Abstract

Five more days to go until the new year, it was a warm, pleasant and busy morning in Dubai, United Arab Emirates. As the clock ticked 10 times, Aditya Bhagat (Aditya), a young, ambitious, passionate entrepreneur, is seemingly intrigued and curious. Exactly 30 minutes from now, he is scheduled to meet Surya Prasad (Surya), his friend, counterpart and co-founder of BankBuddy (

Keywords

Corporate Overview

Business Overview

BankBuddy (

Cognitive computing is a process wherein human intelligence is applied to a computerized model that mimics the modalities of human operations through advanced technologies, such as automation, data mining, pattern recognition and natural language processing (NLP). When a cognitive computing model is applied to banks, it is transformed into a cognitive banking model, which is typically explained through descriptions of cases in which bots or humanoids execute repetitive and mundane customer queries and generate generalized outcomes. These queries include those related to automated teller machine operations, logistics and operations issues related to payment cards, know-your-customer and client onboarding (account opening and induction into banking practices) processes and many others.

AI solutions enable financial institutions to extend their reach across languages, enhance conversion, cross-sell and up-sell across consumer segments and service customers over a variety of channels. BankBuddy fuses AI (NLP, machine learning [ML], big data analytics, recommendation engine technology and computer vision) with insights into customer experiences to provide financial institutions a domain rich, pre-built and easy to deploy AI platform. Within the BFS sector, BankBuddy defines its target segments as new-generation digital banks, leading regional/country banks and progressive global financial institutions. In the long run, the company wants to be one of the top three global providers of solutions with respect to AI banking, customer experiences and product spaces.

With a relentless focus on enhancing the stakeholder (end-user/customer) experiences of their clients, BankBuddy believes in a three-pronged approach to achieve this objective:

Assist—The application of AI solutions using a judicious mix of human and machine interactions to assist stakeholders in effective task completion. Automate—The provision of vertical AI solutions that automate transitions across systems, processes, groups, departments and segments. Analyse—The implementation of cognitive banking solutions to predict, recommend and optimize interactions.

The structure of BankBuddy’s business units (also referred to as product lines) reflect the surrounding market imperatives of the global banking industry, with concentration manifested predominantly in three principal segments of banking consumers: personal banking, business banking and investment banking.

Business Units

Personal Banking

The personal banking product line of BankBuddy is the latest and fast-moving business unit of all. Roughly half of the overall business volume of the company and a sizable number of marquee client engagements constitute this product line. BankBuddy’s retail banking customer experience platform, having been deployed to eight countries in the Middle East and Africa, is meant to leverage the power of banking AI solutions in bringing back the ‘personal’ in personal banking. The solution, which is an amalgamation of chatbots, voicebots, AI recommendation engines, deep learning, computer vision and predictive analytics, is built on a cognitive banking platform that is redefining the personal banking arena by enhancing self-service automation, mass personalization and task automation. This enhancement ultimately enables service delivery at scale across all digital channels and functions.

Business Banking

Accounting for nearly one-third of the company’s overall business volume, the business banking product line boasts of a diverse client base extending across geographies and functional areas. The business unit is predominantly designed to cater to small and medium-scale businesses with guided flows for small business loans and cash management or the use of prompts and triggers to create a dynamic path for the structured resolution of queries in free-flow conversations. This product line facilitates the automation of several banking processes at warp speed. It offers pre-constructed task bots for some of the most frequently used banking functions, including the following:

Small and medium enterprise loan Business/current account operations Know-your-customer operations—keeping journal-verified customer identities Onboarding operations—Account opening and induction into banking operations Top up loans

The product line primarily addresses the problem of high costs to serve the end-customers of business banking providers—costs that stem from a multitude of products, high-touch processes and frequent interaction.

Investment Banking

Comparatively, the newest product line is the investment banking business, which is geared towards alleviating the foremost challenges in the investment banking domain—the substantial volume of dynamic information, unpredictable interaction frequency and the existence of a wide variety of digital channels. The product line is built on a cognitive banking platform that is redefining the investment banking landscape by automating service delivery at scale across all digital channels and functions.

Geo Strategy

BankBuddy is headquartered in Dubai with a development centre in Bangalore, India. Client presence is in eight countries across the Middle East and Africa. The overall ecosystem of the company extends to more than 15 countries, including the customers, partners and business units where the company had performed proofs-of-concept.

Why has Dubai been Chosen as the Headquarters?

As the only country with a dedicated ministry for an Artificial Intelligence Department, United Arab Emirates (UAE) was the first target market for expansion, while Dubai in exclusivity was the first and largest operational base of BankBuddy. Thanks to the true cosmopolitan and multi-cultural nature of the city, Dubai has provided an opportunity to explore a diverse demographic, ethnographic and linguistic user base. Dubai has a culture of innovation and ability to connect and experiment with the 200+ nationalities that are said to be living and operating out of the city. Moreover, Dubai gave BankBuddy an opportunity to perform accelerated adaptational testing of their cognitive banking concepts from a single location.

Dubai is the flagbearer of AI in the Middle East, Africa and South Asia (MEASA) region. As a financial centre, it has a large number of progressive financial institutions that are keen to adopt and co-create innovative solutions in the banking and financial services industry. The confluence of a diverse market, innovative culture, regulatory environment and government support has made Dubai the ideal destination for international FinTechs.

From here in Dubai, the English-speaking part of Europe seems to be the next logical destination for BankBuddy. Due to Dubai’s cultural and linguistic diversity, the next big issue to address, once the firm expands into Europe, would be to find a logical entry to the geographical centroid for their operations.

BankBuddy is also one of the very few firms selected for the FinTech Hive, the first and largest financial technology accelerator in the MEASA region.

As reported by Deloitte (Figure 4), more than 25 European countries have been selected for their IT services and FinTech exports. The most important step is to identify which out of these cities are the three best choices for BankBuddy to immediately consider for expansion: which is the best city to start operations from a cost benefit standpoint? Which is the best city to start operations from a time-to-market standpoint? Which is the best city to start operations from a skill availability standpoint?

