Abstract

This case adopts a dialectical method to illustrate firm-level strategies and competition in the Indian for-profit hospital sector. The case clearly contextualizes its setting within the developing country scenario and against a backdrop of under-provision in healthcare delivery. We compare growth models, horizontal and vertical integration strategies, mergers and acquisitions plans, geographical expansion patterns and physician engagement models of two leading hospital chains in the Indian hospital sector anonymizing them and masking them as the ‘Hospitals on Park Road’.

Keywords

The Hospital on Park Road

Physicians are our core assets; we will go to any length to make them happy and retain them in the system. I am not worried at all if there is another hospital coming up on Park Road, even if it is double our size and has better in infrastructure. But I will lose sleep if our physicians start moving to that hospital.

Ramani had just joined ‘the hospital’ as a trainee in the outreach department, fresh after a rural stint with NRHM. 1 She had recently completed her MBBS and interned with a Government-run medical college as a part of her degree requirements. Her experience in rural healthcare institution left her feeling uncomfortable with a ‘for-profit’ approach to healthcare even as she completed her first week working with a corporate hospital. During her first one-on-one session with Sharma, the senior manager of the hospital, she expressed her discomfort with the corporate style of functioning of the hospital. She wondered aloud ‘Am I failing my calling to help people by working in this hospital?’

Sipping coffee at the in-house Café (run by an MNC chain), Sharma responds carefully with a retrospective question:

Small health centres and nursing homes can function without large capital investments. While these organizations serve the needs of people in important ways, many have struggled to be on secure financial grounds. Way back in the 1980s, would any bank lend to a health entrepreneur? Could charity alone have been a stable source of funds to finance the capital needs for a large hospital chain? Or even a large hospital?

He went on to elaborate:

Our hospitals have already touched 32 million people! Our healthcare costs are at a tenth of that in the US and our quality of care has been of the highest standards possible. This is what we envisioned when we started out in 1980s and we have been able to sustain and stick to this ‘golden one-tenth’ principle since. As a result, we have achieved scale, competence and market impact while maintaining these relative cost advantages as we address people’s healthcare needs. Can you tell me what allows us to continue growing organically?

Sharma went on without a pause

Ever since our first hospital in the 1980s, only few for-profit corporate healthcare providers of in-patient services have commanded as much attention as we have. We relied on multiple operational strategies to deal with different challenges in this fragmented healthcare market: for example, we have been developing multi-hospital chains (horizontal integration), acquiring upstream and downstream businesses (vertical integration) and expanding into semi-related businesses and other geographic markets (diversification) to not only insulate against varying demand, but to also ensure that we can have efficient and least cost sourcing and delivery of our services and products.

Sharma drew Ramani’s attention to the varying organizational models that had come up, namely ‘Focused Factories’—single-speciality hospitals and ‘Health Cities’—multi-speciality hospitals co-located in the same campus.

Sharma elaborates:

[T]his transformation did not happen overnight—we anticipated emerging trends and undercurrents in the business macro environment since inception. On one side, demand for healthcare rose and so did the inflow of money; first, patients began spending more, then the private sector, including private equity and venture capital started flowing in, and eventually even government expenditure opened up to procure healthcare for the poor. On the other side, human capital in this sector rose as many India origin doctors who trained abroad began choosing to return to practice in India and forego foreign stints.

2

The salaries, perks and incomes of doctors rose in India as regulatory environments for medical education abroad became more challenging. In fact, one of the earliest to come back was the founder of our hospital. Our hospital chain is among the earliest of the several profitable and entrepreneurial hospital chains that have become sustainable over the past few decades. Could this have happened without the drive for competition and sustainability outside a corporate culture? Possibly. Some countries have invested in a purely public financed healthcare system, but India’s public expenditure on health, fluctuating at 1% of GDP has been inadequate in comparison to absolute need which has hovered around 5%–6% of GDP for long. Would a charity driven, partially subsidized health system have addressed this gap? I think not. Charity or subsidized care and institution-building and infrastructure to handle population health do not go hand in hand.

Without disagreeing, Ramani points out that these hospital chains are only interested in paying for insured patients, and that too, for the 3% of tertiary healthcare cases as margins are the highest there. Hospital utilization data show that tertiary care mostly involves cardio-vascular treatments, neuro care, joint replacement and orthopaedics, aesthetics and reconstructive surgery and oncology treatments. On the other hand, recalling her internship at Primary Health Centres, Ramani argues that there is a growing need for large volume primary care from medical practitioners, use of routine diagnostic and pathological protocols, and treating simple trauma. Many elective surgeries such as cataract operations, appendicitis, maternal and childcare services that need secondary care remain under provided. Ramani alleges that the hospital chains focus only on tertiary healthcare.

