Abstract

An increasing number of studies have focused on fraud victimization. However, fewer studies have specifically focused on financial fraud, a unique form of fraud that relies on victim participation. Using the Supplemental Fraud Survey (SFS), the prevalence and differences between single and repeat/poly-victims of financial fraud were examined utilizing state dependence and risk heterogeneity variables to identify potential differences. Overall, some support for state dependence was found, while less support was found for risk heterogeneity. Reporting the victimization to a family member and having a higher income reduced the risk of becoming a repeat/poly-victim, while identifying as a victim and having a higher total monetary loss were associated with increased risk. Implications for policy, theory, and prevention are discussed.

Keywords

Introduction

It is estimated that in the United States alone, billions of dollars are lost each year to some form of fraud (Buzzard, 2022). Given this, much research has been devoted to examining the prevalence, risk factors, and outcomes associated with these types of crimes, typically falling under the umbrella of white-collar crime. However, the bulk of this research to date has focused on identity theft, a white-collar crime that can include fraud as an outcome of stealing one’s identity (for examples see Golladay & Holtfreter, 2017; Randa & Reyns, 2020; Reynolds, 2021; Reyns, 2013; Ylang, 2020), with less, but increasing published research focused on other types of fraud such as personal financial fraud. Financial fraud is defined as, “acts that intentionally and knowingly deceive the victim by misrepresenting, concealing, or omitting facts about promised goods, services, or other benefits and consequences that are nonexistent, unnecessary, never intended to be provided, or deliberately distorted for the purpose of monetary gain” (Morgan, 2021, p. 3). Examples of financial fraud include charity, products/services, employment, investment, and debt frauds. Considering the National Crime Victimization Survey’s (NCVS) first ever Supplemental Fraud Survey (SFS) in 2017 estimated that more than 3.2 billion dollars were lost to financial fraud (Morgan, 2021), it is vital for research and policies to focus on a range of different types of fraud.

In addition to the finding that billions of dollars were lost to financial fraud and that a projected three million people were victims, it was estimated that a little over 5% of victims in the SFS were poly-victims, or individuals who experienced more than one type of financial fraud (e.g., charity and product or services fraud; Morgan, 2021). Further, victims may have also experienced the same type of victimization more than once, termed repeat victimization. Given that previous research has found that a small proportion of victims, targets, and places often account for a large portion of criminal offenses across a variety of victimization types, it is reasonable to think this may also extend to the crime of financial fraud (for examples see Farrell, 2015; Sherman et al., 1989). Identifying who these victims might be and why they might become repeat, or poly-victims has important implications for crime prevention and has been noted for decades as a potential focus for victimization research (Hindelang et al., 1978). Thus, the current study explores the intersection of two areas that are understudied: repeat/poly-victimization and financial fraud. Specifically, differences in the prevalence and risk factors between single and repeat or poly-victims of financial fraud are examined, with the goal of identifying potential intervention points and policy implications for services to victims and the prevention of future victimizations.

Literature Review

One reason why financial fraud may be understudied is that many victims may not recognize they have experienced a crime or consider themselves a victim of crime. Specifically, for this type of fraud to occur, the victim must actively engage in providing some sort of information to the offender (e.g., social security number or bank information), albeit under false pretenses. This is different from other forms of fraud which requires no formal action on the part of the victim (e.g., bank account information is accessed without the victim knowing). This involvement of the individual in their own victimization may reduce the chances of them recognizing that they have experienced a crime, impacting the chances of reporting, especially to law enforcement, or seeking out any recompense for the offender. Titus and Gover (2001) argued that in these situations, especially where there is considerable participation by the victim, victim-blaming may be a common occurrence. This notion is also argued by Kemp (2022), who found that online fraud victims were more likely to report their victimization than in-person or telephone victims, explaining that the latter two types of victims may have perceived they “let themselves” be a victim and therefore do not identify as victims.

The existing research in this area appears to support this notion. For example, only 14% of victims in the SFS reported their victimization to law enforcement, with a little over three-quarters (77%) reporting the experience to family or friends (Morgan, 2021). Kerley and Copes (2002) found that so few fraud victims in their sample (only 6 out of 224) had reported their experience to the police, that they could not do any meaningful analysis. Further, Schoepfer and Piquero (2009) stated that while about 43% of fraud victims in their sample reported their experience, it was not known who they reported to, making it impossible to know how many reported to law enforcement.

Risk Factors for Financial Fraud

A smaller, but growing, body of studies have examined potential risk factors that may contribute to experiencing financial fraud including demographics, online behaviors, and personality or psychological characteristics. A large proportion of these studies have focused on older adults, with age used as a primary risk factor (Burnes et al., 2017; Cross, 2015; DeLiema et al., 2020; Li et al., 2022; Smith, 2000). However, results are not consistent across all studies (see Ross et al., 2014) with some research finding that younger individuals may be at higher risk for certain types of financial fraud, such as free prize or product fraud (Schoepfer & Piquero, 2009) or financial fraud more generally (Kerley & Copes, 2002; Titus & Gover, 2001; Van Wyk & Benson, 1997). Conversely, Alves and Wilson (2008), found that victims of telemarking fraud most often were between the ages of 60 and 70, suggesting that differences in risk with age may be dependent on the type of financial fraud examined. Research on risks based on other demographic characteristics such as biological sex is also mixed with some studies finding males to be at higher risk (e.g., DeLiema et al., 2020; Trahan et al., 2005 for investment fraud and Alves & Wilson, 2008 for telemarketing fraud) and others finding no relationship between sex and fraud risk (Kerley & Copes, 2002; Titus et al., 1995).

