Abstract

Purpose

This study contributes to the literature on the inclusivity of microfinance, by examining non-participation in Kudumbashree, a welfare-oriented microfinance initiative in Kerala, India, through the lens of social exclusion.

Study Design

The study integrates both quantitative and qualitative data. A survey was conducted among 678 rural poor households in Kerala, supplemented by in-depth interviews and focus group discussions.

Findings

Despite the programme’s provision of financial and non-financial benefits, women from the most marginalised backgrounds encounter certain barriers in participating in Kudumbashree, leading to passive/implicit exclusion. The observed positive association between participants’ debt attitudes and their likelihood of continued engagement in the programme, highlights the role of financial incentives in enhancing retention rates of welfare initiatives.

Contributions

This paper offers several policy insights for improving the inclusivity of microfinance programmes. Conceptually, it highlights the paradox that policies designed to combat social exclusion may unintentionally reinforce it. The paper argues that institutional exclusion in social protection schemes—where participation is voluntary and conditional—can manifest implicitly through the interplay of three factors: design-stage conditions, their operational-stage enforcement, and individual-level limitations in meeting them.

Implications

To enhance participation in welfare-oriented microfinance programmes, targeted awareness sessions fostering group solidarity and team cohesion are recommended.

Introduction

Microfinance is increasingly recognised as a significant component of poverty eradication strategies in developing nations, occupying a central position in contemporary development discourse (Dichter, 2007; Oommen, 2008). Research highlights its pivotal role in financial inclusion, poverty alleviation, and women’s empowerment, particularly among socially and economically disadvantaged groups (e.g., Abel, 2020; Ismail et al., 2024; Lacalle-Calderon et al., 2018; Maity, 2019). Case studies further suggest that adopting more people-centric approaches can improve the effectiveness of microfinance programmes in reducing social exclusion (e.g., Bahng, 2013; Maity, 2023). Nevertheless, concerns persist about microfinance’s ability to reach the most vulnerable populations (e.g., Coleman, 2006; Hulme & Mosley, 1996; Lonborg & Rasmussen, 2014; Navajas et al., 2000). This concern stems from the recognition that the impoverished, who constitute the primary beneficiaries of microfinance, are not a homogenous group. Rather, variations and fluctuations in household well-being arise due to the dynamic nature of poverty and disparities in the socio-economic capital possessed by different households (Montgomery, 1996; Rahman & Razzaque, 2000).

While empirical research on microfinance has expanded globally, there remains a lack of comprehensive, objective, and independent academic inquiries on why certain eligible households choose not to participate, particularly in diverse contexts. Often, the predominant focus on measuring the impact of microfinance programmes on clients has arguably side-lined research into the exploration of the process of participation (Mahmud, 2000). Since participation aligns with household livelihood strategies, especially for those facing poverty, understanding these mechanisms is crucial (Mahmud, 2000). Furthermore, the lack of representative quantitative data to examine exclusion at various stages of programme implementation, coupled with insufficient qualitative insights to investigate the reasons for this exclusion, has constrained the scope of available studies.

Recognising this gap in the literature and leveraging our prior research experience in microfinance, this paper aims to provide robust empirical evidence on the factors and reasons driving exclusion in microfinance programmes, while offering a strengthened conceptual framework to understand these dynamics. To this end, we examine non-participation among eligible households in Kudumbashree, a welfare-oriented microfinance initiative implemented by the Government of Kerala, India.

Specifically, this paper attempts to answer the following question: despite the financial and non-financial benefits provided by the programme and the government’s concerted efforts to encompass all poor households, why do certain women from rural poor households in Kerala abstain from participating in Kudumbashree, and what distinctive characteristics define this group? Although primarily empirical in nature, this paper also employs the lens of social exclusion to investigate if any particular population group—defined by social category, religion, and economic status in the Kerala context—faces institutional barriers in participating the programme. Additionally, it examines how attitudinal factors, particularly attitudes towards debt, influence participation decisions. By combining quantitative and qualitative insights, this study sheds light on the paradoxical processes of exclusion that could be embedded even in welfare-oriented microfinance programmes or similar social protection initiatives, specifically designed to address multiple forms of socio-economic exclusion, marginalisation, and vulnerabilities. On a broader conceptual level, we argue that institutional exclusion from social protection schemes—where participation is voluntary and conditional—can occur in implicit ways that are often overlooked.

Our choice of the social exclusion framework as the analytical lens of this paper is driven by its dynamic, multidimensional, and relational nature, which encompass a broader spectrum of social challenges (Berghman, 1995; Mathieson et al., 2008). While welfare policies and social protection programmes are widely recognised as crucial mechanisms for alleviating social exclusion (Kidd, 2014; Room, 1995), prior research has highlighted the risk of institutional exclusion potentially rooted within these policies. For instance, Daly (2006) and Kidd (2014) argue that flaws in policy design or implementation may unintentionally reinforce existing patterns of exclusion and discrimination, thereby perpetuating disadvantage. Consequently, in alignment with the European Commission (2008) and Levitas (2006), we acknowledge the importance of rigorous evaluation and monitoring of social inclusion policies. However, we believe that such evaluations should also incorporate ‘inclusiveness’ as a core dimension, for which the social exclusion framework can serve as a valuable analytical tool.

This study is particularly significant in the Indian context. Despite India being one of the world’s largest microfinance markets, limited academic research has examined the determinants and causes of non-participation in microfinance programmes. Most existing studies on the issue originate from Bangladesh or Africa (e.g., Evans et al., 1999; Islam, 2011; Karim & Osada, 1998; Lonborg & Rasmussen, 2014; Pearlman, 2014). Our approach diverges from these studies in several ways. First, unlike many studies that adopt either a quantitative or qualitative lens, providing only a partial understanding, ours integrates both quantitative and qualitative data, offering a more nuanced perspective on the phenomenon of non-participation. This dual approach enables us to discern whether specific communities experience exclusion from the programme and if the reasons for non-participation differ across population groups.

Second, existing literature has not explored how eligible participants’ debt attitudes influence their decision to join or leave a microfinance programme. In contrast, our study incorporates a debt attitude scale in quantitative modelling, recognising its importance given Kudumbashree’s primary role as a source of affordable and accessible credit.

Third, most prior studies focus on specific commercial microfinance programmes run by non-governmental organisations (NGOs) or financial institutions, thereby limiting their scope. Conversely, Kudumbashree’s broader coverage allows for a more comprehensive inquiry into the factors influencing non-participation. By identifying three distinct groups—current members, non-joiners, and dropouts—from a representative sample survey among eligible participants, this study offers a more systematic understanding of the determinants and causes of non-participation. Besides, as an independent study examining a government-sponsored microfinance programme and utilising data drawn from a representative survey collected as part of a larger research initiative, the response bias in our study would be considerably lower compared with studies focused on programmes implemented by specific organisations.

Therefore, Kudumbashree serves as a valuable case study for examining indirect exclusionary processes and unintentional institutional barriers within welfare-oriented microfinance initiatives, despite the many benefits they offer. Understanding these barriers is highly relevant for policy, not only to enhance the outcomes of the Kudumbashree programme in Kerala but also to inform the design and implementation of similar programmes in other developing countries, ensuring that all intended beneficiaries can access the full range of benefits.

The remainder of this paper is organised as follows: Section 2 furnishes the context and relevance of this study and provides a brief overview of the features of the Kudumbashree programme. Section 3 describes the data and methodology employed. Sections 4 and 5 sequentially present the insights derived from the analysis of quantitative and qualitative data. Section 6 synthesises the combined understanding emerging from quantitative and qualitative data, highlighting their policy and theoretical implications. Section 7 concludes the study.

Context and Relevance

Originating in Bangladesh during the 1970s, the concept of microfinance has undergone significant evolution, adapting to diverse contexts and cultures with the proliferation of varied approaches, structures, and operational modes. In India, the Self-Help Group-Bank Linkage Programme (SHG-BLP) is a prominent variant (Ghosh, 2013; Kalpana, 2017), although regional adaptations exist across the country. The Kudumbashree programme launched by the Kerala government in 1998 exemplifies this diversity. With 4.6 million women mobilised into 317 thousand neighbourhood groups (NHGs), 1 this programme is considered the largest SHG-BLP in India, and arguably one of the world’s largest female networks. While broadly adhering to the prevalent SHG-BLP model, this state-sponsored, welfare-oriented, women-centric, poverty alleviation programme, grounded in the concept of microfinance, distinguishes itself with its well-defined decentralised structure 2 and ‘credit-plus’ approach 3 (Oommen, 2008; Williams et al., 2011). 4 With its distinctive features, Kudumbashree has attracted significant academic interest, particularly in relation to gender dynamics (e.g., Agarwal, 2020; Devika & Thampi, 2007; Rajagopal, 2020). However, an underexplored area pertains to the factors influencing enrolment and dropout from the programme.

Motivations for understanding exclusion from microfinance programmes vary based on their goals, structure, and operating context. In commercial microfinance programmes, enhancing participation and minimising dropouts is crucial not only for the well-being of beneficiaries but also for the financial sustainability of the programme itself (Bardsley et al., 2015; Karim & Osada, 1998). Conversely, in non-profit programmes like Kudumbashree, specifically designed for the socio-economic upliftment of vulnerable households, non-participation implies that eligible beneficiaries are excluded from crucial welfare benefits. 5 Moreover, given the diverse models, and operational modes adopted by different microfinance programmes, the elements and processes of exclusion embedded within each may vary. Therefore, it is crucial to study the exclusionary processes across various programmes, each operating within distinct structures, objectives, and contexts.

