Abstract

The case of ‘Zomato’s Quest for Survival’ focuses on the concept of value relevance of accounting information. The case deals with financial ratio analysis, comparative financial statement analysis, cost–volume–profit analysis and DuPont analysis. The case also deals with the effect of acquisition on the acquiring firm’s fundamentals, post-acquisition. The case explores the potential growth of India’s food delivery market and goes on to explore Zomato’s business strategy and source of income. The case starts with Mr. Arghadip considering purchasing Zomato Ltd. Shares. He, therefore, gathered information from various sources to assess the company’s fundamentals and prospects for the future. A lot of questions worth discussing were brought up by the case. The ideal students for the case would be students of B.Com, M.Com, BBA and MBA. The case can also be discussed in Chartered Accountant and Cost and Management Accountant courses.

Introduction

Uber Eats’ India business was purchased by food delivery behemoth Zomato in January 2020. Given that the purchase was an all-stock deal, Uber Eats received Class I–2 compulsorily convertible cumulative preference shares of ₹9,000 each (Abidi & Nair, 2020). The acquisition, which was worth US$350 million, saw Uber Eats obtain a 9.99% share in Zomato.

It was anticipated that Zomato would gain a lot from the acquisition. Uber Eats had a consumer base in the southern region of India; therefore, after buying Uber Eats, Zomato is able to access that customer base. After the deal of Zomato and Uber Eats, it was expected that the former would hold a market share of 55% of the Indian food delivery industry. Additionally, Zomato will have more power when bargaining with restaurants, which will cut down on losses. The deal was a step-closer to the consolidation of the Indian food delivery market with Swiggy and Zomato being the key players (Tandon, 2020).

Mr. Arghadip, a commerce graduate, came across the information about the acquisition in a business publication. His objective was to evaluate whether investing in Zomato would be a beneficial undertaking. To achieve this objective, he delved into the company’s fundamentals and future prospects.

A Note on Indian Food Delivery Sector

In India, the market for food delivery is anticipated to grow by US$716.53 million between 2021 and 2026, showing a compound annual growth rate (CAGR) of 28.13%. One of the key reasons influencing the market’s growth is the rise in collaborations between restaurants and food delivery services in India. However, considerations like the increased danger posed by direct delivery services might limit industry expansion (Technavio, 2021).

Currently, approximately 70% of the business is in the top 7–10 cities. The remaining 490 cities occupy the remaining space and are expanding. The amount of business in these smaller cities has doubled during the last six months. Smaller cities are expanding quickly as a result of the aggressive migration of people there and the declining hesitation of online food ordering. These areas are far more aware of the option of ordering food online rather than going to a restaurant.

Zomato and Swiggy now have a majority of the market share, and it is too early to declare a victor. Swiggy’s business model revolves around convenience. The business grew to offer grocery concierge services since it is aiming to deliver more items to consumers swiftly and conveniently. Zomato, which began as a portal for finding restaurants, has openly said that it aspires to become a farm-to-fork firm, with food delivery playing a significant role. Additionally, it has started a business-to-business grocery service for restaurants to help them join its network.

A Note on Zomato Ltd.

Foodiebay was created in 2008; afterwards, on 18 January 2010, it changed its name to Zomato; and finally, in 2011, it became Zomato Media Pvt. Ltd (Sugermint, 2021). Zomato’s creator aims to make it simpler for users to utilize Zomato’s service. They thus aim to create a mobile application that is simple to use.

They create an app that smartphone users may utilize. Sanjeev Bikhchandani, the creator of Naukri, became enthralled by it and started making investments in the business. Through Info Edge, he spent up to $1 million in 2010. The next year, Sanjeev Bikhchandani received funding of US$3.5 million once more. The next year, Info Edge contributed a total of $10 million in investment. In order to fulfil orders from restaurants who lacked their own delivery service, Zomato first collaborated with businesses such as Delhivery and Grab when it launched its food delivery service in India in 2015. To enable partner restaurants grow their footprint without having to pay any fixed expenditures, the company announced intentions to introduce Zomato Infrastructure Services (cloud kitchen infrastructure) in February 2017. Zomato raised US$200 million from Ant Financial in February 2018 and was valued at US$1.1 billion, at which point it was recognized as a unicorn business. Later that year, Zomato Infrastructure Services’ activities were terminated. In April 2022, Zomato launched a pilot of 10-minute food delivery in Gurgaon called Zomato Instant.

