Abstract

Across the social science and humanities disciplines, there has been an increased interest in questions of value and valuation. This article responds to the new emphasis by scrutinising the evolution of real estate valuation techniques over time, their embedded nature, and the implication of this for the (re)production of the built environment. This is achieved through the lens of two conceptual positions which are rarely used in the realm of real estate valuation. These are (a) path dependency which in this case charts the evolution of the discipline of valuation as it relates to retail related real estate assets; and (b) lock – in, which seeks to understand how valuation techniques and attitudes have become embedded during this evolution. This position sits alongside a series of investigatory interviews with professional valuers in international real estate organisations specialising in the commercial real estate market. This is often a missing voice in recent research into real estate and the wider subject of valuation. Findings suggest that valuation practice is reliant on confirmatory market practices that do not necessarily capture the contemporary affordability-based requirements of tenants. Instead, practice is locked into reinforcing the nature of zone-based market values for landlords and investors. The geographical implications of this situation at the micro-level can be vacant or poorly performing properties that undermine local areas in the interest of maintaining the headline value of properties in macro-level global capital markets. This new conceptual analysis provides understanding of how the physical built environment is developed and reproduced over time through notions of value, helps to connect often hidden practices of real estate valuation into existing academic debates in urban studies and geography, and in conclusion sheds some light on how practices of real estate valuation can be improved in the disrupted world of retail.

Introduction

The aim of this article is to engage with ideas and methods of valuation in contemporary society, specifically real estate valuation. The lens for this enquiry is the current challenge of valuing retail assets in England, within the context of severe disruption in the sector caused by changing consumer habits driven by the rise of e-commerce and the more recent difficulties caused by COVID-19 and inflationary pressures on consumers. While empirically centred in England, this focus is important because retail assets underpin the international financial sector. The International Property Forum (IPF) estimates the value of retail investment at the end of 2020 to be £271bn – in comparison the total office value is estimated at £263bn for the United Kingdom. The analysis in this article, therefore, has international significance as it provokes debate and sheds light on how valuation practices intertwine with global capital markets.

The retail asset class has historically been perceived as the most attractive of the traditional real estate sectors. This is because retail was situated in central locations that occupied buildings offering a long economic life with good tenants that would remain in occupation for lengthy periods of time (Jones, 2010). The significance of this research goes beyond the world of retail. Gilbertson and Preston (2005) describe the importance of real estate valuation, indicating that real estate underpins a major proportion of financial decisions and capital markets in international financial systems. In 2020, the Royal Institution of Chartered Surveyors (RICS) indicated that 70% of global wealth is held in land and real estate assets with much of financialised bank lending secured on these assets. It is therefore surprising that valuation techniques have not received more attention. Indeed, Gray (2021) argues, there is much social change around the built environment and there is a growing perception that real estate valuation is struggling to account for this situation.

The original interpretation of valuation techniques in this article also opens space for a broader intellectual discussion of how techniques and processes of valuation influence and shape the socio-built environment in which we live and work. The underlying research question that guides this article is: how do contemporary real estate valuation practices capture the new world of retail and what are the implications of these practices for the wider built environment?

While there have been some interpretations of value and valuation processes in select fields of academia. (Chiapello, 2014; Konings, 2015), at the time of writing the topic of real estate valuation is largely either passing underneath the scholarly radar, within the typically atheoretical technical practice of valuation (Amidu et al., 2019; Crosby and Henneberry, 2015; Pagourtzi et al., 2003; Tidwell and Gallimore, 2014) or obliquely via academic research considered here as critical real estate studies. Examples include research into Tax Increment Financing and calculative practices (Weber, 2010, 2020) municipal financialisation (Beswick and Penny, 2018), the mortgage market (Aalbers, 2012, 2016) the appropriation of public land (Christophers, 2018) the securitising of single-family assets (Fields, 2018) or historically, research into uneven development, gentrification, and displacement (Lees and Ferreri, 2016; Smith and Williams, 1986).

While much of this latter research deals with the impact of real estate practice on society, rarely does it consider the technical process of valuation that triggers and underpins these processes. Fields (2018) captures this situation when discussing the connected process of financialisation, arguing that it is often poorly understood and utilised as an all-encompassing explanation without any investigation into how the process of financialisation occurs. Indeed, much of this research views real estate practice as an uncontested negative that extracts value from individual locations or asset categories. It rarely delves into the black box of how these processes, underwritten by real estate valuation, occur or how they are undertaken.

By investigating today’s challenges of valuing retail assets, the article sheds new light on this situation by showing how processes of valuation underwrite specific decisions in the built environment and wider capital markets. The article examines how valuation techniques have evolved and become embedded in contemporary practice. The article pursues this agenda through a novel treatment of two conceptual positions which are rarely used together and never in the realm of real estate valuation. These are path dependency which charts the evolution of the discipline of retail asset valuation – Section ‘Conceptual framework’ is structured around the degrees of path dependence outlined by Liebowitz and Margolis (2014). This structure is then complimented by lock-in, to understand how valuation techniques and attitudes have become embedded during their evolution.

This perspective sits alongside a series of investigatory interviews with Valuers of real estate working for international real estate practices – the authors have recruited professionals who specialise in the practice of valuation and retail-based assets. These are professionals who are actively involved with retail markets and have knowledge of changing occupier needs but also wider valuation processes. This approach is significant because it sheds new light on how methods of valuation are struggling to make sense of the new world of consumer behaviour, and the impact on the use of real estate assets – most clearly seen through vacant buildings on the high street. While there are numerous numeric counts of vacant retail properties, econometric assessment of economic performance and policy response that seek to counteract vacant properties, there is little examination of how we arrive at persistently vacant properties. Further, this perspective allows for an exploration of the geographical reality of retail valuation practice and the continual reinforcement of the zone-based market value approach to retail valuation.

