Abstract

Dong-Ping Song and Chung-Yee Lee recommend that, if they want to weather severe disruptions in the future, shippers and ocean carriers must turn toward more collaborative and committed relationships. Digital technologies and appropriate regulations will help them to do so.

Since the outbreak of COVID-19, container shipping has experienced extraordinary changes. Ocean freight rates in shipping lanes, such as those between Asia and the US and Asia and Europe, skyrocketed in 2021, reaching more than five times the pre-pandemic rates. Global supply chains were left staggering, with the leaders of both carriers and their clients desperately seeking any means to expand their shipping capacity, from ordering new ships and chartering older ones to delaying ships on the way to the scrap heap and converting ships built for other uses to carry containers. But in the long term, these measures are unlikely to solve the problem. Indeed, they may even cause already disrupted supply chains to deteriorate further.

The Common Myth about Freight Rates

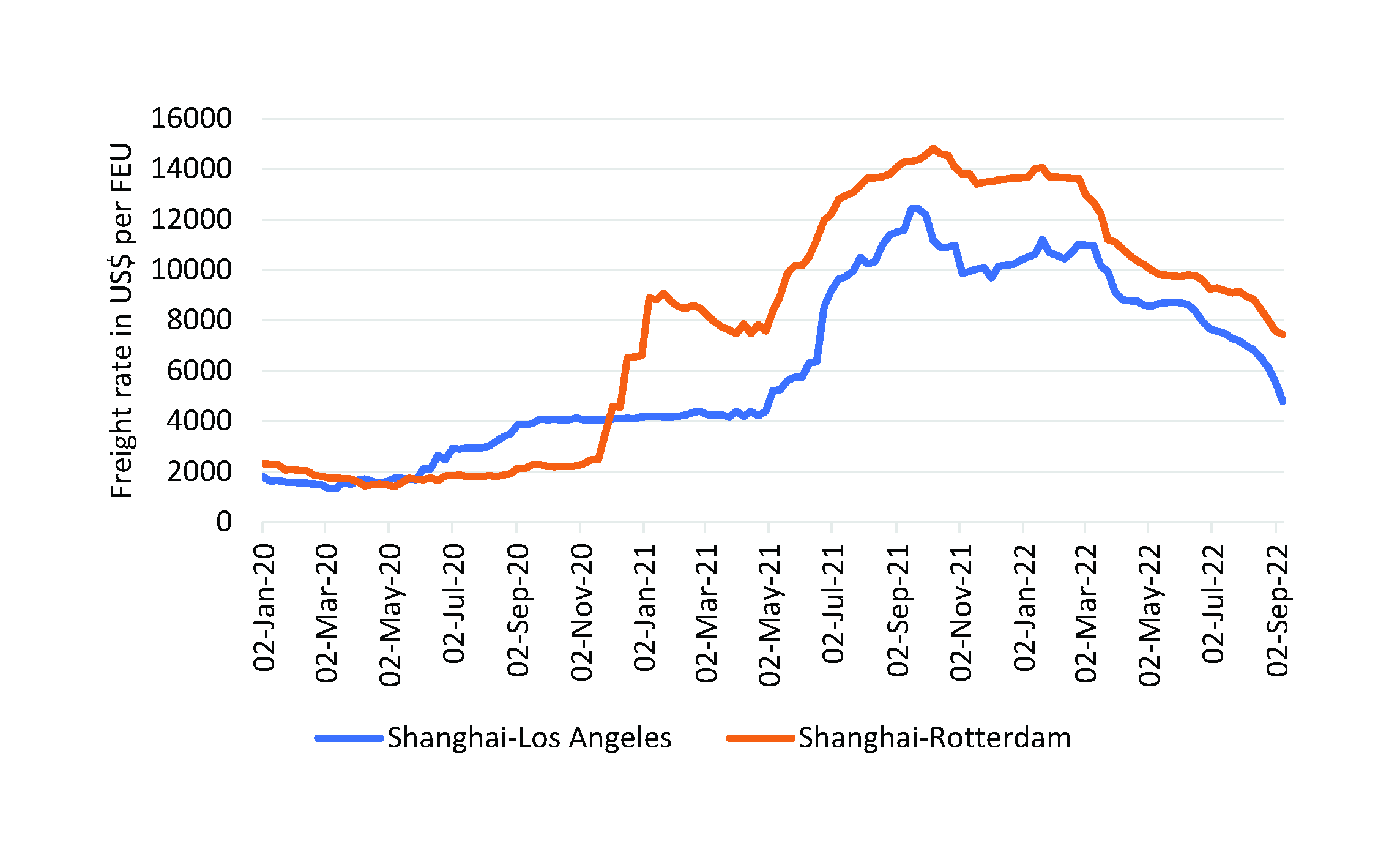

At the beginning of the COVID-19 pandemic, worldwide lockdowns and mass cancellations caused a strong downturn in containerized trade. By the second half of 2020, consumers had altered their shopping patterns, which increased demand for manufactured goods including medical products, home office equipment, and processed foods. Most of these products are transported in shipping containers. According to Drewry, in September 2021, the rates for shipping freight from Shanghai to Los Angeles and to Rotterdam reached historical highs at $12,000 and $14,300 per forty-foot container (FEU), respectively. Rates remained high, at $10,700 and $13,600, in February 2022, more than five times the rates in January 2020 (see figure 1). This drastic increase has raised growing public concern because most businesses cannot absorb the massive costs. This pressure may drive some shippers, especially small ones, out of business. Moreover, most companies will eventually pass the increasing cost of freight on to consumers, which may drive global inflation. In March of 2022, the consumer price index for the US reached a forty-year high of 7.9 percent. Consistently high inflation in the first half of 2022 drove down demand, causing a rapid decline in freight rates. By September 2022, the shipping industry began showing signs of excess capacity. Trade demand is not the sole driver of freight rate increases. Container freight rates from Shanghai to Los Angeles and Rotterdam in US$ per 40ft container (based on the data from Drewry)

