Abstract

This case study is about Dalmia Cement which is one of the oldest cement companies in India, established in the year 1939. In early 2000s, the company started its journey of aggressive growth under the leadership of young promoter-cum-managing director. The company has been one of the best performing companies in Indias in the last decade and being valued as one of the most valuable scrips of the stock market. The company has grown organically as well as inorganically by meticulously executing strategies of mergers and acquisitions and forging strategic alliances to spur the growth. While the company has a clear growth strategy for the future, it needs to find ways of going forward to ensure it traverses on the same growth path as it has done before.

Introduction

It was an early morning of October 2019, when Mr Dalmia, a young promoter and managing director, of Dalmia Bharat Group was concerned because his company’s strategy to acquire Binani Cement was ruled-out due to a recent Supreme Court order. Also, there were no viable and strategic cement assets that was on sale as of now and the company’s operating margin has shrunk (Livemint, Q2FY19 result). The group must show strong financial performance to keep intact its reputation of being the most valued company in the cement industry. The company’s strategy was to enter into new markets of North India and to reach to 37 million tonne (MT) through the acquisition of Binani Cement. Unfortunately, Binani Cement got acquired by one of its competitors during November 2018. Because of the strong performances in the past, the market expectations from Dalmia is very high, be it its expansion and growth or even financial results. Now, what next for Dalmia Cement? Can the company repeat its growth story of what it did between 2004 and 2017? The key question in the mind of Mr Dalmia was can they do it again?

Dalmia Cement is one of the fastest growing cement companies in India and its growth has been meteoric over the last one decade or more. Having a modest capacity of 1.2 MT in the year 2004, it has risen exponentially to 25 MT by the year 2017. The group is planning to continue this spree and has plans to grow to 37 MT in the next 3 years and has launched an expansion plan of US$79 million (Raghunathan, 2018). The dynamic and charismatic leadership of Mr Puneet Dalmia, the promoter of Dalmia Bharat Group, goes behind this. In one of his interviews to Forbes Asia, he said—‘In a business, it is meritocracy, growth, and performance’. 1 During another interview with Business Standard, he articulated ‘In the current phase of expansion, we are allocating capital to strengthening our position in existing markets like Bihar and entering new markets for growth and diversification’. 2

Dalmia Group has been one of the best performers and known for creating value for all the stakeholders. The group is mopping up distress cement assets under the new insolvency law. It has already acquired Murali Industries in Maharashtra and Kalyanpur Cement in Bihar, but it lost Binani Cement to Kumar Birla’s UltraTech after a prolonged legal battle.

An Overview: Cement Industry

After food and clothing, shelter is an essential requirement of human being. Since its inception, humankind had been pursuing a relentless search for viable building material for securing a stable shelter. Right from the Stone Age to Bronze Age and progressively as different civilizations evolved, the building material which has been used varied from stone to wood, joined through any naturally available materials like volcanic ash, mud and diatomaceous earth to semi-processed materials like lime, burnt clay, etc. The invention of Portland cement as a binding material in the year 1824 by Joseph Aspdin provided a satisfactory solution which humankind was in search of for over two millennia. Now cement has emerged as a leading binding material, and until now, its prominence has not yet been challenged.

With increasing population, particularly in underdeveloped and emerging countries, providing housing is one of the biggest challenges across geographies, including India. The countries are aspiring to go to the next level of growth trajectory and for that development of infrastructure is of utmost importance. Overall, the construction industry is one of the most critical industries not only to cater to the basic needs like housing for the population but also for setting a growth path for nations.

When it comes to construction, the first thing, which comes to our mind, is cement and concrete. Cement is the second largest among all industrial products, which are being produced across the globe. Globally, cement industry is growing at a compound annual growth rate (CAGR) of 8.20 per cent, and its annual consumption stands at 4.2 billion MT per annum. The size of the global cement industry is close to US$750 billion. The rate at which this industry is growing, it is likely to achieve a consumption of 0.74 trillion MT by 2024. Almost half of its consumption comes from China, and next to China is India.

In 2017, India was the second largest cement consuming nation after China. India has an installed capacity of 455 MT as on November 2018, and the cement industry is the fifth largest contributor towards India’s exchequer. 3 India accounts for 8 per cent of global installed capacity. When we look at region-wise contribution within India, South India contributes 33 per cent, North India 22 per cent, eastern India 19 per cent, western India 13 per cent and central part of India 13 per cent (CARE Ratings). While India is the second largest cement consuming nation in the world, but per capita consumption wise it lags far behind. The world’s average per capita consumption of cement was 563 kilogram (kg), with the highest per capita consumption being 2,950 kg and median per capita consumption is 287 kg. The per capita consumption of India is 284 kg as against China which is 2,386 kg. Thus, there is a massive scope of growth in India which is much below the world average as more than eight times lower than China.

Cement industry in India is one of the biggest employers, which employs almost 2,000 people downstream per MT of cement production. With respect to technology and sustainability, India is at par with global standards, be it in terms of production cost per MT, fuel cost per tonne of production or technology of cement production with almost all plants which are ‘dry process’ based. On account of heat consumption and waste heat recovery, the Indian industry is competing with the global West. Because of sustainability, two Indian cement companies Dalmia Cement and Shree Cement are top rankers because of climate preparedness.