The next part of this article will explain the techniques of valuation practice, how they are applied to retail assets and how they are utilised to underpin the discussion in this article. This section argues that several facets of the system act as bulwarks against meaningful valuation of retail assets in contemporary times. Yet these methods underpin the continuing development of the built environment and related financial markets and economies. To understand the persistence of inertia in the valuation of retail assets, the article presents an alternative conceptual framework for understanding real estate valuation, introducing ideas of path dependence and lock-in to its practice. The methodology then follows, indicating the sample technique and decision-making process that was followed when approaching and selecting respondents. It then applies the conceptual framework to contemporary valuation techniques alongside interviews with valuers to reveal the current nexus of value, consumer, society, and the built environment. The underlying argument in this section is that valuation practice is reliant on confirmatory market practices that do not necessarily capture the contemporary affordability-based requirements of tenants, instead such practice is locked into reinforcing zone-based market values for landlords and investors. The geographical implications of this situation at the micro-level can be vacant or poorly performing properties that undermine local areas in favour of maintaining the headline value of properties in macro-level capital markets. The article then presents a conclusion, where the authors discuss the significance of the findings for academic debate and valuation practice.

Valuing retail-based real estate assets

The concept of value

To understand the process deployed in the valuation of retail assets it is important to fully recognise what value means in this context. Baum et al. (1997) suggest that ‘value’ is the amount of money which something is exchanged for in the open market. Further, Isaac and O’Leary (2012) state that real estate value is the capital or rental value which a valuer places on a real estate asset in advance of an exchange or debt agreement. It reflects what the valuer feels could be achieved if the asset were to be sold or leased. Value is essentially an amount a purchaser is willing to pay, and a vendor is willing to receive for an asset in the open market. Pagourtzi et al. (2003) go further and define value as clarifying the assumptions made in estimating the exchange price in the open market. Many assumptions are made within the valuation process, and these include variables such as legal interests, physical conditions of the building and more importantly market conditions. The RICS have standardised the term to provide consistency across the real estate profession. The meaning of value or ‘market value’ has been long established by the institution and is defined in IVS 104 paragraph 30.1 as: The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm’s length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion. (RICS, 2022)

Traditional real estate valuation processes

Establishing a value is ultimately determined by applying a valuation method. The traditional methods of real estate valuation were historically termed the ‘5 methods’, namely, the comparison method, the profit method, the residual method, the contractor’s method, and the investment method (Blackledge, 2017). More recently, they have been amended and consolidated into three approaches within the RICS Global Standards and are now known within the profession as the market, income, and cost approach (RICS, 2022). This article focuses on the market approach only as this is the method that is predominantly adopted to provide values for commercial income producing assets. In other words, a given real estate rent (the income derived from a tenant) within the marketplace (considered market rent) is calculated over a given period and then capitalised into a value using an all risks or investment yield (ARY) 1 Underlying this calculation is the need to make comparisons with a variety of real estate transactions within a location to arrive at a market view and consideration of relative risk (Pagourtzi et al., 2003; Shapiro, 2012).

Blackledge (2017) states that the market approach has become the simplest and most reliable method and it is not only employed by the profession but by everyone in everyday life as they look to buy or sell an asset. This view is supported by the RICS (2019) who claim that comparable evidence (in other words recent asset transactions) – the output of which is referred to in this article as ‘comparables’, is at the heart of every meaningful real estate valuation. In principle, comparable evidence, when used to value a target property, should be similar in terms of use, location, and characteristics and demonstrates the rental tone of a given area. An analysis of the data is then undertaken, and any adjustments made for differences between this evidence and the target property. Finally, an appropriate opinion on value is made whether that be via market rent and/or yield.

The appropriate data established from this approach are capitalised via the investment method to arrive at an opinion of market value. Pagourtzi et al. (2003) explain that the direct comparison is rarely appropriate for the investment method and therefore the comparison needs to be broken down further to consider both an opinion of rent and ARY. The focus on market rent in this article is significant for retail real estate as it allows the valuer to establish a rental tone (the level of value which becomes established through transactions) for an individual area. The tone determines the market rent which a tenant is contracted to pay for the occupation of the premises. The rental tone is important to the investor as it aids the maintenance of Market Value (and the underwriting of associated debt) – the main aim of investors in real estate.

Establishing retail rents through the market approach

As discussed in the previous section, rents have a direct correlation to investment value and historically this has been one of the drivers for stakeholders to increase investment values particularly in retail assets (Jones, 2010). The increase in rental value is usually justified through new open market transactions – in other words new lettings of similar properties agreed between parties. These form the comparable evidence, or market tone, to justify new market rents. The rental analysis of a retail unit is based on the concept of ‘zones’ – the valuable space is at the front of the premises nearest the entrance fronting the mall or high street. Historically, this made good business sense as retail frontages attracted consumers into the retail space. Blackledge (2017) suggests that the larger the shop display the more likely a potential customer is to venture into the shop. Therefore, the theory of ‘zoning’ means the shop floor reduces in value the further back the premises goes. In summary, valuers use comparable evidence, duly adjusted, to determine the market-based zoned rental tone (referred to within this article as rental tone) which then establishes the market rent. It is widely recognised by academic and professionals alike that this process (market approach) is not a statistical analysis but a heuristic approach (French, 2013) and that real estate valuation is a professional judgement (Amidu et al., 2019; Gallimore, 1996) rather than an exact science.

This judgement is demanded because of the heterogeneous nature of the real estate market, it’s imperfection, lack of a central marketplace and incomplete information which valuers analyse to provide values. While this interpretation betrays the myth that real estate valuation is an objective calculation, it also opens the opportunity for an interpretive enquiry. For example, Chiapello (2014) albeit within the realm of values in financialisation suggests that there is an element of secondary judgement in any valuation process.

The importance of retailing and changing markets

It is widely acknowledged that for several years retail businesses have come under increasing pressure to change the way they operate and use space. Consumer habits have changed significantly with the increase in e-commerce, heralding a shift from bricks and mortar retail business processes to ones characterised by bricks and clicks. To provide some context to the importance of retail investment in the UK, the IPF in their January 2022 report illustrated that the value of retail assets had fallen dramatically from £366 billion in 2017 to £271 billion in 2020 – a situation that has been further exacerbated by Covid and inflationary pressures.

