Abstract

The micro-credit programme was introduced with multi-dimensional objectives and therefore was always under direct purview of various government agencies. Microfinance in Odisha works under umbrella of Mission Shakti and TRIPTI (a world bank initiated project). Balasore district is selected on the basis of MFPI index taking into consideration the saving, credit linkage and credit-deposit ratio indicators. The analysis had shown positive impact of programme on various economic, social and decision making dimensions. The linked financial institutions have undertaken SHGs as their major customers and therefore positive impact on loan disbursement and recovery rate is observed.

The introduction of micro-credit programme in Odisha on record may be traced back since 2001 with formation of Mission Shakti (State driven exclusive department for women and child development). Over the years, the programme has changed its delivery mechanism to reach the excluded section, resulting in a massive growth in the number of vulnerable women self-help groups (SHGs) formed and linked up at the state level (Rajpal & Tamang, 2016).The programme in Odisha is implemented via two different nodal agencies, that is, Mission Shakti (Chief Organization for implementation of Programme in State) and TRIPTI (Targeted Rural Initiatives for Poverty Termination and Infrastructure—a World-Bank-assisted Orissa rural livelihood project) taking into account geographical differences. The initial agency covers all 30 districts while the later agency covers 10 districts, majorly coastal districts in Odisha, on an intensive care basis. The execution of SHG-based micro-credit programme is supported by various government and non-government organizations along with independent research institutions, volunteers and grassroots-level facilitators. This programme has provided additional capability for grassroots involvement through orientation and participation. According to National Bank for Agriculture and Rural Development (NABARD) report (NABARD, 2013), more than 8.5 million WSHGs were linked to formal financial institutions in India under various social developmental programmes such as Swarna Jayanti Gram Swarojgar Yojana (SGSY), National Rural Livelihood Mission (NRLM), National Urban Livelihood Mission (NULM) and Swarna Jayanti Sahari Rojgar Yojana (SJSRY). In Odisha, SHG programme is mostly women-oriented and thus carried out under the Department of Women and Child Development (WCD) involving Integrated Child Development Scheme staff (mostly women staff is working in offices of WCD, Mission Shakti and ICDS). Till March 2019, there exist 0.663 million WSHGs in Odisha with a saving of ₹13,750 million (third highest in the Eastern region after West Bengal and Bihar).

Being among one of the poverty-driven and regular natural-calamity-affected state, the problems of individual can only be addressed through self-involvement and action. In recent times, the group involvement has gained popularity in state for addressing the needs of grassroots through self-efforts and self-reliance. The SHG-based microfinance (MF) programme is working at nascent level in Odisha (during the time of survey 2012–2013) keeping their services restricted to saving and credit linkage only. Even the state level organization, despite making several interventions, failed to implement the other instruments under gamut in the state. Rajpal and Tamang (2016) conducted a comparative study on financial performance and outreach of MF programme in Odisha and found greater differences and practical loopholes in the execution of the programme between tribal- and non-tribal-dominated districts (Thiyanayaki, 2014). Further, concentration of growth of the programme was observed in developed districts while tribal-dominated districts suffer from low saving and credit rates per member.

Research Problem

SHG-based MF services have received considerable attention from various government agencies in recent years. The involvements of interrelated departments, such as irrigation and watershed, etc., have provided supportive pillars at grassroots. Even though many studies have contributed significantly to the improvement, execution, organizational and impact analysis of the programme, there has been a lack of studies that compare state reports with ground/grassroots reality. Comparison of Macro-economic variables with grassroots position is required to address the invisible barriers and challenges.

Objectives of the study

To analyse the performance and outreach of SHG programme in different districts of Odisha.

To show the effectiveness of MF programme in developing entrepreneurship in the study area by inculcating various socio-economic, entrepreneurial and capacity building parameters.

To analyse the impact of MF programme in social and economic transformation of women members in the study area.

Data and Methodology

The study considers both secondary and primary data for making comparative comparison. The primary data is collected during the period from January 2013 to June 2013. The secondary data is collected via different sources for national level while district-wise state-level data exclusively from Mission Shakti and District Statistical Handbook (Government of Odisha 2011), State Statistical Report (various years).