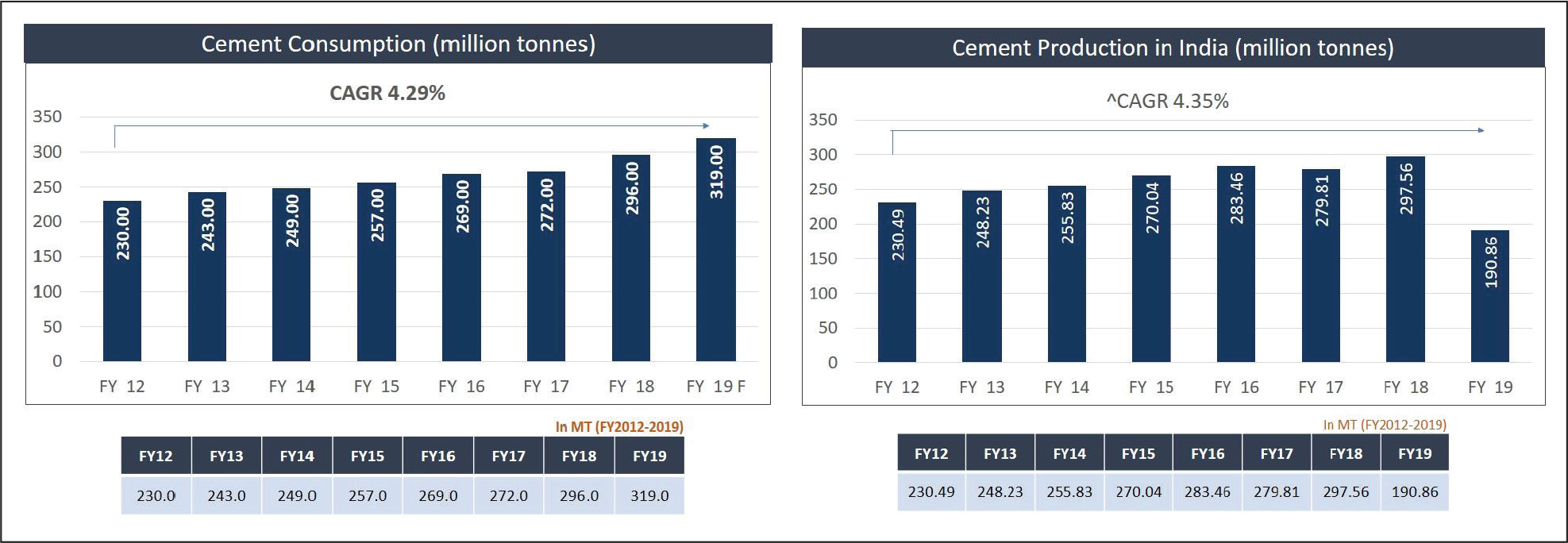

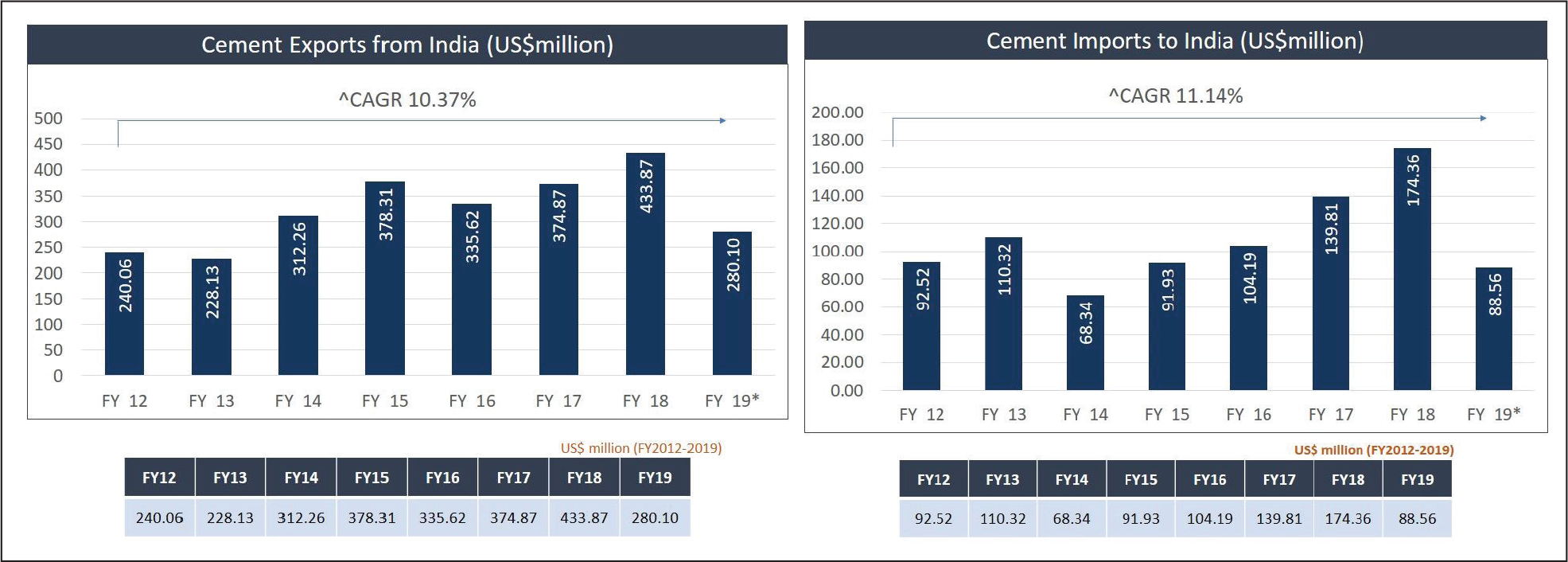

The cement industry has been through challenging times because of varying issues ranging from demonetization, initial hiccups during GST rollout, Real Estate Regulation and Development Act (RERA), ban on sand mining, etc. The industry also got impacted because of restriction on using cost-effective pet coke which was subsequently withdrawn because of the intervention of the Supreme Court of India. Despite all these hiccups, cement industry has come out triumphant. It is now on a growth trajectory, and the outlook looks quite impressive (refer to Figures 1 and 2). For example, cement exports and imports reached US$280.10 million and US$88.56 million, respectively, between April and October 2018. 4

Industry Structural Elements

The industry is cyclical, and demand and supply situation is skewed in favour of the suppliers. Few players dominate the industry, the top 20 players account for 70 per cent of cement production and the top 4 players account for more than 50 per cent of installed capacity. There are more than 550 cement plants across India and the bit plants numbering 210 contributes 410 MT, and rest is being produced by 350 small plants. The barrier to entry is high as installation of cement plant requires high capital expenditure with a long gestation time. Since limestone is one of the primary raw material for cement, even access to limestone quarry is also a significant entry barrier.