Accordingly, Kudumbashree serves as a valuable case study due to its three distinct features. First, while previous studies highlight high interest rates in microfinance programmes as a barrier to participation (Panda, 2012; Rahman et al., 2014), Kudumbashree, as a government-subsidised programme, offers loans at lower rates than commercial banks. Second, research supports the effectiveness of a ‘credit-plus’ approach, in enhancing participation and retention in microfinance programmes (Muneer, 2020; Zaman, 1996). Kudumbashree, functioning as a welfare-oriented and poverty eradication programme, offers a myriad of non-financial services to its members. Third, unlike many microfinance initiatives, Kudumbashree explicitly aims for universal coverage of all economically vulnerable households (Section 7.13 of Kudumbashree bylaw, 2021), with the government undertaking targeted campaigns encouraging enrolment. To support this goal, Kudumbashree’s bylaw (2021) uniquely empowers NHGs to waive institutional requirements—such as regular thrift payments and mandatory meeting attendance—based on members’ specific financial and personal circumstances, thereby striving to enhance the programme’s accessibility for everyone.

However, despite all these concerted efforts, the sample survey conducted among rural poor households in Kerala in 2023, from which the data for this paper were drawn, revealed that 30 percent of these households remained excluded from the programme; some have never joined, and others have dropped out. Therefore, an inquiry into why certain eligible impoverished households opt not to participate in Kudumbashree can offer valuable insights into how, even within an almost economically homogeneous group, some households become disadvantaged in their ability to participate in a government-designed programme specifically aimed at providing benefits and addressing the multiple vulnerabilities faced by this group.

In this regard, the social exclusion framework proves useful, as it broadens the focus from individual and household level factors to encompass community-level dynamics and social relations (Atkinson, 1998; Daly, 2006). While no uniform definition for the concept of social exclusion exists—since it varies according to national and ideological contexts (Silver, 1994)—it is generally understood as the process through which individuals or population groups become either wholly or partially detached from the organisations and communities of which the society is composed and from the associated rights and obligations (Kidd, 2014; Room, 1995). Extending beyond the poverty-driven focus on the lack of disposable income or material resources, social exclusion incorporates a broader array of dimensions, including dysfunctions or imperfections within societal systems that disadvantage certain groups more than others (Barnes, 2019; Berghman, 1995).

However, Saith (2001), cautions against the blind application of conceptual definitions or measurement frameworks of social exclusion developed in the context of advanced economies to the realities of developing countries. Given the limited presence of a fully formed welfare state in many developing regions, Saith (2001) suggests an alternative approach; examining social exclusion within the context of social security schemes that have evolved in response to specific local circumstances and unique challenges in these settings. Thus, by examining inequalities in the risk of exclusion and distinguishing population groups based on the cumulative severity of the challenges they face (Paugam, 1995), social exclusion framework can aid in assessing whether a programme’s design and implementation intentionally or unintentionally exclude any specific population segments from its scope. It also facilitates an understanding of the dynamics and processes behind such exclusion.

Finally, previous studies have identified several exclusionary elements and mechanisms within the design and functioning of microfinance programmes that may exclude vulnerable communities, particularly people with disabilities, from participating (Beisland & Mersland, 2014; Bwire et al., 2009; Cramm & Finkenflügel, 2008; Hulme, 1999; Sarker, 2024). Building on these insights and considering the unique characteristics of the microfinance programme under study, this paper seeks to develop a broader framework for understanding the exclusionary processes within social protection schemes that are designed for voluntary participation but require beneficiaries to meet certain conditions.

Data and Methodology

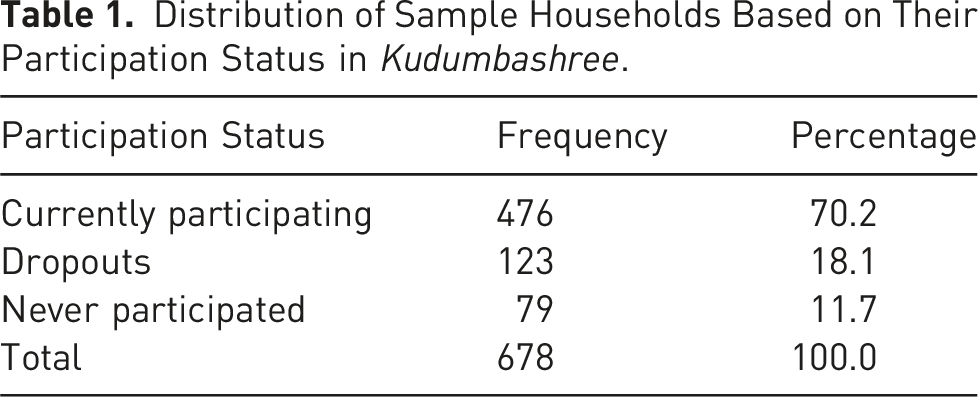

The data for this paper were drawn from a household survey conducted as part of a larger project investigating indebtedness patterns among rural poor households in Kerala. To ensure representativeness, we identified 765 rural poor households 6 using a multistage cluster sampling technique 7 and successfully completed 729 interviews. Data collection took place between November 2022 and May 2023, carried out by 10 professionally trained investigators with prior experience in household surveys. A dedicated section of the questionnaire explored experiences of participation and non-participation in Kudumbashree. Following a thorough review for missing data and inconsistencies, a final sample of 678 households was selected for analysis.

Distribution of Sample Households Based on Their Participation Status in Kudumbashree.

Information regarding households currently engaged in the programme or those that had previously participated but later discontinued was obtained directly from women who were either active or former participants. For households that had never participated, data were collected from the female member with the highest financial decision-making authority within the household. Our study combined quantitative and qualitative data from the same household survey. Given the multidimensional nature of social exclusion, this mixed-methods approach serves as a powerful tool, enabling both an examination of the characteristics of the excluded populations and an exploration of the processes driving their exclusion (Mathieson et al., 2008; Moulaert, 1995).

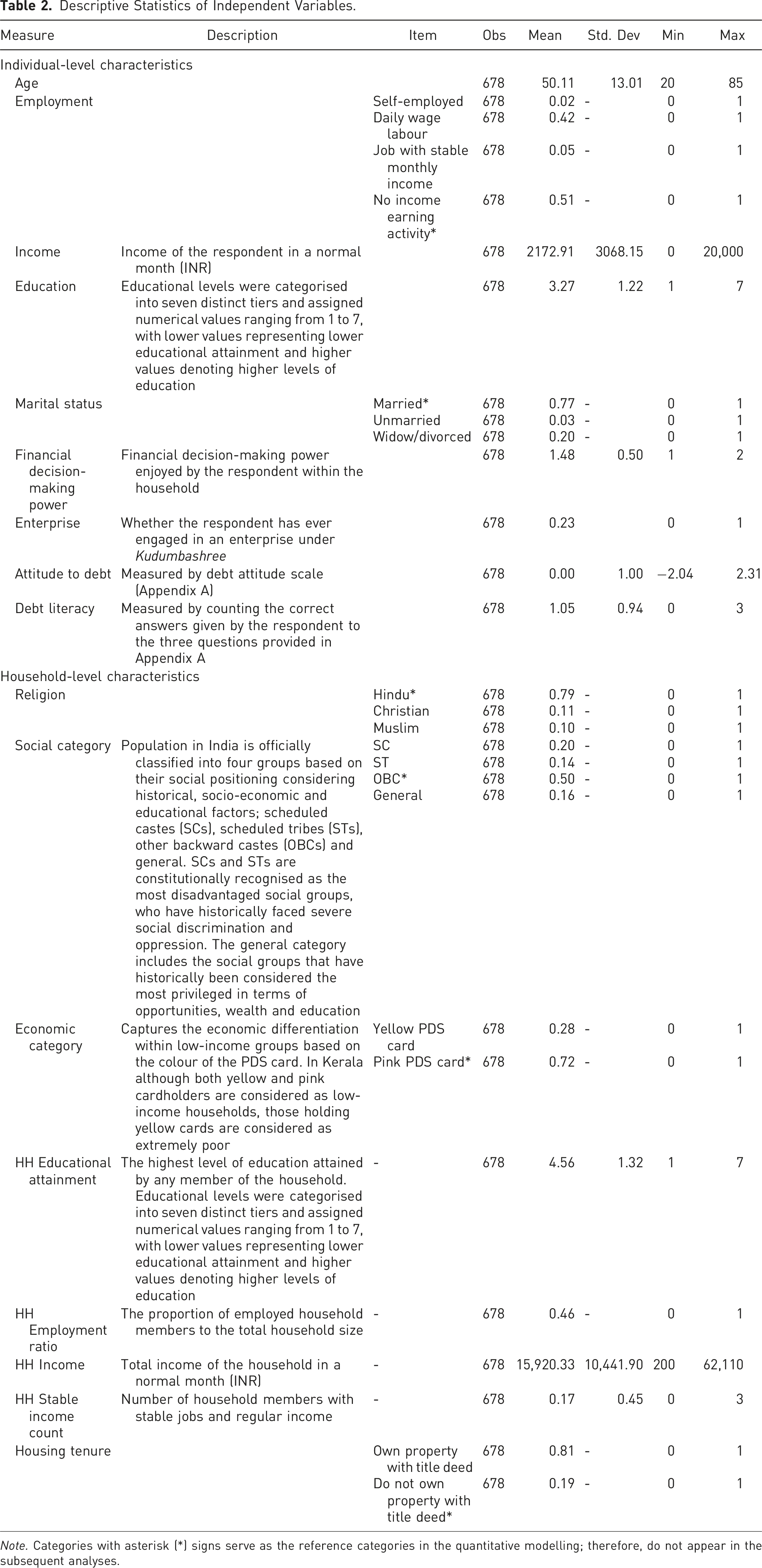

The quantitative component employed two separate probit models to identify measurable characteristics of women or households that influence the likelihood of participation and dropout. This analysis aimed to ascertain if there is a systematic exclusion of any specific population group—defined by social category, religion, and economic status—from the programme. The quantitative analysis also examined if the debt attitude and debt literacy of the respondents significantly influence their participation in microfinance. To this end, we adapted the Debt Attitude Scale developed by Lea et al. (1995) and the Debt Literacy Scale introduced by Disney and Gathergood (2011) to suit the local context of Kerala (see Appendix A). Using survey data, we conducted a confirmatory factor analysis to construct a variable reflecting debt attitude (see Appendix B). The construct meets all established reliability and validity thresholds as per Hair et al. (2019) and MacKenzie et al. (2011).

