Abstract

The present case study is based on the nation’s biggest-ever banking failure of India’s fastest-growing private bank, YES Bank. The YES Bank fiasco showcases the prevalent flaws of uprising NPAs and mounting bad debts in the financial sector. Post Asset Quality Review (AQR) conducted by RBI elucidate that the NPA of YES Bank is seven times higher than the actual reported amount in their audit book. The sudden trauma reflected the events unfolding in the bank as the share market plummets drastically and the losses enlarged exponentially. To stymie further deterioration, the Reserve Bank of India (RBI) stepped in and took over YES Bank management. The economy is already set to decelerate to an 11-year low following demonetization and the outbreak threatens to delay a revival in an emerging economy like India. The subject that this case will fit in is Capital Structure, Corporate Governance and Ethics and Auditing.

On 6 March 2020, I woke up and prepared morning tea at home located on the outskirts of the Hooghly River in eastern India. As per daily routine, I unfolded the newspaper lying in my veranda with the cup of tea in my other hand. Suddenly, my lips burnt as I froze on the news published on the front page of The Indian Express. The news caught me with utter surprise about the 30-day moratorium imposed by the Reserve Bank of India (RBI) on YES Bank, the fifth largest private bank in India. The first thought that struck inside me was ‘how safe is our money, nowadays, in the banks?’ I started reaching my friends and relatives having an account with YES Bank to enquire and console them, in particular.

Holding my nerves, I deep dive into the article as it piques my interest as a researcher. Several questions are bombing inside me while mustering the reasons behind the downfall of YES Bank. The vital reason highlighted was YES Bank’s aggressive lending approach (Barth et al., 2009; Canales & Nanda, 2012; Gambacorta & Van Rixtel, 2013; Zhang et al., 2016) in granting loans with a high repayment rate from 2% to 10% that created room for bad debts and eventually led to its plummet (Sarkar, 2020). A day before the incident (5 March 2020), the RBI imposed a 30-day moratorium period and replaced the current administrator with Mr Prashant Kumar, who was previously serving as deputy managing director of the State Bank of India (SBI) (Business Standard, n.d.). In addition to this, the withdrawal limit of ₹50,000 was fixed per account during the moratorium period (Misra, 2020). Eventually, the share prices of YES Bank shrank, following the outburst (Gupta et al., 2020). This sudden downfall of the top player in the banking industry intrigued the government policy and regulation, societal dilemma and how to overcome the fiasco to gain public trust.

Overview of YES Bank

YES Bank was considered among the fastest growing private banks in its nascent career, which started in 2004, with the prior approval of the RBI. Mr Rana Kapoor, Mr Ashok Kapur and Mr Harkirat Singh were the trio who led the way for its existence. Mr Rana Kapoor had an audacious dream of establishing a professional bank in India. After completing his bachelor’s degree in economics from Delhi University and his Masters in MBA from Rutgers University, he worked as an intern in the Citibank Information Technology (IT) Department in New York. During these days, he was inspired by the new-age banking system and desired to establish a similar banking system in India (Karnik, 2017a). Mr Ashok Kapur and Mr Harkirat Singh were the other two colleagues, who helped him in setting up Rabo India Finance in 1998 (Karnik, 2017b). In 2003, all three partners applied for a license to start YES Bank in India, which got issued in 2004. The year 2005 marked the first initial public offering (IPO) listing of the shares to the general public, and YES Bank was set up with a start-up capital of ₹2,000 million (Dubey, 2015).

The trio did not last long as a small feud led Mr Harkirat Singh to quit his role in 2003 since Mr Ashok Kapur was appointed non-executive chairman in his absence and against his wishes (Bhoir, 2013). Later, Mr Ashok Kapur succumbed in 2008, following the 26/11 terror attack at the Oberoi Hotel in Mumbai (Business Standard, 2008). Since 2008, Mr Rana Kapoor is the lone founder member incumbent at YES Bank. Under his supervision, YES Bank had taken several strategic measures to edifice corporate lending. They primarily focused on renewable energy, real estate, pharmaceuticals, media and the electrical sector. Mr Rana Kapoor emerged as an aggressive lender to corporates and business firms in need. In return, the bank charges a high rate of interest in comparison with other public and private banks (Gopalan, 2019).

