Abstract

Land and property, and the wealth extracted from it, has reappeared as a central concern in understanding the process of urbanisation under capitalism. Much of the academic discussion centres on the re-emergence of ‘rentier capitalism’ drawing on 19th-century concepts of land economics. However, the accumulation of wealth through property ownership and the development process points towards a value proposition contained in the land question that is not satisfactorily explained by notions of ‘rent’ or ‘rentier’ capitalism, rooted as they are on 19th-century concepts of the land development process. This article seeks to extend this debate by exploring multiple regimes of value that underpin the contemporary urban development process. The first part of the article maps out four intersecting regimes of land value, before arguing by reference to empirical analysis of land and property sales data in Sydney Australia that switching between these value regimes – value switching – is a key transformative moment in the urban development process. Specifically, this article argues that value switching, as triggered by the land use planning process, has become the key driver of urban development dynamics and adds a further dimension to theories on land and housing development in the financialised city.

Introduction

Recent urban scholarship has seen a renewed focus on land as a central concern in understanding the process of urbanisation under capitalism Christophers (2018b). The renewed focus on questions of land has perhaps been driven by the re-emergence of wealth inequalities tied to ownership of housing (Adkins et al., 2020; Ronald et al., 2017). Although certainly not universal, home ownership in the second half of the 20th century, socialised the ownership of land to some degree and played a central role in wealth redistribution, particularly in countries like Australia (Gleeson, 2006). However, Christophers (2018b, 2020) has noted that more recent concentrations of wealth since the 1970s have been due to the increasing dominance of ‘rentiers’ across all aspects of the economy, not just residential property. More generally, Piketty’s (2014) concept of ‘capital’ encompasses wealth accumulated by land and property as well as other components of wealth, contributing significantly to the re-emergence of wealth inequality since the 1960s. As housing and housing markets have become increasingly driven by financial logics, actors and networks, Adkins et al. (2020) have argued that property ownership is now the central feature that defines wealth and class inequalities.

While some of this interest stems from studies associated with aspects of gentrification and is associated with scholarly contributions from urban political economists, it has also become an emergent interest in urban studies and planning research with a particular focus on value capture (Crook et al., 2016; SGS Economics and Planning, 2016). The focus on the role of value creation in the urban environment and in the process of accumulating, monetising and extracting that value, has become more evident as urbanists have better understood the financialisaton of housing and its pervasive association with the land development process. There can be little doubt that there is a close link between the emergence of liberalised global capital markets following the great deregulatory impulses of the 1980s and 1990s and the financialisaton of real estate, and especially residential real estate, over the last two to three decades.

This article does not intend to rehearse these debates. Instead, it seeks to do two things. First, we aim to unpack how value is generated within the built environment with reference to recent trends in Sydney’s apartment market. For this, we seek to conceptualise the notion of regimes of land value that underpin the urban residential development process (in our case exemplified by higher density apartments) and impart value to a parcel of land. Second, we argue that value changes can be triggered by a range of processes, but that once triggered the value of a parcel of land will reflect that changed regime of value, regardless of its current use.

The first part of the article presents a broad discussion on land and value in urban scholarship before mapping out four intersecting regimes of land value by which value is ascribe to land and property. The second part argues that switching between these value regimes – value switching – is the key transformative moment in the urban development process which opens up the prospects for value uplift and capture. The third part explores these ideas through empirical examples of value uplift from Sydney which have been generated by changes in the regime of value, triggered by a change in planning settings before offering a concluding discussion ‘value switching’ in relation to property and the urban process.

Land as a source of value

Much of the discussion conceptualising land as a source of value centres on the re-emergence of rentier capitalism, where income generated through land and property ownership increasingly dwarfs wealth generated in the real economy (Christophers, 2020). Focusing on land in particular, the re-emergence of corporate landlordism in various contexts (Beswick et al., 2016; Fields and Uffer, 2016) and the army of ‘mum and dad’ landlords that have emerged over the past two decades in several countries (Hulse et al., 2020; Konings et al., 2021; Murray and Ryan-Collins, 2020; Troy et al., 2020) go a long way to support this thesis. Interrogating land value as rent builds on long standing urban scholarship that identifies the gap between present and future rents as a key driver of urban change (Smith, 1979).

While corporate landlords may well look to maximise rental income as a key investment objective, one of the striking features of the mum and dad landlord, in Australia at least, is an emphasis not on rent but on capital growth as their key objective. This is revealed by the continued political support for negative gearing and capital gains tax reductions which enable such owners to run a loss (where that rental income doesn’t cover expenses of owning), offset these losses against the investor’s income and then reduce the tax take on capital growth once sold. In other words, the main objective of these landlords is to make capital gains, not rental yields. For example, Martin et al. (2022) found that in a study of landlord investment behaviour in Sydney and Melbourne, the most common reasons given for selling an investment property was that it was a good time to realise capital gains or to free capital to reinvest elsewhere. If true, this objective is in contrast to the classical concept of the rentier capitalist living off rental income generated by ownership of property and fundamentally challenges rent gap theories of urban change (Seelig et al., 2009).

Put simply, investor activity in the residential market with the prospect of capital growth, has been a dominant component and shaper of housing markets in Australia. The question then arises as to how the capital growth that such investors seek is generated. The answer, as pointed out by Hamnett and Randolph (1986), is that this value is generated in the home ownership market. In a housing market dominated by mass home ownership, capital values of properties that may be rented are nevertheless set by reference to the wider home ownership market, not as a function of multiples of rental income. In other words, capital values in the contemporary residential market have little, if anything, to do with rents per se.

