Abstract

Kingfisher Airlines Ltd. was started under the chairmanship of a flamboyant industrialist, one of the biggest Indian liquor tycoons who claimed himself as the ‘King of Good Times’. The company garnered multiple accolades and achieved a growing market share in the aviation sector, presenting an attractive and innovative image. By providing passengers with exceptional comfort and an enjoyable flight experience, customer satisfaction soared. Despite its relatively short existence, the company left a notable and impactful mark on the Indian aviation industry. Losses have been reported ever since it started operating in 2005. 1 For many years, it struggled with serious financial problems that ultimately forced the company to cease operations on 20 October 2012. Due to the reputation of its Chairman and Managing Director, several private and public sector banks in India extended loans to Kingfisher Airlines. Further, the airline struggled to incur maintenance, landing, and aviation costs. The employees and pilots staged strikes due to the non-payment of their owed salaries and dues. The collapse of Kingfisher Airlines is attributed to promoters’ inordinate overconfidence stemming from their past accomplishments, tunnel vision, and a weak business strategy. The current case examines the fall of Kingfisher Airlines from the strategic management and accounting manipulation perspective. It also outlines the causes contributing to the airline’s downfall.

Introduction

Indian aviation industry commenced its operations in December 1912. Since then, the industry has undergone a swift transformation. The provisions of the Air Corporations Act of 1953 governed Indian skies. As per the legislation, all existing airlines were nationalized. Two corporations, Air India and Indian Airlines were set up to provide effective, sufficient, affordable, and well-coordinated air transportation services domestically and internationally. However, later in 1990, the Indian government ended its monopoly by adopting an ‘open-sky’ policy, allowing air taxis to operate from any airport nationwide. By 1995, many private airlines were flying over Indian skies, such as Indigo, SpiceJet, Sahara, Jet, etc. From 2005 to 2011, the Indian airline industry saw explosive growth, witnessing a compound annual growth rate of 18% (Srinivasan & Prasad, 2014). However, the global financial crisis of 2008 caused industry growth rates to slow. Resultantly, the aviation industry experienced a difficult period due to unprecedented hikes in fuel prices, causing high operational expenses, turbulent financial markets, and a sluggish economy. The circumstances were much more challenging for the Indian airlines owing to high taxes and domestic regulations. Further, this period witnessed the worst phase of India’s one of the most profitable and second largest acquirers of domestic air travel market share—Kingfisher Airlines.

Kingfisher Airlines: Fly the Good Times

Background

Mr Vijay Mallya, one of the biggest Indian liquor tycoons, grew up in a privileged environment, inherited immense riches, and headed a ₹300 crore business. At the young age of 28, following his father Vittal Mallya’s demise, he took over the United Breweries group, a business valued at ₹300 crore. Additionally, Mallya established Kingfisher Airlines under his chairmanship. The United Breweries group, headquartered in Bengaluru, was the owner of the airline. In May 2005, the company began its operations 2 with a fleet of four brand-new Airbus A320-200s, starting with a flight from Mumbai to Delhi (Pandey & Pandey, 2018). The airline had a vision of offering top-notch amenities, including comfortable seating, hot meals, personalized entertainment, and treating passengers as esteemed guests. Within a year, the airline expanded from operating just four daily flights to an impressive 104 flights per day. It swiftly connected 16 cities by introducing 17 additional aircraft.

The company also set a record in the years 2005 and 2007 for the swift airplane induction process. By 2006, the airline had attained a highly esteemed five-star status and had gained significant popularity among travellers belonging to the business class segment. In May 2007, the company acquired a loss-making airline, Air Deccan, at a cost amounting to ₹1,000 crores through United Breweries Group. The merger between the two was crucial to bypass government restrictions on international flights. The legislation permitted airlines with at least 5 years of operation to fly internationally. Without the merger, Kingfisher Airlines could not operate international flights until 2010. Gradually, in 2008 Kingfisher Airlines became the most significant operating airline in Indian skies. In September 2008, the airline expanded its operations globally by establishing a connection between Bengaluru and London. Subsequently, in 2009, Kingfisher Airlines received a prestigious five-star rating from Skytrax. 3 Among the seven airlines that were honoured with this distinction, Kingfisher Airlines gradually expanded and emerged as the largest airline in the second-most populous country in the world. It commanded a significant 26.7% share of the domestic aviation market 4 and operated approximately 250 flights per day.