The qualitative component explored the reasons behind non-participation. In the survey questionnaire, respondents who had never participated or dropped out of the programme were asked to elaborate on their reasons for non-enrolment or discontinuation. Using NVivo, we systematically categorised these responses. From the identified patterns, we also sought to determine if any specific reason predominantly contributed to the non-participation of particular population groups. Additionally, we conducted 27 focus group discussions with current Kudumbashree members and entrepreneurs, alongside in-depth interviews with grassroots-level Kudumbashree leaders in the surveyed panchayats, as well as district- and state-level programme officials. Where relevant, we supplemented our analysis with insights gathered from these discussions.

Quantitative Analysis

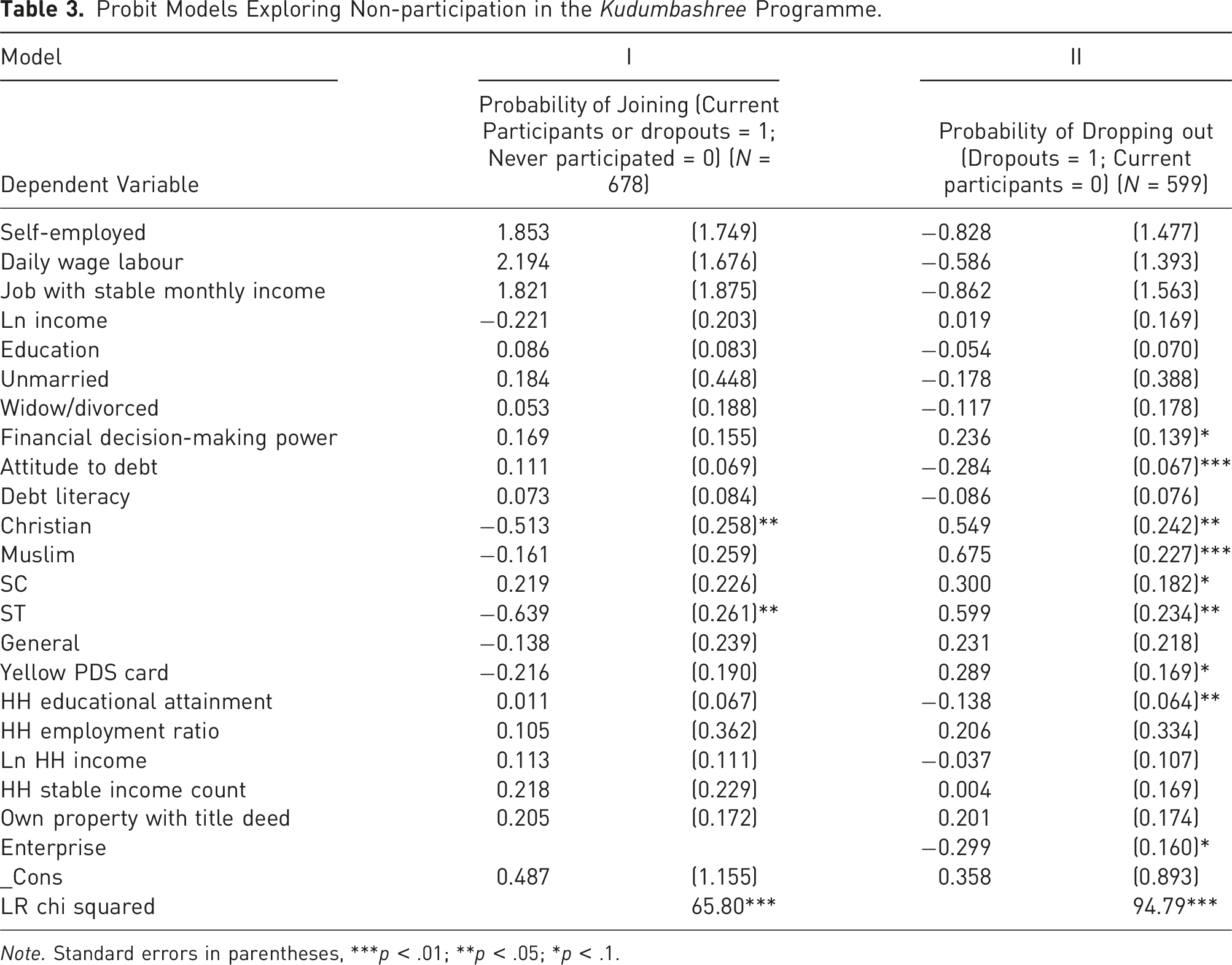

We employed two separate probit models to analyse the factors influencing non-participation in Kudumbashree. The first model assessed the probability of a household joining the programme. For those who had joined, the second model analysed the factors affecting dropout from the programme. To account for potential selection bias in the second stage, we initially considered the Heckman probit model. However, the results indicated no significant selection bias, leading us to opt for two separate probit models.

Descriptive Statistics of Independent Variables.

Note. Categories with asterisk (*) signs serve as the reference categories in the quantitative modelling; therefore, do not appear in the subsequent analyses.

Probit Models Exploring Non-participation in the Kudumbashree Programme.

Note. Standard errors in parentheses, ***p < .01; **p < .05; *p < .1.

As mentioned earlier, to investigate non-participation through the framework of social exclusion, we examined whether certain population groups among eligible beneficiaries—defined by social group, religion, and economic status—exhibit a higher likelihood of either non-enrolment or dropout from the programme. The results suggest that ST women, considered as one of the most underprivileged social groups in Kerala, face exclusion at both the entry and operational stages of the programme, as indicated by their higher probability of non-enrolment and dropping out.

Religion also appears to significantly influence participation. Women from the Christian community are less likely to join the programme compared with their Hindu counterparts. Additionally, the probability of dropout is higher among women from both Christian and Muslim communities than among Hindus. Conversely, economic status, measured by the PDS card colour, seems to have a more limited impact on participation.