This industry is having an intense rivalry and fierce competition. The top five players control close to 50 per cent of the market share. There is a geographical demand–supply mismatch which further triggers the competition. Almost all players are now heavily investing in creating a strong brand and diverse product portfolio. Product innovation has also taken place to create differentiation and to come out of the commodity trap. It is mostly the government that supplies coal and power to cement companies. Now cement companies have started setting up their captive plants, but still, the dependence on government remains very high.

From a buyer’s standpoint, primarily, there are two segments trade and non-trade. While in trade cement is sold through channel partners, in non-trade it is sold directly to customers. Usually, prices and realizations are better in case of channel sales and lower in case of non-trade sales. The reach to customers and markets depends upon the reach and depth of channel network of companies and in a way companies use this as a balancing mechanism to limit the bargaining power of channel partners. From a substitute standpoint, though steel, glass and other prefabricated are gaining a little momentum still there is no viable substitute for cement in the foreseeable future.

Demand Drivers

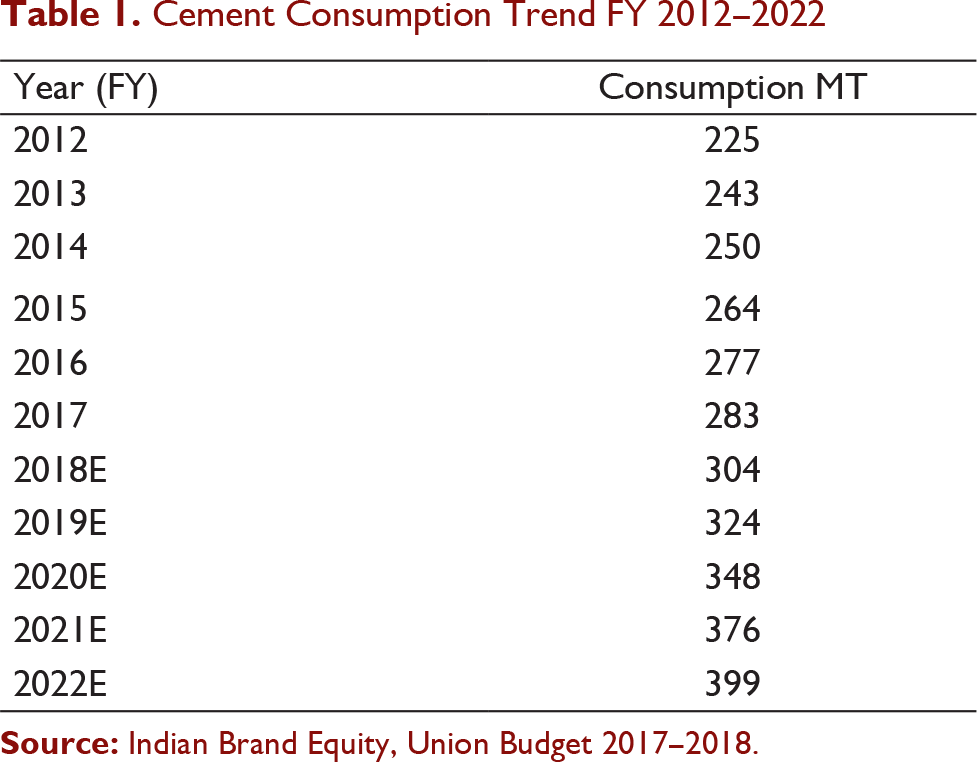

Cement Consumption Trend FY 2012–2022

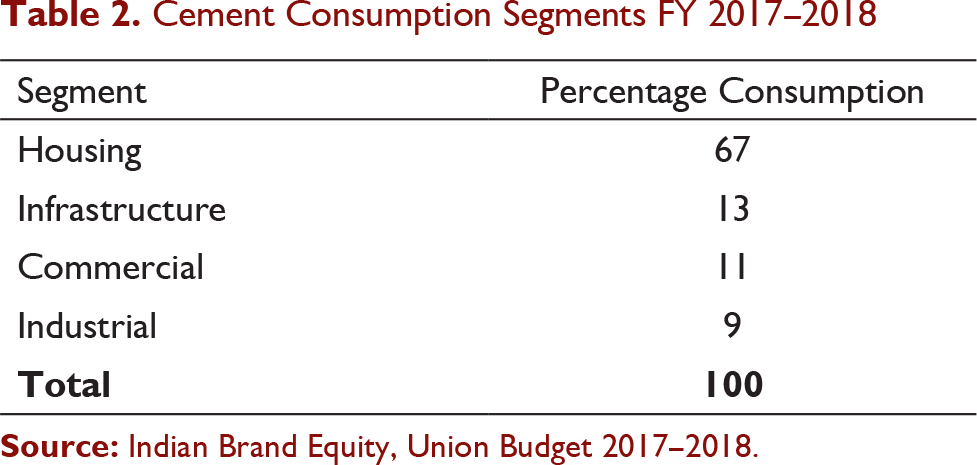

Cement Consumption Segments FY 2017–2018

The central government is pushing ‘housing for all’ by 2022 which is going to drive the growth of the cement industry. The government plans to develop 500 cities having a population of more than 100,000. Infrastructure is growing at the fastest pace, thanks to the focus on infrastructures like highway construction, airports, creation of economic zones, seaports and dedicated freight corridors. The government also has a plan to develop 100 smart cities.

Cost Drivers

The major cost drivers in the cement industry consists of raw material cost 20 per cent, power and fuel cost 23.8 per cent, freight cost 25.7 per cent and manufacturing cost 30.5 per cent. There are cement companies that have their captive power plant and waste heat recovery system which gives them an edge over others as far as power cost is concerned. As far as fuel is concerned, alternate fuel and non-fossil fuel, which have lower cost, give a cost advantage to those companies who have infrastructure and availability to use alternate and non-fossil fuel. Since logistics cost is more than 25 per cent, those companies who have efficient supply chain management and a good network of plants tend to benefit out of this situation.

