Abstract

The case study discusses the buyout strategy of Dell Inc. Dell Inc. was a market leader in PCs in the early 2000s. Due to a substantial change in technology, the market share of PCs declined significantly, and Dell missed opportunities and recorded a decline in sales of over 10% from November 2012 to January 2013 due to a fall in shipments. After analysing the complex circumstances, Mr Michael Dell, CEO and Chairman of Dell Inc., decided to convert the publicly traded company into a private company in 2013 through a buyout deal. On 28 December 2018, Dell was again listed on the New York Stock Exchange for trading through a tracking stock strategy. The case study deals with several ups and downs of the company and also provides a platform to discuss the various benefits of buyouts.

Introduction

The literature indicates a significant increase in the delisting of publicly traded companies globally in the current scenario. Researchers have documented various economic reasons for the delisting of firms, such as declining stock prices and increasing volatility. Distressed firms tend to go private to increase their value, while firms may choose to go private when offered a substantial premium over the market price. Additionally, younger firms may be compelled to go private by public-market investor (Boot et al., 2008). Delisting actions are categorized into two types (Macey et al., 2008): involuntary and voluntary delistings. Furthermore, the economic significance of delisting was analysed through the ratio of delistings to initial public offerings (IPOs; Li &Zhou, 2008). In 2012, the ratio of delisting was 1.3 and 1.5 for the US and European markets (Loureiro &Silva, 2020), respectively, recorded more than once from the listings of IPOs. The literature also documents that firms are more likely to go private due to several reasons, such as less analyst coverage, fewer institutional holdings, more concentrated ownership, and higher mutual fund ownership at the time of IPO compared to firms that remain public. Additionally, firms that go private may be more illiquid (Amihud &Mendelson, 1988), have less share turnover, provide less information to public (Leland &Pyle, 1977), offer fewer growth opportunities, carry high leverage (Kim &Weisbach, 2008) and allocate fewer resources to research and development or minimal capital expenditures (Bharath &Dittmar, 2010).

The following section discusses the suggested answers for the questions given in the case study.

What Are the Major Reasons and Benefits of Becoming a Private Company (Delisting) from a Publicly Listed Company?

Suggested Answer

Reason of Delistings

Previous literature has documented that most delistings result from a failure to meet numerical standards, such as a minimum net income and a minimum market value for shares outstanding. Delistings can also occur due to factors such as increasing volatility, distressed firms going private to increase their value, firms going private when offered a substantial premium over the market price and younger firms being forced to go private by public-market investors.

Benefit of Delistings

There are both pros and cons associated with the delisting of public firms to private firms. However, some benefits arise when a firm faces financial constraints and has limited expansion opportunities in the current scenario, prompting it to opt for delistings. The following are some of the benefits:

Financial reporting to public is not required by sharing financial statement. Minimum shareholding by public is not mandatory. Saving on account of listing fees, annual trading fees and so on leads to cost reduction for the company. Hostile takeover becomes difficult due to low public shareholding Low volatility in the share price as shares are not traded in the market, that is, no speculation. Directors can take faster decisions as ballot voting is not required.

