Abstract

Abstract

Emerging economies like India has been characterized with a substantial ‘bottom of the pyramid’ (BOP) population. BOP has also been one of the most promising market segments for business growth. Firms serving specifically the BOP customer segment was thus engaged in serving a social cause as well because BOP consumers (a weaker segment of society) got benefited because of their consumption of products or services offered by the business firm. In India, a large section of BOP customers who were economically progressing and becoming the new middle class used two-wheeler automobile to commute for personal as well as business needs. Two-wheeler automobile was lifeline for millions of rural and urban Indians. Two-wheelers were used for both consumptions as well as asset building purposes by Indian consumers. Affordability of two-wheeler had been a big challenge for this section of society. Borrowing from Indian credit institutions has been a very potent method towards owning two-wheelers for this segment. There was a section of BOP customers who were beyond the umbrella of the traditional Indian banking and financial sector. Since the decade of mid-2010s, the Government of India had been working hard to include this part of society into the banking system and had floated multiple social schemes to achieve banking inclusion. LokSuvidha, an Indian financial services start-up was founded by Mr Nimish Laddhad and Mr Kamlesh Laddhad. LokSuvidha developed an unique business model for providing credit to this part of society. LokSuvidha had also deployed cutting-edge technology solutions to build a scalable, profitable working model. However, the founders of LokSuvidha were in a dilemma regarding whether to expand LokSuvidha further in scale or scope or to concentrate only in the extant market base of its operations. This decision was paramount for the founders to be answered to shape the future of LokSuvidha in terms of both market reach and organizational span.

Introduction

1

Author’s interaction with Mr Kamlesh Laddhad, Chief Technology Officer (CTO), LokSuvidha, January 2018.

Author’s interaction with Mr Kamlesh Laddhad, Chief Technology Officer (CTO), LokSuvidha, January 2018.

LokSuvidha was a two-wheeler finance company operating out of the city of Nagpur in the state of Maharashtra in central India. LokSuvidha was founded by Mr Nimish Laddhad (here by referred to as Nimish) and Mr Kamlesh Laddhad (here by referred to as Kamlesh). Nimish was currently working as Chief Executive Officer (CEO), while Kamlesh was working as Chief Technology Officer (CTO) of LokSuvidha. During a discussion, both were gazing at the workstation bay area at the LokSuvidha head office in Nagpur. The soft January sunshine was glittering against the magnificent Ambazari Lake in the background beyond the transparent long glass wall in their office. The decade-long journey of LokSuvidha has been a fructifying experience for them. The business model of LokSuvidha had withstood the pressures of competition and time. Both the founders, very early in their journey, had realized that technology was a major catalyst in the growth of the business. They could comprehend that technology provided the ability to a small firm to scale. They were able to foresee how technology infusion would help LokSuvidha achieve business scale with marginal costs. Reaching such scale otherwise would have not been possible for relatively small enterprises. So far so good! But both pondered what next! What would drive the next phase of growth strategy? Should the next script be on scale enhancement or scope enhancement?

Origin2

Author’s interaction with Mr Nimish Laddhad, Chief Executive Officer (CEO), LokSuvidha, January 2018.

, 3

LokSuvidha Internal documents.

Author’s interaction with Mr Nimish Laddhad, Chief Executive Officer (CEO), LokSuvidha, January 2018.

LokSuvidha Internal documents.

In September 2008, Nimish started LokSuvidha Finance Limited (hereby refered to as LokSuvidha). He was a chartered accountant (CA) by profession and had work experience in two-wheeler finance industry for a decade. In the late years of the decade of 2010, Nimish from his experience had realized that two-wheeler would be a very fast-growing market in India in the years to come. He also envisioned that finance would drive the growth of this market. Nimish found that two-wheeler was not only just purchased by middle-class Indians but also the poor Indians at the bottom of the pyramid (BOP) (Sudame & Mourya, 2016; Shah, 2010; Jaiswal & Gupta, 2015). The lower middle class and BOP segment Indian families purchased two-wheelers generally and mostly through a loan mechanism. This was because poorer families were unable to make down payment of about Indian rupees 50,000 (USD 800) at one go. He spotted that there were two kinds of consumer segments requiring two-wheeler finance. One was the salaried class having proof of formal earnings and, thus, could borrow and secure a loan from scheduled banks easily. The second set of customers were mostly new recruits or self-employed individuals in unorganized sectors who were unable to produce documents proving their income status. The first segment of customers who were able to produce healthy income documents were provided with loans by banks or other big financial institutions. But the second section was by and large not catered by any credit institution. In India, the central bank, that is, the Reserve Bank of India (RBI), regulated all financing activities and issued strict guidelines and norms to be followed by credit institutions before sanctioning and disbursing any loan (Karnani, 2007; Das, Patra & Das, 2014). The strictness of the regulator was very well justified as non-performing assets (NPAs) have been a major concern for Indian banking and financial services sector for many years (Prahalad, 2006; Karnani, 2007; Das et al., 2014).

Nimish had noticed that a substantial number of loan requests were coming from individuals who were not able to produce formally documented income statements for supporting their loan applications. Thus, the banks had to reject their loan application. These individuals were thus non-customers to the banks. On the other hand, he also noticed that in India, banks were cash-rich and were not able to deploy the funds it possessed. So Nimish came up with a model to turn these non-customers into customers by bridging the gap. In September 2008, he established LokSuvidha in Nagpur in central India. The business model of LokSuvidha was to act as a bridge between these non-customers and banks.

