Abstract

Watching over-the-top (OTT) video has become the mainstream of daily life worldwide. Except for a few cultural exporters, most countries have experienced a threat of global OTT giants sweeping local audiences. How do local OTT platforms protect local cultures and retain local audiences? From the perspective of media industry studies, this study uses data from four Taiwanese OTT platforms to explore this question and found that Taiwanese OTT platforms are starting to open their business models to external ideas or partners, but the degree of openness has not yet reached the integrated nor the adaptive types. Moreover, we identify six common practices of open business models: (1) cooperation with suppliers, (2) outbound licensing, (3) strategic alliances, (4) buyer–supplier integration, (5) co-opetition, and (6) joint ventures.

Introduction

The surge of over-the-top (OTT) video (also known as streaming video) worldwide, as a form of disruptive innovation, has long affected traditional movie, television, and music industries. The concept of disruptive innovation has received considerable attention since Christensen and Bower (1996) proposed it. Disruptive technologies are new technologies improving on the attributes demanded by the mainstream market and invading each market segment from the low end. Over-the-top, as a disruptive technology, is shifting video consumption from linear TV watching to nonlinear streaming services with lower prices and greater varieties. Over-the-top refers to services delivered via third parties over the internet. Over-the-top is defined as content, services, or apps provided to users through the public internet, encompassing video, music, communication, productivity, tech, and community platforms (BEREC, 2016). This study highlights that OTT video entails internet-based audiovisual content delivery, breaking away from traditional TV and film supply chains, allowing various entities including content producers, platform aggregators, ISPs, and device manufacturers to directly provide content to consumers. This restructuring creates both opportunities and intense competition within the streaming video market.

Global OTT video services, such as Netflix and iQIYI, have entered Taiwan since 2016, which attract a large number of domestic audiences. Taiwan's government and local OTT 1 platforms have taken action to respond. In 2017, two NGOs—Taiwan OTT Association and the New Media Entertainment Association—were established by OTT platforms and content providers to combat piracy on the one hand and promote Taiwanese content on the other. In 2018, the Ministry of Culture launched a New Media Cross-platform Content Production Project to promote the idea of “Taiwanese people use Taiwanese OTT services to binge-watch Taiwanese dramas.” In 2020, the National Communications Commission drafted an Internet Audiovisual Service Management Act, which attempted to regulate large enterprises while relaxing control over small ones. However, these efforts have not been successful in changing the nature of many small-scale Taiwanese OTT platforms.

For small-scale firms, utilizing services provided by partners in their strategic network may be an attractive means of achieving sustainable market performance and, in turn, successful open business models (Chesbrough, 2007). Scholars have studied open business models in various industries (Chu & Chen, 2011; Davey et al., 2010; Frankenberger et al., 2013; Visnjic et al., 2018), but research falls short in explaining the establishment and management of open business models in the media sector. The use of open business models within the OTT video market offers the possibility to engage content producers, platforms, ISPs, and devices (Noam, 2021) at earlier stage of the process, thus allowing viable services to reach the market more quickly or generating revenues from license, spinoff, or divestment. The effective realization of this approach requires knowledge of the actual business models being operated in the market. Thus, the question addressed in this study is: To what extent and how Taiwanese OTT platforms undertake open and collaborative activities in response to the new video market and competition from global giants. Applying open business models, this study attempts to (a) identify Taiwanese OTT platforms’ prevalent business models in terms of openness and (b) examine how Taiwanese OTT platforms integrate their business into partners’ models.

Literature Review

The OTT video market

OTT, abbreviation for over-the-top, represents service that is provided over third parties. The European Union Body of European Regulators for Electronic Communications (BEREC) (2016, p. 3) defines OTT service as “content, a service or an application that is provided to the end user over the public internet.” The definition not only includes video but also music, communication, productivity, technology, and community platforms providing OTT services. According to BEREC, video is classified in the OTT-2 category, referring to the transmission of digital audiovisual content through the public internet to terminal services used by viewers (Liu, 2017). The U.S. Federal Communications Commission (FCC) has yet to define OTT video. However, in 2011, the FCC categorized audiovisual service providers as online video distributor, in which online video is similar to OTT video, and then defined it as “an entity that distributes video programming by means of the internet or other internet protocol (IP)-based transmission path; not as a component of an MVPD subscription or other managed video service; and not solely to customers of a broadband internet access service owned or operated by the entity or its affiliates” (FCC, 2017, p. 3). This study thus defines OTT video as audiovisual content via the internet without requiring users to subscribe to cable or satellite services (MVPD), nor to bundle with ISPs (IPTV).

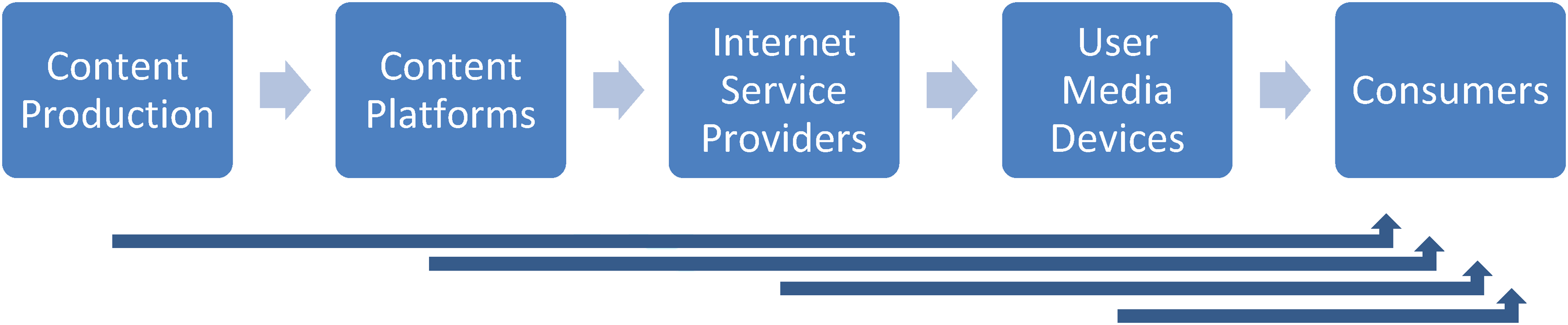

These definitions imply that OTT video not only integrates the content of traditional television and film industries but also deconstructs the traditional supply chains of audiovisual services. Specifically, because of the advancement of internet technologies and low level of regulation in various countries, OTT can be provided through any link of the supply chain to directly engage with consumers. Figure 1 depicts the supply chain of the emerging OTT video services and clearly illustrates the dramatic changes that have occurred in the audiovisual market (Noam, 2021). The traditional supply chains with upstream and downstream links are intricately connected; but, in the OTT market, providers such as content producers, platform aggregators, internet service providers, and even device manufacturers can supply online audiovisual content directly to consumers (Gu, 2017; Yan, 2017), also known as D2C services. The deconstruction of the supply chain has provided competitors with not only unprecedented opportunities but also intense competition.