The Marketing Journey

Marketing Roadmap: The Inception Phase

Financial institutions are struggling to keep up with the rapid changes in customer behaviour, be it with new messaging channels, customer service expectations or personalized service delivery. A vast majority of financial institutions are looking at AI to solve the aforementioned challenges but with limited success because it requires a unique combination of AI, technology, domain, channels and customer experience. AI solutions also require a huge amount of data and continuous maintenance. Therefore, there is a need for a banking domain to specifically productize a customer experience platform to help banks leverage AI to scale.

Aditya explains:

As a software product start-up in a nascent technology space, our first priority was to create a compelling value proposition in terms of the solution breadth, scalability, and coverage. We started with a product roadmap covering high impact areas to help financial institutions enhance revenue with a focus on customer journeys and experience.

Traditionally, financial institutions use internal process automation AI tools for cost reduction: 82 per cent of bank prospects expect to have researched the products online, whereas 59 per cent require help to make the final decision. Additionally, 59 per cent of bank prospects do not find the bank information they need on their website, while 53 per cent of these will end up as an underserved customer. While it was a novel idea to focus on the customer experience, this strategy had seemingly worked well for BankBuddy in terms of positioning them as a revenue enhancement and customer experience tool with pre-defined return on investment (ROI) metrics. The BankBuddy retail banking product is expected to have improved the customer experience in 89 per cent of customer installations. AI adoption in banking is expected to have reached only 35 per cent across the globe, and hence, it is safe to assume that there is market and expansion potential for the BankBuddy product suite.

When questioned about their initial benchmarks and checks and balances towards a successful launch, Surya explained:

We defined specific R&D/product development objectives to create a rich solution and did not go with the traditional MVP approach. We benchmarked our competition, substitutes and alternative solutions and launched our solution only after we reached the maturity level of the industry leaders. After the commercial launch, we set out a target to get at least one paying customer in 4–5 months and managed to achieve much more than that.

Business Processes that are Served by the Product

The product typically enhances business processes such as conversion, retention, cross sell, upsell, customer service, financial literacy, inclusion and journey mapping and proactive robo-wealth management advisory.

The Product’s Proven Functionalities

Due to critical features, such as comprehensive domain coverage in customer journeys, best in class technology and language support, some of the benefits experienced by the clients have been to significantly increase their cross-sell, upsell, retention and conversion by at least 15–20 per cent while also reducing the cost to serve by 30 per cent.

Marketing Roadmap: The Consolidation Phase

When asked about what worked well for you until now, Aditya explained:

BankBuddy had the opportunity to participate and exhibit in a number of events such as GITEX, Dubai World Insurance Congress, Global Finance Forum, BBK EmTech Expo, Middle East Banking Forum, etc., and this helped us in demonstrating thought leadership and generating a steady stream of leads. BankBuddy uses a clustering target market strategy while prioritising the market that they want to operate/expand. We assess typical customer/financial behaviour, cultural and language gaps, demographics and ethnographies, and regulatory constraints. Being in an industry where speed-to-market counts more than margins and agility means imminent success, we always believed that one of the accentuating factors of our growth is the speed with which we help our clients implement our solutions and start leveraging benefits. We have followed processes such as rapid application development models with user testing being introduced very early in the stage, which in turn enables the bank to go live with BankBuddy based solutions in less than six weeks.

