Abstract

This essay is a conversation between Shoshana Zuboff’s theory of surveillance capitalism, Mikkel Flyverbom’s conceptualization of the hyper-visibility afforded by digital architectures, and my own ‘analog’ theory of accounting dynamics in the ‘audit society’. Drawing upon trends in accounting practice and research I develop a number of inflection points which define theoretical tensions between the concepts of audit society and surveillance capitalism. These tensions suggest that theoretical innovation is required in the face of: the accelerating constitution of organizations by platforms and their processes – ‘platformization’; the constitution of human agents as data-driven subjects of these data architectures – ‘cyborgization’; and the reconstruction of the social sciences by a pervasive data positivism in which accounting becomes ‘accountics’. The exploration of these three inflection points reveals the deep operational logic of surveillance capitalism as an ‘economy of traces’ and traceability. Zuboff’s challenge of a political dystopia governed by technology giants and Flyverbom’s image of a society ‘overlit’ by digital architectures necessitate a re-specification of the audit society dynamics that I have previously theorized. The re-specification that I propose in this essay is a form of a critical ‘traceology’ which takes as its focus the ongoing production of all manner of traces and how they make up organizations, people and forms of knowledge.

Keywords

It is said that we now live in an era of ‘surveillance capitalism’ (Zuboff, 2015, 2019, 2022) definable as a pervasive digital apparatus in which all human experience, whether classed as leisure or work, is claimed as free raw material for behavioural modification and profit. Notwithstanding criticisms that this thesis ignores prior work on surveillance (Ball, 2019), understates the role of law (Cohen, 2019) and neglects the historical role of cybernetics (Evangelista, 2019), it is widely agreed that Shoshana Zuboff’s analysis of how technology giants and nation states extract large volumes of data from populations without their consent is provocative and compelling. She argues that the stakes are high. No less than our shared human nature is at risk, including the deliberative capacities essential for democracy. Zuboff’s challenge is also theoretical: the phenomenon of surveillance capitalism ‘cannot be adequately grasped with our existing concepts’ (Zuboff, 2019, p. 14). This essay reflects further on this question of theoretical adequacy and its implications for how we study organizations and organizing in the digital age.

Zuboff’s diagnosis of surveillance capitalism and its effects operates mainly but not exclusively at the level of political critique. Despite her focus on Google, she says relatively little about organizational processes more generally (Flyverbom, 2022). And yet, Zuboff depicts a world in which Taylorist dreams of perfect worker control are being realized by an internet of things based on sensors embedded in every aspect of our working and private lives. The spectre of the ‘omniscient organization’ (Marx, 1990) seems to have moved closer to reality from being mere science fiction fantasy and totalitarian dream. Stiegler (2018) travels a similar path to Zuboff and describes this acceleration in digital automation as a new phase of ‘proletarianization’. Indeed, there is already an extensive labour process literature focusing on how the behaviour of contracted workers is tracked, controlled and made visible in unprecedented ways by carefully designed algorithms (Flyverbom, 2022; Kellogg, Valentine, & Christin, 2020; Leonardi & Treem, 2020; Newlands, 2021; Ranganathan & Benson, 2020). More generally, management and organizational scholarship about these digital transformation processes is diverse and growing (Lanzolla et al., 2020).

Zuboff argues that the object of her analysis is a ‘logic’ rather than technology as such. In this essay, I focus on how we might theorize such a logic of ‘data driven’ social ordering (Zuboff, 2015, p. 76; Alaimo & Kallinikos, 2020). In particular, I explore the implications of datafication (Flyverbom, 2022; Leonardi & Treem, 2020) for critical theories of accounting and organizing, and especially for the ‘audit society’ thesis which I have proposed in my earlier work (Power, 1997). Although these theories were important for the diagnosis of neoliberalism, like Zuboff I argue that they require a ‘rebooted’ lexicon which is more adequate to the investigation of how surveillance capitalism is operationalized at the level of both formal organizations and everyday life. Specifically, I propose the analysis of traces and traceability as a basis for reframing the audit society agenda.

The general question of theoretical adequacy needs to be unpacked a little. Theorizing begins as a response to phenomena and events, to a world which presents itself in puzzling and anomalous ways (Swedberg, 2014) and leads to ‘unsettlement’ in communities of enquiry (Reed & Zald, 2014). It follows that theories and their core concepts may be ‘too slow to adjust to new phenomena’ (Kornberger & Mantere, 2020) and may lose their explanatory, interpretive and critical purchase when the world changes (Nadkarni, Gruber, DeCelles, Connelly, & Baer, 2018). In what follows, I consider three interrelated problematizations of theoretical adequacy which are posed by the phenomenon of surveillance capitalism as Zuboff expresses it. I call these problematizations ‘inflection points’, defined not by the ‘gaps’ and ‘puzzles’ which usually motivate the expansion of normal science, but instead by a sense of unease about the adequacy of existing theories and conceptualizations, and their deep-seated assumptions. Adequacy does not require a tight fit between theories and the phenomena they seek to explain and explicate. Indeed, some tension and dialectic with empirical data is a desirable feature of theory and ‘keeps it honest’ and dynamic. But an inflection point arises when this looseness of fit widens in the face of observable changes, for example, in organizations and their environments. Inflection points are characterized by creative tension between old and new theorizations in the face of new and puzzling phenomena.

Like Swedberg (2014, p. 8), who promotes the role of imagination and concept-building in theorizing, Zuboff (2019, p. 14) argues that understanding the unprecedented phenomenon of surveillance capitalism demands, and begins with, efforts at fresh labelling and naming. Yet theoretical innovation at a point of inflection does not necessarily involve an intellectual rupture requiring the invention of an entirely new theoretical lexicon. As we shall see, innovation may also re-centralize, re-signify and repurpose existing concepts and ideas which have been forgotten or marginalized (Nadkarni et al., 2018). In short, the material for renewing theoretical adequacy may be readily available and awaiting reuse.

In what follows, I discuss three possible inflection points generated by surveillance capitalism for the critical accounting agenda: the accelerating constitution of organizations by platforms and their processes; the constitution of human agents as data-driven subjects of these data architectures; and the reconstruction of the social sciences by a pervasive data positivism. These three formative processes are intertwined and represent a systematic inversion of the centuries-long presumed relationship between humans and machines. Drawing from the lexicon of prior studies, these three processes can be conceptualized as, respectively, ‘platformization’ (Ciborra, 1996), ‘cyborgization’ (Nyberg, 2009) and ‘accountics’ (McMillan, 1998; Sprague, 1922). I shall argue that these three notions are theoretically fruitful for the analysis of how the logic of surveillance capitalism is operationalized at the organizational level. They also foreground the need to study what Stiegler (2018) calls the ‘economy of traces’.

