Abstract

We analyze an instance of philanthropic law-breaking by a group of Canadian charities, who funnelled millions in tax-exempt funds to foreign recipients. Analyzing 20 years of tax data, we identify a pattern of regulatory violation we are calling the burner charity phenomenon. We track a chronological sequence of organizational behaviour characterized by hibernation, growth, and abandonment, across three linked burner charities. Backstopping burner charities, we show, is a network of public and private foundations. We argue that the purpose of burner charities is to enable foundations to transfer funds to foreign agents while remaining shielded from Canadian law. Combining insights from white collar crime and a Zemiology, we conclude by considering the multi-faceted dimensions of harm associated with burner charities.

Introduction

Charity is big business. A recent Citi Bank report estimates that philanthropic activity comprises upward of 10% of GDP in many G7 countries, while charitable assets worldwide total nearly 2.5 trillion USD (Pitt et al., 2021). Growth in Canadian philanthropy has kept apace. Charitable non-profits represented over 8% of Canadian GDP and employed upwards of 10% of the Canadian workforce in 2021 (Johnson, 2021). In analysing financial reporting to the Canadian Revenue Agency (CRA), Blumberg et al. (2022) estimate that in 2019 Canadian Charities generated $321 billion in total revenue and spent $283 billion.

As with any big business venture, opportunities have arisen for legal transgression, and while generations of scholars have applied social harm and white-collar crime lenses towards explaining systemic corporate abuses and infractions (Rorie, 2020; Simpson, 2002; Sutherland, 1983; Yeager, 2007), to date there exists little in the way of criminological research analyzing the unlawful activities and preventable social harms perpetrated within the philanthropic sector. With regulators across all jurisdictions routinely struggling to provide adequate levels of oversight to their rapidly expanding charitable sectors (see Nardi, (2022) for a Canadian example), and the remarkable growth in the entwined economic, political, and social power of charities, this represents a considerable omission.

Towards beginning to address this omission, we bring insights from white collar and corporate crime research to bear on a case study of seemingly trivial regulatory violations by a group of Canadian charities. Drawing on 20 years of tax data and audit findings obtained through a combination of Access to Information and Privacy (ATIP) requests with the CRA and publicly accessible CRA online data, we track the financial activities of a network of 58 registered charities variously involved in a pattern of serial regulatory violations that we are calling the burner charity phenomenon. Much like burner phones, burner charities appear disposable and readily replaceable. Tracking three burner charities (Gates of Mercy, Beth Oloth, and the Jewish Heritage Foundation) across two decades, we outline a relationship of activity and dormancy, wherein once an active burner charity has its charitable status revoked a subsequent burner charity is activated in its place. Following activation, large volumes of donations are redirected to the newly active charity by a large network of public and private anchor foundations, such that funds continue to move overseas uninterrupted. In elucidating a relatively underexamined form of philanthropic law breaking, this paper contributes to existing literature on white collar offending in the philanthropic sector by demonstrating how wealthy private foundations exploit regulatory weaknesses in Canadian tax law to unlawfully funnel hundreds of millions of dollars to international recipients without legal repercussions.

Our paper has five parts. The next section situates philanthropic crime within criminological research on white collar and corporate crime. Given important differences between charities and for-profit corporations, we address the limitations of white-collar crime frameworks by engaging with a zemiological approach to social harm. Doing so allows us to consider forms of harm and potential criminality beyond those narrowly defined by state legislative frameworks. We then provide a brief overview of Canada’s philanthropic landscape before discussing key precedent setting federal court cases regarding the illegal conduit activities of charities. We then turn to a brief description of our methods, before reporting our findings. We conclude by integrating work on white collar crime and a zemiological approach to social harm to discuss the multifaceted criminality and social harms wrought by burner charities.

Literature Review

Looking to White Collar Crime and Social Harm Research to Understand Charitable Law Breaking

When charities fall into the orbit of the criminal justice system, it is often a result of acting as tax shelters for the wealthy, laundering money for organizations identified by governments as terrorist organizations, or scamming donors (Archambault & Webber, 2018; Goel, 2020). Such relatively rare violations may lead to prosecution under criminal law, and have provided the groundwork for academic research, but they also tend to overshadow the more mundane and commonplace forms of regulatory violations that we are arguing characterize philanthropic crime more broadly.

Of the many staple insights drawn from Sutherland’s (1983) pioneering work on white collar crime, most germane to our discussion is that what counts as crime is not limited to violations of criminal law. Part of Sutherland’s project was to highlight how the fixation with street crime among criminologists, to the exclusion of the crimes of political elites and the relatively affluent, shaped the priorities of the discipline and the criminal justice system (Friedrichs, 2020). Sutherland, and the criminologists who have extended his work, argue that studying white collar crime meant treating violations of civil, administrative, and regulatory law as crimes, in their own right (Jordanoska, & Schoultz, 2020; Nelken, 1994; Sutherland, 1983; Yeager, 2007). Moreover, unlike street crimes, the vast number of people harmed by white collar and corporate crimes often struggle to gain legal and public recognition that they are in fact victims of crime (Dodge, 2020). Indeed, the fact that corporate law-breaking is dealt with through civil proceedings and financial penalties, while drug-dealing is dealt with through criminal law and prison, is less a comment on the relative social harm caused by both than it is a product of how social and political power are unevenly distributed throughout our society.

An expansive analytic imaginary of what counts as crime creates much needed theoretical flexibility for a criminology of white collar crime. However, the opportunities for law-breaking that arise within the complexity of corporate practices and the global financial system makes developing a fixed definition of white collar crime unfeasible (Friedrichs, 2020; Yeager, 2007). A challenge across much of the literature has been developing a typology of white-collar crime that contains enough specificity to be of analytic value. In terms of differentiating white collar criminality from other forms of criminal activity, Friedrichs (2020, p.22) highlights four main categories of elite crime: occupational crime, corporate crime, government crime, and state-corporate crime and usefully distills three general points of consensus across the white collar crime literature: “(i) occurs in a legitimate occupational context; (ii) is motivated by the objective of economic gain or occupational success; and iii) is not characterized by direct, intentional violence.”

While philanthropic crime easily meets the first and third criteria, given that income generating activities of charities are a means to an end rather than ends in themselves; profit and personal success as motivators is arguably minor. Whereas the central purpose of business, as Kennedy (2020, p. 176) reminds us, is to “maximize returns through the efficient and effective conduct of commerce, trade, or the provision of legitimate services,” charities are “mission-oriented” (Emmett & Emmett, 2015). Clearly charities seek to maximize income, but as organizations they are arguably intended as vehicles for advancing broader social and, increasingly, political aims. As such, while a key methodological intervention of white collar and corporate crime research was recognizing the importance of evaluating the “essence of the harm of a particular illegal activity, rather than its status as a criminalized behavior under positive law” (Jordanoska & Schoultz, 2020, p. 9), in the context of philanthropic crime it also demands considering what harms are produced when regulatory violations either bolster or undercut a charity’s social (and political) mission.

