Abstract

The conventional design of executive compensation plans is based on an outdated model of executive agency. Behavioural economics has provided a better understanding of the relationship between executives’ pay and their motivation through detailed examination of the psychology of incentives. Four key points emerge from the research. First, executives are much more risk averse than financial theory predicts. Second executives are very high time discounters, thus reducing the perceived value of deferred rewards. Third, intrinsic motivation is much more important than admitted by traditional economic theory. Fourth, executives are more concerned about the perceived fairness of their awards relative to peers than in absolute amounts. Research suggests that companies would be better off paying generous salaries and using annual cash bonuses to incentivise desired actions and behaviours. Executives should be required to invest bonuses in company shares until they have sufficient ‘skin in the game’ to align their interests with shareholders.

Many books, articles and opinion pieces published in recent years have linked inflation in senior executive pay to the growing economic divide within society. Piketty (2014), a French economist, describes very high rates of executive pay as one of the most significant factors contributing to growing inequality. While it might be thought to be in the general interests of public companies to moderate executive rewards, top pay has proved difficult to control. Boards of directors struggle to achieve a balance between offering executive reward packages that are justified by the demands of the job and sufficient to retain top talent, forcing them into a prisoner’s dilemma. I call this the ‘Remuneration Committee’s Dilemma’: in attempting to second-guess competitors’ pay offers, companies defect and propose larger than necessary pay awards. Other companies, in the same position, follow suit, generating spiralling compensation which in time becomes normalised.

The reasons why executive pay has increased exponentially in the last 30 years are complex, but my research suggests that the fundamental problem lies in a continued reliance upon outdated economic models. These assume that executives are self-interested, entirely rational and only motivated by money. By basing executive compensation and performance management on these outdated theories, organisations prioritise pay over intrinsic motivation, personal fulfilment and job satisfaction, crowding-out ethical behaviour by placing the greatest emphasis on extrinsic motivation and high-powered equity-based incentives.

Outdated Economic Models

The two economic theories which underpin the pay-for-performance model of executive compensation are agency theory, made famous by a seminal paper by Jensen and Meckling (1976), and tournament theory, advanced by American economists Ed Lazear and Sherwin Rosen in 1981. Agency theory models the relationship between shareholders and executives as an agency relationship characterised by different interests and motivations. It proposes that, in order to motivate executives (agents) to carry out actions and select effort levels that are in the best interests of shareholders (principals), boards of directors, acting on behalf of shareholders, design incentive contracts which make an agent’s compensation contingent on measurable performance outcomes. Tournament theory extends the agency model by suggesting that principals structure a company’s management hierarchy as a rank-order tournament, thus ensuring that the highest-performing agents are selected for the most senior management positions. It postulates that executives compete for places in a company’s upper echelons via what economists describe as a ‘sequential elimination tournament’. It predicts that compensation is an increasing convex function of the agent’s position in the management hierarchy, with increases in remuneration between levels in the hierarchy being inversely proportionate to the probability of being promoted to the next level. By implication, the compensation of the CEO, ranked highest in the tournament, will typically be substantially more than the compensation of executives at the next highest level.

Agency and tournament theories have had a powerful impact on organisational pay strategies. The problem is that the two theories are based on a flaky and partial understanding of human nature. The standard economic model assumes that agents are rational, self-interested and profit-seeking, that their utility is positively contingent on pecuniary incentives and negatively contingent on effort, and that they are motivated solely by money. It further assumes that time preferences are calculated according to an exponential discount function. These assumptions are abstractions, deliberately simplified, intended to make theory development more mathematically tractable and justified by economists since Milton Friedman on the basis that (so they say) the assumptions do not matter if the predictions of a theory are correct. Yet empirical research from 1990 onwards, the publication date of a large empirical study conducted by Jensen and Murphy (1990), has failed to demonstrate a conclusive link between agents’ pay and corporate performance. Tosi et al. (2000) found that incentive alignment as an explanatory agency construct for CEO pay was at best weakly supported by the evidence. Frydman and Saks (2010) concluded, based on a review of US compensation data for the period 1936–2005, that agency theory is not fully consistent with the available evidence. Conventional wisdom today is that CEO pay increases as a power function of company size. Some economists argue that this conclusion, that ex post executive pay is correlated with firm size, is still consistent with optimal contracting theory (successor to agency and tournament theories) even if, ex ante, firms are trying to link executive pay to firm performance. But this is like arguing that a man or woman intending to travel from London to Delhi who takes a wrong turning and arrives in Mumbai instead has nevertheless achieved an efficient outcome because they have still found their way to India.