Distribution Value Chain

Typically cement reaches to end consumer directly through dealers or retailers of dealers appointed by the manufacturers. In case of big consumers such as contractors, builders, developers, institutions, it is either being supplied directly from manufacturers or at times through dealers. The distribution generally happens through one of the following routes:

from manufacturer to warehouse of company to company appointed dealer to retailer to end consumer, from manufacturer to the warehouse to retailer to the end consumer, from manufacture to retailer to end consumer and from manufacturer to prominent contractors/builders/developer and at times from warehouse.

Installed Capacity

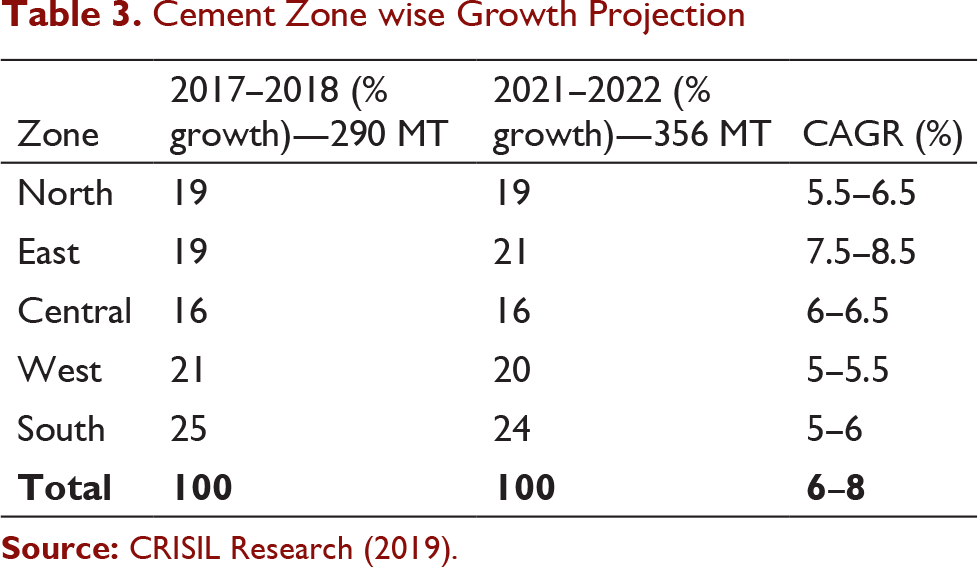

India is primarily being divided into five geographies as far as cement installed capacity is concerned. These divisions are South, North, East, West and Central India (see Table 3). Since limestone is the primary constituent of cement, cement plants are located in geographies where there is availability of limestone. The installed capacity in South India is the highest which is 33 per cent of total installed capacity of India, North India 22 per cent, East India 19 per cent, West 13 per cent and central part of India 13 per cent (CARE Ratings). The total estimated installed capacity in India is 455 MT per annum (CRISIL Research, 2019).

Regional Demand–Supply Dynamics

Interestingly, the growth pattern in these geographies is not as per the installed capacity; hence, there is a mismatch between demand and supply (CRISIL Research, 2019). East and North India is growing at a higher rate than other geographies. On an overall basis, there is a mismatch between demand and supply of cement which results in reduced capacity utilization of 70 per cent at India level. The capacity utilization in East and North India is estimated to be more than 90 per cent (Edelweiss Research). The capacity utilization in South India is the least at 57 per cent.

Cement Players Venturing into Ready Mix Concrete Business

The construction industry worldwide is evolving. While in the developed countries, it is already at an advanced level, in developing countries like India it is evolving. The construction practices are changing aimed at faster and safer construction with a high level of mechanization. Since concrete is an essential requirement of any construction, it is also undergoing a change keeping pace with changes in the construction practices. The mechanized concrete (ready mix concrete [RMC]) is an answer to not only the requirement of faster and safer construction but also various construction site issues. Statutory and regulatory norms are becoming stringent, forcing construction companies and contractors to find ways to reduce pollution and also conserve water. All these external environmental changes have spurred the growth of mechanized RMC in India. The usage of RMC in India is becoming popular, and it is expected to be higher than the rate of cement growth. 5

The penetration of RMC in India is only at 15 per cent whereas in developed countries it is more than 90 per cent. As per an estimate, in India out of total cement consumption, 60 per cent is being used for concreting purpose. Out of this 60 per cent, only 15 per cent is being catered through mechanized RMC plants and the rest is manual site mix where there is no control on quality, and there are issues related to pollution as well. With the kind of mechanization happening in the construction industry, it is challenging to cater to the concrete requirement through manual site mix. Also, there are issues of unavailability of labourers. Since there is a strong push on infrastructure and housing, there is a requirement of mass concrete which can only be catered through mechanized RMC plants.

As mentioned above, there is a significant push from the Indian government for infrastructure development and housing. This push is not only improving prospects for cement companies but also for RMC plants. Since the utilization of capacity is still hovering around 70 per cent, almost all big players are venturing into RMC business intending to be a part of the growth story not only with their cement proposition but also RMC offering which is a complete solution for construction companies. This trend of vertical integration is likely to go up as this also provides cement companies to use their idle capacity, typically with 1 MT of cement 3 cubic meter of RMC can be produced. The recent entrant in the RMC business is Ambuja Cement. The cement companies have started going for a ‘no Capex model’ wherein the plant is being set up by a third party for a monthly consideration and rest other activities including manufacturing, marketing and selling lies with the RMC companies.

Other Related Products

In recent past, cement companies have also started to venture into those products which are related with cement such as dry plaster, aerated autoclaved concrete blocks (AAC blocks), concrete hollow and solid blocks. Some of the companies have even come up with fly ash bricks which is environment friendly. These companies are further thinking big about going for ‘green building’ solution. All these opportunities are being used not only to spur consistent growth but also being ready for the future as the construction industry is evolving fast.

