Abstract

The case deals with ethical issues in marketing in a larger context encountered while managing channels. Freedom AV Life Insurance, established in 2002, was a laggard in terms of revenue generation among private life insurers in the country. A new CEO, Ramesh Ramachandran, was hired to improve revenues, which drastically improved post his joining and upon on him hiring a new sales head. However, customer grievances multiplied, and Rajesh Bhardwaj, the customer services head, was questioned by the CEO and was asked to submit an action plan to stem the rising complaints. Bhardwaj felt this was the result of mis-selling by agents and the salesforce of the company. Bhardwaj proposed a solution by emailing the sales head. Just as he had finished writing the mail, he was surprised to find a new mail from the CEO asking him to prepare a presentation before the company’s board of directors in two days. At the end of the case, Bhardwaj becomes engulfed with self-doubt and anxiety on what to present before the board members. The case deals with ethical issues in marketing financial products like life insurance and looks at solutions to the practice of mis-selling financial services. Students would attempt to find answers to the question of whether they can achieve sales goals without resorting to unethical practices.

It was a hot day in the mid of May 2021 in Mumbai. Rajesh Bhardwaj, Customer Services—Head of Freedom AV Life Insurance Company, was a worried man not only because of the rising fear of Covid-19 but also because of mis-selling by various channels of the company. Bhardwaj had first received an email in this regard from his CEO, Ramesh Ramachandran, which was followed by an unpleasant meeting with him in which he had been asked to explain the steep rise in customer grievances and had been instructed to submit an action plan by the end of the week to bring these down. The CEO in his mail had sounded concerned at the deteriorating service levels leading to a sudden rise in customer grievances. The mail had ended with a question mark, a uniquely characteristic CEO’s usual way of showing unhappiness over issues.

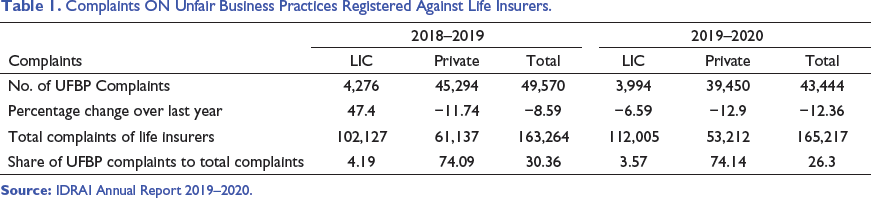

Though Bhardwaj was disturbed, he gathered his thoughts together and began looking at the email received from his CEO. In his mail, Ramesh had shared with him the data received on overall complaints during the year 2019–2020, which showed a jump of the complaints by 50% over last year. It was the 15th May and Bhardwaj had just finished his lunch a little late at 3.30

Indian Life Insurance Industry

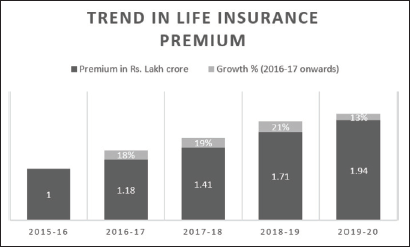

Between 2016 and 2020, the life insurance sector in India grew at an average of more than 15% every year. Life insurance businesses in India had grown from INR 1 lakh crores in FY2016 to ₹1.94 trillion in FY2020. Figure 1 shows the premiums for new and renewal business during the last five years from FY2016 to FY2020. In FY2020, there were 24 players in the life insurance business, compared to only four in FY2002. The only public sector life insurer in India was the Life Insurance Corporation of India, which was the market leader. To gain market share, 23 private firms fought based on strength of their distribution channels, customer service and brand-building initiatives.

The life insurance industry was a regulated sector governed by the rules set by the Insurance Regulatory and Development Authority of India (IRDAI), founded in 1999 under the IRDAI Act. In India, there was a lot of room for expansion in the life insurance industry due to the low penetration of insurance products at a mere 3.76% compared to the global average of 7.2%. The growing economy of India was expected to keep the boom in the insurance sector going. Higher household savings were directed into various financial savings instruments such as insurance and pension policies as personal disposable incomes increased.

