Abstract

Two assumptions drive our policy construct. First, the task of implementing a Green New Deal will necessarily fall on the government. Second, artificial intelligence (AI) and robotics have meant a reduction in labour in the production process.

The connection between the two is production by public firms, and the financial instrument is the government bond. The Real Bills doctrine meant the tracking of credit disbursed by commercial and central banks with the returns realized by borrowing firms. The horizon was finite. In the case of our bond, the issuer is the government, and the horizon is infinite. Balance sheet accounts with the central bank are maintained.

We write down a model with no labour. Households lend to the government, which, in turn, lends to firms to purchase their capital inputs. Households earn returns from their holdings of the government bond. The central bank mediates the accounts.

Introduction

Any inhabitant on planet Earth if asked to comment on a horizon that recedes less and less will articulate climate change and artificial intelligence at the forefront of concern. Fewer and fewer economists will prognosticate that the market will deliver solutions. The scale and universality of the public bad of environmental degradation militate against market measures like pollution certificates being adequate. The jury is still out on the net outcomes of labour being substituted by capital, and it is not obvious that the social outcomes are welfare-reducing. The relative strengths of substitution and complementary effects will play out although the International Labour Organization (ILO) has prognosticated that the net effect will be positive for the working class. We only note the heroic transformation of the health and care industry as a spin-off of both these processes. The demands on nursing and old-age care are galloping and cannot be met by machines.

The additional reasons why Green New Deals are being written all over the world, which, by definition, entail deep government intervention, is that private sector initiative cannot be expected for two reasons. Green technologies are still being developed and matters like upscaling for the successful innovations have to be resolved. Second, the costs involved are gargantuan and beyond the reach of the biggest financial consortia. Risks are high and unquantifiable, and probability distribution functions for the returns do not exist. Third, to the extent that labour displacement is demand-driven, the economics of public works of Keynes must be on standby and polished up for immediate delivery.

We offer the following status report on the efficacy of instruments in the government toolkit. Taking the monetary authorities first, central bank governors have watched haplessly as the short-term interest approaches and breaches the zero-lower bound to no effect. That instrument was intended to target the inflation rate anyway, and since inflation is not visible on the horizon of the monetary authorities, central banks are looking to their fiscal compatriots for support. After decades of central bank independence implanted firmly in theory and practice, models of Bank and Treasury coordination of a comparable rigour and acceptability are yet to be found.

Accordingly, we write down a short-term macroeconomic model whose novel feature is a government financial instrument that is a one-to-one mapping with green output period by period. The government borrows and households lend, thereby subscribing to the environmentally friendly programme of the government. Governments do not disburse and monitor credit. The accounts are maintained with the central bank in an identity between the items on the balance sheets of the two. We use Central Bank Digital Money (CBDM) as an operational interface between households and firms, on the one hand, and the central bank, on the other, although, in practical applications, commercial banks could be the decentralized mechanism of delivery.

The Structure of Real Bonds Doctrine Economics

We define ‘structure’ in two ways. The first is a Stock-Flow-Consistent (SFC) matrix in the heterodox tradition in which microeconomics is absent. Interestingly, Green New Deals are being written in the balance-sheet orientation of Modern Monetary Theory (MMT) (Ehnts & Höfgen, 2020). We will take recourse to work in other groups of non-neoclassical macroeconomics. Many of these factions war with each other. We intervene, however, at the points of détente between the various schools. Thus, MMT is regarded as coterminous with the theory of the French–Italian monetary circuit (Colachio & Davanzati, 2020). In both, the economic process originates in the creation of bank money. Wealth is neglected in these models, it is claimed, and the suggestion is to develop a model of the government and central bank as a consolidated ‘innovator of first resort’. The motivation in this regard is a listless private sector anywhere in the world. A massive increase in public sector employment would generate a sharp increase in output and income and the higher aggregate demand flowing therefrom would ignite innovations in the private sector, so the forecast goes. The reasons are the operation of the Kaldor–Verdoorn Law. Also, as employment increases, it becomes hard for private firms to retain competitiveness via wage restraints. In the second subsection, a general equilibrium, though non-Walrasian, model, is developed.

