Abstract

BYJU’s, an Edtech startup, was launched in 2011. It became the most valued Edtech in the world with a peak valuation of $22 billion. The COVID-19 pandemic accelerated the growth of the Indian Edtech industry to an unprecedented level. To put the huge COVID shift in perspective, BYJU’s saw its registered students and paid subscribers increase almost 2.85 and 2.5 times, respectively. With more and more funding rounds and the opportunity presented by COVID-19, the unicorn looked formidable. The startup made 19 acquisitions, trying to be the one-stop solution for the Edtech Industry. Since the start of the pandemic in 2020, the startup had spent almost $2.5 billion in almost 24 months. But with everything returning to normal, the startup seemed to have lost its growth spree. The startup got tangled in a host of issues. It faced regulatory and legal issues (court cases and ED raids), brand issues (aggressive marketing tactics and employee layoffs), investor issues (valuation cuts and board directors resigning) and financial issues (auditor resigning, worrying audited numbers and tough acquisitions). Things had drastically changed for them.

Introduction

On 23 January 2024, in Delhi, a harsh winter day not only in terms of the temperature but also because of a particular set of news about India’s global Edtech startup BYJU’s. Two news items about BYJU’s raised many questions for the once-poster child of the Indian startup ecosystem. The first part of the bad news was about the much-delayed audited FY22 results of BYJU, which highlighted the Edtech startup’s vast quantum of losses. They had almost doubled to Rs. 8245 crores, thus undermining BYJU’s growth. Nearly 45% of these losses were from two acquisitions of WhiteHat Jr. and OSMO (The Wire, 2023). The star acquisitions had become a headache for BYJU’s. The second part of the news highlighted how things had also gone southwards regarding the investments. BYJU’s was looking to raise $100 million from existing investors at almost a 90% cut from its peak valuation of $22 billion in 2022. The news items pointed out questions about the strategic choices made by BYJU’s. The inorganic growth strategy through acquisitions had become the go-to choice for the startup. This helped BYJU’s rapidly scale its operations and deepen and diversify its product/geographic offerings to gain a competitive advantage. The speed and magnitude of BYJU’s acquisitions were unparalleled. During the pandemic, BYJU’s made 10 significant acquisitions with more and more funding rounds, creating a lot of buzz. Nonetheless, the news items posed more questions than answers. Had BYJU’s obsession with growth led to this situation? Was BYJU’s trying to do too many things at the same time? Was BYJU’s strategy of inorganic growth the right path chosen by the startup?

The Edtech Industry and BYJU’s Position in it

Before the 2010s, the Edtech sector in India was confined to government organizations/institutions, with a few innovative entrepreneurs taking the field. A lot of experimentation characterized this phase through various initiatives around creating an equal-opportunity learning model for the students. Some early initiatives included free learning modules through NIIT TV, an innovative classroom startup named Educomp, and government initiatives like the National Educational Program in Technology Enhanced Learning (NEPTEL), Sakshat Portal and so on. These initiatives laid the foundation and paved the way for shaping the Indian Edtech market. However, the market was confined at this point due to technological constraints and smaller players catering to niche segments. But post-2010, with the entry of startups like BYJU’s, Vedantu, Unacademy and so on, the concept of free and open access to knowledge gained momentum. They also introduced instructions in various Indian vernacular, personalized content shaped towards skill development, test preparation and certifications. Most importantly, the Edtech startups revolutionized the Indian education system by providing many facilities to children of remote villages and small towns. Simultaneously, it provided opportunities for talented educators and skilled individuals. The opportunities ranged from teaching to technology services like data analytics, cybersecurity and AR/VR. Unlike the government-funded institutions of the pre-2010s, a blend of online and offline learning and personalized attention to students by the Edtech startups led to a complete change in the teaching-learning process. The industry is expected to touch a market size of around $30 billion by 2030 from $5.9 billion in 2023 (Inc42, 2023). The industry had also been a great employer, creating a large pool of gig economy workers, other than the formal workforce. From 2017 to 2022, the Edtech industry generated around 75,000 jobs, even when other sectors saw a slowdown in creating jobs (The Economic Times, 2022). Despite this ambitious growth and expansion trajectory, the Indian Edtech industry had to deal with the urban–rural digital divide in internet penetration, the complex regulatory environment controlling the Indian education sector and the challenge of balancing expansion with quality.