Sharma does not disagree.

Yes, you are right! Roughly 95% of the country’s delivery system is delivered in small physician practices; similarly, hospital capacity is split across community health centres, small nursing homes (fewer than 30 beds) and small hospitals (less than 100 beds). Perhaps only 10% of the country’s hospitals are larger than 100 beds. Consultants estimate that 90% of the country’s hospital capacity lies in this unorganized segment. In other words, 90% of the country’s hospitals do not serve tertiary care needs of people. The remaining 10% multi-speciality hospitals are mostly in Tier 1 cities and cater to needs that are much more complex and necessarily expensive. Remember these needs are clearly life-saving needs.

Ramani is curious: how can serving such a small tertiary care segment be profit making? Can hospital chains break-even by not catering to the entire spectrum of healthcare? And what about the Right to Health? How can that be incorporated?

Sharma rises up from the coffee table, wrapping up the one-on-one session with Ramani. He has enjoyed this conversation and decides to push Ramani further and sets her a challenging, albeit exciting task for the new intern.

I suppose there would not be much workload in the outreach department as there are no camps or rural outreach visits happening. Then why not pursue your curiosity? Bring some serious business analysis (of the Indian Hospital sector) on yourself. You would have already known that Fortis and Apollo are the major hospital chains (apart from Max Healthcare) in this market. Both chains have been pursuing strategies of building chains of hospitals (horizontal integration). Two of the systems have also pursued vertical integration strategies by acquiring potential feeders of needed inputs (e.g., physician’s practices, diagnostic centres, training institutions) and potential distribution outlets (e.g., pharmacies). Some have also pursued strategies of diversification into quasi-related businesses (dental practices) and expanded to other geographic markets. Get back to me after following industry report and market analyses on the two hospital chains. Give me an account of the history and evolution of both chains, their business models and strategies, relationships with physicians and current challenges with their horizontal integration and vertical integration. First review our ideas of horizontal integration, vertical integration and diversification. Enlighten me after getting answers to your own questions.

Ramani returns to her cabin picking up market research reports and industry analyses from the Hospital library. Her stethoscope and sphygmomanometer drown in the stacks of the reports on her desk.

Fortis Healthcare

Fortis Healthcare Limited (FHL) is a chain of hospitals, headquartered in India. It was established in 1996 with the vision, ‘to create a world class integrated healthcare delivery system in India’, entailing the finest medical skills combined with compassionate patient care by owners of Ranbaxy, one of the largest pharma companies and one of the world’s top generic pharma manufacturers. Fortis follows vertically integrated, ‘end to end’ health care organizers with capabilities in drug research, clinical trials, laboratory services and health care services delivery. Fortis is mainly focused on cardiac and life-style diseases. During the early years of its operations, Fortis focussed on the hospital businesses, building up a large chain of facilities. They have grown from their first hospital at Mohali (Chandigarh) which opened in 2001 with over 45 healthcare facilities as of today and their growth increases year by year. One possible point of concern about Fortis’s ‘expansion via acquisition’ strategy is that the mix of hospitals in its network may not have a common culture. Fortis managed this heterogeneity by developing a coherent organizational model that links operating units and adopting a standardized, formal operating system implemented in each acquired facility (Burns et al., 2014).

Fortis adopted a ‘hub and spoke’ model for expansion which helps to reduce operating costs and expedite healthcare and reach out to more consumers thus helping the business. Fortis has over 12,000+ beds, 415 diagnostic centres and 76 hospitals in different parts of India (FHL, 2019). The hospital ‘Hub’ served as Fortis’s anchor in that region, serving patients with severe conditions. ‘Spokes’ in the hospital network are stand-alone hospitals which are independently viable and provide more comprehensive services. Physician’s experts at the hub hospital provide the clinical leadership for practitioners at the spoke hospitals. Fortis also operates and manages several hospitals, ostensibly to generate referrals to other in-network hospitals. Fortis reportedly accumulates the majority (70%) of its surgical volume from within- network referrals and the majority of its operating revenues from in-patient admissions. To generate synergies from its network, Fortis implements common back-office functions across its hospitals. As in the US, Fortis charges higher prices to help support the large investments in infrastructure at the speciality centres, as well as the high salaries paid to specialists who are required to work there.