The common wisdom suggests that extraordinary ocean freight rates occur when trade demand significantly outpaces shipping capacity. However, according to Container Trades Statistics, the global volume of container trade in the first half of 2021 increased by 13.5 percent from 2020 and 6.0 percent from 2019. Since the 2020 numbers were influenced by pandemic lockdowns, the 2019 data offers a more realistic comparison, revealing an average growth rate of 3 percent over two years. This rate is in the normal range and, in a normal situation, would not overstretch the available shipping capacity. In particular, demand on the Asia-Europe route grew just 0.7 percent.

1

This modest change indicates that trade demand is not the sole driver of freight rate increases. A more reasonable explanation is that the sudden jump from a drastically reduced volume to one greater than normal caught the shipping industry by a surprise. At the outset, the container shipping supply chain (CSSC) was not ready for the sudden increase and later it suffered from various congestions. The surge in demand placed container equipment, shipping capacity, port and hinterland infrastructure, and human resources under severe pressure and bottlenecks plagued the entire CSSC. During the pandemic, several factors combined to overwhelm the CSSC and drive up ocean freight rates.

Disrupters of the CSSC

During the pandemic, several factors combined to overwhelm the CSSC and drive up ocean freight rates.

The disconnect between outgoing and returning containers

The CSSC is composed of two interwoven chains: laden containers traveling outward and empty ones traveling back. Each relies on the other. In the first half of 2020, carriers responded to flagging demand by increasing blank sailings: cancelling stops in particular ports or cancelling sailings entirely. This strategy left many empty containers in Europe and the US, when regular sailings would have carried them back to Asia. As demand suddenly picked up in the third quarter, many Asian ports suffered severe shortages of empty containers, which triggered a rise in rates for routes from Asia to Europe and the US. The shortage of containers was exacerbated as pandemic-induced delays trapped containers in waiting vessels and intermodal connection points. Since the second half of 2021, carriers have been accused of ignoring US export cargos, choosing instead to send empty containers directly back to Asia so they can earn the far higher freight rates for bringing cargos into the US. This practice has created import to export ratios as high as 5:1, which worsens the already severely imbalanced trade between the US and Asia. 2 In the US, a trucker has to secure a chassis from the maritime terminal pool in order to collect an import container. A shortage of chassis also hinders the flow of both laden and empty containers.