As the focus is on addressing the actual position of WSHGs in the district, 50% of blocks were selected from different subdivisions. There exists homogeneity in rural occupation (i.e., either daily labour, farming or fishing) and living standard among communities in each blocks due to their geographical position. Figure 1 describes the geographical position of the Balasore district and samples selected to provide clarity on adequate representation of selected samples.

For primary data, multi-stage simple random sampling method is applied. Out of 12 available blocks in the district, six were selected randomly. In second stage, two gram panchayats were selected randomly, and, from each gram panchayat, 10 WSHG members were selected on a random basis. The selection of blocks was done keeping into mind various important parameters such as geographical distribution, SHG working, monthly report submission and financial assistance. Therefore, the study is executed in Balasore, Bahanaga, Jaleswar, Bhograi, Simulia and Nilgiri blocks covering 120 WSHG members.

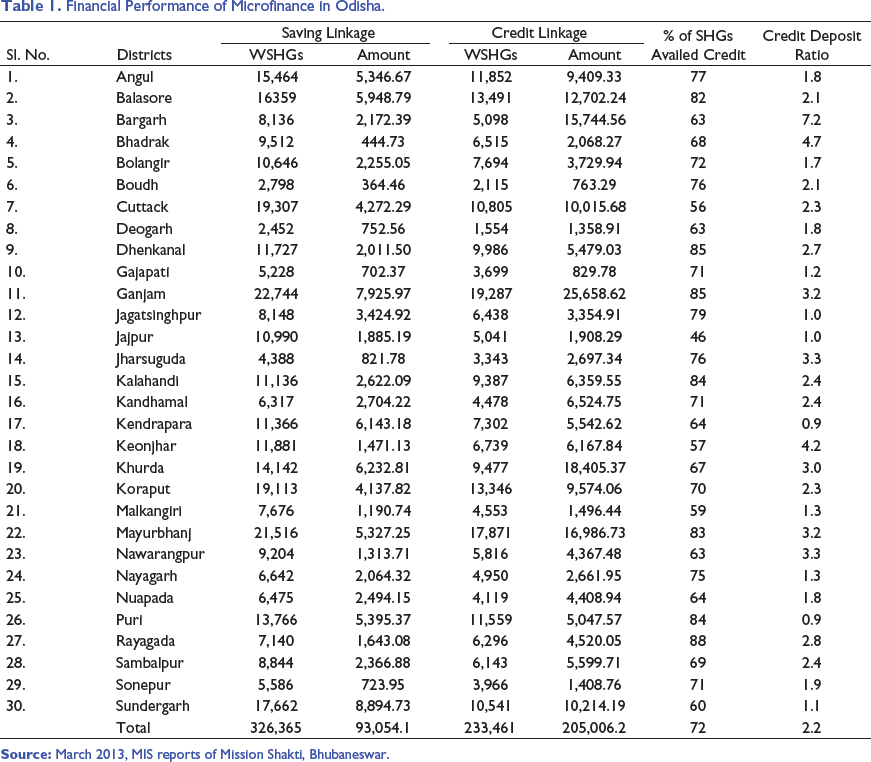

Financial Performanceof Microfinance in Odisha

Financial Performance of Microfinance in Odisha.