A Stock-Flow-Consistent Representation

Two heterodox traditions are united in a common originating cause. The initial condition of the circuit approach to monetary macroeconomics is the availing of a credit line offered by a bank to an entrepreneur to defray the cost of the wage bill in the first instance. Investment is absent in the ‘initial finance’ of the monetary circuit (Godley & Lavoie, 2007, pp. 49–50). This negative item in the current account of the firm is backed by inventory activity, a number of the same magnitude but opposite sign. Using the given notation, inventories are I, the wage bill is WB and the money disbursed is M. We have the following:

The middle term vanishes in our model, and we provide two equations in replacement. Second, our focus of attention shifts from the accumulation of inventories to production. As the growth of national product plummets and with it profits in the production of goods and services, the wage bill continuing on its long-term downward trend, the ‘way forward’ is to fill in the blank in the above-mentioned equation (Benanav, 2019). We fill in the space with the institution of the government bond. Our answer cannot be entered quickly enough as the alternative to deindustrialization and disintermediation is the stocks of private finance circling overhead to prey on banks, transmogrifying them into shadow banks thirsting after returns to liquid capital rather than production and investment in fixed capital.

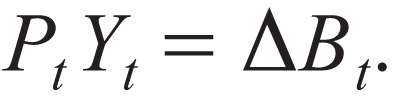

In the beginning, there was also the government comprising its two macroeconomic arms—the Treasury and the central bank. The nexus between the two was intimate, especially in extraordinary times like the unleashing of shocks to the economy. Here as well, the two are connected in SFC terms, items drawn in each cancelling out overall. The point of the issue of the government bond in contrast to the emission of central bank money is the tracking of the flow of production over time.

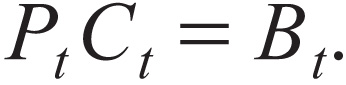

Denoting the GDP in the current period by Yt, the GDP deflator by Pt and the government paper recording the value of goods and services by Bt, we have the following:

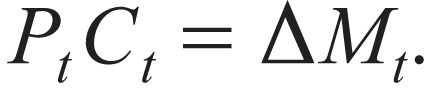

Summing over a finite horizon, we have a Real Bill; over an infinite horizon, we have a Real Bond. Simultaneously, the government bond is an asset in the hands of the erstwhile working class who proceed to spend their interest income on basics. Their interest income is credited into their accounts with the central bank. Note the formal correspondence with wage income and the commercial bank of ‘initial finance’. In addition, the case for central dank digital money has included citizens holding accounts with their central banks. Fundamentally, we posit a continuum between central and commercial banks under the assumptions: with Ct standing for consumption and underscoring the identity between bonds and money

We observe a similar equation in mainstream macro as the ‘cash-in-advance constraint’. However, we insist on the term on the right-hand side being called money, holding to the accounting purity of the circuitists. Income not consumed by the ‘working class’ may be deposited in banks—D—in the box below, or financial institutions. If a comparable slogan is sought, Equation (2) can be described as a ‘money-in-advance constraint’.