The Centre for Retail Research (2022) claims that there is a retail crisis and that the sector has experienced 5 years of change in just 18 months, with 2020 recording 54 corporate retail failures and the closure of over 5200 stores across the UK. These figures do not include smaller independent retailers so the total number will certainly be higher. This situation has led to challenges around affordability, which has resulted in calls for rent reductions, more complex lease structures, changes in payment of rent and adaptation of retail properties into alternative use. Tenants are taking a pragmatic view on the affordability of units and showing scepticism towards market-based rental tones. They are concerned with business turnover generated from real estate and essentially whether they can afford to pay all outgoings associated with building occupation including rent, rates, service charge, and other costs. This has exerted pressure on landlords to restructure leases to increasingly take account of business turnover, rather than relying on a simple zone-based analysis of real estate value.

Yet the RICS Valuation Global Standards, and a great deal of professional practice, is continuing to use traditional valuation methods regardless. Today most retail asset valuations are still undertaken on the market approach where valuers consider rental tones and comparable evidence. Baum (2017) and Blackledge (2017) both agree that there is a reluctance in the profession to change. While the reasons for this are contested (arguments range from the methodological purity of retaining consistency in technique to landlords wishing to retain control over the division of their space), the central argument put forward by the authors is that there is widespread fear in the market in relation to the adoption of new valuation techniques. As Baum (2017) argues, there may be concern within the profession that core skills are outdated. However, he goes onto argue that more important is the potential for the alternative approach, based on turnover, to lead to a revision in traditional valuation processes that would make the market approach and zone-based rents redundant. Any alternative approach would lead to changes in market values and potential problems with debt agreements. The results of this situation can have negative consequences for the built environment and society. For example, landlords choosing to leave retail units vacant rather than reducing rents to attract new tenants. The remainder of this article examines this persistent behaviour further, particularly considering why valuation techniques do not readily adapt to the new circumstances set out in this article and instead become locked into previous modes of consistent production.

Methodology

This section of the article gives a summary of the method adopted and a short foreground to the conceptual framework that is deployed, namely path dependence (to understand how valuation practice has evolved over time) and theories of lock-in (to understand how valuation practice have become ingrained) to better understand valuation practice in the retail sector. Each element of the conceptual framework will then be addressed again in further detail in the subsequent applied sections.

The authors have undertaken a qualitative approach across a 12-month research project examining the practice of valuing retail properties in England and its impact on the built environment. Focus is entirely on private sector valuation professionals. In part, the originality of this research is giving these professionals a voice in the valuation debate. The authors consider that valuation professionals have meaningful insights into the process and challenge of valuing retail-based assets because they experience it daily in their profession. It is recognised that by not approaching valuers, and in general, investors, landlords, or financiers that we present a partial picture of the valuation profession in international academic debate.

The empirical material in this article is based on a two-stage research process, where the main private valuation practices in England were approached for interview, these included both international and national private practices (five in total). The sample appears low, however, it must be noted that the number of firms undertaking retail valuations has reduced over recent years with only larger private practices instructed on such assets in England. The same professionals were interviewed at both stages in the process, an improvised Delphi technique was used to gain consensus in viewpoint (Linstone and Turoff, 1975; Muldoon-Smith and Moreton, 2022). A conscious decision was taken to organically weave the participant content into the text to, where possible, create a narrative account of valuation practice to counter the relative silence given to professional valuers in this debate (Etherington, 2007; Hertz, 1997). The intent behind this approach is to bring to the surface the varying types of institutional language and attitudes that texture the valuation of retail real estate. Therefore, throughout the article, those taking part in the research are considered and referred to as research participants, rather than respondents, and all effort is made to give voice to their opinions.

The authors approached valuation practices directly, rather than via Freedom of Information Request to avoid the risk of legalistic and sanitised responses. Although a relatively modest response was gained, this methodological approach generated a unique sample of responses from experienced practitioners across a comprehensive geography. The valuers all worked within commercial real estate valuation throughout England with senior responsibility for valuation departments undertaking retail asset valuations. Due to the period when the research was undertaken, interviews have been conducted over a variety of mediums, including telephone and software-based communication platforms and when allowed face to face interviews. All findings were recorded, transcribed, and coded using a matrix. The analysis matrix was used to theme findings within an overall grounded theory (Glaser and Strauss, 1967) and constant comparative (Goertz and Le Compte, 1981) form of analysis and theory development. Upon request, practitioner identities and explicit location information have been redacted to protect participant identity (only general location information is revealed). This approach stimulated candid discussion in relation to valuation practice. Yet, on balance, we argue that our perspective provides an original counter-narrative to the current critical view of real estate often found in academia – one that often talks about value extraction without giving a voice to those involved in this process.

Conceptual framework

Path dependency originated from research conducted by Arthur (1989) and David (1985) into how early decisions affect technological pathways in the field of institutional economics. More recently, it has been expanded into fields including organisational studies by (Fortwengel and Keller, 2020), Sydow et al. (2009, 2010, 2012), Dobusch and Schubler (2013), Vergne and Durand (2010) physics and mathematics considered in association with chaos theory Gleick (1987), complexity (Waldrop, 1992) and historical contingency (Gould, 1989). Path dependency eventually leads to a situation of ‘lock-in’, where the historical evolution of a process or procedure means that people, society, business, and locations are through time locked into old practices and circumstances and in this situation no longer have access to better services to improve their situation (Henning et al., 2013). Grabher (1993) was one of the first to consider the transition from path dependency to ultimate lock-in with his work in the Ruhr Valley, integrating the field of path dependence and evolutionary economics into economic geography and regional development.