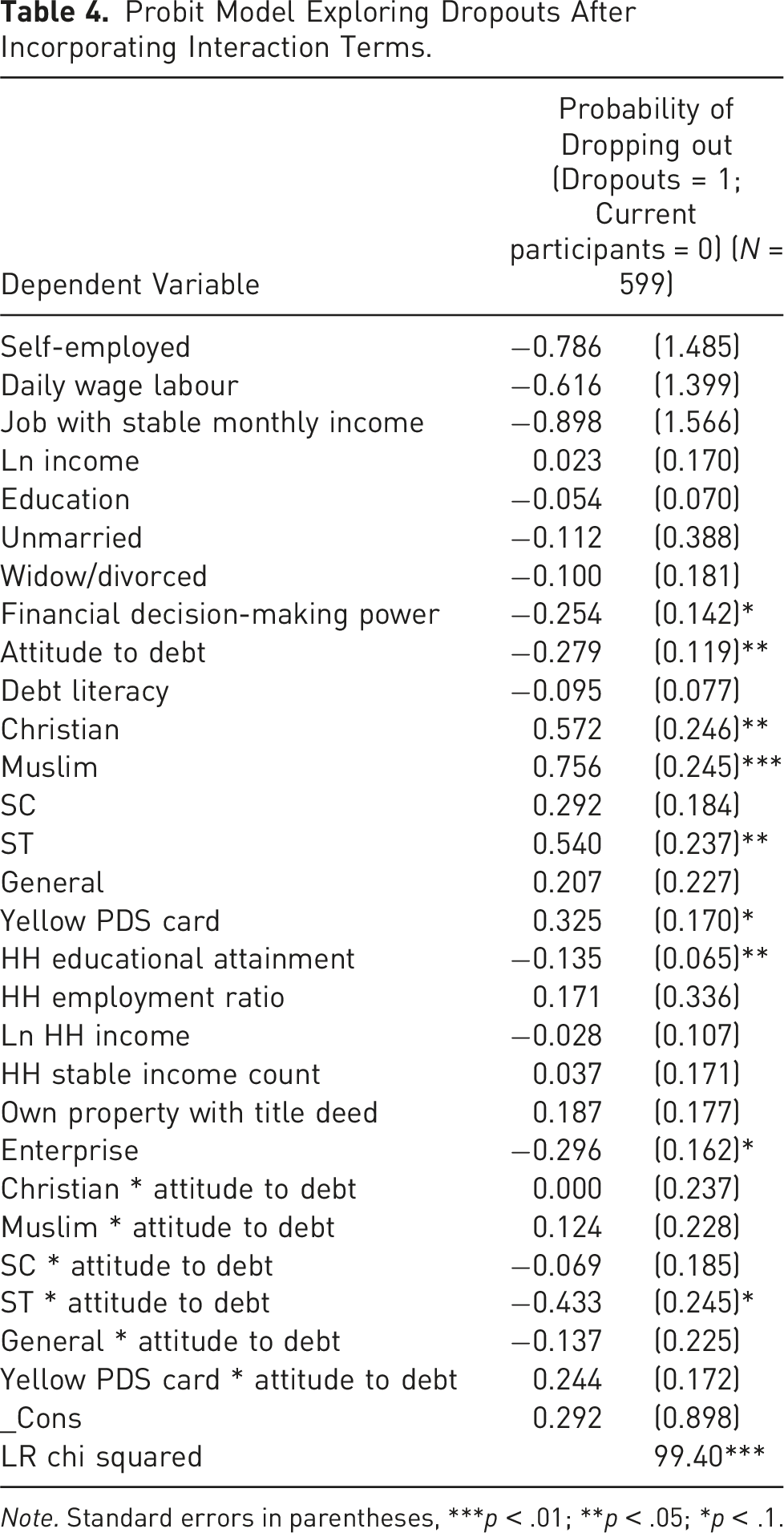

Probit Model Exploring Dropouts After Incorporating Interaction Terms.

Note. Standard errors in parentheses, ***p < .01; **p < .05; *p < .1.

Finally, a negative relationship was observed between the highest educational level within a household, and the probability of women dropping out. This may be because higher education equips family members to recognise and value the benefits of participation, making them more likely to encourage women in their households to remain in the programme.

To verify the robustness of these results, we employed a multinomial logistic regression model with participation status as the dependent variable (results are presented in Appendix C). The dependent variable comprised three outcomes: current participants, non-joiners, and dropouts. To explore potential exclusion from Kudumbashree, the currently participating group was used as the reference category. By calculating the relative risk ratio (RRR), we assessed how the likelihood of being in the non-joiners or dropout groups changes relative to being in the currently participating group, given a one-unit change in the explanatory variables. The results confirmed the relationships observed in the probit models, while also underscoring the significant role of favourable debt attitudes in encouraging continued participation in microfinance programmes. Specifically, individuals with more favourable debt attitudes are less likely to be in the non-joiners or dropout groups compared with the current participants.

Qualitative Insights

The objective of the qualitative data analysis was to elucidate the process of exclusion by examining the reasons underlying certain women’s decisions to abstain from Kudumbashree, despite its provision of numerous welfare benefits. Applying the social exclusion lens, the analysis focused on identifying whether specific reasons predominantly influenced the non-participation of particular population groups.

As previously mentioned, survey respondents who were not currently participating in the programme were asked to explain their reasons for non-enrolment or dropping out. These reasons were collected through open-ended questions in the survey questionnaire.

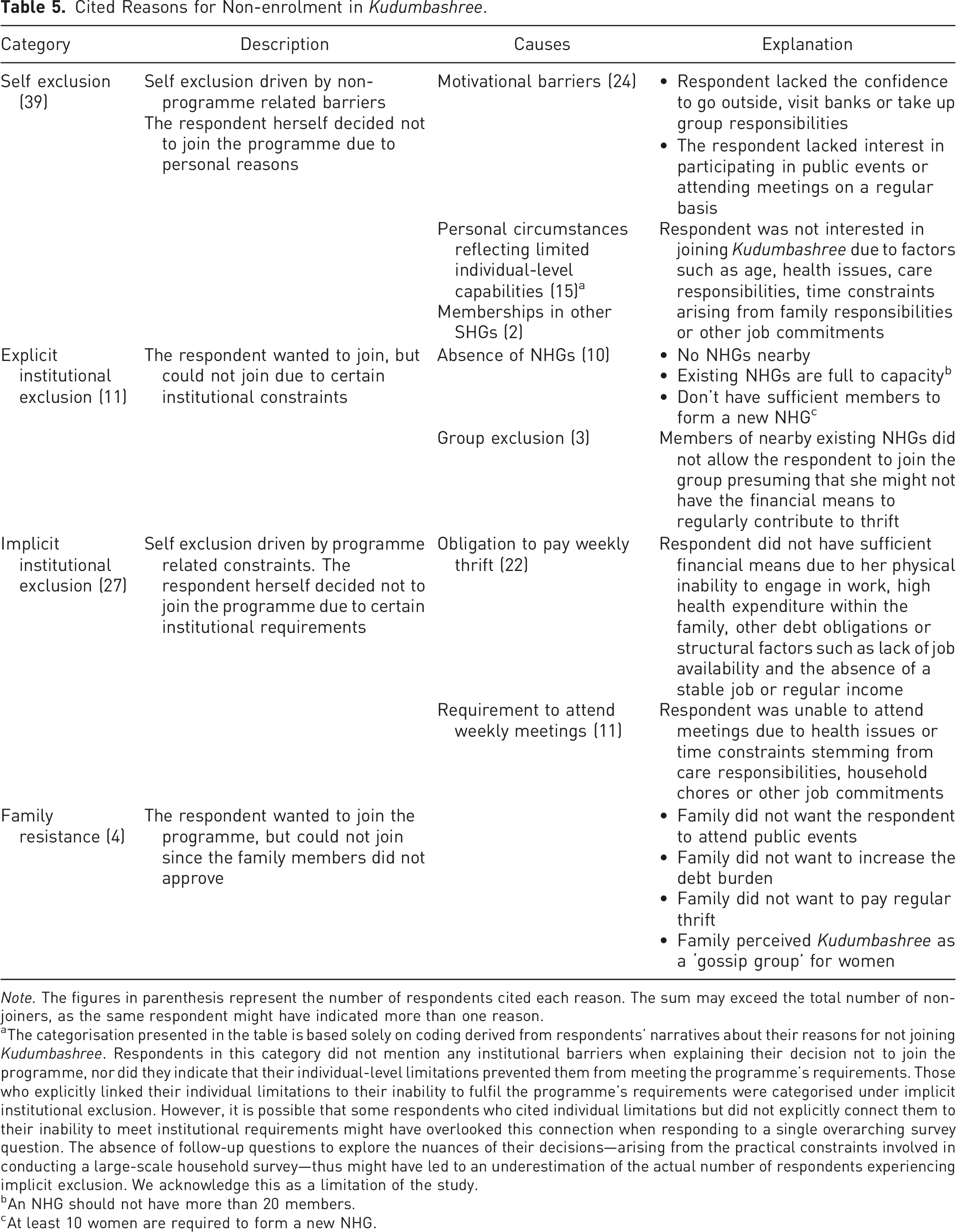

Cited Reasons for Non-enrolment in Kudumbashree.

Note. The figures in parenthesis represent the number of respondents cited each reason. The sum may exceed the total number of non-joiners, as the same respondent might have indicated more than one reason.

aThe categorisation presented in the table is based solely on coding derived from respondents’ narratives about their reasons for not joining Kudumbashree. Respondents in this category did not mention any institutional barriers when explaining their decision not to join the programme, nor did they indicate that their individual-level limitations prevented them from meeting the programme’s requirements. Those who explicitly linked their individual limitations to their inability to fulfil the programme’s requirements were categorised under implicit institutional exclusion. However, it is possible that some respondents who cited individual limitations but did not explicitly connect them to their inability to meet institutional requirements might have overlooked this connection when responding to a single overarching survey question. The absence of follow-up questions to explore the nuances of their decisions—arising from the practical constraints involved in conducting a large-scale household survey—thus might have led to an underestimation of the actual number of respondents experiencing implicit exclusion. We acknowledge this as a limitation of the study.

bAn NHG should not have more than 20 members.

cAt least 10 women are required to form a new NHG.