Congestion at ports and inland depots

A mismatch between seaborne and hinterland transport causes peaks and troughs of port congestion. If the port has adequate storage yard capacity, and the slow periods are long enough to balance the heavy ones, port congestion may be relatively brief. From the second half of 2020 to the end of 2021, many hub ports in Europe and the US had densely packed yards. Meanwhile, bunched vessels kept containers flooding in, diminishing the trough periods. Port capacities have thus become a persistent bottleneck. On Asia-Europe routes, Alphaliner reported vessel delays averaging seventeen days in November 2021 and again in February 2022, brought on by severe congestion in northern European ports, including Rotterdam, Antwerp, and Hamburg. The congestion was fueled by packed yards and a shortage of port workers and truck drivers. In the US, the contiguous ports of Los Angeles and Long Beach have suffered near record congestion since late 2020. Some vessels have waited, anchored, for more than ten days to be berthed because there was no storage space available for import containers. 3 Port congestion ripples through to hinterland infrastructure, including intermodal services and inland depots. Chicago is the leading container hub for rail freight from West Coast ports. Since April 2021, the volume of arriving containers has continuously exceeded the processing capacity of the rail yards. On one occasion, rail operators had to suspend the movement of containers from ports to the Chicago hub for a full week. Here again, shortages of workers and chassis slowed the transfer of containers from rail yards to loading points, increasing the dwell time of containers in the yards and exacerbating the congestion at rail hubs and seaports. 5 China’s zero-COVID policy sparked port congestion, locking down major ports like Shenzhen, Ningbo, and Shanghai and slowing exports as container ships waited to berth. According to project44, the average number of ships waiting per day in the South China/Hong Kong region was 17.5 in December 2021 and 22.5 in January 2022, at least five times more than usual.

Worker shortages

The pandemic caused a shortage of human workers in the CSSC, especially among port staff and ship crews. Fearing the high risk of catching COVID-19, workers shied away from jobs at ports and on ships. Changing ship’s crews became extremely difficult in the face of increasing restrictions on ports and flights. In the UK, both the pandemic and Brexit contributed to a severe shortage of lorry drivers. When the ports of Shenzhen, Ningbo, and Shanghai were partially closed in June and August 2021 and April 2022 because of outbreaks among the staff, both the port’s handling capacity and the effective shipping capacity dwindled as vessels were quarantined and diverted.

Lack of contract enforcement

Historically, the relationships between carriers and shippers are dependent on freight rates. Container shipping is offered at either a contract rate or a spot market rate. In practice, it is not unusual for either side to renege on a contract rate.5 Shippers in the spot market may fail to produce the volume of freight they have booked, termed a no show, while carriers may postpone bookings to a later voyage, termed a rollover. Industry-wide practice ensures that neither party will be penalized for failing to fulfill its commitments. The lack of penalties for no shows and rollovers creates huge uncertainty in the shipping industry and reduces supply chain efficiency. Port and terminal operators also fail to fulfil commitments to carriers and vice versa. Container terminal operators generally have formal contracts with carriers which detail when and where their ships will dock, as well as their terminal handling costs. Although the contracts describe penalties for the carriers if the vessel is late or does not turn up, and for the terminal operators if port handling time runs over, these penalties are rarely executed because neither party wants to risk its business by upsetting the other. 6 The pandemic produced a surge of these broken commitments, especially rollovers. According to Ocean Insights and project44, the container rollover ratio of leading ocean carriers was 5 to 17 percent in the second half of 2019, increased to 22 to 50 percent in April 2020, and a whopping 28 to 56 percent in April 2021. Failure to fulfil contract commitments also worsened. One US shipper took legal action against carriers COSCO and Mediterranean Shipping Company (MSC) for ignoring their contractual obligation to provide a given amount of container shipping space between May 2020 and April 2021. 7 Another accused HMM and Yang Ming Maritime Transport of failing to transport the minimum number of containers guaranteed by 2021 contracts. 8 By increasing blank sailings during the pandemic, ocean carriers essentially also defaulted on their contracts with terminal operators.