Launched as an Edtech startup in 2011 and headquartered in Bangalore, BYJU’s was named after its co-founder, BYJU Raveendran (another co-founder being his wife, Divya Gokulnath). It became one of the most valued Edtech companies in the Indian Edtech industry in 2009, BYJU’s was a coaching institute for competitive exams, later transforming into an online education provider for school students in 2011. BYJU’s used unique pedagogical tools such as visualizations, videos, real-life examples, and simulations to make learning fun and engaging for the students. In 2015, BYJU’s accelerated ahead of its peers with an exponential increase in subscribers through the launch of its mobile application. The application recorded 5.5 million downloads in its very launch year (Livemint, 2016). The company had started setting new benchmarks for innovation, penetration and delivery in the Edtech space. The COVID-19 pandemic-induced lockdowns in 2020 and 2021 further accelerated the growth of the Indian Edtech industry to an unprecedented level. With the closure of all educational institutions, a high demand for online education was created, leading to an exponential rise in subscribers. The ability to raise funding also helped BYJU’s move towards its goal of becoming the one-stop solution in the Edtech space (Table A1) (Inc42, 2023).

BYJU’s potential attracted many significant investments and investors. Since its inception, it has raised nearly $6 billion during various funding rounds. The first funding came in 2013 from a strong educational investor, Aarin Capital, owned by Mohandas Pai and Ranjan Pai of the Manipal Education Group. In 2015, BYJU’s raised $25 million from Sequoia Capital. Several international investors, namely Chan-Zuckerberg Initiative, InnoVen Capital, International Finance Corporation, Sofina Group and Time Internet, joined the bandwagon of BYJU’s existing investors in the year 2016. The year 2017 saw investments from Verlin Invest. 2018 proved to be a blockbuster year for BYJU’s with investments from Naspers, Tencent and General Atlantic. The same year, BYJU’s also entered the prestigious unicorn club of startups, which focuses on transforming education through technology, innovation and strategic funding. After achieving this milestone, BYJU’s rapidly expanded its reach, fast-tracked by the COVID-19 restrictions. These restrictions led students to turn to online classes, and BYJU’s became the go-to resource for millions across India.

BYJU’s had emerged as a leader in the Indian Edtech space and was ready to enter the global stage. It aimed to broaden its learning solutions beyond K-12 and competitive exams. In 2019, it ventured into coding for kids, upskilling courses for young professionals, educational gamification and blended learning models. The same year, the Edtech attracted more investments from Qatar Investment Authority (QIA) and Owl Ventures. In 2020, the firm saw more investments from General Atlantic and Tiger Global. New investors, namely BlackRock, Alkeon Capital and Sand Capital, also came on board. The subsequent years were significant when BYJU’s touched its peak valuation, raising money from UBS, IIFL Finance, Asmaan Ventures, Oxshott Capital Partners, Davidson Kemper and QIA (Business Insider India, 2020). The chain of investments highlighted how BYJU’s had become an investor magnet, raising funds globally and on a large scale. While every new venture wanted a pie of the growing Indian Edtech industry, BYJU’s reached the goal fast. BYJU’s became the most valued Edtech startup in the world in October 2022 when its valuation soared to $22 billion (The Hindu Business Line, 2022).

BYJU’s Obsession with Growth

The present academic research highlights BYJU’s growth in a positive light without any critical analysis of its strategic choices (Rajan, 2022; Tripathy & Devarapalli, 2021). Hence, when drafting this case study, there was limited information regarding BYJU’s acquisition spree and other significant aggressive investments from the lens of an inorganic growth strategy. Ravindran saw this strategy of aggressive acquisitions and investments as a means to expand the reach of BYJU’s not only in terms of products but also in terms of geographies. With each funding round, Ravindran had the resources to aggressively pursue the inorganic growth strategy. BYJU’s wanted to grow and achieve success, which had been a driver for managers and firms forever (George et al., 2023).

Unlike the organic growth strategy, which is done internally by increasing efficiencies and improving revenues/profits, inorganic is when firms take the path of mergers and acquisitions and growth through external means (Hess & Kazanjian, 2006; Lockett et al., 2011). However, empirical evidence suggests that acquisitions hinder the culture of innovation and, more accurately, have a negative impact on R&D inputs and outputs (De Man & Duysters, 2005). At the same time, though, it provides immediate access to new markets and products (Balakrishnan, 1988; Rabier, 2017), which were at the centre of BYJU’s strategy. This was thus, a faster way to grow vis-à-vis developing internal capabilities. Although initially known for its content and innovative delivery, with increased funding, BYJU’s shifted its focus to acquisitions, or faster access to international markets, aggressive popular investments and product portfolio diversification, as listed below.