The first inflection point suggests how critical accounting themes and the motif of the audit society provide useful resources for theorizing the performative character of data architectures to some extent. However, they remain grounded in a number of dualisms which are theoretically challenged by surveillance capitalism. In essence, the audit society thesis focuses on how organizations respond to external performance demands by conforming themselves to auditability and evaluation requirements, with consequences for organizational values and actor motivation. This logic of auditability is performative of organizations and humans to a greater or lesser extent (Power, 1997, 2021). In this essay, I invert these arguments and suggest that accounting, auditing and evaluation, and therefore accountability, are themselves increasingly shaped by data architectures and the platforms which host them. While there are many different definitions of, and perspectives on, platforms as entities (Poell, Nieborg, & van Dijck, 2019), I propose four specific markers of platformization as a process: the algorithmic generation of accounting categories; the rise of self-auditing; the blurring of boundaries between different managerial specialisms; and the intertwining of logics of traceability, control and security.

The second inflection point, closely related to the first, concerns the implications of the rise of data architectures for formative theories of the agents who are subject to accounting and performance metrics (Miller & O’Leary, 1987; Power, 2021). These earlier insights also retain an implicit dualism between humans and accounting technology which is increasingly challenged by algorithmically generated sociality and the intertwining of social learning and machine learning (Fourcade & Johns, 2020). Performance profiling based on data extraction by bodily sensors, such as mobile phones, generates a ‘data double’ for human ‘users’, which is internalized via continuous repetition and ‘curation’ (Alaimo & Kallinikos, 2020; Newlands, 2021). I suggest that this intensification of machine–body interfaces (Ball, 2005; Ball, Di Domenico, & Nunan, 2016) requires an inversion of the sociomateriality concept, namely the ontological and methodological prioritization of non-humans in theories of human self-formation and sociality. I propose that this ‘materiosocial’ turn in critical accounting – ‘reassembling the material’ as Fourcade and Johns (2020) put it – requires a focus on the ongoing processes by which digital prosthetics are attached to humans, extract traces, and generate new human experiences and ‘data hungry’ subjects. These processes define the scope of ‘cyborgization’.

Finally, the third inflection point reflects on the consequences of both platformization and cyborgization for academic management disciplines like accounting. What does it imply for accounting and for management and organization studies when the same data architectures by which organizations know themselves also define what it is for social scientists to be properly empirical? I will argue that surveillance capitalism points towards a ‘post-social’ social science which it requires for its self-maintenance. I repurpose the category of ‘accountics’, which originally positioned accounting as a branch of science (McMillan, 1998; Sprague, 1922), and use it to characterize the increasingly strong symbiosis between academic accounting and data analytic knowledge of organizations. Accounting academics who are enthusiastically embracing the data explosion are also accelerating the formation of the ‘post-social’ sciences as an adjunct of surveillance capitalism.

Inflection Point 1: Accounting and Platformization

From the 1980s onwards, accounting scholars and practitioners debated the need for accounting to be more forward-looking, more strategic in character and more relevant for decision makers (Johnson & Kaplan, 1987). Forward-looking measures of value – so-called ‘fair values’ – based on financial economics rather than transaction history grew in significance, despite being controversial (Power, 2010). Beyond traditional forms of accounting and their measurement conventions there was increasing focus on both the financial and ‘non-financial’ causes of accounting and economic outcomes for businesses, and the need to measure them at source (Bhimani, 2015; Bhimani & Bromwich, 2009). The traditional accounting model of control was failing, costs were out of control, and there was a need to understand the activities that drive them (Johnson & Kaplan, 1987). Organizational accounting and control systems aspired to become causal and predictive, and thereby more relevant servants of strategy, if not strategic in their own right.

The rise of digital technology and the creation of elaborate data architectures within and across organizations represents the potential to realize this decades-long ambition to extend control further down the causal chain of economic value production, even to the level of individual customers, workers and their actions. Such architectures can be defined broadly as apparatuses which intermingle data, technologies for the production and diffusion of data, and the algorithms and analytics by which data is made to matter to organizations (Alaimo & Kallinikos, 2020, p. 20). The rise of these data architectures marks a rupture in the basis of accounting and organizational control (Bhimani & Willcocks, 2014; Constantinou & Kallinikos, 2015). It also challenges the continuing relevance of the ‘audit society’ thesis (Power, 1997), which claims that performance measurement and auditing have become increasingly prominent and consequential ‘logics of organizing’ in many societies. This broadly neoinstitutional argument identifies systematic tendencies for organizations to orient their internal processes around accounting requirements and to make themselves ‘auditable’. Mobilized by animating myths of transparency and efficiency, studies have identified the consequences of this logic of auditability for the unmeasured but valued aspects of organizational practice and for the expertise of organizational members.

At first glance, the emergence of data architectures seems to be readily understandable as a continuation and augmentation of audit society processes, contributing to the further accounting rationalization of organizations. They involve the reductive coding of human activity for data collection purposes, its categorization, quantification and commensuration (Espeland & Stevens, 1998; Flyverbom, 2022; Mennicken & Espeland, 2019), and its aggregation into patterns for further analysis and strategic exploitation (Alaimo & Kallinikos, 2020). Furthermore, there appears to be a convergence between critical accounting research and the sociomaterial turn in organization studies (Orlikowski & Scott, 2008) in the form of shared commitments to understand the formative power of technologies – both bureaucratic and digital – in shaping organizational life and its control practices. Indeed, accounting scholars have begun to draw on work in information systems and surveillance studies to analyse data architectures and their implications for management control, such as online rating platforms like Trip Advisor (Jeacle & Carter, 2011; Scott & Orlikowski, 2012).