With respect to physician engagement, Fortis has followed an ‘employee model’ for doctors in key specialities by hiring them at high base salaries and offering them other incentives such as investments in their specialities, investments in out-patient diagnostic facilities to serve as feeders and variable compensation. They also provide insurance benefits, retirement benefits, etc. Physicians are not allowed to have private practices and must treat all their patients at Fortis facilities. High salaries are extended to physicians with the understanding that they will treat higher volumes of patients. Through this, it tries to avoid the traditional hospital dependence on physicians for their referrals and admissions.

Apollo Hospitals

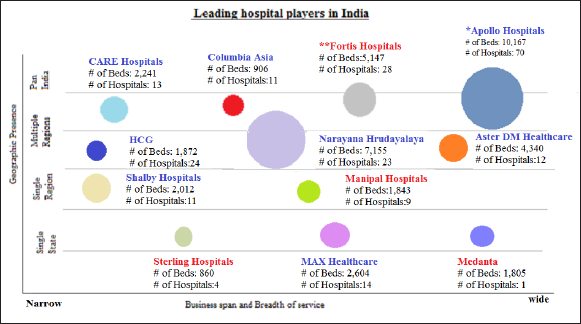

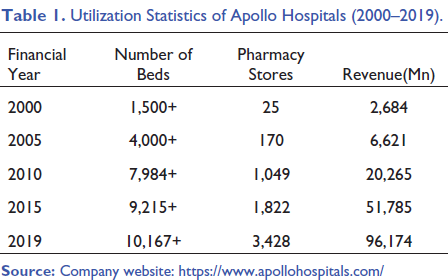

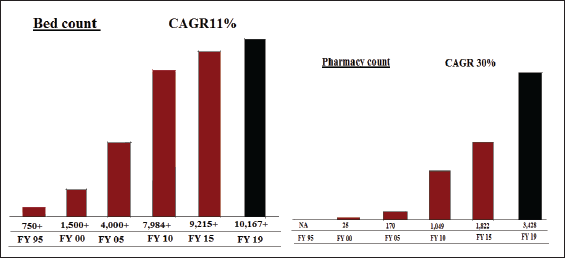

Apollo Hospitals Enterprise Limited is an Indian hospital chain based in Chennai, India. It was founded in 1983 by Pratap Reddy, a cardiologist with considerable clinical experience in the US. Apollo Hospitals started as a 150-bed hospital and now has crossed a footfall of 10 million lives. They believed that they could give hope to an entire segment of the Indian population who did not have an option beyond limited medical infrastructure. The hospital was the first for-profit facility in India. In contrast to Fortis, Apollo, initially, concentrated much of its capacity in southern India. From there, the system expanded to include 71 hospitals and over 10,100+ beds across Indian and Asia (Apollo Health Enterprise Limited, 2019). The founder was heavily involved in the governance of the system along with his four daughters who took leadership roles. In contrast to Fortis, Apollo grew more slowly and organically. Starting from its base in Chennai, Apollo has built hospitals rather than acquire ones. They have focused on building tertiary and quaternary hospitals in several Tier 1 cities (see Figure 1). The Chennai facility has grown from 150 to 561 beds and 46 ICU beds along with 15 operating rooms. In 1988, Apollo Group started their second chain of hospitals in Hyderabad. In 2000, it added six more facilities in different cities and another six by 2004 and in the 2004–2010 period, it doubled its overall capacity from 4,000 to 8,000 beds. By 2019, they owned almost 10,100 beds and 3,428 pharmacy stores (see Table 1).

Utilization Statistics of Apollo Hospitals (2000–2019).

Apollo has now some hospital presence in every Indian Tier 1 market and is expanding into Tier 2 and Tier 3 cities around the country. 3 There are almost 31 hospitals in major Tier 1 cities with 68% occupancy. They are starting new units in major Tier 2 and Tier 3 cities too targeting strong market positioning in select specialities. With such a growth impetus aiming towards a wider geographic expansion, Apollo used the concept of a ‘reach hospital’. So far Apollo has some 200 reach hospitals across India. In contrast to Fortis, Apollo has been more active in the contract management of other hospitals and this would have contributed to the chain’s ability to operate the highest number of beds (see Figure 2).

Clinically, Apollo has focused on cardiac surgery and higher end technological care, much like Fortis. Such technological advances may increase cost of patient care. But still Apollo has striven to keep the cost of care low for the patients. For instance, in the case of a Coronary Artery Bypass Grafting procedure, Apollo does the procedure in India at 10% of the cost in the US. Sometimes, Apollo (claims to have) done surgeries free of cost. How does Apollo manage this? It is seeking to serve a higher volume of patients by using technology to reach break-even faster. It charges patients more for more sophisticated technology, while acquiring the equipment at lower prices and forgoing certain high-end equipment that it believes has no patient benefit.