Acquisition Spree

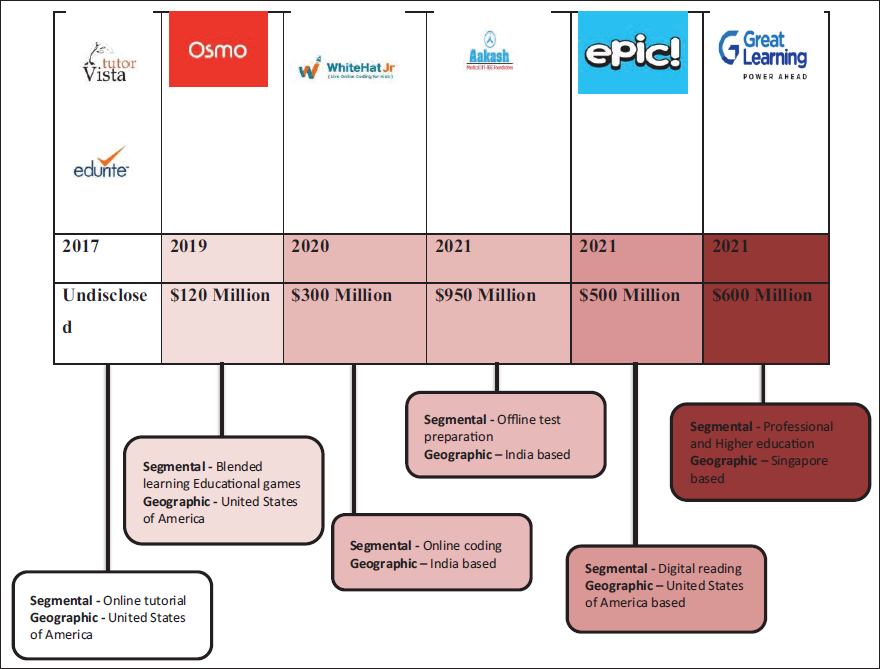

BYJU’s was flush with funds from the various investors pouring in money. With more and more funding rounds and the opportunity presented by COVID-19, BYJU’s looked formidable and went on an acquisition spree. This growth-oriented strategy and ever-increasing valuation led BYJU’s venture into everything possible in the entire Edtech space, but through the inorganic path. BYJU’s made 19 acquisitions, and a considerable number were at the time of the COVID-19 pandemic (Figure 1 for the list of significant acquisitions). As per BYJU’s, these acquisitions aimed to enter new markets and diversify the firm’s product portfolio. BYJU’s tried to be the one-stop solution for the Edtech Industry. With such investments and investors backing, BYJU’s had spent almost $2.5 billion from 2020 to 2022.

Growth

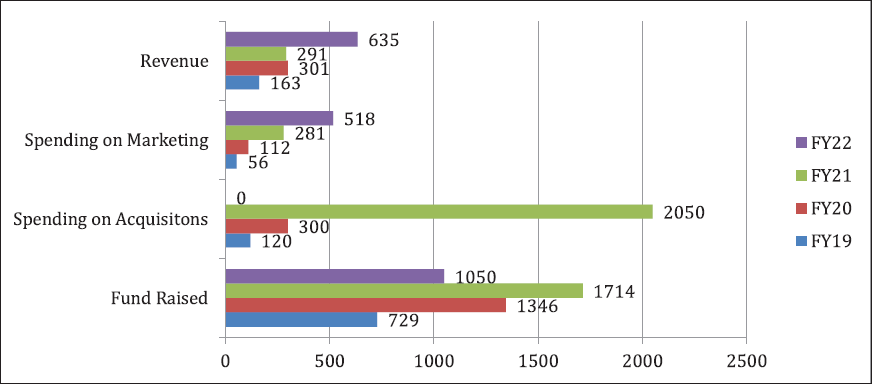

To keep the investors happy and the funds flowing, BYJU’s emphasized the growth of subscribers and revenue. With the shift in online teaching methods during the COVID-19 lockdowns, BYJU’s saw an increase in its registered students and paid subscribers by more than 2.85 and 2.5 times, respectively. Registered students reached 100 million in 2021 from 35 million in 2019, while paid subscribers reached 7 million from 2.8 million during the same period (Annexure A2). In line with this funding increase, there was an increase in acquisition and subscriber growth (Figure 2). The revenue also saw a big jump in FY22 as estimated from the new acquisitions, but the profits did not move along the expected lines.