Notwithstanding these theoretical convergences and exchanges, Zuboff’s analysis of surveillance capitalism suggests that the rise of data architectures also marks a shift in the social order at the heart of the audit society, namely, from accounting by and for humans to a data order in which material machines and immaterial and invisible algorithms are becoming preeminent and performative (Glaser, Pollock, & D’Adderio, 2021). Audit society arguments are dependent on a series of more or less implicit dualisms: between organizations and uncertain institutional environments which impose auditing, accounting and accountability requirements (Meyer, 1986); between human actors and the accounting systems which discipline them; between work and non-work; between principals as one group of human actors and agents as another who are ‘accountable’ to them; and, importantly, between the measurable and visible, and the unmeasurable and invisible. The audit society thesis focuses on how one side of this duality expends energy and time conforming to, or resisting, the demands of the other side in a process of rationalization. Yet, data architectures under conditions of surveillance capitalism render these working theoretical dualities increasingly non-descriptive. Accounting transactions and categories traditionally reflect relations of similarity grounded externally in institutional environments. Emerging data architectures under the conditions of surveillance capitalism invert this process: accounting categories emerge from bottom-up usage patterns, via the extraction of data from humans. Thus, it appears that the logic of surveillance capitalism is radicalizing the change agenda for accounting and organizational control that originated in the 1980s in order to realize the dream of the ‘data driven’ organization (CGMA, 2016; Quattrone, 2016).

Platforms have emerged as a distinctive form of data architecture but they are discussed and conceptualized in different ways (Poell et al., 2019). They are variously: multi-sided markets bringing users and third party providers together (Rochet & Tirole, 2003); discrete business infrastructures (Kornberger, Pflueger, & Mouritsen, 2017; Plantin, Lagoze, Edwards, & Sandvig, 2018); new topologies and organizational forms (Casilli & Posada, 2019; Ciborra, 1996; Frenken & Fuenfschilling, 2020; Stark & Pais, 2020); and methods for enhanced control of the labour process (Kellogg et al., 2020). Furthermore, platforms are in some sense always incomplete, modular and open to new applications and programming. According to Zuboff, they are mechanisms of expanding economization which transcend and reformat traditional distinctions between private and public, society and economy, system and lifeworld.

Regardless of differences between these different optics on, and conceptualizations of, platforms, traces and traceability are at the heart of how they operate. The gathering of traces of the actions of human actors – now defined as platform users – as data for further analysis is a form of market-making whose operating logic is not contracting, commanding or collaborating but that of the co-optation of assets (Stark & Pais, 2020; Zuboff, 2015). While accounting has historically played an important role in constituting organizations as economic entities, platforms and their algorithmically constituted operations radicalize this economization (Alaimo & Kallinikos, 2020; Caliskan, 2021; Cohen, 2019). I propose that this intensification of ‘platformization’ as a formative process raises four theoretical challenges for critical accounting studies.

Accounting categories

Unlike traditional accounting systems, platforms produce higher order categories ‘from below’ via algorithms which group initial traces – such as clicks and likes – via formal relations of similarity. In recommender social media platforms, this raw data can be used to generate higher order objects which can be linked to others (similarity being revealed by the co-location of clicks) to form the basis for suggestions. There is a self-reinforcing loop as humans react to these prompts and make further choices, whether of music or of potential partners (see Alaimo & Kallinikos, 2020; Fourcade & Johns, 2020). Other data architectures are dedicated to tracing and tracking objects and humans, such as gig economy workers (Newlands, 2021), and there is no doubt further variety to be studied, but the principles are the same: human action is captured and converted into digital form, then subject to higher order analysis and algorithmic processing. It is this continuous capture of heterogenous primary data that drives ‘higher’ level forms of data analysis. In this world, the power of auditing and accounting to shape organizations is being displaced and reshaped by the power of data to constitute data-driven organizations (Alaimo & Kallinikos, 2020).

The rise of self-auditing

Two specific effects of these developments are worth noting. First, platforms potentially democratize audit and evaluation practice, taking it out of the hands of experts and empowering consumers to produce ratings and other primary traces which can be used to evaluate organizations (Power, 2011; Scott & Orlikowski, 2012) and which organizations process to understand and manage their reputation and profile in markets. Social media platforms are increasing the capacity of consumers to evaluate and score more products and services, and are generating new forms of community in the process (Fourcade & Johns, 2020). Organizations as users of these platforms invest in tracking and analysing these digital captures of sentiment as lead indicators of their future performance (Alaimo & Kallinikos, 2017).

Second, auditing organizations are themselves embracing data analysis and artificial intelligence techniques in order to be able to audit data architectures. In effect, it may only be possible to audit algorithms with other algorithms. Thus, under conditions of surveillance capitalism, evaluation and auditing become inter-algorithmic in form: there is no need to worry about when the inspectors are coming since they are already here, built into data architectures as just another user-customer interface. Rather than organizations in the audit society making themselves ‘auditable’ (Power, 1997), auditing and evaluation are being re-constituted by data architectures. Indeed, as Cohen (2019) notes, platforms are self-certifying and constitute forms of self-governance which are immune to external scrutiny and oversight. The institutional myth of auditor independence, which was already fragile, is rendered meaningless by the algorithmic organization of surveillance.

The blurring of managerial expertise

These developments are boundary-shifting for organizations. Data gathered about and from customers and employees and their habits brings them ‘inside’ organizational control systems. And as data architectures become more liberal about data sources – the big data concept – the clarity of the internal/external dualism of accountability in the audit society dissolves into a new platform topology (Stark & Pais, 2020). In consequence, traditional organizational jurisdictions between internal functions are shifting. Accounting, human resource and marketing functions participate in common organizational-level platforms which manage data for customer acquisition and retention, and which categorize customers in unprecedentedly precise ways (Constantinou & Kallinikos, 2015). In this way the logic of surveillance capitalism at the organizational level is displacing the century-long cultural position and authority of the accountant as the arbiter of value. Concepts of transparency and accountability grounded in reciprocity and contractualism are no longer adequate to capture what is at stake in the continuous, granular extraction, tracing and tracking of things and their performance (Ananny & Crawford, 2018; Christensen & Cornelissen, 2015; Flyverbom, 2015; Hansen & Flyverbom, 2015; Heimstädt & Dobusch, 2020).

Traceability and security

Data architectures as platforms require feeding by digital traces. The digital tracing of people under conditions of the Covid-19 pandemic has been one of the defining problems of control in 2020. Human actions can only enter data architectures as data traces. The human ‘off platform’ must be digitally tagged. Traces of movement, purchasing, web visits and a whole host of other ‘captures’ or ‘extractions’, and their connection to other traces, produce over time the digitized biography of their referents.

