Abstract

This article examines critical issues, funding desiderata and strategic policy options for financing social development to fulfil the United Nations (UN) Sustainable Development Goals (SDGs). Despite global commitments, financing remains insufficient and continues to focus on particular SDGs, with the COVID-19 pandemic exacerbating disparities. Drawing on recent data, including the 2024 UN Financing for Sustainable Development Report, and contemporary literature, the study reveals that progress is notably diverging from targets. It explores SDG financing strategies, including socially responsible investments, and suggests reforms to fiscal policy and global financial governance. Financing, particularly in the Global South, underscores systemic weaknesses in the international social development financing architecture. The study calls for institutional capacity building and cooperative, equitable and culturally sensitive and solidaristic financing strategies at the global and national levels to expedite social development.

Keywords

Introduction

Financing social development poses a complex challenge that involves mobilising adequate, equitable and sustainable financial resources to support the universal achievement of the United Nations (UN) Sustainable Development Goals (SDGs). However, there has been a significant ongoing funding shortfall in meeting the SDGs. The COVID-19 pandemic further exacerbated this gap, as countries redirected resources towards emergency health responses and economic recovery, often at the expense of longer-term development investments (OECD, 2020).

Based on the Financing for Sustainable Development Report 2024 (United Nations, 2024a), countries remain significantly off track in achieving the 2030 Agenda for Sustainable Development, with around half of the 140 SDG targets for which data is available diverging from required trajectories. Nearly 600 million people are projected to remain in extreme poverty by 2030, and progress on climate action is alarmingly inadequate, as global emissions continue to rise despite urgent calls for deep reductions.

The financing gap for SDGs and climate action runs into trillions of dollars annually, disproportionately affecting developing countries with higher capital costs and more restrictive financing terms. Systemic challenges—including climate risks, financial volatility and rising inequality—strain national financing systems and expose the weaknesses of the current global financial architecture. A shift in macroeconomic conditions has caused average gross domestic product (GDP) growth in developing countries to slow to just over 4% between 2021 and 2025, down from 6% before the 2009 financial crisis (United Nations, 2024a).

The increasing global fragmentation and structural shifts in the world economy necessitate new approaches to growth and development. In response to these complex challenges, the upcoming Fourth International Conference on Financing for Development (FfD4), to be held in Spain from 30 June to 3 July 2025, along with the Second World Summit for Social Development scheduled for November 2025, carries an ambitious mandate to reform global financing systems and accelerate SDG implementation. To contribute to deliberations at these global fora, this article discusses key financing issues and gaps as well as financing strategies for social development.

Key Financing Issues and Gaps

Financing Gaps

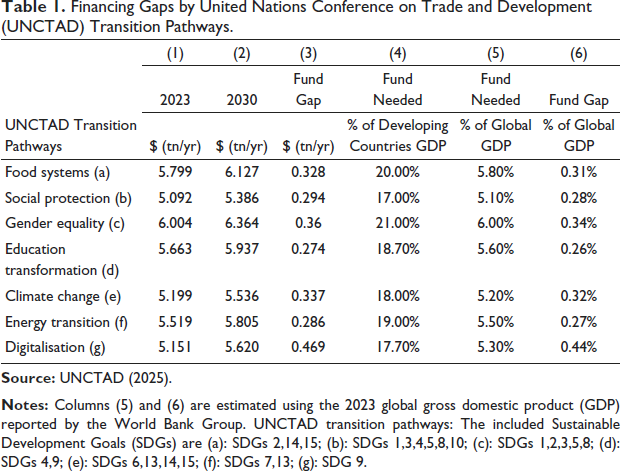

Table 1 summarises the financing gaps categorised by SDG ‘transition pathways’ according to the UN Conference on Trade and Development (UNCTAD) (UNCTAD, 2025). The UNCTAD summary table compiles data from 48 developing economies, representing 68% of the population in these regions. The database was developed in partnership with many international agencies, including the International Monetary Fund (IMF), the International Labour Organization (ILO), the Economic and Social Commission for Western Asia (ESCWA) and the United Nations Environment Programme (UNEP).

Financing Gaps by United Nations Conference on Trade and Development (UNCTAD) Transition Pathways.