A Note on Zomato’s Founders

Deepinder Goyal and Pankaj Chaddah are the founders of Zomato. On 23 December 1985, Pankaj Chaddah was born. After graduating from IIT Delhi, he began his career as an analyst before co-founding Zomato in 2008. In 2018, he resigned from Zomato after 10 years as a co-founder. Mr Chaddah’s net worth is estimated to be US$1 billion as of 2021. Mr Chaddah and his wife, Pooja Khanna, have formed Mindhouse. Mindhouse is an organization that promotes mental health and wellness.

Dipender Goyal earned a degree in mathematics and computing from IIT Delhi in 2005. He worked as a management consultant at Bain & Company in New Delhi after graduating from IIT Delhi. While working at this firm, he saw that there was a high demand for menu cards among his coworkers. That is where the concept of Zomato arose. Soon after, he left his employment at Bain & Company to launch his own food firm, Foodiebay, in 2008, which was then rebranded Zomato in 2010. Till date, he acts as the Chief Executive Officer (CEO) of the company.

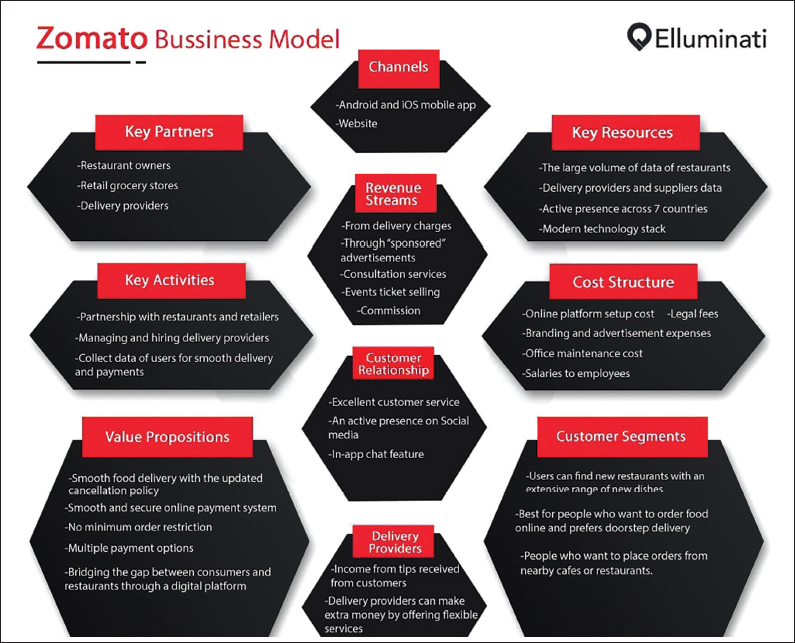

Zomato’s Business Model

In essence, Zomato is an app whose business strategy revolves around the provision of information, user ratings, and menus of partner eateries (Singh, 2020). The innovator for other online food-based applications is Zomato. The essential components of Zomato’s business plan are as follows:

➢ Customer segments: Zomato’s consumer base is separated into three categories: Local eateries: Zomato helps eateries to be seen by their intended audience. Users: Zomato is focused on users who want to find nearby restaurants or certain cuisines. The solution for people who enjoy home delivery is Zomato. Reviewers: They are Zomato content creators. They actively review foods and locations and give consumers pertinent information in written and graphical form. ➢ Zomato provisions: Zomato serves as a conduit between customers and its partner eateries. For their one-and-only delivery service, Zomato has created a well-designed price structure. The addition of Zomato Gold & Piggybank has raised the quality of services that Zomato offers. ➢ Alliance of Zomato: Recent alliances with other well-known companies, such as Uber Taxi, Visa and PayPal, have improved Zomato’s economic strategy. The partners have helped Zomato in a variety of ways, such as locating a space for its headquarters, assisting with hiring and other processes, arranging job placements, doing market research, and resolving operational, accounting, political and legal difficulties.