By 2015, YES Bank launched a campaign namely India bole YES to invade social banking with an initial investment of ₹120 million. The campaign genesis was derived from the ethos of YES Bank. It relies on the findings of the consumer confidence index by Nielson that states Indians, in general, are confident about their future (Dutta, 2015). However, despite penetrative marketing strategies, the campaign failed drastically as the operation of the Indian banks was largely based on trust (Rudner, 1989).

Until 2017, YES Bank triumphed over the market, but its non-performing asset (NPA) started piling up with its ramification over bad loans. The sacking of Mr Rana Kapoor as YES Bank chief executive officer (CEO) by RBI further elucidates the deteriorating position of YES Bank. These consecutive events rampaged the share price of YES Bank, enticing RBI intervention to stabilize the situation. However, despite different optimistic approaches, YES Bank seemed destined to fail.

Building Momentum and Trouble

In December 2011, YES Bank declared a 7% interest on savings account (more than the industry average), following RBI guidelines of abolishing a 4% cap on savings account by liberalizing deposit rates of savings account, intending to attract more customers. In contrast, other private players were offering 3–4% interest on savings. This insurgence benefitted YES Bank as its current account savings account (CASA) ratio rose dramatically from 10.3% in March 2011 to 15% in March 2012, and it recorded a whopping 36.5% in March 2018 as the decision enticed the customers to keep their money with YES Bank (Kumar, 2018).

In 2010, Mr Rana Kapoor announced a rapid expansion by launching 900 branches in total from the present (150), establishing 2,000 automated teller machines—ATMs (94), employing 12,750 human resources (3,030), increasing the deposit base to ₹1,250,000 million (₹267,980 million) within India. The objective shifted from corporate lending to the retail banking business and small and medium enterprises (SMEs). The hunger for growing and spreading wings in different sectors has made YES Bank fall short in the long run (Mahanta, 2013).

YES Bank Crisis Aftermath

The squabble started long back following Mr Ashok Kapur’s demise at the promoter level. Following the demise, his wife proposed her daughter Ms Shagun Gogia (successor) as one of the board members. However, Mr Rana Kapoor and board members not only opposed the proposal on the ground of lack of experience but also wanted to move Mr Ashok’s family’s shares to non-promoter status (Nair, 2018). Not able to resolve the dispute internally, a petition was filed at Bombay High Court. In 2015, the court abstained from transferring Mr Ashok’s shares to non-promoter status and upheld the decision regarding partners’ joint rights (Dugal, 2018). Further, Justice Gautam Patel of the Bombay High Court suggested that the promoters bring down their shares in the bank to below 10% to solve the issue of appointing three directors jointly. This would end the rights given to the promoters as per the ‘Article of Association’ of the bank to appoint a director. However, Mr Rana Kapoor was on the point of mutiny (Express News Service, 2015).

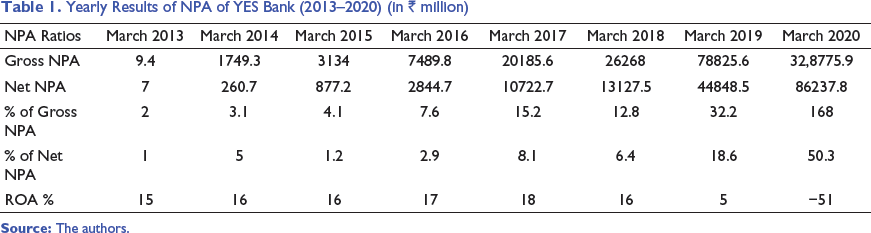

In 2015, RBI conducted its clean-up drive by asset quality review (AQR). This review was conducted to cross-check the corporate loan account as it was showing severe financial distress but was categorized as standard accounts in the books of the lenders (Press Trust of India, 2019). Post this review, the RBI came to know that the NPA of YES Bank stood at ₹49,300 million. This was seven times higher than the actual reported amount in their audit book in March 2016 (Roy & Kant, 2017).

