (Kwok, 1988). A multi-layered housing provision system for different income groups was established in 1994, and the production of commercial housing was tightly controlled by the state (Wang and Murie, 1996). For housing distribution, reform aimed at converting the brick-and-mortar subsidy into a monetary one and then a commodity exchange. To start, the central government required new housing distribution to follow the principle of ‘sales before rent’ (Wang and Murie, 1996). Base-price had been raised several times and differentiated price range was introduced to cater for different income levels (Chiu, 2008). By 1998, almost all newly developed urban housing was distributed on a monetary basis (Wang et al., 2005). Housing consumption in this stage relied primarily on households’ accumulated income, partially because the rigid borrowing regulations (Deng et al., 2009) and partially because the lack of a debt culture in China until recently (Wu et al., 2020). To stimulate housing consumption, various policies had been trialled, including a compulsory housing provision fund and the tolerance of informal financial channels (Zhang, 2000).

In this stage, housing in China had not acquired its fullest commodity meaning or properties as in the West. Housing as a social goods was still deeply imprinted in the minds of Chinese citizens, work units, and governments (Wu, 1996). Wang and Murie (1996), for example, noted that China’s housing ownership surged in the 1990s mainly because the sales of public housing to in-situ tenants. The sales were offered at a government-determined standard rate that was much lower than their cost price for a substantial length of time. Correspondingly, buyers got the use right (high access rights) but were often subject to various restrictions on resale (low disposal rights) (Wang et al., 2005). As a result, the bulk of commercialised housing transferred before the late-1990s featured a partial ownership that was effectively shared between households, work units and/or local governments. The right to access the use value of housing was the primary concern of both individuals and governments in this process.

The 1980s and 1990s witnessed the establishment and expansion of a commercial housing market on both the primary level (mainly occupied by private developers and wealthy households) and secondary level (mainly resales of public housing) (Zhang, 2000). Real housing assets (as use goods) were the returns to households for their consumption purpose, or work units as the middlemen before 1998. By supplanting housing’s welfare function with a consumption function, the period of housing commodification has been argued to have laid the foundation for assetisation (Wu et al. 2020) – hence it is distinguished as one of the pre-financialisation phases in this paper. Although housing speculation and commodification are closely related in the West (Wood, 1956); in China, these two phenomena did not appear simultaneously, and they are embedded in different state-market relations, as will be discussed later.

Housing speculation (Late 1990s – mid-2000s)

The Asian financial crisis and the Chinese government’s market stimulus package, especially its 1998 Notice on Further Reform of Urban Housing System and Speeding Up Housing Development, was regarded by many as the watershed in China’s housing reform history. This policy replaced direct housing distribution with cash subsidies; created a diversified housing supply system with state-supported commercial housing as the main form; and directed attention to new housing finance system to help developers and individuals with loans and mortgages. Moreover, the Chinese government had been very interested in creating a secondary mortgage market since this period, and had set up pilot programs for mortgage-backed securitisation (MBS) through the China Construction Bank (Deng and Fei, 2008), transforming the local and fixed nature of real estate into something liquid and tradable on the financial markets (Gotham, 2009). Although limited to trust certificates traded on the interbank bond market and investment fund certificates traded on the stock market, this pilot allowed for the fix of several regulatory problems (Chiquier, 2006). By the end of 2007, 7.18 billion RMB worth of MBS had been issued. The PBoC also developed the National Corporation and Individual Credit Information Database in 2003, helping commercial banks to price loans appropriately (Shen and Yan, 2009).