Zomato has the following revenue streams:

➢ Commission on delivery services: For FY2019, these commissions accounted for nearly 75% of Zomato’s overall revenue. ➢ Zomato Gold: It is built on the freemium business model. The idea is around offering subscribers premium services. This method enables customers who have gold memberships to take advantage of complementary food and beverage offerings. ➢ Sales of tickets: Zomato receives massive amounts of money in the form of commissions from the purchase of tickets for various events that are conducted in restaurants with their cooperation. Zomato also charges for the partner consultation services they offer. ➢ Promotions: Zomato consistently promotes a variety of eateries. Zomato charges partners for banner advertisements that provide them more exposure and visibility (refer to Figure 1).

Financial Performance and Unit Economies of Zomato Ltd.

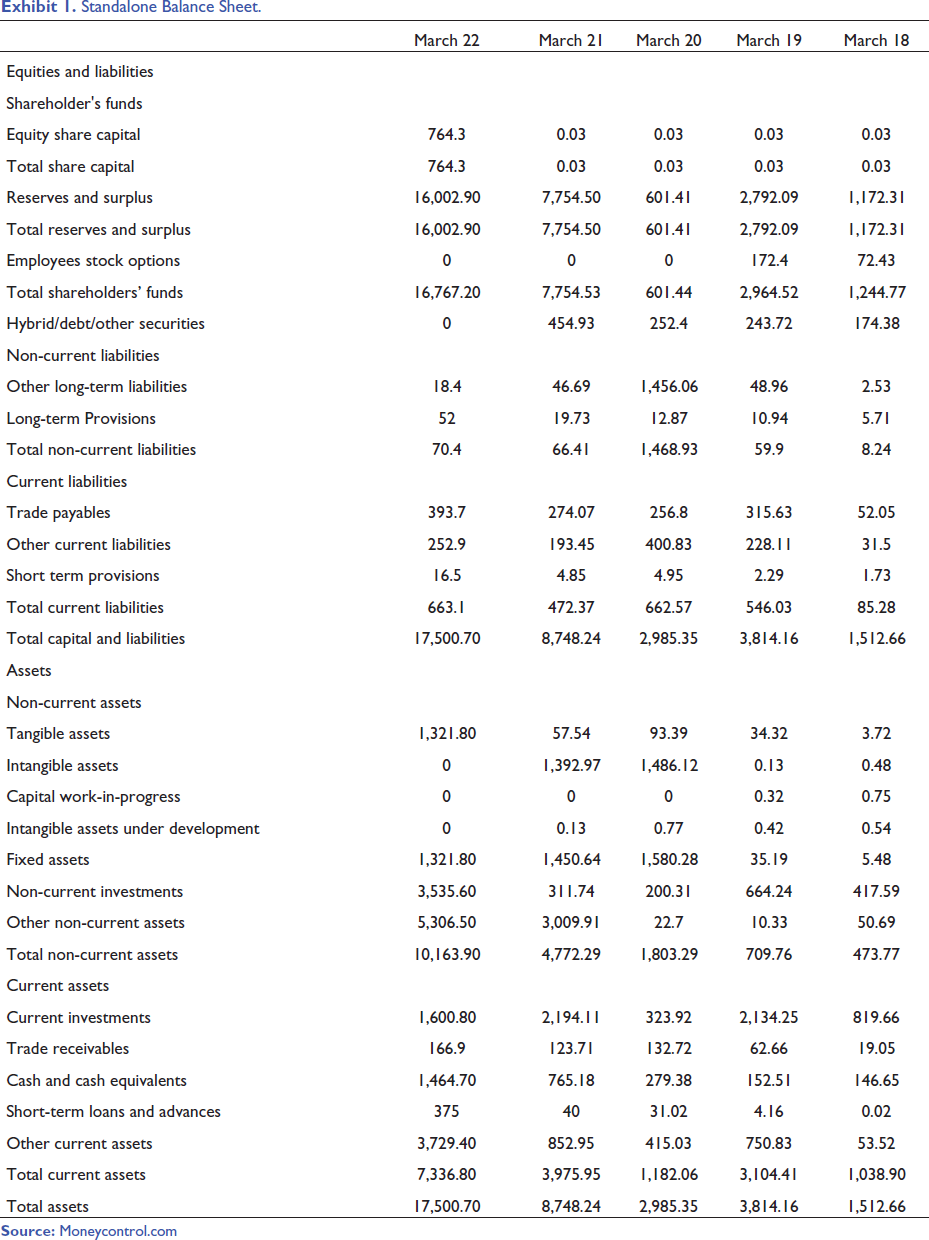

