Abstract

This South African case study controls for the fiscal side of the economy using government borrowing as a potential accelerator of asymmetry in a monetary function that follows Taylor’s rule. Through the linear and non-linear ARDL framework, we find significant asymmetry effects of monetary policy on output and inflation, respectively. We also find government borrowing as an important underlying source of asymmetries in the response of macroeconomic fundamentals to monetary policy shocks in South Africa. Thus, we recommend that monetary authorities consider not only the effectiveness or otherwise of monetary policy instruments to affect the target policy goals, but also the fact that not all the target variables react in a similar way to expansionary and contractionary monetary policy shocks.

Introduction

The objective of monetary policy may differ from one country to the other. What is rather indisputable is the fact that the objective invariably includes price stability, external balance and sustainability of output growth. It is common knowledge that the central banks in most countries are traditionally responsible for the conduct of monetary policy for the actualization of these goals. From the inception of its establishment, the South African Reserve Bank (SARB) was tasked with the responsibility of implementing monetary policy in accordance with the macroeconomic policy objectives of the South African government. The SARB, for example, has a mandate to achieve and maintain price stability in the interest of sustainable and balanced economic development and growth. There is no gainsaying that monetary policy has been proven as crucial for explaining output growth and inflation rate both in the short and long run. It is, however, debatable whether the effects of monetary policy on these critical macroeconomic fundamentals are asymmetric. In his simple monetary policy reaction function, Taylor (1993) assumes the responsibility of the monetary authorities to be symmetric such that, positive and negative inflation and output gaps are met with equally weighted policy responses. However, there has been increasing evidence challenging the view that central banks use simple linear interest rules (see, e.g., Cukierman & Muscatelli, 2008; Gerlach & Schnabel, 2000).

Since the same size of monetary contractions and expansions could result in different magnitudes of policy effects, it might be, therefore, erroneous to assume that the policy goal variables such as output growth and inflation would respond symmetrically to monetary shocks. Thus, there has been growing efforts in the literature to understand the asymmetry effects of monetary policy on the target variables (see Aksoy et al., 2002; De Grauwe & Senegas, 2006; De Grauwe, 2000; Fang et al., 2018; Georgiadis, 2015; Gogas et al., 2018; Gros & Hefeker, 2002; Kilinc & Tunc, 2017; Lee & Yoon, 2016; Nolan, 2002; Ravn, 2014; Karras, 2013; Santoro et al., 2014; Scot, 2016; Weise, 1999; Zakri & Malik, 2013; Zhu & Chen, 2017) Nonetheless, the vastness of literature on the asymmetry effects of monetary policy, the empirical findings have been hugely mixed with little or no consensus on the extent to which asymmetries matter for the effectiveness of the monetary policy. Such mixed results might be due to the problem of model misspecifications, foremost by the omission of some potential as the underlying source of asymmetries in monetary policy.

Both academics and policymakers agree that monetary policy is made in an environment of substantial uncertainty regarding the current and future economic conditions as well as the functioning of the economy (see Montes, 2010). This, notwithstanding, most of the previous on asymmetry effects of monetary policy has continued to ignore the potential of such exogenous conditions as the underlying source asymmetries in monetary policy. The closer to the present article is the study by De Grauwe and Senegas (2006). Motivated by the probable presence of heterogeneity in the national transmission channels of monetary policy, De Grauwe and Senegas (2006) use the case of European Monetary Union (EMU) to show that uncertainty matters in the asymmetry effects of monetary policy. However, it must be pointed out that these authors mainly focused on the case of developed economies, where monetary authorities are highly independent of political pressure. Thus, while acknowledging the contribution of De Grauwe and Senegas (2006) on the role of uncertainty in the asymmetry effects of monetary policy, it might be erroneous to generalize their findings for both developed and developing economies.

Unlike the previous studies, this article is focusing on an environment, where monetary authorities are highly vulnerable to government influence. To this end, we describe uncertainty from the viewpoint of the vulnerability of decision-making process such as the central bank’s vulnerability to political pressure (government influence). More so, the majority of the extant studies have used a variety of modelling approaches to analyse the asymmetry. These approaches which include reduced-form equations, small- and large-scale structural models and standard or structural vector autoregression models (VARs) have though proved to be popular particularly in the industrial countries. It has been, however, recognized that standard applications of some of these tools are not well suited for capturing the nonlinear responses—in the form of either asymmetric responses that theoretical models suggest may be pervasive. To bridge this gap, this article is exploring a nonlinear autoregressive distribution lag (NARDL) of Pesaran et al. (1999) to determine if output growth and inflation rates respond asymmetrically to monetary policy shocks in South Africa.

