Abstract

The article is concerned with the relationship between foreign direct investment (FDI) flows and exports and asks if these two flows are substitutes or complement each other. Empirical work in this area employing industry- or country-level data has generally found a positive or complementary relationship between exports and FDI. Our empirical strategy is different in that we try to throw some light on the issue of substitution versus complementarity between FDI and exports by carrying out econometric analyses directed at assessing how India’s mass termination of bilateral investment treaties (BITs) in March 2017 and such BIT terminations during September–December 2016 and April 2017 to December 2018 impacted India’s FDI inflows and imports. Our finding of a significant negative effect of BIT termination on FDI inflows, corroborating the findings of two earlier studies and the finding of a significant positive impact of BIT termination of India’s imports is conceivably reconcilable only if there is a substitution relationship between FDI and exports. Hence, we find some empirical evidence of a substitution relationship between FDI and exports—at least, this has been the relationship between India’s inflow of FDI and the inflow of goods as imports, if not valid for other countries.

Keywords

Introduction

Firms have several options for internationalising, the most common being exporting, licensing and franchising, partnering and strategic alliances, joint ventures, mergers and acquisitions, or setting up a wholly owned subsidiary. The last four are classified as foreign direct investment (FDI) and are commonly known as the equity mode of market entry. The other options are generally the non-equity mode of market entry. 1 Since (i) exports to a destination country and (ii) equity mode of entering the markets of that country are conceptually alternative options for a firm, one would expect a substitution relationship to arise between the two. This expected relationship is, however, not substantiated by the literature, and in several empirical studies, a complementary relationship, rather than a substitution relationship, between exports and FDI has been found (as discussed later).

This article concerns the relationship between FDI flows and exports from a source country to a destination. The question asked is: Are these two flows (one of equity and the other of goods) substitutes, or do they complement each other? We begin the article with a review of the literature. This literature survey helps us take stock of our current understanding of the subject. In the next step, we provide empirical evidence on the relationship between FDI and exports using data from India. The novelty of our analysis, in contrast to the analysis undertaken in the past, is that we use the fact that India terminated many of her Bilateral Investment Treaties (BITs) during 2016–2018. We assert that if the exports of different countries to India (i.e., India’s imports) bear a substitution relationship with their FDI flows to India, then the termination of BITs should lower FDI flows to India but have a positive effect on exports to India, i.e., on India’s imports. On the other hand, if there is a complementary relationship between exports and FDI, then the termination of BITS will cause both exports and FDI to go down. This is the empirical approach adopted in the paper to throw light on the nature of the relationship existing between exports and FDI.

Until 2015, India had signed BITs with 83 countries, and 74 were in force then. For certain reasons, a need arose to terminate and renegotiate the BITs (for a discussion, see Hartmann & Spruk, 2023; Kotyrlo & Kalachyhin, 2023). India developed a new model BIT in 2015. In March 2017, India carried out a unilateral mass termination of her BITs. In two cases, BIT termination occurred during the third quarter of 2016, and in several other cases, it occurred between April 2017 and December 2018. The econometric analyses carried out by Hartmann and Spruk (2023) and Kotyrlo and Kalachyhin (2023) have established that India’s termination of BITs led to a significant fall in the inflow of FDI in India. The results of Kotyrlo and Kalachyhin (2023) indicate about a 60% fall in India’s inward FDI quarterly on average. From their analysis, Hartmann and Spruk (2023) have found a significant reduction in FDI inflows to India in response to BIT terminations by over 30% compared to countries without terminations. Since the occurrence of an adverse effect of BIT termination by India on her FDI inflows is well established by the results of the analysis of Hartmann and Spruk (2023) and Kotyrlo and Kalachyhin (2023), in this article, we look mainly at the effect of the termination of BITs on India’s imports, investigating whether there was a positive effect or a negative effect—indicating a substitution relationship or a complementary relationship with FDI. We also examine the impact of BIT termination on FDI inflows to verify the findings of Hartmann and Spruk (2023) and Kotyrlo and Kalachyhin (2023).

If exports and FDI have nothing to do with each other, then the termination of BITs, which directly affects foreign investment, may impact India’s FDI inflows, but it should not affect India’s imports. One may argue that a substantial part of global trade is intra-firm trade. Hence, the termination of BITs will adversely impact India’s imports since the flows of foreign equity investment in India will go down without BITs, resulting in imports made by the FDI firms in India going down. We, however, find a significant positive effect of BIT termination of India’s imports from the econometric analysis we have undertaken (presented later in the paper), whose probable explanation lies in a substitution relationship between FDI and exports—at least this has been the relationship between India’s inflow of FDI and inflow of goods as imports, if not valid for other countries.

The empirical analysis revealing a positive effect of India’s BIT termination on her imports is presented in Sections 3, 4 and 5. Before that, we review the literature in the next section to gain an understanding of what the existing studies tell us about the relationship between FDI and exports. We consider both theoretical literature and empirical literature. Section 6 summarises and concludes.

Exports and FDI: Nature of Relationship

Theoretical Issues

FDI and exports have been well highlighted as the important modes of internationalisation of firms in international trade and investment literature, where internationalisation is the process leading to increasing involvement of enterprises in international markets. While trade has been the dominant economic channel integrating nations, foreign investments have started gaining importance since the 1960s. The 1960s saw a significant technological change, which coincided with the rise of multinational corporations. The then-existing theories were found to be inadequate for explaining the changing pattern of international trade and investments. Since then, several attempts have been made to integrate the FDI theory with the international trade theory.

In fact, the expansion of FDI in the past several decades and the continuous growth in the output of multinational firms have changed the structure of international trade to a large extent. By some measures, FDI has become even more important than international trade (Graham, 1996; Helpman et al., 2004). Based on these observations, a related thought-provoking question is whether ODFI (outward FDI) and exports are complements or substitutes. The relationship between outward foreign direct investment (OFDI) and exports has been the subject of many theoretical and empirical studies since the 1970s. In the theoretical literature on the subject, the effect of OFDI on exports can be either positive (OFDI and exports are complements) or negative (OFDI and exports are substitutes).

The empirical evidence on the complementarity-versus-substitution relationship between OFDI and exports is mixed. From the point of view of policymakers, if FDI is undertaken abroad as a substitute for exports, then the effects would be twofold: first, it would divert domestic investible resources to channels other than the home country, and second, it would have a negative effect on balance-of-payments through reduced foreign exchange earnings. On the other hand, if FDI outflows lead to increased exports through forward and backward linkages in the production process, then such a complementary relationship will boost domestic investment and contribute to the economy’s growth through increases in foreign exchange reserves. From an MNE’s point of view, where OFDI acts as a substitute for exports, it implies that the foreign market is growing, and, hence, a large-scale production facility is now justified (Bhasin & Paul, 2016).