Despite these, the bank had managed to add 756,000 new retail buyers in FY 2018–2019 in their vault, along with a 35% annual increment in its bottom line during FY 2008–2018 (Shah, 2019). During this tenure, a whistle-blower alleged irregularities in the operations of YES Bank. The whistle-blower was aware of two agendas, namely misclassification of bad loans and conflict of interest with Mr Rana Kapoor. To investigate the matter, he set up an internal inquiry committee that was supervised by the board members. The board reviewed the outcome of the inquiry in November 2018, with no conclusive results. Owing to this, the management approached a Vadodara-based auditing company JLN US & Co. to scrutinize the issue independently. With the available resource, JLN revealed that few real estate transactions were at arm’s length (parties involved in the transaction were independent). JLN’s stance was also inconclusive due to limited access to the documents provided by the bank. Finally, Securities and Exchange Board of India (SEBI) and RBI had to intervene to figure out a way to douse the growing canker (Gopakumar, 2019a).

Understanding the delicate situation, RBI effectuated the relieving of Mr Rana Kapoor as a CEO of YES Bank in September 2018, due to severe violation of corporate governance. He was succeeded by former Deutsche Bank AG and CEO, Mr Ravneet Gill, with immediate effect (Bloomberg, 2019). Shortly, after taking the charge, Mr Ravneet incorporated a disclosure practice in the company dubbed as ‘kitchen sinking’. It was a communications strategy to foray all bad news at once rather than in sliver. It provided aid to future decisions by receiving all the flak at once. However, the overzealous strategy backfired on him.

Yearly Results of NPA of YES Bank (2013–2020) (in ₹ million)

The stock market quickly reflected the events unfolding in the bank (Figure 1). The bank’s share valuation plummeted drastically from ₹393.20 to ₹181.20 in September 2018 (Kumar, 2018), resulting in a cumulative wealth loss of 40% in merely a week. There were two primary reasons identified for this debacle. First, emotional trading by the investors following the reports that Ms Madhu Kapur had disposed of about 0.04% of her stake. Second, the bank’s constant rebuttals of the charges of window dressing to conceal their NPA (The Economic Times, 2018). Subsequently, the investors suffered another blow of ₹165,000 million (a staggering 30% of their wealth) following the kitchen-sinking exercise initiated in 2019 (Mudgill, 2019).

The management considered raising funds as an avenue of recovery, ultimately, boosting the investor sentiments. It implied holding meetings with potential investors, eyeing investments from US$500 million to US$1 billion. Alternatively, options like issuing foreign currency convertible bonds and global depository receipts were also explored (Chaki & Dhanjal, 2019).

In May 2019, the bank’s reported stressed assets stood at ₹100,000 million, owing to its exposure in infrastructure, real estate and entertainment sectors (Sinha, 2019). It reported a huge downfall in its profits, from ₹42,240 millions in 2017-2018 to ₹1,720 millions in 2018-2019 (Adhikari, 2019), since it earned the title of 2019’s world’s worst lender (Ghosh, 2019).

The RBI appointed Mr Rama Subramaniam Gandhi (former Deputy Governor of the Central Bank) as an Additional Director to YES bank’s board of directors for 2 years. The RBI invoked section 36 AB, subsection (1) of the Banking Regulation Act, 1949. It empowered the regulatory bank to designate an additional director, if necessary, to protect the interest of the bank as well as its depositors (Gopakumar, 2019b). This sudden move by RBI reflected its cautious approach and indicated the grave situation. Subsequently, Mr Rana Kapoor’ family-owned Morgan Credits Pvt. Ltd. sold 2.3% of its shares in the bank for ₹3,370 million (The Economic Times, 2019). Another promoting group owned by Mr Rana, YES capital (India) Pvt Ltd, followed suit by selling 2.17% of its bank holdings at abysmal prices (Maya, 2019).