BYJU’s Financials (FY19–FY22). All numbers in $ million.

Geographic Expansion

BYJU’s wanted to expand globally, and with this vision, it acquired a number of international companies. It also poured in more money to expand its product portfolio and reach across North America, Europe, Singapore and India. The startup even promised to invest nearly $1 billion in the North American market at the time of acquiring EPIC. In line with the aim of growing globally, BYJU’s partnered with Disney to launch a learning application in the United States. The global school, a vocational learning platform, was also launched globally with the aim of reaching markets having higher-paying potential.

Segment Expansion

The acquisitions helped BYJU’s expand into almost all possible segments of the Edtech industry. It strategically expanded into gamification, coding, online tutoring, offline K-12, upskilling and certifications. This brought in many subscribers and a presence that became synonymous with the whole Edtech industry—a one-stop shop.

Reaching the Masses

The company bet big on sponsorships of sports events, trying to catch large audiences. BYJU’s became the official sponsor of the FIFA World Cup in Qatar in 2022 (The Indian Express, 2022). It also sponsored the Indian cricket jersey in the year 2019 (Sportstar, 2019) and the Indian Super League (ISL) team Kerala Blaster, a local football club in 2020 (The Bridge, 2022). The company, in a bid to reach a mass audience, also onboarded big brand ambassadors, including legendary footballer Lionel Messi (Social Samosa, 2022) and famous Indian actor Shah Rukh Khan (The News Minute, 2018). As is evident from the sponsorships and ambassadors, BYJU’s spared no expense in spending money on marketing and promotion. It was very similar to the acquisition spree at the time of the pandemic. BYJU’s spent nearly $280 million in FY21 on promotion, almost 2.5 times what was spent in FY20. At the same time, all of this was being driven by continuing rounds of funding. It all seemed to be going right and in BYJU’s way, with the valuation reaching $22 billion. BYJU’s had expanded both in terms of product and geographic portfolio. The subscribers were at an all-time high, and it seemed as if nothing could go wrong for the Edtech market leader BYJU’s.

What Goes Up Comes Down—BYJU’s Facing the Reality?

The wind in the sails for BYJU’s was knocked out as COVID restrictions started to ease. The students returned to physical classrooms, posing a challenge to BYJU’s pursuit of relentless growth in the virtual arena. From the peak of growth that BYJU’s was at, things started to go downward when the FY21 results were announced. All big acquisitions started to face one issue or the other, which raised a lot of questions about the inorganic growth strategy of BYJU’s. Since the major acquisitions done by BYJU’s were run as separate entities, synergy issues started to arise. This resulted in these acquisitions becoming problematic on multiple points, ranging from financial to branding issues. The acquisitions also created financial stress on the firm. The brand faced issues of negative publicity and numerous marketing mistakes due to the acquisitions (Annexure A).

Branding Issues

BYJU’s brand was hit by its advertising practices and an over-aggressive sales culture. It was criticized for the marketing strategy, especially for its acquisition of WhiteHat Jr. Many complaints were made to the Advertising Standard Council of India (ASCI) about WhiteHat Jr.’s misleading advertisements like claims of applications developed by children who had taken its courses. The ASCI, upon investigation, made the organization remove such advertisements. Several vocal critics also emerged for WhiteHat Jr., including YouTube influencer Pradeep Poonia, who used social media platforms to highlight the aggressive and unethical marketing practices of WhiteHat Jr. He, in many of his videos, posted about dubious claims made by WhiteHat Jr. like one of its students getting a job at Google. He also talked about the application reviews being manipulated by WhiteHat Jr. All this led to him being sued by WhiteHat Jr. in a Rs. 20 crore defamation case. However, ultimately, the company had to drop the suit following a lot of negative publicity that all of this generated. These practices caused much harm to the parent brand and thus became a headache for the firm. Also, BYJU’s sales team gathered a lot of negative press, with stories of products being sold to innocent poor people coming to light. The sales team was pressured to meet unrealistic targets. This negative news about wrongful marketing practices hit the brand in an industry which had trust and ethics at its core (Business Today, 2021).