Over-the-top (OTT) video disruption.

The revenue model of OTT video includes advertising-support video-on-demand (AVOD), time-delayed regular TV (catch-up TV), subscriptions to new types of video-on-demand (SVOD), subscriptions to traditional channel packages (skinny bundles or livestreaming), transactions, pay-per-view and purchase (TVOD), usage fees, public subsidies, voluntary contrition (donations and grants), payments by content and app suppliers, and monetization of data (Noam, 2021). However, OTT video generally features the dual-product market characteristics of the media industry, possessing an economic platform with two potential customer bases: service users and advertisers (Picard, 1989, p. 9), the major options are SVOD, AVOD, and TVOD. The best example of SVOD is Netflix; AVOD is YouTube; and TVOD is Apple TV. Increasingly, OTT platforms apply a mixed model to increase revenue streams; for example, Netflix launched AVOD in late 2022, YouTube pushed its Premium plan (SVOD) to more than one hundred countries. Notably, live stream gaming platforms (e.g., Twitch) use mechanisms such as donations (virtual gifts and rewards), product placements, and shopping recommendations as revenue sources, enabling diversification of revenue streams (He, 2017; Lin, 2017). In the face of revenue loss, mixed solutions have become a coping strategy for major OTT video platforms.

The OTT video research

The popularity of OTT video services has not increased until recent years, so academic research on the topic is still in its infancy. In the field of media studies, OTT-related research mainly focuses on production and consumption. Research on the consumption side, such as Li (2017), applies niche theory to analyze user satisfaction among OTT, IPTV, and digital cable TV in Taiwan. She has found that OTT is most competitive among users and a generalist; IPTV and digital cable TV are competitive with each other because of their similar attributes, and they are specialists in the minds of users. In addition, Chen (2019) also applied the niche theory to analyze users of OTT and cable TV in Taiwan and found that OTT is more competitive than cable TV, especially in terms of convenience. Satisfaction is higher with OTT drama and movies, while cable TV's news and sports are more favored.

Few studies focus on the production side of OTT video, and most of them concentrate on Asia. Park (2018) analyzed how Korea's telecom, cable TV, and satellite channels operated OTT video services. Although the results confirm that OTT video services have the capability of disruptive innovation, judging from the market development patterns and the business strategies of each platform, the innovation only consolidated the existing oligopoly of television and telecommunications firms, which becomes a complementary, not disruptive, innovation. In the following year, Park (2019) used secondary data analysis to examine the business models of 798 OTT video platforms from 71 different countries and found that some business models seem to be related to ownership types on the surface, but in fact, authenticated content usually adopt a subscription model (SVOD); catch-up TV usually adopts an advertising system (AVOD).

Wang and Lobato (2019) used a case study to analyze how iQIYI, one of the largest OTT video platforms in China, performs the best in terms of government policies, market structure, and platform capabilities. As a conclusion, they proposed that if the platform theory and platformization in the West were to be applied to countries under different political systems, they should be revised for “a spatialized platform theory.” Huang and Wu (2020) explored how the local OTT video platforms of the United States, China, the United Kingdom, and South Korea were formed and operated through document analysis. They found that local content was the most important asset, and successful local teams were committed to multiple channels, multiple revenues, and close customer relationships. Unlike global OTT giants, which may adopt a single revenue model to support operations, such as YouTube's advertising model and Netflix's subscription model, local platforms must develop innovative and diverse businesses models. In addition, Lin (2020) carried out empirical research on OTT TV's innovation and transformation in Taiwan. She took PTS+ and Yahoo TV as cases and conducted in-depth interviews with more than 20 executives and employees on the two platforms. She found that PTS+ adopts a continuous innovation strategy, while Yahoo TV prefers a subversive innovation model.

Past studies on the supply side have examined the business models and strategic positioning of OTT video, but there is no single dominant business model in the OTT video market (Huang & Wu, 2020; Lin, 2020; Park, 2018, 2019; Wang & Lobato, 2019). Moreover, none of these models has proven to be consistent performers regarding revenue generation and profitability (Park, 2019). While most research has previously focused on typologies or challenges of OTT business models, the openness of business models itself has not been studied so far. The use of open business models is to reconfigure the activity system involving more of external partners in the execution of selected activities (Chesbrough, 2003, 2006). Our study's objective is to understand the role of open business models in times of OTT innovation among local OTT platforms in Taiwan.

Open business models

Business models have been an integral part of economic behavior since preclassical times, but only became popular as a research concept with the advent of the internet in the mid-1990s (Zott et al., 2011). The term “business model” first appeared in academic journals in 1957, but scholars discussed it as research topics integrating with education and electronics (Osterwalder et al., 2005). Since then, business models have sporadically appeared in different fields such as technology, organization, and strategy. Among them, discussions on strategy are approaching maturity after the vigorous development of the new internet economy (Wirtz et al., 2016). Due to the wide range of application, there is no homogeneous definition of business models. Scholars mostly seek answers from past research or industry communities. In general, Teece's (2010, p. 172) definition is sufficient to cover major research conducted in the field of business models: “A business model describes the design and structure of mechanisms for value creation, value delivery, and value capture.” In a similar vein, Bocken et al. (2014) used three main elements in their definition of a business model: value proposition, value creation and delivery, and value capture.

Chesbrough (2006) was the first to coin the term “open business models,” which enables an organization to be more effective in creating as well as capturing value. Open business models focus on external resources as key contributors to a firm's value creation process; whereas closed business models look at internal value creation and rarely collaborate with partners (Chesbrough, 2006, 2007; Frankenberger et al., 2013). An open business model is to be considered from a network-centric rather than firm-centric perspective. A broader definition proposed by Weiblen (2014, p. 57) is “An open business model describes the design or architecture of the value creation and value capturing of a focal firm, in which collaborative relationships with the ecosystem are central to explaining the overall logic.”