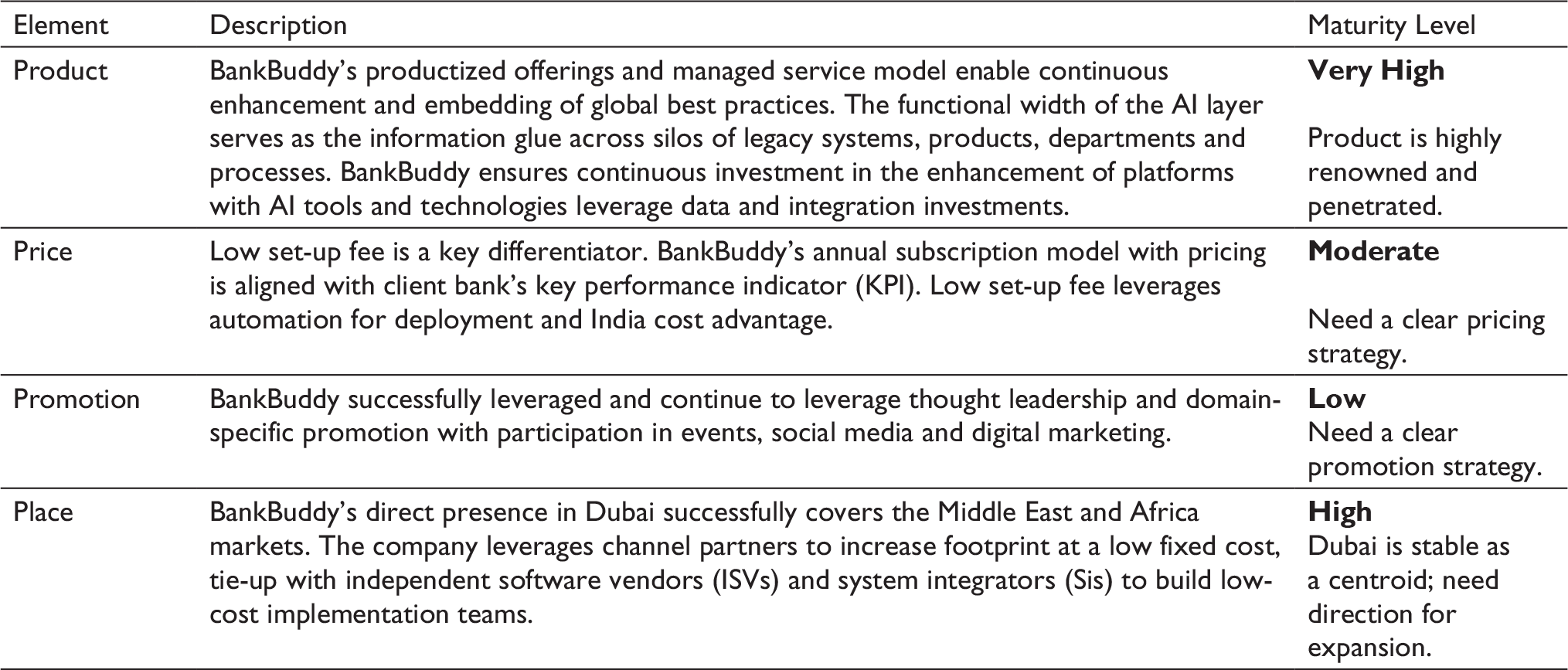

Marketing Roadmap: Marketing Mix

The Macro Economic Environment: Marketspace and the Market Need

Artificial Intelligence

Undisputedly one of the largest technological revolutions of the world, AI is transforming the way businesses have engaged, interacted and supported their customers globally. AI is the technology that helps to simulate and augment the human intelligence component and makes interactions simple, smart, efficient and more purposeful. Increasingly in today’s context, the world’s businesses have stopped looking at AI only as a productivity enhancer. With the emergence of such concepts as ML and enforced enablement of smart machines to continuously learn, adapt and improve on the fundamentals, AI is bringing phenomenal value to the table. Across the world, AI systems have been configured to be the systems that can replicate the preserve of humans to understand and analyse the information they receive, they act based on that understanding and improvise based on the outcomes of the act. This phenomenon of machines and humans preserves the ability to connect and communicate with each other, which has given rise to a clear synergy of far better cumulative outcomes than what both could have achieved individually.

Russell and Norvig (1995) describe an intelligent machine as ‘a flexible, rational agent that perceives its environment and takes actions that maximize its chance of success at some goal’.

Artificial Intelligence in Banks

According to some of the most quoted and referred analyst studies, AI in banking is a US$10 billion market with 48 per cent compound annual grown rate (CAGR). Sixty-three per cent of investments in AI are expected to be in the customer experience arena. Usage of an AI platform can potentially bring down a bank’s operational, maintenance and infrastructure costs by 20–25 per cent. A report by Google Intelligence predicts that roughly 1.9 billion banking customers will be using biometric identification by the end of 2021.

Some of the most prevalent use-cases of AI in the banking industry are observed and outlined by various studies:

Digital transformation/digitalization: AI cuts the lengthy compliance processes of client onboarding, know your customer (KYC) and anti-money laundering (AML) to create a single platform for banking providers and their customers. AI-powered banking core applications driven by data algorithms: The large chunks of unstructured data generated by the global banks and consumers can be used to effectively analyse and create meaningful predictions and projections for clients’ financial needs. Personalization: Enabling personalized financial advisory by making use of the client’s financial preferences. Security: A growing number of banks are using authentication protocols in their financial platforms over and beyond the passwords and up to biometrics and facial recognition. Cybersecurity and fraud prevention: AI and ML concepts are being put to use together to skim through the large amounts of customer data to override the errata that could be otherwise committed by manual interventions. Blockchain: Distributed ledger technology with almost unbreachable limits of data integrity and safety is used to enhance payment processes. Customer support: Enhanced precision and timely response and resolution to customer queries by AI-powered bots has advanced ML and cognitive banking concepts.

FinTech Ecosystem

An analysis by Ernst & Young revealed that the real near-term threat to the banking industry is not by FinTechs but by their competitors that have already started leveraging the FinTech ecosystem. FinTech is expected to work with the banking industry as a hand-in-glove collaborator and not as a competitor.

The FinTech ecosystem consists of banks, financial institutions, FinTech start-ups, innovators, investors, regulatory and governing mechanisms and of course consumers. The segment is currently undergoing tremendous competition from products from native software manufacturers such as Accenture, IBM, Capgemini and Infosys with their indigenous products and other numerous niche FinTech products. The key to win in this segment will be the exclusive ability to address a specific and highly focused business problem as opposed to a core banking platform that serves as a one-stop solution for all banking operations.

Some of the prevalent use cases of FinTechs in the financial service industry:

Blockchain: According to a PwC FinTech report, 77 per cent of the global financial services incumbents are contemplating adopting blockchain as a platform bed for multiple applications.

Example: R3 (Corda; ML powered marketing platforms are bringing the most advanced and predictive marketing capabilities to the marketing industry.

Fitness brand Under Armour uses ML powered segmentation to analyse their userbase and discover complex patterns and correlations in their Record Fitness app. Algorithmic trading: This is trading process automation according to a predefined criterion set by the trader/fund manager that analyses historical market data to enable trade predictions.

Example: Traderobotix ( Customer experience: ML powered data platforms are used to culminate, curate, analyse and predict consumer purchase behaviours.

Amazon, Hyatt and Tumi use ML powered tools to predict and analyse the purchase behaviour of their customers to optimize their in-app/in-store/in-hotel experience.

FinTech and Dubai

It is a common practice for governments across the globe to encourage start-ups by giving them access to growth capital, and these opportunities obviously ease capital challenges. Some of the international hubs have also dedicated funding or fund of funds sources to support FinTechs.

Dubai International Financial Centre

Established in 2004, Dubai International Financial Centre (DIFC) is a major financial hub of the MEASA region. DIFC has independent regulatory and judiciary systems and facilitates in global financial exchange. The Dubai financial district has over 2,000 active registered companies operating across the region with a combined workforce of over 20,000.

More than US$100 million FinTech-focused fund was launched by DIFC in November 2017 to ensure that funding fosters the development of the FinTech sector by boosting start-up investments right from the incubation to growth stages and up to consolidation.

Dubai’s DIFC has also launched its FinTech Hive accelerator programme that focuses on FinTech opportunities in the financial sector of the MEASA region

In another step towards promoting the FinTech ecosystem, Dubai Financial Services Authority (DFSA) launched a regulatory framework for loan- and investment-based crowdfunding platforms.

Aditya explained that despite a large number of financial institutions and FinTechs in the region, the Dubai and MEASA markets are still underserved by FinTech. With their large unbanked population, low financial literacy and diverse customer segments, this gap can be a competitive advantage for a FinTech company that has the adaptability for different customer segments.