Building on scholarly debates about what is to count as crime in the context of corporate law breaking is a broader set of debates about who has the authority to define what constitutes crime. A long-standing critique of early white-collar crime research was that orthodox criminologists tended to cede the power to define crime to states’ legislative and criminal justice systems (Copson, 2018; Ezeonu, 2020; Matthews & Kauzlarich, 2007; Nelken, 2012; Schwendinger & Schwendinger, 1970). If crime has no ontological reality (Hillyard & Tombs, 2004), then establishing its boundaries is a political project in which historically dominant modes of power/knowledge are (re)produced and mobilized to administer uneven social orders. Towards disconnecting criminology from its perceived relationship of servitude to state power, critical criminologists have sought alternative frameworks through which to categorise forms of social harm as crime. Driven, in part, by the recognition that the proliferation of transnational capital flows and neoliberal geopolitical economy means that much of the preventable social harm produced by capitalism exceeds state territorial boundaries, such work mobilizes concepts of crime without ceding definitional power to state legal systems (Ezeonu, 2018; Friedrichs & Friedrichs, 2002; Hillyard & Tombs, 2004).

While a full accounting of a Zemiological approach to social harm within criminology is beyond the scope of this short literature review, Hillyard and Tombs’ (2004) idea of “mass harms” offers a way of de-emphasizing individualistic notions of criminality, which fail to contain largescale harms experienced by whole populations and communities due to things like poor legislative oversight, indifference, and serial technical regulatory and administrative infractions that enable state and corporate violence. Part of the issue here is that the violence of neoliberal state abandonment does not represent deviant behaviour within the context of criminal justice; it is mainstream practice, organized and bolstered by powerful legitimating frameworks. Therefore, something as ordinary as “excess winter deaths,” resulting from state social divestment, for example, does not lend itself to being analyzed by criminological frameworks that assume that crime is something perpetrated by individuals against other individuals (Tombs, 2018). Indeed, Pemberton (2004, 2007, 2015) makes the point that due to the individualist-bias of criminal law, bringing a charge of criminal activity to a corporation, let alone a network of actors from a variety of organizations, is exceedingly difficult.

Critics of a zemiological approach to social harm have astutely pointed out the practical and theoretical challenges of a criminological approach that eschews assigning individual culpability in perpetrating harmful acts, going so far as to argue that such an approach may help enable white collar criminals to be unaccountable for the harm that their actions have caused (Greenfield & Paoli, 2013; Zedner, 2011) Echoing Arendt’s (1987) oft quoted aphorism that “Where all are guilty, no one is”, such critics advance genuine concerns about how justice is to be applied in practice when complicity in the production of avoidable social harms is so widely distributed that identifying the source of social harm is impossible.

Rather than choose between a criminological approach or a social harms approach, Kotzé (2018) suggests recognizing the myriad ways in which criminology (white collar or otherwise) and social harms can function in conjunction with one another. Drawing on Kotzé’s call, in what follows, we integrate a white collar crime framework with a zemiological approach to social harm to track a form of philanthropic crime that we call the burner charity phenomenon. Despite such practices not violating criminal law, white collar crime gives us an analytic grammar with which to assess criminality in terms of the harms produced by corporate law-breaking, more generally. In the context of white collar crime, burner charities may be categorized as deviant because they violate the Income Tax Act, harming Canadian civil society by funnelling government revenues out of the country, and eroding public trust in, and thus support for, charitable organizations (Farwell et al., 2018; Peng et al., 2019).

A Zemiological approach to social harms extends this analysis, forcing us to consider how the broader network of financial and charitable actors are potentially implicated in the reproduction of mass harms not restricted to violations of Canadian law. As our findings show, wealthy anchor foundations enabled burner charities to support Israeli operations in occupied Palestinian territories, such that actors across the financial networks analyzed for this study (whether wittingly or not) are complicit in the reproduction of mass social harms at the very moment they are ostensibly involved in supporting Israeli poverty alleviation and education. In the next section, we situate burner charities within the history of Canadian legal precedent. We then give a brief description of methods and present our findings before returning to these points in the discussion.

An Overview of Canada’s Philanthropic Landscape

There are three types of registered charities in Canada: charitable organizations, public foundations, and private foundations. Upon registration, the CRA assesses a corporation’s or trust’s structure, legal objectives, sources of funding, and how it operates, and assigns an appropriate designation under the Income Tax Act. While all charities are established for exclusively charitable purposes and can issue official donation receipts for income tax purposes, there are important differences between categories.

A charitable organization is expected to conduct most of its own charitable activities, insofar as the organization is expected to spend more than half its yearly income on developing and administering programs aligned with its legal objects [Income Tax Act, 149.1 (1)]. Charitable organizations are allowed to gift some funds to other qualified donees or have a non-qualified donee administer some of its programing as an agent, provided it has a structured arrangement and can demonstrate control and direction over the funds (Canadian Revenue Agency, 2020).

Public foundations, on the other hand, may conduct some of their own charitable activities but generally give 50% or more of their annual revenue to other qualified donees. Like public foundations, most private foundations are constituted primarily as grant-making organizations that advance their founders’ charitable interests, they may, however, also operate more like a charitable organization if their legal objects grant them the flexibility (Blumberg et al., 2022).

Under the Income Tax Act, charitable organizations and public foundations are similar in that revenue originates from arm’s length donors. In both cases, more than half of their governing body needs to be arm’s length as well [Income Tax Act, 149.1(1)]. Large community public foundations (e.g., Vancouver Foundation) and single-purpose foundations (e.g., Canadian Breast Cancer Foundation) are perhaps the most recognizable types of public foundations. They manage large volumes of arm’s length donations, granting funds to smaller charitable organizations and foundations engaged in associated activities (Funk, 2020).

Private foundations, on the other hand, are typically founded by a large capital endowment. Most of their annual donor revenue is derived from a single founder or family, and the governing body need not be arm’s length (Elson et al., 2018). While not exclusively the case, private foundations are typically established by individuals and families comprising Canada’s top 1% of income earners who are affiliated with some of the nation’s most profitable corporations, though corporate foundations (e.g., Mastercard Foundation) play a significant role in the Canadian philanthropic landscape as well (Alepin, 2021). An advantage for the founders of private foundations is that as principal contributors they maintain control over the financial and philanthropic direction of the foundation.

According to Mark Blumberg and colleagues (2022), private foundations are the fastest growing form of registered charity in Canada, with collective assets of over $100 billion held in long- and short-term investments. Capital gains from asset investment are shielded from taxation and represents a significant source of income for private foundations with large endowments. Aside from advancing the philanthropic agendas of their founders, private foundations also provide generous tax relief. A person taxed at Canada’s highest marginal rate can receive a tax credit for up to 57% on 75% of their total income for donating to their private foundation (Alepin, 2021). Corporations can also donate to a private foundation to reduce their tax liabilities.

Canadian Legal Precedent for International Charitable Financial Activities

Much of the Canadian legal precedent surrounding charities operating as conduits, funneling undirected and uncontrolled funds has arisen specifically in response to Jewish charities working with Israeli intermediaries. To be sure, Canadian charities can and do legally operate on an international level. And while the CRA recommends that Canadian-based charities conduct their international operations in conjunction with a currently registered foreign charity, or another “qualified donee” registered with the CRA (Canadian Revenue Agency, 2011), this is not always the case. A Canadian-based charity can, under the Income Tax Act, make use of a locally-based “intermediary” – or agent – that is not a qualified donee or registered foreign charity. Generally, using an international, non-qualified donee, is done on the justificatory grounds that the intermediary has important skills, resources, and/or on-the-ground connections towards maximizing operational impact in the non-Canadian landscape (Canadian Revenue Agency, 2020).