Columns 1 and 2 present the estimated funding costs for UNCTAD pathways in 2023 and 2030. In column 3, the financing gaps estimated in 2023 range from $274 billion to $469 billion per year, falling short of meeting the 2030 SDG Agenda. As shown in column 4, the funding amounts needed by 2030 represent 17%–21% of the total GDP of developing countries. For the least developed countries, the share of financing can be as high as 45% of their GDP for the social protection pathway. However, as shown in column 5, the share of financing needed reduces to 6% or less of GDP when the burden is shared with the rest of the world. When global investors fill the financing gaps, these proportions are less than 0.5% of global GDP, as shown in column 6. This highlights the importance of international partnerships and the pressing need for global interventions and commitments from various private and public entities to fulfil the 2030 SDGs. Furthermore, as noted in the UNCTAD (2024) report, any delay in SDG funding support will increase the funding costs needed to achieve the 2030 goals, while reducing the likelihood of attaining these goals.

Inadequate and Mixed-motivated Official Development Assistance (ODA)

While ODA remains a key external funding source, its allocation is often volatile, insufficient and motivated by mixed interests (Pawar, 2025), failing to address the full scope of social development needs. Additionally, donor conditionalities often undermine national ownership and long-term planning (Browne, 2006; Hujo & McClanahan, 2009; Ortiz, 2009; SDG Action, 2024). Folarin and Raifu (2023) also suggest that ODA contributes to making recipient countries dependent on donors, as it lowers taxes and negatively impacts domestic revenue mobilisation. Therefore, ensuring accountability and aligning ODA with national development priorities remain a challenge (United Nations, 2015).

ODAs come from bilateral (sovereign governments) and multilateral partners (multiple countries acting jointly). Multilateral partners, often referred to as international organisations [e.g., the Organisation for Economic Co-operation and Development (OECD)], contribute approximately one-third of ODA (Nielson et al., 2017). Despite their different interests, multilateral institutions ‘aggregate the preferences and resources of multiple member states in the pursuit of a collective policy’ (p. 157). Member governments may negotiate for compromises and agree on shared policies, which alter their motivation compared to the case in bilateral aid. The impact of differences in policy motivation is also often worsened when recipients’ national development priorities are inconsistent with donor conditions and interests.

Significant Disparities in Socially Responsible Investment (SRI)

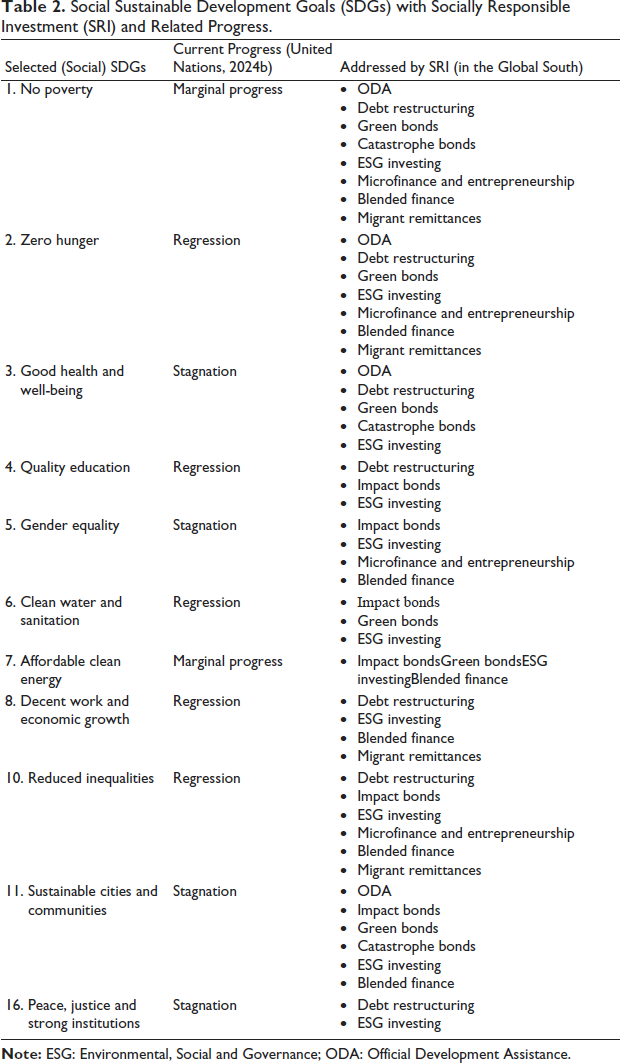

SRI has increasingly addressed specific UN SDGs (Barua, 2020). Research by Folqué et al. (2021) demonstrates that while SRIs broadly aim for sustainability, their alignment with individual SDGs varies significantly. They often focus more on environmental and governance dimensions than on all the SDGs. This creates a funding gap for the other SDGs and raises questions about how to effectively and specifically attract and direct funding for all the social development goals. Table 2 shows that despite a range of funding under SRI, several SDGs have not progressed but rather regressed, indicating that SRIs are inadequate or do not meet the needs. Current SRI strategies closely align with SDG 3 (good health and well-being) primarily due to their measurable returns and defined investment vehicles (Global Sustainable Investment Alliance, 2020). In contrast, goals 2 (zero hunger), 6 (clean water and sanitation), and 16 (peace, justice and strong institutions) are still insufficiently addressed, attributed to higher perceived investment risks and uncertain returns (PRI, 2019). These financing differences reveal significant disparities where SRI strategies could see notable enhancements.

