Abstract

The economic and social consequences of reliance on informal finance are enormous in the case of socially and economically disadvantaged people like the tribal communities. These communities have become more financially vulnerable due to the severe barriers in accessing institutionalised formal finance. Drawing on data collected from 246 randomly chosen households from four tribal communities (Kurichya, Kuruma, Adiya and Paniya) in the Wayanad district of Kerala, and using mixed-method approach, the study seeks to examine the repercussions of reliance on informal source of finance by the tribal communities. The study reveals that the agents of informal financiers also resort to social demoralising and mental harassment towards the tribal households. The study shows that tribal households may not be aware of compounding effect of interest rates when they avail credit from any source of finance, especially informal finance. This in turn increases the indebtedness among the tribal communities. All these call for the need of tailoring institutional (formal) credit solutions suitable to the credit needs and socio-economic conditions of the weaker segments of the society like the tribal communities. The study suggests adopting supply-side cum demand-side strategies.

Keywords

Introduction

Finance has a prime role to play in the present-day monetised exchange economy where it is not easy for an economic agent to effectively function without access to adequate, reliable and affordable financial resources. For the low-income, socially and economically disadvantaged groups such as the tribes, Dalits and unemployed women, access to convenient and affordable finance becomes even more precarious as formal financial channels like the banks appear to be averse to offer financial services in quick response to their demand (Basu, 2006). Due to inadequate access to formal finance, the poor and the low-income people like the tribes often seek informal sources of finance as the last resort (Kumar, 2013). The high dependence on informal sources of finance bears the risk of making them trapped in a vicious circle of indebtedness, creating untoward consequences on their economic and social conditions (Akanji, 2021). Informal finance pushes their clients, mainly the poor into a vicious circle of debt trap, and often ties them to the suppliers of informal finance. Despite several steps taken by the governments over the years to tackle the problem of dependence of people on informal credit, the problem still persists and has surged in recent times. Recent data from the Reserve Bank of India (RBI) and the National Sample Survey Organisation sheds light on the increasing reliance of people on informal sources of finance (Chavan, 2008). Against this background, the study examines the repercussions of dependence on informal sources of finance by the select tribal communities in the Wayanad District of Kerala, India.

Previous Studies

Innumerable studies have been conducted on tribal issues ranging from their anthropological aspects to issues pertaining to their financial access. To begin with, Vyas examined the socio-cultural and economic conditions of Baniyas of Rajasthan, Gujarat, Punjab and Haryana (Vyas, 1967). These states constitute prominent part of the Indian tribal community. He emphasised the difference in the socio-economic organisation of these tribes in different states. The study found the existence of wide disparity among these communities with respect to their socio-economic conditions and organisations. The socio-economic circumstances and the improvements made by the Santhals in Bihar were studied by Thakur in 1986 (Thakur, 1986). Thakur pointed out that tribes in India were at varying stages of development and were suffering from economic exploitation, social discrimination and political isolation. Kumar (1986) analysed the socio-cultural and economic aspects of Mal-Paharias tribal community and concluded that integration of these tribal communities with the mainstream would be possible only through necessary and effective institutional support. Delving into the economic life of tribal communities in Orissa, a state home to a large number of tribal people in India, Mohanthy (1989) emphasised the importance of tribal integration with the mainstream community.

In 1990, Thurston undertook a study on understanding the non-economic aspects of tribal communities in Kerala (Thurston, 1909). A similar attempt was made by Ayyappan (1965) to analyse the effectiveness of development schemes implemented by the government to enhance the living standard of the tribal communities in the state. The reliance of tribal households on moneylenders for quick or even meagre need for finance was examined by Murdia (1975). Rao (1978) emphasised that the land transfers to the non-tribal people by the tribal households involved the hidden hand of the profiteering moneylenders. Making a comparison of the tribes with the non-tribes in Andhra Pradesh, Balagopal (1989) opined that the possession of tribal land by ‘others’ should be tackled effectively to free the tribes from the clutches of indebtedness and other allied issues. Adding secondary evidence to this, Mohanty (2001) revealed that in the years since independence no commendable progress has been made in the possession of land by the tribal social groups in India.

