Abstract

The case is about the food start-up Zomato, which floated its initial public offering (IPO) on 14 July 2021, with the aim of raising money from the general public. It aims to evaluate whether the company is overpriced or underpriced compared to its price band and offer price despite being a loss-making food start-up. The case also highlights how the two valuation techniques—discounted cash flow technique and relative valuation technique can be used to calculate the implied price or intrinsic value of Zomato. Also, which techniques will be better for calculating the intrinsic value and comparing it with the current market price to conclude whether the IPO was overpriced or underpriced? It analyses the advantages and disadvantages of each of these techniques for a firm like Zomato.

Introduction and Background

Zomato was founded by Deepinder Goyal, an alumnus of the Indian Institute of Technology (IIT) Delhi, who completed his graduation in Mathematics and Computers and joined Bain and Company. During his tenure in this company, he realized the demand for food cards and founded Foodie Bay in the year 2008. The company provided information, menus and reviews of eating outlets and food delivery options in select cities in India. The company was renamed Zomato in 2010 and became the largest food aggregator and delivery start-up. Goyal hailed from a middle-class family in a small town in Punjab (a northern state of India) and aimed to achieve big in life. He identified the problem in which people had to struggle and stand in a queue to get food. Moreover, not much choice was available to people in those days.

Business model of Zomato was aggregator-based, which used to bring the buyers and sellers on the same platform. The start-up was a high-technology firm which could efficiently bring these players together to create an effective business model. Moreover, the start-up, at the time of listing, was not generating huge profits but was a unicorn, and most of the value was derived from the future potential of the food business.

The value of the firm was calculated from the future potential of revenues and in the case of start-ups, a large portion was derived from the future growth potential.

Culinary Habits in India

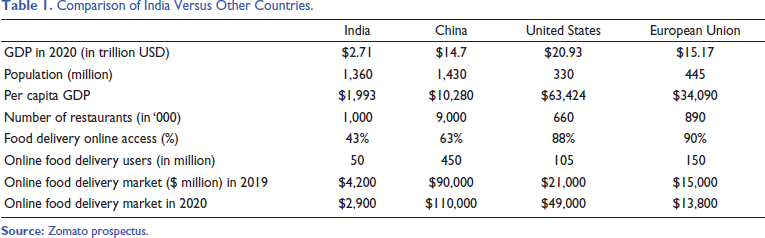

Food is a part of the culture of any country, and the culinary habits of people change over time. A food historian such as Khan et al. (2023), in her book ‘Forgotten Foods’, has mentioned the importance of home-cooked food in India and some of the recipes which had become forgotten and are no longer cooked in Indian households. Traditionally, in India, home-cooked food was considered to be important from both a health and hygiene factor. Nutritionist like Diwekar (2016), in her book ‘Indian Superfoods’, emphasized the importance of home-cooked food and simple food for the long-term health of individuals. Firms like Zomato were targeting the urban, time-poor families who would like to order from outside or visit restaurants and avail themselves of some discounts available through various portals. Professor Damodaran, New York University (NYU) Stern, in his blog, mentioned the rise in the outside food culture in India and also compared it with China and other countries. But still, food delivery and eating out were very less compared to other countries, specifically China. One of the reasons was the low per capita GDP and GDP of India, compared to countries like the United States, China and the European Union. Also, the discretionary income of consumers was also responsible for the low online food delivery compared to other countries of the world. Higher disposable income of the households would lead to higher spending on food. Another reason is that India lacked online access compared to China and other developed nations, as online presence was a requirement for a booming online delivery market.

Comparison of India Versus Other Countries.

The valuation of the firm was derived from the sales growth potential that existed in the Indian food market and hence relied more on the terminal value of the cash flows based on the continuous growth for indefinite time period. This was in accordance with the accounting principle—going concern—where it was assumed that businesses existed for the foreseeable future. Also, one of the important aspects found in the valuation was that a major portion of the value came from terminal value rather than the initial forecasted cash flows. It was assumed that the firm would grow at a constant growth rate forever. Businesses usually showed a high growth rate for initial 3–5 years, followed by a stable growth rate forever. Terminal value was calculated using this stable, constant growth rate.

Funding History

Zomato had raised funds from 21 rounds of funding and 25 investors. Zomato received its seed round of funding in the year 2010 from institutional investor Info Edge, and this was to the tune of $1 million. Info Edge remained invested in the start-up till the exit at the time of floating of the initial public offering (IPO) (refer to Figure 1).

IPO Decision

Zomato decided to go public and tap the markets to raise funds from the general public and also list on the two national stock exchanges—National Stock Exchange and Bombay Stock Exchange (BSE) in India. The capital market was a market where long-term funds flowed, and hence, financial instruments such as bonds and equity were traded, whereas the money market was a market for short-term instruments. The capital markets were divided into the primary market and the secondary market. The primary market was a market for new issues, whereas the secondary market was a market where existing securities were bought and sold. Zomato, being a tech start-up, had a risky business model, which got funding from venture capital and private equity players. Zomato decided to get listed on the Indian bourses and raise funds from the public. Investors investing in Zomato would demand a rate of return for providing capital. The rate of return that Zomato would be required to provide to the suppliers of capital was known as cost of capital (Pathak, 2014).