Traces and trace-making, in the form of audit trails, underpinned the operationalization of the audit society. But the latter was never simply a surveillance society (Power, 1997, pp. 128–34). It was premised on knowing organizations and performance in specific and limited ways, via books and records. The humble audit trail was a bureaucratic procedure for accounts production and checking. Yet under conditions of surveillance capitalism, accounting, auditing and surveillance are entangled in common data architectures and traceability is their shared organizing logic, enabling new forms of behavioural visibility grounded in data visualization techniques (Flyverbom, 2022; Leonardi & Treem, 2020). The performative power of the audit trail (Power, 2021) is being extended and radicalized by the programmatic dream to have unbounded knowledge of everything, which Zuboff sees as a defining ambition of surveillance capitalism. Digital traceability provides the raw data for this limitless expansion of organizational knowledge, reaching far deeper into the everyday and intimate sphere than accounting ever did. For Zuboff, Google is in the ‘truth’ business in which everything can be known, nothing is too trivial, uncertainty is to be limited and certainty is a source of organizational and societal security. Whereas the audit society is underwritten by myths of efficiency, transparency and accountability, the deep logic of surveillance capitalism is that of security (Cohen, 2019).

Inflection Point 2: ‘Cyborgization’, Actorhood and Practice Theory

Studies have shown how accounting, control and auditing practices are formative of human agents as they attend to, are immersed in, and even resist, performance apparatuses and their metrics (Miller & O’Leary, 1987; Miller & Power, 2013; Quattrone, 2015; Power, 2021). This work draws upon a broader landscape of formative social and organization theories informed by concepts of sense-making, habit, disposition, emotion, identity, institutional work and many others (Callero, 2003). Furthermore, there have always been affinities between work in accounting, information systems and surveillance studies which commonly analyse the formative power of technical apparatuses. Yet these different theorizations of subject-formation share an embedded presumption of the primacy of a form of human agency which is more or less coherent and capable of reflection and deliberation in the face of the power of technologies, such as accounting metrics. Indeed, this common presumption of the very possibility of some kind of reflexivity is the source of continuous intellectual resistance to variants of structuralist-institutional ‘iron cage’ theorizing (Cardinale, 2019; Hwang & Colyvas, 2020). In short, there is a more or less implicit and continuously reformulated dualism between humans and (accounting) technologies.

These dualisms are challenged by Zuboff’s surveillance capitalism thesis. For example, customer relationship databases, as provided by organizations like Salesforce, track customer data and interactions, thereby providing a basis for ‘knowing your customer’ (KYC) and also for organizations to know their staff via traces of system usage. These surveillance capabilities place human organizational members in relationships both of observing and being observed via the very same trace of a physical action (e.g. a keyboard stroke). They also potentially result in a ‘data double’ for human actors which is progressively formative of preferences via continuous repetition (Alaimo & Kallinikos, 2020; Newlands, 2021). This is evident in the emergence of social media ‘vanity metrics’ as quantified measures of virtual ‘sociality’ which feed ‘sociometric self-formation’ (Cardon, 2020). The formative outcome is a self-tracking self which is ‘data hungry’ (Fourcade & Johns, 2020) and ‘quantified’ (Lupton, 2016; Swan, 2012, 2013).

In the face of these developments, critical accounting analyses of subjectification and ‘internalization’ fall short of enlightening the way humans are becoming, if not fully cyborgs, then subject to intense cyborg-like processes via bodily attachment to data architectures. Indeed, such cyborgization may be a form of strategic pre-automation – advance preparation for full replacement of the human by automation (Vertesi, Goldstein, Enriquez, Liu, & Miller, 2020). The significance of human bodies in social and organizational studies has long been widely recognized (Ball, 2005; Ball et al., 2016; Blanche & Feldman, 2021) and the theme of cyborgization is also hardly new or original. However, the acceleration of digitalization (Leonardi & Treem, 2020) as a feature of surveillance capitalism and its data architectures problematizes and inverts the theoretical dualism of human and machine and demands a focus on the point at which data apparatuses abstract from bodies and de-physicalize them for the purpose of generating data assets. Traces of human actions, as discussed above, are ontologically transformative as they cumulatively generate a digital social reality. This in turn implicates an inflection point for accounting studies which requires the theoretical re-centring of the cyborgized and prostheticized character of human bodies as sources of traces in order to better understand the performative character of data architectures. Below, I explore this inflection point via two themes: the implications of the immersive nature of data architectures for notions of reflexivity and actorhood; and their consequences for theories of practice, including accounting practice.

Reflexive actorhood at risk?

According to Zuboff, beneath the exchanges of free persons on social media lie mechanisms to harvest data about them for profit, data which are based on traces of bodily movements, such as keystrokes, eye movements, clicks and paces. Devices for the extraction of bodily traces for security and health purposes are not new – fingerprinting and blood pressure measurement devices to name but two. In-house data architectures and related analytics are the organizational form of this extractive process, embodying an advisor-fuelled ambition to realize the ‘data driven’ organization. Whereas accounting studies have focused on within-organization processes of self-formation in the face of managerial and accounting systems, less attention has been paid to how such organizational processes, in conjunction with digitized social media and other services, flow into, and constitute, the ‘private’ realm. In short, platformization and cyborgization put at risk the very notion of ‘reflexivity’ itself, as a fundamental human capacity and condition of political participation.

Developing a history of reflexivity and its centrality to concepts of self and actorhood would be a considerable task. Put simplistically, it originates in a, now discredited, Platonic-Cartesian notion of interiority. That this interiority is complex and cannot be equated with a realm of private freedom has been known at least since Marx and Freud, but the concept of the ‘inner’ nevertheless resists full deconstruction and underwrites reflexivity as a defining capability of what it is to be human, deliberative and responsible. Reflexivity and interiority are at risk in a world of data architectures as implied in Zuboff’s (2015, pp. 83–4) notion of ‘psychic numbness’. Such numbness can be theorized as the antithesis of reflexivity, in part as the condition of human bodies which is produced when experience is digitally extracted. The self becomes a ‘cyborg-self’ constituted by vectors of digital pattern recognition; it experiences a reality and sociality which is coextensive with being tracked and traced (Fourcade & Johns, 2020; Stiegler, 2018). Zuboff thereby posits a world in which the ‘backstage’ of human intimacy and interiority shrinks in the face of digitally constructed personalization and profiling which require continuous maintenance. This is a world of no exit in which reflexive interiority as a longstanding presumption of human actorhood is at risk, notwithstanding reactive efforts to mitigate this risk in the form of a ‘politics of interiority’ (Ball, 2005).

