Abstract

The insurance business model is fundamentally different from that of the banking business model. The Government of India (GoI) is the sole shareholder, both for Life Insurance Corporation (LIC) and Industrial Development Bank of India (IDBI); therefore, it made a business case for LIC’s acquisition of IDBI bank as a proposition for bailing out IDBI bank and then foray into bank assurance, giving LIC a unique footprint in the banking landscape. This case study highlights the rationale of this acquisition by evaluating synergies, economies of size and scale of opportunities, forward-backward integration of their products and services. This case study illustrates that forced corporate marriages, where the ownership is entirely with the GoI, both before and after the acquisition has its advantages, but on the flip side, has many disadvantages.

Introduction

The Indian banking business is believed to have been started sometime around the year 1770, and the first bank was the Bank of Hindustan. The then ruling East India Company established some more banks in India like the Bank of Bombay, the Bank of Madras and the Bank of Calcutta. The abovementioned banks were later merged and gave birth to Imperial Bank of India in the year 1921. It was on 1 July 1955, a portion of the Imperial Bank was nationalized and was known as the State Bank of India (SBI) (Mehra, 2016). The process also gave birth to eight subsidiaries of the SBI. Because of the operational ease and to beat the rising competition from private sector and other public sector banks (PSBs), all the eight subsidiaries were recently merged, thus making SBI as the Asia’s largest bank in terms of deposits and assets under management.

To better understand the Indian banking sector, its historical perspective can be described into two eras, the pre-liberalization and the post-liberalization era. In the pre-liberalization era, the Indian government nationalized 14 banks in 1969 and later in 1980, six more commercial banks were established (Goyal & Joshi, 2011). In post-liberalization era, the policy of liberalization was adapted by the Indian government and new licenses were issued to promote banks in the private sector in order to give impetus to the Indian banking business.

It was somewhere in 2010 that the Indian banking sector saw some of the well-known private sector banking mergers like ‘Bank of Rajasthan and Industrial Credit and Investment Corporation of India (ICICI) Bank, Housing Development Finance Corporation (HDFC) Bank acquiring Centurion Bank of Punjab in 2008’ and Kotak Mahindra Bank acquiring ING Vysya Bank in 2015 (Sharma & Rai, 2012). Post the above mergers, in 2019, Indian banking system has seen some unprecedented mergers among PSBs as announced by Government of India (GoI) to strengthen the respective bank balance sheets, facilitating competition and giving the much-desired impetus to financial inclusion through technological advancements. Last few mergers were done keeping in mind the operational and geographical synergies which has created some of the very large banks in the Indian banking system. These are some ideas that start out on a very positive note and fade away when not operated/executed properly. The merging of PSBs even in the past is one such idea. But sadly, the news does not end here.

Mergers in the past have always brought pain (pain may seem to be a mild word to express actually as an excruciating pain) to the investors—on account of uncertainties as regards newer valuations and aligned gains or losses, to employees of the entities getting merged—have always missed their promotion opportunities, knowledgeable employees who could bear the risk have always crossed over the river from public sector undertakings (PSU) to private sector and have been able to prove their mettle, while PSU institutions had to compromise with the leftovers (Andersen & Young, 2020; Sridhar & Jasrotia, 2020). Asset quality issues of merging banks are addressed through provisioning for likely loan losses, this is a regulatory requirement by Reserve Bank of India (RBI). To the exchequer—have always costed huge sums, just in the case of SBI merger with five associate state banks has costed Indian rupee (₹) 16.60 billion (Times of India, 2016). To the unions—have always delayed the process, nationwide bank strikes by segment of the unions. To the customers—computerization has always been a sour point for the bank taking over the smaller institution, ultimately affecting customer service and customer loyalty and reducing those barely offered/created moments of truth. Incidentally, mergers have never been able to bring to the fore the purpose with which they are being merged (Jasrotia & Agarwal, 2020). The history of bank mergers has always revealed a bad outcome in spite of best legislative intent. This is primarily due to bureaucratic inefficiencies and delays.