The cost of equity capital was the return provided to the suppliers of equity capital in the firm. The capital asset pricing model was used by investment bankers to calculate the cost of equity capital. This return would be higher than the risk-free rate, and equity investors would demand a risk premium over and above the risk-free rate. The risk-free rate was the guaranteed rate which investors got on risk-free securities, such as government bonds. The cost of debt, on the other hand, was the rate of return which the providers of debt capital expected on their investment. The cost of capital/overall cost of capital was calculated using the weighted average of the cost of equity and the post-tax cost of debt.

Zomato decided to tap the primary market as the firm aimed to strengthen its delivery system and infuse more funds into the start-up to expand further. The primary market provided an opportunity to firms to raise capital from the public. Zomato IPO opened on 14 July 2021 and ended on 16 July 2021. The allotment for Zomato IPO was finalized on Thursday, 22 July 2021. The shares got listed on the BSE and NSE on 23 July 2021. Post that, the firm became a listed firm and had to abide by the byelaws of the stock exchange. Listed firms had to be very transparent and compliant in their operations and had to provide quarterly results on a regular basis. Also, more funds are required to further enhance the information technology (IT) infrastructure on which the start-up relied for creating a robust aggregator-based business model. The firm also planned to invest heavily in its delivery infrastructure in order to strengthen the delivery service further. The key costs included payments to delivery partners, support expenses, call centre expenses, insurance expenses, storage, warehousing costs, consumables expenses and transportation costs. The firm proposed to utilize the net proceeds from the offer in both organic and inorganic growth. Organic growth involves growing through expansion of its own assets, whereas inorganic growth involves growing through acquiring other firms and utilizing the synergy. The firm intended to invest in marketing, promotion, branding and advertising for customer acquisition.

The firm also grew using inorganic growth as a method to forwardly and backwardly integrate with firms in similar businesses, as well as technology firms, to provide them with better know-how in the process.

It is an asset-light organization and had not invested in fixed assets to that extent. Zomato’s core was its technology infrastructure, and the main driver of their business was nurtured and developed over the years. Zomato, an aggregator in the food tech space, brought the restaurants and customers together. The platform was used to search for the restaurants, deliver the food and book a table in the restaurant; customer reviews were also generated through this programme. They also provided marketing tools to facilitate the restaurants to acquire new customers along with the last mile of delivery service. The firm needed to invest in three core areas to sustain growth in the future: customer acquisition, delivery infrastructure and technology infrastructure. The firm proposed to utilize the net proceeds from the offer in both organic and inorganic growth. The firm intended to invest in marketing, promotion, branding and advertising for customer acquisition.

The firm also grew using inorganic growth as a method to forwardly and backwardly integrate with firms in similar businesses and also technology firms to provide them with better know-how in the process.

Moreover, post the first COVID wave, there was a 70% drop in business along with the liquidity crunch that it created. According to Deepinder Goyal, Zomato was operating at 30% due to the COVID-19 pandemic (Business Today, 2020). The government put restrictions on foreign direct investment in start-ups from Chinese firms. As a result, many funds from China such as Ant Financials decided to exit from their investment in Zomato, leading to a cash crunch situation.

The company decided to tap the IPO market to meet this contingent situation as it was left with 6 months of cash. The IPO was oversubscribed both in the retail and qualified institutional buyers (QIBs) segments. It was subscribed 4.99 times in retail and 7.45 times in the QIB segment.

The IPO was also a bet on the business model of unicorns such as Zomato, along with the future growth potential. The performance and scale of the company were also dependent on the preferences of Indian customers and their eating habits.

Zomato had an offer price band range of ₹72–₹76 and adopted an offer for sale cum public offer. It used the book-building method to discover the price of a share. Although it opened at ₹115 on the listing day and closed at ₹125.8 on the same day, it was proposed that the proceeds would be used to fund organic and inorganic growth; the remaining would be used for corporate purposes. About 18.55% share of the pre-equity share capital was offered to Info Edge to create confidence in other investors in terms of demand and pricing.

The business model was based on the assumption that the eating habits of the Indian population might undergo a major transformation and eating out would become a trend. People might eat out more than cook at home. Zomato offers (B2C offering) food delivery and dining out, in addition to hyperpure (its B2B offering), which was a customer loyalty programme and included both dining out and home delivery. These offerings enhanced the value of the programme and, in addition, facilitated new customers and increased customer engagement.

Since 2015, the country has witnessed a GDP growth rate of 7%, but it got impacted due to the COVID-19 crisis. Due to worldwide lockdowns, the country’s economy contracted by 7.3%, as per the Indian National Statistics Office. India experienced a growth rate of 9.5% for the fiscal year 2022. This was higher than the projected growth rate of the world economy at approximately 5.4%.