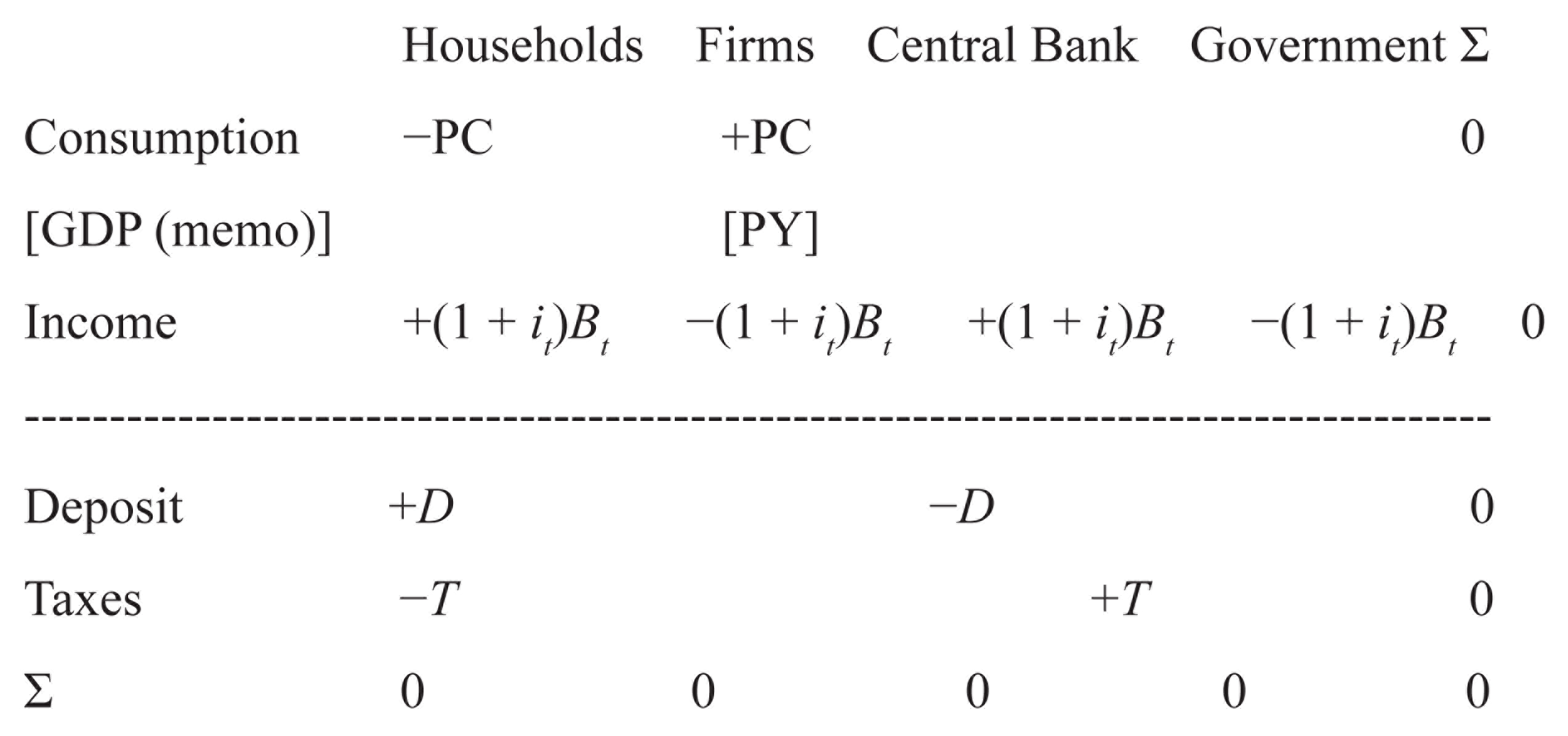

With i as the interest rate, our pared-down balance sheet as given in the Godley and Lavoie (2007) classic is as follows:

The third row is a sharp illustration of quadruple-entry bookkeeping, the principle that defines SFC macroeconomics. Every entry must have a companion entry in a row or column, and each of them, in turn, must be offset by elements of the opposite sign in a column or row, respectively, so as to deliver the row and column of zeroes. In the above-mentioned unique instance, the principle is defined across all the characters on the macroeconomic stage. For the usual vertical relationship between the government and the private sector, a horizontal connection between all the components is proposed here (Ehnts & Höfgen, 2020). We have, in the purity of accounting, pure coordination between the private and the public sectors. The horizontal relationship between the Treasury and the central bank is familiar: the government spends by instructing the central bank to credit the reserve account of the firm. Indeed, the Treasury and central bank balance sheets are consolidated in MMT. A freshly issued interest-bearing bond is no different from interest-bearing fiat money (Mehrling, 2020). The dotted line signifies a firewall between money in the central bank balance sheet and cash deposited by households directly in the central bank. No returns are marked in the box because the deposit rate would be dominated by rates across the board. The return might be nil but so is the risk. Liquidity would never be in peril because a run on a central bank is an unlikely event. In fact, small savers would be happy to pay a tiny fee for the security of their tiny deposit in the vault. The runs during the financial meltdown in 2008 were not on commercial banks, but on mutual funds and investment banks. We hear echoes here of the concern and solution offered by the architects of the Chicago Plan (Tavlas, 2020). The solution was the ‘narrow bank’. The Federal Reserve would pay interest on bank deposits. In order to cover costs, the narrow bank would pay a rate of interest less than that paid by the Federal Reserve on reserves. Above our dotted line was an ‘investment trust’. Admittedly, the trust was entrusted with short-term lending and discounting and funded by issuing securities, but the logic survives our translation. The idea of 100 percent reserve money is attributed to a Nobel Prize winner in chemistry, Frederick Soddy. Mr Soddy distinguished between ‘real wealth’ and ‘virtual wealth’. The first was subject to the inexorable law of increasing entropy of thermodynamics, while the latter obeyed the mathematical principle of compound interest. In thrall to the latter, banks had abrogated to themselves the power of the sovereign and earned seigniorage revenues through their lending activity. The rate of growth of deposits exceeded the rate of growth of output. We take recourse here to the burgeoning literature on CBDM, which enables us to distinguish between Wholesale Central Bank Digital Money (WCBDM) that serves the credit channel originated by the government in our model and Retail Central Bank Digital Cash (RCBDC) which is savings households may prefer to park in accounts held at the central bank. RCBDC is freely accessible, while WCBDM would be available only to firms with addresses. At the same time, WCBDM’s implementation could be effected on public platforms overseen by the Central Bank (Kregel & Savona, 2020). The array of credit and funding risks of private institutions providing finance for investment in capital markets would be on display. The application of the best of data science here improves due diligence and the judgement of creditworthiness limiting arbitrariness in evaluation and reporting. Interoperability is facile in an RCBDC system where every citizen makes or receives payments in a common fail-safe digital currency (Duffie, 2020). The Bank of Canada, more than most central banks, has been hard at work conceptualizing and operationalizing the transition to digital cash (Engert & Fung, 2020). Cash and currency are interchangeable in their framework. The heart of the payments mechanism in Canada is the Large Value Transfer System (LTVS). The LTVS is a collateralized net settlement system with a Bank of Canada guarantee for extreme tail risks like the closure of banks too big to fail. That is, the central bank and the government support commercial bank money for central bank reserves at face value at the end of the day.