Declaring the real estate sector as an important economic pillar by the state in 1998, 2000, 2003 and 2005 repeatedly had successfully stimulated the market and fuelled the continuous surge of housing price ever since (Chen and Wu, 2020), convincing households, developers and financial institutions of the lucrativeness of housing investment. Along with the eagerness to cash in on such a price surge and the further ease of financial regulations, the balance of outstanding home mortgage surged between 1997 and 2007 by more than 250 times (Ren and Wang, 2007). Housing speculation, which refers to the behaviour of gaining high profits in a short period of time through the sale, rental and leasing of real estate (Liu et al., 2013) anchored on extrapolative expectations of past housing price growth (Gao et al., 2020), had become a prominent feature of late 1990s to mid-2000s (Feng et al., 2011; Wu, 2015). Traditionally, housing speculation is measured by the fraction of non-owner-occupied home purchases against all transactions (Gao et al., 2020). But given the poor data availability during this period, housing vacancy rate and the average rooms per capita in a household could be used to estimate this variable. Liu et al. (2013), using the Census of Urban Households Housing Conditions, estimated that the housing vacancy rate was 4–5% in the 2000s, and 18.6% of households occupied more than four rooms per capita in 2010, raised by 5.3% compared to that in 2000. It is very likely that these 18.6% of households occupied more than one property (the average was 2 rooms per capita), indicating the scale of housing speculation.

Analysed through a constructivist framework, three features differentiate housing speculation from the previous phase. In terms of housing rights, both the Chinese government and citizens had gradually accepted its monetary bearing. On the one hand, salaries had been significantly uplifted, and together with the housing provident fund, were supposed to be the primary means of housing purchase (Shen et al., 2005). On the other, social housing in China was marginalised and reserved for those lowest income households. Commercial housing in comparison had become the mainstream supply, accounting for 76.5% of total supply in 2010 for example (Liu et al., 2013). In terms of the ownership rights, speculators were mainly concerned with the rights of disposal (instead of access). In terms of the ownership composition, speculators either obtained complete ownership through outright purchase (Wang et al., 2005), or shared the ownership with financial institutions instead of with their work units or local governments as was previously the norm. The changing attitude of financial institutions from one of caution to one favouring residential mortgage lending facilitated this process (Zhang, 2000). By 2005, with an outstanding balance exceeding 2 trillion RMB, China had become the largest residential mortgage market in Asia (Deng and Liu, 2009).

Since speculation requires subsequent transactions to realise capital gains, the secondary housing market is where the bulk of speculation happens. Its share had increased from 0% in 2000 to 4.6% in 2010 among all sources of homeownership origins (Liu et al., 2013). On the primary market, although China had established a unique forward real estate market where the developers could sell a housing unit before its completion (Chen and Wu, 2020; Deng and Liu, 2009), housing flip at the pre-sale stage was not common and was later prohibited (Yang and Chen 2014). Another unique feature is that compared to speculation on the demand-side, land speculation on the supply-side started earlier, and underpinned a large proportion of the entrepreneurial local states’ revenue stream.

For both demand- or supply-side speculations, expected quick and higher capital return was the fundamental motivation. It is worth emphasising that although the financial sector plays an important role in housing speculation, it is neither a necessary nor sufficient condition for speculation to occur. Gao et al. (2020), for example, found that housing speculation in the US was largely independent of credit expansion to subprime households during the 2000s. In China, given the embryonic financial system and market forecasting techniques, housing speculation between the late 1990s and early 2000s was primarily derived from a herd mentality of individuals and developers (Feng et al., 2011), the lack of other investment channels, and the inflated expectation of real estate assets (Chen and Wu, 2020). Domestic financiers were responding to the growing demand for homeownership instead of the other way round as noticed by Aalbers (2019) in more matured housing financialisation markets. There was limited penetration of global capitals and hardly any global corporate landlords in China’s real estate market. These features, therefore, differentiate housing speculation from financialisation. But this phase further paved the trajectory for a fuller unfolding of housing financialisation in China, as will be discussed next.

Housing financialisation 1.0 (after 2008)

Focused discussions on housing financialisation emerged very recently in China. This is not surprising given the fact that the manifestation of financialisation relies on a comprehensive financial system, growing institutional and individual investors, as well as a wider and higher acceptance of financial risks in the society. It is argued that a progressive relation can be observed between housing commodification, speculation and financialisation. Housing commodification laid the legal and structural foundation for housing financialisation, as it not only transformed Chinese urban citizens from welfare receivers to independent consumers and potential investors, but also necessitated the restructuring of the housing financial system (Zhang, 2000). In between, housing speculation resulted in a higher acceptance of financial risks among citizens, developers, financial sectors and local governments, further preparing the mentality for financialisation. Yet their progression is contingent upon the vertical and hierarchical dynamics of state power (Lin et al., 2019), making China a distinct example of variegated housing financialisation.