If we consider the vast literature on the relationship between FDI and exports, we find that it has been established in various studies that home-country firms have a positive synergy between exports and FDI to a foreign country. As Johanson and Vahlne (1977) demonstrated in their internationalisation model, firms move sequentially while pursuing internationalisation strategies. The first step towards internationalisation is exporting to a host country. As firms carry exports to the country, they gradually become familiar with the host country’s economic, political, social and cultural systems. Accordingly, they adapt their future strategies to adequately meet foreign consumers’ demands. Such firms are better placed to organise and carry out production activities in the host country than inexperienced firms. Hence, in a way, trade paves the way for outward FDI for exporting firms from the home country. Further, a firm may also establish marketing and distribution channels to strengthen trading activities in the host country.

Along similar lines, according to Vernon’s (1966) product life cycle (PLC) theory, a firm would normally start its international operations by ‘exporting’ as a mode of entry, as it is less risky and less costly. Only when the demand in the host country is large enough to warrant substantial investment in production, the firm would consider undertaking FDI as an alternative to exports. However, as Cantwell and Narula (2001) mentioned, firms in certain sectors may skip exporting altogether and proceed directly to FDI. Substitution between them also arises if intangible assets specific to the firm, such as technology and managerial skills, may induce a firm to operate production facilities abroad rather than export. It is often difficult to appropriate rents properly from such assets via contact with a third party, which induces the firm to establish its facilities abroad. FDI also replaces trade when there are high costs of external transactions such as exporting or licensing. 2

Another aspect of the relationship under discussion is the impact on home-country exports once OFDI is undertaken. If the home-country firms offer competitive advantages in the production cycle, it implies benefits to the MNE through forward and backward linkages with firms in its home country. For example, if the home country is a source of cheap raw materials, it would help the MNE through backward linkage in production. In such cases, OFDI and exports share a complementary relationship. We also expect a complementary effect to arise when a firm’s production presence in a foreign market with one product may increase the total demand for all its products. For instance, the presence itself may increase the firm’s knowledge about the market and, thus, help tilt consumer preferences in the firm’s favour. Furthermore, recent empirical evidence reveals that almost half of trade flows are parent-to-affiliate input trade. This may imply that foreign affiliate activities may increase exports of inputs from home countries to the host market.

An interesting idea to which attention needs to be drawn is that the relationship between FDI and exports may change with the level of economic development. In a notable study, Liu et al. (2016) propose a pendulum gravity model of OFDI and exports and find empirical evidence of a complementary association between overseas investments and exports from the home country for countries in their initial stages of overseas investments and a substitutionary association for countries in the matured overseas investments stage. An analysis of panel data of exports and outward FDI flows from China to OECD countries shows a complementary relationship between OFDI and exports. On the other hand, in the case of OECD economies, outward FDI substitutes exports to China. A similar pattern is seen in the panel data on exports and outward FDI flows from the United States to developing countries and vice versa.

Empirical Studies Undertaken in the Context of Developed Countries

A complementary relationship between OFDI and trade has been found in the studies by Swedenborg (1979), Lipsey and Weiss (1981, 1984), Blomstrom et al. (1988), Grubert and Mutti (1991), Graham (1996), Pfaffermayr (1996), Clausing (2000), Lipsey et al. (2000), Head and Ries (2001) and Lipsey and Ramstetter (2003) (see Table 1, which covers some of the studies). 3

Nature of Relationship Between Exports and OFDI: Summary of Developed Country Studies.

Nature of Relationship Between Exports and OFDI: Summary of Developed Country Studies.

To discuss the findings of some other studies undertaken in the context of developed countries, Maza and Gutiérrez-Portilla (2022) examine the link between OFDI and exports using Spain’s FDI flows to the top 50 recipient countries over the period 1995–2019. They find that OFDI had a significant positive effect on exports in the long term, but it is exclusively due to spatial dependence. Mullen and Williams (2011) employed a gravity-type empirical specification to examine the impact of Canada’s inward and outward FDI on exports to OECD countries. They found that outward FDI merely displaces exports, but inward FDI strongly promotes intra-firm export growth. For the EU, Martínez et al. (2012) have found that EU commercial integration and FDI reinforce each other. Thus, these are complements rather than substitutes in Europe. This effect is apparent for the intra-EU FDI. This is also seen for investment coming from countries outside the EU. Africano and Magalhães (2005) reported similar findings from their investigation of the relation between the FDI stock and the geographical pattern of trade flows in the Portuguese economy.

A recent study focusing on Central and Eastern Europe, undertaken by Albulescu and Goyeau (2019), has examined the relationship between FDI and exports within the Visegrad Group countries (four central European countries) and found that bilateral FDI outflow favours imports and exports. In another recent empirical study, Voica et al. (2021) have found evidence of a complementary relationship between FDI and trade. They considered the EU countries.

Using French firm-level data over 2002 to 2009, Bricongne et al. (2023) show that whether FDI and exports are complements or substitutes depends on whether the product belongs to the core competency of the firm and the size of demand in the destination market. The study reports evidence of the substitutability predicted by standard horizontal FDI models, taking place only for the firm’s best-performing products and in high-demand markets. On the other hand, vertical linkages and proximity advantages related to FDI’s foreign presence generate exports of intermediates and products that are further away from the firm’s core competency. This complementarity neutralises the substitutability when aggregating the firm’s products, resulting in an average null net effect of FDI on exports in high-demand countries.

Camarero et al. (2020) examine the determinants of German outward FDI in Latin America and Asia from 1996 to 2012. Their findings suggest that determinants associated with horizontal and vertical FDI motivations coexisted overall. However, the dominant internationalisation strategy differed among these regions. In Asia, the state played a key role in the industrialisation strategy, promoting an upgrading process that tended to substitute horizontal foreign investment, while in Latin America, the firms were the main actors through vertical integration value chains. These findings suggest that, whereas German MNEs accessing Latin American markets predominantly sought lower production costs by undertaking vertical FDI, German FDI was mainly market-seeking in Asia. It appears, therefore, that while FDI in one region may substitute exports, it may bear a complementary relationship in another.

Martin (2010) provides insights into the dynamics of exports and OFDI flows in Spain using a multivariate cointegrated model (VECM). The results provide evidence of a positive (Granger) causality relationship running from FDI to exports of goods (strong) and to exports of services (weak) in the long run, the complementarity relation of which is consistent with vertical FDI strategies.