Consequently, the increasing wealth that is derived from land and property ownership, points towards a value proposition contained in the land question that is not satisfactorily explain by conventional concepts of land rent or rentier capitalism. Property development in cities like Sydney, London or New York over the past two decades has been underpinned by extensive flows of investor – and often international investment – capital, and the wealth extracted through the urban development process bears little direct relationship to the actual production of new buildings per se or the potential rental incomes they might generate. Rather the focus is on the speculation in land values that can be accessed through the development process. Of more relevance here is the issue of how contemporary property development generates changes in value and the processes which enable its extraction.

This is where the ‘compact city’ enters the equation. The vertical expansion of cities through residential apartment building across the globe has been remarkable over the past two decades (Nethercote, 2019; Troy et al., 2020). Policy makers are quick to point towards rapid urbanisation and population growth as well as concerns over the environmental challenges of urban growth as key drivers promoting high density futures (White and Serin, 2021). However, the nexus between housing supply and population demand is contested within the urban studies literature and points to a far more nuanced understanding of property and development dynamics driving the production of new dwellings. Weber (2015) has argued that, in Chicago at least, development had less to do with the demand of future occupants, and more to do with the availability of capital from financial markets. This argument has its roots in Harvey’s (1982, 1985) work on urbanisation of capital, which aimed to outline how broad movements of capital actively shaped the urban investment decisions and physical outcomes as well as the role of land and property as increasingly seen as a financial asset in its own right.

A central theme underpinning much of the literature is the desire to extract value in the form of profit from the urban process, with much of analytical focus on the flows of capital, financialisation, role of the state, or role of market and other actors. For example, a recent paper by (Robinson and Attuyer, 2021) articulates the role of Governments in supporting value extraction and shows how the state itself seeks to capture, at least partially, that value. Weber’s (2015) account of development in Chicago unpacks the logics and contextual drivers of development, highlighting how expectations on capital growth was driving investment and creation of asset price bubbles. Stein (2019: 5) has powerfully argued that housing ‘has become and globally traded financial asset, creating the conditions for synchronised bubbles and crashes’. He concludes, ‘Taken together, we witness the rise of the real estate state, a political formation in which real estate capital has inordinate influence over the shape of our cities, the parameters of our politics and the lives we lead’ (Stein, 2019: 5). What is perhaps less understood in these accounts is how value is actually generated on the ground. A core argument here is that development in urban space is driven by the motivation to extract value from the process of uplift in land and property values, and while there are clues, what is less clear is what is the nature of that value and how this inherently connects to the nature of the development process itself and the urban outcomes it produces.

What constitutes value in urban landscape and how we understand that is the source of much discontent in urban literature. Lake (2023: 3) recently argued that that the absence of an explicit value theory has ‘conceptual and political costs’ and that value should not be seen as ‘monological, timeless and universal’ and that there are a variety of approaches to value. The value in illustrating this plurality of approaches to value, is in exposing the variety of ‘political possibilities for either reproducing or contesting the value assumptions driving material practices’ (Lake, 2023). Similarly for Rogers and McAuliffe (2023) the point is not about the way various things, in their case housing, is valued, but the politics of difference between regimes of value and how they are asserted and reproduced through urban processes. Our intention here is to consider several theories of value that are made real through the constellation of economic, institutional and financial frameworks that regulate the urban process and define particular regimes of value, in our case, determined by the land use planning system. We do not seek to advance a particular theory or value or expose and advocate for new conceptions of value, but to focus on the movement – switching – between different regimes of value as the source of value uplift.

Our use of the term ‘regime’, draws from regulation theory literature which refers to regimes of accumulation to describe a broad set of governing logics or ‘institutional forms and practices’ (Tickell and Peck, 1995: 360) that regulate how the wider economy operates. This is distinct from regime theory, and indeed the sociological use of the term within discussions on regimes of value, which centres the analysis on constellations of actors and interests that coalesce to actively shape the urban process or assert particular claims over what constitutes value (Lake, 2023; Rogers and McAuliffe, 2023). As such, we seek to emphasise the governing practices and the economic, institutional, and financial logics as regimes that underpin the particular drivers that constitute value in land. What follows, then, are four intersecting regimes of how land value may operate or be understood. which help inform our conceptualisation of value switching as an integral and defining component of urban development processes in the compact, financialised city.

Land value as rent

Land rent is one of the most well-trodden debates within political economy not least of which because of the recognition of the centrality that land plays in the whole system of extraction and production (Collins, 2022). Land is literally the foundation upon which the capitalist economy is built. It is also a contested concept precisely because of its connection to the processes of production and exchange. In simple terms, rent can be understood as ‘simply a payment made to landlords for the right to use land and its appurtenances (resources embedded within it, the buildings place upon it and so on)’ (Harvey, 1982: 330). Much discussion has been dedicated to understanding the different forms of rent (Swyngedouw, 2012: 311). Rental payments are not made to land, but to landlords, and ‘would be impossible without general commodity exchange, full monetization of the economy and all of the legal and juridical trappings of private property in land’ (Harvey, 1982: 331).