Social Sustainable Development Goals (SDGs) with Socially Responsible Investment (SRI) and Related Progress.

Lack of Institutional Capacity, Accountability and Domestic Resource Mobilisation

There is increasing agreement on the necessity of transitioning towards more sustainable domestic resource mobilisation approaches, such as progressive taxation and minimising illicit financial flows (United Nations, 2019). However, successfully implementing these strategies demands substantial institutional capacity and political resolve, which may be insufficient in certain regions. In low- and middle-income countries (LMICs), limited fiscal capacity is common, characterised by narrow tax bases, inefficient tax collection methods and high levels of economic informality (Gaspar et al., 2016). Consequently, their ability to generate adequate domestic resources for social investment is severely limited. Poor public financial management practices and corruption often result in the ineffective allocation and loss of funds designated for social development (Bawole & Adjei-Bamfo, 2020; Transparency International, 2024; United Nations, 2024a).

Servicing the Public Debt

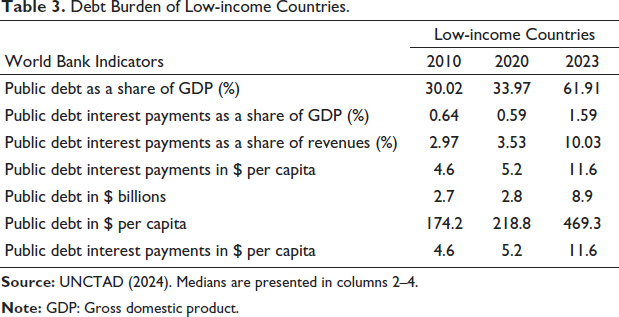

One of the central issues in financing for social development is the burden of public debt. Many LMICs are encumbered by high debt servicing costs, leaving limited fiscal space for investments in education, health or social protection (United Nations, 2025).

According to the 2024 UNCTAD Report on world debt, low-income countries have taken on increasing amounts of debt since 2010. As illustrated in Table 3, in 2023, these countries reported a median of nearly $9 billion in public debt, representing an increase of more than 200% [(8.9/2.8–1)×100%] since 2020. The 2023 total interest payment amounted to 1.6% of the GDP, representing an increase of 2.5 times since 2010, while the size of public debt tripled over the same period. Such an alarming trend would compromise future debt borrowing capacity while raising concerns about escalating default risks arising from debt instruments issued by these countries.

Debt Burden of Low-income Countries.

Underdeveloped Financial and Capital Markets

Meanwhile, technological disruption and digitalisation are reshaping all areas of finance, while financial and capital markets in many low-income nations remain underdeveloped, limiting long-term investment. Misaligned incentives continue channelling resources into environmentally harmful activities, and both public and private finance are not yet sufficiently aligned with the SDGs.

A key contributor to underdevelopment is the absence of a strong financial infrastructure. Numerous emerging markets encounter issues like ineffective legal systems, excessive regulation, and government lending that competes with private sector efforts (Gamkrelidze, 2019). These imperfections obstruct the effective distribution of resources and restrict financial markets’ capacity to foster long-term investment. Moreover, the concentration of global capital markets, primarily controlled by high-income nations, intensifies this inequality. For example, the United States alone accounts for almost 55% of the global equity market (Adrian, 2025). Therefore, it is essential to better align financial flows with SDGs (UNCTAD, 2024).

Declining Global Foreign Direct Investment

According to the World Investment Report 2024 (UNCTAD, 2024), global Foreign Direct Investment (FDI) declined by 2% to $1.3 trillion in 2023, a drop that exceeds 10% when excluding volatile flows through a few European conduit economies. The downturn reflects broader challenges, including economic slowdowns, geopolitical tensions, protectionism and fragmented global trade and regulatory systems, which are disrupting investment flows and supply chains. Particularly concerning is the over 10% decline in international project finance—especially in sectors tied to the SDGs, such as agrifood, water and sanitation—threatening progress towards the 2030 Agenda. Tight financing conditions further compound the issue, contributing to a 26% fall in project finance critical for infrastructure and renewable energy (UNCTAD, 2024). While some manufacturing sectors, like automotive and electronics, attracted investment in market-accessible regions, many developing countries remain excluded. Although sustainable finance products continue to grow, their pace has slowed, with sustainable investment fund inflows plunging by 60% in 2023 (UNCTAD, 2024).