An additional set of studies has focused on identifying online behaviors or personality and psychological characteristics which may predict risk for financial fraud. Examples of online behaviors that have been linked to financial fraud include the amount of socialization a person engages in (Van Wyk & Mason, 2001) and levels of consumer activity (Holtfreter et al., 2008). Schoepfer and Piquero (2009) reported that victims of fraud were more likely to say they engaged in certain risky behaviors such as giving sensitive information to someone over the phone. Another study by De Kimpe et al. (2018) found that victims of email phishing fraud were more likely to engage in digital copying and online purchasing. In a study on investment fraud, DeLiema et al. (2020) found that victims were significantly more likely to engage in certain online behaviors that exposed them to risk such as trading stocks more frequently and making remote investments and were more likely to hold certain attitudes such as materialism and favorable attitudes toward unregulated investing. Other examples of other personality characteristics or psychological factors that have been linked to financial fraud risk are self-control (Holtfreter et al., 2008), loneliness (DeLiema et al., 2022), risk taking attitudes (Van Wyk & Benson, 1997), and cognitive functioning (DeLiema, 2018). Overall, the existing research suggests that a number of different factors may contribute to the risk of experiencing financial fraud.

Repeat and Poly-Victimization Research

While studies on poly, repeat, recurrent, or multiple victimization, among other terms, have increased over the last few decades, research in this area overall still lags. Poly-victimization, as noted earlier, refers to the experience of more than one type of victimization by the same, in this case individual, but could also apply to places or other non-human targets. Often traced to Finkelhor et al. in their 2007 work on poly-victimization among youth, this term has now been applied across several different types of individuals including adult populations (Codina et al., 2022; Ramsey-Klawsnik, 2017), incarcerated populations (Azimi et al., 2021; Listwan et al., 2014), and college students (DeKeseredy et al., 2018; Marganski, et al., 2022; Sabina & Straus, 2008; Snyder et al., 2021).

Regardless of the target, population, or the term used to define repeat or poly-victimization, two findings are consistent; a significant proportion of victims are repeat and/or poly-victims, and these victims account for a large proportion of total victimizations. As noted by Lasky et al. (2021), “One of the most robust findings in criminology is that crime concentrates in a number of ways” (p. 727). For example, Farrell (1992) found that 70% of victimizations were accounted for by only 14% of poly-victims, while Oudekerk and Truman (2017), using 2014 NCVS data, found that victims of six or more incidences of violence made up only 5% victims, but accounted for 27% of all violent victimizations that year.

In terms of the prevalence of poly-victimization, studies focusing on youth have consistently found that a substantial proportion of the victim population experiences poly-victimization (for examples see Finkelhor et al., 2007, 2009; Garnett & Brion-Meisels, 2017; Le et al., 2018; Myers et al., 2017). Sabina and Straus (2008) reported that more than half of the college students in their sample experienced some form of poly-victimization by a dating partner. In a study that included college students from across 27 campuses, 21% of victims were either repeat or poly victims, with 4% experiencing more than one incident of poly-victimization (Kaasa et al., 2016). Finally, in a recent study on poly-victimization among female college students, approximately 32% of the victims experienced more than one type of victimization during the 1-year reference period and a little over 10% experienced at least three different types of victimization (Snyder et al., 2021).

While poly-victimization research is still relatively uncommon, the body of research on repeat victimization is vast by comparison. Numerous studies have been conducted focusing mostly on repeat sexual victimization, bullying, Intimate Partner Violence (IPV), or burglary. Similar to poly-victimization studies, this research suggests that a large proportion of victims are repeat victims (Farrell, 2013; Grove et al., 2012; Moneva et al., 2021; Randa et al., 2019; Short et al., 2009; Walsh et al., 2020). For example, Daigle et al. (2008) found that nearly half of the females in their sample had experienced repeat sexual victimization, with about 7% of females accounting for nearly three quarters of all sexual victimization incidents. In another study utilizing youth data, Turanovic and Pratt (2014), reported that nearly 55% of their sample were repeat victims. Perhaps most telling are the results from a recent systematic review of crime concentration studies that found overall only 5% of victims accounted for 60% of the victimizations, and that many individuals, households, and businesses do not experience any victimization (Martinez et al., 2017). Taken together, this research suggests that repeat and poly-victimization is common across populations and types of victimization, highlighting the importance of continuing to research repeat and poly-victimization using other forms of crime including financial fraud.

