Abstract

Kia India, the wholly owned subsidiary of South Korea based Kia Corporation, was unquestionably a late entrant in the highly competitive Indian passenger vehicle (PV) industry. Its ingress was nonetheless well planned and its strategic initiatives were adeptly executed. A well-conceived product portfolio juxtaposed with an astute segmentation, targeting and positioning strategy enabled Kia India establish itself as an inspiring brand in a hyper competitive Indian automobile marketplace. Timely launch of trend-leading PVs formed part of Kia India’s growth story. Kia drove into the electric PV (E-PV) segment with the launch of EV6. Will the recent product launches enable Kia India add more superlatives to its name? Is there a need to revisit the product portfolio and analyse the status of different models that the company has hitherto launched in the country? How can Kia India continue its storied journey in India?

Keywords

Introduction

Kia India (erstwhile Kia Motors India) 1 , a wholly owned subsidiary of South Korean automobile company Kia Corporation (Kia), had every reason to commemorate its 3rd anniversary in August 2022. In a short span of time, Kia India established itself as a ‘trend leading’ and ‘inspiring’ brand. It was one of the fastest growing automakers and had become the fifth-largest automobile manufacturer in the country (Mitra, 2022). The young ‘automobile disruptor’ had bridged the gap between ‘affordability’ and ‘luxury’ for the consumers (Kia.com, 2021b). Kia India was ranked No. 1 (out of 18 brands) in the 2021 India Dealer Satisfaction Survey (Move, 2021). Kia India’s maiden launch, the mid-sized Sports Utility Vehicle (SUV); Kia Seltos was a roaring success. The company gained further traction in the Indian passenger vehicle (PV) market with the launch of its luxury Multi-Purpose Vehicle (MPV); Kia Carnival and sub-compact SUV; Kia Sonet. Kia India continued to press the accelerator with its 4th launch; Kia Carens, a recreational vehicle for the ‘modern Indian families’. Kia India recorded 47% growth in wholesale unit sales in July 2022 vis-à-vis July 2021. The company registered year-till-date growth of 28%, significantly higher than the industry growth of 16% (The Economic Times, 2022). What strategic initiatives enabled Kia India to drive into the last lane? The electric PV (E-PV) industry in India grew 3.6 times to 17,802 units in 2021–2022 (FADA, 2022). Kia India drove into the expectedly up-and-coming Indian E-PV marketplace when it launched the EV 6; a premium electric crossover in June 2022. The start for EV 6 was encouraging. Will EV 6 supercharge Kia India’s growth?

PV Industry in India

India was the fifth-largest automobile manufacturer in the world with production of 22.93 million vehicles in 2021–2022 (IBEF, 2022). The country was expected to become the third-largest automotive market in volume terms by 2026 (Make in India, 2022). Two wheelers (76.9% share) and PVs (17.5% share) were the biggest segments in the Indian automobile sector. The PV segment included three sub-segments; passenger cars, utility vehicles, and vans.

The Indian PV industry recorded sales of 3.1 million units in 2021–2022 (see Table 1). The slowdown in the PV market was evident before the advent of COVID-19 pandemic 2 . The black swan event pushed the industry into degrowth. Amidst the gloom of plunging PV sales, the utility vehicles sub-segment bucked the trend (SESEI, 2021). Indian consumers exhibited an increased preference for SUVs given the vehicle’s demeanour and road visibility. The SUV segment had become fragmented with compact SUVs in the lead (Financial Express, 2022). MPVs, which had more space but less power than the SUVs, were also sought after by consumers (Charan, 2021). Price played a pivotal role in the purchase decision. Some premium hatchbacks and sedans were comparable to compact SUVs in terms of price range. As a result, compact SUVs were replacing hatchbacks and sedans as vehicles of choice. Preference towards feature-loaded, high-end variants was evident. Customers also accorded high priority to technology, sophistication, safety, ergonomics and functionality of the vehicle (Financial Express, 2022). The proportion of utility vehicles sold to all PVs sold had risen to 40% 3 in 2021–2022, up from 25% in 2016–2017 (SIAM, 2021). Compact SUVs accounted for half of total SUV sales (Mukherjee, 2022a).

Passenger Vehicle (PV) Sales in India from 2016–2017 to 2021–2022.

bEstimated by the author. The total PV sales till 2021–2022 are available from SIAM (2022). However, utility vehicle sales are available till 2020–2021 from SIAM. (2021). Utility vehicle sales for 2021–2022 have been estimated as 40% of total PV sales (Financial Express, 2022).