As such, rent is positioned in relation to the social relations of production and exchange, be it for agriculture or some other commodity. In this way there is a connection established between rent and claims by the landowners on at least part of surplus labour value generated through production. This is most obvious in the case of agricultural land where fertility increases yield and profitability allowing for a greater claim for increased rent. Similar logics can be exhibited in the urban context where more intense uses, be it for industrial or commercial purposes, command greater rents. The value of land then, takes on an inherent relationship to the value of rent that can be extracted – it is related to a given multiple of the annual rental stream. In the case of land used for institutional rental development such as Build-To-Rent, the number or size of dwellings together with the locational advantages in relation to the wider city become the key measures of rent. It is this connection to surplus labour value that gives rise to understanding land value in broader terms: the capacity to command rental payments of greater and lesser amounts underpin ideas of value or worth of the land itself.

Land value as a commodity

Since the rights to land and monopoly to command rent are tradable, land use can also be understood in relation to its status as a commodity. Drawing upon Marx, Harvey (1982: 1) describes a commodity as a ‘material embodiment of use value, exchange value and value’ (p. 1). He notes that once defined, these three ideas of value, have tended to be used as fixed terms within western inquiry. Harvey questions this rigidity suggesting that ‘exchange value and value are relational categories, and neither of them can be treated as a fixed and immutable building block’ (Harvey, 1982: 4). In other words, this categorising of values becomes embedded in historical analysis and ‘to discover the various uses of things’, is ‘the work of history’ rather than of political economy’. It therefore follows that use values fall ‘within the realm of political economy as soon as it becomes modified by the modern relations of productions, or as it, in turn, intervenes to modify them’. (Harvey, 1982: 7). Exchange and use values, are therefore not fixed categories, but are both the subject of social historical context and to be understood in relational terms within economic systems.

Land can, and is, exchanged on the basis of its use values, and by extension, that exchange value is often based on rent that can be commanded for its use. In so far as rent represents either a connection to surplus labour value connected to systems of production or the inherent qualities of the land itself, tied to its productive capacity, then exchange values come to embody these relationships. In each case, in order to realise those values, human labour becomes a necessary component, either through producing goods or extraction from the land. There is no perfect overlap between use and exchange values, and as per the argument put forward in this article, use values can, and usually do, encompass what Harvey describes as ‘the work of history’. In this sense, there is a degree of arbitrariness that is attached to land as a commodity. Furthermore, land also occupies a special place in this discussion because the land itself ‘is not the product of labour’ and ‘the purchase of land “merely secures for the buyer a claim to receive annual rent”’ (Harvey, 1982: 347)

In applying this to land, this is instructive from two points of view. First, both exchange and use values in relation to land are a construct of the social and economic context. Land value in relation to the system of production is driven by a variety of decisions about the economy and how it functions and is not intrinsic to the land itself. Even locational factors that may give advantage to one piece of land over another and so translate into a higher value are also a construct of the urban and planning environment and the decision processes that have led to resultant urban structure and form. While these changes are incremental and slow, decisions to reshape the urban environment through spatial planning ambition can also reshape the land exchange and use value propositions.

Second, the commodity status of land is not fixed, but rather assigned. This echoes wider scholarship on the commodification of ‘natural’ resources which argues that land, water and other natures can be commodified in a variety of ways (Castree, 2003). Importantly, the commodity status of land points towards a different, or at least another, value layer altogether. If we can broadly conceive of rent as a kind of use value payment and understand land as a financial asset, this points towards its exchange value, the final category of value itself. While Harvey is pointing towards a historical conception of value, it alerts us to a much more contingent, and arguably assigned, value of land as a commodity.

Land value as a financial asset

The above discussion centres on notions of value connected to theories of surplus labour value whereby land values become tied to the productive capacities embodied in the use of that land. Ownership therefore is predicated on its productive use whether that be for housing, agriculture, manufacturing or whatever it may be. However, as many have noted, land is increasingly treated as a financial asset in its own right (Christophers, 2010: 97). This implies different expectations about desirable yields in relation to exchange value, and while this does not necessarily disrupt the notion of rent and how that might be established, it does suggest a certain fiction in the relationship to rent based on expectation and wider conditions in the economy. For example, if one investor chooses to accept a lower rate of return, then the value of the property goes up because the rent payments translate into a higher overall value rather like government bonds. What is determined an acceptable rate of return is itself a highly flexible concept dependent on interest rates, returns through other investment channels, and levels of accepted risk.

What is critical then is there is much less emphasis on the land itself and relationship to its use value for production (in the case of industrial owners) or as its use value as a consumption good (in the case of homeowners). In contrast, the primary concern for owners of land as a financialised asset is how much return it generates (either as rent or capital gains) and the relationship to the cost of money in the form of finance. In this way, leverage – the ability to raise finance against the expected future cash flow generated by the ownership of land – becomes a central consideration. This concept is largely dependent on an idea of the financial return for the use of that land.

What this doesn’t entirely consider is how values are arrived at where the connection to rent is limited or non-existent. Land can of course be traded and treated financially independent of rent yield. This may occur where the current value of a parcel of land reflects a capitalisation of expected future value that might be extracted from that parcel which in turn are largely contingent on the volume of capital flows into real estate. This in essence was the process Weber (2015) describes in relation to investment in commercial real estate in Chicago and is fundamentally how housing operates in Australia and elsewhere. In Weber’s example and those we explore below, this conception of value becomes unhinged from the productive process itself, and therefore from surplus labour conceptions of value. This can be contrasted with real estate investment trusts in commercial real estate which is based on returns that can be generated via rents. Banks, in loaning against land, can and do chose particular regimes of value they preference in handing out finance tied to the predominant way property submarkets operate in a given context. Alternate regimes of value can and do become embodied within the financial system in so far as banks become complicit in preferencing particular methods over others. Residual valuation methods, for example, which are commonly used across the development space (Crosby and Henneberry, 2016; Murphy, 2020) are routinely used as the value proposition which is then leveraged as part of the case for obtaining development finance. Land thus can be treated as a financial asset in a variety of ways and is not contingent on recognising rent or, indeed, expected future capital value.