The Intersection of Repeat/Poly-Victimization Research and Financial Fraud

Only a handful of studies could be located that specifically looked at repeat or poly-victimization, depending on the definition, among financial fraud victims. Titus and Gover (2001) reported that 8% of their sample had experienced five or more attempted or completed fraud victimizations, while Kerley & Copes (2002) found that a little over 25% of their sample were repeat victims. This was also the only published study that could be located that examined risk between single and repeat victims, noting that repeat victims of financial fraud were more likely to be between the ages of 25–34, differed on income, and were more likely to know the offender (Kerley & Copes, 2002). Relatedly, there has been some research that looks at differences between single and poly or repeat victims of identity theft. While not exactly the same in terms of opportunity structure, research has indicated some differences including repeat victims being more likely to receive reimbursement and lower initial monetary losses (Wilsem et al., 2021). Overall, the lack of research specifically focusing on differences between single and poly-victims of fraud highlights the importance of further research in this area.

Why Repeat and Poly-Victims? Risk Heterogeneity and State Dependence

Two of the leading arguments that are often made for why some people are repeatedly victimized, including becoming poly-victims, are Risk Heterogeneity and State Dependence. Risk heterogeneity asserts that some individuals possess characteristics that increase the likelihood of being targeted or “flagged” making them more vulnerable to victimization (Tillyer et al., 2016; Titus & Gover, 2001). These characteristics often include demographic characteristics, personality traits, and behaviors. This is also sometimes referred to as “between-person differences” (Turanovic, 2018, p. 20). In terms of financial fraud, this would include demographic characteristics often examined in this literature like age, education, income, biological sex, and gender.

State dependence argues that some individuals become repeat or poly-victims because once an individual is successfully victimized, they are more likely to be targeted again or “boosted” (Tillyer et al., 2016; Titus & Gover, 2001). Turanovic (2018) defines this as a collection of events or actions that influence risk, or “within-person changes” (p. 20). In terms of financial fraud, these individuals may be targeted by the same offender, or other offenders, based on the success of the first fraud experience. This may be especially true for victims that do not identify themselves as victims and therefore may not alter any behaviors or actions after the first victimization. The respondent’s self-identification as a victim likely influences their behaviors, risks, protective measures, and other factors that may have an impact on their risk of becoming a repeat or poly-victim. While these have been asserted as separate concepts, more recently it has been argued that both could influence the risk of repeat or poly-victimization and they should be considered complimentary and not competing (Reyns & Fisher, 2018). Thus, for the current study we will examine both concepts as possible explications for differences in single and repeat/poly-victims.

Current Study

The current study seeks to add to the literature on both repeat/poly-victimization and financial fraud utilizing the recent NCVS’s SFS. Specifically, the current study has two main goals: (1) Examine the prevalence and types of repeat/poly-victimization among financial fraud victims and (2) Identify factors utilizing concepts from risk heterogeneity and state dependence, including if the victim classifies themselves as a victim, that may distinguish between single and repeat/poly-victims of financial fraud. Based on these goals we have identified four hypotheses using the risk heterogeneity and state dependence explanations to distinguish between single and repeat/poly-victims: H1) Victims of financial fraud who identify themselves as victims will be less likely to be repeat/poly-victims (state dependence); H2) Demographic characteristics will impact vulnerability (risk heterogeneity) and distinguish between single and repeat/poly victims; H3) Victims who reported their victimization will be less likely to be repeat/poly-victims (state dependence); and H4) Consequences of financial fraud measured as monetary loss will increase the risk of becoming a repeat/poly-victim (state dependence).

Data and Sample

The current study utilizes data from the SFS, which was collected for the first time in 2017. The SFS is one of the five supplemental surveys that have been administered by the NCVS. The NCVS has collected data annually on victimization since 1973, including victimization type, victim characteristics, reporting information, and consequences of victimization. Conducted by the U.S. Census Bureau, the NCVS contains around 150,000 households from across the United States. Selected households remain in the sample for 3 ½ years and all household members over the age of 12 are surveyed every 6 months (Morgan & Thompson, 2022) 1 . In addition to the traditional NCVS, various supplements have been administered to measure specific types of crime. The SFS is one such focused effort.

Supplemental Fraud Survey

The main goal of the SFS was to measure and estimate the prevalence of financial fraud including characteristics of victims, consequences, including both financial loss and emotional impact, and victim reporting. Seven different types of financial fraud including – charity, consumer investment, consumer products and services, employment, phantom debt collection, prize and grant, and relationship and trust fraud were measured. Screen questions, similar to those in the traditional NCVS, were used to route respondents into incident reports. Screen questions were tailored to the type of financial fraud being examined and participants were provided specific examples, such as the screener for free prize scams that asked, “In the past 12 months, did you pay money to receive a prize, grant, inheritance, lottery winning, or sum of money that you were told was yours?” (NCVS SFS questionnaire, 2017, p. 1).

All respondents were asked about their experiences in the last year (12 months). The incident report included information about financial loss, if they reported their victimization (and to whom), if they identified themselves as a victim of fraud, and other consequences they may have experienced (Morgan, 2021). Participants were also asked if they experienced that type of financial fraud more than once, or if they experienced other types of financial fraud. The SFS was administered for three months (October – December) in 2017 after the traditional NCVS questions had been asked. Normally, all household members 12 and up are included in the NCVS, but for the SFS, participants had to be at least 18 years of age. This resulted in about 66,200 respondents who were eligible to take the survey with around 51,200 completing it, for a response rate of 77.3% (Morgan, 2021) 2 .