LokSuvidha proposed to become the guarantor for all such individuals who could not produce income documents as per the norms of RBI and approached banks for loans on behalf of such customers. LokSuvidha studied these individuals and vetted their potency and appetite for loan repayment. LokSuvidha studied these individuals’ context in terms of their age, education, asset base and their dependent family members’ profiles and such other demographic details over and above their earning capabilities. Upon assessing these individuals and getting themselves convinced that such possible customers had capability to repay a loan, LokSuvidha approached banks on behalf of the customer for loan for two-wheelers. LokSuvidha was the guarantor. This model was highly appreciated by the banks as the banks could utilize the excess funds for deploying into the market. LokSuvidha was providing a service (which was also a social cause) by facilitating loans for customers. The two-wheeler loans provided individuals the scope to own a two-wheeler vehicle and utilize it to undertake a better profession. This facilitated the future career growth prospect of the individuals which improved their lives in many ways. LokSuvidha services thus enriched many lives by providing financial assistance for two-wheeler to the needy Indians in central India. Customers could take these loans either for business purpose to build an asset or in individual capacity for household needs. Examples of LokSuvidha customers could include any of the following representative examples. It could be a 40-years-old individual working in a private firm whose daughter just entered college and she is required to commute on a two-wheeler for attending college, thus a demand for the same sprouted. It could also be a 20-year-old male family member seeking to become a newspaper or milk vendor, who would require a two-wheeler to start his business. This 20 year old, with the help of a two-wheeler, would distribute newspaper or milk to a larger coverage area and thus boosting his income. Another example could be of an individual who has recently secured a job in a factory and has to commute to his workplace daily using the two-wheeler. All these examples indicated the types of service offered by LokSuvidha. Such services were the nature of contribution made by LoKSuvidha towards the growing India.

When LokSuvidha was getting formed, Nimish selected the name ‘LokSuvidha’ for easy brand recognition. LokSuvidha was a Hindi word which meant service for people. LokSuvidha as a term was not a tongue-twister. It was a simple word that every Indian could understand, pronounce and relate to. Further, the term had a positive feeling for Indians in general.

Kamlesh joined LokSuvidha in April 2015. Kamlesh did his postgraduation in computer science and engineering from the prestigious Indian Institute of Technology Bombay (IITB) in India. Prior to joining LokSuvidha, Kamlesh had worked with multinational companies. Kamlesh always had the desire to become an entrepreneur. Kamlesh wanted to build a business which would be consumer-facing and could be scaled through the deployment of technology. So, at LokSuvidha, Nimish became the business brain, while Kamlesh became the technology brain, and they complemented each other with their skills and knowledge.

The Growth1,2,3

Kamlesh was interested to provide scale to LokSuvidha business. To achieve scale, Kamlesh developed an information technology (IT) strategy and developed the required technology resources and capabilities. The technology strategy was based towards providing transparency and visibility of data and information at each level in the organization right from the top until the field-level worker. Kamlesh noticed that the usage of mobile devices was becoming ubiquitous in central India. By the year 2018, Indians had used mobile devices in hundreds of millions. Envisioning the future of mobile in mind, Kamlesh designed his technology strategy. He planned this by keeping mobile device at the centre of LokSuvidha business model. Kamlesh created and maintained an android mobile application (hereby referred to as LokSuvidha app) at the front end. A robust customer relationship management (CRM) system was maintained at the back end. Kamlesh through increased usage of IT based upon mobile devices started providing empowerment to LokSuvidha employees. Earlier field-level employees had to approach the top management team for every decision-making as there was dearth of information at their end. Thus, at earlier times, decision-making was a slow and lengthy process. The organization was lacking agility overall.

Kamlesh created an IT portal for employees. This portal aggregated all the business-related information named ‘LokSuvidha Reports’. This portal provided all the information that was required for decision-making to LokSuvidha employees across organizational levels. Further, all the new initiatives which were being undertaken by LokSuvidha were presented in the portal and made available to employees. Such steps and organizational processes helped employees to undertake decision on their own and reduced their dependence on the top management in decision-making.

Kamlesh brought a cultural change at LokSuvidha with an increased emphasis on digital communications through mobile devices. Kamlesh while interacting with the employees stopped taking phone calls-based instructions. He instead insisted that all communications should be done through email. Approvals and decisions had to be necessarily communicated by emails only. If communication was not done via email, then internally in the organization the communication had no significance. The smartphone revolution (Das et al., 2017) helped LokSuvidha in this endeavour. LokSuvidha employed young individuals typically, in the age group of 22–30 years. Such individuals were comfortable in using the latest technology, and thus there was very little resistance for adopting technology in the organization.

Kamlesh developed training materials which focused on the know-how that field executives needed better interactions with customers. In the IT system-based interface, everyday morning push mails were sent to various executives alerting them regarding the due dates for loan follow-ups, the last date for approval and such others. Kamlesh developed video-based tutorials for training new recruits regarding applications of technology in LokSuvidha business. The video tutorials had two parts, namely mandatory and non-mandatory. Until and unless a recruit completed the mandatory training, she would not be able to operate the LokSuvidha app.

Kamlesh was instrumental in developing a mobile application (LokSuvidha app) that became the keystone of the entire life cycle of loan. The mobile application could be used across the value chain of LokSuvidha. LokSuvidha employed field staff comprising of sales team spread across the market to develop and secure business with clients and customers. These field executives interacted with customers to ascertain the nature of customer requirements. The field executives used the LokSuvidha app to collect data about the profile of the customer—name, age, gender, education, address, family details, profession, past credit history and such others. The potential customers were individuals who had come for enquiring regarding two-wheelers at various two-wheelers dealer outlets. The field representatives of LokSuvidha also collected from the customers physical documents for proving identity—PAN card (Nidugala & Pant, 2017), address document (called Aadhar card in India; Sridhar, 2011), bank statements and such other documents. The field representatives clicked photographs of these documents and uploaded the same via LokSuvidha app for assessment by the LokSuvidha back office team in the head office at Nagpur.

LokSuvidha was operating with 14 offices in two states in India—Maharashtra and Madhya Pradesh. LokSuvidha employed about 170 field executives by January 2018. To promote the use of the app by all field executives, LokSuvidha provided interest-free loan of Indian rupees 7,000 (USD 100) to purchase a smartphone of their choice and download and run LokSuvidha app on it. Field executives were supposed to repay the loan in seven months’ time with equal instalment of Indian rupees 1,000 to be paid back every month.