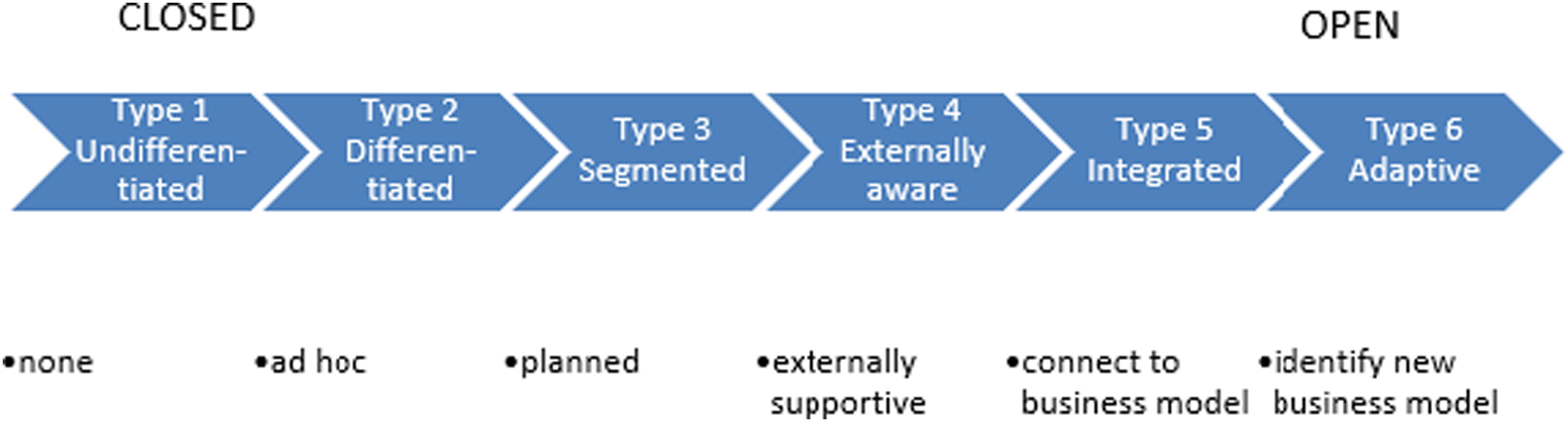

To help firms open their business models, Chesbrough (2006) classifies six types of business models, each producing different levels of differentiation—from close to open. Closed business models refer to the situation where firms market a product using their own assets and relying on other value chain partners through market transactions, whereas open business models refer to situations where the innovating firm relies on its partners’ competencies to jointly create value for customers and share that value according to agreements. Frankenberger et al. (2014) differentiate four basic types of open business models: open R&D, open innovation, open business architecture, and fully open business model. Cozzolino et al. (2018) use eight attributes to qualify the degree of open business models: access to external innovation, innovative role of users, support of enabling tools or platforms, intrinsic motivation, ability to incur lower costs, collective effort, distributed control, and open approach to intellectual property. Our study attempts to include cases which may not strategically implement open business models, so Chesbrough's six-type framework, from closed to open, namely, undifferentiated, differentiated, segmented, externally aware, integrated, and adaptive, is a better fit and thus adopted (Figure 2).

Open business models.

Type 1 business model is undifferentiated in that firms must compete on price and availability. These firms lack much of a process to innovate and manage IP. Examples of Type 1 firms include mom-and-pop restaurants, family farms, and many entry-level services establishments. Firms operating in Type 1 find it very difficult to sustain any competitive advantage in their business. Type 2 firms create some degree of differentiation in their business model and target customers other than those that buy simply on price and availability. Many young technology-based start-up firms and individual inventors are Type 2, also known as one-hit wonders. Type 3 firms can develop a business model that can compete in different market segments simultaneously, for example, the price-sensitive segment is provided with high-volume, low-cost production, whereas the performance segment is supplied with high margins products. Examples of Type 3 firms are young start-up companies grown beyond the one-hit wonder or established companies with well-earned reputation.

Despite the gradual differentiation of business models, Types 1 to 3 firms do not yet open their business models to the external world. Type 4 firms are the ones starting to open themselves to external ideas and technologies in the development and execution of their businesses. Such external innovation reduces the cost of serving the business, reduces the time it takes to get new offerings to market, and shares the risks of new products and processes with other parties. In a Type 5 model, suppliers and customers enjoy formalized institutional access to the firm's innovation process and this access is reciprocated by the suppliers and customers. Firms like IBM have branded themselves as a partner of choice for others to approach with innovation opportunities; P&G is promoting itself as the leader in open innovation. Type 6 business model is an even more open and adaptive model than the previous types. In Type 6, suppliers are integrated into the planning processes of the firm, which in turn has integrated its business model into the business model of its key customers. Dell is a good example of the Type 6 partnership: It works closely with Intel on future technology planning by serving as an early test bed for new Intel chips and developing a new motherboard for Intel's next-generation chip.

The phenomenon of “open business models” remains understudied since Chesbrough's seminal books on the topic, but some studies did find open business models a source of above-normal returns. Frankenberger et al. (2013) found that open business model firms with high customer centricity and their few but strong ties to partners lead to superior performance. Alcalde and Guerrero (2016) collected data from 318 young Spanish firms and found that those firms benefited from open business models toward diverse types of cooperation in expansionary periods. Visnjic et al. (2018) studied 12 case firms which shifted toward service market and open business models and found that these two interlinked changes helped firms to create value by growing their new businesses efficiently and effectively. Referring to the linkage between open business models and market performance, we argue that the ability to undertake open business models that optimizes value creating and value capturing, that is Types 4 to 6, may determine the sustainability of local OTT video platforms. Based on the above theoretical foundations, we propose three research questions to answer in our study.

RQ1: What is the range of openness across local OTT platforms in Taiwan? RQ2: What is the range of openness within each local OTT platform in Taiwan? RQ3: How do local OTT platforms in Taiwan undertake open business models in practice?