Lack of coordinated visibility

Each stakeholder in the CSSC works with its own information. They neither standardize data nor share it in real time. Each participant does its own planning with little coordination. Although carriers do update terminal operators on expected arrival times as each ship approaches, they do not share detailed information about the containers aboard, such as cargo owner, inland destination, and hinterland transport mode. Trains, meanwhile, are often delayed by uncertainty in the national rail networks. Moreover, terminal operators do not receive the loading list of import containers until a few hours before the train arrives because inaccurate information and urgent customer needs may change the list at the last minute. 9 And while road haulers do book appointments through the vehicle booking system (VBS), they don’t always keep them. In the first week of August 2021, Southampton port recorded that 56 percent of vehicles kept their appointments on weekdays and a mere 15 percent on weekends. Truckers either cancel or fail to turn up for bookings, which thwarts the purpose of VBS, which is to make truck arrivals less random, leveling their flow through terminals. This lack of coordination between terminal operators and carriers allows containers to linger in port storage yards, reducing the efficiency of port operations.

Mistrust

According to Sea-Intelligence, the container vessel schedule in July 2021 was 35.6 percent reliable, down 39.7 percent from the previous year.

10

Indeed, global schedule reliability has been consistently below 40 percent since Jan 2021, whereas before the pandemic it was over 70 percent reliable. This uncertainty causes vessels to arrive in clumps, which exacerbates port congestion, further delaying the vessels’ arrival at their next port of call. This network of delays causes mistrust between the port administrators, carriers, and shippers. These parties have also long argued about detention and demurrage charges, fees which carriers levy against shippers for containers delayed outside the port and in port storage, respectively. Shippers complain that carriers and terminals use these charges to generate revenue rather than promote a smooth flow of goods. With only a slight increase in throughput, the port of Hamburg increased its average revenue per container by over 10 percent in the first six months of 2021, mostly in storage charges resulting from port congestion.

11

The Agriculture Transportation Coalition in the US claimed that carriers charged unreasonable detention and demurrage fees without considering the congestion at ports and inland yards. It found that these charges accounted for 20 percent of the 2021 revenue of ocean carriers.

12

The US Federal Maritime Commission responded by launching an investigation into unfair detention and demurrage practices. Soon after, the dispute reached the legislative level, with the US Congress discussing the Ocean Shipping Reform Act of 2021. Among other points, it states that “importers, exporters, intermediaries, and truckers should not be penalized by demurrage and detention practices when circumstances are such that they cannot retrieve containers from, or return containers to, marine terminals.”

13

The initial, quite reasonable, caution of shippers kicked off a vicious circle best known in the literature as the bullwhip effect.

The bullwhip effect

As the pandemic gained momentum, most consultants advised firms to adopt risk-mitigation strategies, making their supply chains more resilient by building up excess inventory, ordering in advance, establishing flexible sources, and using flexible transportation. Bracing for disruptions, shippers began to order larger quantities earlier. Large companies used their ability to pay the high freight rates as an opportunity to squeeze out smaller competitors. All of these moves distorted demand patterns, exaggerating volumes. The exaggeration sent distorted signals to shipping lines which scrambled to expand their fleets, pushing more ships and more containers into already congested ports. As more vessels and containers became trapped in congested ports, they created the appearance of a shortage of shipping capacity. Meanwhile the handling rates in ports deteriorated, delaying the delivery of containers to shippers. In essence, the initial, quite reasonable, caution of shippers kicked off a vicious circle best-known in the literature as the bullwhip effect. 14

Other events have also influenced the availability of containers and shipping capacity in the CSSC. When the Ever Given container ship drifted sideways to block the Suez Canal in March of 2021, it forced carriers to decide whether to keep hundreds of vessels waiting or divert them around the Cape of Good Hope. Hundreds of thousands of containers were stuck at ports or on waiting ships.

The International Maritime Organization’s decarbonization plan may cause similar, though expected, logistical chaos, forcing carriers to adjust to slow steaming and to scrap less energy-efficient vessels.

Possible Solutions

The severe disruption of the CSSC has become a global crisis. Yet a variety of measures could alleviate the problem and prevent its recurrence, and some of them are already underway.