Behavioural Agency Theory

Research which I have carried out with my co-author Dr Julie Gore of the University of Bath has demonstrated that the behavioural assumptions on which agency and tournament theories are based appear to be fundamentally wrong, and have called into question the predictions of those theories (Pepper and Gore, 2014; 2015). We propose a new version of agency theory, which we call Behavioural Agency Theory. We have identified various phenomena which are not consistent with standard agency theory.

These findings are consistent with work carried out by economic psychologists such as Kahneman and Tversky (1979), and Kahneman (2011). Our empirical evidence challenges conventional wisdom about the merits of high-powered incentives plans and pay for individual performance. It suggests that long-term incentives may actually be fuelling increases in executive pay, rather than helping to contain pay inflation. The research indicates that more balanced pay arrangements, incorporating low-powered incentives, may be more efficient and effective, especially when good measures of an individual’s effort or performance are not available, when multi-tasking is required and when cooperation between different agents is necessary.

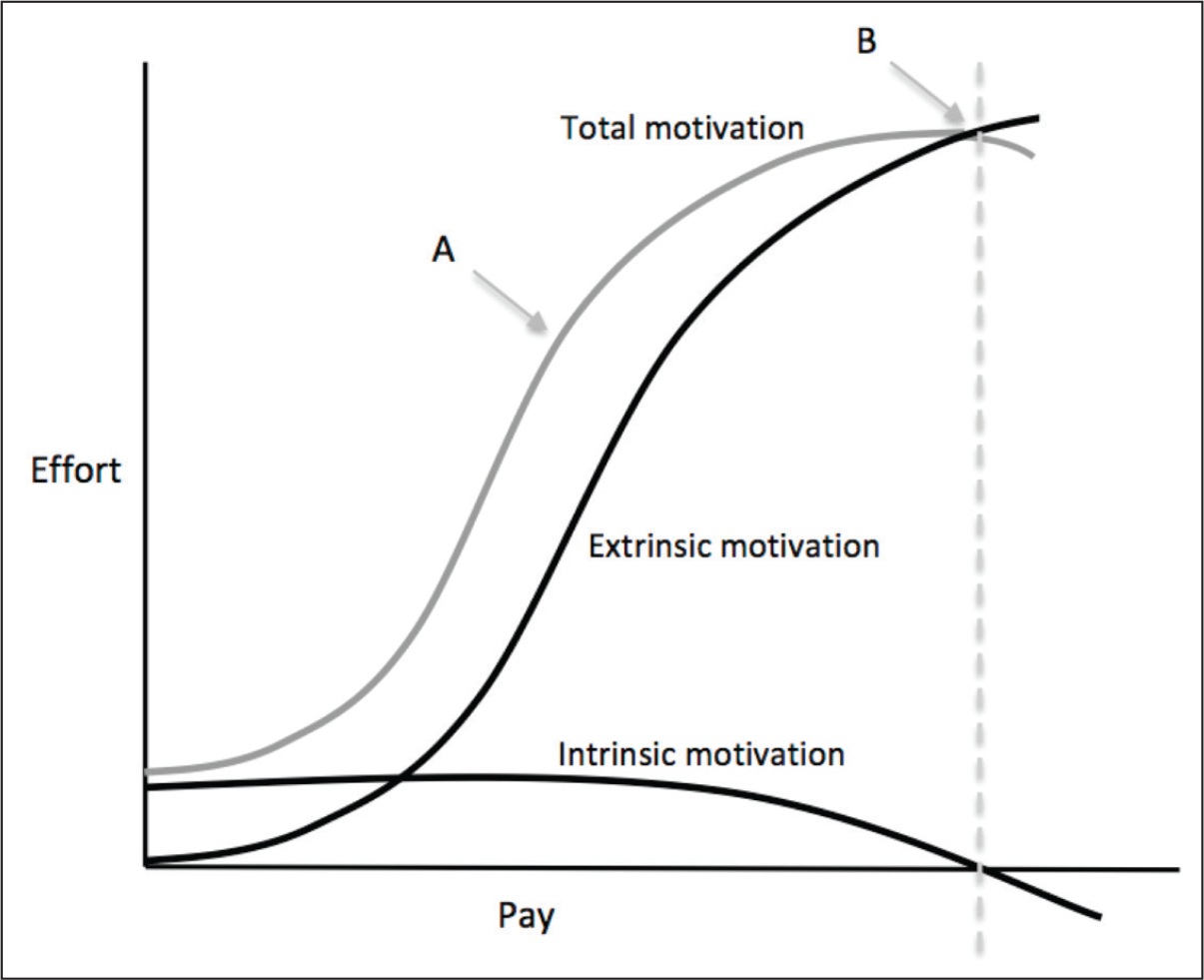

Figure 1 models the relationship between pay and motivation according to behavioural agency theory. It builds on the four key behavioural concepts that have been identified by behavioural economists: very conservative preferences when it comes to risky, ambiguous and uncertain outcomes, heavy time discounting, a recognised trade-off between intrinsic and extrinsic motivation and inequity aversion along with a strong preference for fairness. The graph in Figure 1 illustrates how total motivation is the sum of the intrinsic and extrinsic motivation curves. It shows the incentive ‘sweet spot’ (A), where the motivational benefit of an additional dollar of pay is maximised, as well as point (B) when ‘crowding out’ sets in, after which intrinsic motivation is undermined by each additional dollar of incentive pay, and total motivation therefore declines.

New Design Principles

An example of how a compensation package designed according to design principles suggested by behavioural agency theory might compare with a conventional package is set out in Table 1. Note that detailed tax consideration have not been taken into account. Imagine that the CEO in a large company currently receives a salary of US$ 1,000,000, an annual bonus opportunity of 200 per cent of salary, and an annual long-term incentive plan award of 400 per cent of salary. Pensions and benefits are ignored for the purposes of simplicity. The face value of the compensation package is therefore US$7,000,000. Assume that the CEO has a subjective discount rate for risk of 16 per cent and for time of 33 per cent. After these discounts have been applied the subjective value of the bonus is reduced to US$1,125,000. The perceived value of the long-term incentive, discounted over 3 years at a rate of 33 per cent per annum, as well as for risk, is reduced to US$1,000,000. Thus the total perceived value of the CEO’s current compensation package amounts to around US$3,125,000. The accounting cost to the company, assuming the bonus and long-term incentive both pay-out at a rate of 75 per cent and that the fair value of the long-term incentive at the date of grant is broadly the same as the amount which is eventually disbursed, is around US$5,500,000.