History of Dalmia Group

Cement Zone wise Growth Projection

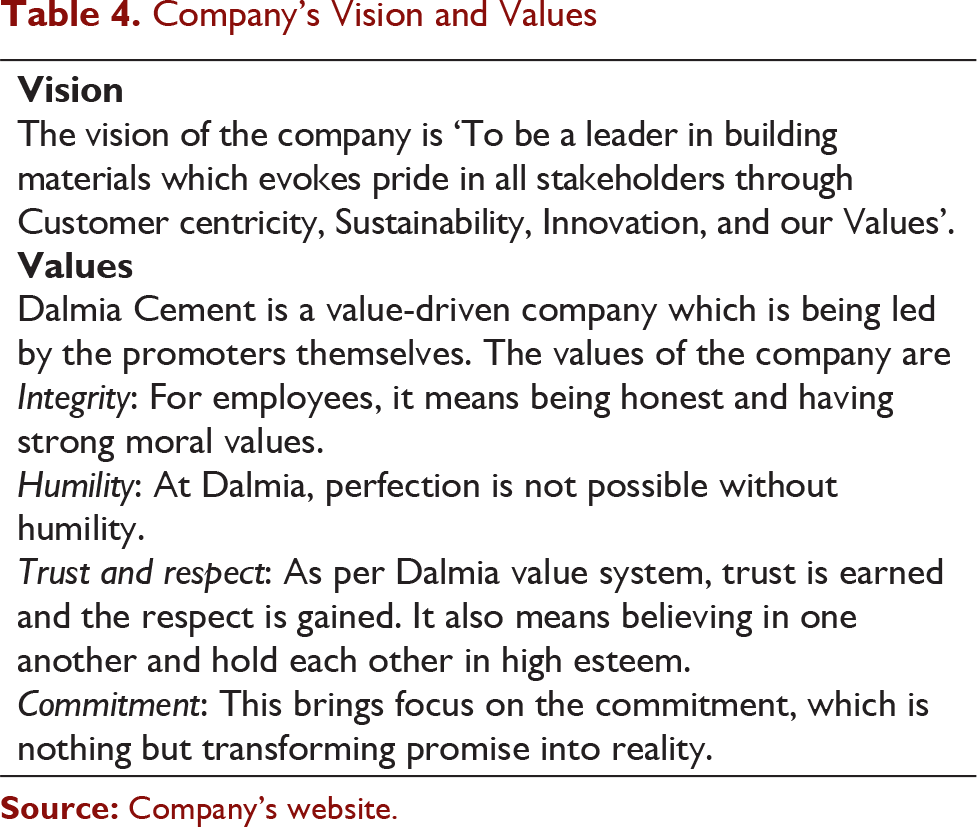

Company’s Vision and Values

Apart from cement, Dalmia Group has interest in sugar, magnesite, refractory, travel agency and electronic operations spread across the country. Dalmia has been a pioneer in introducing new technologies which are now being used by others. Refer to Table 4 for company’s vision and values. The company’s journey can be observed in three distinct phases. 6

First Phase

Dalmia Cement started its journey in the year 1939 with the establishment of 250 Tonne per day semi-dry process kiln for cement manufacturing at Dalmiyapuram in Tamil Nadu, India. Jaidayal Dalmia, the promoter, further expanded its capacity by adding 500 Tonne per day wet kiln in the year 1949. Dalmia ventured into East India and established a cement plant at Rajgangpur in Odisha where super grade cement was manufactured for supplying the same to Hirakud Dam in Odisha. This venture was known as Odisha Cement Ltd (OCL). In the year 1952, OCL sets up its refractory plant. In the year 1956, Dalmia Magnesite Corporation was set at Salem in Tamil Nadu in conjunction with OCL, Dalmia Cement and Magnesite Corporation Ltd of India.

Second Phase

In the year 1973, OCL developed monoblock concrete sleepers for Indian Railways, and they were one of the pioneers in doing so. Further improving its operational efficiency, the vertical raw mill was established in all Dalmia Cement plants. The Dalmia Cement once again came with a new product and developed oil well cement (OWC) in the year 1984. An iconic brand called ‘Vajram’, a Portland Pozzolana Cement (PPC) was launched by Dalmia Cement for South Indian market in the year 2000. In order to reduce its power cost, Dalmia Cement set up 27 MW captive power plant in the year 2004 at its Dalmiyapuram plant in Tamil Nadu.

Third Phase

In the year 2008, Dalmia Cement increases its capacity from 4 MT per annum to 9 MT per annum by adding two integrated cement plants, one in Tamil Nadu at Ariyalur and another at Kadappa in Andhra Pradesh. In the year 2014, Dalmia Cement acquired Jaypee Cement Plant in Bokaro and increased its capacity to 24 MT per annum. This acquisition gave Dalmia Cement a strong foothold in East India also. Another integrated plant was set up in the year 2015 at Belagaum in Karnataka to further strengthen its position in South Indian markets. In the same year, Dalmia Cement enhanced its stake in OCL from 48 per cent to 74.6 per cent through inter-se promoter transfer. 7 In the year 2016 two key amalgamations took place. First, the announcement of amalgamation of OCL India Limited and Dalmia Cement East Limited 'Bokaro' with Odisha Cement Limited (renamed as OCL India Limited). Second, the amalgamation of Adhunik Cement (of North East) with Dalmia Cement (Bharat) Limited.” This phase was the growth phase for Dalmia Cement which took them to 25 MT capacity and earned them a reputation of fastest growing cement company in India. The capacity came about by organic and inorganic growth.

Business Model: Key Elements

Customer Segment

Dalmia sells cement products in almost all states of India. The cement is being sold through two verticals: the first one is through its trade vertical wherein the cement is sold through company appointed channel partners called dealers and their sub-dealers. The second vertical is non-trade or institutional sales vertical wherein the cement is supplied directly to big consumers such as contractors, big construction companies and institutional buyers. The sales support for the institutional segment, at times, is being given by overriding commission (ORC) agents. The institutional segment is further divided into sub-segments like infrastructure segment, government and institutions, processing units, contractors, RMC segment and builder and developer. Dalmia has been giving priority to trade segment where the margins are better as compared to institutional sales, and it has rolled out several products to cater to the requirement of end user, which is being served through trade vertical. Dalmia has one of the best networks in the industry to push the volume to end users. In the institutional segment also, Dalmia is one of the preferred brands for its quality product and services.