Land value as fictitious capital

In drawing together a number of threads from the above discussion, land value can also embody a fiction where valuation of the land is based on some projected or imaginary future condition disconnected from the production process. Christophers (2018a) describes fictitious value as a claim on future real value, with the fiction in two senses. First, that it does not embody real value, that it is disconnected from production and surplus labour value, and second that it has not yet happened. Harvey also makes this connection, noting that ‘like all such forms of fictitious capital, what is being traded is a claim on future revenues, which means a claim on future profits’ (Harvey, 1982: 347). In both cases, it is noted that what is being traded is some claim to future profits, rather than any profits received today. The future profit or value argument is tied to rent linked to surplus labour value, and while we are not disputing this may be the case under certain conditions, our wider claim is that it is not necessarily always the case.

A claim on fictitious future profits need not necessarily be linked to a claim on future rent or future surplus labour value. Weber’s (2015) work provides insight into other future imaginaries that are not tied to rent but tied to expected sales values. In her Chicago case study, Weber notes that development of commercial office buildings ‘. . . were financed by investors speculating on future sales prices, prices inflated by the use of derivatives and other complex financial instruments’ Weber (2015: 3). In this context, future rent was far from guaranteed with very high vacancy rates across this type of property, and what investors were speculating on was rising asset values, not future rent.

Christophers (2016) has previously critiqued the very idea the land could be conceived as fictitious and posits the land is no less real than any other form of commodity or capital. We do not contest this central claim, however, this does not fully address the process through which land is implicated in the process of production, consumption and exchange in the first instance and the different sets of values or relations it can embody. That is to say, as noted above, land can be commodified in a variety of ways and are not intrinsic to land itself but are assigned through the process of marketisation and exchange. Our claim is partly that before land is drawn into these processes, the values ascribed to land may exist in fiction, and linking this to the broader claim around value switching is to suggest that there is a certain amount of effort that goes into the convincing markets that the value attached to any piece of land at a given time embodies one set of relationships as opposed to another. In linking to our wider thesis around value switching, the ‘switching’ in effect moves from one set of values that have been assigned to a parcel of land with another set of values. As we argue, the fictitious claim about the dominance of one regime of value as against another, becomes real through the process of exchange.

Being fictitious however, requires mechanisms to underpin and maintain that fiction. Murphy (2020) exposes this concretely in relation to residual valuation methods noting that value was being assigned through the performativity of developer/speculators and reflect the embodied wider, and often asymmetrical, power relations between actors in the market process. The residual land valuation method is a ‘calculative practice’ employed by developers to ‘make the market’ and embed particular claims and ideas about what constitutes value in the urban development space. Similarly, Crosby and Henneberry (2016: 1434) argue that property valuation methods themselves impact development outcomes due to their performative qualities – they are not simply ‘passive tools of active agents’ – and result in a tendency towards funding and delivery of homogeneous products (e.g. the ‘2-bed investor product’ beloved of apartment developers) concentrate in certain locations. Importantly, Murphy (2020) assigns agency to these feasibility models, recognising that they actively set the starting point of any planning decision in relation to future potential development. Given their pre-eminent application in the development sector, residual land valuation methods essentially determine whether any development takes place or not. In this sense they are pivotal in giving weight to Stein’s (2019) critique of planning as being driven by ensuring financial viability, not maintaining public benefit.

This understanding of how land derives its value from this perspective diverges fundamentally from that of ‘classical’ rent theory which sees land value, in the form of capitalised ground rents, as a product of that part of surplus value generated by the labour process during the production process (e.g. the construction of new dwellings). Instead, land value becomes a derivative of the value of the sale of vacant apartments to home buyers once the costs of construction, including builders profit, is deducted. These sales values have no necessary relation to the costs of building the apartments or indeed, or to any possible rental income that might be charged for the apartments in the future. What the land parcel is valued at and whether the gap between its current and potential valuation is small or large depends, on one hand, the state of the apartment market at the time and, on the other, the conditions under which the developer is able to obtain their finance, their equity stake and the business model and risk assessment. It may be useful in this context to see the development process as embodying two distinctive components–the ‘builder’ and the ‘developer’, whereby the former extracts value from the labour process while the latter extracts value from the speculative land re-valuation process.

For developers, therefore, the feasibility assessment and the residual land value it generates is the key trigger that determines whether they offer to purchase the land and subsequently submit a development application for change of (more profitable) use. As one Sydney developer told us during our research ‘You make your money when you buy the land’, not when you have actually built the apartments. The residual value of the land in this case is therefore a function of the prevailing regime of value for apartment development which determines the exchange value of a parcel of land a developer is willing to pay for its potential redevelopment. Value is fictitious in the sense that it relies upon some imagined future condition to give rise to its present value. That fiction encapsulates future potential for development, the future condition of exchange value, the future condition of housing markets and so on.