Measures

Dependent Variable

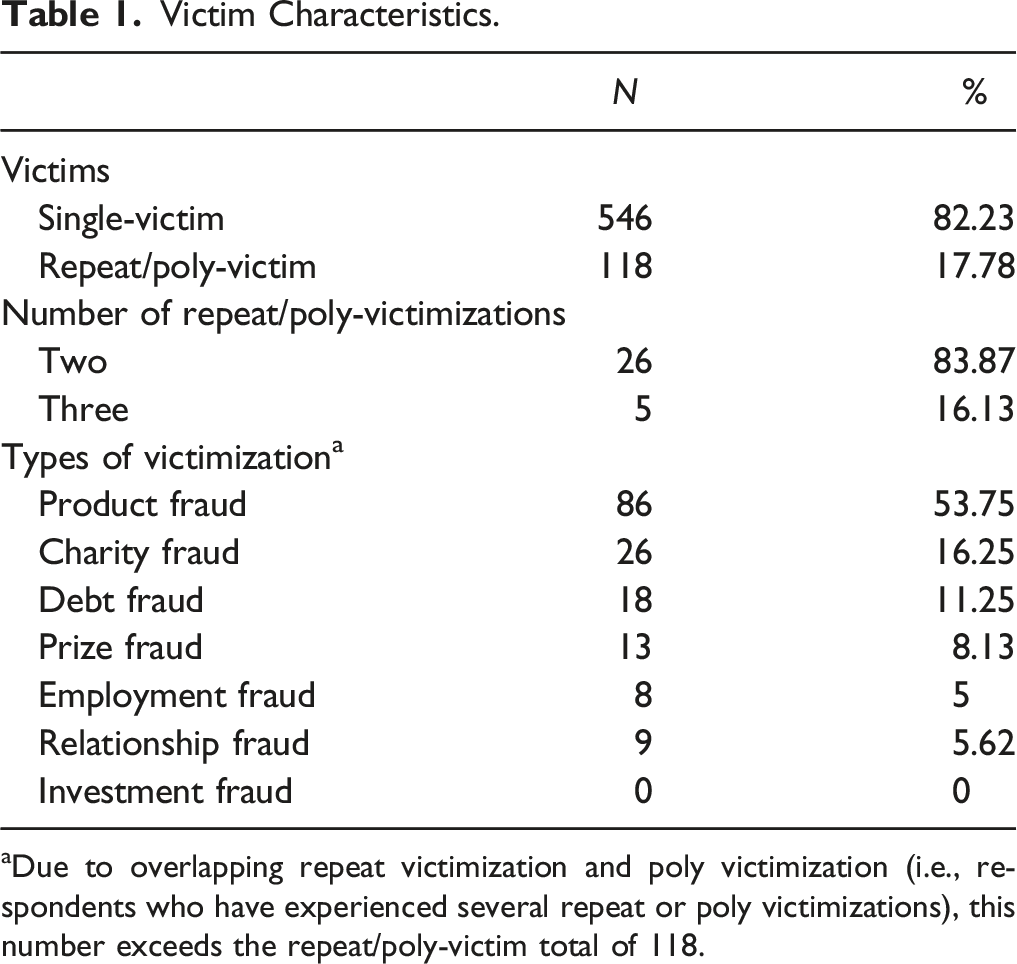

The dependent variable was a dichotomous variable that measured whether the victim was a single or repeat/poly-victim of financial fraud in the last 12 months. Victims that indicated they only experienced one form of financial fraud one time were categorized as single victims (single victims = 0). Victims that indicated they had experienced more than one form of financial fraud or those that indicated they experienced the same type of fraud more than once were categorized as repeat/poly-victims (repeat/poly-victims = 1). In total, 118 respondents out of 664 total victims were categorized as repeat/poly victims, accounting for 17.7% of victims. Of these 118 respondents, 93 victims experienced repeat victimization, 31 were poly-victims, and 6 reported being both a repeat and poly-victim.

Independent Variables

Risk Heterogeneity

The following demographic variables were included to measure risk heterogeneity. Age reflects the respondents’ age in years. Biological sex was measured as (0 = female, 1 = male), with race/ethnicity coded as Black, Indigenous, or People of Color (BIPOC) (0 = White, 1 = BIPOC), and marital status as (0 = single, 1 = married). Education (1 = none/kindergarten, 2 = elementary school, 3 = middle/high school, 4 = college, 5 = Master’s degree, 6 = professional degree, 7 = doctoral degree) and income (1 = <$5,000, 2 = $5,000–7,499, 3 = $7,500–9,999, 4 = $10,000–12,499, 5 = $12,500–14,999, 6 = $15,000–17,499, 7 = $17,500–19,999, 8 = $20,000–24,999, 9 = $25,000–29,999, 10 = $30,000–34,999, 11 = $35,000–39,999, 12 = $40,000–49,999, 13 = $50,000–74,999, 14 = >$75,000) were also included.