That humans are embedded in organizational apparatuses of machines, books and records and many other material artefacts, which enable and constrain possibilities for actorhood and structure routines, is already well established (Smith, 2001). These sociomaterial sensibilities were always implicit in accounting and organizational studies drawing on the work of Foucault and the notion of self as produced by distributed power relations (Raffnsøe, Mennicken, & Miller, 2019). However, when human experience and related sense-making are themselves derived from digital traces extracted from bodily movements and actions, even the concepts of sociomateriality and ‘internalization’ may be inadequate for theorizing the cyborg-like effects of data architectures and how they shape human sense-making. Such architectures generate facticities of performance and sociability which are not so much ‘disconnected’ from lived experience and lifeworlds – the romantic dualism of critical theorists like Marcuse and Habermas – but reconstitute and ground them in platforms. This emptying out of traditional forms of sociality – the creation of an automated social order (Fourcade & Johns, 2020; Stiegler, 2018) – in the face of technology is not a new concern (e.g. Knorr Cetina, 2001), but it marks a potential break with the terms of the audit society thesis. Accounting as sociomaterial practice has been shown to be a source of subjectification. But if we follow Zuboff, data architectures as the capillaries of surveillance capitalism have a more ambitious object, namely the entirety of human experience. The intensity and capacity of emerging data architectures and their performativity provoke a possible inversion of the idea of sociomateriality itself, namely in the form of a cyborg-centred re-reading of it as materiosociality. Clues for this conception of materiosociality can be found in the work of Simondon (2020) who radicalizes the sociomaterial agenda by proposing that individuals are fundamentally and nothing more than the outcomes of material processes, particularly technological, which individuate and generate relations, including reflexivity as an internal relation of self to self, from a ‘pre-individual’ reality. Cyborgization is ‘simply’ the technological acceleration of this biological process.

A cyborg turn in practice theory?

The scale and scope of Zuboff’s thesis, and the potential platformization of organizations as data-driven entities, may also require us to rethink the human-language centred starting point of practice theories, which reach back to the later Wittgenstein (Schatzki, 1996) and to American pragmatists like Dewey. Even the very notion of ‘surveillance’ in surveillance capitalism contains residues of the necessity of a human-centric agency of some kind – the state, the police, Google. But is this adequate to grasp the situation that human observers of an accounting system are giving way to ‘delegated’ algorithmic observers (Alaimo & Kallinikos, 2020; Glaser et al., 2021)? Emerging work on the power of algorithms and its significance for the labour process in different settings is opening up a post-human practice agenda (Kellogg et al., 2020; Newlands, 2021). Practice theories must evolve to deal with the digitized routines of behaviour modification described above. The smart self-executing contract has the superficial form of contractualism but not the underlying reciprocity as we have known it for centuries (Zuboff, 2015). The question is whether ‘smart practice’ like this is any kind of practice at all once we have evacuated human judgement, meaning, negotiation and reflexivity from it?

The challenging theoretical inflection point is this: how far can we conceptually displace the human in theorizing practice using the dystopian vocabularies of cyborgization and materiosociality? Humans and technology may be ‘conjoined’ agencies (Murray, Rhymer, & Sirmon, 2021), but the ‘programmed intentionality’ of algorithms for data extraction and related analytic processes potentially decentres humans in a new form of proletarianization which leaves only a few with elite roles as designers, programmers and analysts. And, in an extreme move of theoretical inversion, if humans are just ‘dividuated’ action patterns (Stiegler, 2018) (namely, digitally fragmented, non-unitary and distributed selves) must we transpose the analytic vocabulary of sense-making, organizational routine and disposition to the algorithms themselves?

These questions verge on science fiction but they challenge us to find new ways to theorize the post-social organizing processes which constitute surveillance capitalism. We can no longer smuggle ‘actorhood’ into our accounts of practice when it is subservient to the power of what Zuboff calls ‘instrumentarianism’. And what kind of ‘practice’ theory could this be when the very possibility of observing, or auditing, such algorithmic ‘practice’ requires another extractive programme to do so? Practice as we ordinarily try to understand it begins in, and is grounded in, human experience – a central phenomenological insight and a resource for critics of the audit society. Yet now we seem to need a phenomenology of the digital to begin to unpick the new materiosociality of accounting practice. This is much more than a call for the methodological symmetry of humans and non-humans that is the hallmark of actor-network theory (Latour, 2005). It is to recognize that practice theories may reach the limits of their theoretical adequacy under conditions of surveillance capitalism and need to take a ‘cyborg turn’, a turn which requires us to take seriously the seemingly crazy question, namely, ‘How do platforms experience humans?’

Inflection Point 3: Accountics as a Post-Social Social Science

The third theoretical inflection point concerns the influence of digitalization and the growth of data architectures on academic disciplines and what counts as knowledge more generally. Drawing on accounting research as an exemplar, I propose that the social sciences are becoming increasingly symbiotic with the expansion of data-driven architectures and the logic of surveillance capitalism more generally.

Developments in ‘empirical’ accounting research have followed the quantitative expansion in social sciences which occurred from the 1960s onwards (Miller & Power, 2013). Drawing from economics and econometrics, this research tradition utilizes large ‘datasets’, originally available in the form of daily stock price movements and corporate governance variables. Broadly speaking the purpose is to investigate statistical patterns of association and influence on and by accounting numbers. The explosion of data via the digital tagging and tracking of both the corporate and the intimate everyday expands the universe of the dataset and also encroaches on research traditions which are more experiential, involving immersion in the field and close attention to accounting practices and routines as processes. This everyday domain of meaning-saturated practice-fields has generally been regarded as too subjective, idiosyncratic and ‘unknowable’ by quantitatively trained accounting researchers whose sense of the ‘empirical’ is operationally bounded by the availability of data that is amenable to theoretical construction, manipulation and econometric analysis. Yet, under conditions of surveillance capitalism, this subjective and intimate world of meanings is now itself becoming extractable in digitally readable form, and thereby also ‘knowable’ via formal methods (Zuboff, 2015, p. 81).

There is considerable excitement and enthusiasm for the new reach of this data explosion and the opportunities for research which big data offers. Yet, it marks a shift in the nature of knowledge in accounting, management and organization studies, and most likely the social sciences in general. A formative dynamic is creating an increasingly tight fit between what counts as research practice, digitized datasets and acceptable method. In effect social science may become an ‘operational’ discipline, a ‘computational social science’ (Ruppert, Law, & Savage, 2013, p. 29) whose emergent purpose is to fine-tune surveillance capitalism. This digital constitution of ‘post-social social science’ is a constitutive feature of surveillance capitalism. It takes the form of a science oriented towards the production of non-humanist accounts of the social grounded in digital methods for tracing, tracking and mapping actions. Indeed, the social group as a unit of analysis is now derived inductively by algorithms and social scientists become data analysts (Ruppert et al., 2013, pp. 37–8).