During that time, the airline offered its guests the following classes of air travel: Kingfisher First: Premium services focused primarily on individuals who have the financial means to afford and enjoy premium-level services; Kingfisher Class: Premium Economy service catered to the trendy middle-class demographic who were experiencing upward social mobility; Kingfisher Red: Low-fare air travel focused on price-conscious middle-income group people. Kingfisher Elite: Focused on providing charter services; Kingfisher Cargo: Focused on delivering cargo services (Panigrahi et al., 2019).

The Turmoil

Kingfisher Airlines enjoyed a prominent position among India’s leading airlines until December 2011. However, it was unable to sustain its high standing over an extended period. Exceptional customer satisfaction came at the cost of profitability. Mr Mallya’s decision-making revolved around prioritizing luxury sales, but in India, only a limited number of individuals were willing to pay an extra amount for such luxurious offerings. Despite this, the airline excelled in terms of product quality and providing exceptional customer service, surpassing its competitors in these aspects.

Poor branding and positioning of Kingfisher Red were the primary reasons for the airline’s downfall. Kingfisher Red was introduced as a low-cost subsidiary of Kingfisher Airlines, targeting price-sensitive travellers. However, the target audience failed to resonate with it effectively. The airline established its brand image and reputation based on luxury and premium services, which became synonymous with the main brand. Introducing a low-cost subsidiary under the same brand umbrella created confusion among customers. Further, the marketing efforts and communication strategies for Kingfisher Red were not executed effectively. The airline failed to differentiate itself from competitors in the low-cost segment and was ineffective in communicating the unique value proposition of Kingfisher Red to potential customers. As a result, it struggled to attract a significant customer base and failed to generate the expected demand. The lack of clear brand identity and positioning, coupled with ineffective marketing and communication strategies, led to poor brand perception and limited customer appeal for Kingfisher Red.

Additionally, the merger of Kingfisher Airlines and Air Deccan served as a significant marketing factor that contributed to the downfall of the airline. The merger brought together two airlines with contrasting positioning in the market. Air Deccan was known as a low-cost carrier, catering to price-conscious travellers, while Kingfisher Airlines had established itself as a luxury airline, targeting premium customers. The merging of these two airlines with distinct market segments resulted in a dilution of brand identity and confusion among customers. The luxury image of Kingfisher Airlines clashed with the low-cost positioning of Air Deccan, making it challenging to effectively target and cater to the needs of both customer segments. This lack of alignment in brand positioning and target audience created challenges in marketing, as the merged entity struggled to communicate a clear and compelling value proposition to customers. The merger failed to leverage the strengths of both airlines and capitalize on their respective market positions. Furthermore, 366 domestic flights and 20 international flights were flown by the airlines. It also owned 67 aircraft, which increased aircraft lease rental. The hiked fuel prices and the economic slowdown of 2008 caused high losses and heavy debts, leading the company to shut down its operations by the end of 2012.

Since its inception, the airline has faced losses that piled up subsequently. 5 Mr Mallya’s emphasis on offering luxurious travel experiences resulted in the incorporation of state-of-the-art facilities onboard, consequently increasing the airline’s operational costs. To support this luxury-focused approach, the airline acquired a diverse fleet of aircraft through purchases or leases. However, this decision led to additional expenses in terms of depreciation costs and lease rents.