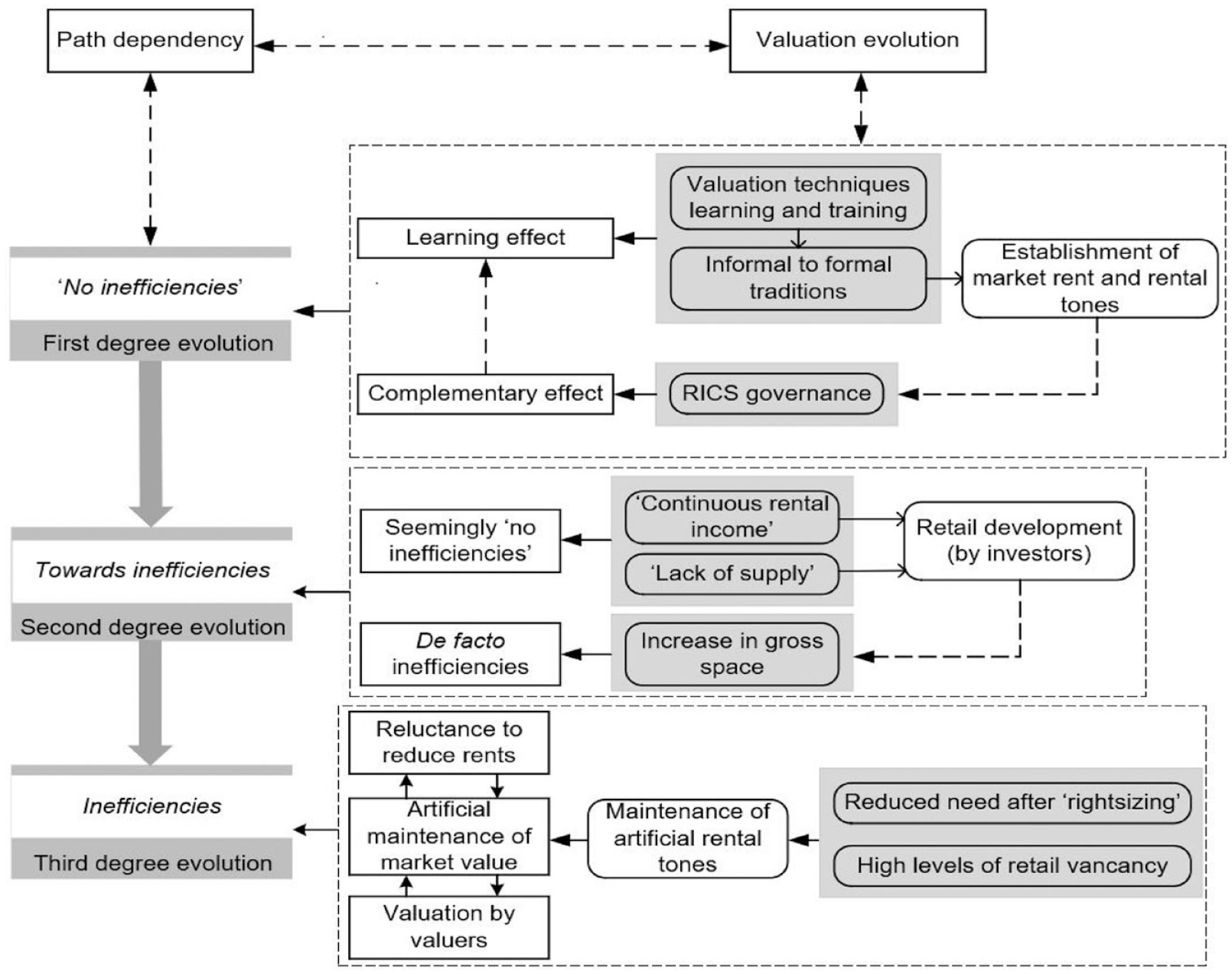

It can be argued that the practice of valuation is on a similar pathway, whereby the central techniques are considered in a rigid framework. To investigate this situation, the authors have adapted the work of Liebowitz and Margolis (2014). Although it is acknowledged that their research is relatively dated and that path dependence has since been explored in various domains, more recently in the realms of education development (Choi, 2022), politics, management (Garud et al., 2010), it is Liebowitz and Margolis (2014) early theory on the evolution of path dependence that provides a meaningful analogy with the practice of real estate valuation This is because it has provided a framework that has allowed the researchers to appreciate changes in the retail asset market alongside the valuation processes. Figure 1 and Section ‘First-degree evolution’ describes this situation.

Path dependency: the case of real estate valuation practices (Authors).

First-degree evolution

Liebowitz and Margolis (2014) argue that the first degree of evolution is a pathway of complete innocence, the path taken is considered the right one at the time with no inefficiencies. Under this position in the practice of valuation, the underlying method, its market assumptions, and decisions made are taken to be correct without critical appraisal. This situation can be further characterised by the work of Fortwengel and Keller (2020) who extend this concept with their consideration of ‘learning effects’ (the knowledge acquired through education and experience) and ‘complementary effects’ (the interplay of routine, rules, and governance).

In this case, a learning effect is a specific task or an operation which is performed often and repeatedly. The process becomes more efficient, reliable, and ingrained with each subsequent attempt. To illustrate this in terms of valuation, Vandell (2007) argues that eventually the processes and techniques of valuation are adapted, learnt, and handed down via informal traditions, and then through formal training with the establishment of associations. In addition to academic and institutional learning of the market approach to establish market rent and rental tones. The ‘complementary effect’, in this case, are the rules and dominance of the valuation procedures and guidance of the RICS which co-evolved with valuation techniques.

These two effects have led the way for further coordinated and adaptive processes where real estate stakeholders have become reliant on both methods and guidance within the global marketplace. This was certainly the case for the method of zoning and establishing rental tones through the traditional processes. Historically, it was beneficial to stakeholders and tenants as the value of the asset to both parties were the ‘attractiveness’ of the front of the shop. Of course, as consumer habits have changed, and tenants are no longer relying on footfall (rather relying on other mediums to attract consumer spending) their use and occupation of real estate has changed, and this renders zoning and rental tones obsolete.

In conclusion, we argue that first-degree evolution in this case characterises the adoption and establishment of the traditional valuation processes and complementary RICS governance. Over time, there has been very little critique of the valuation process, something that continues today even in the face of changing business productivity and empty retail units.