LokSuvidha established processes in the organization not only in IT system but also in human resource management. This delineated the duties and responsibilities of each individual manning the credit life cycle of a two-wheeler loan. The front-line sales (FLS) punched in prospective customer data details from a remote location via the LokSuvidha app, and thus in real time this data reached Nagpur office and the process for credit decision was instantly initiated. A credit decision-making system automated by algorithm computing (incorporating RBI-specified relevant data points) carried out the analysis. Most of the credit decision-making activities were carried out by the system through various checks and rules. LokSuvidha had built a scoring engine for assessment of customers’ profile and repayment capability. According to Kamlesh, 80 per cent of the times, the system by itself provided decisions regarding approval or rejection, and this was called system through pass (STP). While 20 per cent of the credit activity was required to be carried out by manual intervention. The manual intervention was regarding the physical verification of knowing your customer (KYC) (Padmavathi et al., 2017; Soni & Duggal, 2014; Raman, 2012). KYC verification involved actions like name and address verification of the individual.

Organizational Management at LokSuvidha 1,2,3

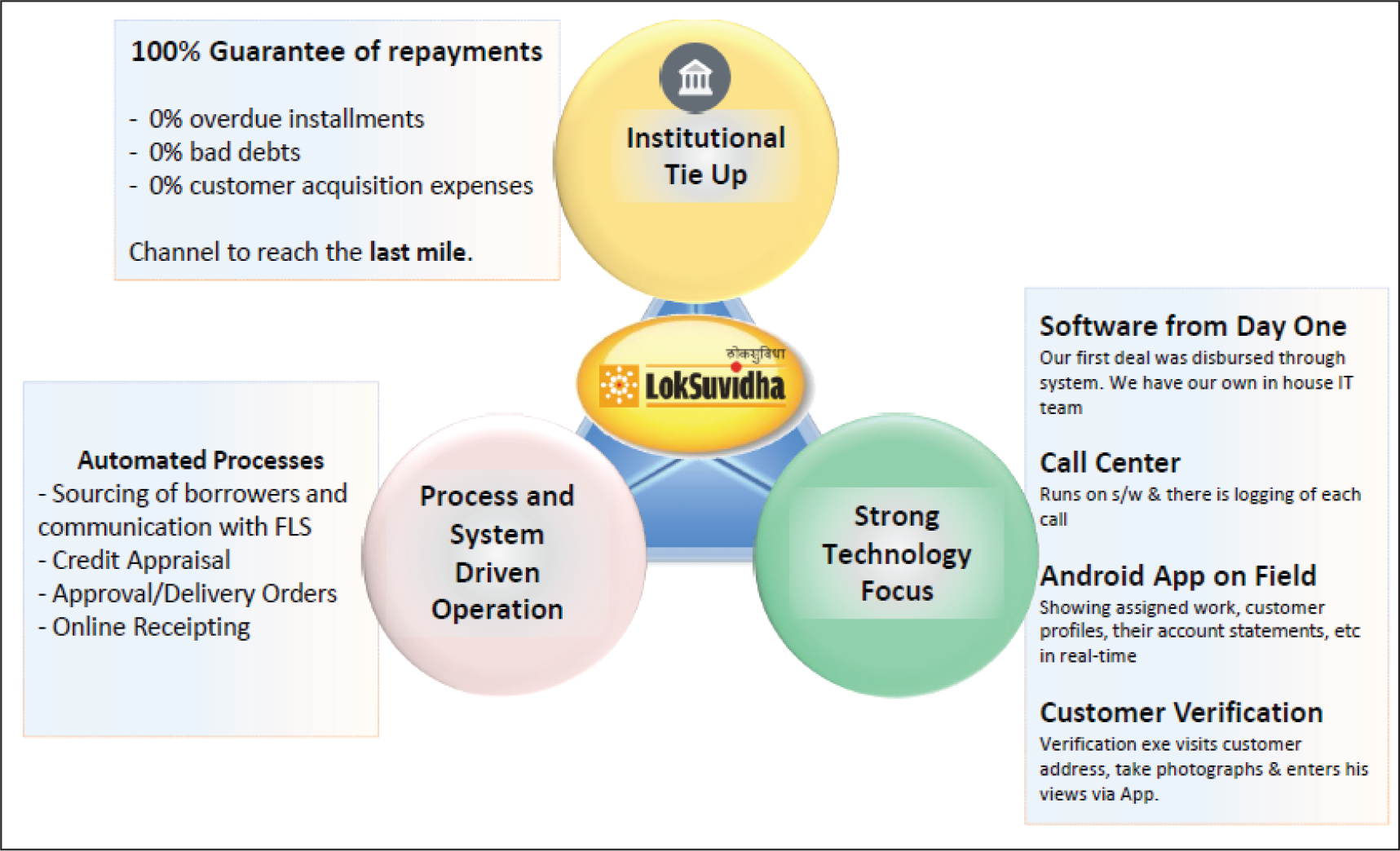

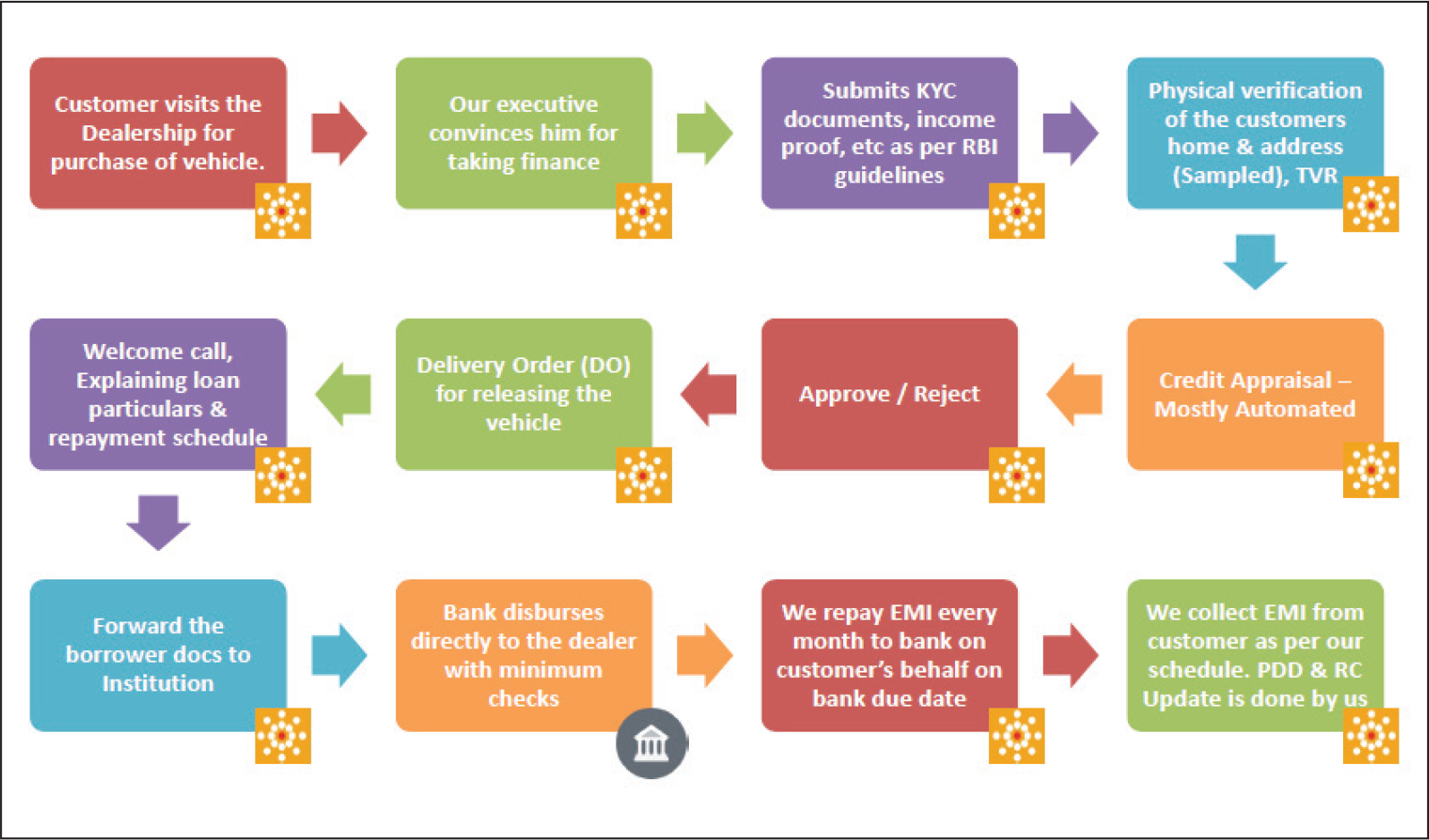

LokSuvidha had three business pillars. These were LokSuvidha’s institutional tie-ups, LokSuvidha’s strong technology focus and, finally, LokSuvidha’s process-based system-driven operations. The institutional tie-ups were with banks. LokSuvidha provided a channel for banks to reach the last mile to the customer. LokSuvidha provided banks 100 per cent guarantee of repayment at 0 per cent default, 0 per cent overdue installment and further, for a bank, there was 0 per cent customer acquisition expense. The second pillar had been the strong technology focus as all the internal processes of LokSuvidha were managed by the IT portal. The customers were catered by the LokSuvidha Android application based on mobile devices on the field. The third business pillar was ‘process and systems-driven operations’. LokSuvidha had developed automated processes for sourcing for borrowers, credit appraisal, credit approval and delivery order and online receipting. LokSuvidha business pillars have been depicted in Exhibit 1. The business process of LokSuvidha consisted of eight steps. Exhibit 2 refers to the process of LokSuvidha business. These step process were the following:

Prospective customer reached LokSuvidha for loan enquiry. LokSuvidha field executives provided the prospective individual customers a checklist of information and documents required. LokSuvidha representatives punched in the data, uploaded prospective customer documents in the app which then become available to central processing team at Nagpur office and within 30 minutes Nagpur office informed the LokSuvidha field representative regarding the credit decision. The field representatives subsequently informed the prospective customer about the credit decision. LokSuvidha field representative informed the two-wheeler dealer regarding loan approval. The dealer released the vehicle to the customer. LokSuvidha approached the bank for disbursement of the funds to the dealer. The individual made payback for the monthly instalment to LokSuvidha to repay the loan. LokSuvidha paid back the money to the bank.

LokSuvidha secured profit by earning a certain percentage of the fund disbursed by the bank. This has been the source of revenue for LokSuvidha. The business of LokSuvidha had thus been very sensitive to cost parameters. Thus, LokSuvidha focused to operate in the rural areas of central India. A case in point was LokSuvidha though has its head office in Nagpur city did not operate in Nagpur city because there was too much competition in the market and too much competition translated into unhealthy cost pressures. The regions of operations of LokSuvidha have been provided in Exhibit 3 and tabulated in Exhibit 4. The customer profile of LokSuvidha has been provided in Exhibit 5. LokSuvidha did not face attrition problem of its human resources because LokSuvidha was located in Nagpur (a Tier-I city in central India). Nagpur offered very little opportunity for alternate employment for LokSuvidha employees (Sudame & Mourya, 2016; Shah, 2010). However, talent acquisition has been a major challenge for LokSuvidha. This was because Nagpur, as a location, inherently offered relatively poorer talent base in the financial sector (Sudame & Mourya, 2016; Shah, 2010).