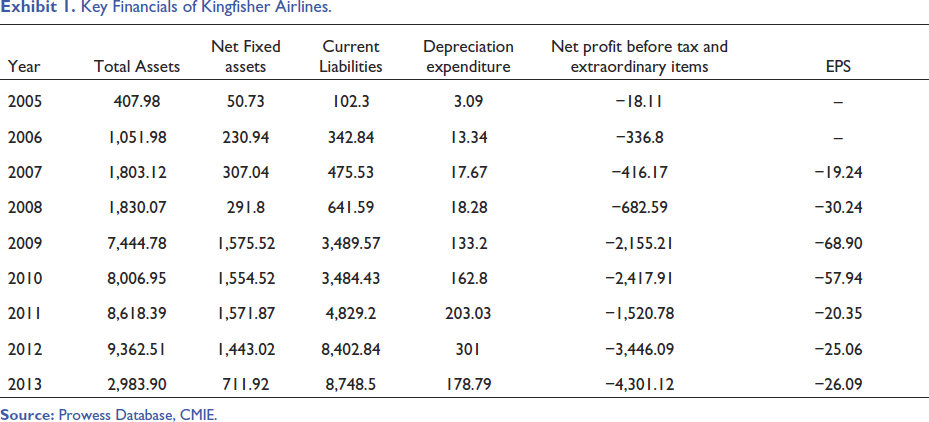

The company faced difficulties in coping with the escalating price of jet fuel due to the growing demand for fuel and intense competition among airlines to operate at a low cost. The continuous rise in fuel prices posed a significant challenge for the company in meeting its financial obligations in this regard. It acquired many aircraft for billions of dollars, including Airbus A330-200s, A350-800s, A380s, and ATR-72-500s. Further, the merger with Air Deccan resulted in the inheritance of additional models. The piled-up lease rental crossed ₹984 crores, leading to the grounding of 66 aircraft. The economic downturn of 2008 served as another external factor that contributed to the downfall of Kingfisher Airlines. A lack of proper management and maturity to handle such a big airline business affected the airlines greatly. Mr Mallya experienced a significant financial loss of ₹ 9,091.4 crores and accumulated loans from 17 different banks. The State Bank of India was the largest creditor, with a debt amounting to ₹ 1,600 crores, followed by IDBI Bank and Punjab National Bank, each owed ₹ 800 crores by the airline. Additional debts include ₹ 650 crores to Bank of India, ₹ 550 crores to Bank of Baroda, ₹ 410 crores to Central Bank of India, ₹ 320 crores to UCO Bank, ₹ 310 crores to Corporation Bank, and ₹ 430 crores to United Bank of India. In the fiscal year 2012–2013, the reported revenue of the airline stood at ₹ 683.4 crores, while it incurred a substantial loss of ₹ 4,301.4 crores. At this moment, the airline was ‘bleeding money’, and the shortage of funds resulted in non-payment of salaries to employees.

Owing to mounting challenges and obstacles encountered by the airline, it was compelled to suspend its operations in February 2012, subsequently facing suspension by the International Air Transport Association. Later in October 2012, the Directorate General of Civil Aviation suspended the company’s Scheduled Operator’s Permit. 6 Following this, the Central Government discontinued the flight entitlement in February 2013, effectively shuttering the airlines. Financial institutions and leasing companies instigated actions to acquire custody of the airbuses. Ultimately, Mr Mallya fled the country with over ₹ 9,000 crores of debt. 7

Reasons Behind the Downfall

Kingfisher Airlines was one of the top five airlines in India till December 2011. 8 However, following significant losses and debt, the company eventually went out of business in 2012.

Earnings Management Practices Adopted

Due to the surge in crude oil prices and the economic slowdown of 2008, most airlines started reporting losses, resulting in poor performance. Kingfisher differentiated from its competitors because of unparalleled premium world-class airline services to its guests. Shortly, issues of high operational costs and diminishing returns came to light. Owing to piling financial pressures and the inability of the airline to manage its operations effectively, lenders requested to pay off all debts before applying for additional loans. By December 2011, the net loss rose to ₹ 444.27 crores from ₹ 253.69 crores in the previous year’s third quarter.

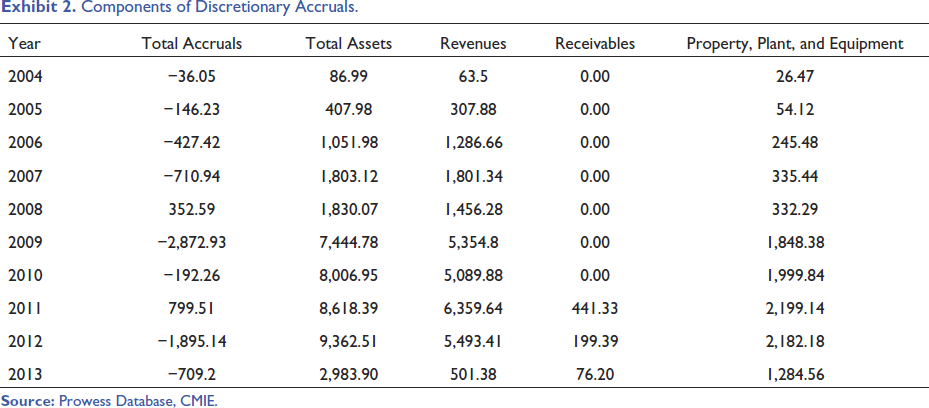

Exhibit 2 shows a continuous rise in total assets by 10,662.7%; revenues grew by 8,551.04%, and property, plant, and equipment rose by 4,752.89% from FY04 to FY12. Conversely, most years showed a negative value of total accruals with an average of −583.807, indicating the company’s engagement in income-decreasing (i.e., depreciation expenditure) manipulation of earnings through accruals. The company either purchased or leased all fleets, which led to the accumulation of lease rents and depreciation expenses. Due to the higher-than-expected lease rental amounting to ₹ 984 crores, 66 aircraft were grounded in 2011.