Lyotard’s (1984) provocative essay on the condition of knowledge speaks to these developments. He draws attention to the rise of what he calls the ‘informatic’ sciences in which truth is replaced by values of performativity and impact. His ideas are consistent with Mirowski’s (2002) identification of the cybernetic, and therefore post-social, dream at the heart of the formation of modern economics. The digital revolution arguably provides the mechanism for the radicalization and realization of ‘machine dreams’ (Evangelista, 2019; Hayles, 2008; Mirowski, 2002; Zuboff, 2015, p. 81) in which behavioural data provides the informational feedback for system control and ultimately profit. Thus a new form of data positivism in social science is emerging which underpins the processes of platformization and cyborgization discussed earlier. Whatever aspects of the ‘social’ are not digitally captured are relegated to non-knowledge, without economic value. They concern the merely human. Thus the same process by which contextual knowledge of gig workers’ performance is effaced (Newlands, 2021) also drives a post-social social science in which truth is internal to datasets and their patterns.

This trend points towards the increased routinization and legitimation of management and organization studies around data in digital form. The research process no longer presupposes or requires reflective human actors to complete questionnaires (Ruppert et al., 2013). The explosion of data and its influence over the attention of social scientists may steadily erode the hermeneutical tension between that which appears as data and our claims to knowledge, a tension which provides the impulse for theorizing the empirical world of appearances. Indeed, while machine-learning is promoted as a supplement to theorizing (Leavitt, Schabram, Hariharan, & Barnes, 2020), there is also a risk that theory is reduced to the exploration of postulated relationships between different ‘regions’ of data, and to repeated econometric refinements of the robustness of these relations. Stiegler (2018) describes this as the ‘proletarianization of theory’.

Accounting as an academic discipline is caught up in this broad shift. Like law, it sits uneasily between a practice-oriented pedagogy on the one hand and a social scientific orientation drawing on economics on the other. Indeed, the ‘gap’ between these two faces of accounting academia has been periodically problematized by practitioners who deride the practical irrelevance of most accounting research. However, the rise of accounting data architectures and related analytics at the organization level is dissolving this gap. I recover the notion of ‘accountics’ to refer to an academic discipline defined by the increasingly tight fit between organizational accounting and the ‘social’ science of that accounting. My usage builds on Charles Sprague’s original formulation of accountics as the ‘mathematical science of accounting values’ (Sprague, 1922; McMillan, 1998; Suzuki, 2007). To survive in an increasingly data-scientized business school environment, academic accounting is becoming ‘accountics’, a core ‘cyborg science’ by which surveillance capitalism can induct its operatives and regulate itself.

As noted already, Alaimo and Kallinikos (2020) argue that the very ontology of organizations is becoming recursively constituted via the categories of data architectures, categories produced by algorithms. The distinction between technology and organization is collapsing. But we can push their argument even further in epistemological terms. Accounting systems in organizations and the accounting research process itself are becoming convergent modes of knowledge as researchers and researched organizations commonly participate in data-centred apparatuses. ‘Accountics’ is becoming a research arm of surveillance capitalism. It draws from an ‘algorithmic culture’ (Dourish, 2016; Glaser et al., 2021) to find and define its empirical material, is diffused in curriculum design – there has been an explosion of ‘accounting and data science’ courses in recent years – and generates reputational capital for its scholars in research journals. This is the very antithesis, and termination, of neoromantic conceptions of academic autonomy and vocation (Shaffer, 1990).

From Audit Society to the Economy of Traces: A Critical Agenda

The tone of the analysis of these three inflection points may seem to be too dystopian and pessimistic, the stuff of science fiction. Empirical studies document the many ways in which humans react to, resist and manipulate processes of data extraction and other technology intrusions into work and non-work settings. Organizations, and even totalitarian states, are less omniscient than critics presume. These hesitations re-implicate the possibility of reflexive subjects operating in tension with data-driven architectures, reasserting both privacy and judgement. Zuboff’s own critique is an example of this very possibility. All of which is to say that ‘surveillance capitalism’ is not yet a self-executing programme, even though this is its animating dream. The implied totalizing formative processes of surveillance capitalism are likely to require continual maintenance and renewal and should not be overstated.

Notwithstanding these limitations of the reach of the surveillance capitalism thesis, Zuboff’s analysis is an important challenge to the theoretical adequacy of accounting and of management and organization studies. As noted earlier, the question of theoretical ‘adequacy’ is not precise. It allows for some looseness of fit, some reductive simplifications, and some tension between phenomena and theory. But adequacy becomes problematic when theory loses tractability in the face of new phenomena. This problematization of theoretical adequacy is captured by the notion of an ‘inflection point’ in which the implicit ways of conceptualizing phenomena which inform observation are at stake (Swedberg, 2014). For example, surveillance capitalism is clearly a point of inflection for political theorists who had always assumed a tight association between liberal democracies and market systems.