LokSuvidha regions of operation

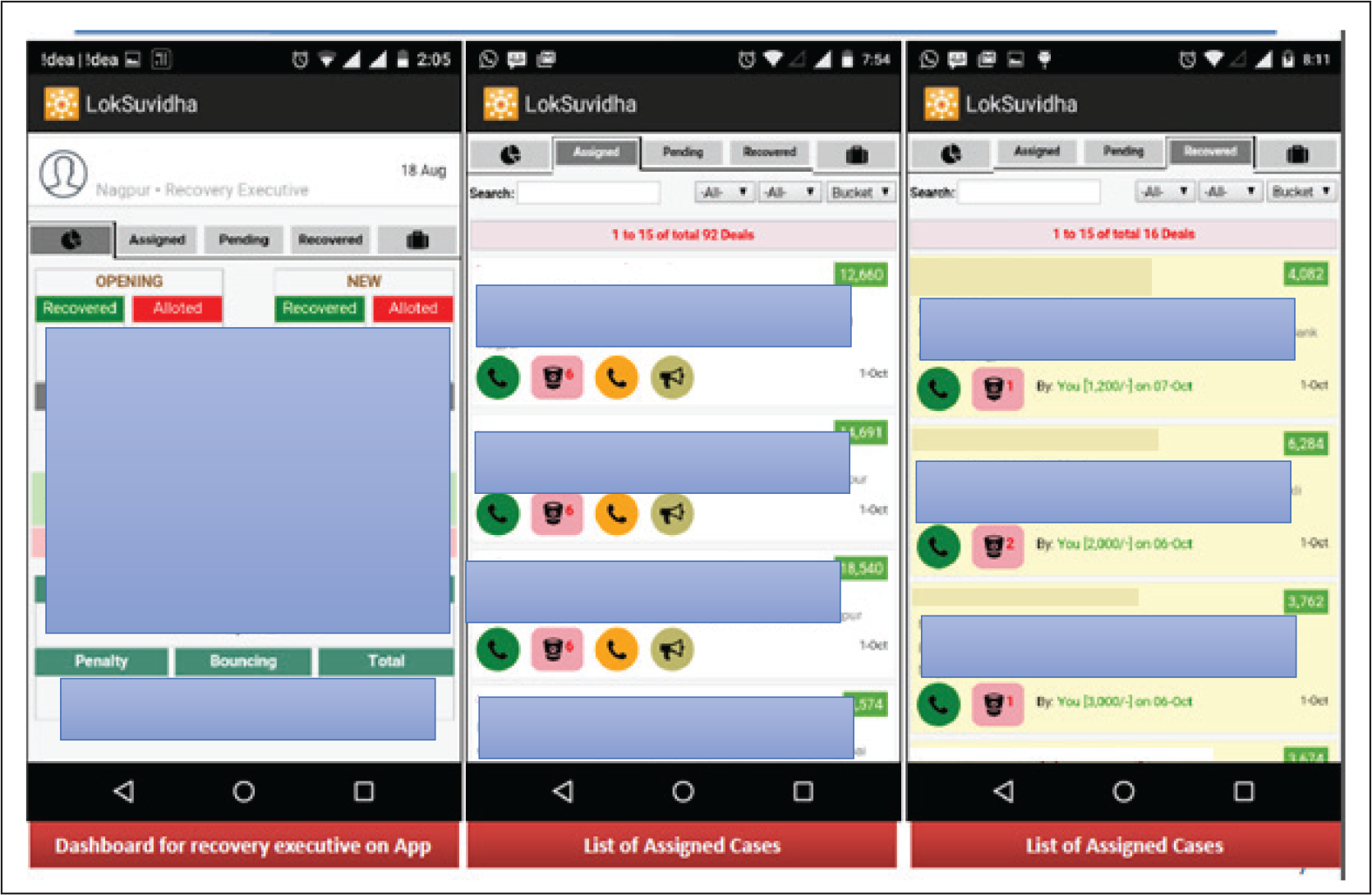

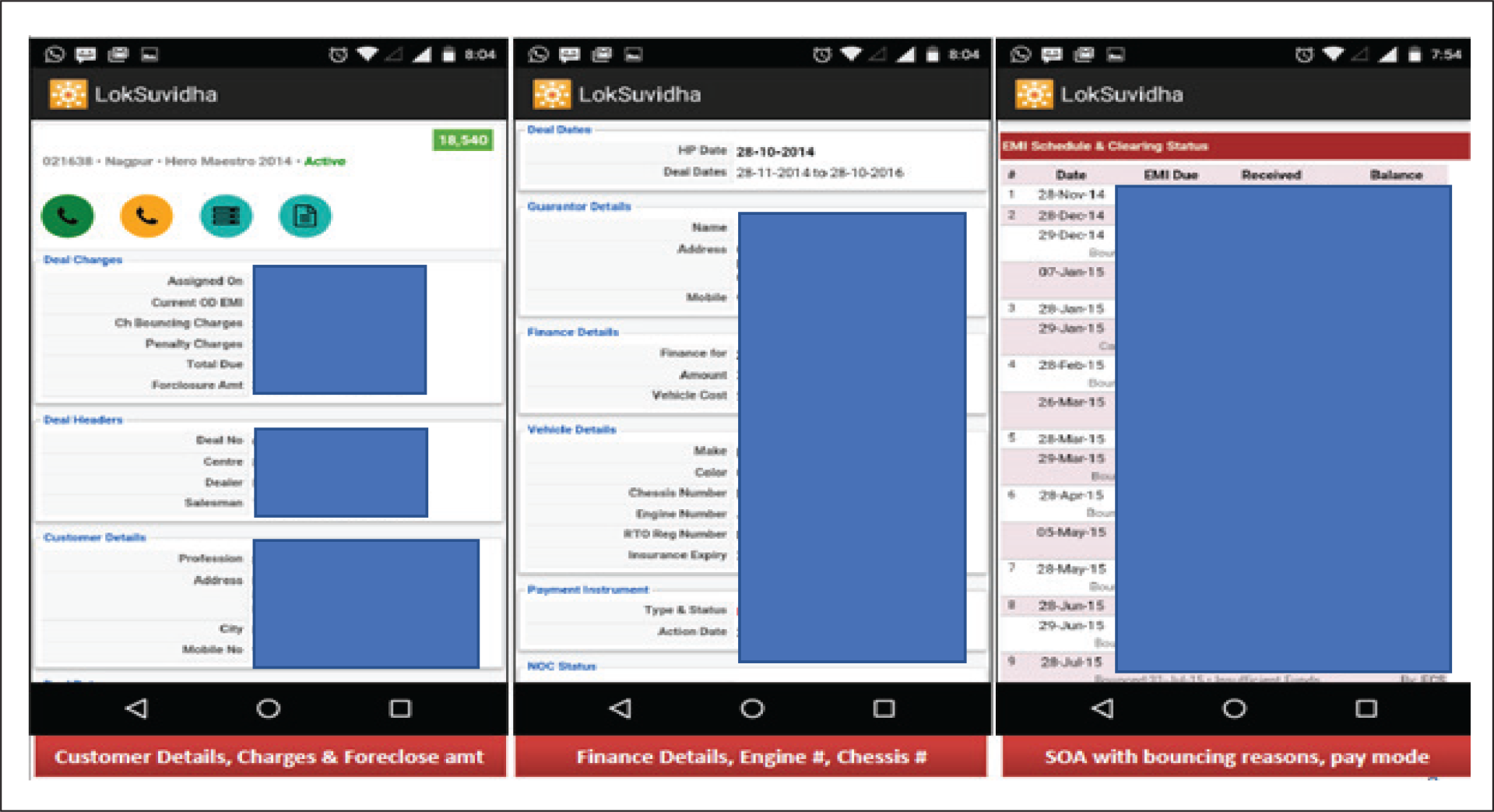

Nimish and Kamlesh every month undertook a performance review of the 170 field staffs. In the review the best performers were rewarded, whereas the poor performers were encouraged to improve. LokSuvidha team led by Kamlesh developed the LokSuvidha app indigenously. This was required to be done because such an app was not available. Development of this app stretched the capability of the IT team of LokSuvidha. The roll-out of the app immensely boosted the confidence of the IT team. This app was developed at a low level of investment and this provided a competitive edge to LokSuvidha vis-a-vis the competitors. Exhibits 6 and 7 are screenshots of LokSuvidha app.

Business Challenges1,2

Two-wheeler financing like any other credit business inherently contained risk of default. Default happens when a customer did not make loan repayments. LokSuvidha executives understood that there were two kinds of loan defaulters. The first set of defaulters were the ones having intention problem and the other having repayment capacity problem. Intention problem occurred when a customer willingly defaulted. LokSuvidha business risk mitigation team based on diligence tests (the study of past history of loan repayments) attempted to stay away from such customers. Customers sometimes had the intention to pay, but did not have the capacity to make a time-bound payment. This might be because of illness of the income earner in the family or a poor harvest of a farmer. In such cases, LokSuvidha bufferd the customer repayment by making payments to the bank until the customer could make the overdue payment. In extreme cases, LokSuvidha has to secure the collateral that is the two-wheeler automobile itself. Two-wheeler loans is a secured loan product where automobile is collateral.