The monetary and the fiscal authorities are not just coordinated but are a unity as a government must be. Central banks were born out of the funding of state-driven investments in commerce and transportation (Cisnero, 2020). The need for a non-profit-making financial institution to manage the sovereign debt arose. Thus, governments could procure real resources targeted at social provisioning. For centuries, state-building institutions leveraged social hoards, wheat and then bullion, to create at first an elastic means of payment for retail trade and then large-value promises to pay for the purpose of wholesale trade. These banks developed into quasi-public institutions and the mechanism to insure against overleveraging of cash hoards was promissory notes endorsed by exchange houses. The banking principle was enunciated. When financial breakdowns threaten, private sector financial assets and banking sector liabilities not underwritten by government guarantees cease to convey value. The solvency of the sovereign is jeopardized. Hyman Minsky proposed that capital markets function on the basis of safe assets provided by the government and, therefore, are dependent on the central bank to offer liquidity in exchange for these assets. Both R. S. Sayers and Minsky believed that central banks and private banks can be ‘rich’ in tranquil times if they structured their balance sheets so that the flow of funds from debtors is constant and low risk. The Real Bills doctrine is illustrated. In the threefold typology made famous by Minsky, the doctrine is adhered to if bank portfolios consist of a mix of hedge and speculative financing. The more of the latter, the richer the bank. The finance of state-building institutions, unfortunately, turned out to have a Ponzi structure. Payments to shareholders and creditors were due in advance of revenue streaming in. Fiscal expenditures burgeoned. The history of European and continental central banks stretching across centuries is illustrative and illuminating (Birdseil, 2019). The outcome was the issuance of a liability of superior credit standing than any other financial liability in the economy. It was constituted through public charters, legislative enactments and laws. The reason is that the emission of central bank money is a natural monopoly and should be provided by the public sector although regulated by the rhythms of the capitalist dynamic. The funding, liquidity and stability of the economy are enhanced by central bank lending protocols, on which private firms can depend, so long as they provide eligible collateral.