It is worth pointing out that state intervention in housing financialisation is not confined to China. As Aalbers (2019: 380) pointed out, ‘mortgage securitization is deeply shaped by the state and can only exist thanks to the market-making capacities of the state’. But for many liberal markets, state intervention is only prominent in the initialisation and legalisation stage of financial products. The financial institutions often take over the lead in capital distributions and consumptions (Van Loon and Aalbers, 2017). In comparison, the Chinese state could manipulate the whole capital circulation to a greater or lesser extent, as the major commercial banks and financial institutions are either state-owned or state-controlled. Moreover, it is noted that the Chinese national and local governments have been increasingly resorting to financial instruments in achieving their governance goals instead of direct intervention in the housing sector (Li et al., 2021), signalling a divergence from previous phases and a convergence towards the international financialisation of the state and the (semi-)public sector. Termed financialisation 1.0, as there is still a noticeable gap between China’s current housing system and a well-financialised regime (see below and Chen and Wu, 2020), the focus of analysis here is shifted from the bricks-and-mortar interventions towards the manipulation of capital production, distribution and consumption.

At the initialisation stage, global literature has primarily focused on mortgage debt and mortgage securitisation as key drivers of increased domestic credit and market volatility (Aalbers, 2019). In China, scholars highlight the intertwined land-finance and housing assetisation as instrumental in creating credit and the indigenous dynamics of the Chinese regime of accumulation (Wu et al., 2020). In particular, Chen and Wu (2020: 1) noted how ‘housing financialisation boosts the demand for housing assets, and land financialisation speeds up the supply to meet such demand’. The state could manipulate the speed and scale of financialisation by setting up arbitrary loan-to-price ratio and mortgage interest rate. It could also establish/abolish financial products and practices when this was seen as necessary. The pilot of China’s mortgage-backed securitisation (MBS) for example, started in 2005 with the issue of the Administration of Pilot Projects for Securitisation of Credit Assets Procedures by the China Banking Regulatory Commission (Dong et al., 2009). However, due to concerns about financial stability at the end of 2008, the major financial administrative bureaus in China impeded the operation of the pilot programme by simply not approving any transactions. It was only until 2012 and 2013 that new regulations were issued and reignited the pilot (Wang, 2014).

Housing assetisation is argued by Wu et al. (2020) as underpinning housing financialisation in China. It emerged in the previous phase of housing speculation when future value appreciation had been proactively exploited by speculators. What distinguishes housing financialisation 1.0 are arguably the scales and asset holding period. It was reported that in 2019, 41.5% of the Chinese households possessed more than one property, and 60% of Chinese citizens’ wealth was tied with real estate, 28.5% higher than the average in the US (PBoC, 2020). Moreover, it was noticed that housing vacancy rates reached 22–26% in major cities, and investors tended to hold a long-term horizon in capitalising their assets (Phoenix Real Estate, 2017). This has partly underpinned the growth of the long-term apartment rental market in China, especially the asset-light model, where real estate agencies lease properties from individual owners on a long-term basis, and then sublet the properties on behalf of landlords (Chen et al., 2022).