Building upon the above discussion, there are different regimes of value that can operate in respect of land, and that they are neither absolute or discrete, but overlapping and relational. What is of interest here is not whether any one way of value is correct, but rather, how different regimes of value can be relevant at different moments in time. Harvey similarly suggested that ‘The goal is to find out exactly how value is put upon things, processes, and even human beings, under the social conditions prevailing within a dominantly capitalist mode of production’ (Harvey, 1982: 38), and we would also add, how we may switch between them. In other words, our focus of enquiry hones in on how we switch from one regime of value to another, what are the determinants of different regimes of value, and what are the implications for this switch. In the next section, we bring these ideas to bare on a discussion of the process of the urban development process. In so doing, we argue that value switching is a key mechanism by which profit – as the realisation of value in capitalist economies – is extract from urban space.

Value switching and urban development

Land values are only partially about the inherent qualities of a parcel of land such as location or aspect. The intensity of development as well as the function of the development on a parcel of land adds further components to the value proposition, over and above these basic intrinsic physical qualities. The higher the concentration of activities on a parcel of land, the greater its potential value. This is the predominant view of value in the contemporary urban landscape and the central idea that supposedly underpins the incentive for developers to develop more housing at ever greater densities. This proposition underpins Smith’s (1979) ‘rent gap’ thesis, arguing that the difference between current and future ‘rent’ potential was what drove urban redevelopment. In essence, this may be seen as a restatement, albeit from a very different theoretical base, of the notion of ‘highest and best use’ thesis. In areas with existing housing, this effectively means that the future development potential needs to be at a scale that makes it worthwhile to demolish and rebuild. In the current context, this usually means at higher dwelling densities. But as we contend below, this only partially accounts for what is happening in Sydney’s property market, where speculation on land value change is a significant component of modus operandi.

Exploring changing tenure and ownership relationships in the higher density flat market in London in the 1970s, Hamnett and Randolph (1986) noted that the impetus for profit, and therefore urban change, was driven by a gap in the value proposition which resulted from the transfer of the apartments from one tenure to another. The change from institutional ownership of a rental flat (similar to Build-to-Rent or Multifamily rental buildings) where the apartment building derived a value based on a multiple of its annual rental return, to fragmented ownership of the building by sale to individual long-leaseholders which derived a value in the owner occupier market completely divorced from any potential rental payment, was enough to unlock a ‘value gap’. It was this gap in property value and the capacity to profit from it that that triggered the change in tenure. This was a highly mediated process. By buying the flats at their investment value and selling them with vacant possession to long leaseholders (often with mortgages provided by the developer) – that is, ‘switching’ from one regime of value to another–a substantial uplift could be generated. Other than superficial upgrading, the buildings themselves remained the same. Only the regime of value determined in these two very different housing tenure markets, and the capital values they generated, changed.

The ‘rent’ and ‘value’ gap notions are not incompatible, but neither are they the same. Smith is drawing on traditional notions of rent prevalent in commercial and institutional property markets as the fundamental concept in determining land value, while Hamnett and Randolph incorporate value as being derived from a set of property relations related to differing housing tenures. The key moment for both, however, is the transfer of the land and/or property from one ‘regime of value’ based on one set of regulatory, financial and legal relations to another.

At this point it is necessary to acknowledge that the price a commodity is exchanged for is not the same as value, but in the moment of exchange they become interchangeable. Harvey (2020: 108) in making this distinction describes value as an ‘immaterial but objective social relation which arises out of the monetization of acts of exchange’. In other words, these social relations that come to define particular regimes of value or value logics, are solidified and made real in that moment of exchange through price. It is at this moment that value and profit can be extracted from the urban process.

Changing the ‘regime of value’: The planning nexus

Moving forward to the contemporary context, it is well recognised that land zoning regimes play a critical role in setting the value framework for urban development. Harvey (1974: 243) has previously noted the critical role regulation plays in the nexus between speculator-developers and zoning regulations, noting that ‘without a certain minimum of governmental regulation and institutional support, however, the speculator-developer could not perform the vital function of promoter, coordinator and stabiliser of land-use change’. Christophers (2020) suggests securing zoning changes is a key game play of the land rentier and while we contend that zoning regulation is central, we argue that this is intrinsically not about extracting a value based on capitalised annual rental income, but rather shifting from one regime of land value to another that is, in essence independent of a rent argument. Of course, there are all kinds of ways that the planning and regulatory system can both accentuate (e.g. actively promote spot rezoning), capture (i.e. value capture) or undermine (control of land markets and setting land prices) these value gains. This merely points out that planning systems are necessarily complicit in value judgements with respect of land and become key tools in enabling value switching to occur. Planning regimes and zoning are one part of a wider ‘unruly web of politicized and marketized relationships’ (Weber, 2002: 537) that shape or create value in the built environment. The critical question arises as to how value is assigned and switched, and how this is implicated in the urban development process. A triptych of short case studies below illustrate how the creation, capture and manipulation of the assigned value in land resulting from the land use planning process has become a primary trigger for change.