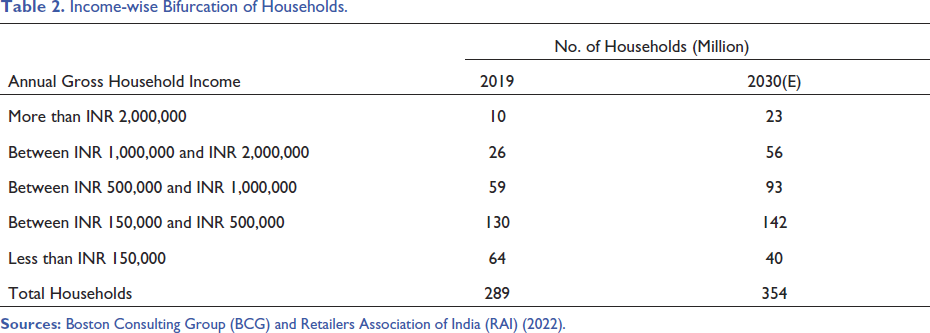

Buyers of SUVs were young, affluent and aspirational. People aged between 25 and 35 years and residing in tier-1 and tier-2 cities buoyed demand for such vehicles. Their annual income ranged between INR 960,000 and INR 1,080,000 (Financial Express, 2022). The proportion of households with higher incomes was expected to rise (see Table 2). This bode well for the industry. Automobile manufacturers had launched nearly three dozen compact and mid-sized SUVs in the last 5 years to cash in on Indian consumers’ penchant for such vehicles. It was estimated that SUV segment would register a compounded annual growth rate (CAGR) of 9% and sales would be more than 2.16 million units by 2028 (Financial Express, 2022). The MPV segment with sales of 248,470 units in 2021 had registered a 32% increase over previous year sales. The growth in MPV segment increased significantly as the segment registered growth of 54% (138,322 units sold) in the first 5 months of 2022 (Mukherjee, 2022b). Within the MPV segment, the growth of more expensive, high-end models was not significant (Charan, 2021).

Income-wise Bifurcation of Households.

Competitive Landscape

The Indian PV industry was highly competitive. As many as 20 players jostled for market share. India was an attractive market but not an easy one to crack. Ford Motor Company and General Motors exited the country due to accumulated losses, industry overcapacity, and sluggish growth (Phadnis, 2021).

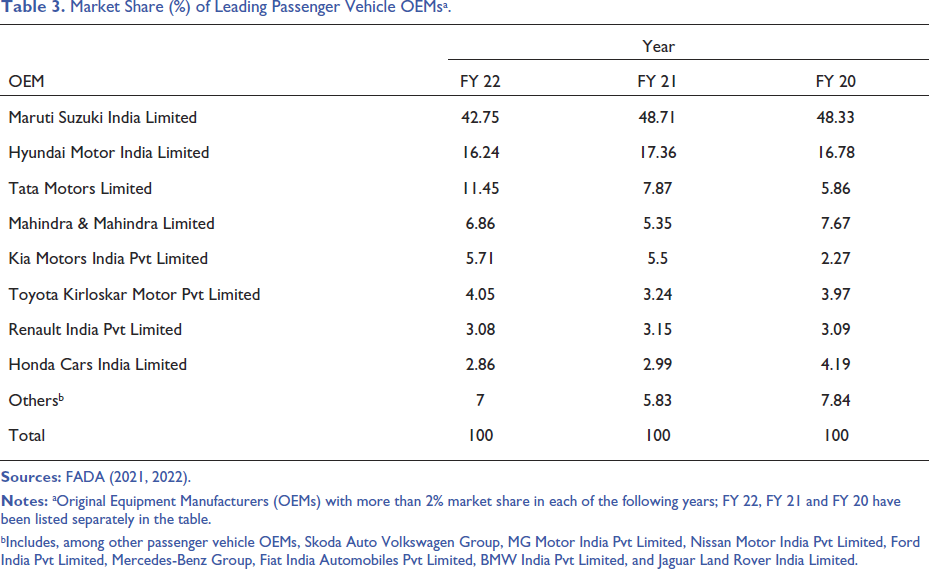

Maruti Suzuki India Limited (Maruti) had been in India for nearly four decades and dominated the PV market with 42.75% market share in 2021–2022, down nearly 6% from previous year (FADA, 2022).

Hyundai Motor India Limited (Hyundai) was a distant second with 16.24% market share in the PV marketplace (see Table 3).

Market Share (%) of Leading Passenger Vehicle OEMsa.

bIncludes, among other passenger vehicle OEMs, Skoda Auto Volkswagen Group, MG Motor India Pvt Limited, Nissan Motor India Pvt Limited, Ford India Pvt Limited, Mercedes-Benz Group, Fiat India Automobiles Pvt Limited, BMW India Pvt Limited, and Jaguar Land Rover India Limited.