In instances where such international intermediaries are utilized, the CRA is clear that the Canadian-based charity must be able to demonstrate “direction and control” of the actions of the intermediary, as it pertains to the intermediary’s handling of the charity’s funds (Canadian Revenue Agency, 2020). A Canadian-based charity cannot simply accept tax-deductible donations, send this money overseas, and claim to be doing charitable work. It must be able to account for the money, and it must demonstrate that the agent/intermediary is carrying on the Canadian-based charity’s stated charitable purpose. The measures that a Canadian charity might employ to ensure proper direction and control over an intermediary are not fixed, but the CRA recommends utilizing a written agreement, a contract, or some similar such structured agreement which would allow for regulator-imposed verification of record keeping. Documented demonstrability of direction and control of funds and purpose is the key because, as Hayhoe (2010) notes, insofar as common law pertains to agency, the operations of the designated international agent are the operations of the charity itself.

Lack of documentation, specifically in relation to the operations of Israeli intermediaries, has formed the basis of several, prior, licence revocations of Canadian-based charities. Troublingly coupled to this precedent, these now-revoked Canadian charities were allowed to operate for years – both before and after their inadequate recordkeeping was brought to the attention of the CRA. One early precedent was the ‘Canadian Committee for the Tel Aviv Foundation’ (CCTAF), which was registered as a charitable organization in 1985, and had a longstanding written agreement in place with a designated agent in Israel, known as the ‘Tel Aviv Foundation’ (TAF). A 1990 audit found that the CCTAF had contravened multiple sections of the Income Tax Act, including a “lack of documents to support its overseas expenditures, irregularities surrounding preparation and issue of a proper T4 for its president, and improper payroll deductions for its employees” (Canadian Committee for the Tel Aviv Foundation vCanada, 2002, para 8). Beyond conducting the 1990 audit, however, Revenue Canada, the CRA’s predecessor, did nothing to enforce pre-existing regulatory measures.

A second audit, undertaken in 1995 for the operations of the 1993 fiscal year, found the CCTAF again in contravention of 11 sections of the Income Tax Act, again specifically pertaining to the uncontrolled and undirected operations of its Israeli agent, the TAF. At this point, the Minister of National Revenue requested that the CCTAF respond within 30 days as to why its charitable licence should not be revoked. In 1996, the CCTAF responded that: “its agent…had undergone a complete change in management since the Agency Agreement had been signed and was not aware of the reporting requirements in that agreement” (Canadian Committee for the Tel Aviv Foundation v Canada, 2002, para 10). Based upon this justification, along with a commitment to align itself to reporting requirements, the CCTAF was allowed to continue its operations.

A third audit, undertaken in 1999 for the 1997 fiscal year, again found the CCTAF in contravention of numerous sections of the Income Tax Act. A 30-days deadline to respond was again requested; the deadline of which was subsequently extended into 2000. The CCTAF’s response to this deadline was ultimately deemed to be unsatisfactory, which began the CRA’s revocation process. This revocation process culminated in the CCTAF launching an unsuccessful statutory appeal in 2002, resulting in the organization’s charitable licence being revoked.

Similar legal and situational precedent is highlighted in the case of the Canadian charity ‘Bayit Lepletot’. Based on audits of the fiscal years 1998 and 1999, the CRA found that Bayit Lepletot had funneled over $6 million and over $5 million per year, respectively, to a single Israeli agent, claiming that it operated as a go-between for three Israeli-based orphanages. The 1998 and 1999 audits repeated initial audits from 1992 and 1993, which had already determined that Bayit Lepletot had less than adequate direction and control of its Israeli-based agent (Canada Customs and Revenue Agency, 2005).

Bayit Lepletot, faced with repeated requests to address the CRA’s concerns, was allowed six extensions to comply, leading into late 2003. This, despite the CRA’s determination that Bayit Lepletot operated “no programs or activities of its own in Israel, whether directly or through any agent” and that “the Organization merely sends funds to foreign non-qualified donees, over whose activities it does not exercise any control or direction” (Canada Customs and Revenue Agency, 2005, p. 6). Bayit Lepletot then launched a legal appeal against the CRA’s intention to revoke the charity’s status. The appeal, while unsuccessful, had the effect of allowing Bayit Lepletot to continue its operations into 2006 (Bayit Lepletot v. Canada (Minister of National Revenue), 2006).

When these charities operated as funnels, they moved undirected and uncontrolled funds into the hands of one single Israeli intermediary, or agent. In each case, problematically, the CRA allowed this circumvention of the Income Tax Act to continue for years without resorting to revocation. Gates of Mercy, Beth Oloth and the Jewish Heritage Foundation, while operating in the same general manner, and under a similar climate of regulatory relaxedness, have amplified their activities, and have moved money to thousands of international agents primarily in Israel and the U.S. However, while each of the legal precedents discussed above concerned the actions of standalone charitable organizations, in the following sections we demonstrate how Gates of Mercy, Beth Oloth, and the Jewish Heritage Foundation in fact operated in conjunction with each other, such that CRA interventions did little to interrupt the flow of hundreds of millions in untaxed funds being transferred to foreign agents with questionable direction and control.

Methods

Access to Information and Privacy requests have become a staple method for criminological research into the activities of public organizations (Bows, 2019). As a method of data collection, ATIP allows researchers to access texts produced within large bureaucratic organizations that were never intended for public consumption (Larsen, 2014). Our ATIP requests with the CRA differ markedly from traditional ATIP research in that the CRA, as the regulatory body, was not our object of investigation. Rather, we targeted the filings made by Canadian charities to the CRA, which are subject to public disclosure. These include but are not limited to financial statements listing yearly assets, revenues and expenditures, databases of financial gifts received from other qualified donees as well as gifts given to other qualified donees, governing documents and statements of purpose, Notice of Intention to Revoke (NITR) charitable status letters, copies for information filed by charities in response to NITR and CRA audits. Donations made by individuals are considered confidential and not subject to public disclosure.

We developed an iterative, multi-staged ATIP strategy for collecting financial data on charities to track the network of charitable organizations and public and private foundations involved in the burner charity practice. We began by requesting a copy of a list of all gifts received by Beth Oloth from other Canadian charities between the years 2000–2020. Requesting information on a 20-years period, to us, represented the possibility of discovering donation patterns or trends extending beyond the timeframe of the CRA’s audit (2011–2014).

Preliminary content analysis of the CRA’s NITR letter issued to Beth Oloth, as well as analysis of the spreadsheet of gifts received by Beth Oloth from other charities, indicated an obscure, yet notable relationship between Beth Oloth and two other charities, Gates of Mercy (whose charitable status was revoked in 2018) and the Jewish Heritage Foundation. As such, we filed a second round of requests to the CRA for spreadsheets of data on all gifts received by Gates of Mercy and the Jewish Heritage Foundation, between 2000–2020, from other Canadian charities. Given similarities in structure and mode of operation between Beth Oloth, Gates of Mercy, and the Jewish Heritage Foundation, we identified four base criteria for categorizing a charity as a potential burner charity: (1) over 75% of the funds they receive leave Canada, (2) a rapid increase in charitable activity from virtually nil to millions within two fiscal years, (3) Administrative costs are less than 1% of yearly fiscal activity, and (4) very limited financial liabilities in relation to expenditures.

Having identified a potential network of charitable organizations operating as overseas conduits, our next step was to identify if private and public foundations were financially anchoring burner charity activities in a systematic manner. Given the high volume of donations moving through Beth Oloth, Gates of Mercy, and the Jewish Heritage Foundation during their years of operation, we established exclusion criteria to determine a list of potential anchor foundations to target with our next round of ATIP requests. We excluded donations from other charities that were under $5000 (unless a donor organization made multiple individual donations under $5000 in a year, at which point we used the sum of donations for that year). We further excluded all charitable organizations, as well as public and private foundations who did not donate to Beth Oloth for more than three consecutive years. Aside from making the data manageable, the exclusions allowed us to identify the most financially significant foundations with long-term relationships to potential burner charities.