The Aspirational Marketspace

FinTech and Europe

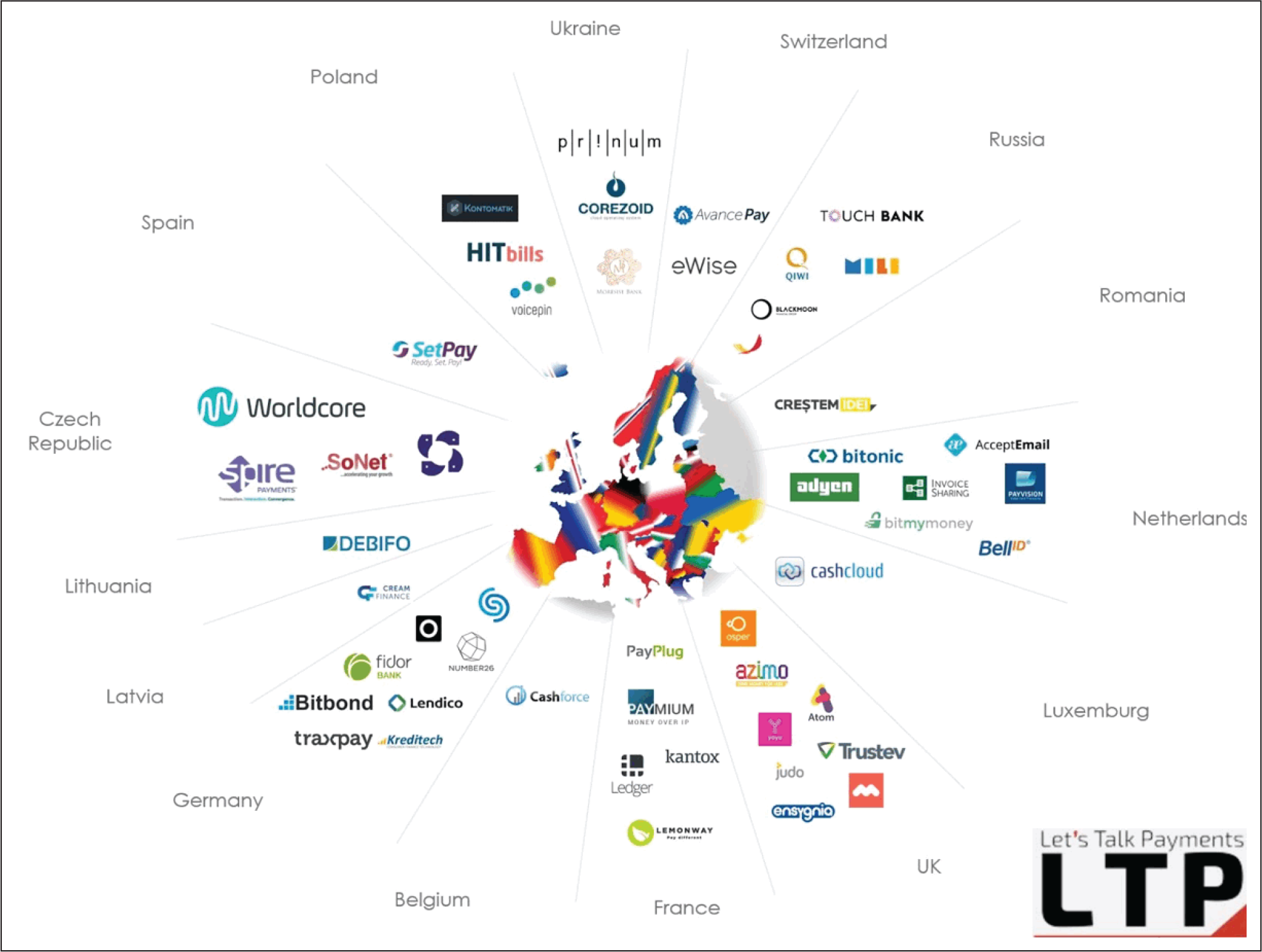

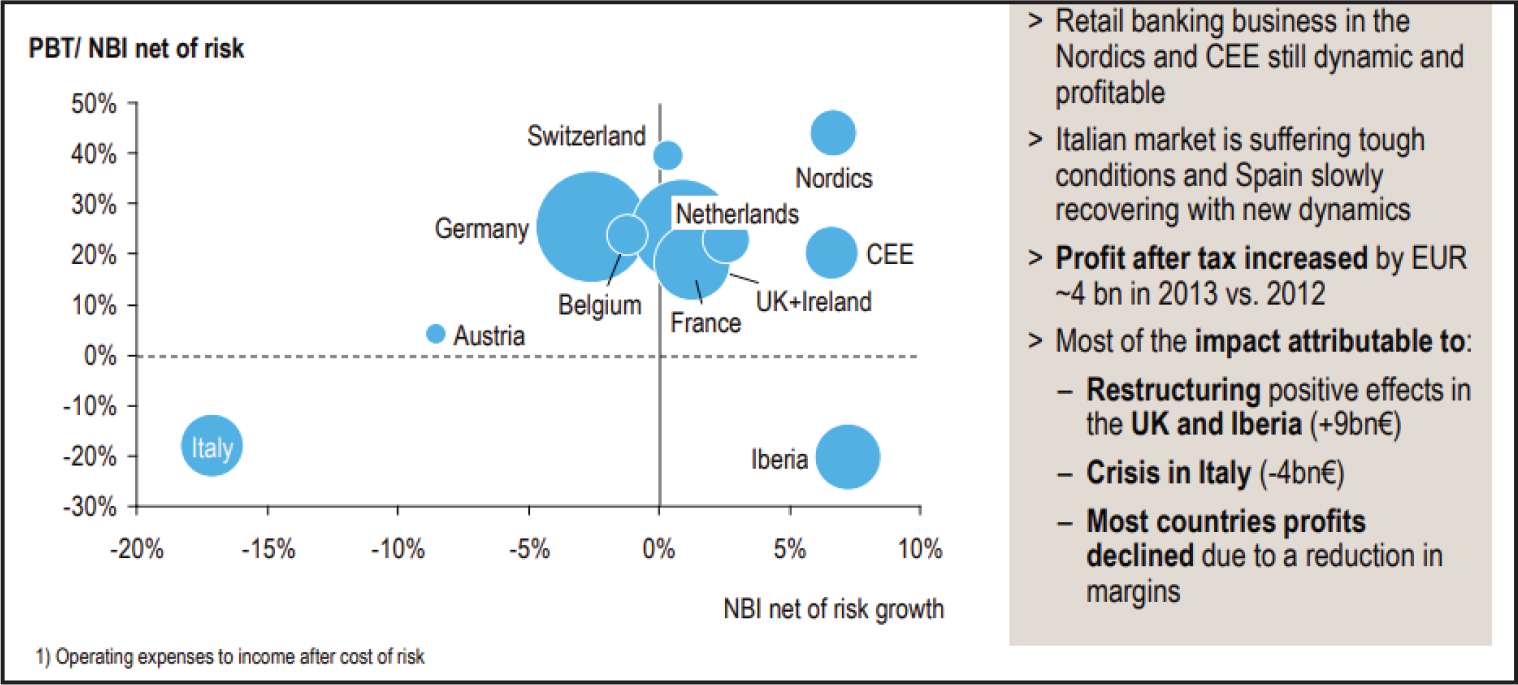

Europe has been the hotbed of FinTech-driven innovation since early 2010s. In some sectors and geographies cited that were reported multiple times by some of the leading publication groups, such as Bloomberg, Huffington Post and TechCrunch, Europe is outshining Silicon Valley in creating opportunities and funds and deal volumes. European FinTechs have created more jobs than California’s Silicon Valley since 2012, as reported by some analysts. Europe has been the world’s burgeoning technology and innovation centre for the FinTech ecosystem (Figure 1). Investments have been increasingly floated into some of the most lucrative areas of the financial services sector, such as personal finance, lending, insurance, regtech, wealth and investment management, mortgage and finance, payments and remittances (Figure 2).