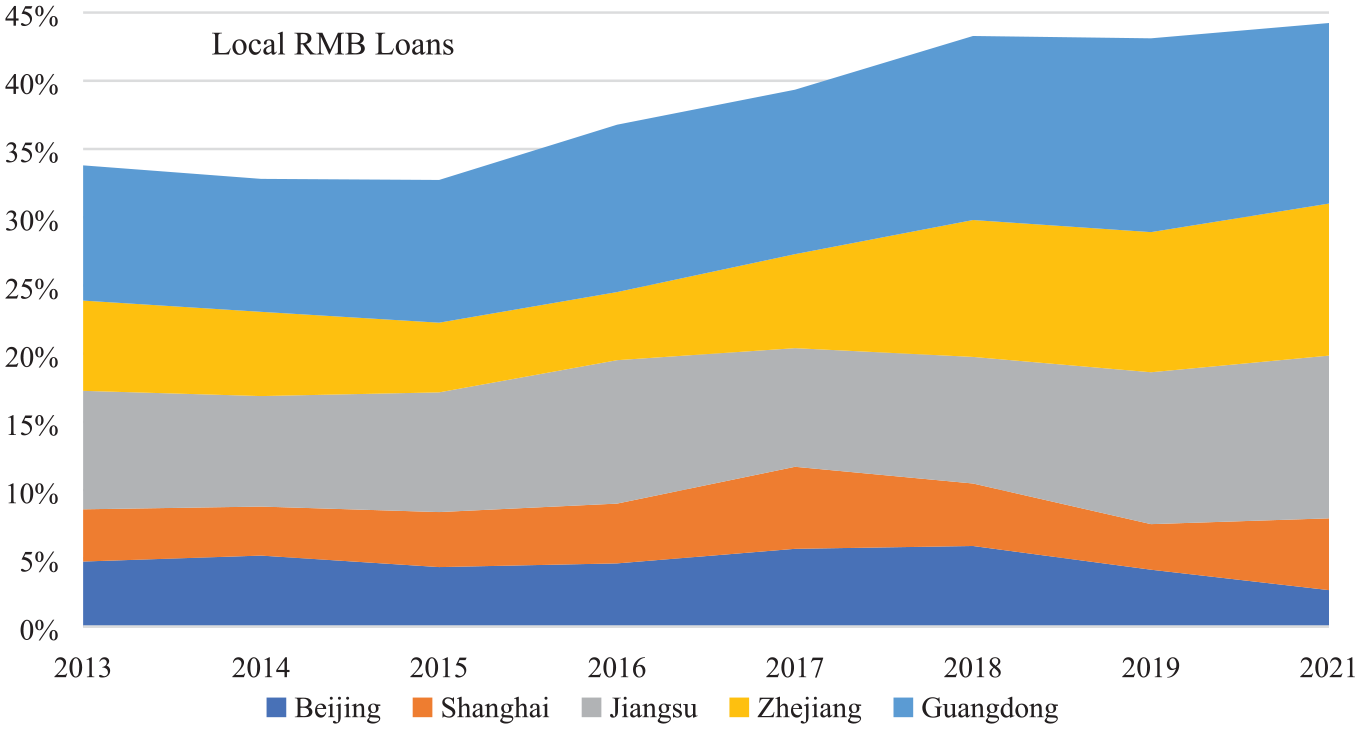

The influence of a ‘shareholding state’ (Wang, 2015) could also be felt in the distribution of capital, which is highly uneven – and politicalised – in China. Lin et al. (2019) for example, denoted a periphery-to-core capital transfer. Beijing’s central position in attracting financial institutions and hence controlling the capital flows nationwide is prominent. The total revenue and registered capital of state-owned banks located in Beijing was 498.9 billion RMB and 16.8 trillion RMB by 2015, accounting for 27.3% and 26.9% of the national total respectively. In the second place, state-owned banks in Shenzhen recorded a much smaller revenue of 299.8 billion RMB and registered capital of 8.1 trillion RMB, 16.4% and 13.0% of the national total (Lin et al., 2019). The bulk of mortgage loans, therefore, are issued to qualified households in these ‘financial hubs’, and lending decisions in lower-tiered cities and towns might also subject to the approval of their headquarters. Figure 1 for example, shows the RMB loans (primarily mortgage loans) issued by the top five municipals and provinces. Together, they accounted for 35–45% of total RMB loans issued in China between 2013 and 2021, demonstrating the concentration of capital distribution.

Proportions of regional RMB loans.

On the consumption of capital, the Bank of International Settlements (BIS, 2020) noted that China’s total household debt as a share of GDP reached 48.1% in 2017, among which domestic mortgages comprised 21.86 trillion RMB, or 31.9% of GDP (Wu et al., 2020). On the household level, it was reported that 57% of households in China had debts in 2019, among which 77% had mortgage loans, worth 3.89 million RMB per household, and accounting for 76% of their total household debts (PBoC, 2020). Partially fuelling this household leverage ratio, more and more financial innovations, such as relay mortgages and reverse mortgages, had been introduced since late 2000s, expanding the choices available to (potential) homeowners. But it also made the housing finance market riskier and increasingly more complicated for normal Chinese to comprehend.