Using these criteria, we identified 114 potential anchor foundations from a total of 301 donors. Within this pool, we identified 40 private and public foundations with consistent donor patterns across all three potential burner charities. These 40 anchor foundations provided the basis for our third round of requests to the CRA for T1236 Qualified Donees Worksheets from 2000 to 2020 for each foundation. T1236 Qualified Donees Worksheets list all donations made by a registered charity to other registered Canadian charities. In addition, we collected the names of the directors and trustees of each of the 40 anchor foundations, which are publicly accessible on the CRA’s Charities Directorate webpage. We cross referenced these names against directors and trustees of the original 114 potential anchor foundation list. We identified another 15 foundations with shared or partially shared board of director membership. This increased the total number of anchor foundations to 55. The rationale was to capture how a network of foundations that share a board of directors may donate consecutively to a burner charity even if an individual foundation within that network may not. After obtaining data responsive to our three rounds of ATIP requests, we compiled all data to search for patterns of donor/donee activity across the 20-years time frame selected for the study.

Findings

Burner Charities in Operation – Hibernation, Activation, Revocation, Repeat

Canadian Revenue Agency data on Gates of Mercy, Beth Oloth, and the Jewish Heritage Foundation indicates that once registered and granted a charitable licence by the CRA, each charity spent several years receiving very limited donations from other registered charities. We postulate that this period of operational hibernation worked towards building each respective charity’s risk profile with the CRA. With a degree of operational credibility duly established, at a certain point – in this case 2008 – the first burner charity, Gates of Mercy, was activated. It then proceeded to move multiple millions of dollars per year into the hands of uncontrolled international agents.

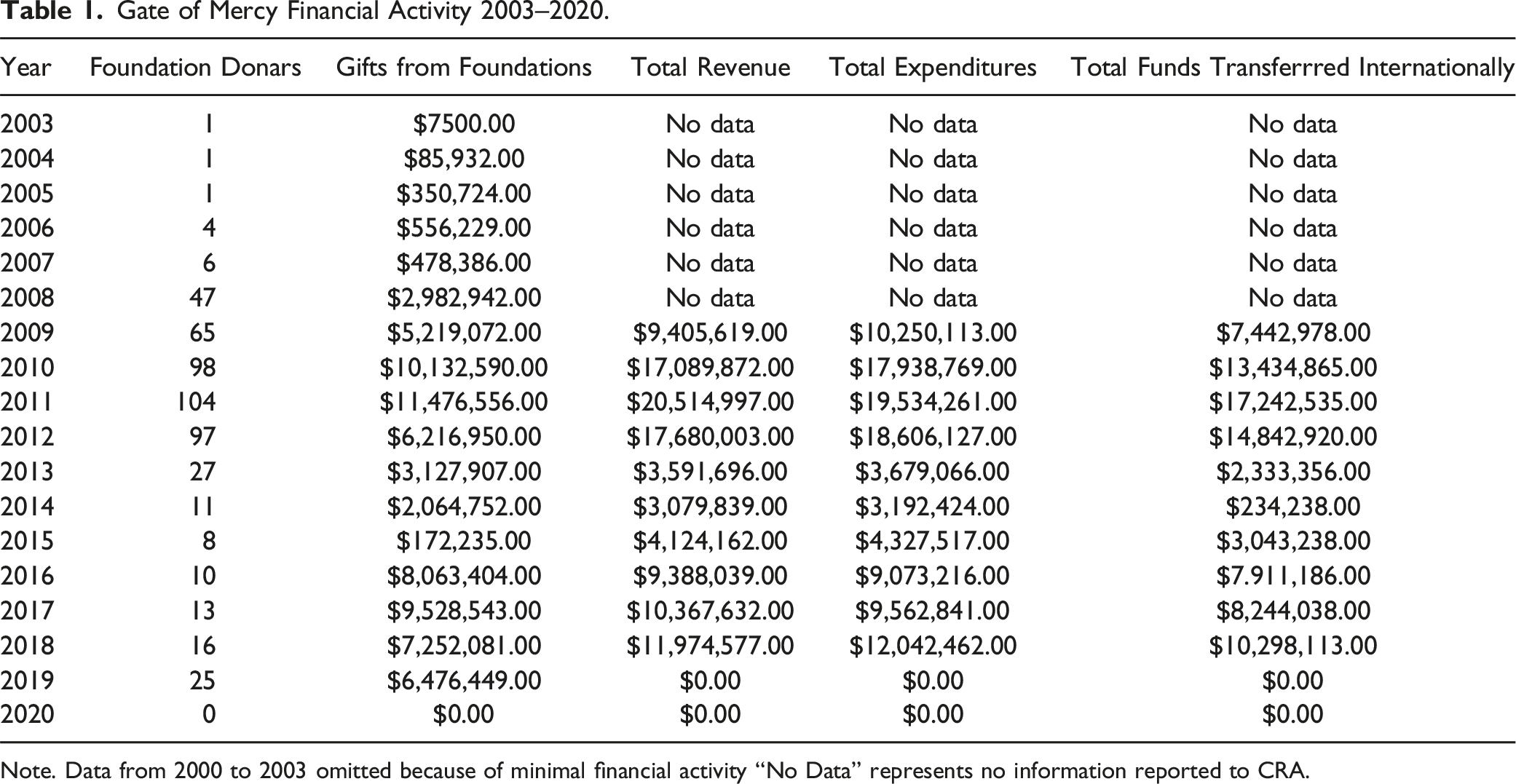

Gates of mercy

Gate of Mercy Financial Activity 2003–2020.

Note. Data from 2000 to 2003 omitted because of minimal financial activity “No Data” represents no information reported to CRA.

This 4-year period represented Gates of Mercy’s apex as the alpha within the burner charity scheme; by 2012, its growth in donations from private foundations had attracted the attention of the CRA, and Gates of Mercy experienced its first audit – for its activities between 2008–2010. The CRA’s audit found that Gates of Mercy had “failed to retain direction and control over the use of its funds,” and had no means to demonstrate or ensure these uncontrolled funds were being utilized for its own charitable activities. (Canadian Revenue Agency, 2018a, p. 1). Beyond this, Gates of Mercy had also failed to keep “adequate books and records”, had “issued receipts not in accordance with the [Income Tax] Act” and had failed to “file an information return in prescribed format” (Canadian Revenue Agency, 2018a, p. 1).

Rather than trigger an immediate licence revocation, or a criminal/terrorism investigation for having sent nearly $30 million in unaccounted money overseas, Gates of Mercy entered a compliance agreement with the CRA in 2012. This agreement was signed by Shmuel Reidel, a director at Gates of Mercy. Considering Gates of Mercy’s actions to be a misunderstanding, the CRA’s compliance agreement was meant to bring Gates of Mercy into regulatory conformity, including developing verifiable reporting practices in all ensuing donation and bookkeeping activities, specifically regarding directing and controlling its overseas agents (Canadian Revenue Agency, 2018b).

Shmuel Reidel’s signing of the 2012 compliance agreement is an important data marker. While Gates of Mercy continued to funnel millions of dollars per year offshore in the ensuing years, Table 1 shows a marked decrease in financial activity and total number of donors post-2011. Seemingly high levels of donor activity at Gates of Mercy between from 2016 to 2018 was driven primarily by two anchor foundations: the Friedberg Charitable Foundation and the Dan-Hytman Family Foundation, both of which donated millions a year until Gates of Mercy’s loss of charitable status. For instance, in 2017 the two private foundations donated a total of $9,008,967.00 to Gates of Mercy, comprising 95% of its anchor foundation income.