Kim and Rang (1997) examined the relationship between OFDI (outward FDI) of South Korea and Japan and their exports. They found that OFDI did not impact exports in those countries. Lin (1995) found that Taiwan’s outward FDI significantly positively affects exports to and imports from the host country. Lim and Moon (2001) asserted that OFDI would positively affect home-country exports if the foreign subsidiaries were located in less-developed countries or were relatively new and in a declining home industry. Aizenman and Noy (2006) investigated the intertemporal linkages between FDI and disaggregated international trade measures using a sample of 81 countries (including industrialised and developing countries) for the years 1982–1998. They found that the most robust linkage between the sub-accounts is between FDI and trade in the manufacturing sector.

Kim and Lee (2014) studied the interaction between trade and FDI from South Korea to India and found a unidirectional link between trade and FDI, but not vice versa. They found that exports of South Korea to India positively affect the growth of the outward FDI of South Korea into India. Lee et al. (2009) found that FDI outflows to less-developed large economies like China could decrease exports for small source countries, implying a substitution relationship. Furthermore, Goldberg and Klein (1999), while examining the relationship between trade and FDI using data on bilateral capital and trade flows between the United States and individual Latin American countries, found mixed results indicating that OFDI had both substitution and complementary effects on manufacturing trade.

Bouras and Raggad (2015) have found complementary relationships between total exports and total FDI, manufacturing exports and FDI, and non-manufacturing exports and FDI, focusing on ten developing and non-developing countries from 1988 to 2012.

Sahoo and Dash (2022) have investigated the implications of foreign investment for exports of 93 developing countries during 2000–2017 using panel data. They distinguish between different types of developing countries. The sample is divided into lower-income countries (LICs), lower and middle-income countries and emerging economies—to study the differential effects of FDI for these different country groups. The study finds that FDI complements exports, and the complementary effect is contingent upon the development levels of the host country. FDI is most effective for promoting exports in the case of emerging economies and least effective for LICs.

Osabuohien-Irabor and Drapkin (2021) examine the interaction between OFDI and disaggregate international trade based on the World Bank country income classification, which includes the low-income, lower-middle-income, upper-middle-income and high-income for a panel of 179 countries for the period of 2003–2019. Based on a dynamic panel data model applying the system generalised method of moments (GMM) estimator, empirical findings reveal that OFDI has negative and significant effects on exports and imports of low-income countries, indicating a substitutional relationship. Regarding the impact of exports on OFDI, except for low-income countries, they found a positive and significant relationship for all income clusters, indicating a complementarity relationship.

Akadiri et al. (2020) focused on the relationship between FDI, trade openness and economic growth for 25 African countries during 1980–2018. The study used the Granger causality approach. The results demonstrate ‘bidirectional causality running between FDI and trade openness for the sampled countries over the period’. So, among the African economies covered in the analysis, FDI and trade complement rather than substitute.

To test the nature of the relationship between trade and FDI, an FDI-augmented gravity model, 4 where inward and outward FDI are added as additional determinants of trade, has commonly been used (Ahn et al., 2004). Researchers have augmented the gravity model by including population, per capita income, trade arrangement, common language and historical and cultural ties between countries, potentially influencing the intensity of trade between countries. The analysis is then extended to take outward FDI and inward FDI into account as additional determinants of trade. Such an analysis will indicate whether trade and FDI are substitutes or complements after controlling for comparative advantage (Ellingsen et al., 2006; Hejazi & Safarian, 2001; Türkcan, 2007). The gravity model has also been extensively used in the trade literature to examine several trade issues, such as ascertaining, for example, the impact of trade liberalisation, a currency union and FDI on trade flows (Ellingsen et al., 2006; Frankel, 1997; Rose, 2000). For example, Martínez et al. (2012) studied the relationship between trade and FDI in the context of the economic integration of the EU and found that the EU commercial integration and FDI reinforce each other, thus being complements rather than substitutes in Europe. Another important study using the gravity model is by Goh et al. (2012), who examined the relationship between trade (export and import) and inward and outward FDI using Malaysia as a case. They found that inward FDI has a complementary relationship with trade, while outward FDI and trade linkages are not significant.

Xiong and Sun (2021) explore the linkage between exports and FDI, covering a group of 140 countries for 2001–2006. The study employed augmented gravity models and found complementarity between foreign investment and exports for a selected sample of economies. However, the impact seemed to be more pronounced for pairs of developed-developing countries than for pairs of developed–developed or developing–developing ones.

Applying the Mundlak approach to the gravity-type trade model, Sohail et al. (2021) examine the effects of FDI on bilateral trade between East and South Asian emerging economies from 2001 to 2019. The analyses for different subsamples reveal varying results following the economic development in the countries. FDI flows from developing countries have positively influenced bilateral trade with developing countries. However, it becomes insignificant after introducing additional variables to the model. Regarding the subsample of FDI flows from developed countries, and their influence on bilateral trade with developing countries, the relationship between FDI and bilateral trade is found to be trivial.

Empirical Studies for India

Having discussed the international literature on the relationship between exports and OFDI, attention may now be turned to the empirical studies on this issue undertaken for India. Several studies have examined the issue of long-run causality between India’s exports and FDI outflows. Applying Granger causality and vector autoregression (VAR), Dasgupta (2009) showed unidirectional causality from the trade variables to the FDI outflows in India. The study further indicates that there is evidence of a negative influence of OFDI on exports. Verma and Brennan (2011) examined the causal linkages between Indian OFDI and exports based on time-series data for 1981–2006 using a vector error correction model (VECM). The results of the study suggest that there is a unidirectional causal relation between India’s exports and her OFDI. The results indicate that increased exports from India will lead to greater OFDI. However, the study did not find clear empirical support for a ‘substitution’ relationship or a ‘complementary’ relationship between exports and stocks of OFDI. Along similar lines, Malhotra (2014) found that while there is no evidence of causality from OFDI to exports, there is weak causality running from exports to OFDI.

Using a large sample of developing countries for their analysis, including India, Bhasin and Paul (2016) find that OFDI negatively and significantly impacts home-country exports, implying that OFDI is a substitute for exports in these countries. Their results also indicate a long-run causality from exports towards OFDI. However, no long-run causality was found from OFDI to exports. Similar results were found in a study by Bhasin and Kapoor (2020) for BRICS nations.

Sharma and Kaur (2019) examined the causal relationships between FDI and trade in India and China from 1976 to 2011. The results for India show bidirectional causality between FDI and imports, FDI and exports, and exports and imports. Jana et al. (2020) endeavour to understand the dynamic relationship between FDI and foreign trade in terms of India’s export using a time-varying parameter model with vector autoregressive specification during the period of the first quarter of 1996–1997 to the last quarter of 2018–2019. The study reveals that FDI significantly contributes to promoting the export of the Indian economy only in the short run, whereas export plays a vital role in promoting the inward flow of FDI in both the short run and long run. The study concludes that the absence of long-run causality from FDI to export results from much domestic market orientation of foreign investors and less emphasis on the export-oriented sectors in India.