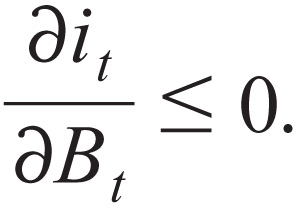

The grounding of the ‘reality’ backing the government bond in environmentally kind production cannot be emphasized enough. Political economists have protested that the sharp and sustained rise in the market price of long-term bonds aggravates inequality since low-income households have meagre endowments of this asset (Honohan, 2019). Environmentalists are also upset with central bank purchases of bonds issued by firms that leave behind massive carbon footprints. Thus, the European Central Bank (ECB) and the Bank of England (BoE) purchase bonds of carbon-based energy companies to an extent disproportionate to their importance in the economy. A total of 62.1 percent of ECB corporate bond acquisitions occur in manufacturing and electrical and gas production, which account for 58.5 percent of the Eurozone greenhouse gas emissions but just 1 percent of the gross value added (GVA). Similarly, in the case of the BoE, manufacturing and electricity production explain 52 percent of the UK emissions, make up 49.2 percent of the eligibility benchmark, but contribute only 11.8 percent of the GVA. Collateral eligibility rules for central bank lending to banks will influence access to finance across firms and households. Our central bank Overton window offers the creation of purchasing power solely by way of a loan or outright purchase of a security, not as an advance or grant. Corrective and constructive measures have begun to be taken with environmental, social and governance (ESG) criteria becoming widespread in the scrutiny of investment projects (Dikau & Votz, 2020; Fender et al., 2020). ESG implies long-term value, risk and return. The Banque de France is on board as is De Nederlandsche Bank. To elaborate, green bonds are fixed income securities whose proceeds are used to support projects that combat pollution, climate change, and the depletion of biodiversity and natural resources. The instrument is asset-backed. That is to say, it must specify at issuance the set of green projects eligible for funding. At root is the rediscovery of transformative innovation policy (Grillitsch et al., 2020). Innovation was directly oriented to improving public health, controlling pollution and preserving the natural habitat and not just increasing consumption possibilities. The USA being the canonical example, the earlier model was one in which the government underwrote a push to science for solving technical problems. The outcomes were so-called mission-oriented programmes like the Manhattan Project or the Apollo Program. The government supplied and was the sole customer. The global challenges, today, like the loss of biodiversity and ageing societies, are unstructured problems. Climate change calls for pushing the obsolescence of existing technologies with strong distributional implications. ‘Brown’ must be phased out in a process of ‘exnovation’. Indeed, the call is for transformative socio-technical systems. Core concerns like energy and nutrition must be addressed. Accordingly, there is clear direction in the articulation of specific demands. Given the uncertainties and the long-term nature of the destabilizing changes, reflexivity on processes is essential. Continuous monitoring is not less important than the evaluation and anticipation of outcomes.

Finally, the absence of commercial banks alongside the central bank, coterminous with the monetary and fiscal authorities working in tandem, is not to be taken literally. Indeed, it is unlikely that in the nitty-gritty of the actual implementation of the scheme, the network of commercial banks would not be the agents and the central bank the principal. As a matter of fact, scholars have discerned two interpretations of the Real Bills doctrine (Adam, 2020). One was oriented towards self-regulation of a decentralized system of commercial banks, while the other of centralization of real bills. It was the former that was believed to ‘have its ear to the ground’ in offering elastic credit founded on the needs of the economy. The bills were to be short term and self-liquidating. The latter consisted in centralizing reserves and worked with an acceptance market rather than a close tracking of the fortunes of the projects backing the bills. Acceptors would have privileged access to the discount window, and the discount rate was the instrument by means of which the central bank would steer the market. Prior to 1931, the real activity on which the acceptance was written was not factored into the risk pricing in the secondary market. A bill was regarded as blue chip by investors as long as the names of the endorser and investor were above board. The buck of monitoring of the fortunes of business was passed from the investor to the accepting bank, which passed it to the endorser who usually was a foreign resident.

Government Bonds are Net Wealth

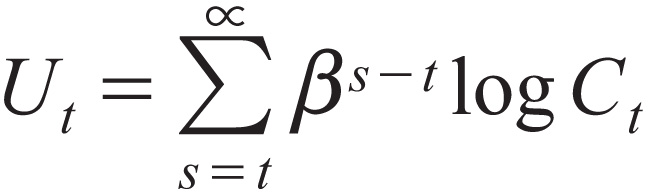

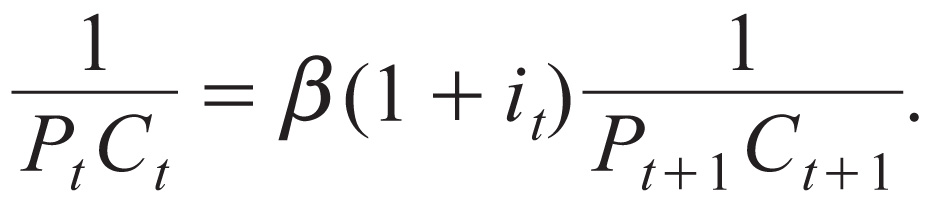

We answer Robert Barro’s classic question implicit in the title of this section contrariwise to the answer given by the profession. In order to connect with mainstream practice, we follow in the footsteps of Bénassy (2007). Thus, a production function relates the stock of robots and computers and clouds—Kt—with aggregate output—Yt = F(Kt). The problem of the representative consumer is given by the choice of a consumption stream by maximizing the following utility function where Ω is the symbol for wealth:

subject to

The first-order condition is

Bénassy observes that the price level is indeterminate, and the ‘liquidity effect’—a fall in the interest rate brought about by expansionary monetary policy—does not emerge.