Maruti offered a full range of cars. It is product repertoire included hatchbacks, sedans, MUVs/SUVs, and sedans (MarutiSuzuki.com, 2022). The company was well known for manufacturing and marketing affordable cars. High mileage, low cost of maintenance and a service network located in every nook and corner of the country were added advantages that the company offered (Nambiar, 2021).

Hyundai was the only ‘realistic competitor’ to Maruti (Dutta, 2018). The two-horse game was evident but there was no room for complacency. Home grown players, as also international companies, had entered and exited the top league in the past. They were clearly vying for a larger chunk of market share.

Kia India was the 5th largest automobile manufacturer in the country, a position that it had achieved in quick time by offering highly differentiated vehicles and making inroads in the SUV segment (Chaudhary, 2022b).

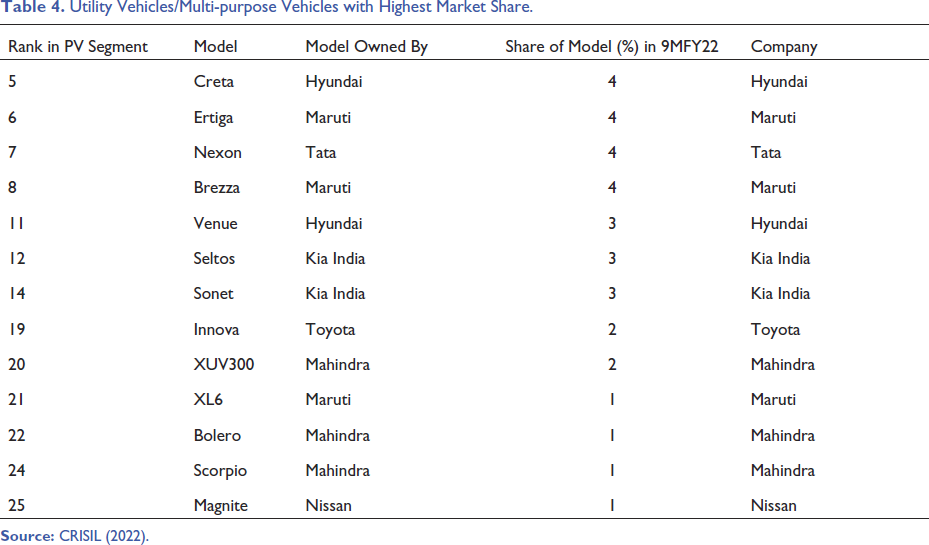

Maruti had not been able to gain traction in the booming SUV segment. Hyundai had two popular SUVs in its portfolio; Creta and Venue. It sold 250,000 SUVs in 2021–2022 and commanded 22% share of the SUV segment. Tata (18% share), Mahindra (14%) and Maruti (12% share) were in 2nd, 3rd, and 4th position in the SUV segment (Mukherjee, 2022a). During the first 9 months (9M) of 2021–2022, 13 UVs/MPVs featured in the list of top 25 PVs sold in the country (CRISIL, 2022). Kia Seltos and Kia Sonnet featured in the list (see Table 4). Kia India had disrupted the Indian SUV marketplace. The Kia Seltos had found 300,000 Indian homes in less than 3 years, a feat that no other SUV had achieved in this span of time.

Utility Vehicles/Multi-purpose Vehicles with Highest Market Share.

Lately, Tata had emerged as the leading SUV player in the country. Tata’s repertoire of SUVs included entry level Tata Punch as well as Tata Nexon, Tata Harrier, and Tata Safari (Chaudhary, 2022a). Tata Nexon was the top-selling SUV in India in July 2022. Toyota dominated the large MUV segment with Toyota Innova and Toyota Fortuner. The former recorded sales of 34,078 units in 2020 and 55,250 units in 2021. Toyota Fortuner recorded sales of 9,204 units in 2020 and 10,915 in 2021 (Surendhar, 2022). Expensive MPVs such as Kia Carnival did not find many homes (Charan, 2021). Kia Carens gained immediate traction in the marketplace and had the second highest market share at 18.7% in the MPV segment during the period January to June 2022. Maruti Ertiga continued to remain at the pole position with 40.6% share of the segment (Harsh, 2022).

Indian EV Marketplace

Amid growing concerns about air pollution and resultant global warming, stakeholders strived for an EV push in the country. The government promoted electric mobility with the overarching objective of making the country carbon neutral. India was committed to reducing emissions by a billion tons by 2030 and become a net-zero emissions country by 2070 (Bandhu, 2022).