Expanding the fleet

Shippers are struggling to find enough empty containers and vessel space to meet demand. In response, carriers are working to increase their shipping capacity by relaunching laid-up vessels, chartering or buying second-hand ones, purchasing new-built craft, and converting dry bulk carriers into container ships. In March 2020, 13 percent of the container ship fleet was idle. By July 2021, this figure had dropped to below 3 percent, a number which is essentially equivalent to the number of container ships that, at any given time, are out of service for mandatory surveys or dry-docking. 15 In the first six months of 2021, over one million TEU capacity in ships – one TEU being a standard twenty foot container – changed ownership in the second-hand market, a record high for a six-month period. 16 The number of new container ships that carriers ordered in 2021 exceeded the combined number ordered from 2017 to 2020. Clarkson Research reported that, in 2021, shipbuilders received orders for a total of 4.2 million TEU of capacity. The combined 2021 demand for container ships was thus equivalent to nearly 25 percent of the world’s existing shipping capacity. Both shippers and carriers also looked into other options, including air and rail, as well as general cargo and break-bulk ships, which have traditionally been used for goods that don’t readily fit into a standard container. ISS Global Forwarding India chartered twelve bulk vessels and converted them for container shipping. Walmart and Home Depot directly chartered vessels to carry their goods. In its bid for more shipping capacity, TJX Companies narrowed its list of carriers to increase its negotiating power. 17 Meanwhile, GENCO Shipping & Trading chartered its bulk vessels to Walmart and FedEx Logistics to carry containers from China to the US West Coast. 18 And Concordia Maritime, a Gothenburg-based tanker shipping company, began to investigate the cost of converting a tanker into a container ship. 19

But expanding shipping capacity by itself will not solve the current crisis or ward off future disruptions. It may even cause disrupted supply chains to deteriorate further. Because the weakest link in the current CSSC is port and hinterland infrastructure, increasing the fleet will not improve efficiency. Congested ports reveal that the handling rate of the port logistics system, including quayside, storage, and inland operations, has fallen below its normal level. More vessels will only push more containers into these overburdened port systems. Little’s Law argues that the more things you work on in a given time, the longer it will take to complete each. With fixed or even decreasing port handling rates, adding more ships to the system will only increase the time that each ship and container has to wait. Indeed, in October 2021, about 12.5 percent of the world’s container fleet had been absorbed by port congestion delays.