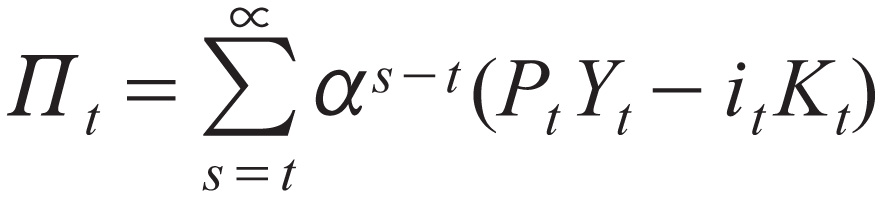

In our framework, we need to separate out production in the standard formulation. Accordingly, with i the rental on capital, the problem of the firm is to choose a stream of Kt so as to solve the following problem. The profit function is additively separable:

The per-period first-order condition is familiar:

We write down a wealth accumulation equation for the firm comparable to Equation (3) for the consumer using the same notation:

Adding Equations (3) and (6) and abusing the notation, we get an aggregate private sector wealth accumulation equation. The term in curly brackets on the right-hand side of the equation below can be described as the government wealth accumulation equation:

The public and the private sector are in lockstep. The equation is not the familiar theorem of macro, a government deficit equalling a private sector surplus. A period-by-period equivalence is suggested. Post-Keynesians like Randall Wray have worked out a formula for a ‘ratchet’-like increase in government expenditure through the cycle. In a regime of a permanent government deficit, public debt will not be onerous (Hein & Martschin, 2020). As a logical possibility, those holding government bonds and those paying taxes could be identical, resulting in an internal transfer. In a growing economy, interest payments will not be out of sync with tax revenues at given tax rates. Digging deeper, since the term ‘secular stagnation’ coined by Alvin Hansen has been resurrected to apply to the present state of the world, it is relevant to return to the context, which drove his characterization (Assous et al., 2020). The USA as an engine of innovations was spent, and expectations were at a nadir. Income was at an all-time low, and investment plans were not to be seen. Consequently, Hansen concluded that a continuously increasing level of government expenditure would be required to maintain income at higher and higher levels. Far from being just counter-cyclical policy to stimulate consumption, government expenditure should increasingly be the mechanism to direct savings to real investment. Equilibrium would be at a level of full employment at a positive interest rate. The summation of the terms in the equation and the imposition of a transversality condition would be inappropriate. There is no debt for which a terminal repayment condition must be imposed. Neither player is a Ponzi, whose game playing must be circumvented. It is not that ‘in the end’, Ricardian equivalence must hold—the benefit of government expenditure ‘today’ matched by the present value of the taxes to be paid ‘tomorrow’. If anything, the golden rule for public investment is invoked in the present instance. Deduct net public investment from the headline structural deficit, and the former would be financed by way of deficits. Public investment would be privileged by separating the current and investment budgets. Since present government spending would provide future benefits and augment the social capital stock, a pay-as-you-use principle would satisfy intertemporal equity. It is not unreasonable to expect core infra capacity as an input that is complementary to private capital. Also, present value accounting is a central precept in a modern interpretation of orthodox political economy. However, care has been advised in the treatment of the concept (Anderson, 2019). Capital is said to be ‘fictitious’ if the expected future returns are not based on production from physical assets, but on derivative contracts ranging from plain vanilla to esoteric products many removes away. Japan was able to manage massive tranches of liquidity because 95 percent of the government debt was denominated in yen and held mostly by the Japanese. The world rose from the ashes of the Depression because of the leadership of pre-war Japan with its model of coordinated monetary and fiscal action of an order far greater than the New Deal. The lack of success of the big bang of Quantitative Easing can be understood here (Gaffard, 2018). The demand for goods and services to match the demand and supply for credit was non-existent. The milieu to undertake reliable forecasts so as to underwrite long-term investments via banks was not opportune.