The Great European FinTech Opportunity

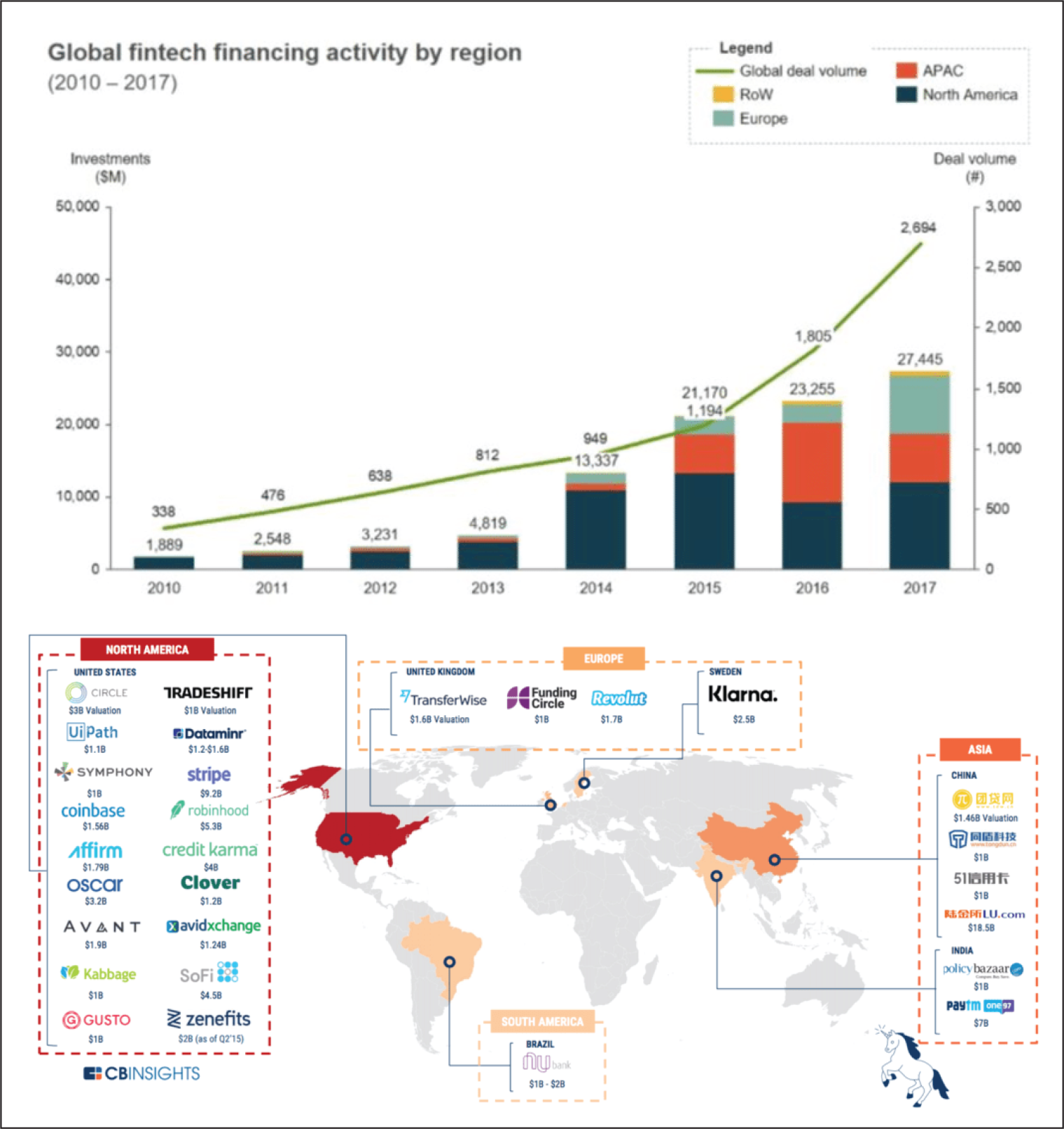

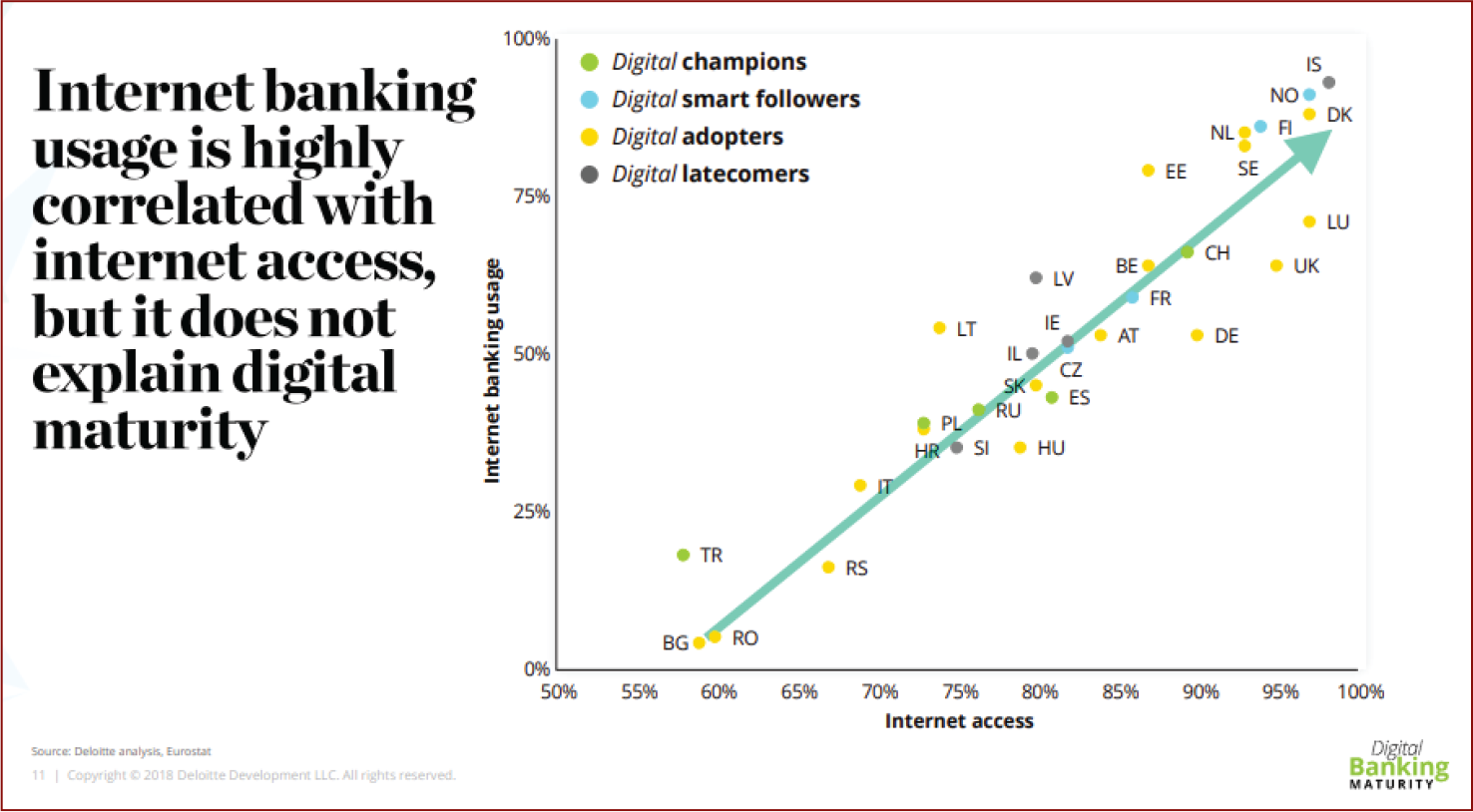

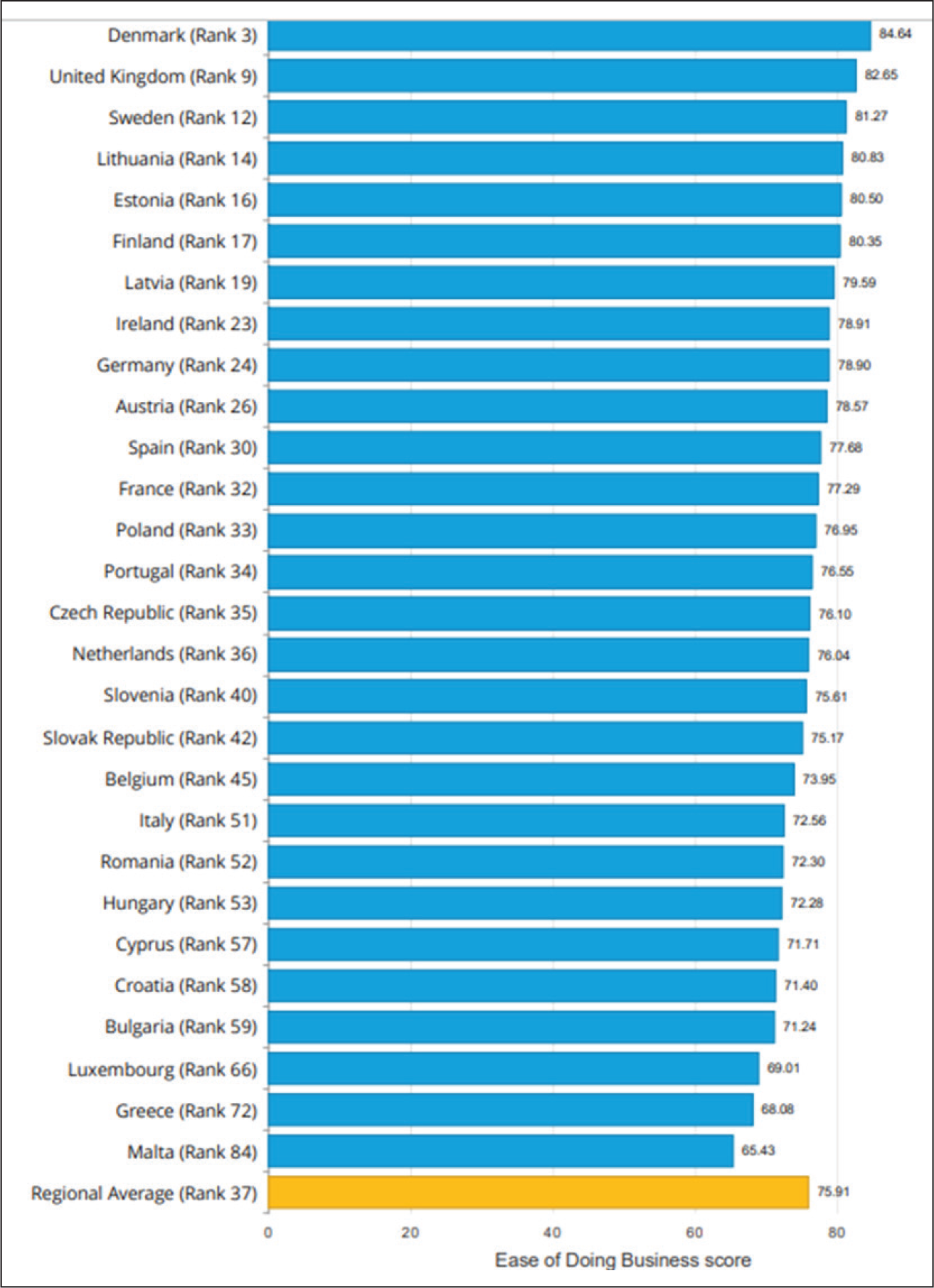

As financial transformation enabled by digital has intensified lately, Europe, home of some of the leading financial institutions globally, has been the battlefield of such transformation attracting huge and multi-folded investments into the FinTech fraternity. More than two dozen countries with unique culture, diversification and spending and regulation patterns are trying to create their own versions of monetary, trade policies and regulations (Figure 3). Consequently, there are umpteen local laws to ensure that financial systems stay compliant to the rules of the land. This scenario has opened enormous opportunities for world FinTech providers to begin operations in Europe and start filling these gaps.

Customer experience and real-time customer experience monitoring have been the disruptive technology trends for European financial institutions for a long time. There is an imperative to develop intuitive mobile apps. Other identified areas of FinTech dominance in the European marketplace are near real-time data processing units for banks and predictive customer analytics platforms for global services providers (Figure 4).