Second-degree evolution

Second degree path dependence, when applied to the evolution of real estate valuation, still assumes no inefficiencies in the method when carried out, although in hindsight inefficiencies are demonstrated. Historically, retail assets have been the attractive asset sector for investors and although there was a slight shift towards office accommodation in the 1980s retailing regained its position in the early 1990s. Jones (2010) argued that historically there were two key aspects that attracted investors to retail assets, rental income and continued rental growth (increasing rental tone) which was supported by the longevity of consumer spending. Second was the lack of supply in retailing locations due to urban limitations on development. This point illustrates the hegemonic market opinion in relation to retail assets, that retail will always be the best asset class with continued rental growth associated with limited supply of physical space but considerable demand.

However, in today’s market when we consider the amount of vacant retailing space and the problems associated with high streets and shopping centres some truth can be gleamed from Liebowitz and Margolis (2014) who suggested The inferiority of a chosen path is unknowable at the time of choice made, but later recognized that some alternative path would have yielded greater wealth. (p. 985)

As the retail market experiences a retraction in physical presence through the process of rightsizing, 2 the consequences can be clearly seen in the increase of high streets and shopping centres peppered with vacant and void units throughout both town and city centres in England including Newcastle, Gateshead MetroCentre, Sheffield Meadowhall, Trinity Square in Leeds to name a few.

As demonstrated above with the evolution into second degree path dependence, the problems surrounding retail values are not new, the disruptions to the market and consumer habits have been evolving and changing for some time. In hindsight the relaxation of the planning laws coupled with an increase in car usage in the early 1990s led to the development of new out of town retail centres. In addition, the high street experienced a decline of department stores as cities began to develop through the addition of new covered shopping malls. Despite this increase in retail space, market stakeholders continued to assume that market rental tones would increase into the future with little thought to the increase in supply and reduction in demand as retailers adapt and change their retailing format.

Third-degree evolution

Finally, Liebowitz and Margolis (2014) put forward what they called ‘third-degree’ path dependence, which explains past, present, and future events or conditions that effect and promote errors in practice (in this case the mispricing of retail assets) but recognise that the error was avoidable. They argue that persistent behaviour leads to an inefficient outcome, while recognising that a preferable outcome can be achieved, but a choice is made not to obtain it. It is this third-degree pathway that has most relevance to real estate valuation in the retail sector. It has been clearly demonstrated that there have been changes in occupier demand in the sector as businesses have strived to consider ways of adapting to the contemporary challenges – particularly through companies reducing their physical store footprint.

This process has led to an increase of vacant space in town and city centres. The expectation would be that an increase in vacant space would influence the downward tone of market rents (the case for which is set out in Section ‘Valuing retail-based real estate assets’). However, there is little appetite from investors and landlords to consider reducing rental tones to (a) reflect the increase of additional space on the market and (b) to reflect the reduced need of rightsizing rents. Instead, their main concern is retaining the high tones which defines the overall market value of their asset. This echoes the work of Levy and Schuck (2005) who consider the influence that clients have on value. They indicate that valuations are likely to retain biased estimates of market value. They argue that Clients have economic incentives to influence valuations in order to maximise asset-based fees or increase loan books. (Levy and Schuck, 2005: 185)

In this section, we have set out a framework that explains how the practice of valuation has evolved and been constrained over time, through various stages of path dependency. In the proceeding section, the authors develop this argument to explain how this inefficient behaviour becomes locked into practice, inhibiting improvement.

Conventional lock-in

Grabhers’ (1993) notion of lock-in, developed initially in the domain of regional development, shows how the lock-in of processes and close relationships (often agglomerating) between actors can at the beginning be beneficial but detrimental as economies and occupiers change and processes become outmoded and harmful to progress going forward. Grabher (1993) presents three types of traditional lock-in: functional; cognitive; and political. Functional lock-in refers to the hierarchical and close relationships that exist between actors or as Hassink (2011) suggests, enterprises. In this sense, we can observe that real estate valuations underpin financial decisions within the built environment and there are close relationships between the actors involved (e.g. investors, developers, financiers, and institutions). The close historical relationships between stakeholders result in a lack of research, development, and marketing as they are too heavily reliant on one another, self-perpetuating market values and a consequent lack of self or comparative critique. Second, cognitive lock-in refers to markets or ‘secular trends’. In this case, we can observe the practice of valuation developing an attitude or mindset that markets will continue moving in the same general ‘herd’ direction for the foreseeable future. An example of this is research into (and market adherence) to the idea of regular short-term real estate cycles (and subsequent shocks) which help to regulate markets over time alongside a longer-term belief that value will increase progressively in the long term (Ball et al., 2011; Barras, 2009). Reinforcing a belief that retail assets will, eventually, regain and maintain their value based on a zonal system and conventional lease structure.

The final form of lock-in, political, is concerned with organisations themselves or actors. The concept of political lock-in captures the institutional or network values of the organisation who wish to preserve existing traditions and processes and in doing so tamper with new development and creativity. The practice of valuation is overseen and regulated by the RICS. The organisation governs and regulates all the techniques, quality, and professionalism of the international real estate profession. The organisation is widely interlinked with other stakeholders across other professionals and is influenced by investors, banks (financiers), and institutions within the market. The RICS is in a very difficult position, charged on one hand with maintaining a meaningful valuation system but on the other pressured by major investors who want to maintain their asset value in global systems of capital, first to use as security to raise loans, and second to protect the share price of listed companies (Crosby and Henneberry, 2016). This highlights the underlying importance attached to the value of real estate assets and the close links to the economy, society, and the built environment.

Previously Fields (2018) and Berndt and Boeckler (2009) have argued that markets do not simply appear but are continually produced and constructed socially with the help of actors. These actors are interlinked in dense and extensive webs of social relations. In a different sense, we argue that webs of social actors (investors, developers, financiers, and institutions), all of whom have varying degrees of power, come together to prevent a new affordability-based market forming in the retail asset sector. Instead preserving market norms, credit systems and a false sense of value in capital markets – with the local outcome being vacant or poorly occupied properties.