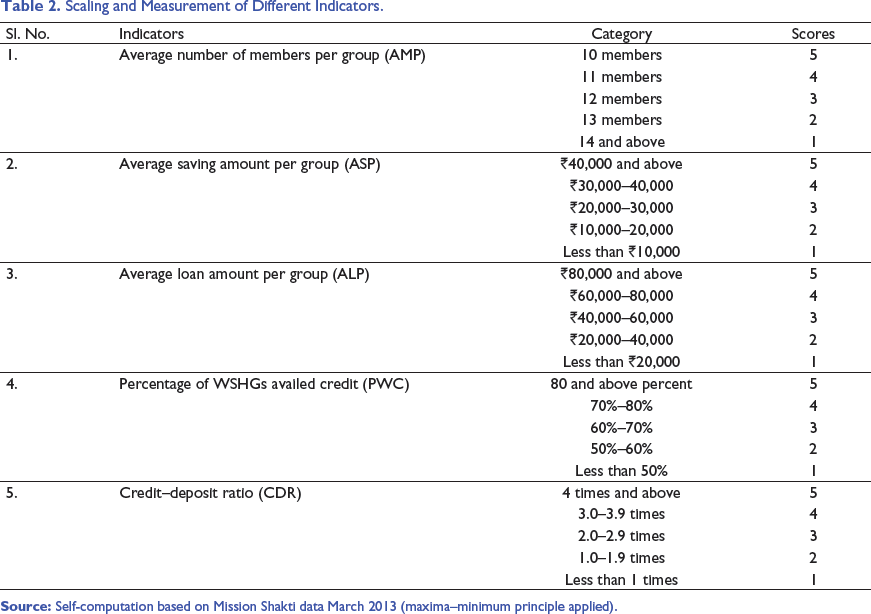

Scaling and Measurement of Different Indicators.

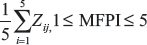

Based upon the indicators in Table 2, the MF performance indicator index is developed to analyse the performance of programmes in different districts of Odisha.

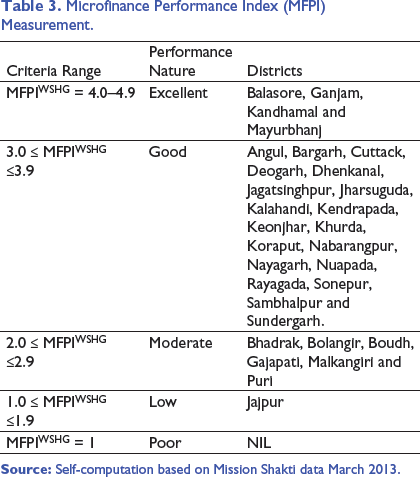

Microfinance Performance Index (MFPI) Measurement.

The intensive analysis in Table 3 shows that 13% of districts are excellent performers on the MFPI index, with top performer being Ganjam district (score 4.2), 63% of districts are showing good performance (mean—3.4, median—3.4 and mode—3.4), moderate performer districts accounted to 20% and only Jajpur was the low-performing district (poor performance in all parameters).

Therefore, being among the excellent performer category, Balasore district has been purposively (or methodologically) selected to conduct micro-level analyses for understanding the effectiveness and efficiency of MF programme on rural women transformation. The study is divided into four sections, that is, MF status in selected district, socio-economic status, SHG-based business operation and management and, last, benefits accrued and challenges.

Microfinance Status in Balasore District

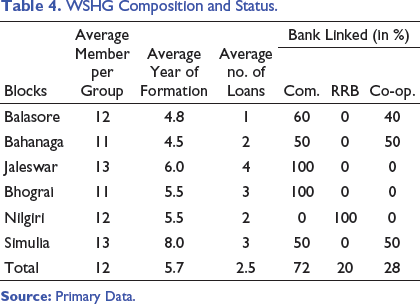

WSHG Composition and Status.