Traditionally, the life insurance industry was dominated by a huge number of commission-based insurance agents, which as a distribution channel contributed the maximum revenue. Employee turnover was significant in the insurance industry. The financial advisors (agent) level had the most employee turnover, with minimal entrance barriers but strong targets and work pressures.

High employee turnover rates dramatically increased the investments invested in staff. The issue of losing money on staff recruitment was serious. In the beginning, companies invested a large amount of money and effort in training, but these investments did not necessarily translate into tangible earnings.

In the insurance industry, recruiting an agent involved preparing the agent to pass a pre-recruitment exam of IRDAI to get a license; this cost an insurer roughly ₹15,000, with other costs such as conveyance and administrative services. For almost the first 2–3 months, each agent remained in a non-productive or partially productive mode in the organization, learning how to get customers.

High staff turnover in the insurance industry was attributable to many factors. The first and foremost reason was that being an insurance agent was regarded as a societal embarrassment due to the unpredictability of employment and income. People worked as agents for part-time employment or a fill-in positions, not as a long-term career.

Because of the poor social status associated with becoming an agent, only a small percentage of capable people preferred to do so. An agent was required to understand the demands of the consumer and sell the products accordingly. This procedure needed a high level of persuasion as well as a long-term commitment. The tremendous income potential of becoming an agent enticed many people. Being an agent required a lot of patience, tenacity and persuasion on the field to make a decent living. Despite their hard work, the agents’ revenues were meagre in the early stages. Many of them experienced burnout during their first few years in the field as a result of this expectation-to-accomplishment gap. A lot of them dropped out and used to turn inactive.

Agents played a crucial role in advising consumers on the importance of insurance and assisting them ethically. Agents were often more concerned with meeting their targets than with the needs of their customers.

FREEDOM AV Life Insurance

A lot had changed over the last three years at Freedom AV. The chairman of KDFC group (holding company for Freedom AV) had hired Ramesh Ramachandran as the new CEO at an astronomical package that was being talked about in the insurance industry. The package given was with a promise to take Freedom AV Life Insurance, which was at Number 17 in the industry in 2017 in terms of market share, to among the top 3 life insurers in India. Freedom AV was languishing for the last 15 years at the bottom of heap and was seen as a poor performer, both in terms of its top-line and bottom-line numbers with a market share of a mere 1.2%.

To achieve this task, Ramachandran had hired Lovesh Kumar from BCICI Life Insurance. As Retail Sales Head, Lovesh was regarded as a super sales guy who had taken BCICI Life to the number one insurer in the country in just three years from number seven. Lovesh was a tough-talking boss to his team for whom achieving his sales targets was everything in the world. He cared less about the means to achieve them but was focused only on results.

The sales graph of the company had shot up with his joining and Freedom AV Life Insurance had moved up 10 places from 17th largest insurer to number 7 in only a year’s time. Lovesh had the full support of Ramesh to recruit more and more Feet-On-Street (FOS) salespersons to achieve this goal. Freedom AV salespersons in the direct sales team worked largely on the variable pay structure package. Only 40% of the salary was fixed, and the rest 60% was paid only on achievement of sales targets.

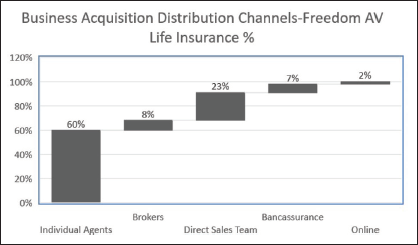

Agency Channel and Direct Sales team contributed 60% and 23% of the total sales revenue of Freedom AV Life Insurance, the remaining 15% of the business came from Bancassurance and brokers, and online channel contributed a measly 2% for Freedom AV Life Insurance (see Figure 2).