Thus, the contribution of this study is mainly twofold: first, we expand the conventional Taylor’s rule to include government influence in the hypothesis that central banks will raise interest rate when inflation is above target or when output growth is above potential. Second, we follow a rigor but scientific approach to capture the potential asymmetric response of macro fundamentals to monetary policy shocks. Besides this introductory section, the article presents five more sections. The next section presents the theoretical foundations of asymmetries in monetary policy. The third section discusses the data, while the fourth section explains the model and estimation procedures. The fifth section presents and discusses the empirical findings. The sixth section concludes the article and offers some recommendations.

Theoretical Foundations of Asymmetries in Monetary Policy

There are several theoretical reasons why monetary policy has asymmetric effects on aggregates, such as output and inflation (see Zakri & Malik, 2013). However, it is the Keynesian interpretation that prices and wages are sticky downward and flexible upward that has remained the workhorse for analysing the asymmetry effect of monetary policy. This approach attributes the potential of asymmetries in monetary policy to the fact that prices are likely to be ‘sticky’ or less likely to adjust downward. Consequently, it is suggested that an expansionary monetary policy is likely to be less effective than a contractionary monetary policy. That is, for the downward rigidity nature of prices and wages, firms are most likely to respond to a contractionary monetary policy by reducing output rather than prices. Hence, contractionary and expansionary monetary policies are likely to give different consequences when prices or wages are rigid in the downward direction but flexible in the upward direction. This, by implication, generates a ‘kinked’ aggregate supply curve such that negative (contractionary) monetary shocks are asymmetric (see Tan et al., 2010). Similar to the Keynesian interpretation are models with cost of menu strategy. The cost of menu approach relates the source of asymmetry in monetary policy to the fact that firms keep prices constant in response to a small shift in nominal demand to avoid menu cost (see Wooheon, 1995; Zakri & Malik, 2013). It is on this note that big monetary shocks have been widely proclaimed as likely to be neutral, but the same cannot be said of small monetary shocks, thereby constituting asymmetries in monetary policy. There is also the ‘credit view’ approach suggesting that firms are likely to encounter credit constraint during the recessionary period than they would in expansions.

Data and Preliminary Analysis

For monetary policy indicators, we find interest rate as the most prominent in the empirical literature. Other most widely used variables in the monetary economics are output, inflation and exchange rate. We further control for government influence via fiscal measure using government borrowing. All the variables are in a monthly period sourced from the International Financial Statistics (IFS) and FRED online database, respectively. The start date for the sourced data is January 2000, and the end date is December 2018.