Socio-economic Status of Respondents

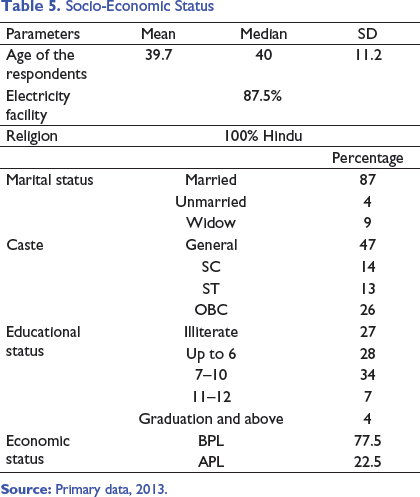

Socio-Economic Status

SHG-based Business Operation and Management

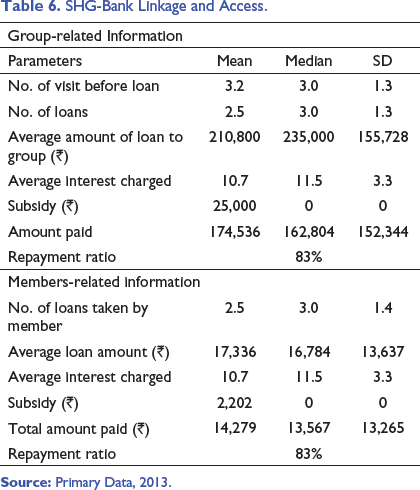

The major objective of the SHG programme is to promote livelihood through entrepreneurial activities and thus has given flexibility in the selection and operation of businesses jointly/independently. There exists no such restriction to opt for a specific activity with a specified person/permission. Before proceeding for entrepreneurship-related aspects, an attempt has been made in Table 6 to show the SHG—financial linkage and related aspects. The study found that 92% of WSHG members have bank loan via SHG programme while 8% of respondents (that too from Balasore block) have not availed any kind of loan since its inception. The quoted reason is the non-availability of all members to meet the required formalities. The number of bank visits before getting loan is higher in Bahanaga, Bhograi and Nilgri (50% of samples have visited more than 7 times for each loan), while it is the lowest in Simulia and Jaleswar (loan disbursed after 1–3 visits). The linked financial institution-wise analysis shows a higher average number of visits in the case of RRBs (4), Commercial Banks (3) and Co-operatives (2).

SHG-Bank Linkage and Access.

Interaction with members reported higher loan amount disbursement by commercial banks compared to RRBs and co-operative banks in the study area. The intensive financial institution-wise analysis shows that the mean loan amount disbursed to SHG is the highest with commercial banks (₹279,838), followed by co-operative banks (₹194,142) and the lowest with RRBs (₹125,500). The one-way ANOVA shows significant differences among these institutions on loan amount disbursement as the F value (17.33) is found to be significant at 0.01%.

The average loan received by WSHG members in the study area is ₹17,336 with same defined 10.7% rate of interest (no difference between bank loan and group loan). Block-wise analysis shows higher loan per member at Bhograi (₹30,597) while the lowest is shown in Balasore (₹7,925) and Nilgiri (₹9,119). The subsidy disbursement is made upon satisfaction of bank officials, resulting in two bulk instalments (first of ₹90,000 and second of ₹100,000) in Bhograi and Jaleswar blocks (21% of SHGs have received Subsidy under SGSY). None of the WSHGs have received seed money to revive their corpus fund till the date of survey.

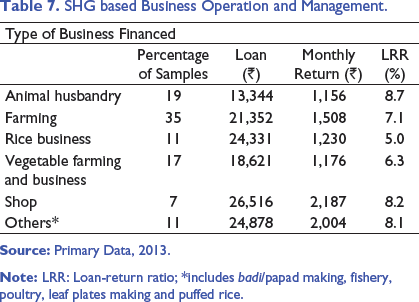

SHG based Business Operation and Management.

Note: LRR: Loan-return ratio; *includes badi/papad making, fishery, poultry, leaf plates making and puffed rice.

The average loan amount is higher in the case of shops (₹26,516) and others (₹24,878) while the lowest is in the case of animal husbandry (₹13,344). In terms of monthly return (in absolute terms), a similar pattern is followed, that is, the highest return from shops and others, and the lowest from animal husbandry, but in LRR terms, animal husbandry provides the highest return (8.7%) than the shops (8.2%) and others (8.1%).

Efficiency and Effectiveness of Programme in Women Emancipation

Multi-dimensional Indicators.

Economic Indicators Assessment

Dutta and Sahu (2020) observed improvement in livelihood practices across 350 MF borrowers through changes in income-generating activities and manpower engagement in West Bengal. The type of enterprise, duration of loan and volume of credit played a significant role in employability. Our analysis also found a significant impact of the SHG programme in selected dimensions of economic indicators, that is, income, expenditure, saving and employment. The average number of days of total employment before joining the group was 14 man-days, which has increased to 22 days after joining the programme and is statistically significant at 0.01% (t = −20.535, p < 0.00).