Low and Inconsistent Contributions from the Private Sector

Besides financing arrangements, the private sector plays a critical role in advancing the SDGs. Berrone et al. (2019) argue that a long-term partnership between the private and public sectors is essential in addressing the financial gap required to provide public goods and services, particularly for developing countries. Using the life cycle approach, Stewart et al. (2018) highlight the global role of companies in ensuring sustainable development and consumption under SDG 12. For social development, it is essential to explore financing options that extend beyond domestic markets and include international funding, especially for the Global South.

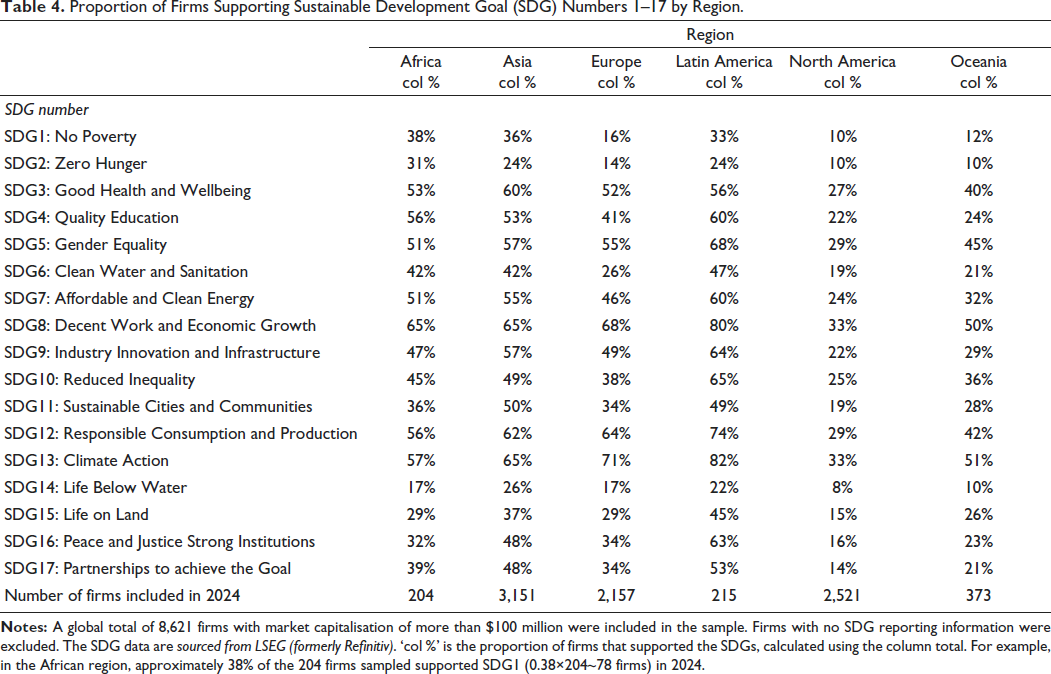

To better understand firms’ role in supporting the attainment of SDGs, we examined the data from LSEG (formerly known as Refinitiv). In Table 4, a global total of 8,621 firms from different industries were sampled. To ensure the selected firms are reasonably large and mature, we included only firms with a market capitalisation of more than $100 million in our analysis. Firms with no SDG reporting information were excluded. In columns 2–7 of Table 4, the proportion of firms that supported the SDGs was calculated using the column total. For example, in the African region, approximately 38% of the 204 firms supported SDG 1 (0.38×204~78 firms) in 2024. Notably, support for no poverty (SDG 1) and zero hunger (SDG 2) for Europe, North America and Oceania is 16% or less, sharply contrasting with the corresponding SDG proportions reported for Africa, Asia and Latin America. These regions typically consist of the Global South countries. However, SDG support from Europe, North America and Oceania is as high as 52% for good health and well-being (SDG 3) and 55% for gender equality (SDG 5). Overall, these observations imply that private sector contributions are low and inconsistent. Firms in the Global North devoted less attention to key social goals such as SDG 1 and SDG 2.

Proportion of Firms Supporting Sustainable Development Goal (SDG) Numbers 1–17 by Region.