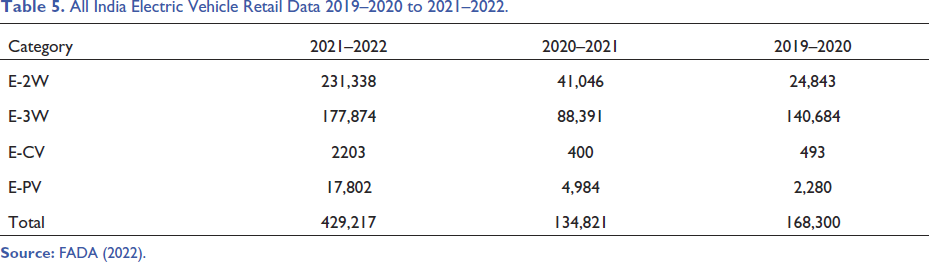

A total of 1,392,265 EVs plied on Indian roads. Of these, only 4% were four-wheelers (Print, 2022). EV sales in India had registered a 3× increase over previous year to 429, 217 units in FY22 (see Table 5).

All India Electric Vehicle Retail Data 2019–2020 to 2021–2022.

India was among the ‘starter nations’ in terms of its EV-readiness (Sen, 2022). However, the government’s intent, ambition and capacity commitments coupled with policy initiatives to promote EVs were likely to upend the status (Sen, 2022). By 2030, nearly 30% of all vehicles sold in India would be EVs (Mohile, 2022).

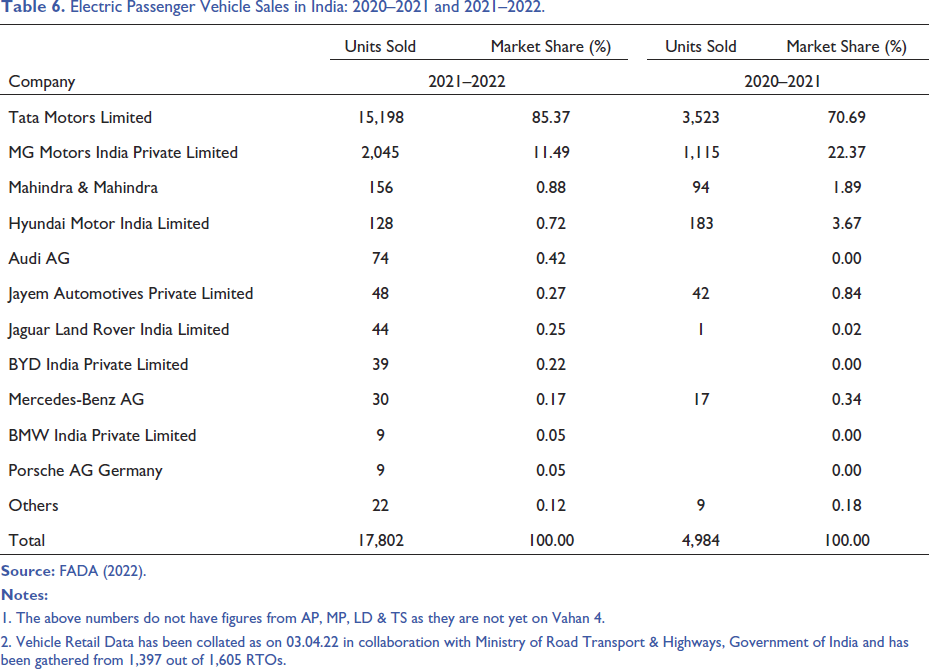

The E-PV sales were 17,802 units in 2021–2022 (FADA, 2022). Tata led the market with 85.37% of EV sales, followed by MG Motors with 11.49% of sales (see Table 6). India recorded highest ever half-yearly sales of 20,440 units of E-PVs from January 2022 to June 2022 (Rohira, 2022). Tata’s EV lineup included Nexon EV that topped the sales chart (Zee News, 2022). It provided a compelling value proposition; price, performance, and range (Kant, 2022).

Electric Passenger Vehicle Sales in India: 2020–2021 and 2021–2022.

1. The above numbers do not have figures from AP, MP, LD & TS as they are not yet on Vahan 4.

2. Vehicle Retail Data has been collated as on 03.04.22 in collaboration with Ministry of Road Transport & Highways, Government of India and has been gathered from 1,397 out of 1,605 RTOs.

MG Motors made inroads in the Indian E-PV market with its MG ZS EV. The price of MGZS EV ranged from INR 2,199,800 (Excite variant) and INR 2,588,000 (Exclusive variant). The company was planning to introduce a sub-INR 1,500,000 EV also (Kant, 2022).