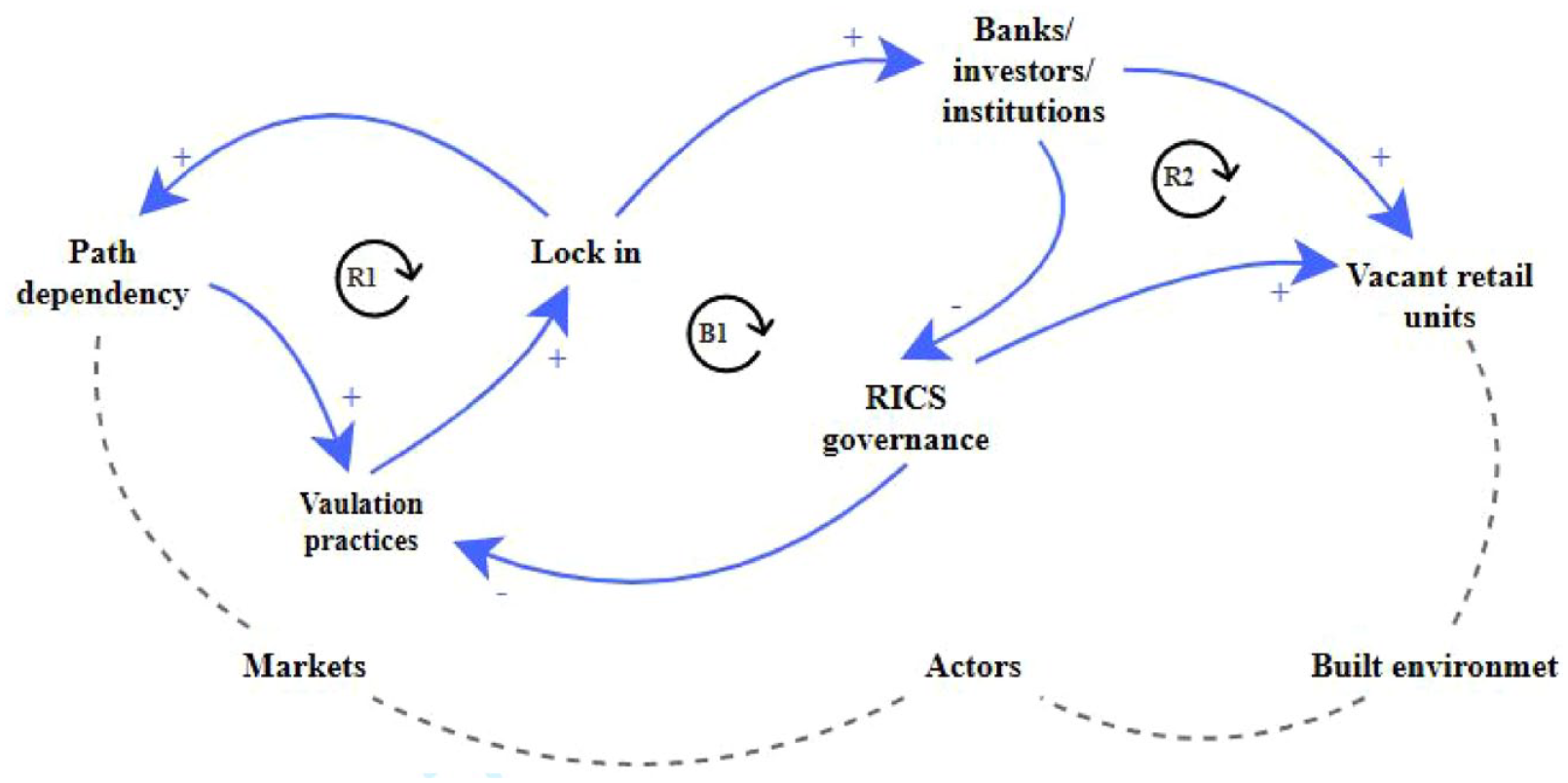

Figure 2, a causal loop diagram, describes the complex relationships that influence value, the connection between value and the built environment and wider society through capital flows. It helps to understand the links with other important aspects of the valuation process. The figure illustrates the reinforcing loop that encompasses path dependency (R1) and lock-in through the valuation processes. This is influenced by actors, specifically the RICS through governance, bankers, investors, and institutions which creates a balancing loop (B1) that depicts the interconnection between these actors based on valuation, markets, and the built environment. While R2 illustrates the lock in (R2) of vacant units influenced by the valuation practices and the actors. The loop demonstrates the positive and negative result of actions. In this article, the authors argue that specific actors (specifically institutions and investors) have more power and vested interest than others and have prohibited new market conventions forming, hence their dominance within the loop.

Interlinking sub-systems influencing value and infiltrating the build environment (Authors).

In partnership with research participants, the proceeding section takes forward this conceptual framework to investigate this situation further.

Results

Establishing the traditional valuation processes through first-degree evolution

The previous section sets out an argument that valuation professionals are becoming aware of the complexities that traditional valuation processes present, particularly the market approach. This process was established very early in real estate markets and has been used throughout valuation practice with no critical and/or adaptive view of the retail sector.

All participants in the research agreed that historically the retailing sector has always been perceived as the best-performing commercial sector. The group of participants considered their own early experiences in valuation practice. There was a consensus regarding training all suggesting that they ‘learnt’ the process of establishing rental tones and subsequently market rent through practice and discussion with experienced practitioners. The traditional processes established through the profession have been passed to further generations of practitioners hinting at Fortwengel and Keller’s (2020) ‘learning effect’ introduced in the previous section.

All participants interviewed agreed that their skill with the market approach had been passed to them by senior professionals while training as graduates. They themselves are now training their own graduates with the same procedures, skills, and knowledge: Although I was taught the principles of valuation techniques at university the real skill of valuation was learned once I was in practice. I learned from my boss who learned from his. (Director of valuation; International Surveying Practice) The skill of doing a valuation is learnt when in practice from experienced practitioners who have knowledge of the real estate markets and have undertaken valuations for a long time. (Partner of valuation; International Surveying Practice)

This evidence suggests the ‘learning effect’ has aided the development of traditional valuation processes throughout the market. Supporting the arguments of Fortwengel and Keller (2020) that the learning effect is a specific task performed repeatedly.