Shah (1969) investigated the reasons that keep the tribal economy a subsistent one and the forms of informal lending. Further, highlighting the adverse consequence of overreliance on agriculture and the unwillingness of tribes to adapt to changing circumstances, Kumar (2001) analysed the widening inequality among the tribal families in the Nilgiris district of Tamil Nadu and attributed such inequality to their persistent dependence on the farm sector for employment. The study found that nearly about 90% of those depending on the farm sector were indebted to both formal and informal finance. Ramaiah (1981) in his study concluded that the possession of land by the tribes is an important determinant of their creditworthiness. Bhaskaran (2006) studied the Scheduled Tribal Cooperatives in the Wayanad district of Kerala to understand the progress attained by these institutions in materialising their objective of lending to the credit needy people, especially the tribes. Kunhaman (1980) in his study on the regional differences in the socio-economic advancement made by different tribal communities pointed out that the protective measures followed by the Travancore Kings had resulted in making the tribes in southern Kerala more progressive and outward-looking compared to their counterparts in the northern regions of the state. The intra-tribal variations in tribal development due to geographical reasons or location-specific factors have been brought out by Paul in 1989. Focusing on the Paniya tribes, Varghese (2010) addressed the issues that make the life of tribal communities cumbersome in Kerala. The study observed that landlessness is the central factor fuelling issues pertaining to the tribal communities in the state.

A report on the Human Development Index prepared by Cochin University of Science and Technology categorised tribal communities in Kerala into backward and forward tribal communities. Paniya and Adiya are the two backward tribal communities, and Kurichya and Kuruma are the two forward communities (Rajasenan, 2009). Paniya is classified as ‘Aborigines-Predial, slaves’ (Nair, 1911). History tells that Paniyars were bought and sold like commodities, and such trading used to take place at Valliyoorkav temple (Rajasenan, 2009). Kurichya, the community known for its martial tradition, occupies an important place among the tribes of Wayanad. Wayanad houses 70% of the Kurichya population in the state (Kumar, 2013). They are also said to have originated from the class of Nayars named ‘Theke Kari Nayar’ in the Travancore part of Kerala (Nair, 1911). Unlike the other tribal communities, they work as bonded labourers under the duress of non-tribal landlords. Kuruma occupies a unique place among the tribes of Wayanad. This dominant tribal community relies more on forests for their livelihood. Wood cutting and the procurement of minor forest produce are the chief occupations engaged by the Kuruma tribes (Thurston, 1909). In Kerala, approximately 95% of Kurumas live in the district of Wayanad. Like the Paniya, Adiyans are also bonded labourers who migrated to Wayanad from Coorg of the Mysore region. Because of this affinity to Mysore, they speak a hybrid language ‘between Canaries and Malayalam, more akin to Canaries’ (Nair, 1911). Tribes are the most socially and economically excluded segments of the population in India, and in the case of Kerala, they have been identified as the outliers of development (Shyjan & Sunitha, 2008).

Olipha and Sibindi (2022) studied the role of informal finance in filling the credit gap being confronted by small and medium enterprises. Informal finance has been widely used to fill the credit gap, especially in the micro-manufacturing sector. But still, notwithstanding these benefits, it is alleged that informal financial suppliers widely engulf in exploiting their clients by charging exorbitant interest rates. Madestam (2014) detailed out how formal and informal finance can either be complementary or substitutes in serving the credit requirement of recipients. Formal finance is endowed with enormous capital, whereas it lacks credible clarity in the disbursal or the use of the credit on account of information asymmetry in the credit market. On the contrary, informal finance knows how to disburse the credit but it is fraught with the issue of inadequate capital. The study also laments that the absence of adequate legislative measures results in the spawning of erroneous informal financial suppliers (Madestam, 2014). Another study examined the problem of financial vulnerability among the tribes in the Wayanad district of Kerala. The study revealed that the real financial vulnerability of people, especially the low-income and economically deprived communities like the tribes, stems from their incessant dependence on the informal sources of finance (Kumar, 2017).

Studies have shown that government-led self-help group (SHG) programmes enabling beneficiaries to have low-cost credit has had a remarkable impact on reducing the reliance on informal finance (Hoffmann et al., 2021). In the long run, it has substantial effect on enhancing the economic and social well-being of the beneficiaries. On the question of the livelihood of the tribes, studies show that forest dependency of tribes for resources still continues unabated. Particularly in the case of tribes who reside within the forest, the dependency on forest resources for employment and livelihood appears to be abysmally high (Soman & Anitha, 2020). Among some tribal communities in States like Andhra Pradesh and Telangana, 83% of households still depend on forest produce for their livelihood (Dev, 2020). It is evident that land alienation still continues to be an important cause for the economic and social impoverishment of tribal communities. Land alienation for a number of reasons has resulted in substantially reducing the livelihood opportunities of tribal communities (Madhava, 2019). Institutional vulnerability being faced by the tribes has been a burning issue in India over the years. Tribes have been evicted from their inhabitations in the name of extending the ‘reserve’ forests under Forest Acts of various kinds. This has increasingly pushed tribes into utmost misery depriving them of their traditional livelihood opportunities (Ganorkar, 2020).