Keeping the above experiences in mind, it is known that IDBI Bank has been in ‘tatters’. There are actually no gains for LIC, expect for a bailout for the lender. A case in the point is if an insurance company wants to enter into a bank business or vice versa (SBI and SBI Life, HDFC bank and HDFC Life), then LIC can apply for a bank license, the way India Post applied for a bank license with the RBI. Going by the past experiences, it is expected that it will take more time for IDBI to attain some stability which means LIC will have to bear the losses for this investment and potentially provide more for the years to come. Researchers find it difficult to look for any logic for this investment. The purpose of this study is to bring to the fore the following: Indian bankers, economists, bureaucrats and politicians need to understand that forced mergers do not work anymore, and LIC-IDBI merger is another disaster in the making and its impact on the banking industry, objectives of creating larger and efficient organizations need better understanding of the synchronization theme where institutions of similar nature, size and activity be looked at and lastly, mergers are merely not an Investment Bankers job, but it is much more than it meets the eye. Successful mergers can create world class organizations, provide value for investors and an institution for employees to feel aligned and clinked to.

The Banking Landscape in India

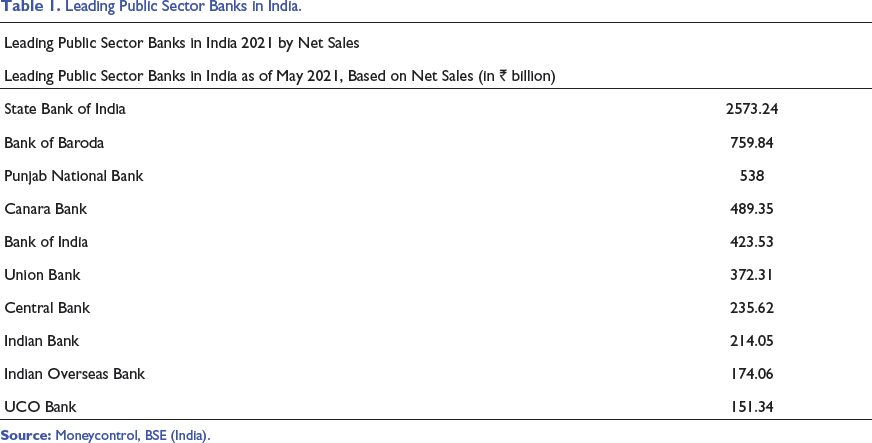

Leading Public Sector Banks in India.

The Indian Insurance Industry

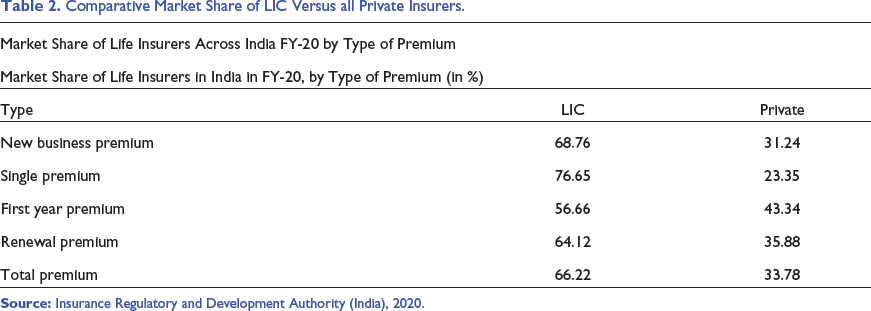

The insurance industry of India comprises 50+ insurance companies of which almost 20+ are on life insurance side and remaining almost 30+ are on the non-life insurers (Krishnamurthy et al., 2005). Other than LIC, the sole public sector organization in the life insurance space there are more than 5+ PSU non-life insurers. The market share of LIC in comparison to the private life insurance service providers in India is depicted in Table 2. India has a sole national re-insurer, that is, ‘General Insurance Corporation of India’ (GIC Re). Other stakeholders in the Indian insurance market are agents (individual and corporate), brokers, surveyors and third-party administrators offering health insurance claims.

Comparative Market Share of LIC Versus all Private Insurers.

Gross premiums in India have reached ₹5 trillion in FY-18, with ₹4.6 trillion from life insurance and ₹1.5 trillion from non-life insurance. Insurance sector in the past here in India has raised more than ₹434 billion through initial public offerings (IPOs) in 2017. September 2018 saw the birth of National Health Protection Scheme launched under Ayushman Bharat by GoI to provide coverage of up to ₹500,000 to more than 100 million needy families. The future looks bright for insurance industry in India especially for those dealing in life insurances with several changes in regulatory framework. Most of the changes are related to industry conducts, its business and engagement with its customers. The rate of growth of life insurance industry is projected at 12%–15% annually in the years ahead on account of the demographic factors—rising middle class, young insurable population and rising awareness among people of the need for protection and retirement planning etc. This is just the tip of an iceberg.