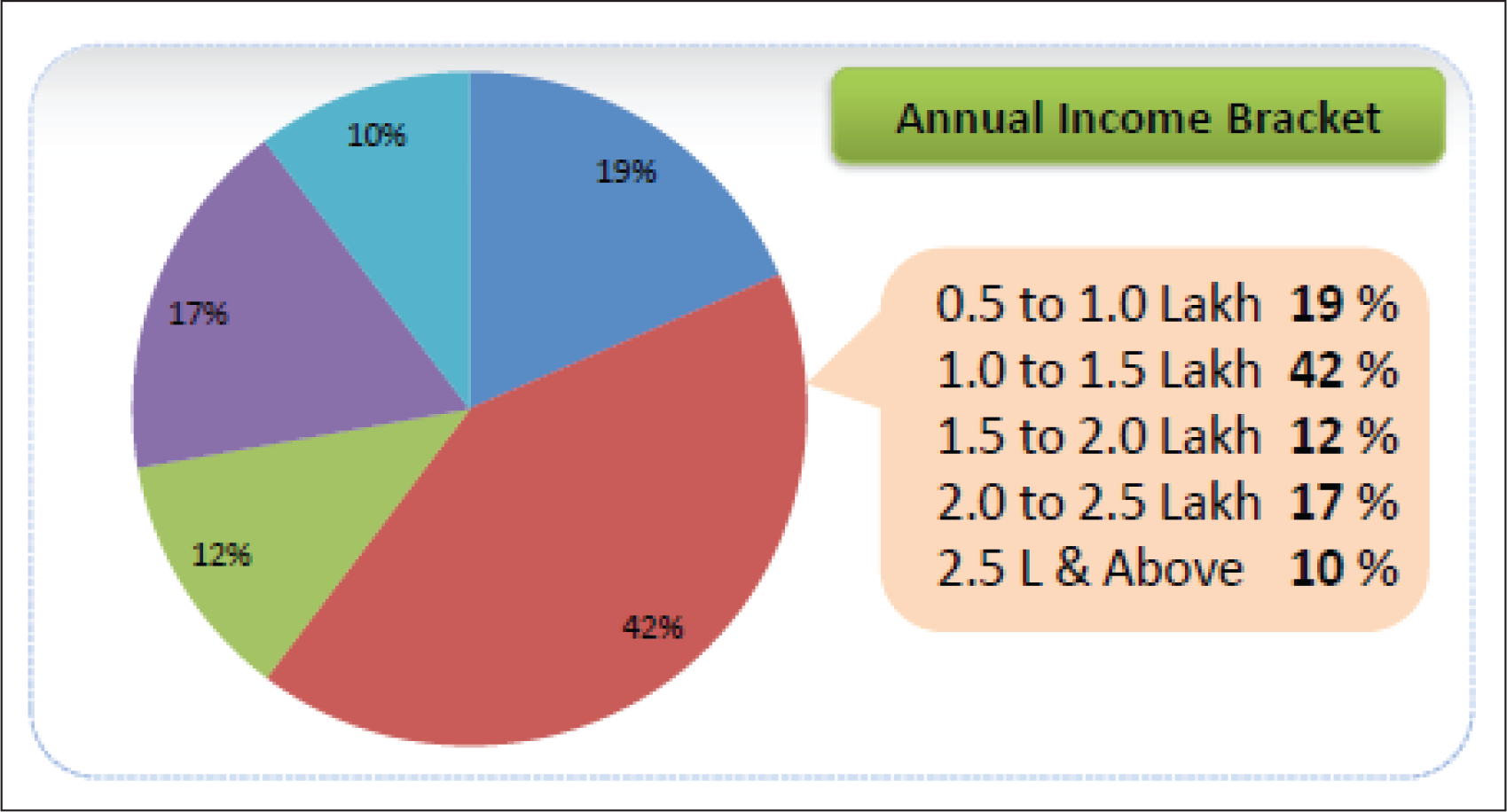

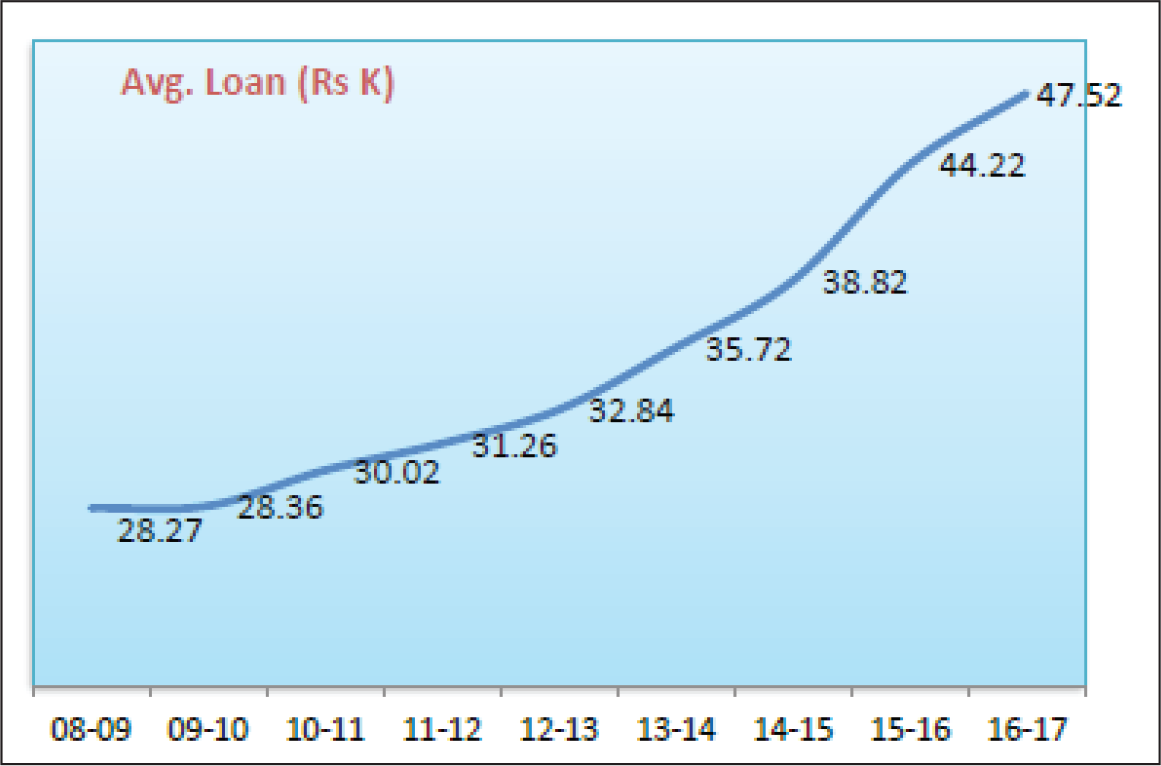

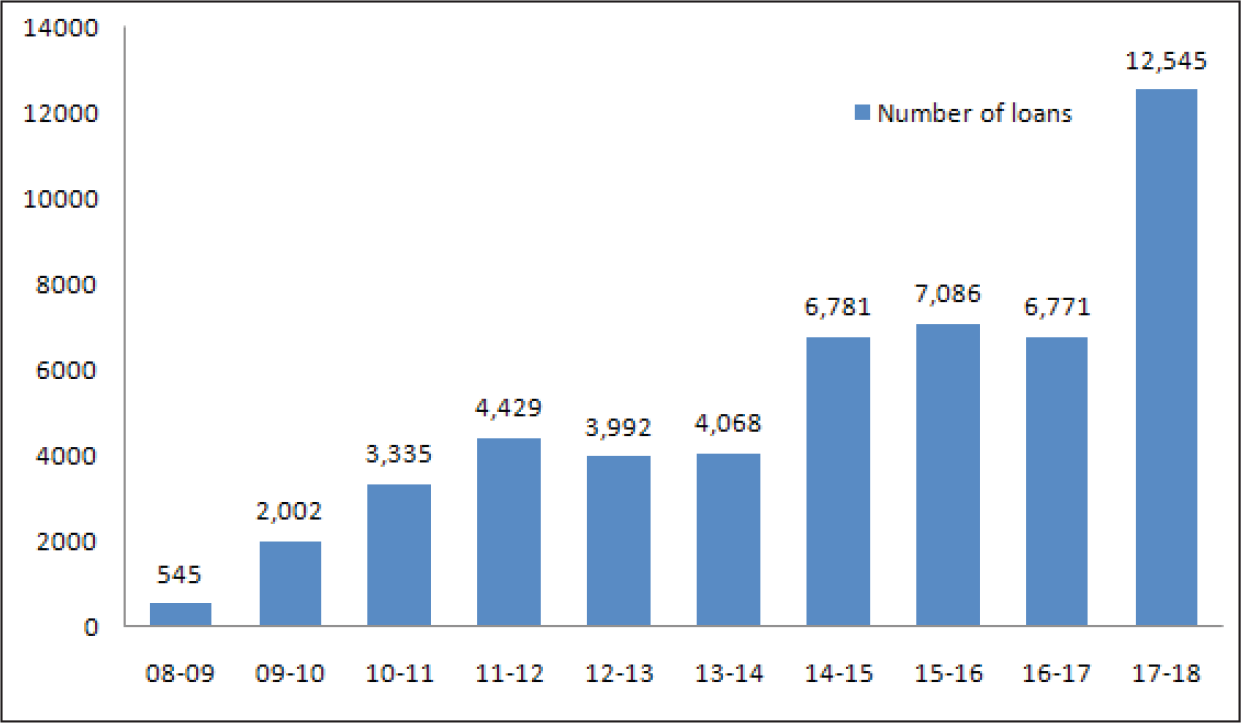

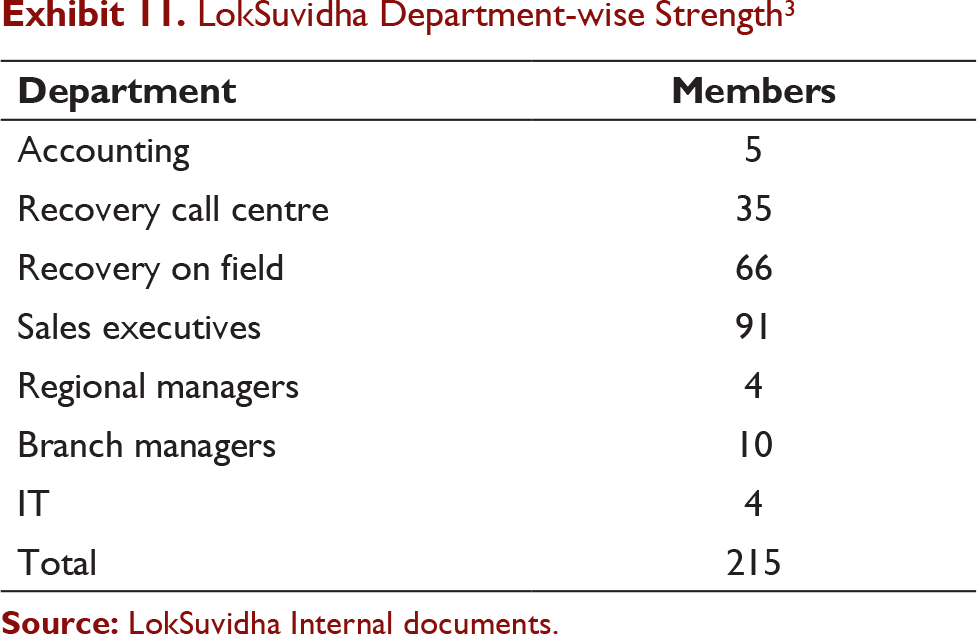

LokSuvidha executives understood that in credit business there would be a long line of customers (as everyone required money), however the key was while expanding the credit base from X to say 10X, finding out the right customers who could repay the loan (refer to Exhibit 8 for customer annual income bracket of LokSuvidha customers). Refer to Exhibit 9 for average loan amount taken by LokSuvidha customers over the years. Exhibit 10 explains the business growth of LokSuvidha in terms of the number of loans provided by LokSuvidha to its customers over the years. The average age of LokSuvidha employee was 24 years as of January 2018. There were a total of 215 employees in LokSuvidha. Exhibit 11 provides the department-wise strength at LokSuvidha.

LokSuvidha Department-wise Strength3

Customer interaction with LokSuvidha field executives was also unique. When a customer walked into the dealers’ shop, she was interested to buy a two-wheeler. Though customers took the assistance of LokSuvidha for getting a finance, customers generally had vehicle in mind. BOP customers wanted progress in life, and business-based offering solving their socio-economic problems had great value in their lives (Verma & Bhattacharyya, 2016). Thus, LokSuvidha had selected prime dealers in its area of operation and had set up a small booth inside the dealer showrooms. LokSuvidha executives relied on positive word of mouth of the satisfied customers for business growth.