Products and Distribution

Dalmia Cement has a sound product portfolio. It has in its portfolio, Dalmia PPC, Dalmia OPC 43 grade, Dalmia OPC 53 grade, Dalmia SRPC, for specific sulphate resistance usage, Dalmia DSP, a premium product for home builders, Dalmia PSC and Konark composite cement. It has some unique special application products in its portfolio such as Dalmia Airstrip Cement, Dalmia OWC and Dalmia Railway Sleeper Cement which gave them an edge over their competitors. Dalmia is known for its world class quality products suiting to different requirements. Dalmia Cement supplies its product to its dealer and institutional customers either directly from its manufacturing unit or through its warehouses. It is always preferable to supply directly from plants to save on logistics cost. Dalmia is one of the most efficient companies when it comes to logistics cost. The mode of supply is through both road and rail.

Plant Locations and Capacity

Dalmia Cement has its plant at 11 different locations across South India, East India and Northeast India. It has a capacity of 12.1 MT in South, 9.3 MT in East and 3.6 MT in Northeast. In all these three geographies, Dalmia is among the top three players in market share, capacity-wise.

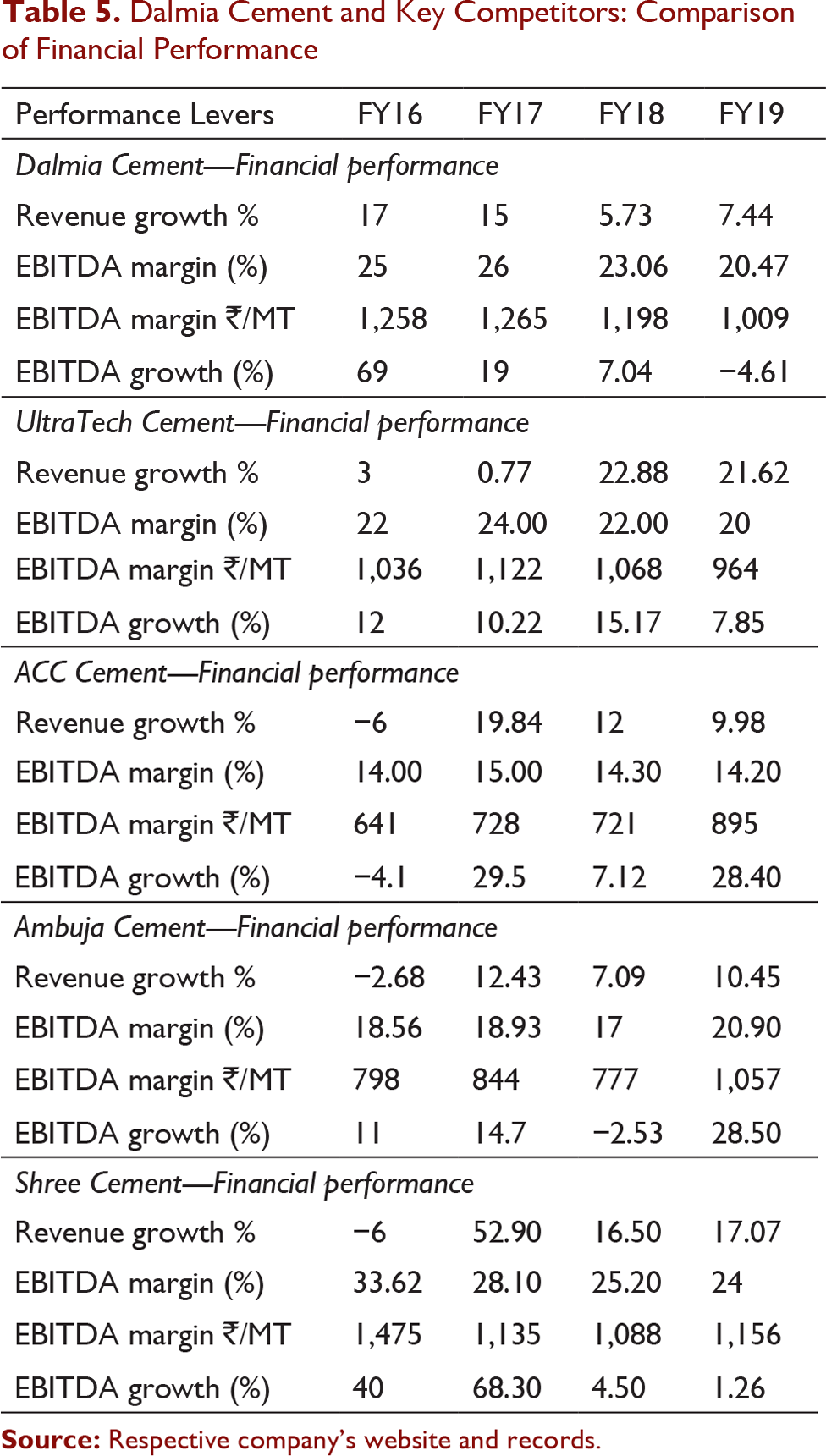

Financial Performance

Dalmia Cement has been one of the best cement companies in India in the last decade. It has not only grown exponentially but also has been one of the best-performing companies financially. Based on past performances, the stakeholders have very high expectations from them. They are one of the most profitable cement companies in India with sustainable high margin backed up with strong financials. The challenge for them is how are they going to maintain this strong performance going forward.

Research and Innovation

Dalmia Cement Research Centre (DCRC): Customers centricity being part of the value cement, DCRC was set up by Dalmia to support customer’s construction site issues. This centre is not only involved in doing research to ease out construction site issues related to concrete and cement but also engaged in doing research for finding ways to come out with solutions which exceed customer’s requirement. For example, TechMobile is an extension of DCRC which does testing of the raw material of concrete at customer sites and help them in choosing the right material for their construction. This channel also educates customers and site people with respect to quality of raw material and best construction practices. The mobile DCRC are on wheels (mobile vans) and provide on-site testing activities.