The studies reviewed so far have not adequately focused on the plight of the tribal communities on account of their excess reliance on the informal finance. It is true that tribal households are poor in resources and lack remunerative employment opportunities. They languish in abject poverty despite the implementation of many schemes aiming at uplifting their lives. The poor access of tribal households to formal institutional finance has been a menace that makes them vulnerable at all times. The present study looks into this aspect of tribal life in detail.

Conceptual and Theoretical Framework

Both formal and informal finance coexist with each other. The approach of the people to each of these depends upon their financial behaviour, resources endowment and the financial structure of the society. Sometimes, people may regard informal finance as a substitute to formal finance and vice versa. For instance, for the tribal communities who were facing different barriers in accessing and using formal finance, informal finance may seem to be a suitable substitute. But, for socially and economically privileged communities, informal finance could be a complementary one in many instances. Looking at informal finance through the lens of the market, one needs to consider both the supply and demand dimensions. In the case of informal finance, supply dimension is often premised on the principle of information asymmetry and low transaction cost. As we know, local informal financiers, mainly the moneylenders have a relatively well-informed understanding about the credit-worthiness and behaviour of their potential borrowers which lead to narrowing down information asymmetries in the informal credit market. This information advantage primarily rests on the power of social relations and interactions that the lenders enjoy on account of their constant touch with their clients (Stiglitz, 1990).

Thus, the possession of superior credit information about the borrowers leads to lowering of verification costs, reducing moral hazard and adverse selection. In many ways, it is obvious that the lower transaction and verification costs may compensate at least a part of the relatively high interest rates that the informal lenders impose on their borrowers. Moreover, as the relation between the informal lender and borrower is bound by the social ties, this will mitigate many problems pertaining to the credit contract and default in repayment through the threats of social sanctions (Besley et al., 1993). On the demand side, it is theoretically argued that the demand for informal finance stems out of the rational (sometimes bounded rationality) choices of the borrowers. Rational choice predicts that while demanding the credit from whichever source, the borrower takes into account the cost of borrowing (Mujabi et al., 2021). A rational borrower is unlikely to demand the credit where the rate of interest is irrationally high. Nevertheless, it is often found that despite the exorbitant interest rates charged on the informal finance, low-income and socially disadvantaged people like the tribes may indulge in demanding such credit, a case of bounded rationality that often goes against what the rationality theory holds true (Kim, 2021). It is true that tribes generally demand quick and small finance which can meet their immediate requirements, regardless of the interest rates. That is why it is often articulated in literature that for the low-income and disadvantaged people, the demand for credit is interest inelastic.

Study Setting and the Methodology

This study is based on a mixed-method approach consisting of survey data and focus group discussions (FGDs). Combined cluster and proportionate random sampling methods were adopted to choose the sample. As the Manathawady and the surrounding places of Wayanad district are home to the majority of Kurichya and Paniya tribe households, samples of both communities were taken from these places, while sample households of Kuruma and Adiya tribes have been collected from Sultan Batheri. Since Nenmeni panchayat has the largest number of Paniya households, Paniya sample households have been chosen at random from the randomly chosen wards of this panchayat. Likewise, Adiya, Kurichya and Kuruma samples have been drawn from Thirunelli, Thavinjal and Meenagadi panchayats, respectively. Using stratified proportionate random sampling, a total of 246 (n = 246) sample households were chosen giving proportionate preference to each tribal community. Stratifications were made on the basis of the nature of the tribe households that come under the present study. The tribe-wise break-up of the sample includes Paniya—87, Kurichya—63, Kuruma—52 and Adiya—44. Kurichya and Paniya households were chosen from the Edavana and Panamaram grama panchayats, respectively. Ten participants were chosen at random from each tribe category for the purpose of forming the focus groups. The samples in FGD were selected in such a way that they were not related to each other. The interview data were collected in the month of November 2020 and FGD was conducted in the month of January 2021. A field survey using a structured and tested interview schedule was executed to obtain relevant responses from the participants of the study. Funnel approach to questioning, which commences with broad questions followed by more narrow questions on issues, was employed in FGD. FGD was also used to collect the information from four tribal communities. Participants were given codes, and note-taking method was used to record the reactions and opinion of participants in the FGD. The analysis involved descriptive statistics and constant comparison methods. First, the focus group data were grouped into small units and then each unit was given a code. In the second stage, these codes were put into different categories, and in the final stage, certain representative expressions were chosen to be presented and interpreted for the purpose of examining the situations.