Mis-selling in Insurance Industry

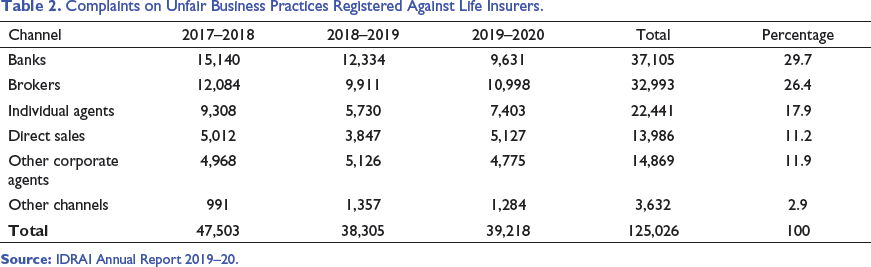

Complaints ON Unfair Business Practices Registered Against Life Insurers.

Complaints on Unfair Business Practices Registered Against Life Insurers.

One of the root causes of mis-selling in the insurance industry was that insurance products were complicated, and consumers frequently struggled to understand the differences between different types of products, let alone the relative merits of identical products from different insurers. This complexity contributed to a knowledge gap between the provider and the consumer. Many clients purchased a policy based on their advisor’s recommendation, only to be disappointed since the coverage was either unaffordable or did not meet their long-term financial goals.

This complexity had created an imbalance between buyers and sellers. This condition was referred to, in economic theory as ‘information asymmetry’, a situation where one party in a transaction has more information than the other and tries to benefit from the other’s lack of knowledge. In the insurance sector, this asymmetry of information encouraged mis-selling as the seller of insurance was in a more advantageous position than the customer.

All the life insurers were directed to bring out a company-specific policy on handling mis-selling complaints by the regulator IRDAI, which existed but was not followed in its spirit.

Mis-selling in Freedom AV Life Insurance

The complaints data of Freedom AV Life Insurance showed that among various complaints of customers, mis-selling by salesforce topped the list among grievances. The effect of mis-selling was that it was leading to an increase in policy cancellations and non-renewal of policies. The company of late had hired a lot of lawyers to meet up with the increased legal suits filed up by angry customers against the company in consumer courts all over the country.

This was not surprising as this was not a sudden turn of events, but the circumstances which had led to the present state of affairs, which the company had gone into had been building up gradually over the last 2 years.

Renewals had dropped as a result of high lapse rates, and the company was spending extensively on advertising, promotion and high commission expenses to attract new business.

The company had a Customer Service department headed by Bhardwaj who was working with Freedom AV Life Insurance for the past 18 years, right since the inception of the insurer in the year 2002 when the life insurance sector was opened to private sector players in the country. As Head of Customer Service at Freedom AV, Bhardwaj was responsible for providing leadership and direction to the whole customer service staff. Customer service executives and managers who worked in customer support, who were in charge of implementing initiatives and routine operations worked under his leadership. The CEO examined Bhardwaj’s work every month in the presence of other members of the leadership team. Bhardwaj had to gather and evaluate data on customer complaints to prepare reports and presentations. These were shared with the executive team regularly.

There was no distinct training department in the company, therefore the customer support team, led by Bhardwaj, was in charge of training salespeople, agents and customer service representatives in policies, operating procedures and processes. This included educating salespeople and implementing agent training programmes to familiarize them with current and upcoming product launches.

These training sessions were held in response to requests from the sales team. Salespeople and the customer care team collaborated with the sales team to plan a year’s worth of training.

To improve the salespeople’s confidence and competency, a budget for training was set aside each year according to the training calendar. The amount spent on training was charged to the sales budget. Due to lack of requests for the same from the sales staff, about half of the fund was left unused. The new sales head Kumar considered this a waste of time and energy. There were no dedicated trainers; customer service personnel who handled grievances at the inbound call centre of the insurer, doubled up as trainers. As the salesforce was spread all over the country. The customer services personnel had to travel to different locations to conduct training. The customer services personnel lacked respect as trainers in front of the salesforce as the salesforce and agents felt they lacked both field experience and knowledge.