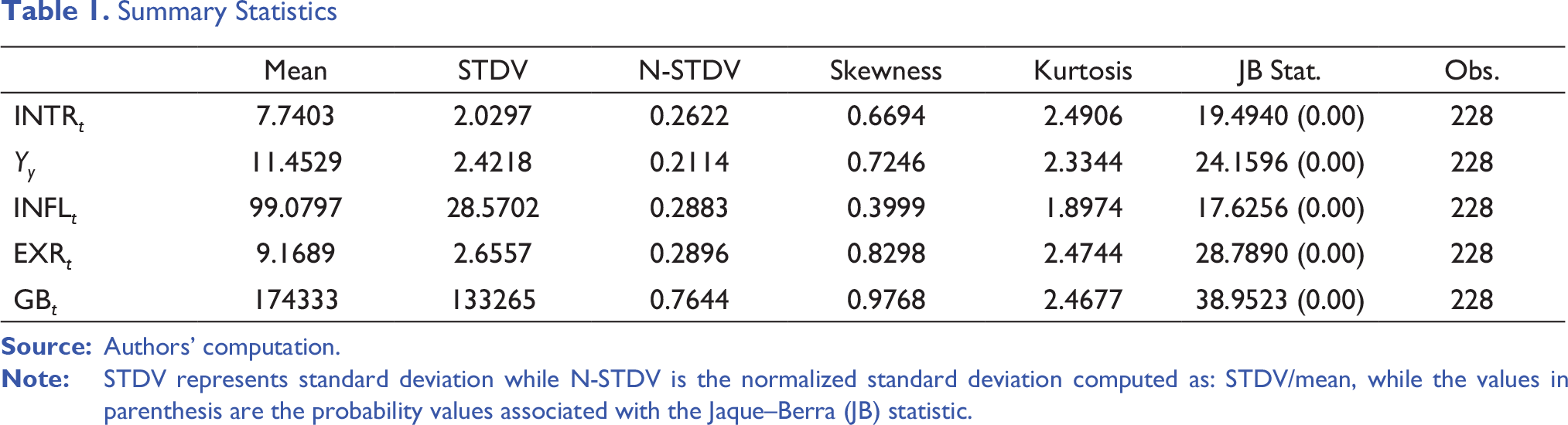

Starting with the summary statistics where all the variables are expressed in their respective original unit of measurement, the average interest rate for the period under consideration is 7.74 per cent. However, the standard deviation statistics for the individual variables cannot be compared in absolute terms because the variables are expressed in varying unit of measurement. Therefore, for the purpose of comparison we normalize the standard deviation statistics and a cursory look at Table 1 shows that government borrowing, a proxy for government influence or exogenous condition, is the most volatile given its relatively higher value of standard deviation statistic. With respect to the statistical distribution of the variables, all the series appear to be positively skewed but output. Similarly, the kurtosis statistics are mostly leptokurtic. On the whole, the computed probability values associated with the Jarque−Bera normality test statistic appears to be less than 0.05, implying the rejection of the hypothesis that the series are normally distributed at 5 per cent level of significance.

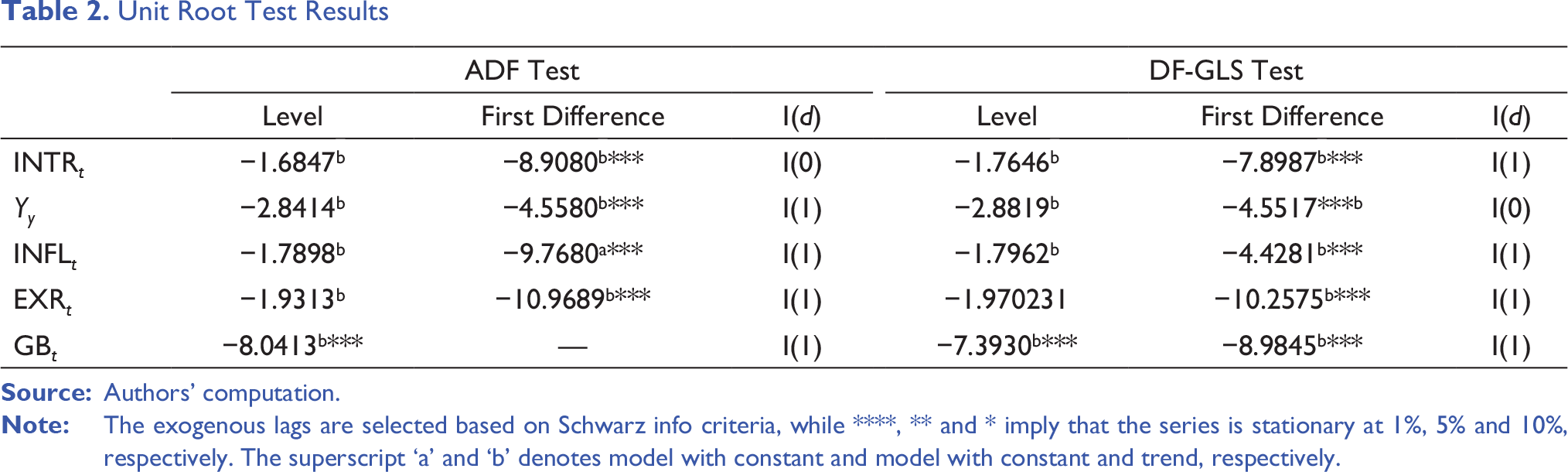

As a precondition for dealing with time series, we further subject each of the series to unit root tests. For robustness purpose, we consider both the augmented Dickey–Fuller (ADF) test and the modified version, namely, Dickey–Fuller GLS (DF-GLS) test. Table 2 presents the unit root test result which is performed on the natural logarithm of the series. Strengthening our choice of estimation technique, for instance, ARDL framework is the mixed integration properties exhibited by the variables. For example, a look at Table 2 shows that the order of integration for the series hovered between I(0) and I(1) nonetheless the choice of unit root test.