Methods

Multiple case study approach

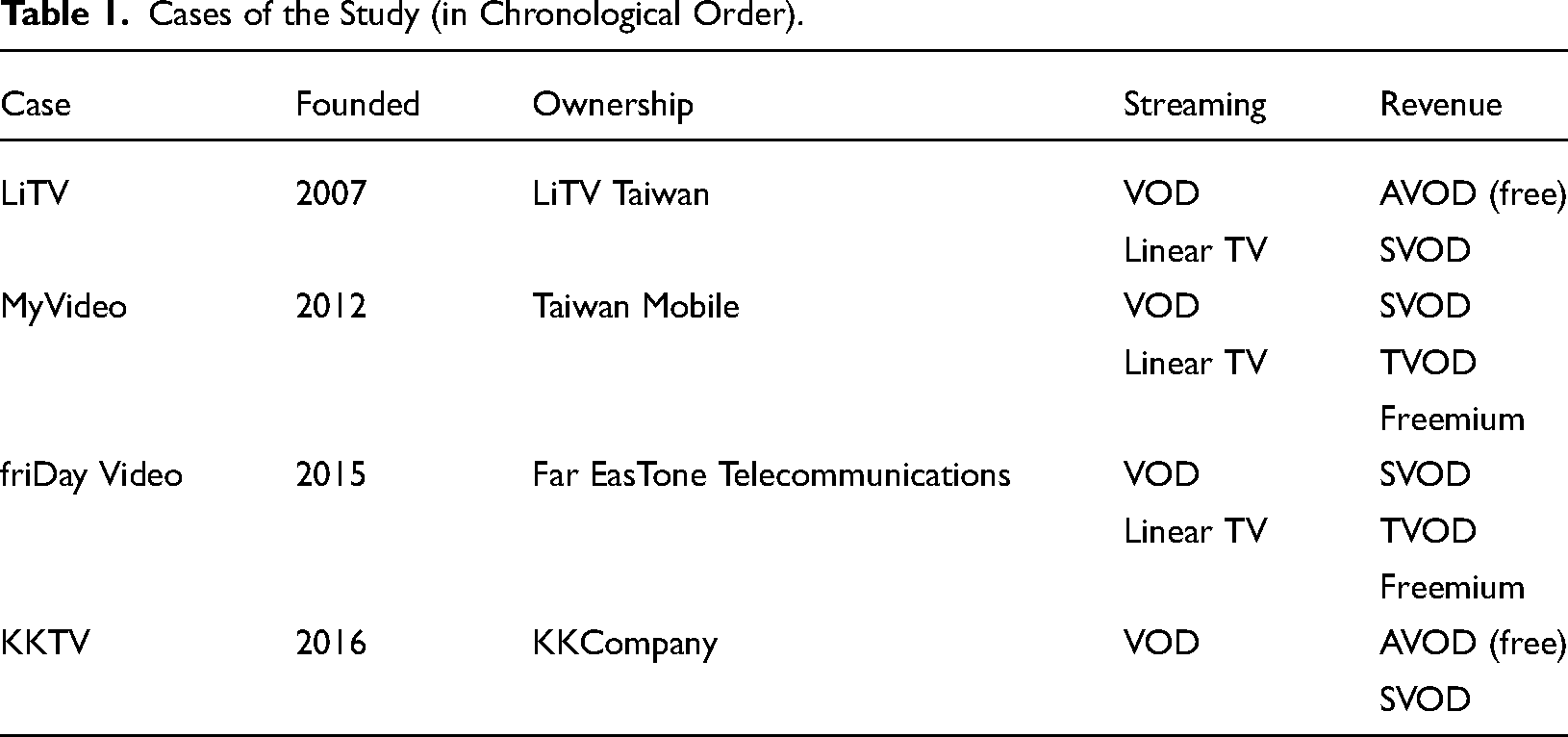

Given few prior studies on the open business models of OTT video platforms, a qualitative research design seems advisable, and a multiple case study approach is employed (Yin, 2014). There are over 17 local OTT video services in Taiwan, but only several have significant market shares. Based on Media Partners Asia's (2021) consumer survey, a sample size of 4076 respondents, SVOD adoption in Taiwan is still growing. The total number of paid subscriptions reached 3.4 million in the second quarter of 2021, with an average household subscribing to 2.9 OTT services. Netflix leads with a 19% share of paid subscriptions, followed by iQIYI Taiwan (10%), friDay Video (9%), MyVideo (9%), and KKTV (7%). In the freemium category, Line TV, LiTV and iQIYI Taiwan are the most streamed services. Based on the above statistics, this study excluded top global platforms, Netflix, iQIYI, and Line TV, and chose friDay Video, MyVideo, KKTV, and LiTV as the local OTT platforms in Taiwan as our cases (Table 1).

Cases of the Study (in Chronological Order).

LiTV is an OTT video platform established in 2007. LiTV is the first OTT in Taiwan that provides VOD and TV channels (Chen, 2020). Content on the platform includes six types of VOD, which are movies, dramas, animations, variety shows, children, and life and 400 TV channels, which are daily news, sports, financial, and other channels (also see https:/ /www.litv.tv/). In terms of business model, LiTV has developed a mixed model of advertising and subscription with the help of powerful connected TV technology. In terms of free services, LiTV provides users with many dramas and variety shows to combat pirated websites and apps (Su, 2018). LiTV also cooperates with many streaming equipment manufacturers such as smart TVs and set-top boxes.

Taiwan Mobile launched its OTT video platform MyVideo in 2012, which supports cross-platform viewing of on-demand videos and live content. MyVideo upholds the idea of “co-creation” and supports the development of Taiwan's original content through the strategy of “investing instead of purchasing” (Li, 2022). The works invested and coproduced by MyVideo have performed well. In 2022, five works were shortlisted and a total of 12 were nominated in Golden Bell Awards. In addition, in November 2021, MyVideo and Disney+ became exclusive partners in Taiwan. Relying on Taiwan Mobile's mobile user base of more than 7 million subscribers and telecommunications and channel service capabilities, Disney+ jumped to second place in Taiwan's OTT SVOD platform in 2022 (Wang, 2023).

friDay Video is a value-added service of Far EasTone, the third largest telco behind Chunghwa Telecom and Taiwan Mobile. In 2015, Far EasTone announced the launch of 4G and mobile digital brand “friDay,” which included friDay Video, friDay Shopping, friDay Reading, friDay Music, friDay PLAY, and other services. friDay Video is an OTT video platform that provides movies, dramas, and live TV (see https://video.friday.tw/). friDay Video has been actively cooperating with various film festivals, such as obtaining the online exclusive right to live broadcast the Golden Horse Awards and cooperating with Taiwan International Women's Film Festival to curate festival films (Central News Agency, 2013; Huang, 2014). In recent years, friDay Video has successfully attracted fans with diverse exclusive content and phenomenal Korean and Japanese drama and films thanks to its precise content selection strategy (Fan, 2022).