LokSuvidha top management team executives every year went and had discussion with banks regarding the number of customers (with a secured percentage of collateral) it can develop as business. The banks vetted this every year and allocated a said amount of fund for LokSuvidha. LokSuvidha executives while interacting with the dealers understood the symbiotic nature of the relationship. LokSuvidha executives thus helped these dealers to convert non-customers to customers. However, LokSuvidha executives understood that the dealers have many choices and thus dealers had more bargaining power (Porter, 2008). LokSuvidha advertisement was also carried out through hoardings in dealer shops. LokSuvidha had customer loyalty programmes in place. Customers who in the past had made loan repayment in time were provided the benefits of bigger loan amounts or cheaper loan rates. LokSuvidha management understood that manpower was a key strategic resource and its constant development was a business necessity.

Nimish and Kamlesh looking at the expanse of the Ambazari lake pondered that LokSuvidha business model had been established and it had also grown in size over the years. LokSuvidha was in present in market with one product (two-wheeler finance) concentrated in one geographic market (that was central India) and operating in one niche market segment (BoP). If competitors were to enter the LokSuvidha market segment, the market dynamics would get altered most possibly in an unfavourable manner. Rather than a market crisis drive, the startegy of LokSuvidha, it would be more desirable that LokSuvidha decided its future strategic path. LokSuvidha had been succesful in implementing digital technologies to serve BOP (Verma & Bhattacharyya, 2016). LokSuvidha being a small and medium enterprises had its own share of resource and capability constraints (Bhattacharyya & Jha, 2015 ). Technology, skilled manpower and competitive business process capabilities coupled with the innovative business model had aided LokSuvidha in its journey.

Nimish and Kamlesh, based upon this context, were contemplating what should be the next strategic step for LokSuvidha. Should LokSuvidha expand its product market offerings or should it concentrate on only two-wheeler loans? Another thought that was resident in their minds was that should LokSuvidha expand the market by reaching new geographies. However, they pondered that it would be challenging for LokSuvidha to expand into new geographies. This would be because it would stretch the organizational resource and capabilities base, specially the human resources of LokSuvidha. Expansion of product service porfolio would not only challenge the human resources of LokSuvidha but also the extant technology resources of LokSuvidha. This would be because the technologies applied at both the front and back ends need to be expanded to accommodate specific requirements of other offerings. The more expanded the stretching of capabilities, the more challenging would be the achivement of competitive success. Any business venture needs to have sustained competitive position in the market as well as achieve growth over the years. In the minds of Nimish and Kamlesh, thoughts were criss-crossing on how they could further grow this business. Could the growth be achieved in scale or in scope? They were contemplating regarding what specific organizational capabilities would they require to fuel LokSuvidha to enter the next orbit either as scaling or scoping?

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.