Government Input in Restructuring YES Bank

In the wake of deteriorating capital, liquidity, financial position and no prospect for capital infusion, RBI adhered to the following measures to safeguard public interest:

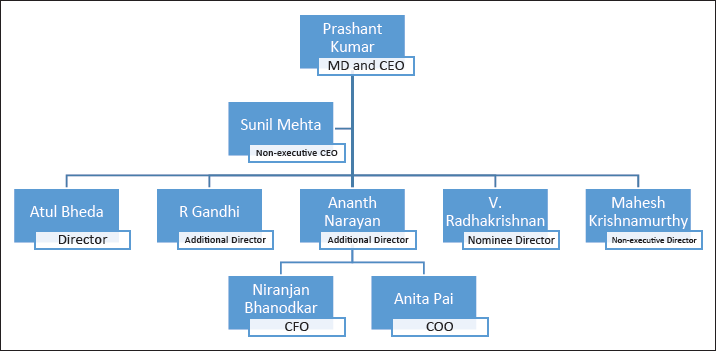

The RBI took charge of the board management and appointed Mr Prashant Kumar as an administrator on 5 March 2020. He previously worked at the SBI as the Chief Financial Officer (CFO) and Deputy Managing Director. Figure 2 represents the revised chart of the organizational structure.

A moratorium is a period where all activities are suspended temporarily until the related problem is resolved. RBI has also imposed a moratorium on YES Bank’s operational work, setting the withdrawal limit up to ₹50,000 for savings, current and other account holders. The limit applied to account holders having multiple accounts with the bank, as moratorium will apply cumulatively. However, RBI has relieved depositors to withdraw up to ₹500,000 in case of emergencies, such as medical, marriage, education and other unavoidable situations.

In 2020, RBI came up with a specific reconstruction scheme/plan directly oriented towards YES Bank. This scheme was entitled ‘YES Bank Reconstruction Scheme, 2020’.

YES bank’s reconstructed share capital

This scheme was initiated by RBI to alter the YES Bank’s authorized share capital to ₹500,000 million. Furthermore, the bank’s equity shares were revived to ₹24,000 million share in total with a face value of ₹2 per share, thus the sum aggregating to ₹48,000 million. For the reconstruction of the YES Bank, investor banks were allowed to invest with a restriction of 49% of the total share capital as post-infusion limit at a predetermined rate of ₹10. The investor bank’s infusion of their investment in the bank were to be locked for 3 years to restrict the investors from reducing their holding below 26%.

Board of directors constitution

RBI had restricted the appointment of the YES Bank’s administrator. The office was to be deemed vacated till the constitution of a new board. The reconstructed bank’s board had an addition of two nominee directors specifically appointed by the investor bank. RBI has been imbued with the power to appoint two additional directors according to Sec 36 AB of the Banking Regulation Act. Furthermore, the Act provides liberty to YES Bank to opt for additional directors. It is to be duly noted that the total number of directors in the board was not to exceed the mentioned limit in the bank’s Article of Association, excluding the number of additional directors that were appointed by RBI. The appointed directors of the board had to hold office for a time frame of 1 year from their appointment or till the time an alternate board member was constituted through the normal process mentioned.

Rights and liabilities in association with the reconstructed bank

All the associated contracts, deeds, legal papers and representations and similar instruments would function similarly as pre-time of the reconstruction scheme were implemented. All inflows and outflows of the reconstructed bank, like deposits, liabilities along with the rights and obligations towards their creditors were to be continued similarly, except as directed in the reconstruction scheme. As per the rules under Basel III norms, any instruments issued by YES Bank that were/could be qualified as an additional Tier I capital would be considered permanent. In addition, these had to be permanently written in their records from the date of the appointment.