The compliance agreement failed to change management and governance practices at Gates of Mercy. A 2016 CRA audit determined that initial issues of non-compliance, far from being resolved, had been compounded. While significantly redacted, the publicly available version of the 2016 audit confirms that multiple agents, on behalf of Gates of Mercy, were still operating in an uncontrolled and undirected manner, and on several occasions were engaged in non-charitable activities (Canadian Revenue Agency, 2018b). Despite Gates of Mercy’s continued operation until 2019, many private and public foundations shifted their donations to Beth Oloth following the signing of the 2012 compliance agreement with the CRA.

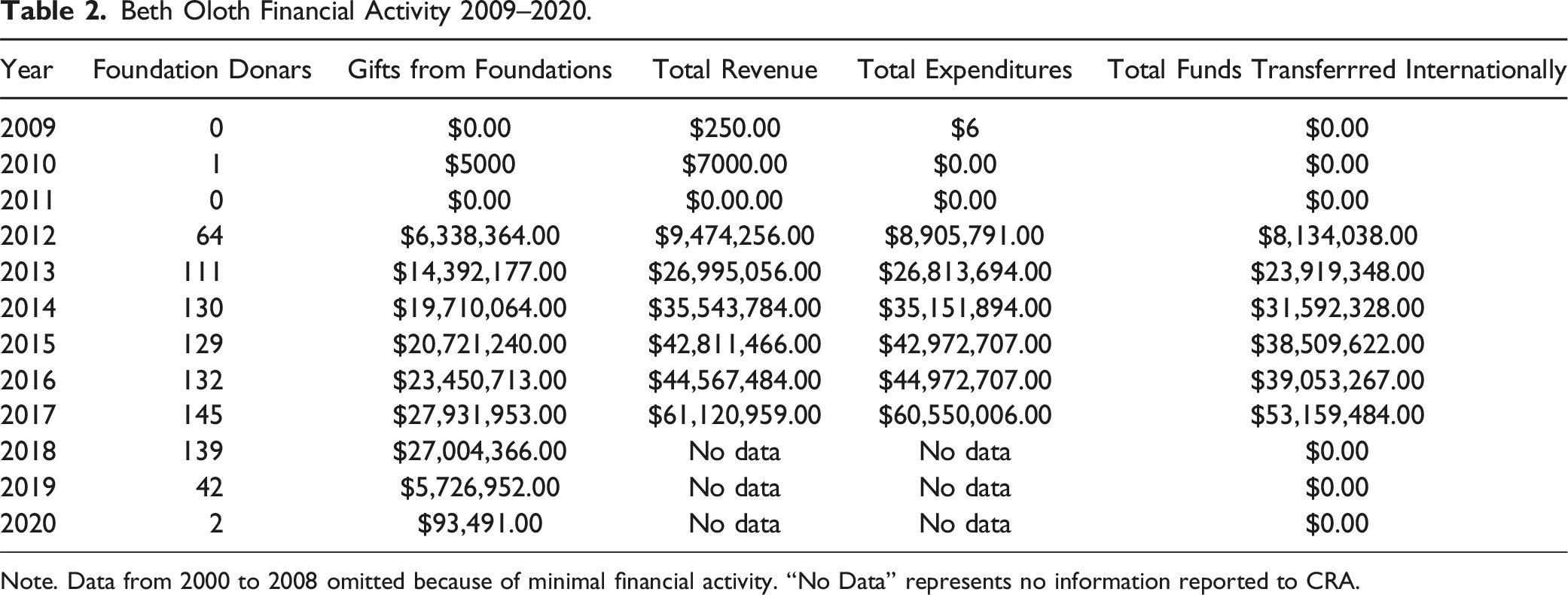

Beth Oloth

Incorporated in 1980 by Yitzchok, Bernice, and David Kerzner, Beth Oloth was initially granted tax-exempt status as a registered charity in 1981. Canadian Revenue Agency tax records show no record of any moneys coming into Beth Oloth between 2000–2005. The years 2006 and 2007 saw a total of four donations from private foundations, cumulatively, and in 2008 the charity took in a total of $7800 worth of donations from other Canadian charities. For reasons unexplained, Beth Oloth was re-registered as a charity in 2008 with Yitzchok and David Kerzner joined by Shmuel Reidel, director at Gates of Mercy, and two others (Canadian Revenue Agency, 2008). Notably, on the 2008 registration application, Kerzner and Reidel claim that Beth Oloth would conduct no activities outside Canada. In the ensuing 4 years, into 2011, it again conducted minimal charitable operations.

Beth Oloth Financial Activity 2009–2020.

Note. Data from 2000 to 2008 omitted because of minimal financial activity. “No Data” represents no information reported to CRA.

The CRA responded in 2016 with an audit of Beth Oloth’s 2011–2014 activities. As with Gates of Mercy, Beth Oloth was found to be non-compliant with the Income Tax Act on a variety of levels. These included: “Failure to be constituted for exclusively charitable purposes”, and a “failure to devote resources to charitable activities carried on by the organization itself” with a specific emphasis on a “lack of direction and control over the use of resources/resourcing non-qualified donees” (Canadian Revenue Agency, 2018a, p. 11). In addition, the CRA evinced a concern that Beth Oloth was depositing cheques made out to Shmuel Reidel and the Gates of Mercy and that this suggested an undisclosed relationship or arrangement between the organizations (Canadian Revenue Agency, 2018a, p. 15).

The CRA’s audit into Beth Oloth’s activities revealed a massive – and accelerating – overseas funnelling operation. In 2012, Beth Oloth had funnelled over $8 million to 713 agents. In 2013, this increased to nearly $24 million to 1784 agents, and in 2014 over $31 million was funnelled to 2274 agents (Canadian Revenue Agency, 2018a, p. 15). Notably, Beth Oloth accomplished this impressive scale of international activity using one fulltime employee, one parttime volunteer, and $100K in administrative costs. The 2016 audit found extensive issues related to control and direction of these agents. In addition, the CRA found it improbable that two staff members could adequately manage over two thousand projects and alleged that “the purpose of the Organization may not be to carry out its own activities, but to fund and facilitate the work of the agents” (Canadian Revenue Agency, 2018a, p. 23). The findings of the CRA’s 2016 audit did little to rectify Beth Oloth’s law-breaking. As Table 2 indicates, public and private foundation donations continued to grow until 2018. A CRA’s follow-up audit found the charity had made no attempt to make its activities compliant with the Income Tax Act. CRA revoked Beth Oloth’s charitable status in 2019.