Results

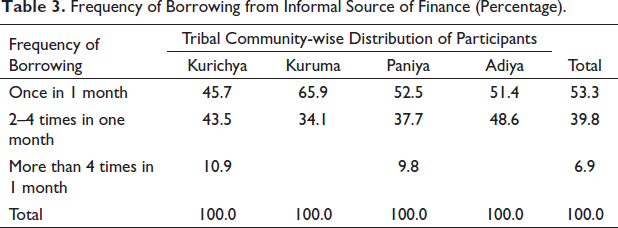

First, we look into certain socio-economic variables which are deemed important in taking the analysis ahead. As Table 1 itself vividly speaks of the status and nature of such socio-economic variables, it would be worthwhile to highlight some contrasting things which require some more interpretation. First of all, the employment status, type of house they live in, other sources of income and so on do not appear to be contradictory and thus deserve not much elaboration. Nevertheless, the distribution pertaining to the landholding speaks of some inbuilt contradictions. Tribal households being poor and economically backward do not own much land, and, being landless, it is true that their struggle for land continues to haunt the policymakers and rulers. In some cases, the government has provided at least five cents of land as mandatory for the tribal households. On account of this, the study clearly brings out that a relatively overwhelming percentage, that is, a little more than 68% tribal households hold five cents or less than five cents of land. It is interesting to note that 17.15% of households among tribal communities hold more than 25 cents of land (Table 1). Now, we turn to the crux of the analysis that is the question of not accessing formal finance by the tribal households.

Socio-economic Background of Participants.

Reason for Not Accessing Formal Finance

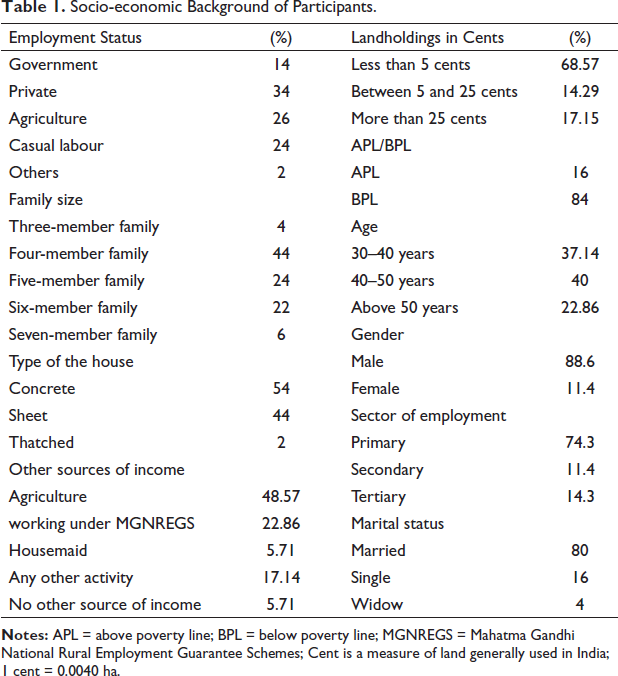

The majority of tribal households opine that they are not interested in approaching formal financial sources including banks for credit mainly because of an inherent fear of approaching banks (Figure 1). This fear in accessing banking services, especially in obtaining credit may be attributed to different reasons like lack of financial literacy and not possessing enough securities to offer for credit. But, at the same time, it is quite disheartening to note that a good percentage of tribal households feel that the procedural delay is a factor that keeps them away from accessing credit from banks. For Kuruma, Kurichya and Adiya tribals, the main reason for not accessing formal credit is the fear of approaching banks while for Paniya, it is the lack of sufficient security with the banking system.

Reasons for Not Accessing Formal Finance (Percentage).

The formality of informal financing might tempt tribal households to keep themselves away from accessing credit and financial services from such sources. That is why the fear of approaching banks has been suggested as the prime reason for not availing formal credit. Participant 207, a tribal woman hailing from Adiya, working as a housemaid says

We consider informal money lenders as more approachable irrespective of what repercussion it may bring in case of default in repayment. They are at our doorsteps to serve our needs at any time. Going to banks to see people sitting behind the glass is too much embarrassing for us. The language they speak; the terms they use…all are alien to us.

Undoubtedly, it calls for revamping the banking system, particularly rural banking, to cater to the specific needs of the clients. A quite universal banking practice and approach appear meaningless when it comes to banking with specific categories of people. Instead of directly financing such people, the banks can even ponder over refinancing legitimate credit unions or joint liability groups in an effort to disentangle the credit tie-up of people with the moneylenders and indigenous banks.