By redesigning the compensation pack according to our new design principles, the same subjective value of US$3,125,000 can be delivered at a lower total cost to the company and with a lower headline rate of executive pay. The redesigned package comprises a base salary of US$2,000,000, twice the amount payable under the conventional arrangements, and an annual bonus opportunity of 100 per cent of salary. By the time the value of the bonus has been discounted for risk by 16 per cent and for time by 33 per cent, its perceived value is reduced to around US$1,125,000. Assuming that the actual bonus pays out at a rate of 75 per cent, the cost to the company and headline rate of executive compensation is reduced to US$3,500,000.

One of the main objectives of incentive contracts under agency theory is to align the interests of shareholders and managers in order to reduce agency costs. In the present case, alignment of the CEO’s interests with those of the corporation’s shareholders is obtained by requiring the CEO to invest his available after tax cash in company shares until a meaningful shareholding has been obtained, combined with participation in the long-term incentive plan. In the example, under the conventional compensation package, on the basis that the executive is required to buy shares with a value at the date of acquisition equivalent to 200 per cent of salary, and assuming a tax rate of 40 per cent, the combination of shares and long-term incentive plans (LTIPs) represents around 3 years of free cash flow. The shareholding, combined with exposure under the long-term incentive plan, means that at any one time the CEO will have an interest in around US$6,000,000 worth of shares in the company. Under the new design, a similar level of exposure to own company shares can be obtained by investing after-tax free cash flow over a period of around 4 years.

Case Studies

Comparison of Conventional and New Design Compensation Packages

bFree cash flow assumes the executive has an annual cash requirement of US$600,000 and a tax rate of 40%.

cThe time to meet the shareholding requirement is an estimate and assumes that salary accumulates pro-rata during the financial year and bonuses are paid at the start of the following year.

There is at least one American company whose executive reward strategy is consistent with many of the design principles described in this article. In his letters to shareholders, Warren Buffett has explained how Berkshire Hathaway’s incentive compensation system rewards key managers with generous salaries and cash bonuses, but eschews equity plans. Managers are encouraged to buy Berkshire stock with their bonuses, thus benefitting from the strong sustained share price performance of Berkshire Hathaway over many years. By buying stock with their own money, managers accept the risks and carrying costs of ownership as well as benefitting from dividends and opportunities for capital growth. In this way their interests are much more closely aligned with those of other shareholders than would be the case if they were beneficiaries of stock option awards or other types of equity incentive.

Perhaps everyone should have listened more carefully to the Sage of Omaha’s views about executive compensation.