Apollo follows a traditional approach in physician engagement and managing medical staff. In India, Physicians have historically owned most of the hospitals in the form of nursing homes. Influenced by this pattern, Apollo was convinced that physicians may want to retain their autonomy and leadership position when they come on to work with corporate chains. At Apollo, doctors can have their own practices and are paid for their professional services on a fee for-service basis by patients (not by the hospital). Apollo bills the patients for the costs of equipment, facilities and supplies. In Apollo, physicians are evaluated according to their clinical outcomes, not the revenues they generate. This may be largely due to the philosophy of an organization founded and run by a medical doctor. Apollo now has shifted to a model where physicians have to take equity (purchase a number of shares) in Apollo’s hospitals and perhaps its new companies as the chain grows. This is in line with the traditional model of physician ownership (Burns, 2014).

Fortis Versus Apollo

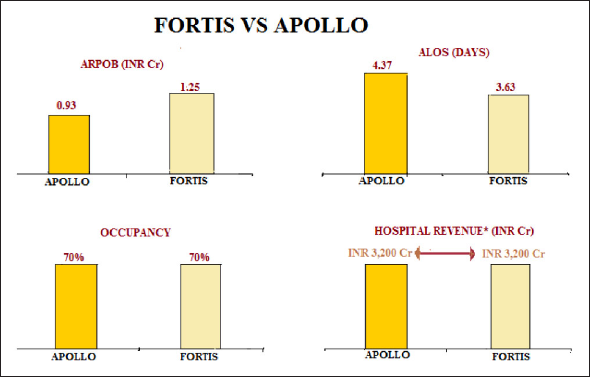

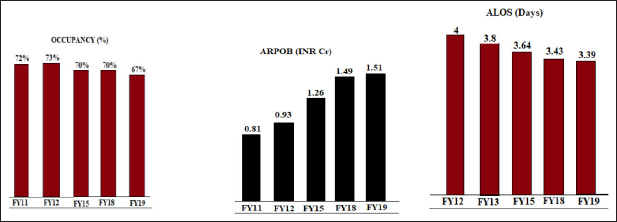

Apollo and Fortis are two competing hospital chains with similar geographic presence and also business span and breadth of service (see Figure 2). Like Fortis, Apollo strives for efficiency in delivering health care service, particularly through tightly controlled operating costs and high utilization of equipment. It also seeks to grow its revenues by expanding outside of Tier 1 cities. Moreover, it has sought to ensure a steady supply of clinicians (both physicians and nurses) by diversifying into clinical education and research. Apollo does not emulate Fortis’s effort to recruit ‘star physicians’ to whom patients flock. On the contrary, Apollo reportedly does not promote individual physicians, but rather believes in their own mantra, ‘More doctors, more provision and better system’. Fortis follows a fast and aggressive growth strategy while Apollo chooses to take a slow and organic growth trajectory. Unlike Fortis, Apollo has minimized its expenditures on physicians by avoiding employment models at least in Tier 1 cities. Apollo has distinguished itself by diversifying its revenue streams to include the sale of pharmaceuticals and engaged more heavily in contract management of hospitals within and outside of the country. Also, Apollo has sought to create a high local market share to drive utilization, scale economies and charge a premium. The implication of this pattern is clear when we plot Average Revenue per Occupied Bed, Average length of stay, occupancy and hospital revenue of Fortis and Apollo (see Figure 2). On an average, Fortis seems to be earning comparatively more revenue from each occupied. In contrast, on an average, in-patients of Apollo seem to be spending more time in the hospital when compared to their counterparts in Fortis. Surprisingly, both Fortis and Apollo perform similarly in terms of occupancy and hospital revenue. This implies that despite the different strategies, both hospital chains perform similarly. The individual performances of Fortis and Apollo in these dimensions are depicted in Figures 3 and 4, respectively.

The Other Hospital on Park Road

Ramani emerges out of the clutter of reports on her desk and laptop. She is convinced that she needs to bring in a different perspective. She wants to know the perspective of the ‘other’ hospital chain, the key competitor in the space. With an introduction from Sharma, she meets with Krishnan, the senior health manager of the ‘other’ hospital chain. Krishnan is curious and yet guarded about the interview, after all, Sharma is from a competing hospital. Ramani begins by exploring questions around operational aspects of the hospital chain?