Harvey (2020: 108)To offer some context to our case studies, it is worth noting the scale and significance of change in Sydney’s residential apartment market over the past two decades. The shift to apartment development over the past two decades in Sydney has been nothing short of revolutionary. Like other Australian cities, single family dwellings had been the dominant form of supply for much of the 20th century, yet since the 1990s, most new development has been delivered through renewal and regeneration in existing built-up areas, and a commensurate shift towards medium and high density provision in the form of apartments. While apartments remained unchanged at 13% of the overall stock across Australia, in Sydney, this share increased from 22% to 28% between 1996 and 2016 (Australian Bureau of Statistics (ABS), 2006, 2016). The largest portion of the growth has come in the form of apartments in buildings of 4 or more stories which grew by 114% in over this period. Much of this growth has been investor-driven, supported by generous tax concessions introduced in the late 1990s and early 2000s, and by a planning system that increasingly emphasises housing delivery in purely quantitative terms (Troy et al., 2020).

Change in total residential apartments, Australia and Sydney, 1996–2021.

Data source: ABS Census (1996, 2021).

Underlying this trend is the change in prices over the past two decades with Sydney median apartment prices more than doubling during this period, with the Sydney median dwelling price increasing by 25% in 2021 alone (Janda and Pupazzoni, 2022). This price rise drove increasing development approvals for apartments as developers and speculators sought to capitalise on rising values, with a close alignment between price increases and approvals (Gurran and Phibbs, 2016; Ley, 2023). However, one observation that is striking about multi-unit development is there are large numbers of development approvals that are never commenced or completed, unlike detached housing. Time lags in development make it hard to estimate a precise figure, but over the time period of interest there is about a 20% gap between approvals and completions (Troy et al., 2020). There are many reasons this may occur, but part of our argument here is that this points towards both an underlying motivation for, and temporality to, seeking out approvals and development that relate to different regimes of value that frame land economies in the financialised city. Once achieved, land with development approval can be traded at a value that reflects this permitted future use without any physical activity being undertaken. Second, there is often activity in land transactions even prior to approval, driven by speculative decisions around strategic planning, infrastructure investment and rezoning, representing an assessment of the ‘hope value’ a future planning approval will activate. As the following examples will show, value can be extracted before any physical transformations have occurred providing real world examples of ‘fictitious’ capital extraction.

The impact of land use planning on value uplift: Up-zoning

In this section, three vignettes capturing a range of contexts and markets are presented. Figure 1 shows the location of each of the example sites across the Sydney metropolitan region. Historical property sale transaction data from the Valuer General of NSW dating back to 1990, were used to establish verify accounts of the three examples listed below.

Location of examples within the Sydney urban region.

Example 1: Randwick

Our first case is a large piece of land located in an inner suburban location. The land was previously used as horse stables for racehorses, is adjacent to one of Sydney’s major universities, a major hospital, a popular ocean beach, and is surrounded by existing residential development. The property had been held by a well know horse racing family for decades. The whole package of adjacent land lots were sold in 2015 to a large superannuation company 1 month after a development approval for rezoning to high density residential land use was secured for the site for 750 dwellings, with the sale price recorded as A$290 million. Most of the site was acquired well before 1990, which are the earliest sale records available, meaning that the original land value would have been relatively negligible in today’s terms. There were no doubt various taxes and charges on this transaction, however, these would be insignificant relative to the crude profit margin on this transaction, which total A$284 million.

A pivotal moment in this transaction was securing development approval for 750 apartments on a site that had been used for a previously non-residential use, in this case, horse stabling. This guaranteed any prospective owner the right to redevelopment for residential use, though materially the site was only suitable for horse stabling at that point with a valuation that would have reflected that use. The development approval was sought by the former landowners and was ultimately supported by local and state governments due to it having strategic merit in the local planning context, which triggered the upzoning.

Example 2: Ashmore estate in Erskineville

The second example is part of large light industrial area in an inner-city suburb of Erskineville. The area had a long previous history of industrial activity and the specific lots in this example had a number of warehouses occupied by various companies with large space requirements, such as long-term storage and clothing wholesalers. The lots were owned by a well-known Sydney based industrial landowner who operate similar precincts across the region. This group purchased the two land parcels in 2011 for approximately A$83 million, and later sold the northern lot to a development company for A$260 million in 2016 and the southern lot for A$120 million in 2017 for a combined total of A$380 million. The crude profit margin on these transactions is about A$300 million or 360% over a 7-year period.

This catalyst for the sale was a strategic planning process led by the City of Sydney that identified the wider area – called the Ashmore Precinct – for future residential development. The area is part of a highly gentrified suburb and a few hundred metres from a train station two stops from Sydney’s central station. The planning arguments in support of a rezoning are robust and not in contention here. The strategic process was in this case driven by government rather than the landowner but ultimately conferred large benefit to the landowners. The land was transacted without any physical transformation occurring on the site, and indeed part of the site is still operating as a light industrial warehousing while the residential development is delivered in stages.

Example 3: Lewisham

Our final example captures more speculative activity and involves a relatively small older industrial site in the inner west suburb called Lewisham. The site was purchased in 2005 for A$8.5 million as industrially zoned land and sold again in 2012 with an outline development approval for higher density residential (an ‘in principle’ approval, that requires further detailed applications to be made) for A$48.5 million (an increase of 471% over a 7-year period). A development of 298 apartments was subsequently completed on the site by the new owner. The site itself had some strategic merit being located near an existing train station and a newly opened light rail stop, but the rezoning process was instigated and driven by the developer landowner who made the first purchase before on-selling the site with planning consent. At the point of the second transaction, there had been no change to physical structures or practical use of the land and buildings.