20

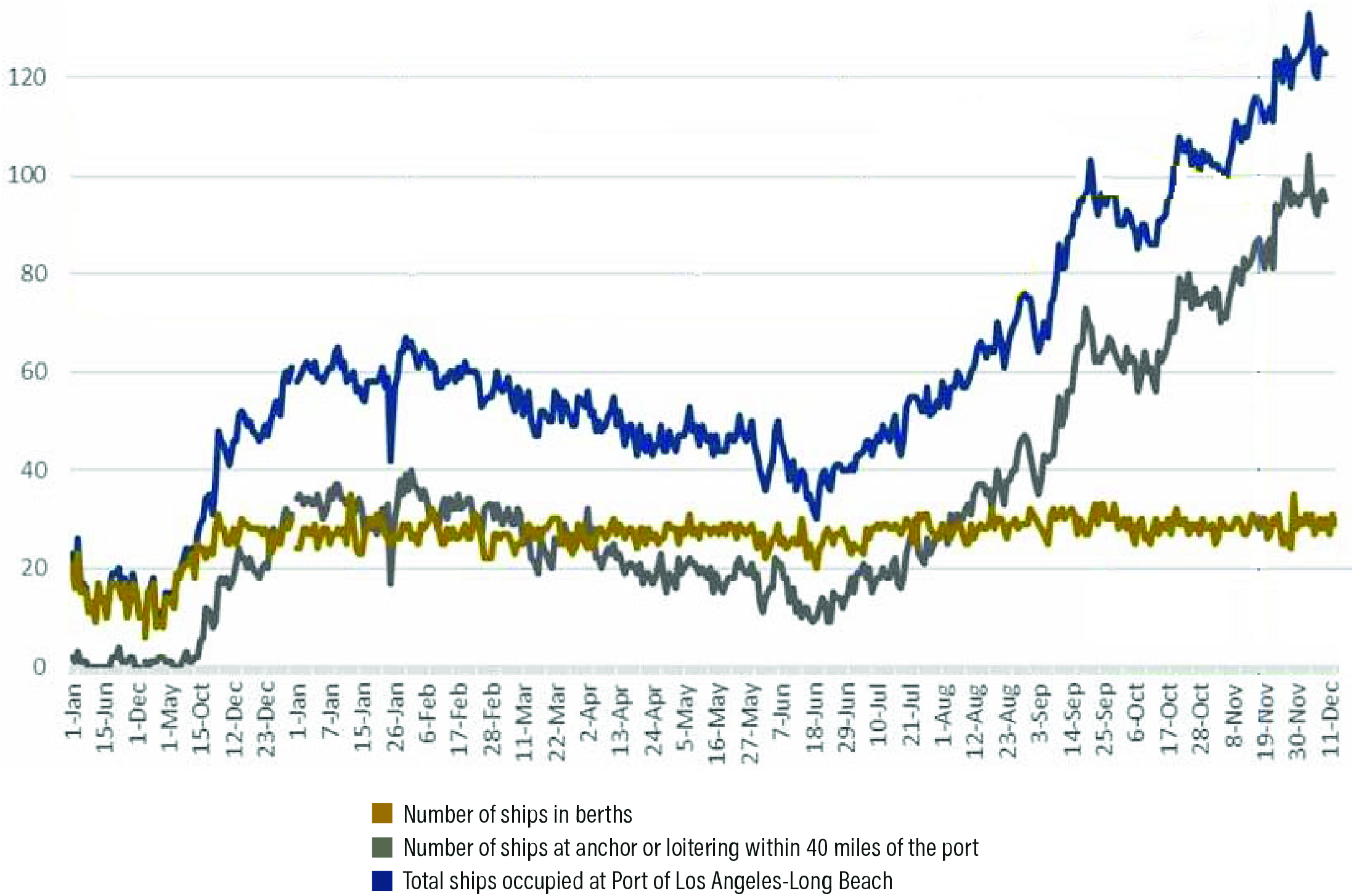

The time that container ships waited to enter the port of Los Angeles-Long Beach in November 2021 was seventeen days, twice the September wait (see figure 2).

21

All of these contributing factors spring from the failure of stakeholders in the CSSC to build collaborative relationships, thus inviting fragmentation and inefficiency. Container ships at Port of Los Angeles-Long Beach from January 2019 - December 2021

22

Solutions

All of these contributing factors spring from the failure of stakeholders in the CSSC to build collaborative relationships, thus inviting fragmentation and inefficiency. In order to repair the disrupted CSSC and prepare it for the next crisis, stakeholders must move toward more collaborative and committed relationships. They can start down this road by addressing several core problems. 1. 2. 3. 4. 5. 6. 7. In order to rebalance supply with demand, ocean carriers may turn to frequent blank sailings, slow steaming, and scrapping old vessels.

These measures have different implications for different stakeholders. High freight rates are good for carriers and high yard density for ports. Ocean carriers also tend to be conservative and risk-averse; they may not be very keen on changing supply chain relationships. But between 2009 and 2019, these companies experienced a radical change in market situations, suffering supply chain fragmentation and overcapacity. The 2016 bankruptcy of Hanjin Shipping, one of the top ten ocean carriers in the world, was a wake-up call. Carriers have plenty of motivation to build more sustainable supply chains.