KKTV is privately owned by KKCompany, Asia's leading media technology group headquartered in Taipei, Taiwan, which has expanded its business internationally through five major business lines: Social-Audio Streaming platform KKBOX, OTT service KKTV, streaming solutions provider KKStream, live entertainment company KKLIVE, and content accelerator KKFARM (see also https://kkcompany.com). In terms of content strategy, compared with other platforms mainly focusing on popular Korean dramas and American dramas, KKTV cuts into Japanese dramas to make a market segment. KKTV has the largest library of Japanese dramas in Taiwan and simulcasts the latest Japanese dramas every season. Since 2018, the number of simulcasts per season has reached 7–11 dramas, ranking first among local platforms.

Data collection

For each of the cases, a database analysis was conducted. The method allows us to track the cases since the OTT video boom in Taiwan (i.e., 2016). Moreover, using third-party data provides an objective view of business strategies implemented by each case. We chose UDN Data and Business Next because the former includes the online full text of the eight newspapers of the United Daily News from the date of its first issue in 1951 and the latter focuses on the dynamics and trends of the latest technology, internet, entrepreneurship, and digital marketing issues. We identified 724 articles from 2016 to 2021, among which were 120 articles about LiTV, 223 articles about friDay Video, 159 articles about KKTV, and 222 articles about MyVideo.

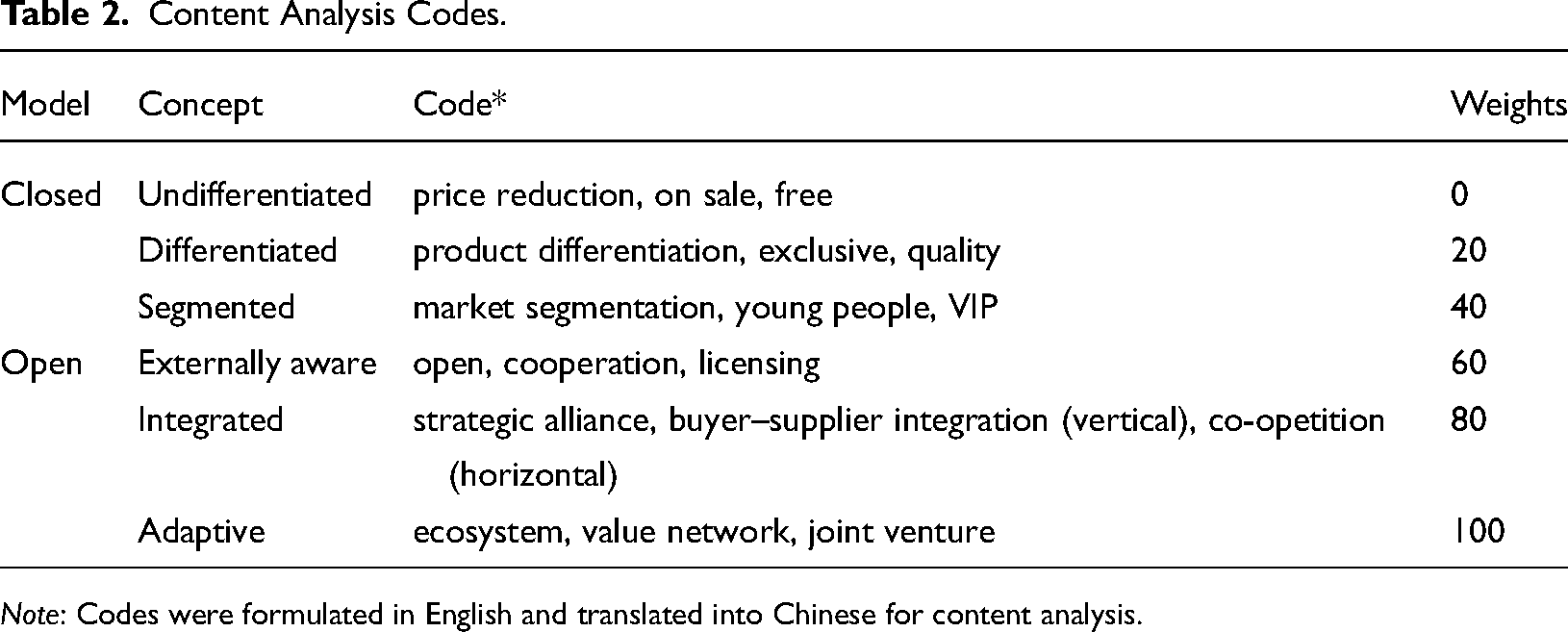

Two analyses were then implemented: a quantitative content analysis and then a qualitative document analysis. In the content analysis, we applied Chesbrough's (2006) operational definitions of undifferentiated, differentiated, segmented, externally aware, integrated, and adaptive business models to code-related paragraphs (Table 2). To prevent unbalanced coding, we retained the three most relevant codes to represent each concept. As a result, 2161 codes were identified. Moreover, we weighted each code's paragraph based on a business model openness index: 0 as undifferentiated, 20 as differentiated, 40 as segmented, 60 as externally aware, 80 as integrated, and 100 as adaptive. For example, we assign a weight to a paragraph if a business model code intersects with a case code. The purpose of weighting is to complement quantitative content analysis’ imprecision. Two graduate-level student coders were trained and guided to implement the coding and weighting. Intercoder reliability reached 0.85 to 1.00 for all codes. For the qualitative document analysis, we closely examined the weighted paragraphs and summarized the different practices of open business models adopted by the local OTT video platforms.

Content Analysis Codes.

Note: Codes were formulated in English and translated into Chinese for content analysis.