The Reverse Merger: IDBI (Financial Institution) in IDBI Bank

IDBI, which commenced operations in July 1964 as a subsidiary of the RBI, was set up as an apex lending institution in India (Garg & Kumar, 2012). Since its inception, the disbursals of the institution have been on a consistent rise and more than 70% of the large-term lending has been to private sector. The same has also been in the form of underwriting and direct subscription of shares and debentures.

IDBI in the past has played roles—promoting, nurturing, supporting and monitoring a range of national level developmental activities from industries to infrastructure to agriculture. The role has been quite significant more; so in alleviating poverty, reducing the developmental gap across regions and increasing the share of employment in the non-agricultural sector. The list seems never ending, and hence, it would not be wrong to say that as financial institutions defining its contributions in few lines would be much difficult.

ICICI was merged with ICICI Bank on 30 March 2002, keeping the above precedence in mind, the Parliament approved the merger of IDBI with IDBI bank earlier functioning as its subsidiary. This merger somehow raised questions and made it unclear as to how the development banking commitment would be met. It was realized later that such decisions further worsen the situation leading to shortage of long-term capital for the manufacturing sector, especially for Micro, Small and Medium Enterprises’s (MSME) seeking to grow in the country and essential for the GDP of the economy.

Reverse merger of IDBI into its own banking entity has always been raising eyebrows and have been in news, views and discussions for a very long period of time. It has always been looked at as merger among government institutions. After the IDBI merged with IDBI bank, RBI has classified IDBI bank as a private bank which did not bear any good results. In an effort to create a financial behemoth, decision makers completely missed on cultural fit resulting in humongous amount of losses and NPA’s getting accumulated (Jasrotia et al., 2020).

LIC Acquisition of IDBI bank: The Stakes

LIC has infused an enormous amount of ₹216.24 billion, acquiring 51% stake in IDBI bank (The Economic Times, 2019). Though there are enough doubts on IDBI bank ability to turn around its business, the deal has been in the news for two major reasons—(a) once again LIC is being seen as rescuing the government in its disinvestment programme and (b) the fact that the insurer has picked up a bank which is among the worst performing banks in India despite it being considered under private sector.

With the current price of IDBI bank less than half the price at which LIC was allotted shares in the bank, the insurer has already lost over half of the value of its investments. Owing to rise in slippages and huge provisioning, IDBI bank’s Tier-1 capital ratios fell sharply in June 2019 quarter, failing to meet the RBI’s regulatory requirement. LIC has stepped in again by committing to infuse ₹47.43 billion and another ₹45.57 billion would be pumped in by the government, which holds about 46.5% in IDBI bank (India Today, 2020). This ₹93 billion capital infusion into IDBI bank, which have been trading at a sharp discount to its book value, would lead to about 10% dilution in the book value, hurting LIC. If IDBI bank continues to underperform and keeps requiring capital infusion in the coming times too, it would bring accentuated pains for LIC. The RBI has classified IDBI bank as a private bank for regulatory purposes only after LIC’s acquisition.

The Good

In India, not more than 15% an insurer can take exposures in any one company. Any concentration of interest (i.e., to enhance stakes) would require specific approval of the Indian Insurance Regulator (IRDA). In light of the large size of policyholders and the most popular insurance organization in India, an exposure of ₹130 billion is just miniscule, and hence, the impact seems to be limited. Without an iota of doubt, this bank assurance tie-up will benefit the bank enormously with the insurer’s reach, number of policyholders, popularity and the ability to push products far and wide, and thus, contributing to the revenues of the bank. It would not be wrong to mention that internationally, acquiring a distressed asset by an insurer is nothing new and is a usual global practice. They buy assets cheap and sell at a premium.

The Bad

Is IDBI bank a turnaround story? There seems lot of ifs and buts. For LIC, the investment decision will make sense only and only if it is able to sell off the stake and make some money. But, with IDBI bank’s gross, NPA’s looming around 28% of its loan book, as on March 2018 and its capital adequacy ratio remaining below regulatory requirements, the decision seems going south. Moreover, for bank to come back on a growth path, it may need timely and multiple capital infusions. This is another cause for worry for the insurer’s policy holders and other stakeholders as it pays huge bonuses and dividends to its shareholders (mainly Govt.) Poor return on the investments will echo in the form of lower bonuses than the last ones (averaging out) affecting trust and brand of the insurer to a greater extent.