The total average income of the respondents has also shown an improvement from ₹1,284 to ₹2,272 after joining the SHG programme, which is statistically significant at 0.01% (t = −17.133, p < 0.00).

The average expenditure of WSHG members in the study area has increased from ₹1,930 to ₹2,870 after joining the programme, which is statistically significant at 0.01% (t = −29.519, p < 0.00).

The number of respondents having a saving account prior to joining the SHG programme was 6%, which has increased to 50% after joining the programme. The average amount of saving was ₹7.5 per month, which has increased to ₹89 per month and is significant at 0.01% (t = −7.62, p < 0.00).

Assessment of Social and Decision-making Indicators

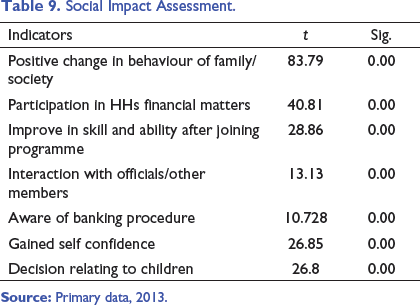

Social Impact Assessment.

The study reflects massive significant changes in social and decision-making indicators of the respondents after joining the group. Many respondents have reported that, due to increased share in employment, income and capacity of investment, the following changes in the behaviour of the family and society are observed. They make active participation in family or village related issues and if any problem/issues are unresolved within themselves, necessary possible supports are withdrawn from higher authorities like federation, promoting agencies and various others stake holder.

Discussion

The SHG programme has been initiated to develop livelihood opportunities through providing required financial support from formal financial institutions and skill enhancement. This programme upgraded the status of poor organizers and entrepreneurs and now serves among the major customers of the Indian banking industry. Mission Shakti—an apex organization for nourishing and maintaining databases has successfully transformed the programme outreach and efficiency. Its achievement may be revealed through the MFPI score (in Table 3), where all districts except Jajpur stand between moderate to excellent performer category. Further, the programme has shown similar potentiality by providing basic requirements such as regular interaction/meetings, book keeping, maintenance of corpus fund, repayment and training for skill development. An improvement in economic parameters, that is, employment, income and expenditure (i.e., proxy to income) is observed.

Implication of the Study

The present study highlights various methodological implications and utilization of indicators for evaluating the SHG programme’s performance at grassroot level. The programme was implemented with the objective of improving the socio-economic status of women, and similar results are being observed (in Tables 8 and 9) in a study of the Balasore district of Odisha. Economic upliftment is observed to be an important factor in social and cultural upliftment. Theoretical analysis through literature review also reveals a similar outcome at various regional levels.

Limitations of the Study

Various sensitive indicators that are required to be addressed for making programme and policy analysis are addressed by the authors with utmost care. However, there may have been chances where respondents had not revealed true information pertaining to loan structure, defaulters details, group lending mechanism, loan, income and savings.

Future Research

The present study has opened the scope for promoting agencies and linked financial institutions based on research on MF. Since improvement in various socio-economic and political indicators is observed, it also provides an opportunity to make comparative studies in other districts of Odisha. Further, this study/ analysis could also be done for districts under moderate and low MFPI index for a better understanding of the facts and reasons thereof.

Conclusion

The SHG-based micro-credit programme has shown potentiality in brining significant positive impact on various dimensions of empowerment in the study area. The major deficits identified through operational and interventional studies are lower amount of loans compared to national and regional levels, a massive dependency on mediators for marketing of their produce and a lack of market information accessibility. Being among the excellent performers in MFPI, the micro-level analysis also showed the same positive impact. The authors suggest the promoting agencies and financial institutions to increase their gamut of services by providing large amount of loans, doorstep saving and EMI collection, introducing low-cost insurance products and facilitating product marketing. Further, individual members have undertaken business as per their convenience and knowledge. The promoting agencies should take possible measures for developing group business as this could provide identity, large platform and returns.