State Dependence

Several variables were included to measure state dependence. Total lost measured the total monetary amount the respondent lost as a result of their financial fraud victimization or in the case of repeat/poly-victims, multiple victimizations. 3 Victim status was measured as a dichotomous variable indicating whether the victim self-identified as a victim (0 = non-victim, 1 = victim). It should be noted that respondents may be classified as fraud victims based on their survey responses; however, they may not personally identify as a fraud victim or feel that the incident they experienced constitutes financial fraud.

Reporting behavior was measured using three different avenues of reporting. Each reporting measure was dichotomously coded to indicate whether the respondent reported their victimization to a specific person or agency. Law Enforcement reporting measured whether the victim reported the crime to law enforcement. Lawyer reporting indicates whether the victimization was reported to a lawyer. Family reporting measured if the respondent reported the victimization to a family member. All were coded as (0 = did not report, 1 = reported). Two prior victimization experiences were also controlled for. Property victimization measured whether the victim had previously been a victim of a property crime (0 = no, 1 = yes) and violent victimization indicates whether the victim had previously been a victim of a violent crime in the past 12 months (0 = no, 1 = yes).

Data Analysis

Stata 13 was used to clean and analyze all SFS data. First, prevalence and demographic characteristics for single and repeat/poly-victims were analyzed to better understand how single and repeat/poly-victims compare as well as the prevalence and types of repeat/poly-victimization experienced. Second, a zero-order correlation was run to preliminarily test the correlation of the study variables at the bivariate level. Next, a binary logistic regression was used due to the dichotomously coded dependent variable. The dependent variable of single verses repeat/poly-victimization was regressed on the risk heterogeneity and state dependence variables to test the study hypotheses.

Results

Prevalence and Characteristics of Repeat/Poly-Victimization

Victim Characteristics.

aDue to overlapping repeat victimization and poly victimization (i.e., respondents who have experienced several repeat or poly victimizations), this number exceeds the repeat/poly-victim total of 118.

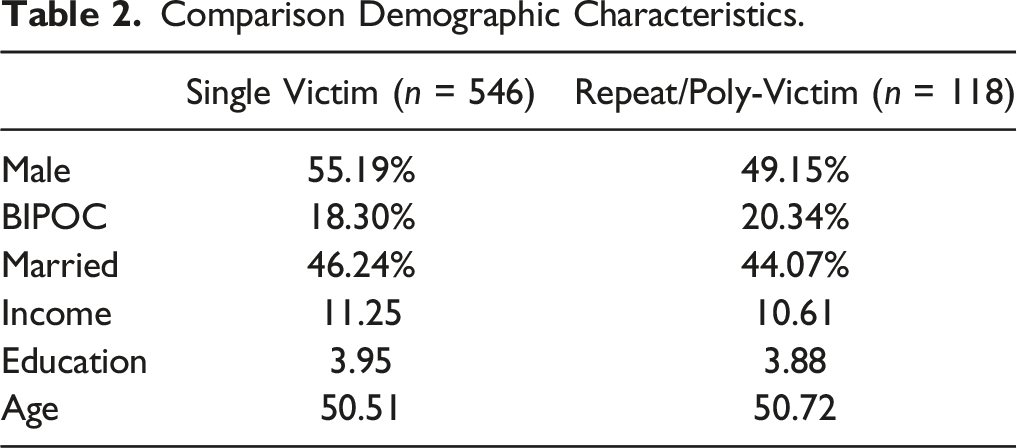

Comparison Demographic Characteristics.