The Worse

The decision to take stakes in the bank seems a forced one. Had the insurer been a listed organizations, it would have definitely needed to defended its decision in front of its large shareholders who would have never agreed upon these investments. Though the exposures/stakes of LIC in the IDBI bank are miniscule keeping the size of the organization, the deal from all angles does not seem to be providing for any comforts as far as returns on investments are concerned. Nonetheless, times will tell what is in store for LIC as far as these investments and any transparency on information related to this deal from time to time will help researchers to dissect it as minutely as possible in the good interest of its large policyholders.

Dilemma

The government in its enthusiasm to address the teething troubles of divestments and fiscal deficit and at the same time exiting some loss-making public sector undertakings which are cash consumers and value demolishers; comes out with a ground-breaking idea of merging IDBI bank with LIC. This arrangement even goes contrary to the LIC’s own investment directives, which blocks it from taking over any business. The deal will lead to absorption of risk in the banking system, and it is still a mystery that how it will work to enhance the bank’s performance.

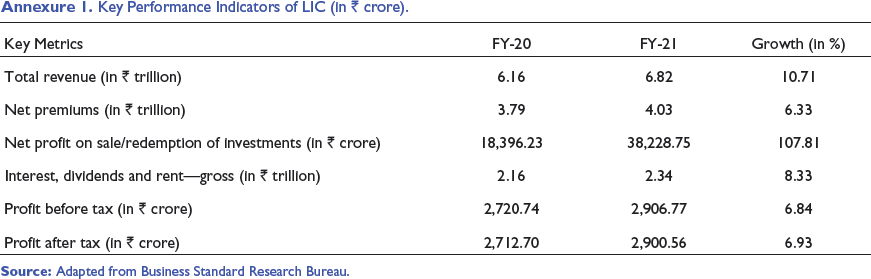

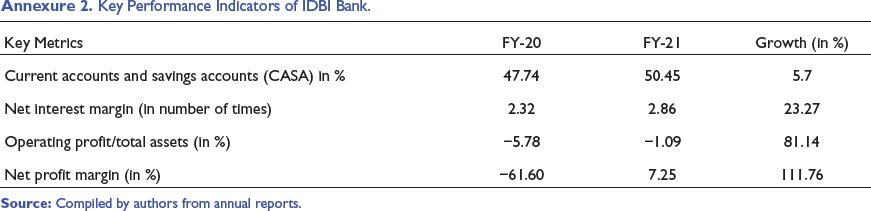

Given the fact LIC has been invited to select IDBI bank—which is among top worst performers in India with huge NPA’s and cash crunch—it completely now is on LIC and its ability to make the bank profitable, the chance of which seems very less or the policyholders of LIC will have to take a hit on the bonus payouts (Annexures 1 and 2). LIC is already burdened with NPAs in large chuck of portfolios and the Indian government instead of addressing the issue of resolving NPA’s are forcing LIC to buy a loss-making enterprise. On the other hand, the total non-performing assets of the bank now stands at ₹556 billion (more than 28% of the total credit). The capital adequacy is also lower than the stipulated one. LIC is a big name in India and giant player in Indian insurance sector. Since 2000, the private players in insurance sector are allowed to operate in India, but LIC still grasps over 70% of the new business premium, which is the sustenance factor for any insurance organization. Every year LIC issues nearly 20 million policies (Wire, 2018). Given that investments are made using public money, the rationale needs to be well explained and seems not in order. When the eyebrows are raised, it is always said that the idea muted is not good and this forced merger is simply a play with policyholders money which might reduce the bonuses for them. One small cut in the body, if not looked after properly, keeps bleeding and leads to multiple complications. It is just a beginning of another flop.

It will be a huge task for LIC to cut down the NPA’s of IDBI bank just offering the capital support will not serve the purpose. LIC has stayed the market leader in the insurance industry since inception but has started facing competition from private insurers now. Another major question which LIC should think is to whether focus on the losing market share of its core business or to diversify into an industry of which they do not have any prior experience of.

Key Performance Indicators of LIC (in ₹ crore).

Key Performance Indicators of IDBI Bank.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.