Mahindra was ready to up the ante on its EV play. The company unveiled five electric SUVs in August 2022. These SUVs were sold under the existing XUV brand (HT Auto, 2022b).

Hyundai launched the Kona electric SUV in July 2019 at INR 2,500,000. The company had managed miniscule E-PV share in but was eager to press the accelerator. Hyundai planned to launch six EVs by 2028 (Mukherjee, 2021).

Maruti had delayed its EV plans and intended to wait for the battery cost to come down (Autocar India, 2021). It considered an EV launch in 2025 (Mukherjee, 2021). Honda Cars India Ltd (Honda) launched the hybrid version of Honda City (Kant, 2022). Toyota Motor Corporation (Toyota) tried its luck again in the hybrid EV fray as it unveiled the mid-size SUV Urban Cruiser Hyryder. Earlier, it had tested the Indian E-PV waters with two highly priced models; Toyota Camry and Toyota Prius (Business Today, 2013; Sinha, 2017; Umrethi, 2010) but failed to gain traction.

China-based BYD used low-cost lithium iron phosphate batteries which enabled it to market EVs at lower prices vis-à-vis foreign rivals (Business Standard, 2022). BYD sought to position itself as a ‘tech premium’ brand in India (Balachandar, 2022). It had introduced the E6 MPV in India at a starting price of INR 2,915, 000 (Business Standard, 2022). To make further inroads in the Indian EV marketplace, BYD announced its plans to introduce a mid-sized electric SUV in Q4CY22 (Balachandar, 2022).

U.S. based Fisker Inc. (Fisker) planned to introduce four EVs in India by 2025. The company believed that ‘affordable, exciting’ technologically sound EVs would make a mark in the marketplace. Fisker believed that EVs priced between INR 2 million and INR 2.4 million could bring in good retail volumes (Wadhwa, 2022).

U.S based Tesla Inc. (Tesla) put its plans to enter the Indian EV market in abeyance as high import tariffs proved to be a deterrent (Charan, 2022). The Indian government attracted companies to invest and set up manufacturing base in India through the product linked incentive (PLI) scheme. The Tesla-void was filled by manufacturers of luxury automobiles such as Audi AG, Mercedes-Benz AG, and BMW India Private Limited (BMW). BMW expected 10% of its revenue to come from EVs in the next year (Mukherjee, 2022c).

Major Challenges

The EV industry in India was fraught with challenges. The mass-produced EVs relied on mild-hybrid technology. Full hybrids commanded a hefty price tag (Kant, 2022). Dearth of charging stations, huge acquisition costs for the companies, lack of choice for the customer, and shortage of battery swapping centres led to a low EV adoption rate (Mohile, 2022). To overcome the problem of lack of public charging stations, most PV manufacturers provided at-home charging solutions (Kant, 2022) but these were at best baby steps.

China, the largest EV market in the world, was also the largest EV battery manufacturer accounting for nearly 80% of the Li-ion manufacturing capacity (Bhutada, 2022b; Patton, 2022). Augmenting battery manufacturing capacity was a sine qua non for achieving the desired transition from internal combustion engines (ICEs) to EVs.

India either imported Li-ion cells that were assembled in batteries at a local level or imported the EV battery packs. Both these options cost dearly (EV Reporter, 2019). Local manufacturing of EV batteries was a means to strengthen supply chain and reduce the cost of EVs. Battery manufacturing infrastructure was ramped up as apprehensions of shortage of availability of lithium, the key ingredient of these batteries loomed large (Chatterjee, 2022).

The cost of lithium-ion (Li-ion) EV battery pack had reduced significantly in the last decade (Bhutada, 2022a). Nonetheless, it still constituted 40%–50% of the total EV cost. Reduction in the price of batteries was thus critical for mass adoption of such vehicles (Kant, 2022).

In order to overcome these challenges, the industry needed financial, fiscal, and infrastructural support. The government provided this support through various policy measures aimed at developing an ecosystem for the EV play to flourish.

Policy Measures

The government promoted sustainable transportation by providing fiscal and incentives for production and adoption of electric vehicles. The GST rates were slashed from 12% to 5% on EVs (Kant, 2022). Likewise, GST on charges at charging stations was reduced from 18% to 5% (Make in India, 2022).

Production linked incentive (PLI) schemes amounting to INR 181 billion for manufacturing of advanced chemistry cells (ACC) batteries and INR 259 billion for EV manufacturing were approved (Kant, 2022).

In July 2022, three companies; Ola Electric, Reliance New Energy and Rajesh Exports signed the Programme Agreement under the centre’s PLI scheme for ACC battery storage. Other players had ventured into EV battery manufacturing which was likely to augment the capacity by 95 GWh (Ministry of Heavy Industries, 2022a).