For Indian auto ancillary exporters, Singh (2013) finds a complementary effect of OFDI intensity and the number of non-manufacturing OFDI enterprises on the probabilities of export participation at the Original Equipment Manufacturer (OEM) and OEM and/or Tier level up to a certain level. However, a substitution relationship is found in the case of a high degree of OFDI internationalisation. Thus, the likelihood of being an exporter to OEMs lessens with a higher number of countries of OFDI investment, reflecting substitutability between OFDI and exports.

Suri and Banerji (2017) examined the relationship between exports, OFDI and total Indian pharmaceutical industry sales. They develop a VAR model on exports and OFDI, keeping total sales as an exogenous variable using a lag of one and two years. It was found that in the context of the Indian pharmaceutical sector, exports cause OFDI, and in turn, the previous year’s OFDI directly impacts the current year’s exports.

The studies on firm-level determinants of India’s OFDI that have attempted to understand the importance of exports for OFDI require a mention here. To give an example, Lall (1986) surveyed 162 Indian enterprises, including 24 foreign investors, during 1977–1979, and the study revealed that impediments to exports provided an incentive for OFDI. Dasgupta and Siddharthan (1985) and Agarwal (1985) found interdependence between Indian exports and OFDI during the late 1970s and early 1980s in sectors comprising largely standardised goods and relatively low skill and technological content. Pradhan (2007a, 2007b) and Kumar (2007) reported a similar result in their analysis. They found that manufacturing firms already engaged in exporting were more likely to be outward investors, in line with the PLC framework where foreign production follows exports. Similarly, Thomas and Narayanan (2017), using data from Indian manufacturing firms from 1998 to 2009, also find complementarities between export intensity and OFDI. Likewise, for India’s IT (information technology) firms, Narayanan and Bhat (2011) have reported a favourable impact of higher export intensity in the previous year (i.e., lagged export intensity) on the firm’s decision to become an MNE.

Summing Up

From the above discussion, it may be inferred that there is no consensus on the nature of the relationship between FDI and exports, neither from a theoretical nor an empirical point of view. The relationship between OFDI and trade could be any of three: substitution, complementary or mixed. However, most empirical studies’ findings suggest a complementary relationship between OFDI and exports (Forte & Silva, 2017; see also Villar et al., 2019, who have conducted a meta-analysis).

The literature on the topic under discussion tells us that the type of economic relationship observed between FDI and trade is dependent on the domestic firms’ strategies to invest abroad, e.g., horizontal investment (i.e., seeking to get better access to the foreign market by relocating home production to foreign production), vertical (i.e., seeking to take advantage of cheap factors of production abroad by establishing a subsidiary in the host economy) or both. The nature and purpose of FDI inflows are crucial for determining their impact on exports (Ahmad et al., 2018; Goh et al., 2017; Moran, 2011). The effect of FDI on trade may differ depending on whether foreign firms invest to gain resources, markets, strategic assets or productive efficiency. However, empirical work in this area that employs industry- or country-level data generally finds a positive or complementary relationship between exports and foreign affiliates’ activity.

It should be noted further that the type of relationship that a researcher observes empirically depends on the level of analysis of the studies—whether the analysis is done at the country, industry, firm or product level. As evidenced by Forte and Silva (2017), most studies with more aggregate-level data found a complementary relationship, while studies undertaken at a more disaggregated level tend to find a substitution relationship. Apart from the level of aggregation, the motive and structure of OFDI and the home–host OFDI policies affect the OFDI–exports linkage (Tyson et al., 2012).

Another point to be noted is that the findings of an analysis depend on the countries covered in the study and their level of economic development. The nature of impact may change with the level of development, as brought out by the analysis (pendulum gravity model of OFDI) of Liu et al. (2016).

Keeping the above discussion in mind, it becomes clear that a study of the relationship between OFDI and exports assumes relevance and significance for an emerging economy such as India. Thus, the three sections below attempt to contribute to this literature by studying the effect of India’s BIT terminations on imports and FDI inflows.

Analysis Based on a Difference-in-Difference (DiD) Research Design

We employ a staggered differences-in-difference research design to analyse the impact of BIT termination on India’s imports from different source countries. We apply the methodology proposed and developed by Callaway and Sant’Anna (2021), which has significant methodological advantages.

A brief discussion on the choice of econometric methodology would be in order here. The two-way fixed-effects (TWFE) model has found wide application in empirical econometric literature for applying the DiD methodology to analyse the effect of a policy or policy change. Many studies have applied such a methodology. 5 In many studies, linear regressions with period and group fixed effects have been estimated to assess the impact of new policies or a change in existing policies. Recent research on econometric methodology dealing with the estimation of treatment effects has shown that such regressions may produce misleading estimates if the effect of the policy is heterogeneous between groups or over time, which is often the case. That the TWFE model has a serious limitation has been noted in recent years (for a discussion, see Baker et al., 2021; Callaway & Sant’Anna, 2021; de Chaisemartin & D’Haultfoeuille, 2022). The methodology suggested by Callaway and Sant’Anna (2021) has the advantage that it can control for the biases that arise in applying the standard TWFE estimator in a situation where there is staggered treatment adoption and dynamic heterogeneity in the treatment effects. 6 This feature of the methodology developed by Callaway and Sant’Anna (2021) makes it attractive for application in the present study.

We use quarterly data on India’s imports from about 30 countries from 2015 to 2020. The logarithm of India’s imports in US$ is the outcome variable. The control variables considered are the GDP of the source country (i.e., the country from which the goods have been imported in India), the growth rate in India’s quarterly GDP to capture the demand effect (lagged by one quarter to avoid any issues of endogeneity) and the relative exchange rate, i.e., the exchange rate of the source country of India’s imports divided by the exchange rate of India; the exchange rates considered are the local currency vis-à-vis the U.S. dollar.

Data on GDP have been taken from the World Development Indicators (WDI) of the World Bank. The country-wise quarterly exchange rate in the national currency per U.S. dollar is taken from OECD statistics. In addition, quarterly GDP growth data for India are also collected from OECD statistics. Data on India’s imports from various countries in the different quarters from 2015 to 2020 have been collected from the Export–Import Data Bank, Ministry of Commerce and Industry, Government of India.