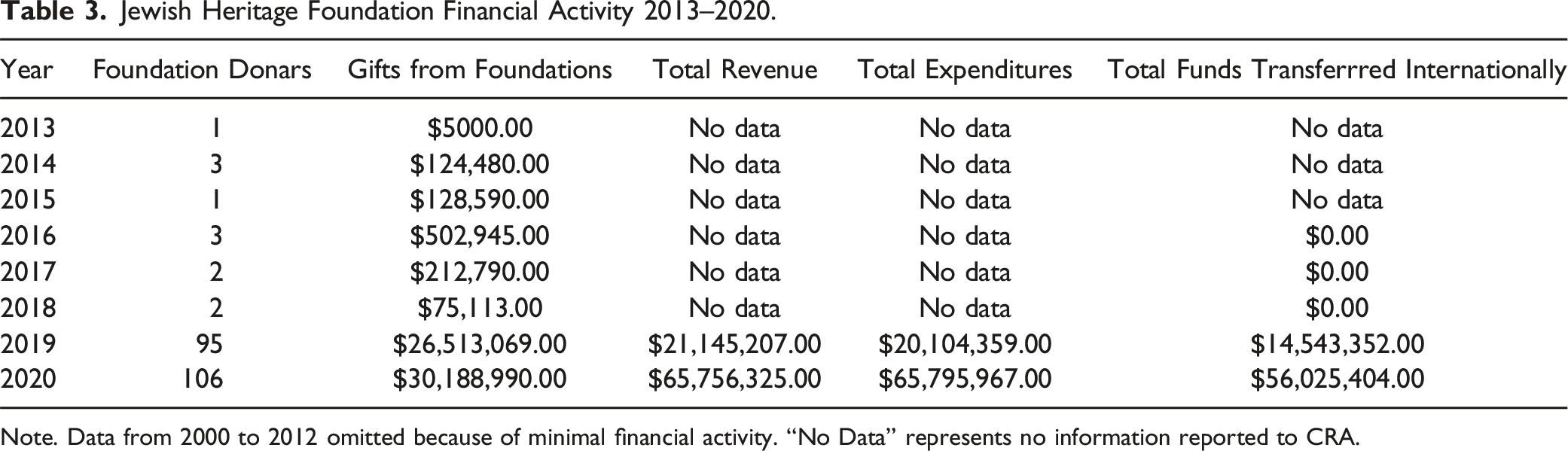

Jewish Heritage foundation

Jewish Heritage Foundation Financial Activity 2013–2020.

Note. Data from 2000 to 2012 omitted because of minimal financial activity. “No Data” represents no information reported to CRA.

Aside from sharing the largess of large private and public foundations, Gates of Mercy, Beth Oloth, and the Jewish Heritage foundation shared connections of people and place. Shmuel Reidel, the director of Gates of Mercy from 2009 to 2016 and director of Beth Oloth in 2008, was also director of the Jewish Heritage Foundation for the same period. In addition, Google Maps notes a recent, 2022, address change for Beth Oloth from 525 Coldstream Avenue, a private residence in Toronto, Ontario, to 32 Brookview Drive Toronto, Ontario, another private residence, and the former corporate address of Gates of Mercy. 32 Brookview Drive is also the address of the Dana Charitable Foundation, a private foundation incorporated in 2017 which counted Shmuel Reidel, Chava Reidel, Baruch Horowitz, and Hennie Tepler as its directors. Tepler is still a director at the Dana Charitable foundation and is currently a director of the Jewish Heritage Foundation.