Financial Issues

The major financial issues that resulted with the acquisitions were significant debt levels, high losses and overvaluation of the acquired firms. BYJU’s, to fund the acquisitions, took a $1.2 billion loan, which got embroiled in legal complications. The acquired companies, Epic and Great Learning, had already been put on sale to settle a $1.2 billion loan before the loan repayments went into legal trouble. BYJU’s got embroiled in a legal tussle with a lender, Redwood, over the Term Loan B (TLB) of $1.2 billion taken in 2021 (Reuters, 2023). BYJU’s not only delayed payments but also sued the lender. The two acquisitions mentioned above had been put up for sale to raise money to pay for this debt. However, they did not get any buyers even when they were put on sale at a devaluation. This indicated towards BYJU’s having overpaid to make the first acquisition. In addition, BYJU’s FY22 financial disclosure, reported after a delay of almost 22 months, projected equally worrying numbers. Revenue for BYJU’s had doubled to ₹5,014 crores, and at the same time, the losses had also increased almost 80% to reach ₹8,245 crores. Even after cost cuts in the form of layoffs, which again were detrimental to branding and scaling down of loss-making businesses, the losses did not come down. These star acquisitions seemed to be the most problematic for BYJU’s with WhiteHat Jr. and OSMO accounting for 45% of the losses (The Wire, 2023)

Integration Issues

Most of the acquisitions were never integrated into BYJU’s fold. The employees of the acquired firms were never integrated into the parent company. Most of the acquisitions ran under their old founders having no integration or synergy with the parent brand. Of all, Aakash Education had been one of the best-performing acquisitions of BYJU’s (Sood, 2024). But it also faced issues with respect to management. Mr Aakash Chaudhary, the founder, was reported to make a comeback as the CEO of Aakash Education through an equity swap agreement. He also tried to buy back the firm. Ranjan Pai of the Manipal Education Group, with an investment of ₹1,400 crore, became the largest shareholder in Aakash Education, leading to a lot of speculation. Great Learning was also an acquisition where the founders tried to buy back the firm from BYJU’s (Livemint, 2023). All these actions by acquired firms highlighted how acquisitions never truly became part of BYJU’s.

Loss of Investor Confidence

Board members and representatives of investors like the Chan-Zuckerberg initiative, Prosus and Peak XV partners also resigned (Singh, 2023). Such were the differences between management and the investors that this exit was denied by BYJU’s but confirmed by the investors. After these resignations, the board of BYJU’s was left with only three members, all from the promoter family. All of this caused an unprecedented situation at the startup, with a lot of speculation all around. The valuation was cut by BlackRock, an investor, by nearly 95% to just $1 billion, from the peak of $22 billion (Singh, 2024). The firm in need of immediate cash infusion tried to raise funds through an off-the-record rights issue from existing investors at a valuation in the range of $500 million to $1 billion, but not with great success. All this happened after investors lost confidence in the firm’s management’s ability to maintain growth and move beyond the decisions that caused the startup to land in this present predicament. The brand, its financial ability, employee morale and the trust of customers were all hit hard by the decisions taken by the top management.

Conclusion

With a teacher’s mission of falling in love with learning and not just being a part of the rat race, BYJU Raveendran set out to change the education industry in India. He aimed to pioneer the Edtech industry in India, which was expected to reach a market volume of $30 billion by 2030. In 2015, BYJU’s launched its mobile application and gained millions of paid subscribers. It hired superstars as its brand ambassadors and acquired 19 firms funded by more than 20 rounds of funding from global investors to reach a valuation of $22 billion. Everyone and anyone in the investor landscape wanted to invest in the poster boy of the Edtech startup space. Investors included some impressive names, including Chan-Zuckerberg Foundation, General Atlantic, Tiger Global, BlackRock and so on. This made BYJU’s the most valued Edtech startup in the world. This journey was helped by the COVID-19 pandemic, where technology reshaped how learning happened amidst COVID restrictions. But with everything returning to normal, BYJU’s seemed to have lost its growth spree. The startup got tangled in a host of issues. It faced regulatory and legal issues (court cases and ED raids), brand issues (aggressive marketing tactics and employee layoffs), investor issues (valuation cuts and board director’s resigning) and financial issues (auditor resigning, worrying audited numbers and tough acquisitions). Everything came crumbling down and continued to do so. What had started out as a dream of a teacher to reach the masses and help the students, was confronted with a number of questions. Did BYJU’s growth obsession lead to its downfall? Was the inorganic growth strategy the wrong path followed? Was there anything that BYJU’s could have done differently? What are the lessons for startups from BYJU’s? How can BYJU’s still come out of this situation and survive the current crisis?

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.