The Model and Estimation Procedure

In an attempt to validate or refute the earlier established theoretical foundations regarding the asymmetry effect of monetary policy, we employ an empirical framework similar to that given by Cover (1992). The framework which consists of two equations is often referred as two-step procedure (see Gogas et al., 2018; Karras, 1999, 2013; Ravn & Sola, 1996; Tan et al., 2010; Zakri and Malik, 2013, among others). In the first step, we follow Taylor’s rule, which assumes that a typical monetary policy authority responds to variations in inflation and output.

Summary Statistics

Unit Root Test Results

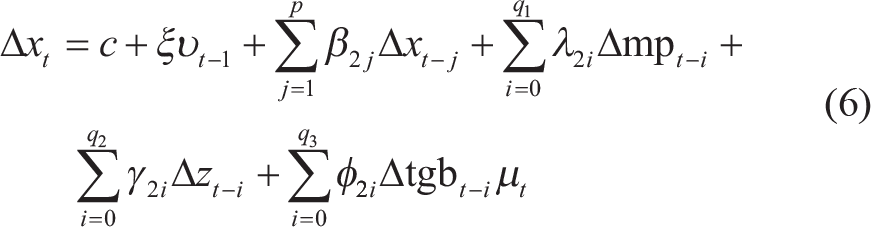

The next step is to reflect the unanticipated monetary policy shocks obtained in each of the macroeconomic equations under consideration, namely, output and prices (inflation).

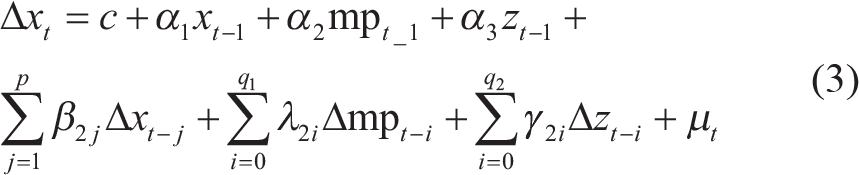

Linear (Asymmetry ARDL) Model

Although, the nonlinear ARDL (NARDL)

1

developed by Shin et al. (2014) is the preference of this study to capture the probable of asymmetric response of output and inflation to South African monetary policy shocks, but for the sake of robustness, consistent and unbiased comparison, we started with conventional (linear or symmetric) ARDL as our baseline model,

where xt = yt, πt denote output equation and inflation equation, respectively. The term mpt denotes monetary policy shocks while zt is the control variables which may vary for output (yt) and inflation (π

t

) equations. Starting with the former, the term zt includes some of the traditional determinants of output growth, namely, inflation and exchange rate. For the price level equation, we follow the exchange rates pass-through approach, such that the zt in that regard capture the small-open economy feature of South Africa using exchange rate and output growth to capture demand-pull determinant of inflation. The long-run parameters for the intercept and slope coefficients are computed as:

where

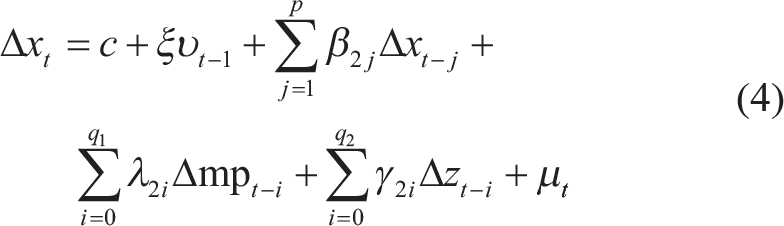

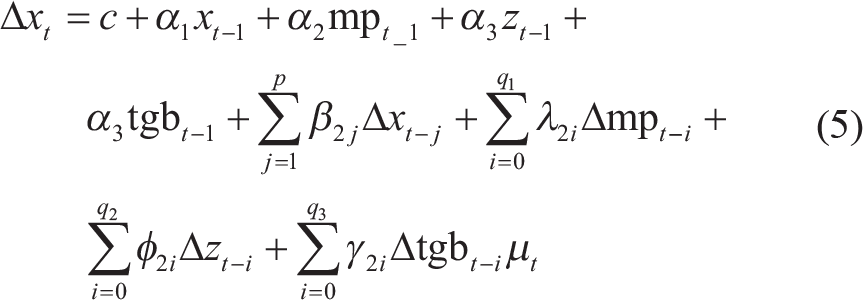

The error correction version of model (4) that includes the fiscal side of the economy is as given below, where the error correction term, as well as the term for speed of adjustment, remains as earlier defined.

Non-linear (Asymmetry) ARDL Model

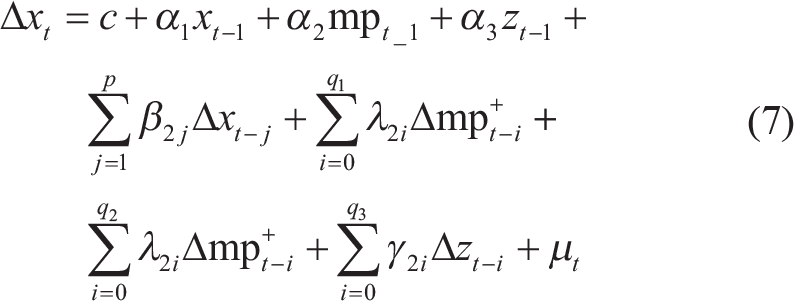

The focal point of this study is to test whether macroeconomic fundamentals, namely, output and inflation, react differently to contractionary (tightening monetary policy shock) and expansionary (easing monetary policy shock). The starting point, therefore, is to partition the unanticipated monetary policy shocks generated in Equation (2) into positive (contractionary) and negative (expansionary) monetary policy shocks. These decomposed unanticipated monetary policy shocks are defined as follows:

and

where the series

where

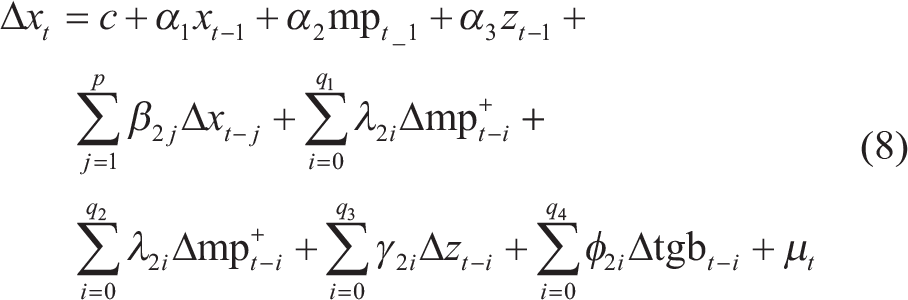

We further extend the NARDL to examine the extent to exogenous conditions such as government influence via fiscal borrowing also matters for the asymmetric impact of monetary policy shocks on output and inflation.

Again, all other procedures for error correction form of the extended NARDL in Equation (8) as well as the procedures for obtaining long and short-run coefficient remain the same as demonstrated in the case of ARDL.