Data analysis

Both quantitative and qualitative analyses were implemented with the assistance of MAXQDA. MAXQDA is a software used to analyze qualitative finding for explaining and theorizing in the social and cultural phenomena. The software is developed and distributed by a German company VERBI Software since 1989. Marjaei et al. (2019) found that MAXQDA was one of the methods which allow researchers to do both content analysis and thematic analysis by counting the words and phrases and showing the relationship among them. In particular, our study took advantage of the software's MAXMaps function to visualize connections of different elements of codes, documents, memos, or coded segments on a workspace, a so-called map, and to put them in relation to one another.

Results

Open business models across platforms

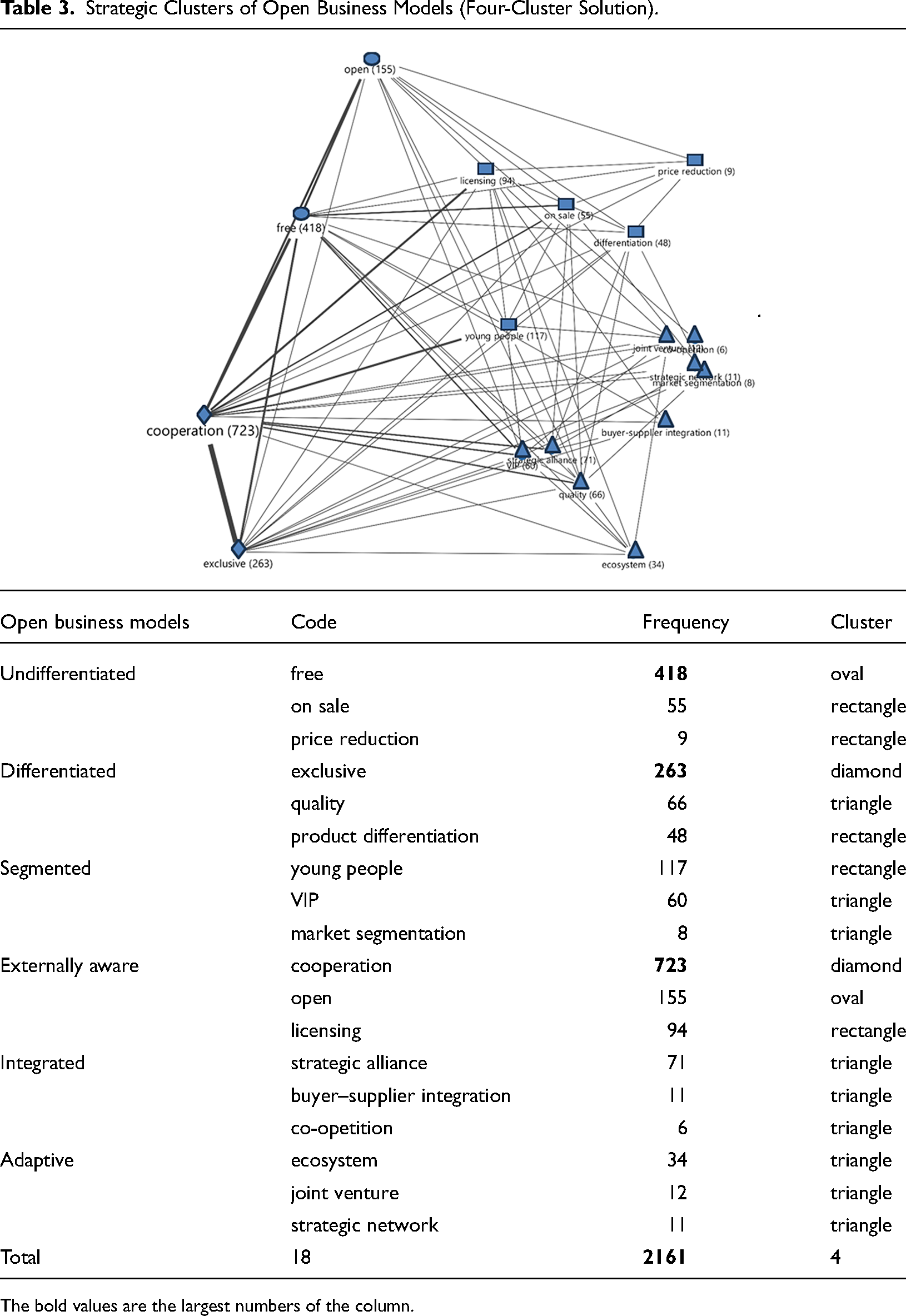

To address our first research question: What the range of openness is across local OTT platforms in Taiwan, a code map was generated by MAXQDA and illustrated in Table 3. By mapping the proximity of codes within the same paragraph, we were able to picture which business models were reported together in the news articles. Among the different business models, cooperation (723) is the most reported business model, followed by free (418) and exclusive (263); whereas co-opetition (6), market segmentation (8), and price reduction (9) were least stated in the articles. Collectively, we found that the externally aware (972) activities were reported the most, followed by undifferentiated (482), differentiated (377), segmented (185), integrated (88), and adaptive (57). The externally aware type is the mainstream model among the local OTT platforms in Taiwan, but undifferentiated activities are widely mentioned as well. That is, although Taiwanese OTT platforms have started to open their business models to external ideas or partners, they have a long way to go before some degree of differentiation and multiple market segments are developed; suppliers and key customers integrate their business models with them to achieve superior performance.

Strategic Clusters of Open Business Models (Four-Cluster Solution).

.

.

The bold values are the largest numbers of the column.

Moreover, given different business models are often implemented simultaneously in the real world, a further cluster analysis was explored, and a four-cluster solution emerged. The first cluster is “cooperation and exclusive” (diamonds), which has 193 coincidences. We found that exclusive content is a common differentiation model, and it often goes with cooperation with external suppliers, such as filmmakers or production houses. friDay focuses deeply on film festivals, including Golden Harvest Awards, TIDF Taiwan International Documentary, Urban Nomad Film Festival, etc., and will launch “One Chinese Film a Week” and launch

The second cluster is “free and open” (ovals) with 85 coincidences. Results show that OTT platforms open their businesses not only to partners but also to their customers. Platforms like KKTV launched the AVOD revenue model by providing free content without registration to the public. [KKTV] Under the premise of “no registration” and “login-free,” 20 episodes can be watched for

The third cluster is among “young people, licensing, on sale, differentiation, and price reduction” (rectangles). Coincidentally, OTT platforms regard outbound licensing as an ideal revenue stream but may sacrifice product differentiation. In other words, out-licensing and differentiation are competing business strategies so when and how the OTT platforms undertake the licensing model is a strategic action. In addition to relying on self-made content to point out the characteristics of the platform, CHOCO TV does not rule out

Business models in the fourth cluster (triangles) is least reported. Over-the-top platforms are not yet ready to fully cooperate with external partners in terms of integrative or adaptive types.