The government planned to install charging stations at strategic locations on busy highways to promote inter-city EV travel. A battery swapping policy was to be unveiled (Shah, 2022). E-Amrit portal provided EV related information including policies and subsidies on such vehicles (Make in India, 2022). A one stop EV super app was in the works to enable faster dissemination of information on location and availability of charging stations (Mukherjee & Thakkar, 2022).

The Automotive Mission Plan (AMP) 2016–2026, National Electric Mobility Mission Plan (NEMMP), FAME India Scheme—Phase-I, FAME Phase II, and National Automotive Testing and R&D Infrastructure Project (NATRiP) were developed to buoy the EV industry.

Automotive Mission Plan (AMP) 2016–2026

The Automotive Mission Plan 2016–2026 (AMP 2026) was a 10-year roadmap for the Indian automotive industry. It encompassed aspects related to fiscal policy measures, emission norms, research & development (R&D), technical standard, and homologation. The vision statement of AMP 2026; ‘Vision 3/12/65’ envisaged that Indian automotive industry would be amongst top three in the world, contribute 12% of the GDP and create 65 million additional jobs by the end of the plan period that is 2026 4 .

NEMMP

The NEMMP 2020 was unveiled in 2012 with the vision of promoting domestic xEVs (hybrid and electric vehicles) manufacturing capabilities, requisite infrastructure, and technology. The overarching objective of NEMMP was to catapult Indian automobile industry on global stage and contribute significantly to national fuel security.

FAME India Scheme—Phase-I

The Department of Heavy Industries formulated the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles in India (FAME India) Scheme on 1 April 2015 to promote hybrid vehicles and EVs. It was done through a four-pronged framework; demand creation, technology platform, pilot project, and charging infrastructure. The total fund allocation under Phase I of FAME India Scheme was INR 5.29 billion (Ministry of Heavy Industries, 2019).

Market creation was led by providing demand incentives across various segments including PVs. Customers could purchase xEVs at upfront reduced prices. Evaluation of the 1st phase of FAME India Scheme revealed increased awareness about clean mobility. However, the target of fuel saving and emission reduction fell short. Automobile manufacturers did not take the requisite quantum jump. Instead, they operated adjacent to their existing competencies.

The Department of Heavy Industry formulated the Phase 2 of FAME India Scheme based on the experience of Phase 1 of FAME India Scheme as well as inputs from various stakeholders.

FAME Phase II

The Phase-II of FAME India Scheme was approved with an outlay of INR 100 billion. It commenced from 1 April 2019 for a period of 3 years (Ministry of Heavy Industries, 2019). 86% of the fund allocation under Phase-II of FAME India Scheme was earmarked for demand creation (Ministry of Heavy Industries, 2022b). The EVs were also exempted from road tax and registration charges (CNBC, 2022). In 2020, there were 1,827 charging stations in India. Establishment of 2,877 charging stations in 68 cities was sanctioned under FAME Phase II (Mukherjee & Thakkar, 2022).

The scheme provided for inter-segment and intra-segment fungibility as well as supported establishment of charging infrastructure (Ministry of Heavy Industries, 2022b). In June 2021, Phase-II of Fame India Scheme was extended for a period of 2 years till 31 March 2024. Less than 5% of the INR 100 billion outlay had been spent before the extension (Mint, 2021). The scheme was amended and made more lucrative. State-level incentives were provided to boost the EV demand (E-Vehicle world, 2022).

NATRiP

The NATRiP was a government-funded initiative to develop high-tech automotive capabilities in the country and make the Indian automotive industry a force to reckon with on a global stage. The total cost of the project was INR 37.27 billion and included automotive testing, homologation and R&D facilities under its ambit (NATRIP, 2022).

The policy measures and efforts notwithstanding, EVs remained a drop in the Indian PV Ocean. The fledgling market was nonetheless expected to boom and grow at a CAGR of 90% from 2021 to 2030 (Malik, 2021).

KIA India: The Journey So Far

Kia, the oldest South Korean automobile manufacturer, had morphed into a major international automobile company even before it commenced operations in India. It had operations in China, Europe, United States and many other countries as well. Kia had a vast repertoire of models ranging from SUVs, crossovers, sedans, hatchbacks, minivans, hybrid vehicles and EVs. Kia generated more than 80% of its sales from international markets. Kia’s India entry was part of the company’s strategy to further strengthen its presence in emerging markets. Kia established a wholly owned subsidiary, Kia Motors India (renamed as Kia India in 2021) to set foot on Indian soil.