Strategic Policy Options and Instruments for Financing Social Development

As noted by Thomas (2025), the 2015 Addis Ababa Action Agenda (United Nations, 2015) blueprint highlights the importance of necessary financial resources for ‘reducing social, environmental and economic vulnerabilities…’ and ‘the need for the coherence of developmental and humanitarian finance…’ (p. 32). While the UN’s 17 SDG goals are intended for all nations by 2030, developing countries (mainly the Global South) are generally lagging far behind developed countries (the Global North) in some respects due to a general lack of financial resources. Furthermore, some developing countries are experiencing far more social issues, such as poverty, inequity, armed conflicts and poor governance structures. While developed countries are mostly capable of self-financing their social goals, developing countries need to rely on donors, international agencies, private sectors and foreign and domestic governments to fulfil the SDG goals (Barua, 2020).

Realising the UN SDGs by 2030 heavily relies on bridging ongoing financing gaps in social development. Yet, even with a global agreement on the need for investment in these fields, existing financial structures and their limitations continue to pose a significant obstacle. The United Nations (2024c) estimates a global annual shortfall of approximately $4 trillion in SDG-related financing, much of which pertains to the social sector. Addressing these gaps through global and national fiscal policies is essential for creating equitable, resilient and sustainable societies. This section discusses various strategic approaches aimed at informing policy actions related to financing.

Domestic Resource Mobilisation

It is essential to enhance domestic resource mobilisation. This includes reforming tax policies for greater equity and improving the efficiency of tax collection (IMF, 2021). Additionally, measures to combat illicit financial flows can help to retain resources within national borders. Another strategy is to utilise blended finance (further discussed later), which merges concessional finance with private capital to support social development. Therefore, enhancing institutional capacity and encouraging participatory budgeting alongside accountability mechanisms are essential for boosting the effectiveness and fairness of social spending. Furthermore, fostering public–private partnerships can leverage additional domestic resources and expertise, while promoting transparency and good governance ensure that funds are used efficiently and reach those most in need. By integrating these approaches, countries can create a more sustainable and inclusive financial system that supports long-term social development goals.

ODA

Aid through ODA offers significant opportunities for funding social development in the Global South (Folarin & Raifu, 2023; Nielson et al., 2017). ODA is a development aid extended to governments of developing countries by developed countries (often members of the OECD). These development aids are usually given as a grant or a loan, with a component of it being a grant targeted at particular projects and providing expert and technical support towards promoting economic growth and improving efforts to achieve the imminent SDGs in developing countries. As Pawar (2025) noted in this issue, such aid needs to be free from vested interests and fully benefit the recipient countries. However, development assistance from international organisations, such as the UN agencies, is provided as grants, and recipient countries do not have to repay them (Nielson et al., 2017).

Developing countries may therefore finance their social SDGs by building relationships through agreements and treaties with their bilateral development partners (individual countries) and multilateral partners (e.g., the UN, World Bank, European Union). According to the OECD (2024), the total ODA in 2021 constituted about $152.9 billion, of which $63.8 billion was received by Africa and $39.5 billion by Asia, Latin America and the Caribbean. While strong evidence suggests that ODA creates welfare benefits, this assistance may crowd out domestic revenue mobilisation in Global South countries, leading to aid dependency (Folarin & Raifu, 2023). Folarin and Raifu, therefore, recommend that ODA should be targeted at strengthening the tax system and administration to promote domestic revenue mobilisation. Also, considering the recent funding cuts by the United States affecting the UN and ODA funding, there is a need for developing countries to explore alternative funding sources beyond ODA and diversify their funding of SDGs (Folarin & Raifu, 2023; Janus et al., 2015). In the spirit of international solidarity, many developed countries need to meet their ODA target of 0.7% of their gross national income.

Debt Restructuring

The majority of developing countries are saddled with huge debts from ODAs. They often prefer investors to use debt restructuring to absorb these losses (Biglaiser & McGauvran, 2021). Through debt restructuring, investors, such as the International Development Partners (IDPs), may prescribe various restructuring measures to governments of indebted countries. These measures often include cutting government spending, freezing public sector employment, lowering income inequalities through tax reforms, social spending and enhancing services for poorer constituents. There have been growing calls for international debt relief and restructuring to create room for countries to invest in long-term development.

Debt restructuring aims to provide indebted countries with the opportunity to lower their debt costs in the short term and reduce the potential for debt crises. However, Biglaiser and McGauvran (2021) found that governments of developing countries undergoing debt restructuring chose to lower social spending and reduce taxes in favour of the wealthy, to the detriment of poor and lower-income groups in society. These fiscal strategies tend to worsen income inequality (Biglaiser & McGauvran, 2021). It is understood that IDPs, such as the IMF and the World Bank, may exert pressure through some specific austerity measures. Governments concerned with financing their SDGs may, however, negotiate fiscal restraint strategies and implement debt restructuring to secure adequate funding for the SDGs. From an ethical perspective, such negotiations need to be just, fair and reasonable on recipient countries.