Open business models within each platform

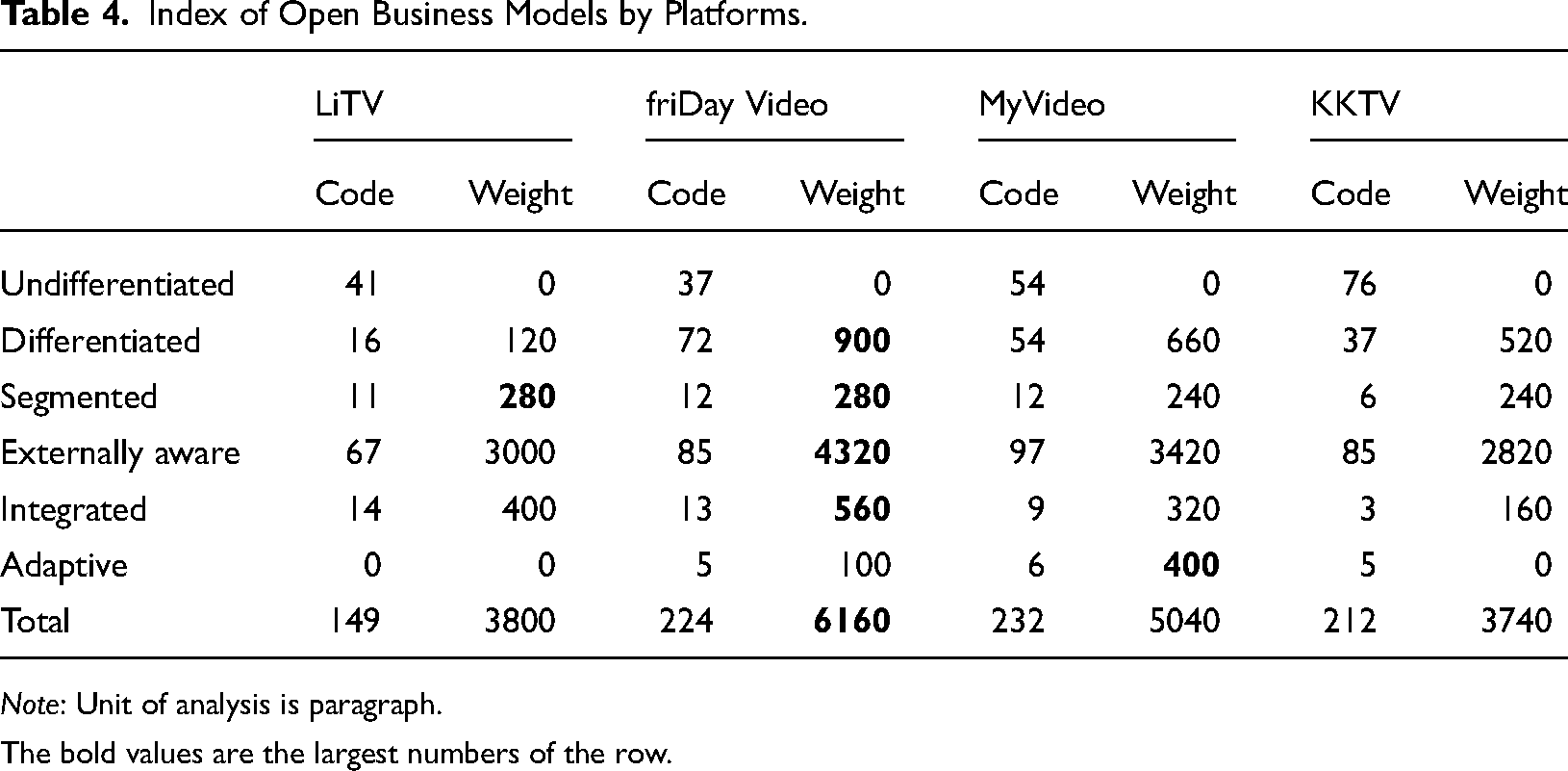

To address our second research question: What is the range of openness within each local OTT platform in Taiwan, Table 4 is an open business model index of the four cases. The index was created to weight the 2161 codes where cases are contained. As a result, 817 intersection codes were identified and weighted by five intervals from 0 to 100. Confirming the results from the collective data, “externally aware” is still the mainstream business model within each platform, but different OTT platforms pursue open business models differently. As listed, friDay Video scored 6160 and is the most innovative platform in terms of open business models, followed by MyVideo (5040), LiTV (3800), and KKTV (3740). Specifically, friDay Video tops the differentiated (900), segmented (280), externally aware (4320), and integrated (560) models. MyVideo tops the adaptive (400) model, though the adaptive activities are not common across OTT platforms. LiTV is tied with friDay Video for the lead in the segmented (208) model. The actual practices are presented in the third research question.

Index of Open Business Models by Platforms.

Note: Unit of analysis is paragraph.

The bold values are the largest numbers of the row.

Practices of open business models by platforms

Our third research question is: How local OTT platforms in Taiwan undertake open business models in practice. Throughout our document analysis, we identify six of nine most common open business practices that lead platforms to open their businesses: (1) cooperation with suppliers, (2) outbound licensing, (3) strategic alliances, (4) buyer–supplier integration, (5) co-opetition, and (6) joint ventures. We draw on case evidence and literature to explicate our results though examples are representative and not comprehensive in nature.

Cooperation With Suppliers

Externally aware firms start to open themselves to external ideas and technologies in the development and execution of their businesses (Chesbrough, 2006, 2007). Our cases score high in this category. Most OTT platforms in Taiwan do not possess content production capability so cooperation with suppliers, that is, content providers, is frequently adopted.

Taiwan Mobile announced yesterday that the energy of MyVideo's self-produced drama has exploded. After investing in three well-received and popular drama series in the first half of the year, it once again

Outbound Licensing

Moreover, OTT technically is able to offer D2C services, which are usually web-based or app-based, but if consumers prefer watching it on big screens, smart TV, or set-top boxes are required. Thus, our cases have licensed as many distribution channels as possible, including multisystem operators, telecommunication companies, and TV or set-top box manufacturers.