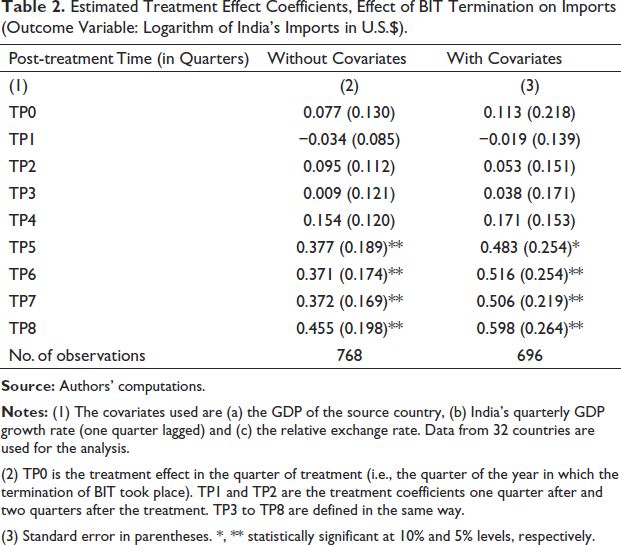

The analysis is undertaken in a treatment effect estimation framework. By using the term ‘Treatment’, we refer to the termination of BITs. The treated cases are those countries with which India had a BIT, which was terminated sometime during the study period, 2015–2018. The estimation of the treatment effect has been done by using an event study format. The estimated treatment effect coefficients for different time points from the quarter of treatment (when the BIT was terminated) are shown in Table 2.

Estimated Treatment Effect Coefficients, Effect of BIT Termination on Imports (Outcome Variable: Logarithm of India’s Imports in U.S.$).

Estimated Treatment Effect Coefficients, Effect of BIT Termination on Imports (Outcome Variable: Logarithm of India’s Imports in U.S.$).

(2) TP0 is the treatment effect in the quarter of treatment (i.e., the quarter of the year in which the termination of BIT took place). TP1 and TP2 are the treatment coefficients one quarter after and two quarters after the treatment. TP3 to TP8 are defined in the same way.

(3) Standard error in parentheses. *, ** statistically significant at 10% and 5% levels, respectively.

Table 2 shows that the estimated treatment effect coefficients for TP5 (five quarters from the time the BIT was terminated) to TP8 are positive and statistically significant. The results obtained using covariates are similar to those obtained without the covariates. Overall, these results indicate that India’s termination of BITs led to a hike in India’s imports. This finding is consistent with a substitution relationship between FDI and exports. The firms in foreign countries apparently reduced their FDI in India in response to BIT termination and then raised their exports to India.

It was mentioned in Section 2 that, in many earlier studies, the gravity model has been used to explain inter-country variations in trade or FDI flows. Among the key or core variables in such a model are the GDP of the home country and that of the host (destination) country, which have a positive effect on trade flows or investment flows, and the distance between the two countries, for which an adverse effect is expected. It would be appropriate to carry out an analysis based on the gravity model to confirm whether India’s termination of BITs led to a decrease in FDI flows to India (which has been found by Hartmann & Spruk, 2023; Kotyrlo & Kalachyhin, 2023, by applying the DiD analysis technique) and an increase in India’s imports (found in the analysis in the previous section based on the DiD analysis technique). For this analysis based on the gravity model in this section, the following specifications of the models are adopted:

Model for FDI inflows

Model for imports

The subscript i is for India, and j is for a foreign country investing in India (in Equation (1)) or exporting to India (in Equation (2)). The subscript i does not change across observations, but subscript j changes. FDI denotes FDI flow from country j to India. M denotes India’s imports from country j. The subscript t is for time. The period considered for model estimation is from Q1 of 2015 (t = 1) to Q4 of 2020 (t = 24). The explanatory variables considered are the GDP of foreign country j, the GDP of India (subscript = i), the growth rate in India’s GDP (over the same quarter in the previous year) denoted by

The distinguishing feature of the present study in applying the gravity model lies in the introduction of the BIT termination dummy variable denoted by BITD in Equations (1) and (2). If country j and India did not have a BIT (or the BIT was not terminated), it takes the value of zero. If India had a BIT with country j before 2015, and this was terminated at the time τ (during the study period), then the dummy variable takes the value of zero for t < τ, and the value of one for t ≥ τ. This dummy variable captures the impact of BIT termination. The coefficient β6 shows the effect of BIT termination on FDI, and the coefficient δ6 shows the impact on imports.

The data source used for the study may be briefly mentioned. The source of data on the country-wise FDI flows to India is the Department for Promotion of Industry and Internal Trade, Ministry of Commerce and Industry, Government of India. Data on the GDP of source countries (in 2015 U.S.$) have been obtained from WDI of the World Bank. These GDP data are for calendar years. The estimate of GDP for a calendar year has been applied to the four quarters of the year (as quarterly data on GDP for each country covered in the study is difficult to obtain). India’s quarterly GDP data for 2011−2012 price have been taken from the Handbook of Statistics on Indian Economy (Reserve Bank of India), and we have computed the quarter-on-quarter growth rates from these data. The data on the distance of the source countries from India and the presence of a common language have been taken from the CEPII (Center for Research and Expertise on the World Economy) database.

The estimation of the two models specified above was first done by applying the fixed-effects model. This estimation technique has the advantage that unobserved heterogeneity among countries is accounted for in model estimation. One estimation issue that needs to be addressed is that in about 14% of the observations, the reported FDI flow to India is zero. Thus, the dependent variable is truncated at zero. Zero values in the dependent variable are a lesser problem in the model estimated with import data. However, there are some observations with zero imports. These observations form about 1.6% of all observations. To address this issue, we have added the value of one to the dependent variable and then taken the logarithm, as has been done in some earlier studies, for instance, Bhasin and Manocha (2016) and Kotyrlo and Kalachyhin (2023).

Adding the value of one to the dependent variable and then taking the logarithm does not solve the estimation problem entirely when the fixed-effects model is used because the model does not consider the fact that the dependent variable is truncated at zero. This is a serious concern for the regression equation estimated for FDI inflow because, as stated above, about 14% of observations on FDI inflow are truncated at zero. To address this estimation problem, the models have been estimated by applying the random-effects Tobit model, 7 which considers the dependent variable’s truncation at zero, although in the case of the model for imports, a Tobit specification is not necessary.