Ramani: Why do you follow a Hub and Spoke model? What is the basis of the choice?

Krishnan: We follow a Hub and Spoke model only in certain markets. Before us, Wockhardt already had a hub and spoke model in place. Contrarily, Escorts had its presence in the cities of Delhi, Jaipur and Amritsar. We adopt such models in large markets and more specifically in the tertiary care space. We place hubs in geographically well-connected centres which would have niche-services and clinical offerings with well-established clinicians. For example, take our ‘Spoke’ clinic in the neighbouring suburb and this Hub hospital on the Park Road. The Spokes provide preliminary screening and outreach activities and sometimes support follow-up care after tertiary care too. They refer cases like cardio-vascular and neurological surgeries and joint–replacement to the Hub. This does not mean that Spoke hospitals need to pursue referral targets, that is, number of cases being referred to the Hub. Our system requires them to be ‘self-sustaining’ hospitals with their own financial goals. Each of these facilities are expected to break-even and not be revenue dependent for routine operations. Spoke hospitals are often located in locations with or little to no health care and sparse health facilities around. Markets naturally respond and expand to these locations given financial viability (and purchasing power of the floating population). We believe that through such hospitals, we can make some of the clinical talent available to such locations where these clinicians could do some simple surgeries. We follow the same clinical and support service quality standards in both hub and spoke. But when spokes start demanding more resources and better high-end infrastructure and services, we start thinking of promoting and empowering them gradually into hubs.

Ramani: You seem to be following an ‘employee model’ while engaging with the physicians. You hire doctors in key specialities at high base salaries and offer them good perks and incentives such as investments in their specialities and variable compensation. You also make key investments in out-patient diagnostic facilities to serve as feeders for their outpatient (OP) facilities. In your setup, physicians are not allowed to have private practices and must treat all their patients at your facility. High salaries are extended to physicians who treat higher volumes of patients. Does not this deprive them of their autonomy and bring down their efficiency?

Krishnan: First, I disagree with these terms—‘employee model’ or ‘autonomy model’. We believe that we follow the ‘full-time’ model while (the hospital) follows a ‘visiting model’. A full-time model helps create a large volume of work for the clinicians and the institutions. Here, the institution supports the clinicians, helps them build their experience and makes them a more valuable part of the brand. In our models, key decisions such as buying or upgrading technology are often taken in consultation with the clinicians. But in the visiting model there is little vesting in the relationship between the organization and the clinician. Working like a rental model such organizations function like a distribution centre with low levels of collaboration across the organization and only modest ownership of the brand among the clinician when compared to our full-time model.

Ramani is reminded of a signature statement she has heard HR mention in the Hospital

Physicians are our core assets, and we will go to any length to make them happy and to retain them in the system. I am not at all worried if there is another hospital being established next door on the Park road even if it is double our size and has better infrastructure, but I will lose sleep if our physicians start moving to that hospital.

Ramani: Your hospital chain seems to be adopting an aggressive, expansive route. You are acquiring more and more hospitals and even hospital chains and revamping them. How do you keep a tab on quality and standards during the process?

Krishnan: We have been in the industry for around decades. When we look back at our growth trajectory, you could easily find that our growth has been rather inorganic, at least in the early phase. But of late, we are averse to further major acquisitions and mergers. Currently we are concentrating on maximizing and standardizing the output efficiencies of the existing institutions in our system. We find ourselves in a potential maximizing phase. Now, given that we have reached a certain scale, we want to bring the best out of ourselves while trying to maximize returns. Still, there could be another expansion in the pipeline (Krishnan smiles)

Ramani (intervenes): But how do you assure quality standards then?

Krishnan: We have two quality systems in place: the medical operating system or the clinical process system and (our chain’s) operating system or the managing process system which standardizes activities.

Ramani: The other hospital chain is testing miniature versions of their hospitals in smaller Tier markets (mostly Mofussil towns) to maximize patient access and convenience. Such reach hospitals seem to be having a lower cost structure, charge lower prices (around 30% less than in Tier 1 markets) and deal with lower severity of illness patients. What is your take on such a reach hospital model?

Krishnan: Today our brand is a large system. We focus on Tier 1 cities and major metros, but we are slowly moving into Tier 2 cities. We are taking baby steps and is in search of the right model. When it comes to expanding to the lower Tier cities, often the constraint is locally available human capital, namely trained medical manpower. What we try to follow is a scale-down model. We look for financial viability in the new scale-down project through a quick SWOT. But what differentiates establishment cost in Tier 1 cities from Tier 2 cities are the real estate costs. We believe that there is no major difference in medical manpower costs across Tiers and locations.