The long-term debt of Zomato Ltd. decreased by 100% in the financial year ending March 22. However, at the same time long-term provisions and total non-current liabilities increased by approximately 32% and 4%, respectively. Among the current liabilities, trade payables showed the highest change in the financial year ending March 22. In the context of the fixed assets, tangible fixed assets increased by 2197% in the financial year ending March 2022. Zomato Ltd. had 784.3 crore equity shares of ₹1 each in the financial year ending 2022. Further, non-current investments raised by ₹3223.86 crore in the financial year 2021–2022. The total current assets had also seen a significant increase (refer to Exhibit 1 for the balance sheet).

Standalone Balance Sheet.

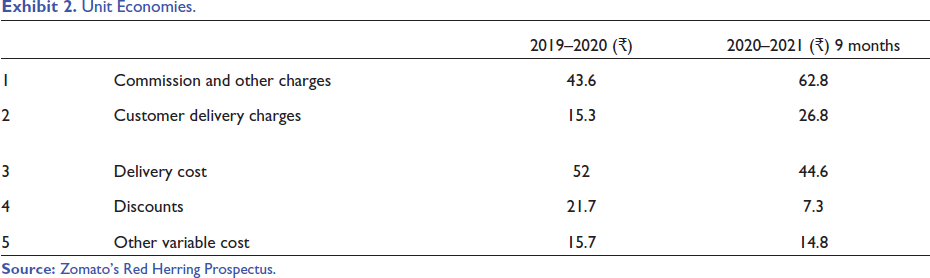

Exhibit 2 presents the comparative unit economies of Zomato Ltd. for the fiscal years 2019–2020 and 2020–2021.

Unit Economies.