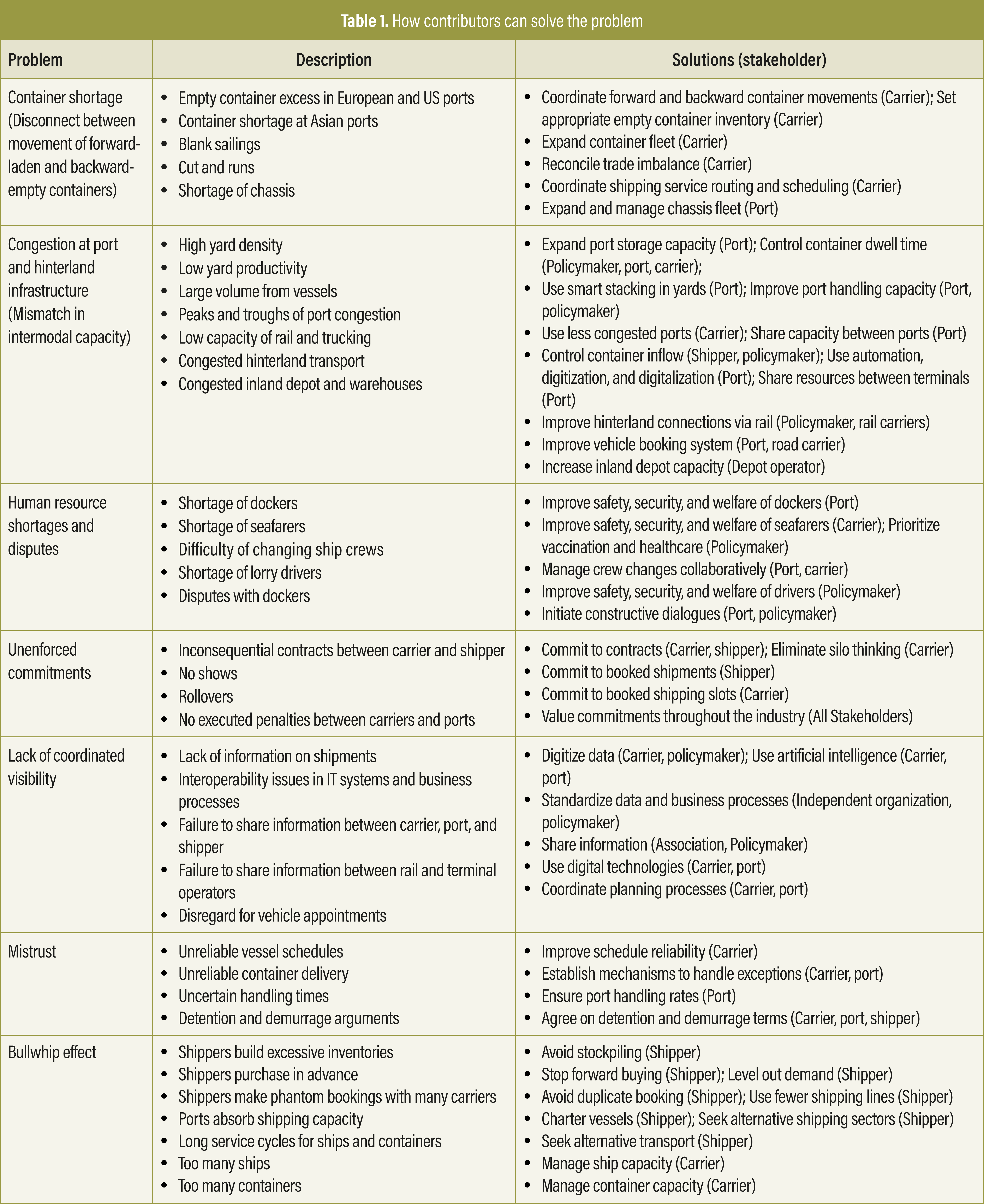

During the pandemic, congested ports were the primary bottleneck, with a yard occupancy rate of over 90 percent in most major US and European ports. Since a port’s efficiency plummets as its yard occupancy increases, all stakeholders in such cases should immediately take steps to alleviate the congestion. Bringing port productivity back to normal will allow the entire CSSC to recover its efficiency. Participants at every stage can contribute: shippers, by eliminating their forward buying to reduce demand; carriers, by reducing the frequency and slowing the speed of ships departing from Asian ports to prevent bunching; and the ports themselves, by clearing the backlog as efficiently as possible. However, this approach requires a collaborative effort by all parties. Shippers, whose business is most harmed by a disrupted CSSC, should take the initiative, working through associations like the Global Shippers Alliance (GSA), the Federal Maritime Commission (FMC), and the European Shippers’ Council (ESC). They should also consider engaging with policymakers. But all contributors must do their part to repair a disrupted CSSC and to increase its resilience before the next disruption (see table 1). COVID-19 has shown us that key stakeholders in the CSSC, including shippers, ocean carriers, and ports, should rethink their relationships, cooperating to devise sustainable ways to repair, or even avoid, future disruptions. How contributors can solve the problem

COVID-19 has shown us that key stakeholders in the CSSC, including shippers, ocean carriers, and ports, should rethink their relationships, cooperating to devise sustainable ways to repair, or even avoid, future disruptions.By using digital technology and supporting appropriate regulation, they can strengthen supply chains and mitigate the vicious cycle of congestion. Number of ships in berths Number of ships at anchor or loitering within 40 miles of the port Total ships occupied at Port of Los Angeles-Long Beach

Footnotes

Author Bios