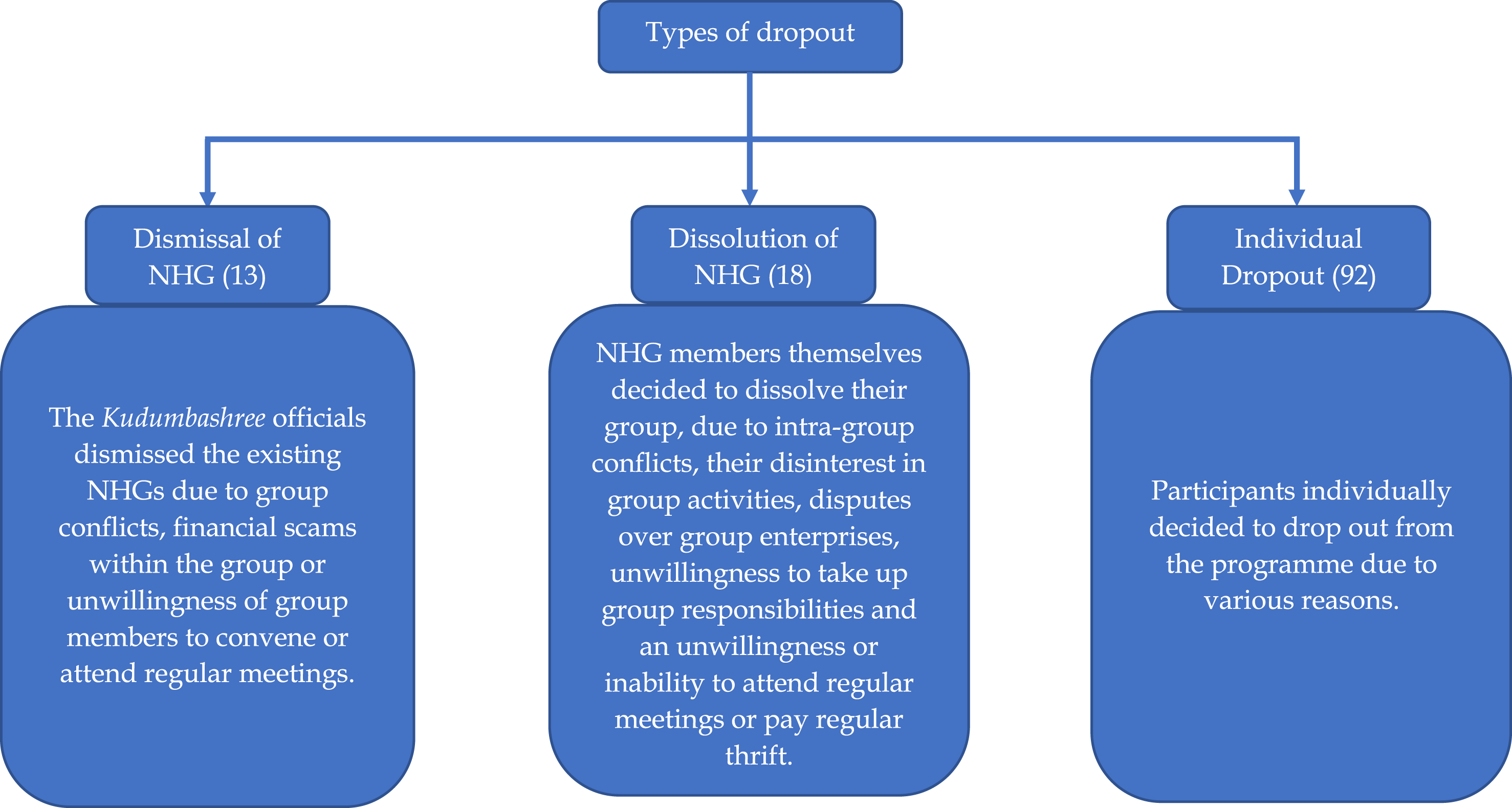

Types of discontinuation from the Kudumbashree programme.

Previous research conducted in non-Indian contexts has sought to classify the reasons for non-enrolment in microfinance programmes into programme related barriers and client related barriers (e.g., Evans et al., 1995, 1999; Hulme, 1999). However, based on the pattern emerged from our data, we recognised that simply categorising the reasons for non-joining into programme-related barriers and client-related barriers, or self-exclusion and institutional exclusion, would not comprehensively capture the complete narrative of exclusion. There were instances where the decision for self-exclusion stemmed from the perceived inability to fulfil the programme-related requirements, amounting to an indirect form of institutional exclusion as articulated by a 60-year-old respondent belonging to the ST category. There is enough work at home. Will not be able to attend meetings amidst all these. And don’t I have to pay thrift every week? From where I will give it when there is no job?

Consequently, in line with Wright (1997), we recognised that distinction between ‘self’ and ‘organisation-driven’ exclusion is largely arbitrary, as the programme designs at times force the potential beneficiaries, particularly coming from socially and economically disadvantaged backgrounds, to ‘self-exclude’. Therefore, we introduced a third category to account for responses indicating self-exclusion driven by programme-related constraints (Table 5).

Table 5 reveals that women who had never participated in the programme mostly attributed their non-engagement to self-exclusion driven by factors unrelated to the programme, chiefly tied to their lack of motivation. Although instances of direct institutional exclusion appeared relatively fewer, programme-related factors frequently influenced the decision to opt for self-exclusion. By aggregating these two categories—explicit and implicit institutional exclusion—the number of individuals attributing their exclusion to institutional factors is almost equal to those citing self-exclusion driven by non-programme-related factors. From a broader perspective of social exclusion, it is possible that motivational barriers, such as lack of self-confidence or hesitancy to attend public events, are shaped by the social capital possessed by each population group, their environments, and their upbringing (de Haan, 2000). However, a thorough investigation into these aspects is beyond the scope of this study.

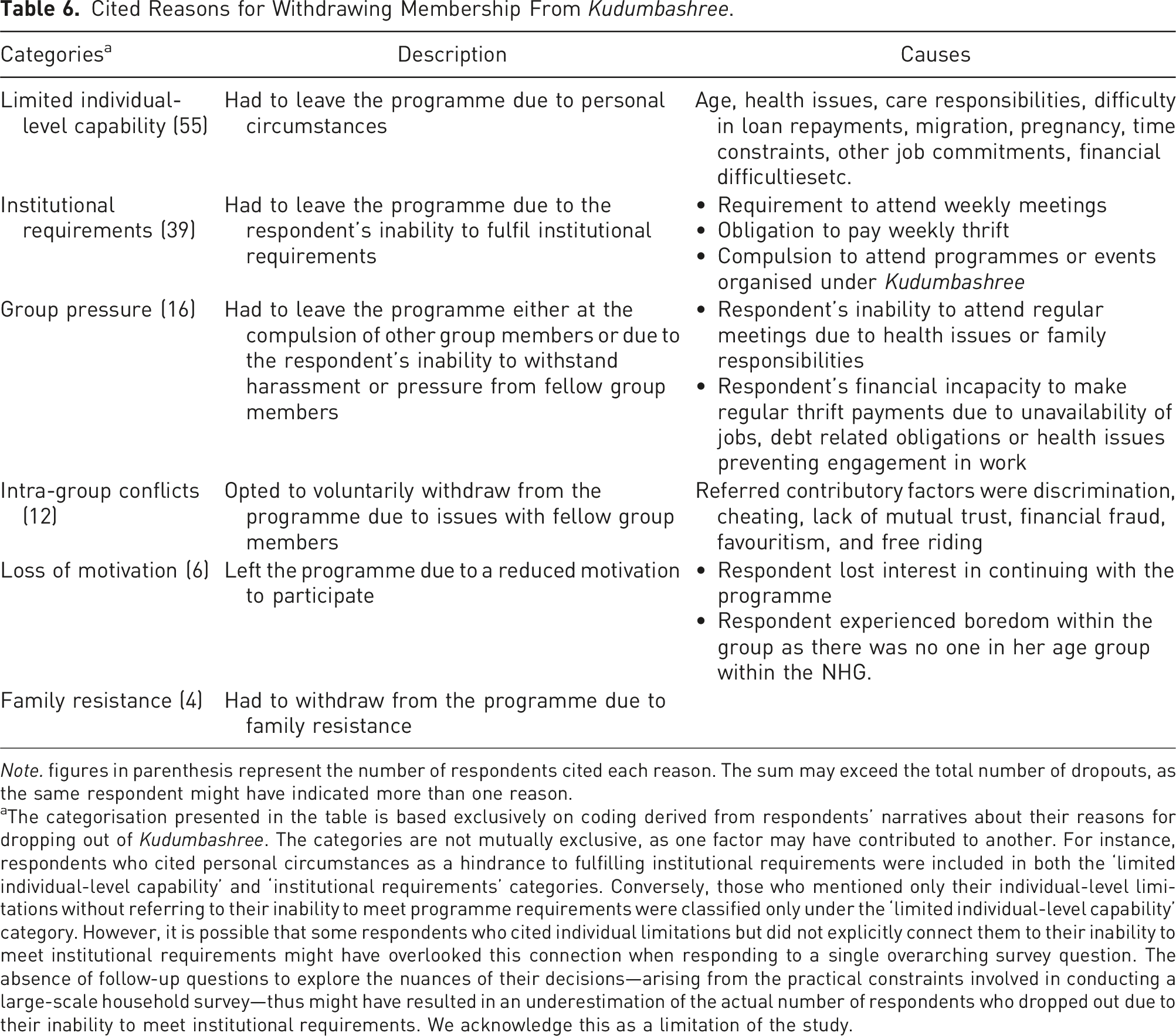

Cited Reasons for Withdrawing Membership From Kudumbashree.

Note. figures in parenthesis represent the number of respondents cited each reason. The sum may exceed the total number of dropouts, as the same respondent might have indicated more than one reason.

aThe categorisation presented in the table is based exclusively on coding derived from respondents’ narratives about their reasons for dropping out of Kudumbashree. The categories are not mutually exclusive, as one factor may have contributed to another. For instance, respondents who cited personal circumstances as a hindrance to fulfilling institutional requirements were included in both the ‘limited individual-level capability’ and ‘institutional requirements’ categories. Conversely, those who mentioned only their individual-level limitations without referring to their inability to meet programme requirements were classified only under the ‘limited individual-level capability’ category. However, it is possible that some respondents who cited individual limitations but did not explicitly connect them to their inability to meet institutional requirements might have overlooked this connection when responding to a single overarching survey question. The absence of follow-up questions to explore the nuances of their decisions—arising from the practical constraints involved in conducting a large-scale household survey—thus might have resulted in an underestimation of the actual number of respondents who dropped out due to their inability to meet institutional requirements. We acknowledge this as a limitation of the study.