SAMPO launched a new generation of “4 K Smart Network Display,” which mainly built-in legally

Strategic Alliances

Integrated firms enjoy formalized institutional access to the firm's innovation process and this access is reciprocated by suppliers and customers (Chesbrough, 2006, 2007). In practice, firms may form a strategic alliance by signing a memorandum of cooperation to formalize a partnership (Osterwalder & Pigneur, 2010). friDay Video has catered to Taiwanese’ passion about Korean pop culture and has built formalized relationship with Korean-related firms, including content providers and telecommunication companies.

friDay Video said that it will join hands with Korea Telecom [KT] to exclusively broadcast the “Lovelyz” concert overseas on the 18th. This is after Far EasTone and KT signed a

In addition to commercial alliances, LiTV and KKTV convene local OTT video platforms to form an association, promoting legal rights and common interests. According to Statista's (2021) projection, global online TV and movie revenue lost through piracy is roughly USD 52 billion in 2022. Unauthorized streaming has a substantial impact on OTT platforms’ revenues and overall profitability. After a year of preparation, Taiwan's first OTT

Buyer–Supplier Integration

To assure reliable supply and demand, set-top box developers or telecommunication companies, especially those which did not produce nor license content, actively form upstream partnership to integrate software and hardware together.

Asia Pacific Telecom launched the “BANDOTT Audio-Visual Service” nicknamed “Bento (lunch box)”, which

Co-opetition

Co-opetition is a special type of strategic partnership between competitors (Osterwalder & Pigneur, 2010). After Netflix exclusively teamed up with Taiwan's largest telco Chunghwa Telecom in 2019, Taiwan Mobile owns a OTT video service MyVideo, cooperated with Discovery in 2020 and Disney+ in 2021. The telcos believe that the co-opetition strategies have brought positive network effects.

Disney+ and Taiwan Mobile announced today that Taiwan Mobile will become Disney+'s exclusive

Joint ventures. An adaptive business model is an even more open and adaptive model than the previous types (Chesbrough, 2006, 2007). Suppliers are integrated into the planning process of the adaptive firm, which in turn has integrated its business model into the business model of its key customers. Strictly speaking, no company meets the definition. However, MyVideo formed several project-based joint ventures by investing in content coproduction. KB Entertainment, invested by KBR and Taiwan Mobile, has actively invested in movies and dramas in recent years. MyVideo has become a powerful OTT channel; Win TV has also entered the 76 channels of cable TV. The two channels are formed and will increase investment in content. It is expected that A Taiwanese Tale of Two Cities, a

Notably, Far EasTone just announced a firm-based joint venture, Ideaworks Entertainment, in 2023 to produce and invest in high-quality films and dramas and to promote Taiwanese culture (Yahoo News, 2023). Because the news was released after the study's data collection, the joint venture was not recorded in the results.

Discussion

The OTT video market is highly competitive because of the presence of many global players. Intense competition and increasing technological advances are significant risk factors for local OTT platforms. In previous studies regarding open business models, small-scale firms utilizing services provided by partners in their strategic network may achieve sustainable market performance and successful business models (Chu & Chen, 2011; Davey et al., 2010; Frankenberger et al., 2013; Visnjic et al., 2018). This study looks at the Taiwanese OTT video market using multiple case studies with firm-level data collected from two prestigious news databases in Taiwan from 2016 to 2021.

Our study finds that the externally aware type is the mainstream model in the Taiwan market, whereas the adaptive type is the least focused. The result shows that OTT platforms have started to open themselves to external ideas and technologies, implying that the industry is going toward a promising direction because firms may reduce the cost of operation, reduce the time it takes to get new offerings to the market, or share the risks of new products and process with other parties (Chesbrough, 2006, 2007). Moreover, friDay Video scored highest in terms of business model openness partly because of its parent company's telecommunication resources and partly because of its market insights about Korean pop culture and new economies. Finally, six common practices of open business models were identified: (1) cooperation with suppliers, (2) outbound licensing, (3) strategic alliances, (4) buyer–supplier integration, (5) co-opetition, and (6) joint ventures. Linking the open business models to local OTT platforms allows us to develop an initial understanding of the relevance of the specific activities for each OTT platform.

In academic contribution, we relate to the literature on OTT video and open business models in several ways. It contributes to the understanding of the OTT video disruption that creates unprecedented opportunities and intense competition and the business model openness that may achieve sustainable market performance. Furthermore, while most of the previous literature provides typologies of OTT video business models (Huang & Wu, 2020; Lin, 2020; Park, 2018, 2019; Wang & Lobato, 2019), this study offers empirical evidence of open business models. In managerial contribution, we make several implications for industry and policy. First, we identify the OTT video market as externally aware, representing that local OTT video platforms are starting to open their business models to external partners, but the extent of cooperation should be greater if they are to compete with international giants. Second, we provide the most open case (i.e., friDay Video) and six most common practices of open business models so local OTT platforms can be studied, benchmarked, adopted, etc. Last but not least, co-opetition is the most complex and advantageous relationship between competitors (Engtsson & Kock, 2000), so the government can play an intermediate role to promote cooperation among competitors. Related public and financial policies may incentivize local content coproduction and local platform mergers and acquisitions with tax breaks.

It is also important to address limitations in our study and direction for future research. First, database analysis of news articles enables us to review longitudinal and collective data, but the selected databases may not provide comprehensive information, nor we know the reasons behind these practices of open business models in each OTT platform. Future research might conduct in-depth interviews to fill the gap. Second, friDay Video was found to be the most-open local OTT platform in Taiwan, but the market is transient and young; given the domination of global giants, no local OTT platforms can take it lightly. Future study might focus on the case and conduct a deeper analysis to get a thorough picture of its open activities and trade-offs. Finally, few studies empirically test the open business models for OTT video platforms; therefore, future research may want to improve and modify the operational definitions of each type in this study.

Footnotes

Acknowledgments

The authors would like to thank Min-min Tsai and Man-Hsiu Hsu for their assistance of literature review and data collection and to thank the anonymous reviewers and the Editor for their constructive comments in bringing this paper to fruition.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Science and Technology Council (grant number MOST 110-2410-H-A49-043-MY2).