All three of these sites experienced a large uplift in value, and it was the sites themselves – rather than production or consumption tied to those sites – that experienced that uplift. No labour, bar the effort and risk associated with gaining planning permission, has been deployed to fundamentally alter their value, but rather traded on the basis of a ‘fictitious value’ related to their approved change of use before any shovels had broken ground. The planning system, often supplemented by public infrastructure investment, provides the trigger for a change to the prevailing regime of value of these sites. The redevelopment seen in Randwick benefitted from its proximity to major government institutions and new transport infrastructure; the impetus for residential densification in the Ashmore estate Example 2 was a government-driven planning process that rezoned a much larger area, and our Lewisham example was able to leverage the planning system in a speculative play on rezoning for development associated with proximity to existing and new transport infrastructure.

The impact of strategic planning policy on value uplift: Transit-oriented development

While our examples above capture value switching generated by a point-in-time planning decision (development approval), the switch can also be seen to take place in more systematic ways over an extended timescale though broader strategic planning decision-making. Prominent among these has been the shift in strategic planning policy to promote development more closely aligned to transport infrastructure (Curtis et al., 2009). Reflecting this, a key shift in Sydney’s strategic planning policy to favour transport nodes followed the change in the NSW Government in 2010 (Bunker et al., 2017; Crommelin et al., 2017). The policy shift of the incoming government not only gave renewed emphasis on public transport within strategic planning frameworks but linked these nodes very concretely to their ambitions around housing supply and housing targets, reinforced through a variety of planning strategies and infrastructure plans (Bunker et al., 2017; Crommelin et al., 2017). Whether coincidental or not, this moment in time also marked the beginning of a housing price acceleration following the Global Financial Crisis which significantly underpinned the development boom that continued for much of the following decade.

To assess the impact of this policy shift on land prices, the property sale database for Sydney was interrogated to generate a list of repeat land sales across the same property over a 19-year period, from 2001 to 2019. Only transactions above A$3 million for land sales that were zoned for residential use were included in the analysis and any properties that had been developed into apartments have also been excluded. As such, the following analysis shows only land sales where the underlying land title (either Torrens or Strata) was unchanged. With some exceptions, sales relating to almost all existing dwellings have been excluded by limiting sales to those only above A$3 million. 1 Importantly, while it is possible that some improvements to the land were made prior to sale, no additional dwellings were created as this would have generated a new land title through some form of horizontal or vertical subdivision and thus have been excluded from the analysis.