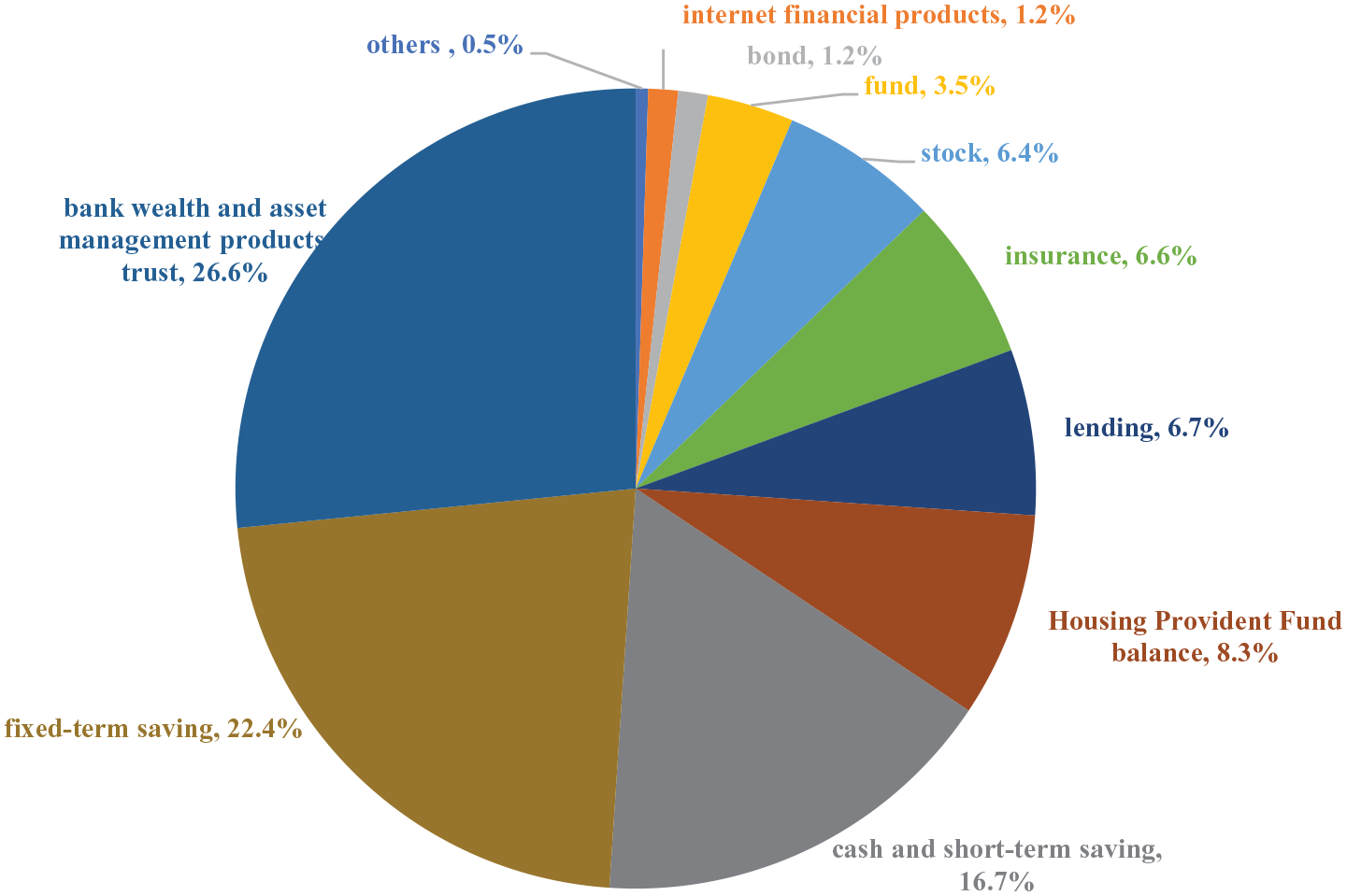

It is also worth noting that financial assets only accounted for 20% of total household assets in 2019 (Figure 2). This was largely caused by the lack of financial investment culture and products in China. MBS for example, should have been very attractive to investors due to mortgage loans’ stable cash flow and high credit rating. However, the Chinese commercial banks are not very keen to securitise mortgage loans exactly because they are regarded as safer loans. To increase asset liquidity and limit the costs of securitisation, these banks tend to retain MBS within their realm through interbank trading, thus reducing MBS to a mechanism of exchanging benefits and sharing risks among insiders (Wu and Deng, 2010).

Composition of financial assets of urban households.

Examined through a constructivist framework, housing consumers in financialisation 1.0 tend to have a partial ownership that is shared with financial institutions. Compared to the phase of housing speculation where consumers often obtained full ownership early on, a partial ownership is a must in a more developed financialisation arrangement, when ‘financial institutions mobilising mortgages as a speculative form of rent, and land and housing titles given to ‘homeowners’ as claims on their future labour’ (García-Lamarca and Kaika, 2016: 319). In other words, the desire for homeownership is used by the financial institutions (and real estate agencies) to lure households onto the housing ladders, so that their mortgage repayments could be turned into profitable financial products that get further traded between various financial institutions. To secure a smooth and predictable capital flow, financial institutions tend to make the mortgage serving term rigid so to discourage early repayment, refinancing and/or switching lenders (Deng and Liu, 2009). This ownership structure also impacts consumer rights, as financial lenders have the first right to recover their losses through property collaterals when default happens. This puts individual households in a much more vulnerable position compared to the eras of housing commodification and speculation, when households might lose money but not their homes.