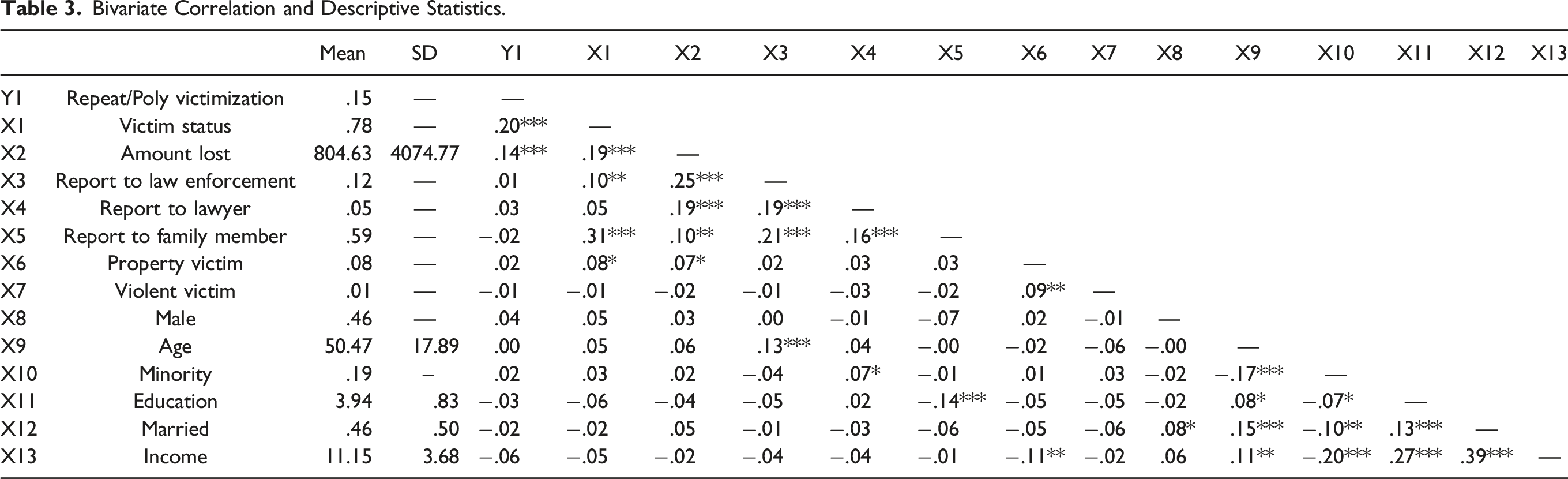

Bivariate Correlation and Descriptive Statistics.

Factors Associated With Repeat/Poly-Victimization

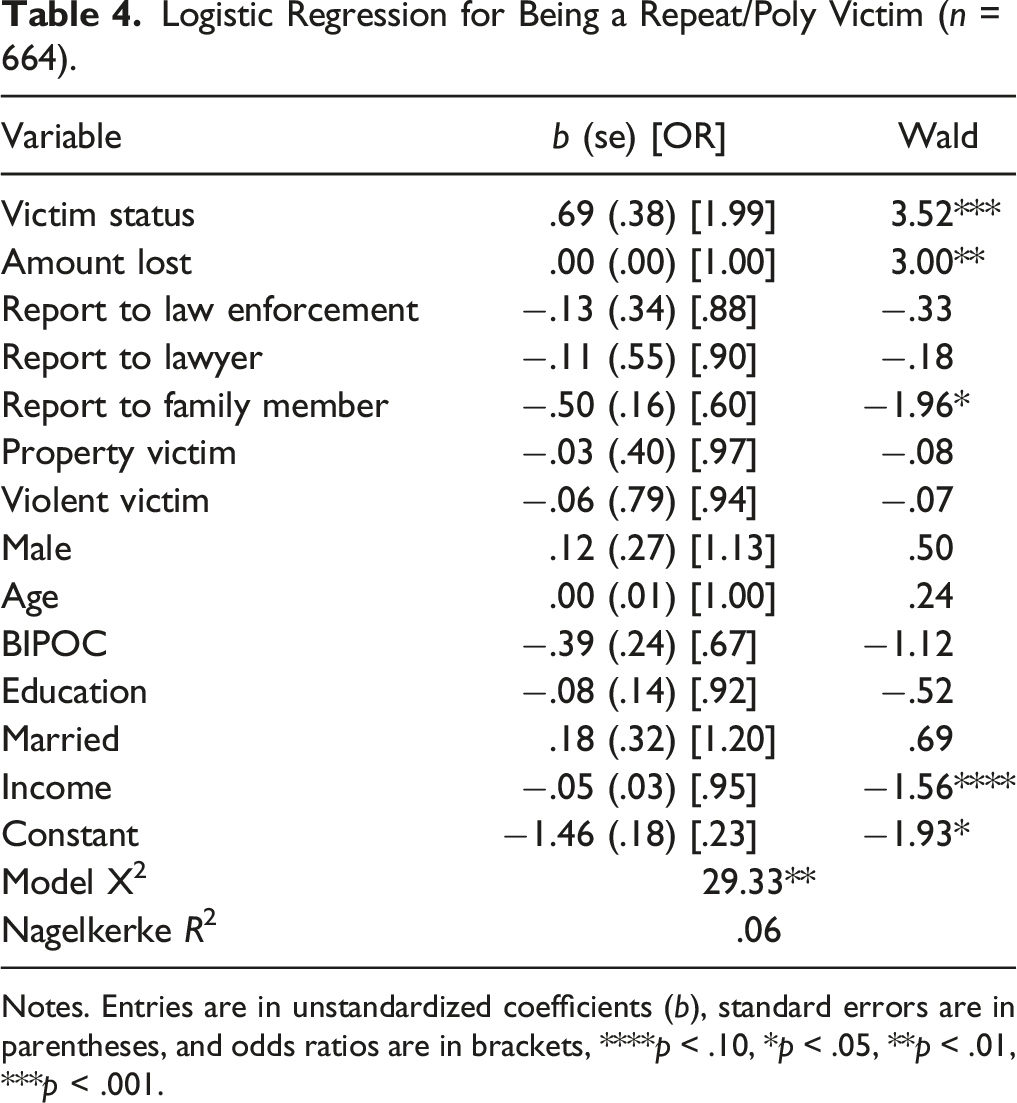

Logistic Regression for Being a Repeat/Poly Victim (n = 664).

Notes. Entries are in unstandardized coefficients (b), standard errors are in parentheses, and odds ratios are in brackets, ****p < .10, *p < .05, **p < .01, ***p < .001.