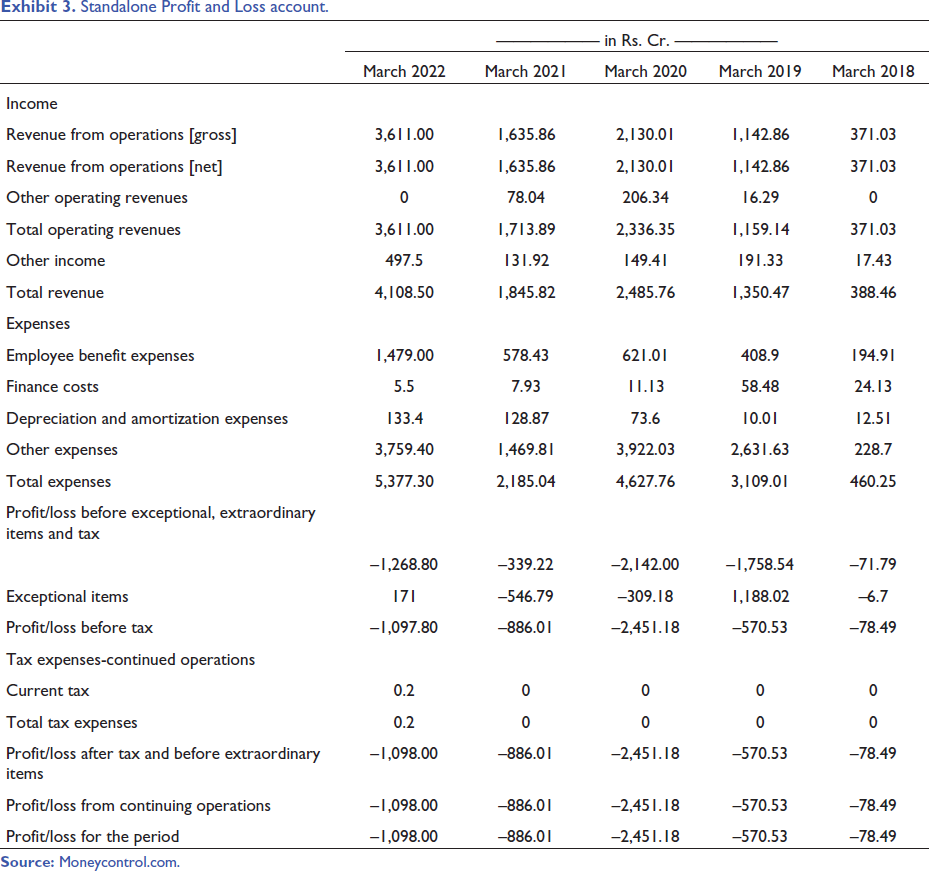

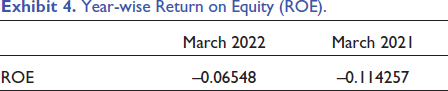

Zomato remained a loss-making venture till March 2022 (refer to Exhibit 3 for the statement of profit and loss). In March 2018, the losses of the company stood at ₹78.49 crore which raised to ₹2,451.18 crore in March 2020. In March 2021 due to a decrease in total expenses the losses fell <1,000 crore (for year-wise ROE data refer to Exhibit 4).

Standalone Profit and Loss account.

Year-wise Return on Equity (ROE).

IPO and the Behaviour of the Zomato’s Equity Price

The initial public offering (IPO) was priced at a range of ₹72–76 per share and the minimum order quantity was 195 shares. The IPO was 38.25 times over-subscribed. In the retail category, the issue was subscribed 7.45 times, 51.79 times in the qualified institutional buyer (QIB) category and 32.96 times in the non-institutional investor (NII) category. On 23 July 2021, equity shares of Zomato Ltd. were listed on the stock exchange. The market capitalization of the shares exceeded ₹1 lakh crore after they were listed at a premium of 51%. On the day of the IPO, the equity share’s opening price in the stock market was ₹115. The stock price hit an all-time high of ₹160 in November 2021. However, the prices fell dramatically in January 2022 as a result of the collapse in internet stocks, the introduction of a new goods and services tax (GST) of 5%, and JP Morgan’s pessimistic prognosis on the sector.