Consistent with the findings of previous studies (e.g., Bardsley et al., 2015; Wright, 1997), our analysis reveals the complexity and multi-dimensional nature of factors contributing to dropout from a microfinance programme. The decision to withdraw often cannot be attributed to a single event or cause; rather, it is the culmination of a series of events. In some instances, multiple causes accrue hierarchically, with one event triggering another. At other times, several events may occur concurrently. In such scenarios, identifying the immediate reason for dropping out becomes challenging as it is intertwined with other contributory events. This complexity makes it difficult to pinpoint a single root cause and formulate targeted interventions, as exemplified in the words of a 55-year-old daily wage labourer from Central Kerala. In our NHG, I have the worst financial situation. When there was no work I couldn’t manage to pay the thrift regularly. So, everyone together started blaming me in meetings. Kudumbashree’s policy is that it is not compulsory for those who have no money to pay thrift. But those in the NHG won’t agree, right? Thus, when I reached a position that I couldn’t endure that torture anymore, I quit.

In this example, the apparent reason behind the respondent’s decision appears to be the pressure from the NHG. However, there were underlying factors that had driven her to this decision. She had to endure the group criticisms due to the non-repayment of thrift, an institutional requirement under the programme. She was unable to fulfil this requirement due to her already precarious financial position, compounded by lack of regular job availability or a fixed income flow—issues commonly faced by rural poor households in developing countries. Therefore, in this case, the respondent’s limited capability, as reflected by her financial difficulties, hindered her ability to meet institutional requirements, resulting in group pressure, ultimately influencing her decision to drop out from the programme. Aligning with the views of Sen (2000), such forms of self-withdrawal, driven by the ‘public shame’ tied to limited capabilities, represent an extreme form of social exclusion, even though it may not always be explicitly recognised as institutional exclusion.

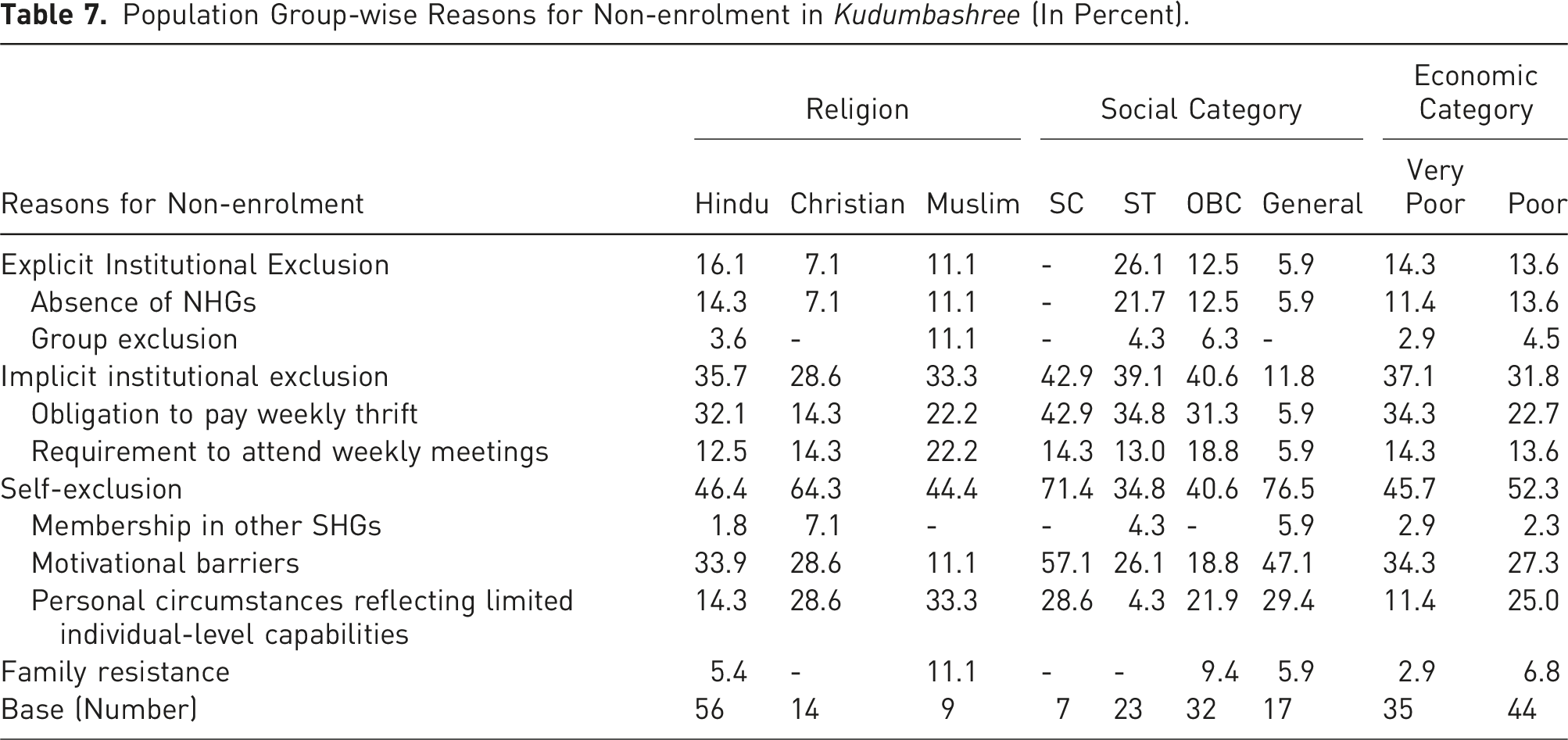

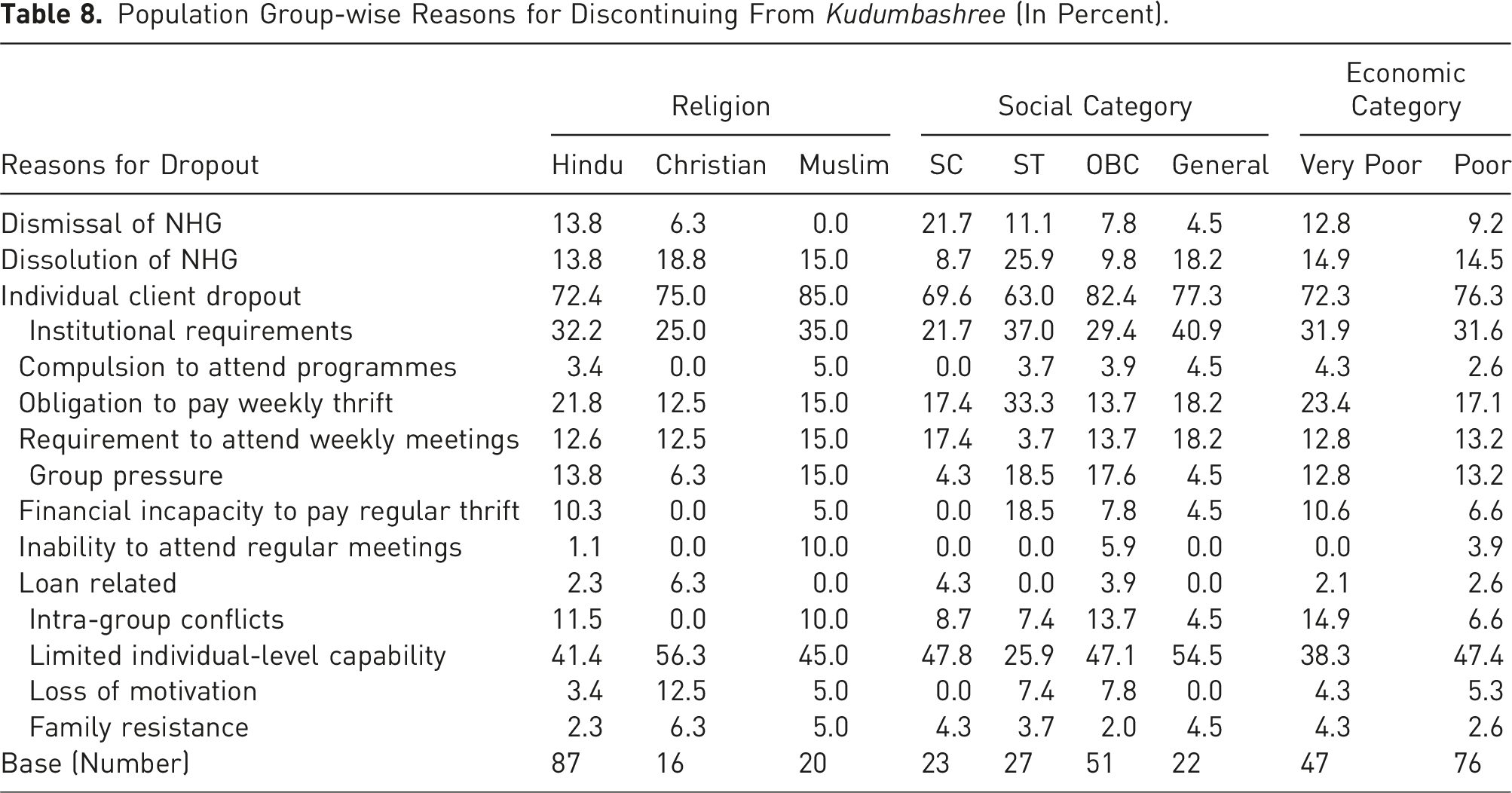

Population Group-wise Reasons for Non-enrolment in Kudumbashree (In Percent).