The sales head was of the view that the time spent in the field to meet customers and make sales calls was more important than training. The sales head also felt that there was a need for sales trainers who could give product knowledge as well as teach recruits in selling skills. He had frequently told in leadership meetings that customer service personnel were good product trainers but knew nothing about skills required to recruit new agents and handle customers. Training for him meant stoppage of daily activity of salespersons who took part in the training. The salespersons also saw no advantage of attending these training events. A lot of them felt that if the time spent in training was utilized in doing activities related to target achievement, then these would be more fruitful for them. Bhardwaj believed that after passing the IRDAI’s mandatory pre-recruitment exam for getting a license, agents should be provided on-the-job training in addition to routine product training. This would aid them in having an experience of real-life situations. To save time and money, he felt the company had to switch to internet-based training. Because of the organization’s vast structure, online training would play a pivotal role in the future.

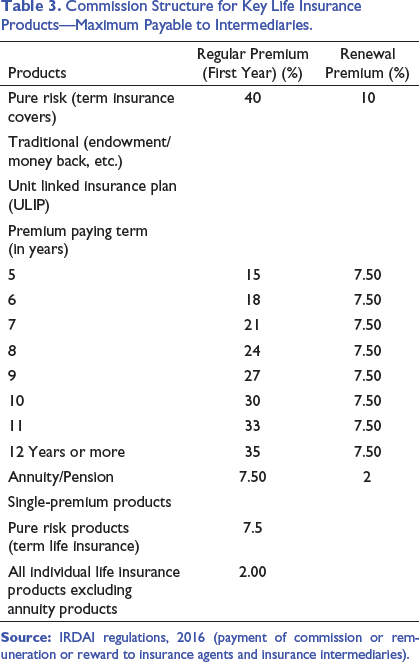

Commission Structure for Key Life Insurance Products—Maximum Payable to Intermediaries.

Another, key issue harming the organization was agent attrition or churning. This was due to the way commissions were structured in the life insurance sector, which was frontloaded. The majority of a policy’s commission was earned in the first few years, so there was little motivation for an agent to look long-term. The current system needed to be changed to ensure that commissions were distributed more equitably, to encourage agents to stay for servicing the customer for the long term. Because the agent’s future earnings would be impacted if the customer canceled the policy due to the product’s unsuitability, such a structure would encourage the agent to provide the proper product to the consumer. This would also ensure that the agent offers the consumer long-term service. In the current arrangement, for unit-linked insurance plan (ULIP) products, around 55% was paid up front, breaching the norm set by the IRDAI regulator with the 15% paid annually on renewal of policies. Agents were not interested in selling pure term insurance covers, which offered high sum insured at a lower cost. The push was to sell endowment, money back and ULIP policies. Bhardwaj felt that the commission paid could be split, so that 15% was paid up front and balance commissions on renewals spread over several years. However, this required a consensus of all life insurers as well as the regulator.

There were several underlying reasons for the occurrence of mis-selling at Freedom AV Life Insurance. The first was the incentive for agents to work on a commission basis. Because of the part-time nature of the employment and the low volume of business per agent, maintaining the entire agency force was costly, and regulatory caps on commissions were challenging. The temptation for salespeople and agents to offer policies that pay the highest commission without regard for an individual’s financial circumstances was strong.

The sales pitch that was made by executives of the company was the promise to double or treble money in a ULIP in a few years appealed to customers and customers fell for the same easily. Customers often ended up with incorrect or insufficient coverage. This resulted in a high rate of cancellations and lapse of issued policies. Too much emphasis was being placed on ULIP’s potential for wealth generation without a thorough discussion of the risks involved. The investment risks in ULIPs were wholly borne by the policyholders, a fact which was not disclosed to prospective customers by either agents or the direct salesforce.

Back to 15 May 2021, 3.30 pm

Just as Rajesh had finished reading his CEO’s mail he was startled to find Ramachandran the CEO walking in his cabin with a copy of Golden Times, the leading business newspaper which carried a news item regarding a complaint from a consumer group for which IRDAI the industry regulator had levied a hefty fine on Freedom AV Life Insurance. The complainants had been sold some policies by salespersons of Freedom AV by promising to give them smartphones and other gadgets as freebies post-sale, which were never given to policyholders. The customers had also been sold regular premium policies while telling them they were single premium policies. There was a mention of other complaints made to the regulator of unrealistic returns on ULIP’s to customers in the news item.