Regulatory Disruptions and the FinTech Opportunity

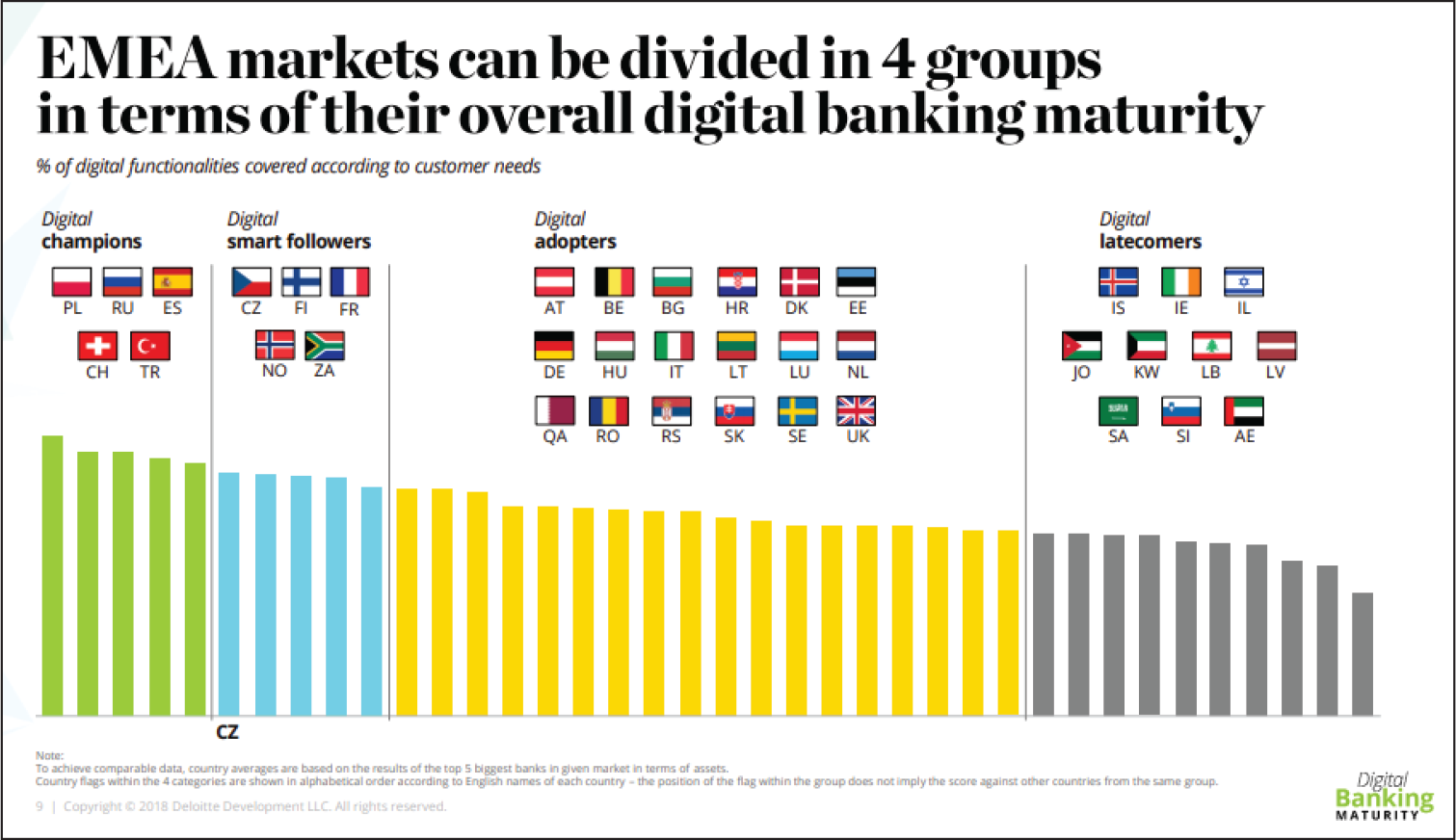

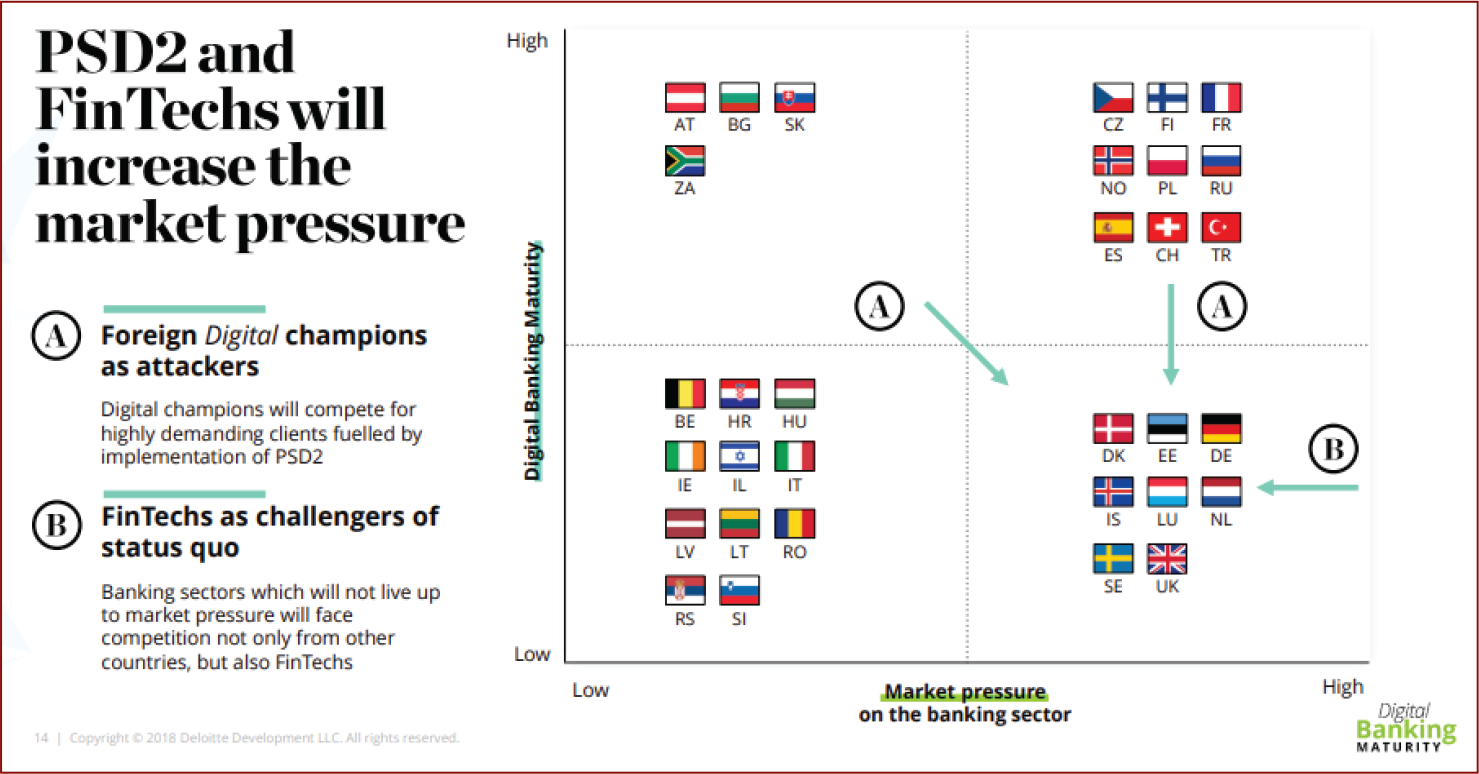

Distinct and pragmatic, Europe’s work culture is fundamentally built on the foundation of a laser-focused educational system. This calls for a strong regulatory ecosystem to standardize the methods of working among these countries (Figure 5). Regulations such as Payment Service Directive (PSD2) and General Data Protection Regulations (GDPR) have raised the complexity levels of the operating mechanism of financial institutions with pan-European operations. This apparently became yet another opportunity for FinTech start-ups to look up to Europe as their playground. The complexity and criticality of EU bound financial technology platforms are yet other areas of opportunity for FinTechs (Figure 7).

What is Expected to Drive FinTech Expansion in the Banking Sector in Europe?

Mobile payments: As increasing numbers of US players such as Apple and Google forayed into mobile payment space, Europe is gearing up to see innovation in this domain.

Crowdfunding and equity crowdfunding: Some of the identified big banks have already collaborated with FinTechs and are exploring ways of financing small- and medium-scale enterprises (SME financing). Due to agile and digitally transformed solutions. FinTechs can turn around the lending process much more quickly, efficiently and effectively than traditional banks.

Alternate financing instruments: As the European Union continuously enforces financial regulations, there is an increasing need for alternate financing instruments like crowdfunding. Some public financial institutions have also invested in these areas giving a boost to the crowd lending marketplace.

Money transfer: With over 28 countries being part of the EU and some of them still accepting their own indigenous currencies in addition to the euro, transferring money between these countries and currencies has been a great challenge, thereby offering an imminent opportunity for FinTech companies across the world to devise flexible solutions (Figure 6).

The Way Forward—Decision Dilemma

As team BankBuddy looked to expand into the European markets, there are a host of unanswered questions about the languages, timing and potential marketing channels. Should we focus our efforts on expanding further in the MEASA or expand into other markets like Western Europe (English speaking)? Should we invest in creating more products or should we diversify into other product lines within this segment? Until now a clustered approach has worked well for BankBuddy in the English-speaking Middle Eastern countries, for example, Dubai as an event cluster for the Middle East. What should be my expansion approach for Europe that is diverse in linguistic parameters? What should be my geo strategy? What is the best possible marketing approach to ensure sustained business growth and a steady stream of qualified leads?

As Aditya glances through the window of his corner office in the DIFC, he contemplates the most appropriate, time-sensitive and executable approach that powers his marketing muscle in the new year that is set to start in the next 120 hours.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.