Population Group-wise Reasons for Discontinuing From Kudumbashree (In Percent).

While the quantitative analysis suggests a lower likelihood of Christian communities enrolling in the programme, Table 7 does not highlight any disproportionate institutional barriers faced by this group. Rather, members of the Christian community are more prone to voluntary self-exclusion due to personal circumstances or a lack of interest and motivation. In terms of dropout, the quantitative data indicate that women from Christian or Muslim communities are more likely to leave the programme compared with those from the Hindu religion. However, Table 8 reveals that these two groups face different reasons for discontinuing participation. Among the three religious groups, the Christian community had the lowest percentage of women reporting institutional requirements influencing their decision to drop out. While the difference with the Hindu community is not substantial, a slightly higher proportion of Muslim respondents mentioned institutional requirements as a reason for their withdrawal. Additionally, the data indicate that individuals from the Hindu or Muslim faiths are more susceptible to group pressure or intra-group conflicts compared with their Christian counterparts. This suggests that, relative to the Christian community, a higher proportion of Hindus and Muslims are likely to experience exclusion from the programme due to institutional barriers.

Furthermore, compared with the General category, vulnerable social groups including SC, ST or OBC communities were more likely to report explicit or implicit institutional barriers as reasons for non-enrolment. Although the difference is not substantially wider, a higher proportion of respondents holding yellow PDS cards (indicating the very poor category) mentioned explicit and implicit institutional exclusion compared with those with pink PDS cards. These observations suggest that socially and economically vulnerable groups are more likely to encounter institutional barriers at the entry level, or they may exhibit greater hesitancy to join the programme due to the associated institutional requirements.

Compared with those from the OBC or General categories, a higher proportion of individuals from the SC or ST communities reported dismissal of NHGs by officials as a reason for discontinuing their participation. However, there is no apparent indication of other institutional barriers disproportionately driving the dropout decisions of these most vulnerable social groups. In fact, a larger proportion of respondents from the General category cited institutional requirements as reasons for dropping out, compared with those from the SC/ST/OBC categories.

Similarly, while a slightly higher share of respondents from the very poor category mentioned the dismissal of NHGs as the reason for terminating their participation, no significant difference was found between the yellow and pink PDS card holders regarding the proportion of respondents reporting difficulty in fulfilling institutional requirements. This pattern implies that once enrolled in the programme, the institutional constraints or requirements of Kudumbashree do not significantly discriminate against or disproportionately force out socially or economically vulnerable groups.

Discussion and Implications

Examining the case of non-participation of eligible households in Kudumbashree, a unique welfare-oriented microfinance initiative in Kerala that centres on women’s empowerment and poverty eradication, this paper seeks to contribute to the literature on the inclusivity of microfinance programmes. More broadly, by employing the social exclusion framework, it aims to understand how exclusionary processes can arise even within social protection schemes specifically designed to combat social exclusion or promote social integration. Through its ‘credit-plus’ approach and targeted focus on poor women in Kerala, Kudumbashree aims to address multidimensional deprivations, including gender inequality, poverty, and credit inaccessibility. As such, it provides a valuable case study for exploring exclusion within an anti-exclusion framework.

The concept of social exclusion serves as a fitting analytical framework for our study, as it not only focuses on the characteristics of the excluded groups but also examines the processes that drive exclusion, extending the discussions beyond mere descriptions of individuals’ circumstances (de Haan, 2000; Room, 1995). Additionally, the social exclusion framework, with its adaptability to different local contexts, enables context-specific analyses and policy recommendations (de Haan, 2000). In this study, both quantitative and qualitative data from a survey of 678 rural poor households in Kerala were analysed to comprehensively understand the state and process of exclusion within Kudumbashree.

This section discusses the insights gained from the combined analysis of both quantitative and qualitative data, along with the specific policy suggestions and broader theoretical implications emerging from them.

A key objective of the study was to investigate whether certain population groups are systematically excluded from the programme, with a particular focus on identifying institutional barriers. To achieve this, respondents were categorised based on their socio-economic and religious characteristics. The complementary use of quantitative and qualitative methods offers a dual perspective in this regard, addressing distinct yet interconnected research questions.

The quantitative analysis identifies which population groups are not participating in the programme by examining their socio-economic and religious characteristics. It reveals that women belonging to the ST category, one of the most disadvantaged social groups in Kerala, are more likely to be excluded from the programme, either due to a lower likelihood of joining or a higher propensity to drop out. Religion also significantly influences programme participation. However, within the broader category of low-income households, no significant differences in participation were observed across economic subgroups.

The qualitative analysis uncovers the nature of obstacles different groups face in participating the programme. Findings indicate that, compared with women from the General category, vulnerable social groups—including SC, ST and OBC—are more likely to cite explicit or implicit institutional barriers as reasons for non-enrolment. Similarly, a slightly higher proportion of respondents from the very poor category reported both explicit and implicit institutional exclusion compared with those from relatively economically well-off groups. These observations imply that socially and economically disadvantaged groups are more prone to encountering institutional obstacles at the entry stage, or may be more hesitant to enrol due to the programme’s requirements.

Regarding dropout reasons, a higher proportion of women from the SC and ST communities, as well as those from the very poor category, reported dismissal from NHGs by officials as a reason for discontinuing their participation in the programme, compared with their socially and economically better-off counterparts. However, there was no strong evidence indicating that other institutional requirements—such as weekly meetings or thrift contributions—disproportionately influence the dropout decisions of these vulnerable groups. This suggests that, once joined, the programme’s institutional constraints do not systematically disadvantage socially or economically vulnerable participants.

While the quantitative analysis suggests that religion influences women’s non-participation in the programme, the qualitative data indicate that this is not always due to institutional exclusion. For instance, although Christian women are less likely to enrol and more likely to drop out, qualitative findings do not reveal any disproportionate institutional barriers affecting this group. Given the relatively better socio-economic standing of Christians in Kerala—both compared with other religious groups in the state and to Christians elsewhere in India (Harriss-White, 2002; Zachariah, 2017)— despite their numerical minority status, this pattern is understandable. In contrast, both quantitative and qualitative findings point to a higher likelihood of systematic exclusion faced by Muslim communities.

Another objective of the study was to examine the influence of respondents’ debt attitudes on programme participation. The quantitative analysis reveals a significant association between debt attitudes and continued participation in Kudumbashree. This observation underscores the notion that, despite the array of other benefits the programme offers, Kudumbashree is predominantly perceived as a microcredit initiative and a pivotal credit source for rural poor households in Kerala. This perception highlights the significance of financial incentives in enhancing the retention rate in social protection schemes. However, none of the non-joiners or dropouts explicitly cited aversion to borrowing when qualitatively explaining their reasons for non-participation. This could imply that respondents tend to prioritise material constraints over attitudinal factors when explaining their decisions in response to a single overarching question. In-depth interviews with follow-up questions could provide deeper insights into the role of debt attitudes in shaping participation in microfinance programmes.

Policy Implications

Although the policy recommendations presented in this section are derived from the findings of the case study of Kudumbashree, most of the issues identified are rooted in the general structural design of microfinance programmes. Therefore, we believe that the barriers highlighted and the recommendations that emerge from them are relevant not only for improving the inclusivity of Kudumbashree but also for enhancing the accessibility and effectiveness of similar initiatives worldwide.

Overall, our findings indicate that, even within a non-profit, welfare-oriented microfinance programme like Kudumbashree, institutional requirements—such as weekly meetings and regular thrift payments—can create barriers to participation for certain vulnerable groups. Their particular circumstances—such as age, health issues, care responsibilities, joblessness, and financial difficulties—often limit their ability to meet these requirements. These challenges are further exacerbated by peer pressure and the group dynamics inherent in microfinance structures.

It is pertinent to note that at the design level, Kudumbashree envisions a culture of empathy among members, fostering mutual understanding of each other’s situations. As noted earlier, the programme structure is deliberately designed with flexibility, granting NHGs the autonomy in decision-making and explicitly authorising them to waive institutional requirements—such as regular thrift payments and mandatory meeting attendance—for members in need, if necessary. However, in practice, this flexibility is not always consistently implemented at the grassroots level. Although direct expulsion may be rare, the intolerance or displeasure displayed by fellow group members becomes a persuasive factor leading participants to withdraw their membership. While completely compromising on these institutional requirements is not advisable, due to their integral roles in ensuring the programme’s sustainability, awareness sessions aimed at improving group solidarity, sensitising members to each other’s situations, and developing a sense of empathy and mutual support, may be explored. There could also be contributory factors or underlying reasons forcing participants to abstain from thrift payment or attending meetings. Identifying these factors and collectively addressing them at the community level is also equally important.

There were also instances of women dropping out due to intra-group conflicts, often arising from personal disputes between neighbours. This situation highlights the need for training focused on building group cohesion, encouraging open communication between members, and helping them understand the delineation between ‘personal space’ and ‘group space’. Strengthening team spirit is especially crucial for Kudumbashree, as the concept of a ‘neighbourhood group’ is built around the vision that friendly solidarity among neighbours will ensure the smooth running and enhance the efficiency of the programme. Providing specialised training on group dynamics to grassroots-level organisers could enable them to identify various types of group issues at an early stage and intervene before conflicts escalate.