Competitive Advantage 8

Dalmia Cement has a good network of plants in East, Northeast and South India, which gives them an advantage over others being able to serve their customers better at an optimum logistics cost. The Dalmia brand commands good brand equity in these markets. Dalmia Cement is a pioneer in manufacturing monoblock railway sleepers and is one of the preferred suppliers of the same. Dalmia Cement produces OWC confirming to the world class standard and are preferred supplier in that segment. They also produce sulphate resistant pozzolana cement (SRPC) being used for specific usage at construction sites. Dalmia Cement also has a range of products which includes Dalmia DSP, which caters to premium segment requirements. Dalmia is also one of the most significant players in the composite cement segment. Dalmia Cement is the least carbon footprint company in the cement industry worldwide and is leading cement industry in various national and international forums to promote sustainability in the cement industry.

Corporate Social Responsibility and Sustainability

Dalmia’s corporate social responsibility (CSR) mission is ‘To facilitate the stakeholders hasten their social, economic and environmental progress through effective management of human and natural capital’. Dalmia Bharat foundation is engaged in a plethora of activities supporting the CSR mission of the company. Dalmia Cement is known to be the least carbon footprint company worldwide in the cement sector. As a virtue, the company had continuously focused on sustainability-related concerns and have represented the industry on multiple occasions. Dalmia is a member of Cement Sustainability Initiative (CSI), World Business Council for Sustainable Development (WBCSD), International Finance Corporation (IFC), TERI Council for Business Sustainability (CBS), etc. 9

The Competition

Dalmia Cement and Key Competitors: Comparison of Financial Performance

UltraTech Cement

UltraTech Cement is the largest cement player in India with a capacity of 102.75 MT per annum. 10 They are the fifth largest cement producer in the world. They have 20 integrated plants, 1 clinkerization unit, 26 grinding units and 7 bulk terminals. They are also the largest manufacturer of white cement with one white cement plant and two wall care putty plant and largest RMC producer in India with more than 100 RMC plants. UltraTech Cement is also the largest exporter of cement and clinker in the countries of the Indian Ocean, Africa, Europe and the Middle East. They command a market share of more than 21 per cent as per installed capacity. UltraTech has a presence in all the geographies of India and has a balanced capacity portfolio across India. 11

UltraTech Cement provides a range of products and solutions to its customer. While cement (grey cement), white cement and RMC being largest of their building material portfolio, UltraTech does supply products like AAC block and light weight blocks. They also supply dry mix products like waterproofing, grouting and plastering solutions. UltraTech Cement claims to provide ‘one-stop-shop’ for every primary construction need. The retail format version of ‘UltraTech Building Solutions’ provides a varied range of construction products to end consumer under one roof. Within cement (grey cement) also, they have different products under the category of ordinary Portland cement (OPC), PPC, Portland slag cement (PSC) and composite cement. As per Edelweiss, UltraTech is going to be the prime beneficiary of the rising trend in capacity utilization. As per them ‘endeavour to increase market share through acquisitions and organic growth is heartening and the recent acquisition will fortify its leadership position’ (Edelweiss Research).

ACC Cement

ACC is the second-largest cement manufacturer in India with an installed capacity of 33.5 MT per annum (Edelweiss Research). ACC is present across geography (all five zones) and is part of Switzerland-based LafargeHolcim group which has a 54.5 per cent stake in the company through Ambuja Cement. LafargeHolcim Group is the world leader in building material industry. 12 ACC has 17 cement plants and 75 RMC plant spread across geography. It is one of the oldest cement companies in India and got established in the year 1936. ACC was involved in some of the iconic projects like Bhakra Nangal Dam in the year 1960. 13

The key product strategy of ACC is innovative and differentiated products and solutions by anticipating customer’s requirement. They have the gold range and silver range of cement products suiting to different construction requirements. ACC is also one of the leaders in RMC business having more than 75 plants, and its plants are spread across the geography. The company has several value-added products in its portfolio of RMC solutions. The growth of RMC business of ACC has been a phenomenon. The EBITDA has grown from 341.2 million in 2014 to 1338.3 million in 2018, a growth of 292 per cent. 14 This shows the potential and power of the RMC business. For the company, sustainability is a crucial aspect of their business strategy and is committed to sustainable development plan 2030. As ACC is present across geographies, it will be benefited out of expected recovery in cement demand, improved capacity utilization, high operating leverage and synergy with Ambuja Cement as they are part of the same group (Edelweiss Research).

Ambuja Cement

Ambuja Cement is amongst top five players in India with an installed capacity of 29.65 MT per annum. 15 As per the installed capacity, they have a market share of more than 6 per cent and has its presence across geographies except for South India. Ambuja Cement is part of LafargeHolcim with 50.6 per cent stake (Edelweiss Research).

Ambuja Cement is known for hassle-free home building solutions. Its products are tailor-made for Indian climatic conditions. Ambuja Cement was a pioneer in transporting cement through waterways by establishing a captive port with four terminals which gave them an edge over others as far as cost-effective transportation is concerned. Ambuja also has an excellent portfolio of products like Ambuja Plus Roof Special, Ambuja Plus Cool Walls and Ambuja Compocem. All these products are meant to fulfil the customer’s requirement and also reduce carbon footprints. 16

Shree Cement

Shree Cement is the third-largest player in India with a capacity of close to 37.9 MT per annum and has 10 plants across geographies. The company is present in all five geographies with overwhelming presence in North and East India and marginal presence in South and West India. Shree Cement also has a power production capacity of 646 MW which gives them edge over others when it comes power cost, which is quite substantial in cement production. They have a distinction of largest waste heat recovery-based power generation capacity (WHRP) globally in cement industry except for China. 17

The company is being managed by promoters Mr B. G. Bangur, Chairman, and Mr H. M. Bangur, Managing Director. The promoters hold a controlling stake of 64.79 per cent (Edelweiss). Shree Cement believes in ‘on-time delivery’ in order to keep customers satisfied and happy. They claim to have the capability to deliver small requirement customers which is as low as 20 MT to large customers having a requirement as high as 5,000 tonnes. 18 For this, they are continuously engaged with all the stakeholders to grow their truck fleet.