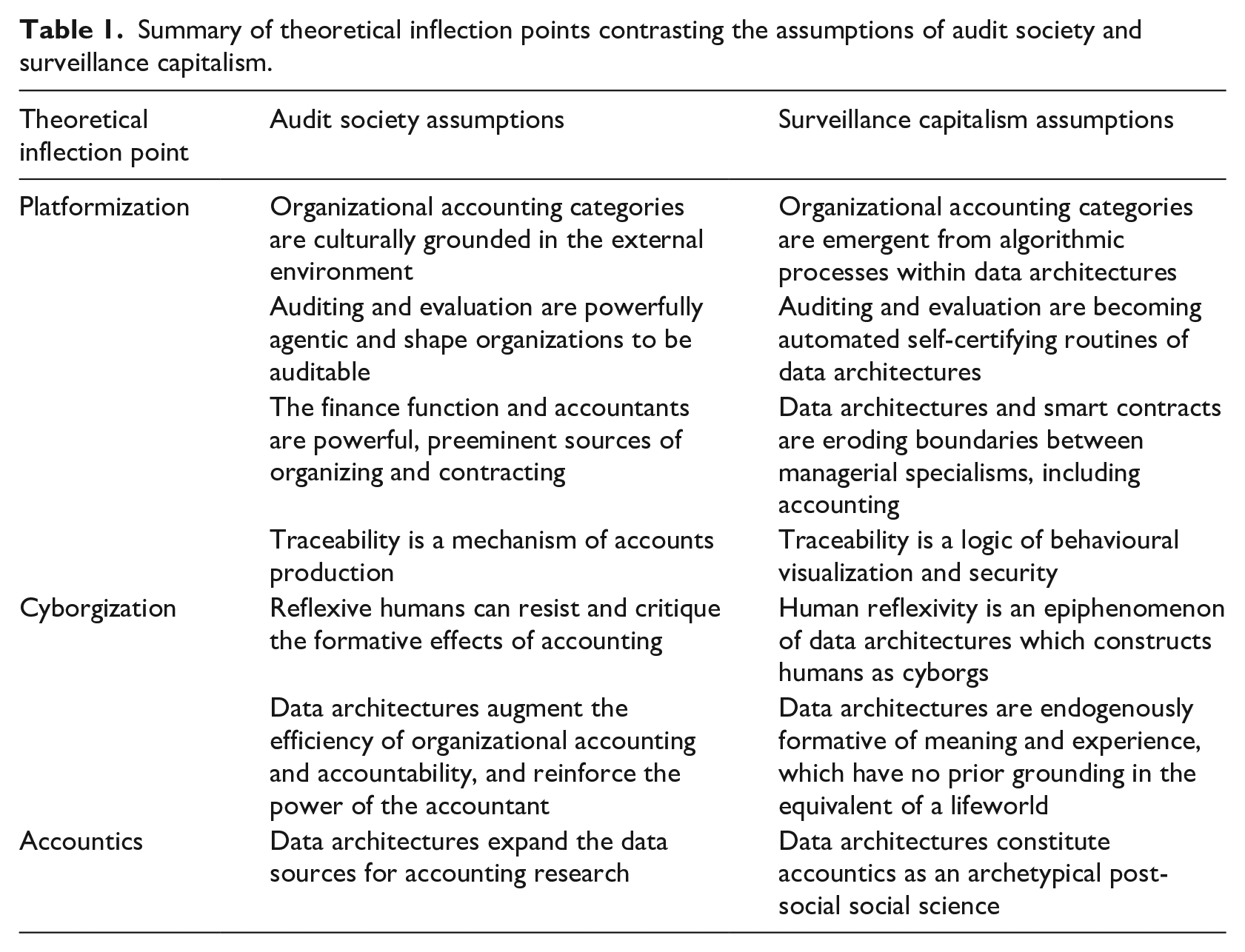

Three closely related theoretical inflection points have been developed which jointly suggest a need to re-engineer the theorization of audit society to be more adequate to the conditions of surveillance capitalism. In Table 1 I summarize the discussion of these inflection points by contrasting the respective assumptions underpinning the concepts of audit society and surveillance capitalism.

Summary of theoretical inflection points contrasting the assumptions of audit society and surveillance capitalism.

Surveillance capitalism as Zuboff articulates it marks a break with the contractualist underpinnings of audit society and the institutionalized asymmetry of principals and agents which drives monitoring and evaluation practices. The historically grounded structural independence of the ‘firm’ from its populations became the source of this ‘agency’ problem, and was solved by juridical-contractual forms of reciprocity, including audits. This model is broken under conditions of surveillance capitalism. It is as if Coase’s neoliberal theory of organizations as a nexus of durable contractual forms must give way to a conception of organizations as platform-entities, generating ‘surveillance assets’ from co-opted traces. Whatever asymmetries of power existed in prior contractual forms, it is argued that these are magnified by data extraction processes which are indifferent to consent (Zuboff, 2015). Thus the myth of transparency, grounded in Enlightenment ideals (Christensen & Cornelissen, 2015), which has mobilized the expansion of accounting and auditing, is being reductively and operationally reconstructed as ‘traceability’ within data architectures.

I suggest that we can theorize the process of ‘platformization’ as one in which accounting categories are an algorithmically produced effect of data architectures and not a cultural input; in which auditing and evaluation are primarily internal, not external, to such data architectures; in which the power of accounting as a logic of organizing is being eroded; and in which traceability is no longer a means of accounts production but of platform and organizational security. Where the old accounting problem was that of informing decision-making under conditions of uncertainty, the dream of accounting in the world of surveillance capitalism is the production of certainty and knowledge of everything. And, as data architectures increasingly blend accounting, information systems and surveillance practices, the very category of ‘accounting’ is itself a fragile marker of what is at stake in this ‘economy of traces’ (Stiegler, 2018, chapter 2).

And yet, I also suggest that the principal–agent problem of accountability is far from being effaced; accounting is needed more than ever to hold these platformizing tendencies to account. Critics of audit society overlook this potential by focusing only on the pathologies of accounting and the urge to quantify. I suggest that the theoretical inflection point between audit society and the platform society of surveillance capitalism also requires a normative turn towards the value-enhancing role of accounting and its latent capacity to infuse organizations and data architectures with values (Selznick, 1957). There is evidence that this normative re-evaluation of accounting is under way in the form of critical ‘counter-accounts’ like Zuboff’s own, and is visible in experiments with different metrics of performance, not just financial (Gallhofer, Haslam, Monk, & Roberts, 2006; Vinnari & Laine, 2017).

The second inflection point concerns the adequacy of prevailing theories of self-formation under conditions of surveillance capitalism. Human bodily encounters and interfaces with varied and increasingly precise forms of data extraction, which underpin performance and reputational metrics spanning work and non-work, suggest a need to re-centre cyborg models of human agency. The cyborg is no longer an exotic metaphor; it names the fragility of our deepest presumptions of reflexivity. It also provokes theoretical and empirical attention to Zuboff’s notion of psychic numbness and to new modes of politicized performance, such as ‘social credit’, and finely calibrated forms of personalization which efface the interior spaces of the real (Ball, 2009; Stiegler, 2018; Zuboff, 2019, p. 471). A digital turn in practice theory requires the rethinking of, for example, human-centred notions of sense-making and the repositioning of the ‘intentionality’ of non-human ‘actors’ such as algorithms (Fourcade & Johns, 2020; Glaser et al., 2021). Latour’s methodological injunction to treat human and non-human agencies symmetrically lays the groundwork for this machine-based theorization of practice.