Motives for Dell to Become Private from a Publicly Listed Company in 2013

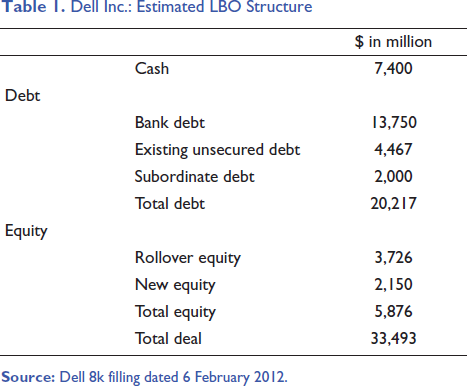

Dell Inc.: Estimated LBO Structure

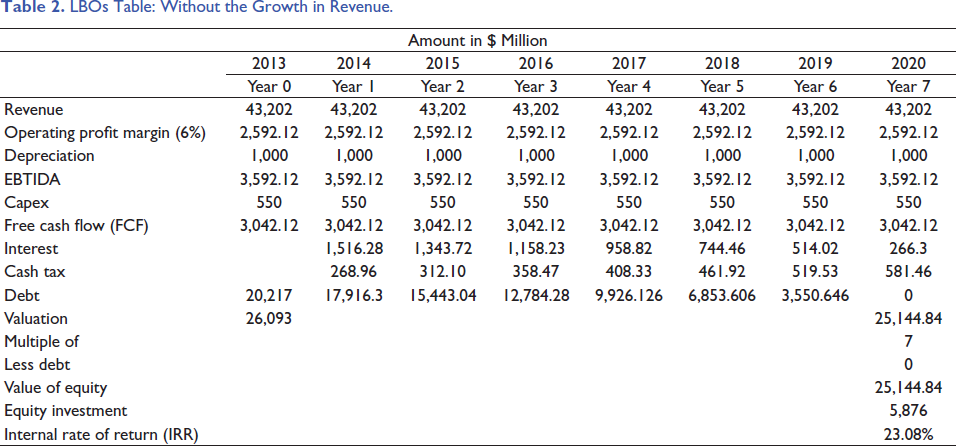

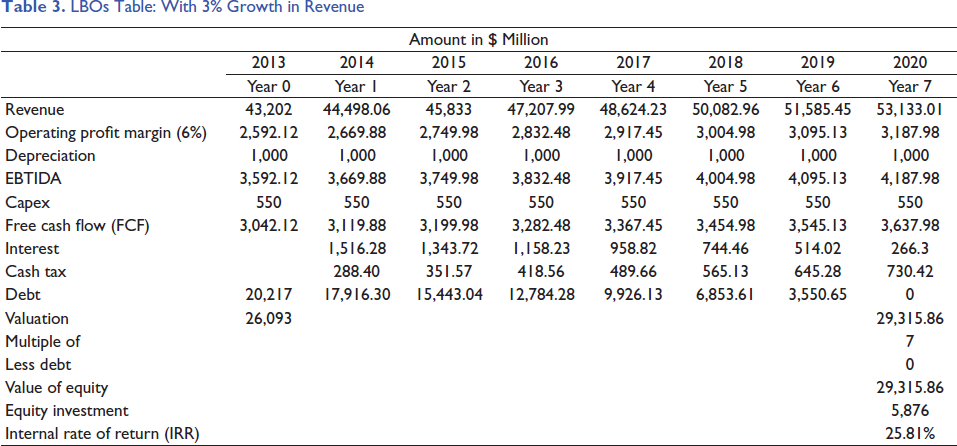

1. What is your understanding of a LBO? You are required to analyse the LBO process with the given assumptions with an exit multiples of seven. Michael locked a deal to take Dell private for $24.4 billion, marking the largest LBO after the financial crisis. Dell collaborated with the Silver Lake private equity firm and Microsoft Corp to rescue the distressed computer company. The funds were sourced from various channels. The average cost of debt was assumed to be 7.5% for 7 years. The revenue for 2013 was recorded as $43,202 million. Assuming an operating profit of 6%, a tax rate of 25%, depreciation of $1,000 million and capital expenditure of $500 million was observed. You are required to consider two scenarios: first, there is no growth in the revenue, and second, the revenue grows at the rate of 3% (Tables 2 and 3).

LBOs Table: Without the Growth in Revenue.

LBOs Table: With 3% Growth in Revenue

Suggested Answer

1. The empirical findings suggest that LBOs have several benefits, such as an increase in operating performance, reduction in agency costs through effective monitoring of leverage, better governance facilitated by financial sponsors, creation of concentrated ownership, and increase in firm values from the time of the buyout to a subsequent change in ownership or restructuring, resulting in significant returns on invested capital (Guo et al., 2011). A LBO is a financing technique, wherein debt is used to purchase a corporation’s stock, often involving the transition of a public company to private ownership. Various entities, such as the management of a corporation or external groups such as other corporations, partnerships, individuals or investment groups, may employ this method. LBOs typically entail cash transactions financed by the acquiring firm. The target company’s assets are frequently used as security for the loans acquired to fund the acquisition. This type of lending is often referred to as asset-based lending. Consequently, capital-intensive firms with assets of high collateral value can easily secure such loans. Non-capital-intensive firms, such as those in the service industries, can also obtain these loans if they generate sufficiently high cash flows to service the interest payments on the debt.

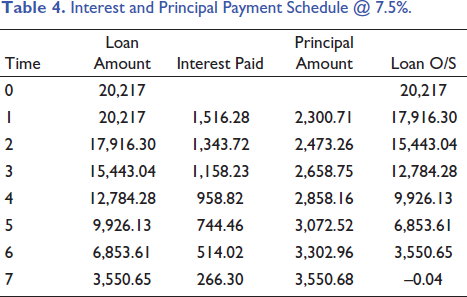

Solution for LBO Strategy

Table 4 above provides the interest payment and principal payment schedule for the company over a seven-year period. The expected rate of interest was considered @ 7.5%.

Interest and Principal Payment Schedule @ 7.5%.

In the first scenario, Dell generates $3,042.12 million in FCF every year before cash taxes and debt service. This amount is approximately consistent with historical performance, excluding acquisitions and share buybacks. Over the seven-year time horizon, the company repays all the debt which was borrowed under the LBO strategy. In terms of the enterprise value of the company, it is lower than at time 0 over this timeframe, while the value of the equity accounts increases, generating an IRR of 23.08% on the value of the original investment, which represents a very good return.

In the second scenario, Dell generates $3,637.98 million in FCF every year before cash taxes and debt service. This amount is approximately consistent with historical performance, excluding acquisitions and share buybacks. Over the seven-year time horizon, the company repays all the debt which was borrowed under the LBO strategy. In terms of the enterprise value of the company, it is lower than at time 0 over this timeframe, while the value of the equity accounts increases, generating an IRR of 25.81% on the value of the original investment, which represents a very good return.