Overall, some support was found for the variables examining state dependence, with one type of reporting, identification as a victim, and total monetary loss emerging as significant factors. In line with H3, victims who reported their victimization to a family member were significantly less likely to be a repeat/poly-victim (OR = .60; b = −.50; SE = .16). On the other hand, contrary to H1, those who self-identified as a victim were more likely to report being a repeat/poly-victim (OR = 1.99; b = .69; SE = .39). H4 was supported with victims who experienced a greater total loss associated with their victimization being more likely to report being a repeat/poly-victim (OR = 1.00; b = .00; SE = .00).

Little support was found for H2, with only one demographic characteristic measuring risk heterogeneity emerging as significant. Having a higher income served as a protective factor for repeat/poly-victims (OR = .95; b = −.05; SE = .03), which was consistent with H2 expectations. Put differently, the higher a respondent's income and the less likely they were to be a repeat/poly-victim. While some differences existed at the bivariate level (see Table 3), no other risk heterogeneity (demographic characteristics) factors including biological sex, age, or race/ethnicity were significant in the multivariate model.

Discussion

Research on financial fraud remains scarce, with the SFS representing one of the first major efforts to examine these specific types of fraud at the national level in the United States. Utilizing data from the SFS, the current study examined differences between single and repeat/poly-victims for financial fraud. The theoretical constructs of state dependence and risk heterogeneity were included to potentially explain any differences. Overall, some support was found for most of the hypotheses, apart from H1. Identifying as a victim and experiencing a greater monetary loss were related to an increased risk of experiencing repeat/poly-victimization, while two protective factors for repeat/poly-victimization also emerged: reporting to a family member and having a higher income. Both variables decreased the chances of being a repeat/poly-victim.

While many of the variables examined were not significant, especially demographic characteristics measuring risk heterogeneity, the finding that income acted as a protective factor warrants further discussion. It may be that those with higher incomes are more likely to change their behavior after the first victimization to protect further asset loss. This finding is in line with past research on fraud that suggests income or financial stability may be associated with certain types of fraud victimization (DeLiema et al., 2020). Additionally, those with a higher income may feel the impact of the loss less and therefore be less likely to continue with the same potentially risky behaviors in an attempt to recoup losses. Past research suggests that those with a lower income are more likely to report financial burdens associated with fraud victimization (Golladay & Snyder, 2022). This coupled with other emotional outcomes such as stress and depression (DeLiema, et al., 2017; FINRA Investor Education Foundation, 2015) may translate into further behaviors that result in additional victimization. For example, a victim of product fraud in the form of technology support may seek additional technological services that also turn out to be fraudulent in an attempt to reduce the financial burden and recover monetary losses incurred from the first victimization. Further, these victims may be targeted by scams that promise to recover their money, adding another layer of risk.

This may be further supported by the finding that total monetary loss was related to increased risk. While it is not surprising that more monetary loss was associated with repeat/poly-victimization ($2,261.13 on average compared to an average of $558.34 for single victims), given these individuals experienced greater total numbers of fraud, it could explain why some desist or change behaviors and why some do not. It could be that the first victimization resulted in a larger loss, and this coupled with a lower income and greater financial burden furthers the cycle of victimization. Further, these victims could be seen as more attractive targets, given the larger amounts that were successfully taken from them, increasing the potential chances of being targeted again by the same offender or others. Alternatively, it could be that the first fraud resulted in such a minor loss, that the individual did not see themselves as a victim or the need for behavioral change. While we do not have the time course of each victimization to know if this is the case or know exactly how much money was lost with each victimization, it warrants further research to examine this possible explanation.

Unlike risk heterogeneity, several of the variables measuring state dependence were significant including reporting the fraud to a family member. This reporting acted as a protective factor, suggesting that disclosure to someone else may have altered future behavior or in the very least alerted the person to their victimization. Further, family members may have become more involved with the victim, intervening in online activities and financial affairs, decreasing the changes of further victimization. As with many other financial crimes (see Anderson, 2005; Golladay & Holtfreter, 2017; Harrel & Langton, 2013), having familial and financial support are important protective factors associated financial fraud. Given that reporting to law enforcement in the SFS was relativity rare overall (only 11.7% of single victims and 12.6% of repeat/poly-victims), this could be an area of focus for prevention. Specifically, the reporting to anyone, even if it’s not law enforcement, could make an impact and encouraging those that experience financial fraud to discuss it with someone, could reduce the changes of experiencing additional victimization. Interestingly, repeat/poly-victims were more likely to report across every category (e.g., law enforcement, lawyer, bank) compared to single victims, except for family where single victims were more likely to say they reported. This difference was small (59.2% for single victims compared to 56.5% for repeat/poly-victims), but again highlights the potential importance of this type of reporting.