Impact Bonds (IBs)

IBs provide a diverse source of funding for social development. IBs are responsible investments that reward social and environmental outcomes (i.e., impact) beyond mere outputs based on measurable impact while generating financial returns (Trotta, 2024). IB investors intentionally seek to make a positive difference through their investments, aiming for financial gains and positive outcomes for society and the planet. IBs deploy the much-needed capital to address critical environmental and social global challenges while simultaneously achieving financial goals.

IBs are prevalent in the Global North and are emerging as an innovative way to finance social development challenges in the Global South, as IBs are generally attractive to investors (Mishra & Dash, 2023). However, there is significant inequality because only about 10% of the global IBs are related to projects in the Global South (World Bank, 2022). IBs constitute both environmental impact bonds (EIBs) and social impact bonds (SIBs). Given the focus of the social development funding for this study, we concentrate on SIBs. They are performance-based contracts that governments use to invite investors to finance projects with designed, measurable social outcomes for targeted social groups. The performance of service providers (i.e., for-/nonprofits and social enterprises) is monitored and evaluated by independent evaluators against the measurable social impacts. Governments then pay investors their initial investment plus a return if impact targets are realised (Jackson & Harji, 2014). However, investors do not receive all their investment back if impact targets are unmet. This explains why SIBs are sometimes referred to as ‘Social Benefit Bonds’ in Australia and ‘Pay for Success’ in the United States (Mishra & Dash, 2023, p. 23). With SIBs, the risk to the government and the service providers is rolled over to investors, providing investor capital protection and guarantee mechanisms with termination clauses.

Green Bonds

Green bonds are a range of climate financing that may also be used to finance the other SDGs, which are largely affected by climate change. This option involves a ‘fixed-income product’ designed to raise capital from investors to fund environmental projects (Mishra et al., 2023, p. 128). However, since some environmental projects related to water and sanitation and providing affordable renewable energy have direct social development implications, green bonds may be considered for financing the SDGs, such as 1, 2, 3, 6 and 7.

Government organisations or corporations issue these green bonds following national green bond criteria, often based on the Green Bond Principles developed by the International Capital Markets Association (ICMA). Interested investors concerned with relevant projects or initiatives lend the government their money by buying the green bonds. The capital raised is then used to fund projects. In Ghana, for instance, the Securities and Exchange Commission (SEC) is responsible for regulating the issuance and management of green bonds through its Green Bond Guidelines 2024 (SEC, 2024).

The global market for these green bonds almost doubled from $596 billion in 2020 to $1.1 trillion in 2021 (Mishra et al., 2023). For example, the International Finance Corporation (IFC) invested $30 million through green bonds towards the production of 25,767 MWh of clean power annually and water access for Ghanaian manufacturing firms (IFC, 2022). The World Bank, through a $14 million investment, also supports two plastic waste collection and recycling stations in Ghana (World Bank, 2024b). While green bonds are attractive to individual private investors, they also appeal to IDPs.

Catastrophe Bonds

Catastrophe bonds are insurance-linked securities used to cover the costliest catastrophe events (Braun & Kousky, 2021; Makariou et al., 2021), such as severe storms (i.e., cyclones and tornadoes) and earthquakes, that may significantly impact society, displace people and disrupt communities. For example, these bonds are used by insurance companies to reinsure by transferring the risk of major disasters to investors. They share this risk by spreading the risk of loss between themselves and investors who gain profit in case the event does not happen (Braun & Kousky, 2021).

Considering the major risks of investors losing all their principal should a determined disaster occur before bond maturity, the yields from this financial instrument are also often higher. Thus, investors benefit from both (a) floating returns payments from low-volatile securities that special-purpose vehicle entities, which are bankruptcy-remote, invest their principal, and (b) premium payments for bearing the catastrophe risk. The sponsor sets up the special purpose vehicle entities (i.e., initial insurer or insurance company) and has legal authority to represent the insurer and protect both parties from each party’s credit default risk (Braun & Kousky, 2021).

Hence, catastrophe bonds help alleviate the financial repercussions of natural disasters, thereby advancing the UN SDGs by enhancing resilient infrastructure, minimising economic losses and nurturing sustainable communities. Moreover, they support social SDGs by safeguarding at-risk populations, guaranteeing access to essential services and encouraging inclusive and sustainable economic development.