Mr. Bhardwaj I do not know how golden times got wind of this probably from the customers themselves. KDFC group has an image to maintain in the market. You just ensure you do your job properly. I need an update on actions taken by Customer Services to resolve these issues. Do speak to all concerned stakeholders and update me by end of the week on your action plan for immediate damage control and long-term plan as well for improvement of customer image and relationships. We should not remain, silent spectators when something as serious as the company’s image is in peril besides regulator going after us.

Rajesh did not react to this as Ramachandran walked out of the room.

Immediately after the interaction with the CEO Ramachandran, Rajesh went to see Lovesh Kumar. Lovesh Kumar startled him by saying ‘I know why you have come. Ramesh has apprised me of your meeting with him. I have a kind of busy schedule today. Why don’t you email me on how can I be of help? Come some other time if you need to’ said Kumar smilingly.

Bhardwaj was unhappy; he felt like an innocent victim who was being accused wrongly. Anyway, being in customer services and dealing with customers for years, he had acquired a Buddha-like demeanor while dealing with people.

He went to his cabin and began writing an email addressed to Lovesh Kumar. The mail read as follows:

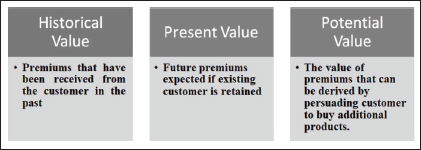

Dear Lovesh, As you are aware, the graph for customer complaints has been going up. I seek your support to reduce the same. I believe, to gain the confidence of policyholders there should be better disclosure of information about products in sales brochures. Before customers buy our products, they should be informed about all costs that would be incurred for the product, the expected returns that they would be getting, as well as the assumptions that the estimates are based on. The projections should be authentic, not unattainable. If returns are not assured, the company should be very clear-cut about that. Conditions and risks that are excluded from the insurance coverage should be emphasized and described to customers at the time when policies are being sold. This will avoid unhappiness later on when customers file for claims. When it comes to selling insurance policies, I believe ‘Telling the truth is the best option’. I have got a survey conducted among consumers which have highlighted the existence of serious concerns regarding the behavior of agency channel and our salespersons. The retail Sales Team must set high expectations both in terms of product knowledge and the ethical behavior of their agents. This involves adopting strict requirements for the selection of direct salespersons and individual agents. At the same time, there is a need to pay close attention to staff training, to make sure that the sales force is proficient to make the correct product recommendations to customers. This will minimize the instances of mis-selling. I suggest adoption Kirkpatrick’s model of training evaluation consisting of four levels of learning (Figure 3). Trust is a fundamental requirement in the business of Insurance; it symbolizes its core intangible asset. Hence, transparent and ethical practices are needed to build the reputation of any insurer. This involves working with unwritten value systems and having written codes of conduct agreed to by external stakeholders and the challenge for us as employees are to live up to the same in our daily operations and to maintain high ethical standards through our agents and salespersons. There are valid concerns about Mis-selling practices and problems associated with insurance agents’ compensation system, which is affecting Freedom AV’s reputation among consumers. We must at once make simpler and standardize the practices, to increase customer confidence. We need to include measures that reward ethical behaviour, such as incentives to encourage customer centricity, into their agents’ rewarding processes. It seems that a mix of result-based and measures based on ethical behaviour as well as customer-centric would be like adopting the middle ground to get sales numbers and have happy customers. Salesforce control systems can be categorized into those that monitor the outcomes of a process (i.e. outcome-based control), and those that monitor individual stages in the process (i.e. behavior-based control). In an outcome-based control system, salespeople are measured and rewarded based on results, like their sales numbers, new accounts opened, and whether they achieve their sales quotas or targets. In contrast, in a behavior-based control system, salespeople are assessed and remunerated based on their behavioral performance (i.e. their actions, knowledge, and skills); examining closely the ways and means they use to reach sales results and whether they sustain good relations with customers. Hence, insurers should not rely only on sales-based assessments in rewarding their agents. Instead, they should also combine further behavioral-centered control methods in their compensation scheme. This will reduce undue stress on agents to meet short-range sales goals. Also, it will inspire them to act ethically to create long-term relations with customers. One approach to measuring agents’ behavioral performance is to monitor the number of complaints and accolades that insurers get from each customer of the servicing salesperson or agent. The insurance industry’s usual practice is to give incentives to agents on meeting sales targets. Possibly, insurers could think of rewarding those agents as achievers who deliver as per the complaints and compliments received, and who deliver enduring customer contentment. Such rewards would act as solid motivations for agents to apply their energies to building good, long-term relations with policyholders. On the other hand, insurers could discontinue working with agents who produce a high level of complaints. Insurers should make such a policy highly noticeable to their agents so that it will act as a real deterrent to unscrupulous behaviour and unpleasant approaches toward customers. We need to track renewal rates of policies agent and salesperson wise. Those with low renewals need to need to be tracked and penalized by way of lower commissions and those higher renewal rates need to be incentivized suitably. Growing customers’ trust is most important; the customer needs to be assured and must have faith that the salesperson can be trusted to work in such a way that his/her long-term interests will be addressed. Therefore, insurers and their agents must win customers ‘trust and build a long-standing association with them. Customers’ faith in the insurance industry is not only reliant on the features of the product’s design but very significantly, on the insurers’ and their sales forces’ level of honesty and professionalism when selling them insurance covers. There is a need for agents and salespersons to form long-term relationships It makes economic sense to take a long-term view on client relationships over the long term. The sum of economic benefits received from customers throughout their lifetime is characterized as customer lifetime value (Figure 4). A business model with long-term survival necessitates implementing an ethics-focused business plan. To increase customer trust, we must ensure customer-centric processes with transparency and fairness. Thanks and Regards, Rajesh Bhardwaj Customer Services Head Free AV Life Insurance Co. Ltd