Another state dependence variable that emerged as significant was self-identification as a victim. Those that identified as victims were more likely to be repeat/poly-victims. This finding seems counterintuitive, and was contrary to H1, but may have a couple explanations. First, since the data are cross-sectional, it is difficult to say when self-identification as a victim occurred. It may be that it took several victimizations for the individual to see themselves as a victim, suggesting that some single victims may simply not see themselves as victims. The sample characteristics trend that way with 64% of single victims self-identifying as victims compared to 72% of repeat/poly-victims. It may also be that repeat/poly-victims are more likely to self-identify as victims because the frauds they experienced were more severe. They may have lost more money, which is supported descriptively (as noted above about $550 for single victims and a little over $2,200 for repeat/poly-victims), experienced more distress, or had greater financial impact than single victims. This cannot be extrapolated from the current data but warrants future attention.

Overall, these findings have several implications for research in the area of financial fraud. First, the lack of significance among demographic characteristic variables measuring risk heterogeneity, aside from income, and other variables, aside from reporting to a family member, total amount lost, and victim status, suggests that financial fraud may not operate the same way as other types of victimization. Specifically, the theories that are often used to explain more traditional forms of victimization such as lifestyles/routine activities (Reisig & Golladay, 2019), or in this case risk heterogeneity, may not be as applicable to these types of financial fraud or may need to be rethought in this context. DeLiema and colleagues (2018) reported similar conclusions, finding there was no specific demographic characteristic that emerged as a risk factor for all fraud victims in their study. They assert that the lifestyles/routine activities framework may be most useful when examining specific types of fraud. For example, those with lower incomes might be more likely to engage with free prize scams while the wealthy may be more likely to be a victims of product fraud (DeLiema et al., 2020). Further, Kerley and Copes (2002) also found differences in risk by income varied by type of fraud examined, suggesting nuance is warranted.

Another potential explanation for the lack of demographic characteristic significance is the difference in victim participation. By definition, financial fraud as measured here, requires the victim to actively participate in order for the fraud to be successful through providing the offender information or otherwise engaging in behaviors that make the fraud possible (Morgan, 2021). The victim donates money to a fraudulent charity or willingly provides their money to someone who fraudulently invests. This active participation may result in a different opportunity structure including who is targeted and what demographic characteristics may be most at risk. These findings underscore the importance of not only examining this type of fraud as a whole, but also within, to examine how different types of victimization may have very different factors that contribute to risk. It may be that demographic characteristics are related to financial fraud risk, but the measurement as one variable containing several subtypes obscures any individual impact. Past research in this area has been mixed on findings for demographic characteristics (See Ross et al., 2014 and descriptively the victims were almost identical, see Table 2), suggesting disentangling the types of financial fraud may be vital to our understanding of the role demographic characteristics may play in risk.

A second important implication is understanding how time sequencing may impact becoming a repeat or poly-victim. Past research on repeat victimization has often found that risk for a second victimization is highest directly after the first, then wanes over time (Bowers et al., 1998; Lantz & Ruback, 2017; Robinson, 1998). While the time course may vary (e.g., 1–4 weeks for burglary compared to about 2 months for domestic violence (Lantz & Ruback, 2017; Mele, 2009), the point directly after the first victimization is crucial. This may also be the case for financial fraud. It could be that those that told a family member about the fraud right after it occurred, were less likely to become victims again because of these actions. It is possible that the family member was able to help relieve distress or help with financial burden translating into prevention. Knowing what happens right after the first fraud victimization and also how long before a second might occur are important considerations for future research when attempting to understand what differences might exist between single and repeat/poly-victims. Future research utilizing longitudinal data is needed to fully unpack the potential relationships between variables and how time sequencing may influence risk.

Limitations

While the SFS provides useful information that has not previously been collected on such a large scale, it also has limitations to acknowledge. First the data are cross-sectional and bound by the reference period, limiting the ability to make causal inferences and understand how time sequencing may influence risk. Second, the data do not allow for examination of specific incidence characteristics in terms of understanding how much monetary loss, for example, was attributable to each victimization of the same type of fraud. Third, even though the data set is large, it only contained a total of 664 victims limiting the ability to compare within subtypes of financial fraud. This is further perpetuated by limiting poly-victimization experiences to “one time” and “two or more times.” As discussed earlier, the opportunity structure for charity fraud is likely different than product fraud and some differences may have emerged if it were possible to examine risk factors for each type of fraud. Finally, the SFS does not include all factors that may contribute to risk. Additional factors that could be explored include personality characteristics such as self-control, cognitive abilities, on and off-line risky behaviors, and loneliness. Despite these limitations, the SFS provides important insights into financial fraud that add to the limited research in this area.

Conclusion

The current study examined the prevalence and factors associated with financial fraud among single and repeat/poly-victims. While some significant differences emerged, the lack of differences especially for demographic characteristics highlights the importance of potential differences in opportunity structures for certain crimes. Among the differences that did arise, income and reporting to a family member emerged as protective factors, while identifying as a victim and total monetary loss increased risk of becoming a repeat/poly-victim. Future research should focus on identifying additional risk or protective factors that influence risk and understanding the importance of time sequencing and behaviors directly after victimization such as reporting to aid prevention efforts.

Footnotes

Acknowledgement

The authors would like to thank the anonymous reviewers for their comments and feedback on this paper. Their contributions have been invaluable.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.