Environmental, Social and Governance (ESG) Investing

In recent years, the growing corporate conscience among business practitioners and policymakers has heightened their focus on sustainability issues. They recognise that ESG activities are crucial in benefiting corporations and all stakeholders (e.g., Business Roundtable, 2019; Harrison et al., 2020; McKinsey & Company, 2020; UN SSE, 2015). Notably, studies have explored and demonstrated the predominantly positive relationship between ESG investment activities and various financial aspects of companies, including corporate financial performance and stock returns (Lisin et al., 2022).

Companies that integrate an ESG strategy position themselves for long-term success, profitability and value creation that benefits shareholders (Eccles & Klimenko, 2019). ESG-oriented firms often demonstrate effective governance, fewer environmental regulatory issues, reduced earnings volatility and improved access to capital at a lower cost (Kumar, 2020; Lisin et al., 2022; Raimo et al., 2021; Wong & Neher, 2024). Research has also highlighted that incorporating ESG considerations into a corporation’s valuation model positively impacts non-financial indicators, such as consumer satisfaction, market acceptance and societal values (Mohammad & Wasiuzzaman, 2021; Wong & Neher, 2025). At the same time, ESG-guided investment minimises investment risks (Henisz et al., 2019). Governments of LMICs may, therefore, develop frameworks to regulate the ESG investment environment to align activities of both multinational and local firms with the imminent social SDGs.

Microfinance and Entrepreneurship

Microfinance presents another form of financial arrangement for funding social SDGs, such as eliminating abject poverty (Newman et al., 2017; Singh et al., 2022). It continues to attract growing interest for its success in enhancing the lives of low-income families since its emergence in Bangladesh during the 1970s (Newman et al., 2017). Governments may create a conducive institutional environment for microfinance and services, including microcredit loans, insurance and savings, to support local livelihoods and entrepreneurial activities of the million poor households currently underserved by existing traditional banks (Newman et al., 2017). These poor households often lack the capacity and, therefore, are unable to provide the required collateral to traditional banks.

While this situation negatively impacts entrepreneurship, it also keeps small business owners in a cycle of debt (Newman et al., 2017; Singh et al., 2022). Microfinance offers poor households and small business owners access to capital (i.e., small loans), helps them break away from the cycle of debt and improves their living standards. Considering its significance to financing social development, the need for a favourable formal and informal institutional environment cannot be overemphasised (Nair & Njolomole, 2020). Such conducive institutional environments could minimise uncertainty, reduce transaction costs and increase resource flow through the microfinance market for productive entrepreneurial activities and growth (Nair & Njolomole, 2020; Singh et al., 2022). Although it is commonly associated with developing countries, microfinance is also beginning to gain attention in developed countries, where it is used to subsidise the running costs of nonprofits and social enterprises (Pedrini et al., 2016).

Blended Finance

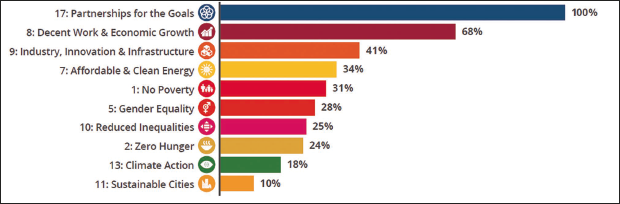

Blended finance also provides an opportunity to attract and leverage public/philanthropic capital to increase private investment for financing social development projects, such as renewable energy, infrastructure and social SDGs in developing countries. These projects are less risky and may not necessarily be economically viable but have implications for generating significant social development outcomes. This concessional capital is diverse in nature, with guarantees that reduce perceived risks for investors. Blended finance is usually managed by governments, international organisations and nonprofit organisations to catalyse development projects. Alternatively, bilateral and multilateral development institutions (e.g., World Bank), commercial banks, pension and insurance firms, asset managers, corporations, and individual institutional and impact investors may also use blended finance for commercial projects (Dembele et al., 2022). Convergence (2024), a global network aimed at increasing private investment in emerging markets in developing countries to promote the attainment of SDGs, reports that the total blended finance in 2023 grew to $15 billion. However, 2023 observed a 25% decrease in deal closures compared to 2022 (Convergence, 2024). The report (p. 13) adds that between 2014 and 2023, blended finance has been used to fund projects related to different social SDGs (see Figure 1).

The partnership between Global Financing Facility (IBRD, 2020) and IFC was created through blended finance in 2020 to ‘de-risk’ investments to help partner countries improve the health and rights of women, children and adolescents related issues, thus addressing the social SDGs. From the perspective of an individual investor, the main investment barriers are perceived investment risk and poor returns relative to comparable investments (Convergence, 2025).