Cyborgization is not new. Many scholars today take for granted reductive means–end models of human rationality and agency. Such models were able to ground economics and the decision sciences precisely because of their cyborg character (Mirowski, 2002). I propose that the study of cyborgization processes should become more central to the critical accounting agenda. As noted above, accounting and ‘counter accounts’ have a role to play in identifying organizational and social sources of psychic numbing by focusing on the materiosociality of platforms (cf. Barad, 2003) and specifically on how the dynamics of trace extraction and processing is formative of ‘dividuated’ selves.

Cyborgization is not only a tendency of organizing, but also of scholarship – the third inflection point implicated by Zuboff’s analysis of surveillance capitalism. There is an emerging symbiosis between modes of organizational and societal control, and with the nature of social scientific knowledge itself. Such a power-knowledge apparatus is familiar to accounting and organization scholars who have been inspired by the work of Foucault. What Foucault elliptically calls the ‘sciences of the human’ and their methods have their origins in projects of control (Ruppert et al., 2013). Yet, however variably we may understand the historical circuits by which social science is connected to the worlds of its applications, these circuits become tighter and narrower when academics form dependencies on data architectures which define the limits of the empirical and of what can be said. In this world, the conditions of possibility for Methodenstreiten have simply been removed by the explosion of data in digital form.

I have borrowed and re-purposed the term ‘accountics’ as a placeholder concept for this mutually reinforcing relationship between organizational control and a social science of accounting in the service of surveillance capitalism. While this tight fit has long been a dream of the control-oriented academic disciplines, most explicitly in cybernetics itself, Zuboff shows us that the digital conditions for the realization of this dream now exist. If the trajectory is increasingly towards ‘post social’ social science, I suggest the need for a new but recalibrated Methodenstreit and the acceleration of critical studies of digitalization. What is at stake is not a new form of the ‘two cultures’ problem of science and humanities, but a new kind of conflict which is epitomized by the difference between accounting and accountics, between the digital augmentation of accountability and the digital constitution of our knowledge of reality (Raisch & Krakowski, 2021).

We should remind ourselves that the terrain of surveillance capitalism and its organizational effects are familiar to an older body of critical theorizing. In an important sense, the problem of post-humanism in the face of technology has a long history. For example, Marcuse (1986) had argued that the triumph of positivism resulted in ‘one-dimensional thinking’ that only the therapy of critique could break. Similarly, Habermas (1977) famously drew attention to the impact of technological progress on possibilities for practical and political reflection. For Habermas and other members of the Frankfurt School, the German university in the 1960s was a battleground between administrative positivism and teacher–pupil Bildung. The latter could no longer be romantically grounded and detached from society, but needed to engage in it, and be critical of itself. Both Marcuse and Habermas would therefore readily recognize the contours of surveillance capitalism. Indeed, Zuboff’s notion of ‘instrumentarian’ power corresponds closely to their older category of ‘technical reason’, and surveillance capitalism is the digital apotheosis of technology tendencies that they had already identified in the 1960s. In the twenty-first century, social struggle is already platformized (Fourcade & Johns, 2020) and the threat of administrative positivism exists both in the continuing normative elevation of the data-based sciences beyond their augmentative advantages, and also in the cyborgization of education. Whereas earlier critical theorists took as their object the ‘falsity’ of the consent of populations to the prevailing order of things, Zuboff posits a world in which even the pretence of consent has disappeared in the face of digitally taggable and extractable habits. In the end, digitally grounded positivism is still positivism.

Notwithstanding these critical theoretical affinities which span half a century, the vocabularies of Frankfurt School critique – instrumental reason, science and technology, and one-dimensionality – are somewhat blunt conceptual tools with which to unlock organizational worlds subject to surveillance capitalism. If data is now the fundamental building block of organizational and social life (Alaimo & Kallinikos, 2020), then the terms of theory and critique must also evolve. Hence, I have highlighted and tried to recover and repurpose notions of platformization, cyborgization and accountics as disruptive placeholders for theorizing the processes which constitute a data-driven organizational world.

An important focus for future work on these processes should be the trace as a unit of analysis and traceability as an organizational and societal value (Power, 2019). In essence, this essay is an extended case for renewing the audit society agenda but now as a critical traceology which re-focuses theory and observation on the digital/non-digital interface. If the audit society is not dead but is newly intensified as an economy of traces underpinning surveillance capitalism, we require more studies of how traces of things and human actions are produced within data architectures and how they recursively construct the human and the social (Power, 2021). It is also at the level of these traces – the primary datafication of human experience – that the accumulative character of surveillance capitalism operates and can be made visible. Attention to trace-making will not only help us to better understand how surveillance assets are generated but it will also reveal how the control logic of the audit society is mutating under conditions of datafication. Traces are not new objects of interest as studies in archaeology and anthropology demonstrate. But the acceleration of datafication, and the enormity of its implications, which Zuboff has brought to our attention, requires new critical approaches to them and to the manner in which traceability is reconstituting governance and accountability.

In conclusion, the preceding arguments are a provocation, in conversation with the work of Zuboff, Flyverbom and many others, to rethink ways of seeing accounting and organizations, and to reconstruct and reinvigorate the audit society thesis as a source of critical theorizing about traces and trace-making. It is undoubtedly empirically far-fetched to suggest that humans under conditions of surveillance capitalism are literally cyborgs, but it is theoretically generative to see them ‘as if’ they are, just as many decades earlier it was theoretically fruitful, and really not so different, for social science to see humans as if they were rational actors. Such ‘as if’ thought experiments are a source of continuous theoretical innovation in many disciplines (Kornberger & Mantere, 2020). The question for theoretical renewal is not whether and how a reflexive self escapes the totalizing orbit of the ‘digitization of everything’. Rather, the task is to develop a critical traceology to understand the subtle capillaries which constitute and colonize this reflexivity, and to develop more fine-tuned conceptualizations appropriate to organizational and social environments pervaded by data. Accordingly, I have proposed a post-human theoretical lexicon to energize critical theorization of how surveillance capitalism operates at the organizational level. As a final point, we must also remember that theoretical adequacy goes hand in hand with empirical capability. There will need to be careful observation of traces in all their variety – digital and otherwise – if we are to understand how they perform people, organizations and societies.

Footnotes

Acknowledgements

The author is grateful for the advice and comments of Per Ahblom, Cristina Alaimo, Joep Cornelissen, Markus Höllerer, Jannis Kallinikos, Finia Kuhlmann, Nadia Matringe, Andrea Mennicken, Peter Miller, Jeremy Morales, Julia Morley and Tommaso Palermo.

Correction (February 2023):

This article has been updated with minor corrections since its original publication.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.