Substituting Equation (5) in Equation (4):

The (current) price level is determinate now with an expectation operator applying to future values, and we can expect the ‘liquidity effect’ to hold. We follow Bénassy, but with a ‘bonds in advance constraint’ this time:

Plugging Equation (8) into Equation (7), we establish:

In addition, we propose an ‘illiquidity effect’. In the case of the magnitude of the term attached to the concavity of the production function being higher than the other term:

The government bond is conducive to the accumulation of capital. However, investment is outside the purview of our model.

Discussion

Recall the first lecture in Econ 101. The National Income identities include government. While government consumption is placed alongside private consumption explicitly, government investment goes with private investment implicitly. Through force of habit or under certain assumptions, the connection between the two is depicted through substitutions and crowding out. In contrast, we have developed a positive and normative framework at the unity of the private and the public. Households are increasingly becoming sensitive to environmental degradation, as the ravages wrought therefrom are present and not present-valued. People are likely to be more than willing to grasp the nominal returns offered by a government instrument in which real returns are visible in green enterprises dotting town and country.

We use the broad brushstroke of the public firm to characterize our business although we welcome the recent distinction made between the corporation and the enterprise (Segrestin et al., 2020). The enterprise emerged at the end of the 19th century, while the genesis of the shareholder value maximization model of the corporation was laid earlier in the distribution of profits to merchants and producers. The enterprise was the fruit of the scientific and technological breakthroughs brought about by the R&D wings of industries. It was productive and commercial and creative at the same time. It not only produced goods and services but also devised new goods and services, developed new technologies, novel competencies and fresh jobs. The corporation, by contrast, was set up by shareholders who contracted to appropriate property to a joint end. Workers were not part of the compact. The enterprise at the service of employees and managers was not defined in the law. A vitally different form of organization was called for to systematize innovation and new industrial relationships. The heart of the enterprise was the collective education of workers so as to make them flexible enough to adapt to changing conditions. A clear illustration of the distinction between the modern financialized corporation and the enterprise is Apple (Lazonick et al., 2020). With the focus of management on stock buybacks, innovative investments in technologies, such as communications, energy and healthcare, have been ignored. Similar to our distinction between money and cash, buybacks and dividend payouts are disbursements defined as cash, not capital. The difference is highlighted by the fact that the only stock Apple raised from the public was its initial offering in 1980. All the current shareholders have purchased shares in the market. They are not investors in Apple as a productive enterprise. Finally, we support the case for a return to the unlimited liability of the enterprise that prevailed till the 19th century, albeit in a vitally different sense (Goodhart & Lastra, 2020). The institution encouraged responsibility and accountability. However, (equity) owners had to possess adequate wealth to meet with potential liabilities as well as perfect information about other equity holders and the corporation. Since these conditions were onerous, the mechanism collapsed into the limited-liability company.

We conclude tentatively with a modus vivendi between the private and the public sector. The platform firms of today represent a new way to create and capture value (Rahman & Thelen, 2019). The objective is not ownership but control. The data and algorithms on a platform allow the degrees of freedom available to participants to coordinate on actions. The capital is ‘patient’ though not in the sense of the coordinated capitalism between workers and capitalists of yesteryears. In this case, interests are non-antagonistic and concentrated between managers and investors. The industry structure is oligopolistic with high barriers to entry. Venture capitalists are known to be in possession of deep pools of investment capital and might be capable of providing the scale called upon just so long as they can be ensured of market dominance over a finite period (Lazonick, 2020, connects venture capital with collective learning). Second, they might backstop the risk-taking of ambitious governments in new financial arrangements like long-term stock exchanges (LTSE).

Conclusion

Not a few of the classicals foresaw a world in which technological change would render work obsolete. The workers of the world would be united in their enjoyment of leisure activities. The other aspects of their ruminations included participatory democracy, where citizens shared in the fruits of enterprise. If there were no workers, there would be no capitalists. Investment would not be left to the vicissitudes of business mood swings, but it would be conducted by public enterprises. The Treasury and central bank would return to their original unity in underwriting production and consumption in a capitalist economy. We have provided a macroeconomic model to reflect this denouement with the government bond as an axis.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.