Migrant Remittances

Besides the various financing sources recommended for realising the social SDGs, there has been a growing interest in how migrant remittances are also contributing to social development outcomes, such as reducing inequality (Malecki, 2021) and alleviating poverty (Ojeyinka & Ibukun, 2024). World Bank data suggest that remittance flows to LMICs stood at $627 billion in 2023, almost equivalent to the combined amount of ODA and foreign direct investment (World Bank, 2025). This high remittance data are facilitated by the continued increase in international migration, which was estimated at 302 million in 2023. Germany, Russia, the United States, Saudi Arabia and the United Kingdom were among the top destination countries for most international migrants from the Global South (World Bank, 2024a).

Recent studies (de Haas, 2009; Ojeyinka & Ibukun, 2024; Saud et al., 2024) indicate that migrant remittances may provide an alternative pathway through external financing of social development challenges, such as alleviating household poverty in LMICs. However, this effect may be adversely affected by two factors: remittance costs and the lack of a conducive environment for channelling remittance proceeds into productive ventures (Ojeyinka & Ibukun, 2024). While the SDG target for remittance cost is 3% by 2030, the current remittance cost is more than twice that (World Bank, 2024a). Policymakers and governments from LMICs may liaise with destination countries to reduce remittance costs and remove unnecessary legal and institutional barriers to encourage the use of formal financial mediums by remitters. Where formal and official financial channels are utilised, policymakers can establish conducive frameworks for remittance–recipient households to channel their remittance inflows into productive ventures, such as micro-businesses and entrepreneurship, rather than into mere consumption activities (Ojeyinka & Ibukun, 2024). As most migrants provide critical services, politicians should stop using them for political purposes, as they contribute to the economy both in their origin and destination countries.

Strategic Financing Policy Options and Social SDGs

In summary, we propose ten strategic policy options that focus on financing social SDGs. These options feature distinct motivations, risk levels and return margins designed to attract investors who seek to promote social SDGs. They include both domestic and external/international resource mobilisation options, such as strategically structuring the use of migrant remittances, ODAs, debt restructuring and microfinance. Increasing remittances to recipient countries in the Global South could help mitigate income inequalities, poverty and hunger. Additionally, it could provide capital for entrepreneurial activities for low-income families lacking decent work or adequate livelihoods. Aligning debt restructuring and ODAs with national social development priorities should emphasise building capacity to self-finance social goals beyond aid and avoid creating dependency in recipients. These financing options may contribute to enhancing quality education, providing good health and reducing inequalities in the long term. Strengthening the tax system and effectively administering it could help mobilise domestic revenues that could be used to promote entrepreneurship through microcredits. Climate financing, such as green and catastrophe bonds, is another vital source for addressing social development challenges. Although environmentally focused, they often provide funding to mitigate and adapt to the negative social impacts (i.e., poverty, hunger and well-being) caused by climate change. Finally, impact investing through IBs, ESG investing and blended finance has also proven beneficial for addressing all eleven social SDGs outlined in Table 2.

Conclusion

The stagnation and regression in the advancement of the SDGs, coupled with funding shortages, highlight the necessity of evaluating current and alternative financing policies for social development. This article discusses key financial issues and gaps, as well as several national and international strategic options for mobilising financial resources. The analysis clearly reveals a significant funding gap at the national level, whereas at the global level, it is less than 0.5% of the GDP, according to the selected SDGs. This situation calls for global solidarity, partnership and cooperation on one hand, and domestic efforts to efficiently and effectively mobilise local resources on the other. The proposed alternative models for sustainable financing may further address shared challenges facing the global community, including climate change, disaster financial risk protection and global health concerns. Policymakers and stakeholders must consider cultural differences, institutional capacities, existing and potential geopolitical tensions and diplomatic relationships when selecting from the discussed policy options and alternative models. While the suggested financing options are relevant and need to be scaled up, substantial financial arrangements and infrastructure reforms are also essential to make them just, fair and participatory for both recipient and donor countries. Considering this, our study is limited by the absence of information on the consequences of the emerging changes in the US trade tariff regime and the sudden withdrawal of US aid, as it is too early to assess these effects. Additionally, a lack of adequate financing is merely one of the barriers to achieving the SDGs. Therefore, beyond financial barriers, other obstacles and gaps as highlighted in this special issue also need to be addressed.

Data Availability Statement

This article is based on secondary data. All material used is included in the reference list.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Approval and Informed Consent

There are no human participants in this article, and informed consent is not required.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.