Just as Bhardwaj was about to get up from his seat after writing the long mail. He was surprised to find a mail from CEO Ramachandran marked ‘Confidential- Customer Grievances Issue’ to him. He hurriedly opened the mail. The mail read as follows:

Dear Mr. Bhardwaj, I hope you recall my earlier mail and meeting on the above subject. I had asked you to submit an action plan on countering the bad press coverage received and the penalty imposed on us by the regulator. The board of directors has taken a serious note of the same and the Chairman has convened a meeting at a short notice of 2 days. Request you to prepare a presentation to be made before board members and the chairman. Just outline the steps you would be taking to stop the repetition of such incidents in the future. You have my full support to try new ways to stem the tide of rising customer grievances. Best Wishes, Ramesh Ramachandran CEO–Freedom AV Life Insurance

Bhardwaj’s worries multiplied manifold after reading the mail. His team and he would be put to scrutiny now. His heartbeat raced faster as he thought of making a presentation.

What should he suggest? Should he share what he had shared with Kumar, the sales head in his mail before the board? Was the approach workable in reality? Should he just say that the news item and fine imposed by the regulator was not a systemic issue but a one-off case? Self-doubt and worry gripped his mind.

His mind was now full of questions for which he had no clear answers. He had just 48 hours to make the presentation as he looked at the clock on the wall hanging in his cabin with anxiety.

Footnotes

Acknowledgments

I would not have been able to write this case study without the support of Chairperson-Insurance Business Management programme Prof (Dr) Abhijit Chattoraj and Dean Research Dr Arunaditya Sahay also my fellow colleagues at Birla Institute of Management Technology who extended their support and help.

Disclaimer

This case is written solely for educational purposes and is not intended to represent successful or unsuccessful managerial decision making. The author/s may have disguised names, financial and other recognizable information to protect confidentiality.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.