The burner harity/anchor foundation relationship

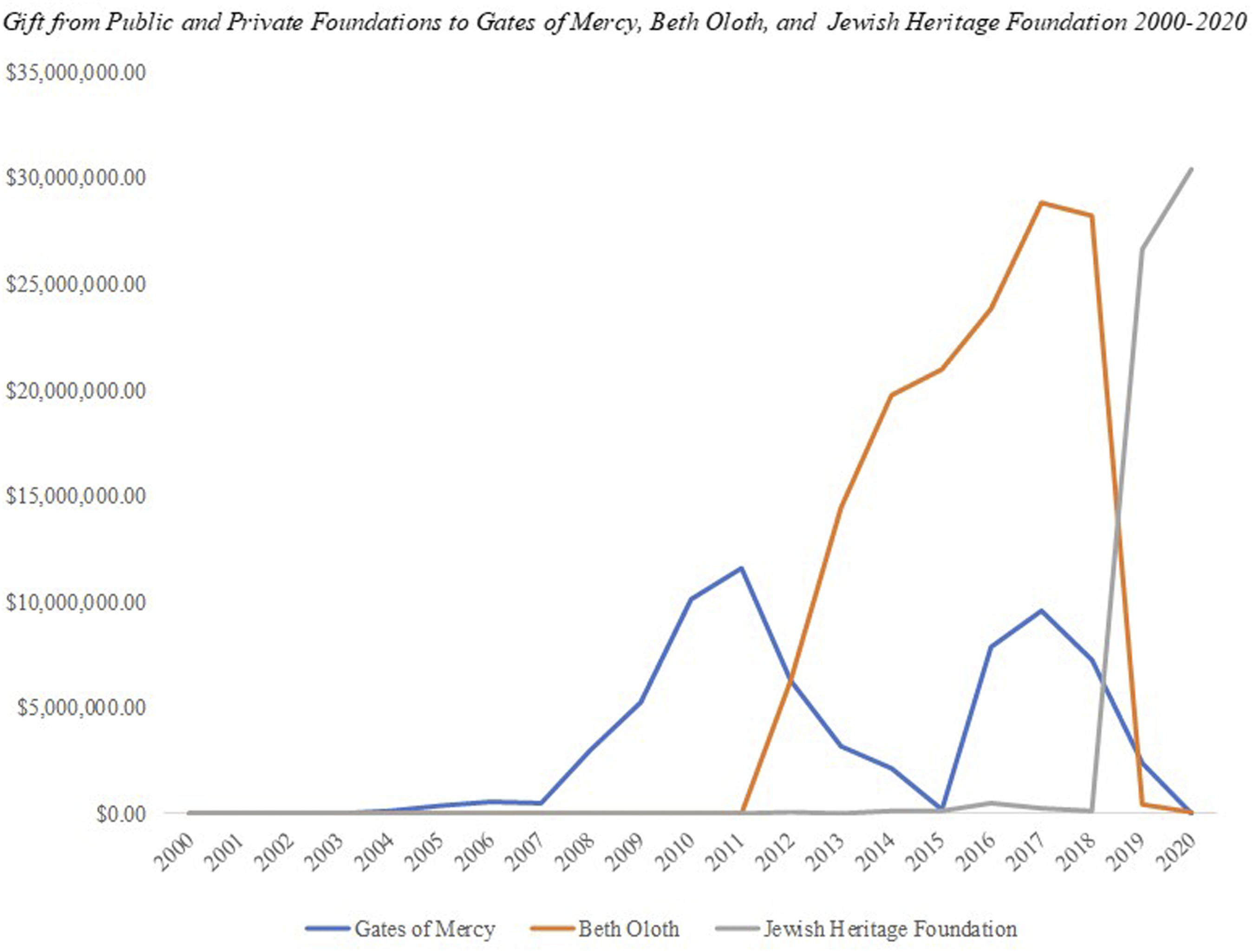

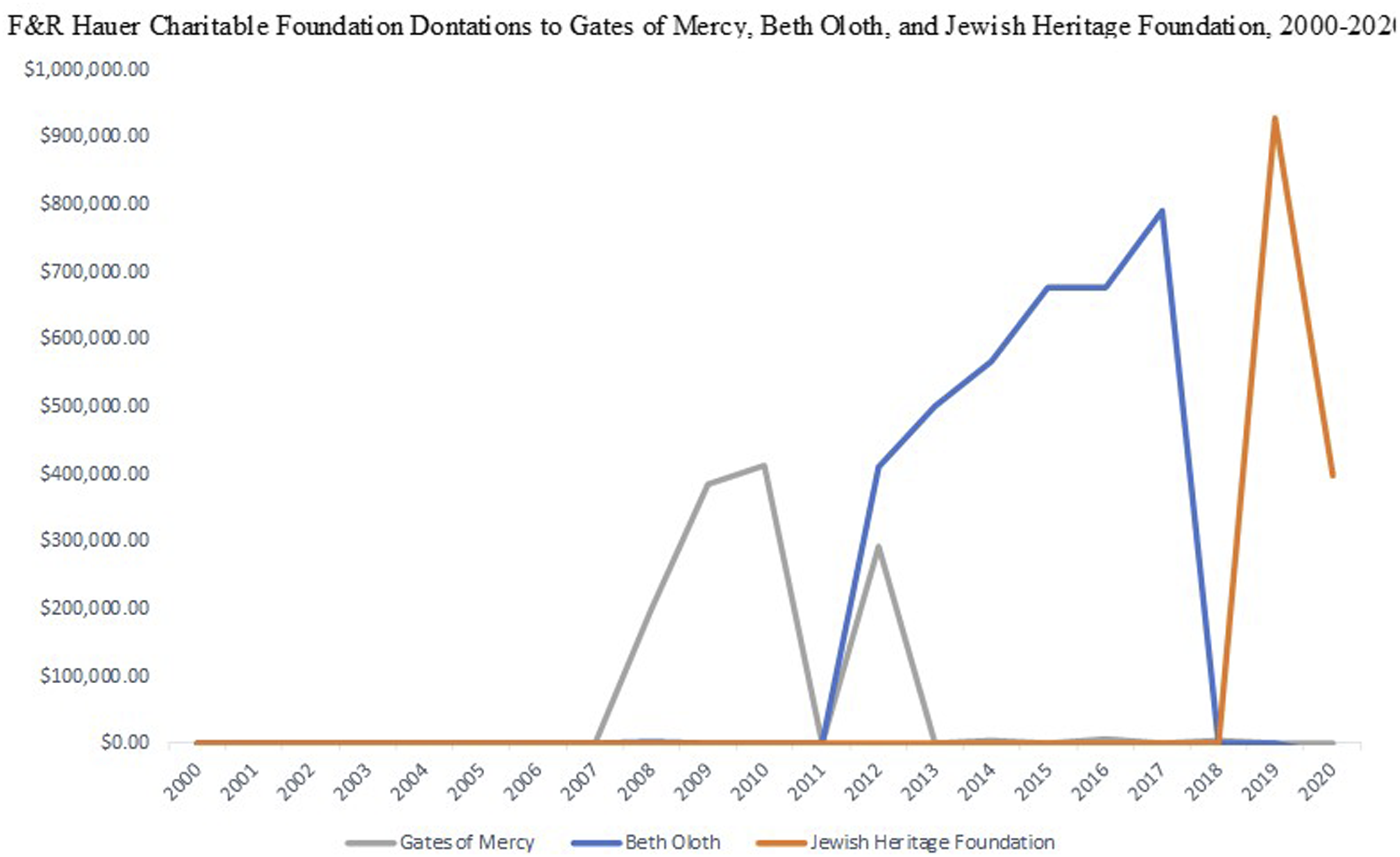

Figure 1 illustrates shifting donor patterns of public and private foundations, from 2000–2020, across all three of the burner charities. Behind the shifting and growing financial support to burner charities between 2008 and 2020 was a network of 55 anchor foundations whose donor patterns mirror the financial activity represented in Figure 1. While year to year, anchor foundations typically represent less than 50% of total number of foundation donors, they account for a disproportionate amount of foundation funding. For instance, in 2017 48 anchor charities donated $16.7 million to Beth Oloth, accounting for 60% of total public and private foundation funding while comprising just 33% of total foundation donors. Most private and public foundations gave intermittently to one or more burner charities. What sets anchor foundations apart is their consistent patterns of giving, which pivot nearly simultaneously to a subsequent burner charity following a CRA crackdown. Figure 2, showing donation patterns of the F&R Hauer Charitable Foundation across all three burner charities from 2000 to 2020, is indicative of the shifting patterns of donor support (with minor variations) we observed across all anchor foundations (for a more detailed breakdown of the financial activities of all 55 anchor charities across Gates of Mercy, Beth Oloth, and the Jewish Heritage Foundation please see Table 4 in supplementary data file). Gifts from Public and Private Foundations to Gates of Mercy, Beth Oloth, and Jewish Heritage Foundation, 2000–2020. F&R Hauer charitable foundation donations to Gates of Mercy, Beth Oloth, and Jewish Heritage Foundation, 2000–2020.

While we have identified 55 individual anchor foundations, many of these foundations may be better understood as networked organizations tied to the root family fortunes of wealthy Toronto-based real estate corporations. For instance, as supplemental data in Table 4 indicates, the Zolty Charitable Foundation, the Chaim Moshe Friedman Memorial Foundation, and the Mae Day Foundation have board members in common who are affiliated with the Toronto-based Zolty-Freidman real estate conglomerate, now operating as Ranee Management Ltd (among other companies), an investment company that owns 7500 units in the Greater Toronto Area (Keep Your Rent Toronto, 2020). Similarly, The Albert & Egosah Reichmann Family Foundation, the Philip & Hannah Reichmann Family Foundation, the Paul and Lea Reichmann Foundation, the B&C Zy Gezunt Charitable Foundation, the IV Charitable Foundation, the Gross Family Foundation, the F&R Hauer Charitable Foundation, the Koenig Family Foundation, and the H&R Brachfeld Charitable Foundation are directed by trustees with familial ties to the fortune generated by Olympia and York Developments, the multibillion dollar, Toronto-based international real estate firm founded by the Reichmann Family, which has spawned a number of successful subsequent real estate corporations (e.g. ReichmannHauer Capital Partners, O&Y Properties Inc., and O&Y REIT). Samuel Grosz, original president of Gates of Mercy, is also the long-time president of real estate conglomerates G & S Regal Group and Greatwise Development Corporation, as well as a director of the Matan Bsayser Foundation, a significant anchor charity. Of the 55 anchor foundations we have identified 30 as operating in seven distinct assemblages, meaning they have partial or total overlap in board of director membership. Such linkages may help explain, in part, how the shifting pattern of burner charity founding is orchestrated on the ground.

Discussion and Conclusion

No law bars Canadian citizens and businesses from directly funding foreign charities, schools, hospitals, military, police etc. through the direct transfer of funds. They are, however, not entitled to the generous suite of tax breaks the Canadian government reserves for charitable giving. When Canadian charities transfer tax exempt funds to foreign agents without clear direction and control, they are operating as illegal financial conduits. A key rationale for Canada’s generous tax regime for private and public foundations and their donors is the belief that such tax incentives will entice wealthy Canadians to fund the growing number of organizations providing the vital social services that successive neoliberal governments have been abandoning for decades (Emmett & Emmett, 2015; Philipps, 2003; Raddon, 2008). Funds held by public and private foundations – whether they are personal income tax exempt funds derived from a founder’s yearly contributions or large revenue generating endowment funds, shielded from capital gains tax and used to manage family estate taxes – have already resulted in considerable tax relief for their founders and significant reductions in government revenues. Offshoring funds subject to generous tax breaks to non-qualified donees amounts to, at best, the Canadian public subsidizing social services in other states. More importantly, when a charity does not maintain adequate direction and control over their funds, the Canadian public may become unwittingly complicit in subsidizing criminal activity and mass social harms.