Ramani: So, what are your views on expanding to lower Tier cities using such low-cost models?

Krishnan: Take it from me. ‘Low-cost models’ definitely do not assure quality at all. And probably such models do not work in private healthcare. Not all offerings and services can be provided in such hospitals. Often such locations provide lower demand and hence lower workload for our institutions well below the optimal levels. I could share multiple experiences of different hospital chains. These experiences clearly showed that such ‘low-cost models’ are indeed not feasible. A major hospital chain subscribing to the low-cost model expanded to a mofussil town. There they created a huge in-patient facility in that town without any air-conditioning. They had to face multiple problems in managing its processes. Such low-cost models often face man-power crunches mostly at the level of junior doctors and nurses.

Ramani: Finally, what is your take on your vertical and horizontal integration strategies?

Krishnan: To discuss the same, let us be clear of what the mainline activity is? A hospital’s operations could be segmented to in-patient and out-patient service segments or a segment such as the pharmacy services. Take the case of pharmacy services. We find it within our hospitals or as stand-alone pharmacies. But now this segment is hugely contested. The biggest threat to this segment in our hospital operations is posed by online/ app-based pharmacy services and local pharmacies doing home delivery. Apart from this, upcoming online healthcare platforms such as Practo and growing ‘home-care’ segment: Portea, Nightingale, etc. are beginning to eat into our pie. They are providing all possible entry level services and home-based medical care especially post-operative, pathological and diagnostic care. Now we are being slowly forced to locate and optimize our brand around our mainline activity: in-patient care. There is a rising presence of totally different set of players in the out-patient space. Thanks to this multi-level competition especially from these new generation players, soon we may have to restrict our focus to our core area- tertiary care, the surgeries and outsource home delivery of pharmaceuticals, diagnostic services and nursing care to these new players. Sometimes we do not know whom we are competing with-is our threat the ‘other’ hospital chain on the Park Road or the new online healthcare platforms?

Epilogue

Ramani is back at her desk and a Mckinsey report catches her attention. The report prepared for Confederation of Indian Industry forecasts that non-communicable diseases (NCDs), the non-metro urban market, the urban poor segment and the Government-sponsored social health insurance program would emerge as the four major opportunities for the Indian hospital chains. The report forecasts NCDs as a high-volume and high-value opportunity and the Non-Metro urban market to be the largest opportunity even for secondary and tertiary multispecialty hospitals. Ramani notices the near non-penetration of the corporate sector in the urban poor segment. She wonders whether the strengthening of state-led health financing systems through the Government sponsored social health insurance program, intended mainly for the underserved population, would help private hospitals enter this demographic segment and result in a win-win situation for both the patient and the provider (Gudwani et al., 2012).

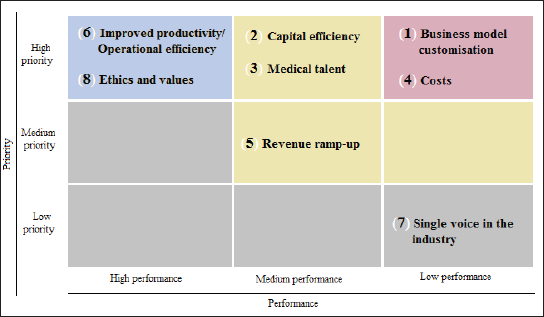

Flipping through the pages of the report, she reads about a roundtable organized by the consulting firm in 2012. This roundtable was attended by senior management of nine hospitals wherein they explored the top-of-mind issues which they face then and the issues they would face in the next decade and their preparedness to tackle them. They were asked to collectively rank different these issues along two dimensions: priorities and current performance and depicted in a 3 × 3 priorities and performance matrix which analysed the rankings. The message was loud and clear in the top right cell of the matrix: most hospital chains are ill equipped to perform well in business model customization and containing costs especially capital expenditure (see Figure 5). The roundtable has clearly flagged the issues of the hospital chains.

How would the two hospital chains be responding to these opportunities? What would be the best course of action for the two hospitals in the years to come. Would they continue to cherry-pick and cream-skim the tertiary care segment? How would their growth strategies, expansion and integration plans and most importantly their physician engagement models change when both hospital chains start tapping into these opportunities characteristic to a developing country? Calling it a day and waiting at the metro station next to the Hospitals on Park Road, she recognizes that her questions have changed.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.