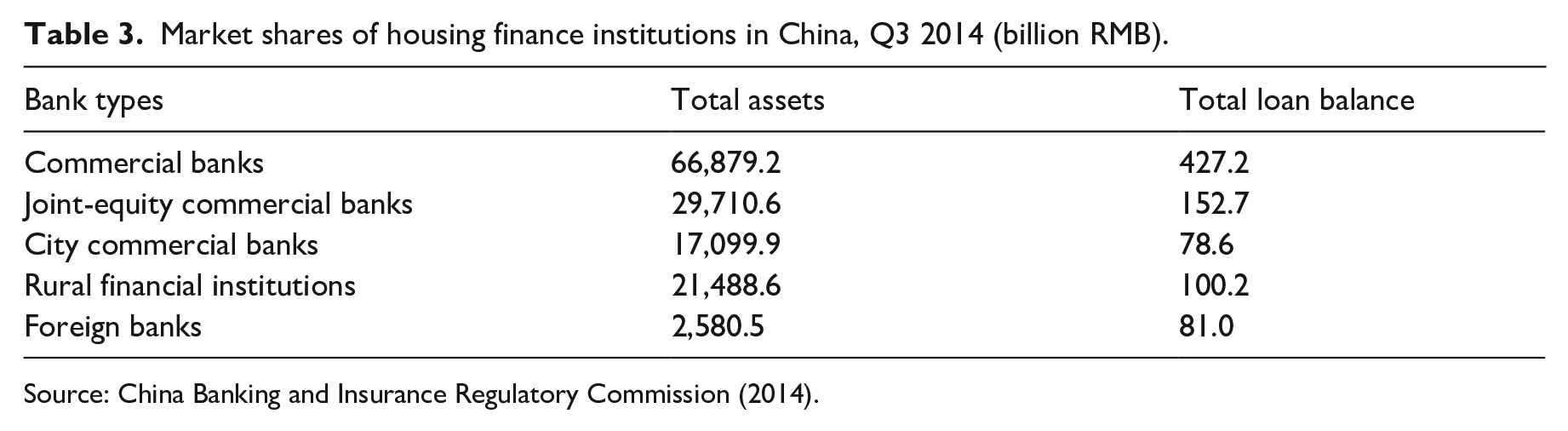

The main market arena for housing financialisation 1.0 is the first mortgage market between households and lenders, and increasingly, the secondary mortgage market between lenders and investors. But in the chasing of a complete capital cycle, the primary and secondary housing markets, such as the rental market, are also part of the jigsaw (Fields and Uffer, 2016; Wijburg et al., 2018). Chen et al. (2022), for example, draw our attention to the ‘rental loan’ as important financial vehicle used by asset-light long-term apartment rental firms. It is worth noting that the scale of China’s secondary mortgage market is still relatively small and products are often treaded inter-institutionally (Deng and Fei, 2008). On the first mortgage market, the ratio of households with mortgaged homeownership was 43.4% (PBoC, 2020) compared to over 50% in the US, leading Chen and Wu (2020: 7) to argue that at the household level, ‘the Chinese housing regime shows an emerging financialisation trend rather than a well-financialised status.’ Yet latest data suggested that by the end of 2019, the ratio of household debt to disposable income had surged from 44.77% in 2007 to 128.59% in 2019, close to the peak value (130.88%) before the subprime crisis in the US. Among the total household debt, the balance of household mortgage loans had increased by 11.14 times, from 2.7 trillion RMB in 2007 to 30.07 trillion RMB in 2019, which grew faster than the total household debts. So it is evident that the surge in household leverage was largely owing to the rising home loans (Sheng et al., 2021). Moreover, China had lifted the restrictions on foreign bank branches conducting full operations of both foreign-currency business and RMB business in the country in 2006, and had further eased the constrains in 2011. By the end of 2014, there were 48 foreign commercial banks providing housing finance in China, although their shares were still smaller compared to the major Chinese commercial banks (Table 3). Also divergent from the phases of housing commodification and speculation, returns to investors at financialisation 1.0 are capitalised future income flows via interest, dividends and/or capital gains related to housing assets, which are subjected to more rigorous economic modelling and market analysis than before (Dong et al., 2009). Motivations of financial investors also arguably differ from speculators, as they are not only seeking for higher returns but also to diversify their investment portfolios.

Market shares of housing finance institutions in China, Q3 2014 (billion RMB).