The company always has a quest of advertising their brands in a cost-effective manner, and one of the ways they adopted was painting trucks. Shree cement does have a product portfolio which is known as ROOF ON, Rockstrong Cement, Bangur Power, Shree Jung Rodhak Cement and Bangur Cement. Shree Cement is an investor’s delight given their credential of continuous gain in market share, sharp focus on cost-driving margins superior to peers and sustainable high RoEs of over 17 per cent.

The Current Status

With its current capacity, Dalmia is the fourth largest player in the Indian cement industry, thanks to its exponential growth from 2004 to 2017. This was a combination of organic and inorganic growth. With recent addition of Kalyanpur Cement in Bihar and Murali Agro in Maharashtra along with Binani Cement acquisition which it is vying for, its capacity would become 40 MT, and it will become the third-largest cement company in India. Dalmia Cement, which is not present in North markets, Binani Cement acquisition would give them access to a non-represented and profitable market. This will also ensure their commitment to growth and performance.

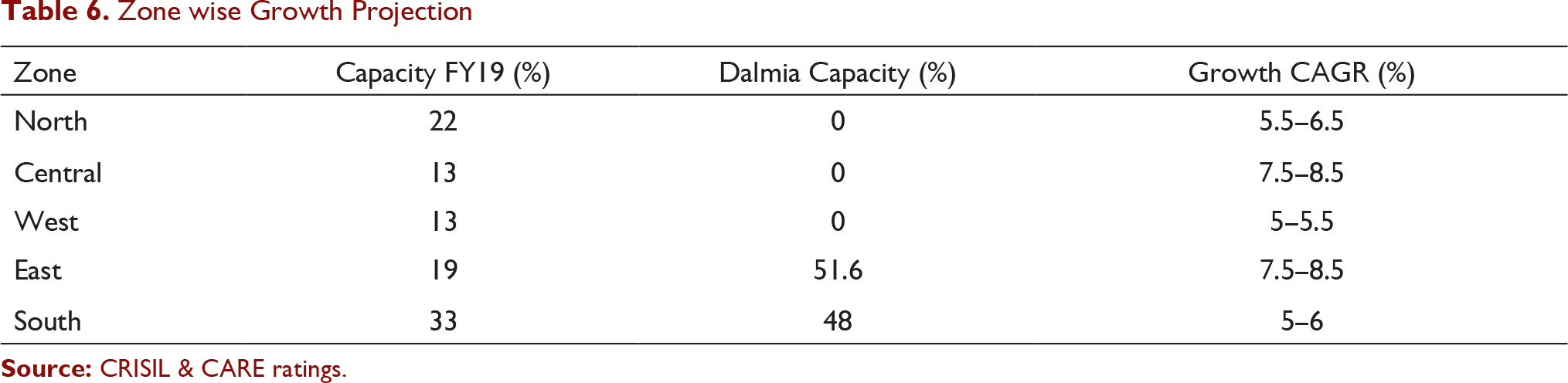

Zone wise Growth Projection

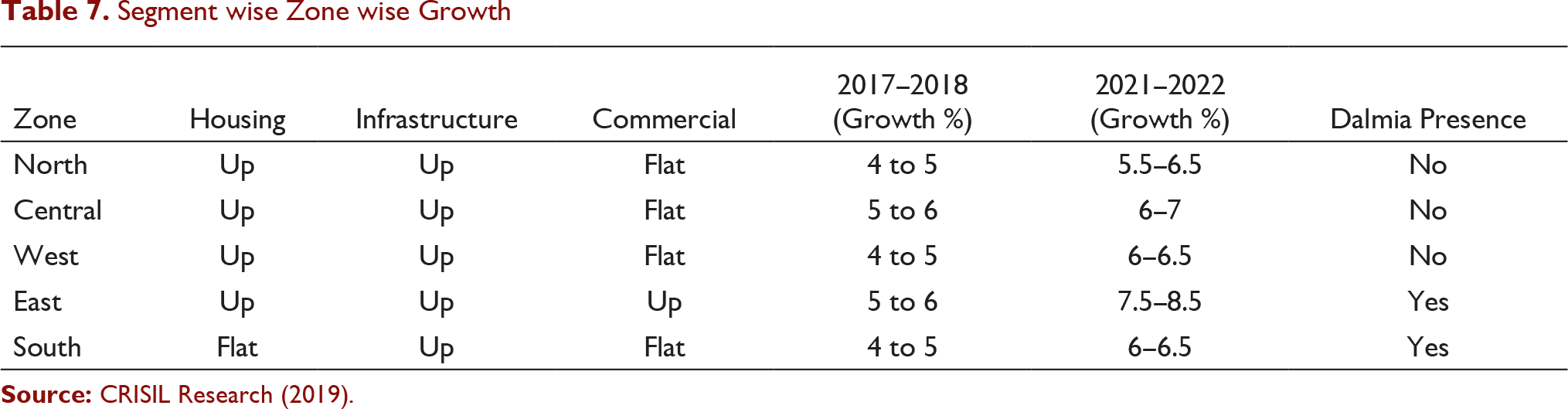

Segment wise Zone wise Growth

As per a leading business daily, the expansion plan of Dalmia hinges on the outcome of Binani Cement acquisition. If it goes another way, then there could be some issues as there are no cement assets up for sale after Binani Cements. Also, Dalmia own assets are currently at 68 per cent utilization level as against industry average of 73 per cent (Pillay, 2018). Like all cement companies, Dalmia is also bullish about India infrastructure story. The capacity utilization in South India is the lowest among all zones (refer Tables 6 and 7).

The Way Forward

At last, the tug of war between Dalmia Cement and UltraTech for Binani Cement Limited ended on 20 November 2018. As per the apex court order, Binani Cement became the wholly owned subsidiary of UltraTech Cement (Jethmalani, 2018). The Indian cement industry is fierce in competition, and players are finding ways to outpace others. The way it looks, the BIG FOUR will continue to compete with each other in order to become darling of the stock market. As per Dalmia, ‘next 5-7 years, we will continue to balance the asset portfolio in existing and new markets to achieve consolidation, growth and diversification, while maintaining a strong balance sheet and managing risk carefully’. The key question for Mr Dalmia was how to repeat the company’s success story given the recent development, existing industry structure and competition.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.