Empirical Results

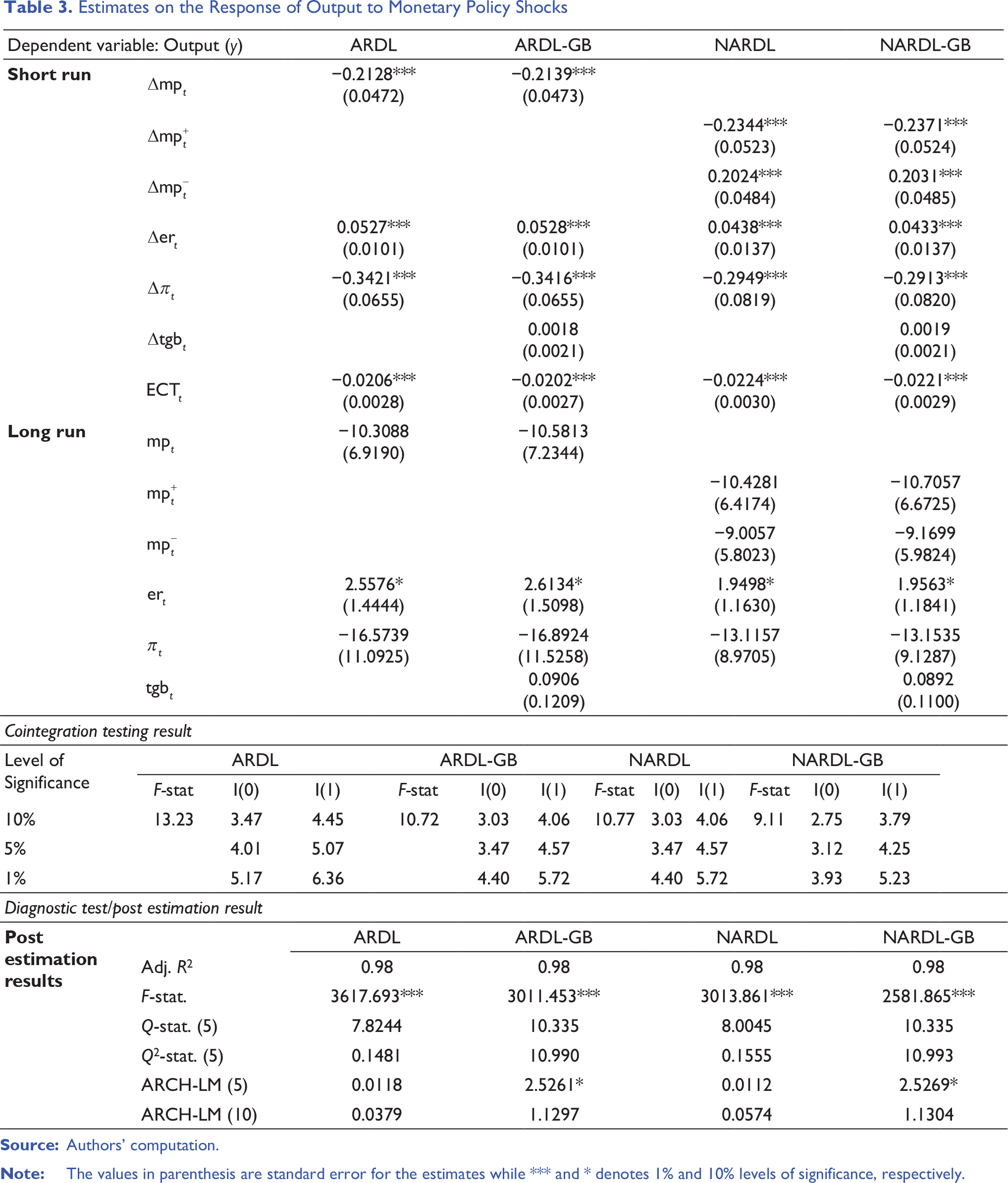

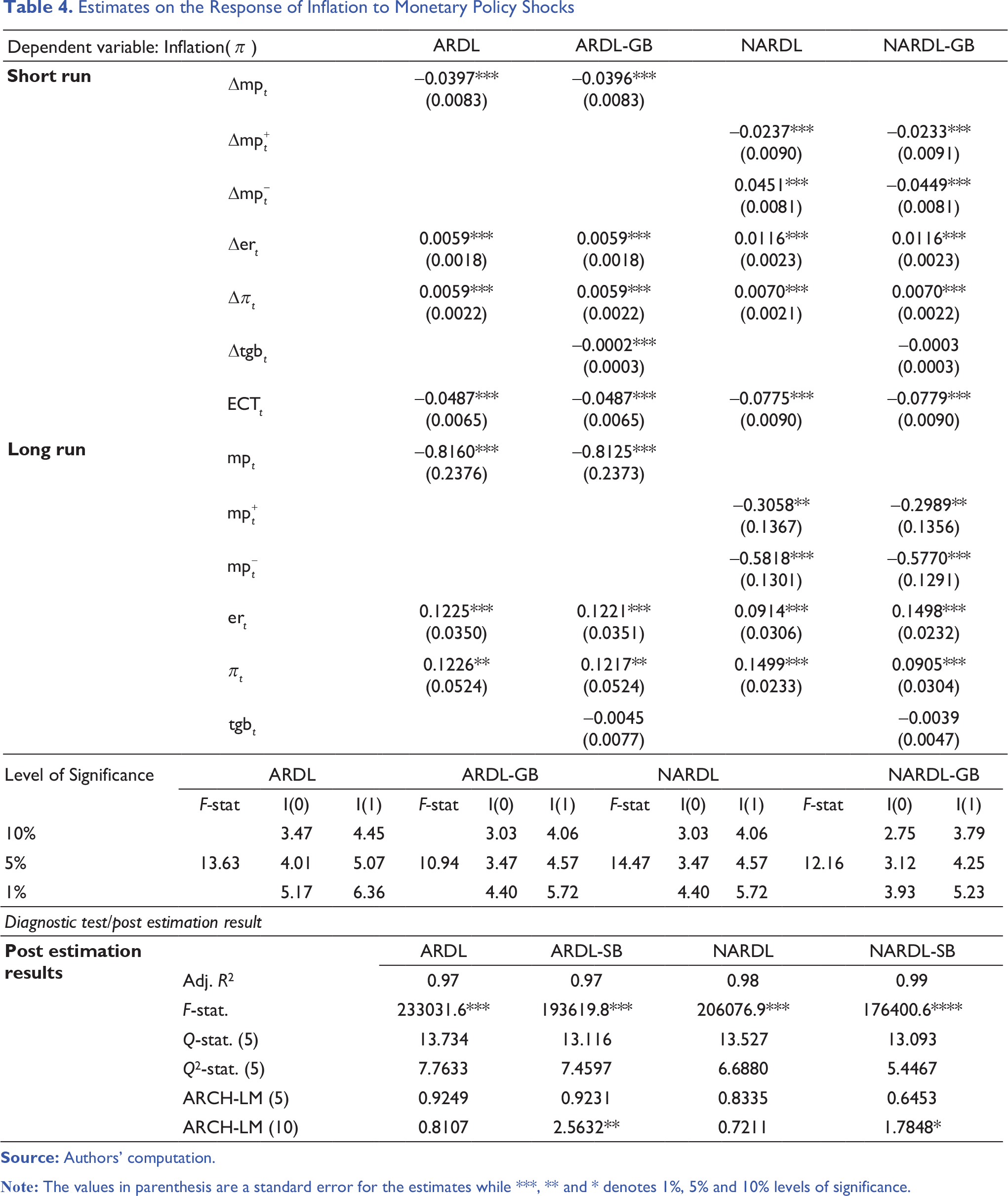

Beyond our finding of significant response of output growth to positive (contractionary) and negative (expansionary) monetary policy shocks (Table 3), the fact that the magnitude is higher for the positive shock relative to the negative shock confirms our hypothesis that asymmetries matter in in the response of the macroeconomic fundamentals to monetary policy shocks in South Africa. More importantly, the fact that the sign on the coefficient on the positive shock is negative but positive for negative is in line with the economic prediction of negative response of output growth to contractionary monetary policy and vice-versa for easing (expansionary) monetary policy shocks. The empirical result shown in Table 4 confirms the trade-off consequence of such an asymmetry relationship , where a positive shock to monetary policy causes declining inflation and the reverse is the case for a negative monetary policy shock.

Estimates on the Response of Output to Monetary Policy Shocks

Estimates on the Response of Inflation to Monetary Policy Shocks

Conclusion

Using the South African dataset as a representative of developing economies, we control for the fiscal side of the economy using government borrowing as potential accelerator of asymmetry in a monetary function that follows Taylor’s rule. This is motivated by the relative higher vulnerability of monetary authorities to exogenous conditions such as government influence through their fiscal behaviour. Through the both the linear and non-linear ARDL framework, we observe the asymmetry effect of monetary policy to be significant for both the output and inflation, but mainly in the short run in the case of the former. We also find government borrowing a measure for government influence as an important underlying source of asymmetries in the response of macroeconomic fundamentals to monetary policy shocks in South Africa. This, among others, suggests that monetary authorities must not only consider the effectiveness or otherwise of monetary policy instruments to affect the target policy goals but also the fact that not all the target variables react similarly to expansionary and contractionary monetary policy shocks, particularly in an environment where monetary policy decision is likely to be influenced by exogenous conditions.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.