Conclusion

This paper adds to the literature on variegated housing financialisation through a case study of China. Two arguments are made: first, the temporal variation of financialisaton is an important sub-theme worth exploring further. Second, the role played by the state is an important mediating factor of a financial geography. This paper draws our attention to the evolving state-market nexus and the intrapreneurial adjustment of the public sector in this process. It is also worth pointing out that local variations in the state-market nexus could further temper a generalised reading of housing financialisation, which, however, is beyond the scope of this paper.

The constructivist analytical framework proposed in this paper bears the potential of comparing housing financialisaton across spaces and time. Focusing on housing rights, ownership, markets, returns and motivations, and using China as an illustration, this paper distinguishes at least three periods of reform that characterised by different understandings of ‘housing’ and ‘housing finance’. Housing commodification (early 80s – late 90s) initialised the transaction and asset-based housing system, and underpinned the subsequent growth of housing financialisation both structurally and psychologically. Housing speculation in China (late 90s – mid-2000s) had stimulated its early property market boom-and-bust and legal system development. China’s financialisation 1.0 (since 2008) started to exhibit some of the key financial features. But differ from Wijburg (2019)’s use of ‘financialisation 1.0’ in the liberal markets, where private equity funds and opportunistic investors were regarded as the main drivers, China’s embryotic financial activities were mainly led by governments, developers and banks (Lin et al., 2019; Wu et al., 2020).

More broadly, this paper calls for something of a re-think in the approach to investigating housing systems in emerging capitalist economics and/or the global south. Simply adopting seemingly relevant terminologies crafted in the West may undermine both unique local histories and contexts, but also obscure important differences in understanding, and meanings underlying, those terms as they translate from English. Mobilising the heuristic of ‘uneven and combined’ development (Fernandez and Aalbers, 2020), this paper indicates the value of a locality-based, bottom-up approach to interpreting and comparing evolving housing systems, housing financialisation and its impact on socio-economic development at large.

Footnotes

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.