Further, the company offered discounted tickets to boost sales. 9 It grew by 8,711.96% from FY04 to FY12. Manipulating earnings through real activities reduces firm value in the long run, considering the actions taken to boost earnings in the present can negatively impact cash flows in the future. Moreover, providing discounts to customers can create an expectation of future discounts, which may result in reduced sales margins. The airline gained a competitive edge by offering superior products and exceptional customer service. It provided premium amenities such as hot meals, comfortable seating, and personalized entertainment, and treated passengers with the utmost hospitality, considering them as valued guests. However, the airline could not sustain itself by providing such luxury travel at a discounted fare, resulting in negative cash flows and mounting losses.

Structural Problems

Mr Mallya has a history of acting extravagantly. The airline made mistakes with the types of aircraft it purchased, resulting in capital expenditures that did not generate a profit. The whole fleet of Kingfisher Airlines was either owned or leased in 2005, which piled up the lease rent amounting to ₹ 984 crores. The company acquired most airbuses following the ‘buy-and-leaseback’ model. 10 including Airbus A330-200s, A350-800s, A380s, and ATR-72-500s. It owned 67 aircraft (64 leased and three owned). After merging with Air Deccan, it inherited more models from it. However, other companies had a mixture of new and old aircraft, which reduced maintenance and operating costs. Significant structural inefficiency once again highlighted the absence of strategic management skills, as he did not exhibit any interest in researching or benchmarking competitors.

Operational Problems

Since the beginning, Kingfisher Airlines has incurred substantial operational costs. The merger with Air Deccan further dragged the resources. It necessitated taking over the business model adopted by Air Deccan based on European airlines (namely, EasyJet and Ryanair). In 2009, the company fired over 100 pilots and increased its fares substantially due to significant losses. By the fall of 2010, it began falling behind on airport payments. Further, service tax payments were delayed until December 2011. By the start of 2012, the company began to cancel its flights frequently. The flight maintenance, landing, and navigation expenses accounted for roughly 10.86% of its total revenue. Due to unpaid salaries, employees and pilots started protesting in March 2012. Around the same time, the company also started losing its independent directors.

Moreover, the engineers declined to certify the take-off and unpaid lease rentals resulted in the repossession of its aircraft by June 2012. The airline could not keep any promises, and payments to banks, airports, employees, pilots, and oil companies continued to rise as the interest burden kept mounting. By the end of 2012, the majority of its creditors and suppliers had not been paid, and the company was on the verge of losing its airline operating permit. Living in denial and keeping an outward appearance of ‘all is well’ allowed things to deteriorate for too long. Mr Mallya might have been able to save Kingfisher Airlines if he had recognized these warning signs and acted upon them in time.

Strategic Issues

Inappropriate decision-making and an opaque business model led Kingfisher Airlines to collapse 11 . Mr Mallya could not understand consumer needs and made all his decisions to provide luxury travel. Only a handful of Indians were ready to pay for luxury travel for domestic routes (Pathak, 2015). The merger with a loss-making, low-cost airline Air Deccan at the cost of ₹ 1,000 crores, showed no business prudence. Furthermore, the rebranding of Air Deccan as Kingfisher Red in 2008 led customers to expect a certain level of service, similar to the full benefits offered by Kingfisher, which a low-cost airline could not provide. Due to this, both Kingfisher Red and Kingfisher received negative feedback from customers. Competing airlines increased profitability by eliminating services that customers would not value anyway. The high fuel cost, airport user fees, and the mandate to fly on several unprofitable routes had already created constraints and problems for the company. Even though Mr Mallya was aware of these restrictions, he made no effort to create a business strategy that took them into account. Therefore, Kingfisher’s extravagant business model became unsustainable.

Appendix A

Key Financials of Kingfisher Airlines.

Components of Discretionary Accruals.

Components of Abnormal Cash Flow from Operations.

Discretionary Accruals, Abnormal Cash Flow from Operations, and ∇Sales.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.