In tracking the activity of the Gates of Mercy, Beth Oloth, and the Jewish Heritage Foundations between 2000 and 2020, we have sought to demonstrate a pattern of regulatory violation through which over $400 million in tax-sheltered funds were transferred out of Canada to international agents, or, in the regulatory language of the CRA, “non-qualified donees”, located predominantly in Israel and the United States. In using CRA tax data to map what we are calling the burner charity phenomenon, we began by tracking Gates of Mercy’s shift from a state of operational stasis to rapid growth and activity between 2008 to 2012. Following its failed 2012 audit, and subsequent compliance agreement with the CRA, anchor foundation support shifted uniformly to the previously dormant Beth Oloth. The CRA revoked Beth Oloth’s charitable status in early 2019 for, among other things, functioning as a financial conduit for foreign intermediaries. That year 40 anchor foundations, in concert with a host of other donors, again as a group shifted their donation patterns, this time to the Jewish Heritage Foundation. More anchor foundations would follow in the ensuring years. While the 55 private and public foundations we identified as anchor foundations gave a disproportionate share of gifts relative to their numbers, they are by no means the only donors giving to burner charities. Aside from their largesse, what sets them apart is the way in which their giving follows the rise and fall of the burner charities. As of 2021, The Jewish Heritage Foundation had distributed over $121.4 million in Canadian-made donations to hundreds of organizations, primarily in Israel and the U.S. Given the limitations of CRA tax data, we cannot discern whether the foundation’s two part-time staff and $230,686.00 in management and administrative costs constitute sufficient resources to maintain adequate direction and control of these funds. Neither are we able to ascertain what, if any, structural arrangements exist between the charity and its hundreds of intermediaries. As such, despite displaying the characteristics of a burner charity and funded in large part by the 55 anchor foundations’ donations, we cannot conclusively state that the Jewish Heritage Foundation is functioning as a conduit. We have encouraged the CRA to investigate.

To be sure, Canadian registered charities can make grants to overseas agents, provided that the CRA recognizes the agent as a qualified donee, or that the Canadian charity has a structured arrangement with the non-qualified agent, which demonstrates sufficient direction and control over funds. This was not the case with Gates of Mercy, Beth Oloth, or any of the precedent setting charities, such as Bayit Lepletot or the CCTAF, involved in funnelling money to non-qualified donees in Israel. Where burner charities differ from these earlier precedent setting cases is the sheer scale of foreign activities, both in terms of money and number of foreign agents. Limitations of CRA tax data make it impossible to discern what percentage of this $400+ million exited Canada legally and what did not. Regardless, the CRA accused both charities of acting as conduits and revoked their charitable status. Unlike the earlier precedent setting cases discussed above, neither Gates of Mercy nor Beth Oloth sought to appeal the CRA’s decision in federal court. Instead, those involved in running the charities, we argue, opted to activate previously dormant charities to continue their conduit activities.

While the activities of individual burner charities are clearly intelligible as law-breaking within the regulatory gaze of the CRA, the supporting role of anchor foundations in enabling conduit activities is not. Yet the way in which their gifting tracks so closely to the rise and fall of burner charities, we argue, strongly suggest a measure of complicity. To be clear, anchor charities are not breaking the law. Yet their consistent support of burner charities represents, at best, a kind of informed indifference regarding the conduit activities of burner charities. At worst, anchor foundations are knowingly complicit and utilize burner charities as a tax evasion scheme to shift a portion of their family legacy to Israel and the United States, where, due to the lack of direction and control of the agents, the money effectively disappears into a black box. The ability of anchor foundations to collectively shift in tandem across burner charities may arise from the fact that many are assemblages of foundations tied to some of the wealthiest family-owned real estate empires in the Greater Toronto Area and share considerable overlap in governance. Research into charities clearly demonstrates that philanthropic law-breaking results in a loss of donor trust in offending organizations, which in turn translates into a loss of donor revenue (Farwell et al., 2018; Peng et al., 2019). This is clearly not the case with burner charities, where despite clear commonalities in terms of governance and a pattern of serial regulatory violation, donor support increased across each subsequent charity. We argue that this is because the purpose of burner charities is to allow private and public foundations to fund foreign activities that contravene Canadian law while remaining shielded from the legal consequences of their actions. This may explain why financial support for burner charities grew between 2008 and 2020. They have proven themselves to be an effective vehicle for accomplishing this end.

Using the literature on white collar crime and Zemiology, as an integrated conceptual framework for analyzing the burner charity phenomenon, enables us to theorize the nuanced and multifaceted nature of this form of philanthropic crime in a manner not limited by positive law (Copson, 2018; Kotzé, 2018). At one level, the conclusions set forth in the CRA audits allege clear violations of Canadian tax law. In this sense, burner charities are engaged in a species of theft of millions in potential government revenue. In the context of governments claiming to lack revenues to support important social services, the harms tied to this kind of theft are not trivial. As white-collar crime scholars have noted, the social, economic, and political power of the wealthy, tends to translate into radically different legal responses to crimes of the powerful (Comack, 2018; Ezeonu, 2020; Nelken, 1994; Yeager, 2007). That tax evasion is not generally framed as theft seems germane here. Indeed, the fact that the CRA’s findings regarding Gates of Mercy’s and Beth Oloth’s conduit activities has not been brought before the courts and that, to our knowledge, none of the funds have been recovered, is itself telling.

Expanding our understanding of crime beyond regulatory violations codified in the Income Tax Act allows us to better address the burner charity/anchor foundation relationship without having to narrowly frame crime as the intentioned acts of the individuals who run burner charities. With respect to our study, the CRA’s allegations of law-breaking provided an opening for tracking the wider network of actors involved in supporting the philanthropic criminality of burner charities. While anchor foundations may be operating on the “right” side of a legal boundary delineated by positive law, the patterns of support we have identified do suggest a degree of collusion. We approach this cautiously. As Wim Huisman (2020) notes, writing about collusion between organized crime and legal corporations, it can be exceedingly difficult to delineate legitimate and illegitimate activities and practices across the blurred lines of collusion. In the context of philanthropy, this takes on an added dimension of complexity. Many of the anchor foundations identified by this study are demonstrably engaged in legitimate charitable endeavours in Canada and abroad. In addition, funds moved through burner charities likely do produce social benefits for their foreign recipients. Nevertheless, given the rapid proliferation of private and public foundations, and the apparent oversight challenges faced by the CRA, burner charities offer a means of exploiting systemic weaknesses and loopholes in Canadian Tax law. Given the pattern of private and public foundation support, we recommend that anchor foundations face a level of accountability and scrutiny to their donation patterns, rather than having their activities shielded by burner charities.

Stepping out further, and shifting from crime to social harm, the CRA audit of Beth Oloth was unequivocal in its findings that the charity was funding Jewish organizations operating in the occupied West Bank in breach of international law and supporting the Israeli Defence Force in contravention of Canadian policy. Here we see a particular challenge to theorizing philanthropic crime. As much as the financial support distributed by these burner charities may address social needs by supporting hospitals, schools, etc., when the social benefits of charity are bound up in entrenching Israeli occupation of Palestinian territory, they are complicit in mass social harms associated with settler colonial state violence. Therefore, we suggest that philanthropic crimes may often suture social harm for some to the social wellbeing of others in highly uneven and complicated ways. Future work developing a concept of philanthropic crime will need to be attuned to how the entwined crimes and harms perpetrated by charities, work to reproduce and extend the uneven geographies of state and corporate violence.

Supplemental Material

Supplemental Material - International Cash Conduits and Real Estate Empires: A Case Study in Canadian Philanthropic Crime

Supplemental Material for IInternational Cash Conduits and Real Estate Empires: A Case Study in Canadian Philanthropic Crime by Miles Howe and Paul Sylvestre in Journal of White Collar and Corporate Crime

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.