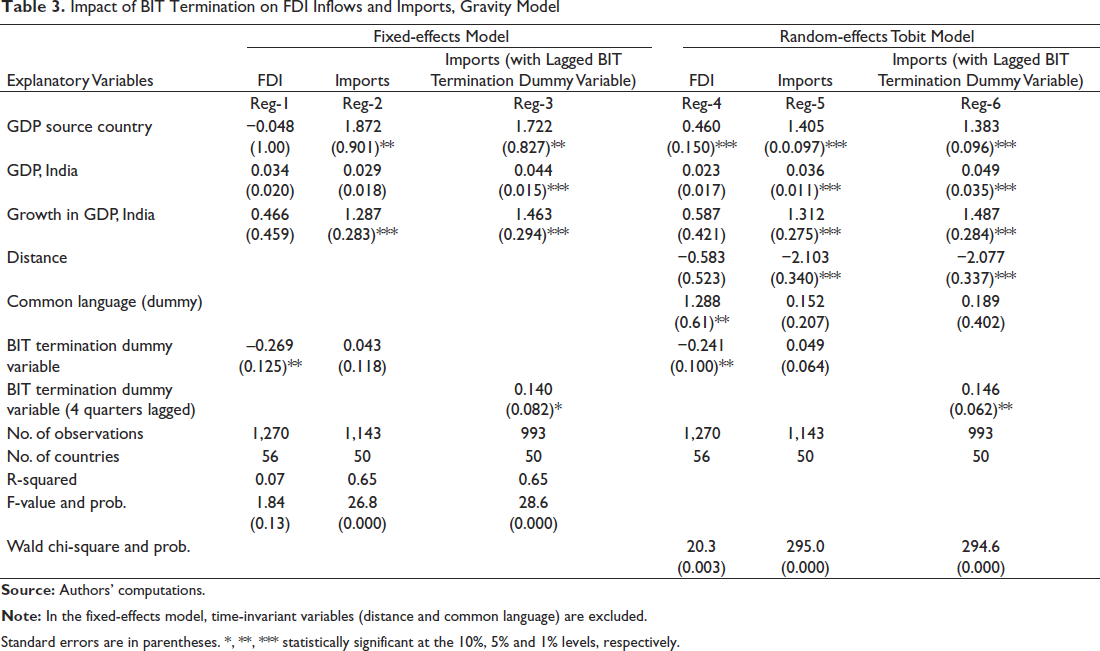

The estimates of the two Equations (1) and (2) by the fixed-effects model and the random-effects Tobit model are presented in Table 3. Two sets of estimates of Equation (2) are shown. In one case, the BIT termination dummy variable has been lagged by four quarters; in the other, this is not done. The justification for the variant with a lagged impact of BIT termination arises from the fact that in the estimates of treatment effect coefficients based on the DiD method in Table 2, the treatment effect coefficients from TP5 onward are consistently positive and statistically significant, implying that the effect of BIT termination on imports occurs with a lag of over four quarters.

Table 3 shows that the coefficient of the BIT termination dummy variable is negative and statistically significant in the Equation (1) estimates. This finding corroborates the findings of Hartmann and Spruk (2023) and Kotyrlo and Kalachyhin (2023), which indicate that India’s termination of BITs led to a significant fall in the inflow of FDI in India. The numerical value of the coefficient is about 0.25, indicating a 25% fall in FDI inflows, which is broadly consistent with the estimate of Hartmann and Spruk (2023), who found a significant reduction in FDI inflows to India in response to BIT terminations by over 30% compared to countries without terminations.

Impact of BIT Termination on FDI Inflows and Imports, Gravity Model

Standard errors are in parentheses. *, **, *** statistically significant at the 10%, 5% and 1% levels, respectively.

The coefficient of the BIT termination dummy variable in Equation (2) estimates is positive and statistically significant when the dummy variable is lagged by four quarters. This is in agreement with the findings from Table 2. Considering the two pieces of empirical evidence on the estimated impact of BIT termination on imports (from Tables 2 and 3), it may be inferred that the termination of BITs led to a hike in India’s imports.

The coefficient of the distance variable is negative, and that of the common language dummy variable is positive. Such results are expected. As expected, the coefficients of India’s GDP, the growth rate in India’s GDP, and the GDP of the source country of FDI and imports are positive.

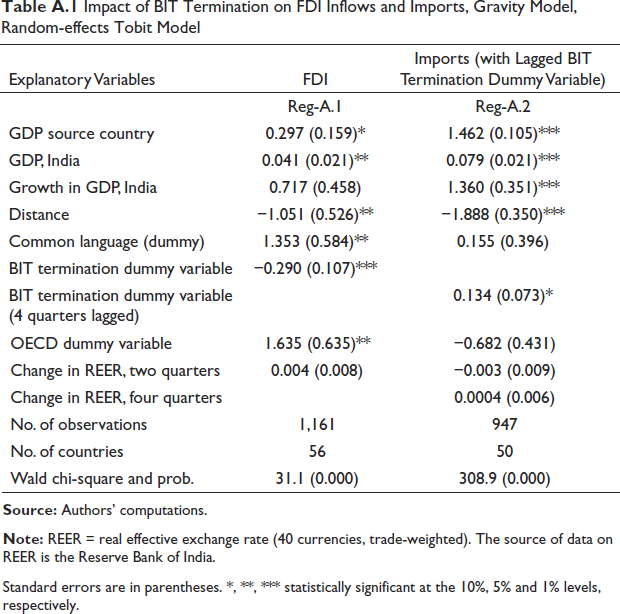

In Equation (2) estimates, the coefficients are statistically significant in most cases. One unsatisfactory aspect of the results in Table 3 is that in the model estimated for FDI inflows, the coefficients of India’s GDP or growth in GDP are statistically insignificant. To explore this aspect further, Equation (1) has been re-estimated by adding two explanatory variables and estimating the equation by the random-effects Tobit model. The results are shown in Table A.1 in Annexure A. A dummy variable distinguishing between OECD countries and other countries has been introduced in the model. Also, the change in India’s real effective exchange rate has been included as an explanatory variable. In this case, the coefficient of India’s GDP is found to be positive and statistically significant, as is expected in a gravity model.

We also present in Table A.1 an estimate of the model for imports by using more or less the same specification [with a lag of four quarters for BITD as in Regression (6)]. The results are similar to those in Table 3. The coefficients of India’s GDP and the growth rate in GDP are positive and statistically significant. One would expect a higher level of GDP and faster growth in GDP to affect imports positively. The empirical results bear this out.