The Three Pillar Strategy

Kia India had ambitious plans. The Korean company intended to make it to the list of top five companies in the Indian automobile marketplace by 2021. It intended launch two models every year. The company’s marketing strategy rested on three pillars; product differentiation, advertising dexterity, and distribution prowess.

Kia India competed on product differentiation. The Korean company backed itself on its design and quality capabilities. Many of Kia’s existing brands were sold globally (Move, 2017). The company could have introduced one of its existing models in India but chose not to do so. Instead, Kia India’s first market offering was designed for the local market.

Second, it leveraged its creative marketing capabilities and cemented its position as a ‘trend leading innovator’. Kia India’s first television commercial; ‘Magical Inspirations, Stunning Designs’ became the most watched advertisement on a video streaming on YouTube. The campaign witnessed 236 million video views on YouTube alone and bagged the distinction of becoming the most watched advertisement on the video-streaming site in the country (Brand Equity, 2019). Kia Motors roped in Tiger Shroff as brand ambassador. The Bollywood actor’s ‘youthfulness’ resonated with the Kia brand personality. The company intended not only to enhance the driving experience of its target market; millennials and Gen-Z, but also wanted to elevate the overall engagement experience with the Kia brand (Business Standard, 2021a).

Third, Kia India set up a ‘wide and deep’ dealership network to have a pan-India presence. Kia India conducted a multi-city ‘Design Tour’ to spread awareness about the Kia brand amongst customers and dealerships (Kia.com, 2019b). Kia India entered into an agreement with eight leading financial institutions in order to expand the reach of Kia India to smaller towns and cities (Kia.com, 2019a).

Kia India commenced sales with the largest distribution network for a first-time automobile manufacturer in India (Sukumar, 2019). To begin with Kia India had 260 customer touch points which were increased to 300 dealerships in quick time. The company planned to increase the tally of its customer touch points to 350 by adding dealers in Tier-3 and Tier-4 cities (Business Standard, 2021b).

Dream Debut

Kia India was in top gear right from the word go. Kia India began commercial sales began in August 2019 with the launch of mid-size SUV; Kia Seltos. Kia Seltos had the ‘sophistication’ and ‘assertiveness’ of a SUV (Kia.com, 2019c). A BS-VI engine, avant-garde interiors, host of safety and connectivity features, adept design and high quality provided value-for-money and created a magnetic pull on the Indian consumers. The entry level Kia Seltos HTE (petrol) was priced at INR 989,000 (Express Drives). The high-end variants boasted of many additional features as compared to the entry level variants. The strategy was to enable customers with different budgets buy the Kia Seltos. Kia Seltos competed with segment leader Hyundai Creta. Other competitors included Mahindra XUV 500, Tata Harrier, and MG Hector. Kia Seltos hogged the limelight with spectacular sales numbers. It upended the segment status and was a regular chart topper in the UV segment (Kia.com, 2020c). The brand was positioned as ‘aspirational’. The target market of Seltos was the young, tech-savvy consumers. The vehicle was designed to fit their lifestyle (Tiwari, 2019).

Other Introductions

Kia India introduced its luxury MPV, the Kia Carnival, at the Auto Expo 2020. The Kia Carnival was offered in 3 variants; the Premium variant at a price of INR 2,495,000 (ex-showroom), the Prestige variant at a price of INR 2,895,000 (ex-showroom) and the Limousine variant at a price of INR 3,395,000 (ex-showroom). The premium MPV was targeted at the ‘young-at-heart, trendy, and elite’ customers (Kia.com, 2020). Kia Carnival competed with Toyota Innova and Toyota Fortuner. A refreshed Kia Carnival was launched with four trim levels with Limousine Plus variant being the addition in 2021 (Financial Express, 2021).

Kia Sonet was the third product offering from Kia India and targeted the ‘young, social, tech-savvy, connected’ customer. Kia cemented its brand promise of ‘The power to Surprise’ by providing fun-to-drive dynamics in Sonet. The company believed that Sonet would hit the right chord with Gen Z customers (Kia.com, 2020a). It was launched at a competitive introductory price of INR 671,000 (Kia.com, 2020b). Hyundai Venue, Maruti Vitara Brezza, Tata Nexon, and Mahindra XUV were top competitors of Kia Sonet.

Kia India’s growth journey continued as it launched Kia Carens in February 2022. The vehicle epitomized the design philosophy of ‘Opposites United’. Kia Carens provided a unique blend of sportiness, sophistication, style and aesthetics (Kia.com, 2021c). Carens, the three-row seater was a vehicle for ‘modern Indian families’. The price range of Kia Carnes was between INR 899,000 and INR 1,699,000 (Kia.com, 2022b). The company rolled out exclusive after sales packages (Kia.com, 2022d). Kia India received 7,738 booking for Kia Carens on the 1st day of its booking (Kia.com, 2022a).