There is then evidence that Fortwengel and Keller’s (2020) ‘complementary effect’ has taken shape while the traditional market process has become embedded in practice. Participants agreed that this effect is observed in regulations and governance produced by the RICS. All participants agreed that the RICS involvement in governance has aided the development of valuation processes. However, the consensus from participants was that the RICS do not offer opinion or recommendations in relation to changes in techniques or processes.

One participant commented as follows: The RICS are keen to see changes in the way we value real estate although they are not willing to put forward advice other than quality procedure and best practice, they tend to leave the application of the methods to the professionals. (Director; International Surveying Practice)

Participants suggested that to some extent this was down to external influence on the RICS, they are aware that changes to processes would have huge implications for the headline values of real estate in global capital markets and by extension the wider economy. Echoing the compromised valuation levels in the sub-prime mortgage crisis in 2008. All participants agreed that systematic changes to retail-based valuation practice would send shockwaves through the valuation of real estate assets and the wider economy.

The evolution of the retail asset category

The participants interviewed remembered changes in planning laws which opened the way for the development of out-of-town shopping centres and retail parks. This development contributed an increase in retail floor space under different formats. In fact, an interesting comment from one participant suggested that the new formats (retail warehouses and out of town centres) became occupied by tenants already present within city centre locations who at the time wanted to increase their representation in different areas, offering consumers better parking facilities, easy access, and more product choice.

Most large retailers became represented in different formats throughout the retailing sector but still retained their city centre presence. (Partner of valuation; International Surveying Practice)

Unfortunately, during this time, the practice of retail valuation was not adapted to account for these new circumstances. This can be seen as the point of transition into the second degree of path dependency. Liebowitz and Margolis (2014) assume that there are no inefficiencies at first glance, although in hindsight inefficiencies are demonstrated.

Indeed, one participant commented that development of new retail warehouses and out of town shopping centres increased total retail floor space significantly. However, most participants agreed, this was not scrutinised when considering values and valuation processes at the time. Naively, city centre retailing was still considered to be the best assets class, while in theory, the increase in total floor space should have resulted in a reduction in rents due to the excess supply.

Demonstrating third-degree evolution

The first two processes of path dependence demonstrate how the valuation process has developed over time through a defined trajectory of technique and repeated practice. The third captures the current situation in retail real estate valuation, describing a situation where there is some concession that retail valuation is inefficient, indeed there is concession that the valuation practice could be improved (e.g. considering business turnover) yet this preferable outcome is not obtained. Instead, the practice of retail valuation is locked into the conventions of the market method. Research participants were asked about the reasons for this persistence and consensus formed around the pressure from clients to maintain values and consequently the traditional processes.

The research participants were questioned on the current issues surrounding zoning and whether valuation practice was starting to accept the need for change in valuation practice. All suggested that their clients (clients in this sense are taken to mean investors/landlords) did not understand any other practice and zoning was the only way they could relate value to retail assets. This illustrates that it is not necessarily valuation professionals themselves who are locked into market norms, rather it is landlords and investors who rely on ‘market based’ valuations to make their financial decisions – and in turn pressure valuation professional to adhere to market convention. Altering the format of this information, and potentially the underlying valuation, would draw scepticism (and an altered assessment of risk) from the banking system as secured debt would have previously been agreed on a consistent forward projection of value.

Consequently, the solidification of current valuation practice can be considered a recursive situation that is not only led by valuation practitioners. Market stakeholders also influence (see Figure 2) professionals to provide and retain traditional processes. Corroborating this assertion, a respondent suggested that Clients only understand rental tones and Zone A rates when considering their retail investments. (Partner; International Surveying Practice)

While another reiterated a similar view.

I have advised some of my clients about the problems with zoning and that tenants are no longer considering rent on this basis. (Partner in valuation department; International Surveying Practice)

In fact, the respondent explained that tenants now consider the affordability of the unit. They contemplate costs associated with occupation including tax and service charge against intended consumer spend and subsequent profit from the unit. Feedback is often that the market rental tone is too expensive when considering other costs.

All participants indicate that they are keen to develop an understanding of different ways of establishing rental tone and market rent, however, there appears to be pressure from clients to remain consistent (even if the information is consistently flawed) when carrying out valuation practice. Participants indicate there is genuine concern from valuers in relation to establishing more meaningful valuation calculations. However, they also indicated that this is a multi-faceted situation. All participants acknowledge that the retail sector has undergone significant change which has seen tenants adapt quickly to changing consumer habits and that they deserve a more accurate and meaningful rent. Tenants are now more likely to prefer a rent based on affordability, rather than any market calculation and wish to negotiate with landlord to ‘rightsize’ their physical footprints and timing of payments. Indeed, tenants now appear to prefer flexibility and affordability over the traditional priorities of location and proximity to maximum footfall.

One participant advised that Tenants are considering not just rent, but all other outgoings and they are more likely to agree a rent that includes business rates and service charge. (Partner within valuation department; International Surveying Company)

However, from the landlord/investor point of view, any alteration could potentially undermine the valuation of assets. When questioned about potential changes to processes in establishing rental tones and market rents one participant suggested that Investors always have an eye on income and cashflows more so today than ever as they have constant financial decisions to make and consider. (Director of valuation; International surveying company)

Locking in traditional valuation processes

Participants discussed increased pressure from landlords and investors to retain conventional valuation procedures. This can be described through the lens of lock-in set out in Section ‘Conceptual framework’. Within the conceptual framework the authors considered three types of lock-in, namely, functional; cognitive; and political (Grabher, 1993). Most notably, functional lock-in refers to the hierarchal systems and organisations which surround a given situation. As discussed in the previous section, the participants understood that any valuation change would need to be considered with their clients. It was interesting to note that more than one participant commented that clients insisted rental tone remains consistent during falling markets (i.e. the rental tone does not reduce in line with markets but remains at the historic high level), rather than being reduced in line with market sentiment. A clear finding in this research is that client pressure prohibits improvements in valuation practice, further demonstrating the causal situation described in Figure 2.