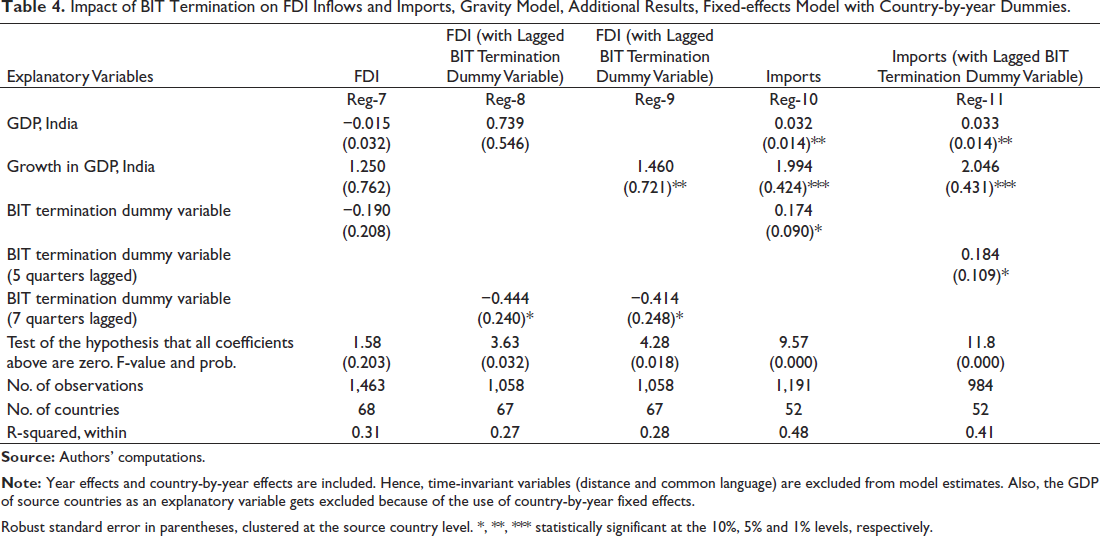

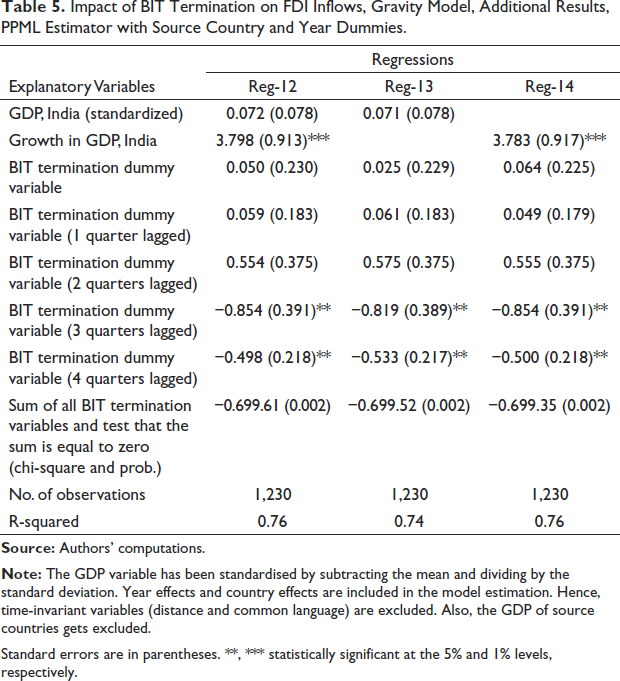

Two econometric exercises have been undertaken to check the robustness of the econometric results presented in Section 4. In the first exercise, the fixed-effects model is estimated, with country-by-year fixed effects introduced. In the second exercise, the Poisson Pseudo Maximum Likelihood (PPML) estimator is used to estimate Equation (1).

The PPML estimator has been recommended by Santos Silva and Tenreyro (2006, 2011) for estimating the gravity model of trade when a significant portion of the reported trade data has zero values. This methodology has been applied in several studies. The study by Hartmann and Spruk (2023) mentioned earlier on the impact of BIT termination on India’s FDI inflow used the PPML estimator for the analysis. The application of the PPML estimator has been made only for the regression equation explaining FDI inflows to India, not for India’s imports because the issue of truncation of the dependent variable at zero applies to FDI inflows (14% observations truncated at zero) and does not apply to imports (only 1.6% of the observations have zero value of imports in the sample used).

The estimates of regression equations explaining quarterly FDI inflows and imports incorporating source-country-by-year dummy variables are presented in Table 4. In the estimates shown in Regressions (10) and (11), the coefficient of the BIT termination dummy variable is positive and statistically significant. The coefficients of India’s GDP and the growth rate in India’s GDP are positive and statistically significant, as expected. The results in Regressions (10) and (11) are in accord with the results in Regression (6) in Table 3. These results indicate that the termination of BITs led to an increase in India’s imports, confirming the findings based on the DiD methodology in Table 2.

Impact of BIT Termination on FDI Inflows and Imports, Gravity Model, Additional Results, Fixed-effects Model with Country-by-year Dummies.

Robust standard error in parentheses, clustered at the source country level. *, **, *** statistically significant at the 10%, 5% and 1% levels, respectively.

In Regressions (7), the coefficient of the BIT termination variable is not statistically significant. Also, the coefficient of India’s GDP is wrongly signed. Hence, in Regressions (8) and (9), India’s GDP and the growth rate in India’s GDP are included separately. Also, we have taken the BIT termination variable lagged by seven quarters. Different lags of the dummy variables were tried, and a seven-quarter lag yielded the best results. The results indicate a positive effect of India’s GDP and GDP growth rate on FDI inflows into India. A negative impact of BIT termination on FDI inflows is found, consistent with the results in Table 3 (Regressions (1) and (4)).

Impact of BIT Termination on FDI Inflows, Gravity Model, Additional Results, PPML Estimator with Source Country and Year Dummies.

Standard errors are in parentheses. **, *** statistically significant at the 5% and 1% levels, respectively.

The results in Tables 3, 4 and 5 regarding the impact of BIT termination are in harmony. Also, these results are in harmony with the findings of Hartmann and Spruk (2023) and Kotyrlo and Kalachyhin (2023). The inference that may be drawn from these findings is that BIT termination led to a significant decrease in India’s FDI inflows. The other important finding of the study is that BIT termination led to an increase in India’s imports. These findings are consistent with a substitution relationship between FDI and exports—since the foreign MNEs lowered their FDI to India, they opted to raise their exports of products to India.

Conclusion

Until 2015, India had signed BITs with 83 countries, and 74 were in force then. Over 25 of these treaties were terminated in March 2017. Between April 2017 and December 2018, another 12 BITs were terminated. Two BITs were terminated in the last quarter of 2016. This article examined how India’s BIT termination impacted India’s FDI inflow and imports. This analysis aimed to investigate an issue in the Indian context that has received much attention in several earlier studies, namely, whether FDI and exports are substitutes or complement each other. If exports and FDI are independent, there is no good reason why the termination of BITs will impact imports. If there is a strong complementarity between FDI and exports, the fall in FDI inflows caused by BIT termination should also be reflected in the negative effect of BIT termination on India’s imports. On the other hand, if a positive impact of BIT termination of imports is found (as is the case in the results presented in the paper), this may be treated as empirical evidence of substitutability between FDI and exports.