What is Your Understanding of Tracking Stock, and Does Dell Management’s Strategy of BODs Provide a Successful Platform to Revive the Financially Distressed Firm?

Suggested Answer

Tracking Stock

The issuance of tracking stock is a form of corporate restructuring. Tracking stock, being common stock, is issued to existing shareholders based on the performance of the subsidiary company. When a tracking stock is issued, investors assess the subsidiary and parent companies separately. This track is usually issued by the company when the performance of the parent company is lower than that of the subsidiary company. Holders of tracking stock do not have voting rights. Notably, the concept of tracking stock gained popularity after its issuance by General Motors in the 1980s, and since then, many companies have issued tracking stock. In 2015, Dell acquired EMC for US$67 million, and VMware was a subsidiary of EMC. Dell issued tracking stock of VMware to all the shareholders of EMC. In 2018, Dell acquired all tracking shares of VMware for US$23.9 billion and converted them into Class C common stock. Dell’s Class C shares allow investors to invest comprehensively in Dell Technologies.

Salient Features of Tracking Stock

According to Prof. Ian Giddy, Professor of Finance at the Stern School of Business at New York University, the following are the major features of tracking stock:

Turnaround Strategy

It was a highly successful decision made by Michael in 2013. ‘After years battling Silicon Valley sceptics and Wall Street adversaries, Michael Dell has pulled off the deal of the century, borrowing and flipping his way to a $50 billion fortune. His biggest ambitions lie ahead—and they have nothing to do with space’ (Gara, 2021).

The strategy and the challenging phase of Dell teach crucial lessons to the business community, researchers, academicians and entrepreneurs. The entire episode of this turnaround story suggests that all companies and CEOs should adapt their business environments to changes in technologies and customer demands. In this strategy, several firms supported Dell in a positive manner.

In August 2012, Michael formed a Special Committee (Bocconi Student Investment Club, 2023) with an interest in taking Dell private. The committee was led by the Lead Director, Alex Mandl. The Special Committee retained independent financial and legal advisors J. P. Morgan and Debevoise &Plimpton LLP to advise the Special Committee with respect to its consideration of strategic alternatives, the acquisition proposal and the subsequent negotiation of the merger agreement.

Dell has always preferred to operate extraordinarily compared to other firms. For example, Dell implemented an efficient inventory management system in the IT world, pronounced as the ‘build-to-order’ (Bocconi Student Investment Club, 2023) business model, which led Dell to become the top computer manufacturer globally without any loss of inventory due to rapid changes in technology. However, the decline in revenue and margins in the PC industry started after the introduction of tablets, laptops and smartphones in the IT industry, changing customer preferences.

The strategy to ‘Go Private Dell’ was implemented after the change in industry demand and customer preferences. ‘Michael is special for his willingness to take risks, but to be right and do it in a way that’s going to be successful as opposed to lighting dollar bills on fire recklessly’ (Gara, 2021). Presently, Dell, valued at $75 billion, is worth more than four times its value before going private. Due to the LBOs, Dell, Durban’s Silver Lake and co-investors have worked immensely to bring Dell to this level, with total gains of >$40 billion (Gara, 2021).

The Following Buyback and Reverse Buyback Methods Can Also Be Used for the Restructuring of the Firm

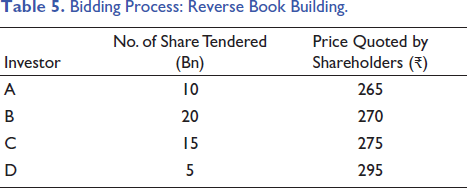

Karuna Limited has 100 billion (bn) outstanding shares, with 50% held by promoters and 50% by the public. In a recently held AGM, the company decided to delist its stock from the stock exchange. The delisting will be carried out through the RBB process. They have invited public shareholders to tender the shares by fixing a floor price of ₹250. Bids received are as follows (Table 5):

Bidding Process: Reverse Book Building.

To make the delisting success, promoters must purchase at least 40 bn shares from public.

Conclusion

‘After years battling Silicon Valley sceptics and Wall Street adversaries, Michael has pulled off the deal of the century, borrowing and flipping his way to a $50 billion fortune. His biggest ambitions lie ahead—and they have nothing to do with space’ (Gara, 2021). On 28 December 2018, Dell was listed on NYSE at $46 per share with a market capitalization of $16 billion after a gap of five years, as Michael converted it into a private company through LBO deals. Dell bought backtracking shares from VMware with a cash and stock deal worth approximately $24 billion. The strategy of buying back shares provided a platform to list on the stock exchange without the traditional IPO process. The enormous changes in the industry, with the entry of tablet computers, smartphones, and high-powered consumer electronics such as music players and gaming consoles during 2000 to 2012, forced Michael to take the company off the public market. During the six years as a private firm, the company changed its business through acquisition activities, transforming from a PC manufacturer into a broader seller of information technology services, ranging from storage and servers to networking and cybersecurity. Importantly, the decision of LBOs led to a successful story, turning around the financial and operational distressed firm into a successful one.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.