Effect on the banks internal employees

The reconstructed bank’s employees were allowed to continue their services for the bank. Their remuneration as well as the terms and conditions associated with their services were to be considered to be the same as earlier. The reconstructed bank’s board of directors was imbued with the freedom to discontinue any key managerial personnel’s services.

Effect on the branches of the reconstructed bank

The branches will not meddle. In the future, the reconstructed bank needs to follow the RBI guidelines whenever they wished to open any new branch or close down an existing branch.

Reporting

The reconstructed bank was directed to declare/report all the necessary information associated with the bank functioning, including their schemes, course of action and other essential information to the RBI.

Conclusion

Since the banking system plays a crucial role in the development of an economy (Akhtar et al., 2020; Boyson et al., 2014; Flannery et al., 2013; Menicucci & Paolucci, 2016; Reinhart & Rogoff, 2014), its failure may have a catastrophic collapse for a developing nation like India (Allen & Gale, 2000; Demirgüç-Kunt & Detragiache, 1998; Furman et al., 1998; Mishkin, 1996; Shrivastava et al., 2020). The YES Bank fiasco showcases the prevalent flaws of rising NPAs and mounting bad debts in the financial sector. Surprisingly, this is not the first stance of banking failure. Oriental Bank of Commerce acquiring the Global Trust Bank and Industrial Development Bank of India (IDBI) Bank acquiring the United Western Bank were other stances when RBI had to intervene and exert its power to merge them (Goyal & Joshi, 2011; Jayadev & Sensarma, 2007; Kaur & Kaur, 2010; Kumari, 2014; Patel, 2018). Uniformly, RBI enforced its authority along with the finance ministry to contemplate the damage done due to the misappropriation of data to the YES Bank’s credibility. Their joint efforts put back the reconstructed bank on track.

The RBI had to step in and extend a 3-month special liquidity amounting to ₹500,000 million specifically for YES Bank to help them recover the deposit shortfall.

Currently, YES Bank requires a final investment of approximately ₹150,000 million capital to overcome their final hurdle for recovery, and this could probably set the lenders as well as the bank on track. YES Bank incorporated ‘cost optimization and productivity transformation’ through digitalization. It will assist in achieving a minimum of 5% saving for the financial year 2020–2021. Concerning recovery of the loans, YES Bank has officially announced to dispose collateral securities from Essel Group, SKIL infrastructure and many others, which constitute approximately ₹13,681.6 million of the dues. Furthermore, Avantha Holdings—a subsidiary of Thapar Groups and Oscar Investment Ltd.—constitute more than ₹10,000 million in dues.

These steps may propel YES Bank to perform better in the upcoming years and help them to regain their market capitalization, promoting investor’s confidence. It is noteworthy to mention that YES Bank’s performance is flourishing during the ongoing pandemic. The rejuvenated bank provides the notion that the probability of the YES Bank merger for survival is highly unlikely. The investors are poised to reap the benefits of their infused capital during the crisis time. Thus, the possibility of the government and RBI abandoning it during dire times is highly unlikely. Furthermore, the government and RBI has attempted to harness and safeguard the investors’ interest, in particular, and the public at large.

Recommendation to Avoid Such Crisis in Future

RBI had allotted significant time to exploit the loopholes in the management of YES Bank. However, YES Bank disclaimed any such allegations, and by the time of their acknowledgement, the bank was on the brink of destruction. This propelled the need for stricter norms, speedy measures and better control over the supervision by the regulators.

The situation calls for a separation of ownership and control at the basic level to avoid conflict. It was previously witnessed in the case of Global Trust Bank, where Oriental Bank of Commerce brought forth their rescue.

The YES Bank’s fiasco occurred due to misrepresentation of the bank’s balance sheet by the auditors. It implies that the selection and appointment of auditors require more precision.

Trust plays a pivotal role in any organization’s success as it dramatically reduces the potential for conflict. The same holds for the banking industry and demands transparency and regulation to protect the interest of the stakeholders.