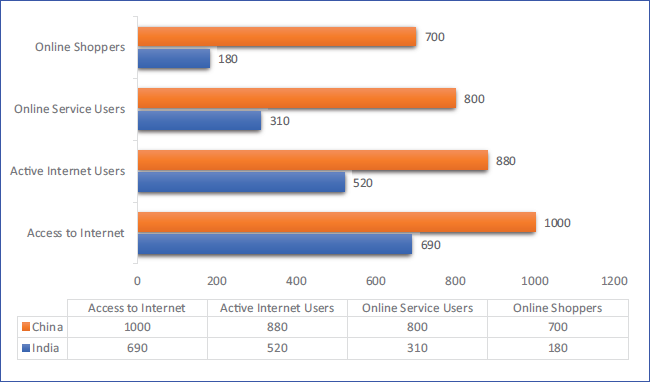

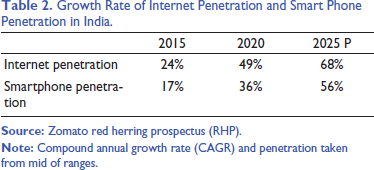

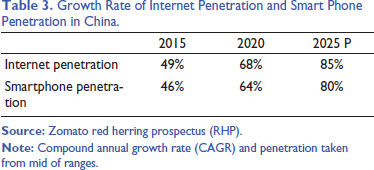

World Economic Forum estimated that India would become the largest consumer market by 2030 in terms of communication, infrastructure, education, rising spending on capital expenditure and more job opportunities. Consumption had shown a rise in recent years and was mainly service-industry-driven. India had an advantage in terms of the young working population, with a median age of 28 years compared to the median age of 38 years in countries like China and the United States. Also, as per the World Bank Report, around 470 million people resided in urban areas in India, which was approximately 33%–34% of the Indian population. Smartphone penetration also nearly doubled in India from 2015 to 2020. In 2020, around 98% of phone connections were mobile, compared to 90% fixed connections in the same year, as per the Department of Telecommunications. The adoption of the internet in the country had also considerably improved due to the launch of Reliance Jio. It was $1/GB, and as a result, the number of users increased to 660–690 million users in 2020 from 310 to 330 million in 2015. Moreover, the availability of smartphone users had improved due to low-cost alternatives from China. With the smartphone revolution, customers have access to platforms that are based on high technology and provide an interface between buyers and sellers. The smartphone boom represents an opportunity to high-tech firms whose business models can be accessed by the parties through mobile device and the internet (refer to Tables 2 and 3).

Growth Rate of Internet Penetration and Smart Phone Penetration in India.

Growth Rate of Internet Penetration and Smart Phone Penetration in China.

The stock price opened at ₹76 on the BSE and reached ₹138 at its peak price on the listing day, and finally closed at ₹125.85. Zomato was subscribed 38.25 times and it included five times subscription in the retail segment (see Table 1).

Zomato got listed on the National Stock Exchange and BSE at a premium price of 53% and 51%, respectively. Post-listing, Zomato’s market capitalization rose up to ₹1,000 billion (The Economic Times, 2025).

There had been a downtrend in the prices since the day of listing. Table A1 (refer to Appendix A) indicates the price trend from the listing month. There had been a 6% fall in the value of the Zomato share in the last year from ₹134.55 to ₹55.45 per share (Shah, 2021).

Moreover, there had been a decline in the trading volume by almost 80% 1 over the last 1 year (based on Table A1 in Appendix A). Analyst and professor, Professor Damodaran categorized the IPO to be overpriced at ₹75 and valued it at ₹41 before the launch of the IPO. Recently, the valuation had been revised to ₹35 per share (Damodaran, 2006, 2021).

Company Financials

Operating profit for the firm had been negative from 2019 to 2022. The revenue for the firm increased to ₹41.9 million from ₹13.1 million from 2019 to 2022. Net income and earnings per share remained negative from 2019 to 2022 (refer to Tables A3 and A4).

Free cash flows were also found to be negative for the time period between 2019 and 2022, along with the cash flows from operating and investing activities. Profit margin ratios were negative during this period, along with return on equity from 2019 to 2022 (see Appendix A).

Way Forward

Zomato had cleared the way for unicorns riding a wave of high valuation, to raise capital from the market and list on the bourses. But, it had lost its value on listing, raising concerns about the future of start-ups when the real value got unlocked. Was Zomato’s share overpriced, and was there a gap in the intrinsic value and market price per share, leading to the fall in prices in the market? Which would be the right valuation approach for Zomato—discounted cash flow or relative valuation?

Zomato share had shown a downward trend in the last year. The big question before the analyst was the pricing of the share—was it overpriced or underpriced?

Also, was it feasible to rely on a revenue-driven model and list start-ups like Zomato which were operating in a super-competitive market and yet not profitable? Was Zomato a profitable investment for an investor? Was Deepinder Goyal right in having this price band for the Zomato IPO?

Discussion Questions

Q1. Was the Zomato IPO overpriced or underpriced?

Q2. Which valuation technique should be applied to value Zomato—DCF versus relative valuation?

Q3. What are the post-listing price trends of the last year indicate about the deviation between intrinsic value/fair value and market price? Do you think that the price band was underpriced, leaving a lot of money on the table?

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.