Road to Break-Even in the Future

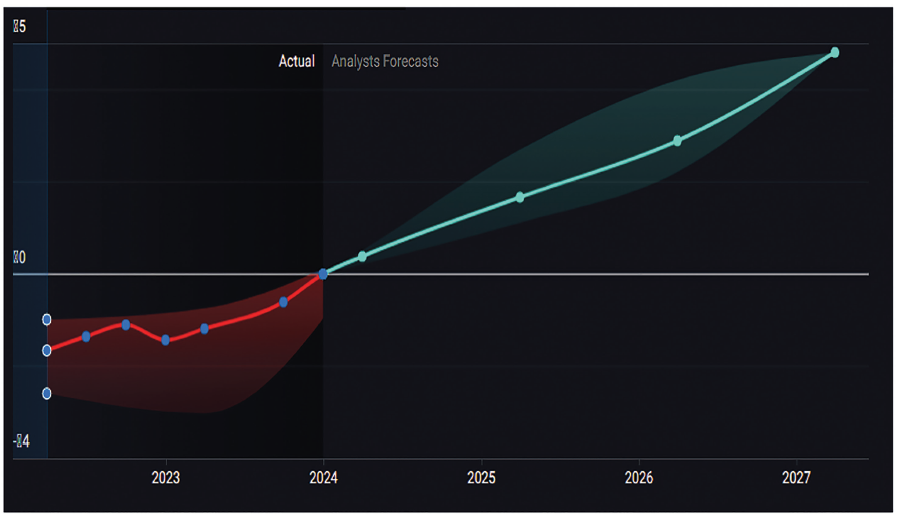

According to 22 Indian Online Retail analysts, Zomato is on the verge of breaking even. They expect the company to make a final loss in 2024 before turning a profit of ₹1.5 billion in 2025. As a result, the company is expected to break even in about 3 years. What rate of growth must the company achieve year over year to break even on this date? SimplyWall ST calculated an average annual growth rate of 78% using a line of best fit, indicating high analyst confidence (refer to Figure 2).

ZOMATO Earnings Per Share Growth.

The 2 Factors

Scalability

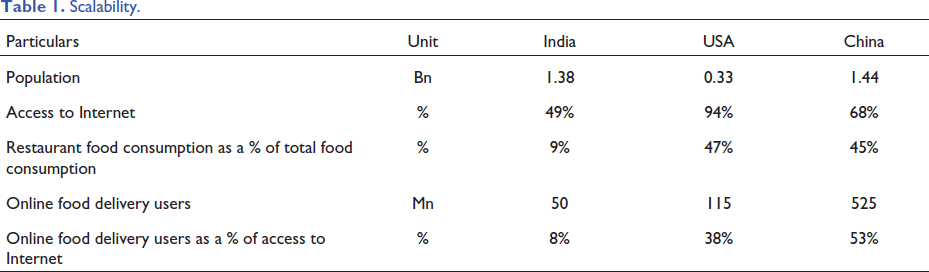

Food consumption, at approximately US$607 billion in 2020, accounts for roughly a quarter of India’s GDP. However, the majority of this is driven by home-cooked food. Restaurant food (or food services) currently accounts for only 8%–9% (US$56 billion) of the total food consumption market. This is significantly lower than in the United States and China. The food service market in India is benefiting from a cultural shift toward eating food outside the home, which is being accelerated by a lack of time, convenience, and quality improvement (mainly taste and temperature of food in India).

The Indian online food services market has grown 7x (c.50% CAGR) over the last five years to US$3.6 billion, but it still accounts for only 6% of the overall US$56 billion pie that Indians spent on eating out in FY20 (refer Table 1).

Scalability.

Management Quality

Zomato began in FY2011 as a restaurant review platform and expanded to food delivery in India in FY2015. In FY2016, it introduced the table reservation concept, followed by Zomato Pro in FY2017. Carthero Technologies was acquired in FY2018 to add hyperlocal delivery capabilities. In fiscal year 2019, HyperPure was introduced. Finally, Uber Eats India was purchased in FY2020. Deepinder Goyal, the company’s founder (also Managing Director and Chief Executive Officer), holds an integrated master’s degree in mathematics and computing from the Indian Institute of Technology, Delhi. He worked for Bain and Company before founding Zomato.

Long before Zomato became a billion-dollar public company, it was spotted by Sanjeev Bikhchandani, the founder of Info Edge NSE –2.82% and a non-executive director on the board. Bikhchandani has played an important role in Zomato’s success, advising and supporting the founders in both good and bad times. Deepinder Goyal recently announced that he will donate all of the proceeds from his employee stock option plan (ESOP) worth Rs 700 crore to the Zomato Future Foundation. The Zomato Future Foundation will pay for up to two children’s educations of all Zomato delivery partners who have been on Zomato’s fleet for more than 5 years.

Mr. Arghadip is required to make a decision on the matter of investing in Zomato stocks, based on the provided information.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.