From the econometric analysis undertaken based on the DiD method, followed by the estimation of a gravity model each for explaining India’s FDI inflows and India’s imports, an adverse effect of BIT termination on FDI inflows was found, corroborating the findings of two recent studies by Hartmann and Spruk (2023) and Kotyrlo and Kalachyhin (2023), and a significant positive effect of BIT termination on India’s imports was found. This finding of a positive impact of BIT termination on imports and a negative effect on FDI inflows is conceivably reconcilable only if there is a substitution relationship between FDI and exports. Hence, we find some empirical evidence of a substitution relationship between FDI and exports (in accord with the findings of Bhasin & Paul, 2016 and Bhasin & Kapoor, 2020)—at least this has been the relationship between India’s inflow of FDI and inflow of goods as imports, if not valid for other countries.

What are the policy implications of a strong substitution relationship between FDI and exports? It follows that if there are significant impediments to foreign investment in a developing country, the firms in foreign countries will serve the local markets in the developing country through exports. If the foreign firms had set up production facilities in the developing country, this would have led to local value addition and job creation. Since the local market is served by foreign firms by exporting their products to the developing country, because of impediments to FDI, value addition and job creation take place abroad. Clearly, action is needed to encourage and facilitate the inflow of FDI. A bilateral investment treaty is an important element of the strategy to encourage FDI. Another alternative is to opt for a comprehensive economic cooperation agreement with a component dealing with foreign investment.

Turning to the situation in India, Indian firms have been making investments abroad on a significant scale. Our results suggest that the outward investments made by Indian firms lead to a loss in exports. For a capital-scarce country, such investments raise a concern because value addition does not occur on Indian soil with concomitant creation of jobs but takes place on foreign soil with employment opportunities created there. Yet, there is no strong case for restricting such outward investments because OFDI contributes significantly to the productivity and competitiveness of Indian firms. The answer lies in creating highly attractive business conditions in India for foreign MNEs so that FDI inflow significantly exceeds FDI outflow. This course of action will be facilitated by renegotiating and bringing into force the BITs that have been terminated during 2016–2018 or have comprehensive economic cooperation agreements with a chapter dealing with investment. In addition, there is a need to quickly implement the new labour codes formulated for easing labour regulations, carry out other policy reforms to improve the ease of doing business in India, and make further progress in infrastructure development. Such steps will create a more conducive environment for FDI in India. Such investments in India from foreign firms will displace imports of industrial products to some extent and thus help create industrial jobs in India rather than in other countries.

Annexure A: Additional Regression Results

Impact of BIT Termination on FDI Inflows and Imports, Gravity Model, Random-effects Tobit Model

Standard errors are in parentheses. *, **, *** statistically significant at the 10%, 5% and 1% levels, respectively.

Annexure B: The Gravity Model for FDI: Theoretical Aspects

The gravity model has extensively been used to explain trade among countries. This model, with some medications or extensions in some instances, has also been applied in many studies to explain FDI flows among countries (see, e.g., Bhasin & Manocha, 2016; Buckley et al., 2007; Chakrabarti, 2001; Loree & Guisinger, 1995; Pradhan, 2011; Root & Ahmad, 1979). Several econometric studies applying the gravity model to FDI flows have referred to Bergstrand and Egger (2007) and Head and Ries (2008) as studies that provide a theoretical basis for applying the gravity model to FDI. Another paper in which some theoretical basis for the applicability of the gravity model to FDI flows has been provided is by Kleiner and Toubal (2010).

Head and Ries (2008) treat FDI as a manifestation of an international market for corporate control through mergers and acquisitions. They develop a model of FDI where heterogeneous investors attempt to obtain control rights on existing overseas assets. The model yields an equation of bilateral FDI that resembles the gravity equation. There is an outward effect reflecting the characteristics of the origin country and an inward effect reflecting the characteristics of the destination country. Distance enhances monitoring costs and thus tends to lower FDI flows, as in the case of the gravity model for trade.

Bergstrand and Egger (2007) develop their theoretical argument by considering the nexus of the literature on trade, FDI and MNEs. The point of reference of the analysis is the 2 × 2 × 2 general equilibrium theory of Markusen (2002). In the two-factor ‘knowledge-capital’ model with only skilled and unskilled labour, Bergstrand and Egger introduce a third internationally mobile factor, physical capital. Also, extending the two-country model, they introduce a ‘third’ country, taking the rest of the world as the third country. These modifications imply that national exporting enterprises can coexist with horizontal MNEs, which was not possible in the theoretical framework of Markusen (2002); in that framework, the national firms and trade between the two countries get completely eliminated by the sales of horizontal MNEs. Bergstrand and Egger show in their analysis that with the presence of a third country (i.e., the rest of the world) and capital mobility, the national exporting firms and MNEs covary positively and monotonically, with the two countries’ GDPs becoming similar in size.

Kleiner and Toubal (2010) establish that a relationship similar to the gravity applied to the FDI flow may emerge from three alternate theoretical constructs. In the first theoretical model, they assume a foreign affiliate’s production process is dependent on domestic intermediate inputs, which are costly to trade. In the second theoretical model, they assume fixed costs of production in a foreign country, which goes up with the distance between countries in a heterogeneous firms framework. In both these models, distance has a negative effect, in line with the gravity model of trade often empirically applied. Kleiner and Toubal (2010) note that both models are proximity-concentration models that explain the emergence of horizontal multinational firms.

The third theoretical model of Kleiner and Toubal (2010) is based on the factor proportions theory. In this framework, firms fragment their production process to take advantage of different countries’ comparative advantage. In this framework, considering two countries for the analysis, it is shown that the relative factor endowments and the joint size of the home and host countries’ economies influence bilateral affiliates’ sales. Kleiner and Toubal show that the bilateral affiliates’ sales are affected positively by both countries’ incomes. Distance between the two countries reduces the volume of affiliate sales. These theoretical findings justify the application of the gravity model for explaining FDI flows, taking the GDP of the home and host countries and the distance between them as explanatory variables.

Following Kleiner and Toubal (2010), it may be argued that the success of the gravity model in explaining FDI flows in various empirical studies is attributable to the fact that the critical components of the gravity model equation may be derived from alternate theoretical frameworks.

Footnotes

Acknowledgement

The authors have immensely benefited from the comments and suggestions of two anonymous reviewers of the paper. Views are the authors’ own. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.