Closely linked to this finding is the manifestation of political lock-in. As previously discussed in Section ‘Second-degree evolution’, the RICS does not seek to change valuation processes, rather they seek to retain consistent approaches. Participants indicated that the RICS has also come under pressure from external parties including financial institutions, investment funds and investors. There was agreement between participants that the RICS retains an unspoken concession that retail-based valuation processes need to evolve. However, the organisation is facing the same degree of pressure as individual valuers to resist this.

Under this pressure, it was clear from the interviews undertaken that the RICS are particularly wary about changing processes or directly advising on valuation methods. One participant commented that there appears to be lack of interest from the governing body to change valuation processes or give advice on this aspect: The RICS are keen to see changes in the way we value real estate although they are not willing to put forward advice other than quality procedure and best practice. They tend to leave the application of the methods to the professionals. (Director; International Surveying Practice)

Finally, cognitive lock-in describes dominant word views or narratives (in this sense the market valuation technique) and can be seen to interrelate with the third degree of path dependency set out in Section ‘Conventional lock-in’. Research participants indicate that the mutual ties and conventions of the market approach over time have led to a form of group thought that now underpins the valuation of retail assets across England. Just as in Grabhers’ (1993) original work into the coal industry, where slumps in performance were onerously interpreted as short-term phases in a business cycle that would maintain long term growth. Slumps in retail real estate performance are onerously explained away as short-term economic glitches which will be recovered once the economy rebounds.

All participants were asked about lock-in and whether adherence to the traditional valuation approach was contributing to the increased number of vacant retail units. All valuers agreed that the consequences of retaining high rental tones was an increase in vacant units as more tenants become concerned with ‘affordability’. Although it was recognised that other factors such as ecommerce and more recently COVID have accelerated this problem.

The consensus of opinion from the participants was time to change practices as the techniques of valuation have become obsolete within retail practices. In fact, one participant mentioned that the valuations have become so complex that they are calling on specialist teams to consider rents and market values, suggesting: Even before the pandemic it was becoming increasingly difficult to value retail assets as thorough analysis of income suggested rental tones were inconsistent, however we are now looking to bring in specialist teams to consider this type of asset. (Partner; International Surveying Practice)

Conclusion

This article set out to explore whether traditional valuation practices are contributing to the increase in void and vacant retail units within the physical built environment in England. In response to the underlying research question–how do contemporary real estate valuation practices capture the new world of retail and what are the implications of these practices for the wider built environment? Findings suggest that the evolution of real estate valuation and the ‘market approach’ is defined through a constrained and specific evolution. Although, this research has been based on practices within England only, which is perceived by stakeholders as a mature market. It is considered that real estate assets operate within a global capital market. While it should be acknowledged that many countries in the global north have different valuation practices, particularly when establishing rent, they are all grappling with the challenge of adapting valuation techniques in the face of changing socio-economic conditions. Therefore, the findings in this article have (a) relevance for any context considering how concepts of value and associated techniques play out in territorial situations and (b) the conceptual framework and practitioner focus can be used to study any market context. Furthermore, the evolutionary approach can also be used as a reference point for any location in the formative stage of developing a valuation procedure, as the findings provide a knowledge basis to avoid similar issues.

With reference to Liebowitz and Margolis’ (2014) interpretation of different degrees of path dependence, the process of valuation has evolved through a combination of ‘learned processes’ followed closely by the ‘complementary effect’ or the rules and governance which define the valuation procedures set out by the RICS. This ‘learning effect’ demonstrates how the market approach utilises comparable information, the often-heuristic nature of associated analysis which has been passed down through generations of valuers and has followed a specific path dependence. However, there was unanimous agreement between research participants that the retail market has evolved over several years and the change has not been accommodated within valuation practice.

Retail tenants are being driven by disruptions in the market to become flexible both in business and in their occupation of space – something that has only been accelerated by COVID. It is, however, concerning that although these changes have taken place old valuation practices persist, coalescing around market rent, zoning, and the process of establishing a rental tone through the market approach. This can be seen as a form of market-wide confirmation bias. The real impact of this situation on the ground is void and vacant units that litter the traditional high street because landlords and investors do not want to revise down their rents. Preferring instead to maintain the headline values agreed at previous valuation dates which were subsequently fed into debt agreements.

From this research, it has been established that problematic forms of lock-in have not only arisen in the process of valuation but that powerful stakeholders have a vested interest in maintaining traditional valuation methods that underpin valuation processes. Stakeholders in this instance include the RICS, banks, financial institutions, investors, and developers – who all have a stake in maintaining conventions of market value. Grabher (1993) and Hassink (2011) would argue that these stakeholders have become too reliant on old ideas and the interested parties are too reliant on each other with little objective scrutiny.

Research participants, and indeed retail tenants, do offer a potential way of improving this situation. The traditional market approach now produces unaffordable rents that are unrealistic for occupiers. This prices them out of occupation and in most instances out of business which leads to vacant buildings. To develop new practices and procedures, the authors argue that there needs to be a new engagement with affordability which has the potential to lead to rents that are more palatable to tenants.

In making these arguments, it is also important to highlight some limitations of the study at hand. This research has been solely concerned with market rent and the process of investment value or market value has not been considered in any depth. This is also an area of current concern for the RICS who are undertaking a review of investment practices. This article only provides a general description of valuation approaches and more detailed research will be needed to fully understand the situation surrounding the investment approach and indeed alternative approaches to value that are undertaken elsewhere in the world.

Furthermore, value is only one part of a complex web of actors, interests and relations who are either directly or indirectly involved in the production and reproduction of the built environment. This article has only focused on the perceptions of private sector valuers involved with the valuation of retail-based assets. Clearly, additional research into the complex relations between the different actors involved (investors, landlords, developers, financiers, and agents) will enrich this line of enquiry. Despite these caveats, we consider that the material within this article, situated within a new conceptual framework for the disciple of valuation, provides a range of interviewee perspectives on current valuation processes and gives other disciplines an insight into the black box of real estate valuation. Indeed, this initial conceptual framework creates some scope for real estate professionals to exert leverage over the RICS, valuation policy and an opportunity to collaborate with other disciplines in its application to wider intellectual debate.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.