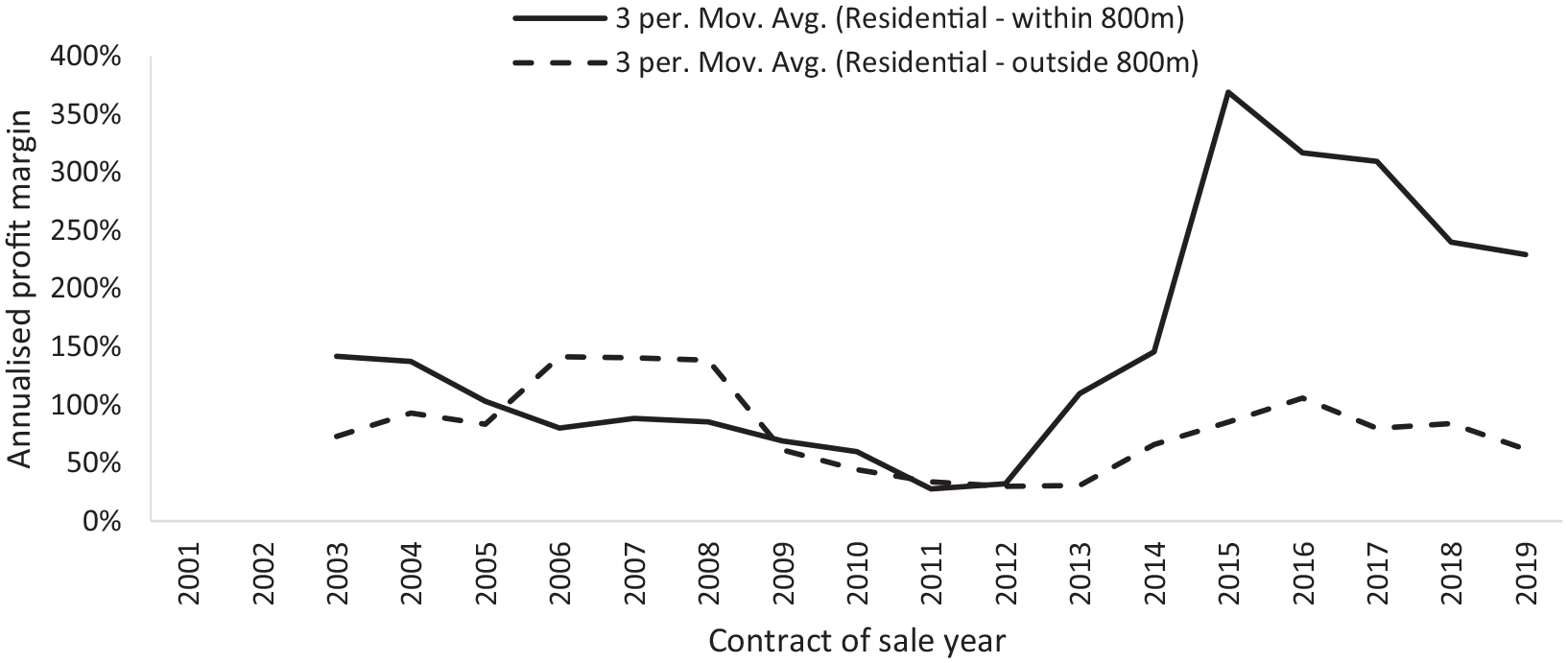

Our data set consists of 3980 non-strata sales transactions over the 2001 to 2019 period in the Greater Sydney region (which includes the Central Coast to the north of Sydney) on residential zoned land which had sold for over A$3 million for which repeat sales could be matched. Only the two most recent sales points were included in the analysis, resulting in 1990 paired data points. For these matched sales pairs, annualised profit margins were imputed based on these two sales, and classified into the two zones for analysis. The resulting annualised uplift data were plotted in relation to the 202 train and metro stations in the region using 800-metre buffers to located properties within and outside station precincts Figure 2 shows the three-period moving average of value uplift over time for the two zones. While annualised values were generally falling during the 2000s for sales zoned within the 800-metre zones, there was a noticeable change in relationship around 2011, which marked the point at which the new government’s policies began to gain traction and the apartment boom began to accelerate. Values escalated rapidly for sales within the 800-metre zones with annualised increases peaking at around 350% by 2015, indicating mounting competition for sites. Thereafter value increases started to subside as the apartment boom (which peaked in 2016/17) started to ease. In contrast, value increases for sales outside the station zones remained generally subdued during this period. This would suggest, land transactions within station buffer zones were subject to much greater price escalation following the policy shift. These results can be taken as confirmation of how successful transport focused planning policy had become during the post-GFC period. They also indicate how much additional value was generated through this policy to the benefit of landowners within the buffer zones.

Annualised profit margin for property within and outside 800 metres of a train station for latest two transactions between 2001 and 2019.

Concluding discussion

Each of the three vignettes and the analysis of the role of increased planning policy focus on transport infrastructure, highlight the complex relationships that configure notions of value in urban land. They all indicate that values vary considerably and are often independent of the physical manifestation of the land in question. The vignettes articulate a value regime that embodies an expectation of future speculative capital gains as the basis for establishing exchange value, often replacing a regime contingent on future expectations of rent linked to their prior uses as non-residential property. Land as fictitious capital relies on valuation methods that are used commonly across the urban residential development space, which in effect project forward to some imagined future use and are contingent on the guarantee of some end or future state of the land via the planning process. The central value proposition is a promise or expectation of a future use. In these cases, this future use – as higher density residential – had a legal foundation instigated through the planning process, or was bought on the speculative expectation that a push for rezoning would be successful. What is crucial here is that it reveals a certain kind of fiction in the creation of value, in that it can change through the decision processes of public institutions, coupled with the confidence of certain actors to seek out those decisions. In this way, the land value becomes a form of fictitious capital, and can only be sustained so long as each actor is complicit in maintaining the fiction that, for example, future dwellings can be built and sold and likewise, that governments and the legal system maintain a surety that they will support the construction of these dwellings. These fictions are made concrete by an economic, political and legal system that provides these guarantees.

The regimes of value pertaining to our three vignettes were altered through a value switching process enabled through decisions within the spatial planning system, in combination with expectations about future capital investment into residential property markets. The focus here is not whether one regime of value is more appropriate or correct than another, but rather to make three points about land value in relation to urban processes.

First, it illustrates the values are conceived, understood and realised in a variety of ways, and made concrete through a system of exchange. We are careful here not to suggest that values are produced in the sense that they make a contribution to surplus or productive value, but rather certain values are realised and extracted through the process of exchange. They are produced in the sense that they are monetized at that the point of exchange, and they are produced through the assigning of a regime of value in conjunction with the economic and legal frameworks together with wider processes of capital accumulation at particular moments in time.

Second, moments of value switching, from one regime of value to another, are the key movement that enables significant profit to be extracted from the urban process. In the vignettes presented, there was a switch from a value representing a redundant or existing land use to one based on capitalisation of expected capital growth of an, as yet, fictitious future development. This switch is to some extent abstract, but made concrete, as noted above, through exchange, and so at that point became the real foundation of a system of value in residential property markets. This is an important point for wider debates on financialisation of housing and wider housing system affordability crises that are evident in cities globally. While it may be the case that monopolising ground rent of housing in many cities is part of the urban housing crisis, it is by no means universal and lacks explanatory power for many contexts, particularly in relation to the development of new housing.

Third, interrogating the conceptualisation of land value helps us further unpack capitalist urbanisation processes. Understanding the different regimes of value that may apply across urban contexts, is important to understand the motivations for engaging in the development process broadly. For the developer, profit is derived not from extracting surplus labour value from the production process (this remains in the realm of the building process itself and is exploited by the builder who works under contract to the developer), or from realising a gap between current and future ‘rents’, but rather from securing the rights to more intense use of that land, whether they are realised or not. This speculative pressure drives the spatial outcomes in a city, which renders spatial planning ambition subservient to, and increasingly supportive of, the desires of speculative capital. This also means that for apartment development, the primary logic is not that of actually housing people, it is the speculative value in land assets that is shaping both how and where housing is actually delivered. More importantly, it underlies the polarisation of wealth outcomes where asset prices bare little relationship to waged labour of the wider population.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This research was supported by Australian Research Council discovery project funding (DP190102762).