Kia India was going strong with its limited portfolio of vehicles. It had recorded cumulative sales of 500,000 vehicles (Banerjee, 2022). Of these 400,000 units had been sold in the domestic market and 100,000 units had been exported to 91 different countries (Kia.com, 2022c). The tally of Kia connected cars on Indian roads had increased to 175,000 (Kia.com, 2022d). Top-end variants constituted 60% of total sales at Kia India (Kia.com, 2021a).

Latest Launch: EV6-The Electric Crossover

The 5th product offering from Kia India was EV6, an electric crossover. EV 6 was launched in India in June 2022. The vehicle had been launched in global markets earlier. Kia India was not to manufacture or assemble EV6 in India. Rather the vehicle was to be offered through the Completely Built Unit route (HT Auto, 2022a). EV6 carried a price tag of INR 5,995,000 (ex-showroom). The vehicle was offered in two variants; GT RWD and AWD. The top variant was priced at INR 6,496,000 (ex-showroom) (Rawat, 2022).

The number of EV6 bookings was more than 3.5X the allocated quota of 100 units. Deliveries for the vehicle were scheduled to commence in September 2022. In India, the EV6 would compete in the premium E-PV segment with the upcoming models; Volvo XC40 and Hyundai Ioniq5. The EV6 had won accolades on the global stage (Move, 2022).

Kia had announced the ‘Plan S’ strategy in 2020. As part of this strategy, Kia planned to extend the battery electric vehicles portfolio to 14 models by 2025 and derive a quarter of its sales from eco-friendly vehicles. Meanwhile, Kia India planned to develop and launch an India-centric EV by 2025 (Mint, 2022).

The EV6 carried a hefty price tag. The E-PV segment in India was still nascent. Should Kia India have focused on the ICE segment and steered clear of the E-PV segment?

The Road Ahead

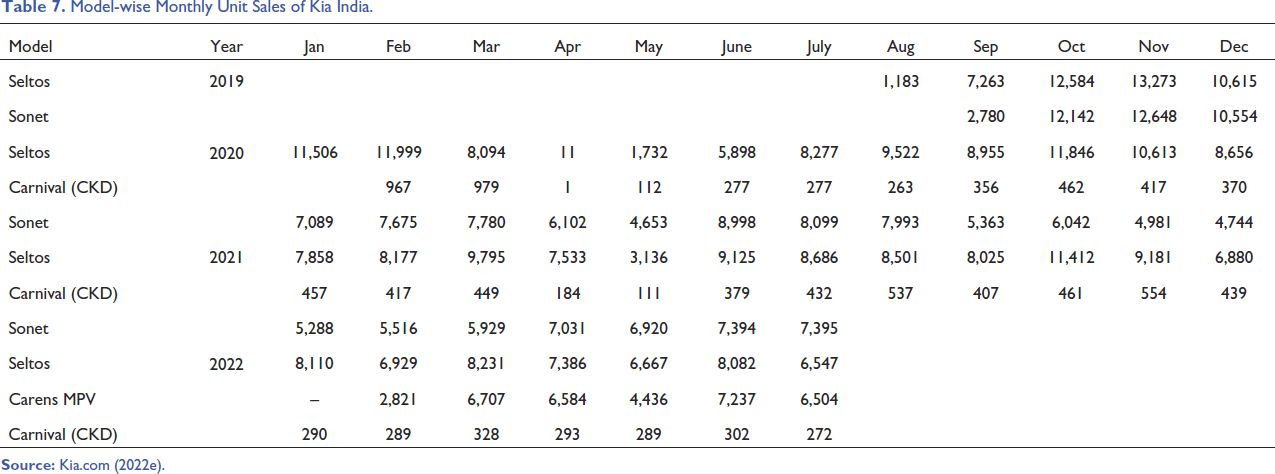

During the period 7-month period from January to July 2022, Kia India registered sales of 133,777 units. These included 51,952 units of Seltos, 45,473 units of Sonet, 34,289 units of Carens and 2,063 units of Carnival (Table 7). Sales spread across different models apparently establish that Kia India was not a one-trick pony. Is there a need to analyse the company’s portfolio through the lens of BCG Growth Share Matrix? The latest launch of EV6 entailed Kia India’s foray into the hitherto small but rapidly increasing EV marketplace. Is the Indian E-PV industry attractive? What factors have encouraged Kia India to foray in the Indian E-PV industry? How can the company replicate its earlier success in the broader PV market in the E-PV segment as well?

Model-wise Monthly Unit Sales of Kia India.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.