Finally, in the specific case of Kudumbashree, A higher proportion of respondents from ST category cited the absence of NHGs in their area as a reason for non-enrolment. In certain instances, the maximum membership limit of nearby NHGs is exceeded, while simultaneously facing challenges in gathering enough members to form a new NHG. The spatial isolation faced by ST communities may have contributed to this phenomenon. Prior research has demonstrated how spatial disadvantages experienced by certain communities can exacerbate their social exclusion (e.g., Béland, 2007; Chorianopoulos et al., 2014). Given this specific disadvantage faced by one of the most vulnerable social groups in Kerala, it may be worth considering the relaxation of minimum and maximum membership requirements for forming an NHG, when necessary.

Theoretical Implications

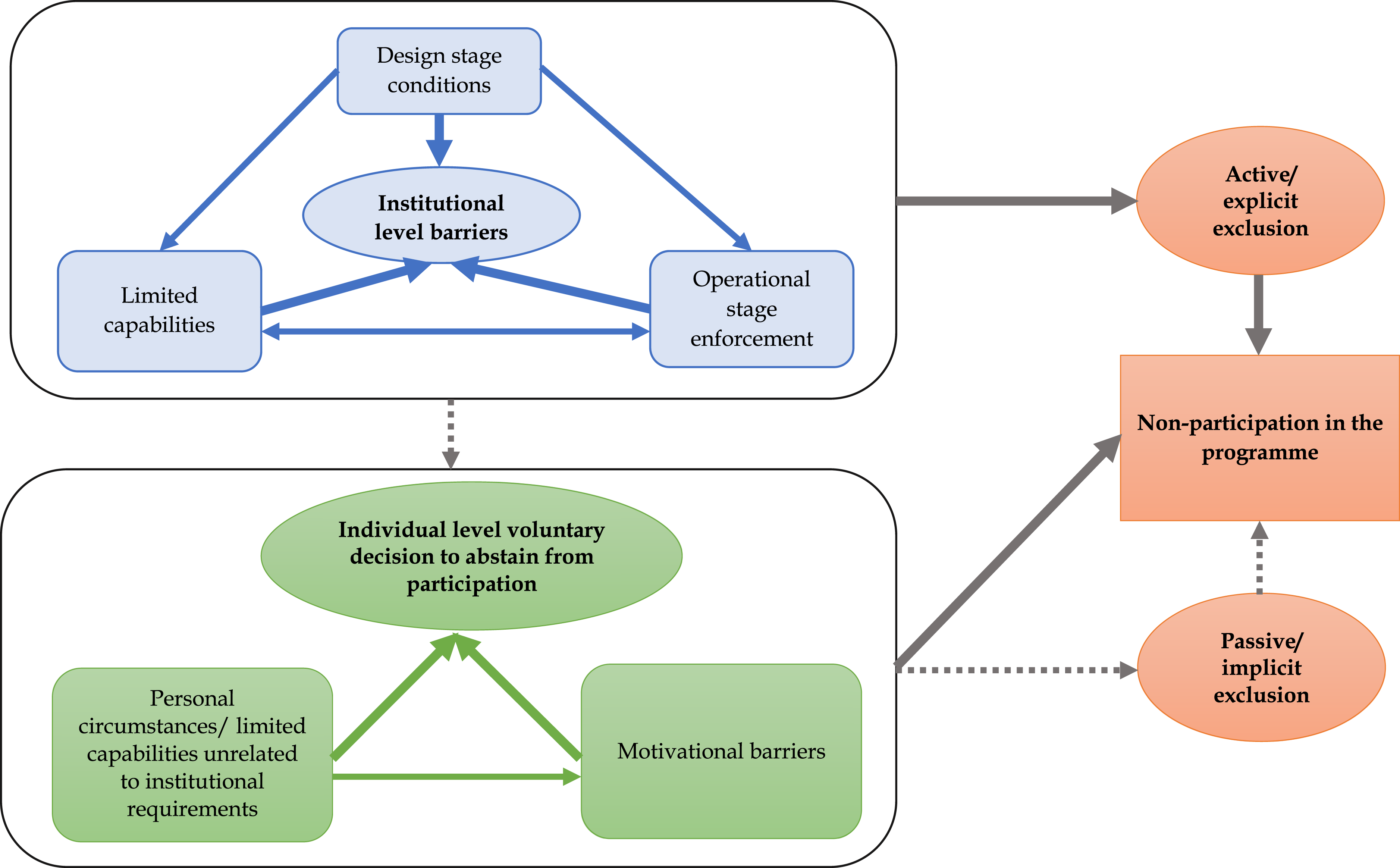

In addition to advancing the empirical understanding of the inclusivity of microfinance programmes, this paper, on a broader conceptual level, contributes to the discourse on social exclusion by critically examining how policies specifically designed to address social exclusion may, paradoxically or inadvertently, embed elements that perpetuate exclusion. Building on prior literature that highlights the exclusionary elements within the design and functioning of microfinance programmes (e.g., Beisland & Mersland, 2014; Bwire et al., 2009; Cramm & Finkenflügel, 2008; Hulme, 1999; Sarker, 2024) and drawing on insights from our empirical study, we posit that, from an institutional perspective, exclusion from social protection schemes— where participation is voluntary and subject to fulfilling certain conditions—can arise from three factors: design-stage conditions, their operational-stage enforcement, and individual-level limitations in capabilities in complying with them.

Like many microfinance programmes, Kudumbashree’s design-stage conditions—such as regular thrift payments, mandatory meeting attendance, and emphasis on group cohesion—are intended to ensure the sustainability of the programme but often unintentionally exclude vulnerable populations during the operational stage, primarily due to their limited capacity to comply with these conditions. While the programme does not deliberately exclude any community and allows flexibility and concessions in these requirements, group dynamics can hinder the effective implementation of such accommodations. This can lead to the exclusion of certain vulnerable segments, simultaneously creating a misleading perception that their withdrawal was voluntary. Thus, the cumulative and combined effects of design-stage conditions, operational-stage enforcement, and individual limitations makes it challenging to pinpoint a single root cause of exclusion or to distinguish between voluntary and forced exclusion in Kudumbashree and similar social protection initiatives.

As illustrated in Figure 2, exclusion from these programmes can extend beyond explicit institutional barriers or entirely voluntary non-participation. Institutional conditions, combined with individuals’ limited capabilities to meet these requirements, may lead some eligible beneficiaries to opt out. While this decision may seem like a voluntary non-participation, it often constitutes a form of passive exclusion, as described by Sen (2000), occurring at varying degrees. Therefore, from a methodological standpoint, we align with Levitas (2006) in critiquing surveys that force respondents to choose between ‘don’t want’ and ‘can’t afford’ as reasons for non-participation in common social activities. The ‘don’t want’ category can mask various capability-related constraints, such as illness, disability, time limitations, and perceived difficulties in overcoming these challenges, thereby failing to capture the true nature of exclusion—whether voluntary or forced. Even when non-participation appears voluntary, fully understanding the underlying complexities driving that decision requires deeper investigation. Broad framework for capturing non-participation in social protection schemes.

Conclusion

By exploring the factors influencing non-participation in the Kudumbashree programme in Kerala, India, this paper enriches the empirical understanding of the inclusiveness of microfinance programmes in developing countries. Designed to combat multiple deprivation and exclusion, detachment from such programmes can further exacerbate existing vulnerabilities and deepen social exclusion, as noted by Sen (2000) and Walker (1995). Additionally, the study identifies a positive link between respondents’ debt attitudes and their likelihood of continued participation, underscoring the role of financial incentives in improving retention rates in social protection schemes.

On a broader conceptual level, this study illustrates the paradox that policies aimed at reducing social exclusion may unintentionally reinforce it. The paper argues that, exclusion in such programmes—where participation is defined as voluntary, and comes with certain conditions for beneficiaries to meet—can manifest implicitly through the interplay of three factors: design-stage conditions, their enforcement during implementation, and individual-level constraints in meeting these requirements.

Finally, this paper acknowledges the critical need to deepen the empirical understanding of non-participation in microfinance programmes across diverse contexts, given the limited existing research. As microfinance initiatives vary in structure and operation, each may embed distinct exclusionary forces. To address this, the study advocates for a comprehensive approach that integrates both quantitative and qualitative data, while considering the unique design and objectives of each programme. Ensuring inclusivity and eliminating barriers for vulnerable groups is not just an aspirational goal for the concept of microfinance; they are essential steps toward realising its core mission.

Footnotes

Acknowledgments

In undertaking this study, we acknowledge funding support from Lendwithcare and logistical support from the Centre for Socio-economic and Environmental Studies, India. The authors wish to convey their profound gratitude to the survey participants and in-depth interview respondents for generously contributing their time. We extend our thanks to the expert panel and translators involved in the local adaptation of attitudinal/cognitive constructs employed in this study. Special appreciation goes to Dr N Ajith Kumar, and Dr Rakkee Thimothy for their invaluable comments during the earlier drafts of this paper.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was financially supported by Lendwithcare and logistically supported by the Centre for Socio-economic and Environmental Studies, India.

Declaration of Generative AI and AI-Assisted Technologies in the Writing Process

During the preparation of this work, the authors used ChatGPT 3.5 in order to enhance the readability and language. After using this tool/service, the authors reviewed and edited the content as needed and take full responsibility for the content of the publication.

Ethical Statement

Data Availability Statement

The data that support the findings of this study are openly available in Pure portal at 10.17,029/9cbe0079-41c1-4ddd-9de0-94883a1d51b9.