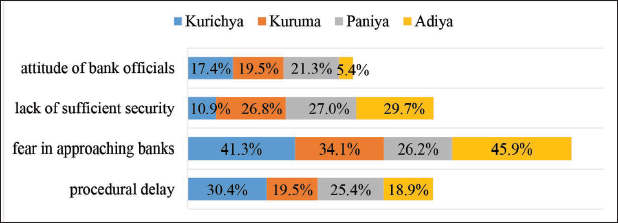

Sources of Informal Finance

The sources of informal finance include village moneylenders, native moneylenders and others belonging to the same village, those who hail from other states, friends, relatives and so on. It is important to note that relatives are the main source of informal finance for the tribes that come under this study (30.9%). While native village moneylenders are the second-largest source (20.7%), neighbours constitute 17.1% of households ‘finance sources’. Contractors are the least source of informal finance to the tribal households (Table 2).

Tribal Communities and the Sources of Informal Finance.

The tribal community-wise distribution of the sources of informal finance brings us interesting results (Table 2). The largest beneficiary of the native village moneylenders is the Kurichya tribe. This is because of the reputation that the Kurichya tribe enjoys, as it is a forward tribal community compared to the rest. Kuruma, another forward tribal community, also gets the largest credit from the native village moneylenders. On the other hand, it could be observed that most of the Paniya households seek credit from the other states’ village moneylenders. It is the Adiya tribe that comes in the first position as far as the credit from the friends is concerned. Thus, it is obvious that there is a wide disparity with respect to the tribal community-wise distribution of sources of informal fiancé.

Participant 79, hailing from a Paniya settlement colony sums up his experience as

Having defaulted several times, village money lenders avoid us. Hence, we seek money from other state moneylenders who charge high-interest rates and use physical force in case of repeated defaults. But, caught in severe debt trap, we have no option left. As we are constantly caught in this vicious circle, we have no escape…and are literally trapped in this system

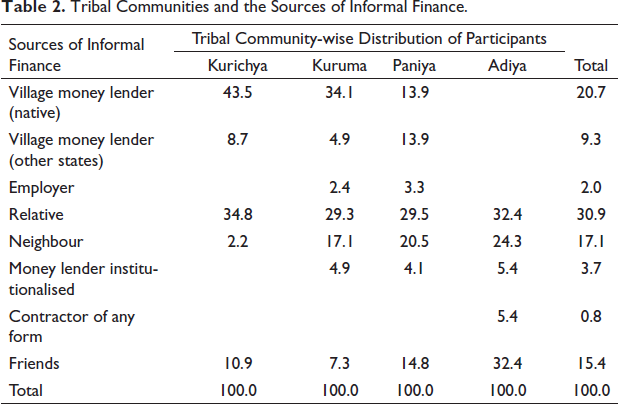

Frequency of Borrowing from Informal Source of Finance

As informal finance does not entail any procedures as it generally happens with formal banking, the clients of informal finance have a general tendency to engage in borrowing without any restrictions. It is seen from the data that 53.3% of tribal households borrow only once in one month, whereas only around 7% borrow more than four times in a month (Table 3). The data also indicate that 65.9% of Kuruma tribes and 52.5% of Paniya tribe households borrow only once in a month. It is important to note that Kurichya tribe (a forward tribal), borrow more than four times in a month. Kurichya could borrow more times as they are more credit-worthy owing to their status in the tribal system. It shows that the forward tribal communities which have a relatively high reputation have a higher frequency of access to credit from informal sources of finance.

Frequency of Borrowing from Informal Source of Finance (Percentage).

Repayment of Credit by the Tribal Households

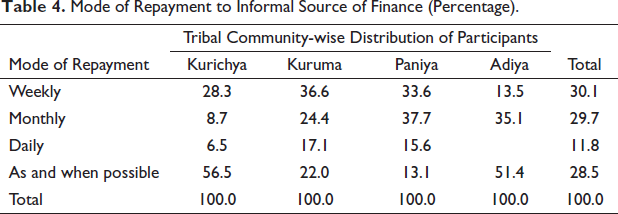

Tribal households make payments in cash as they do not use other modes of transaction. Majority of the tribal households repay their debt in weekly instalments (30.1%) and 29.7% in monthly instalments (Table 4). It is important to note that 28.5% of tribes repay loan whenever possible which implies that there is a clear possibility for default in repayment leading to exacerbation of financial vulnerability among the tribes. Looking at the tribal-wise distribution of the mode of repayment, the Paniya tribal community, a backward tribal community, uses both the weekly and monthly modes of repayment. But, in the case of Kurichya, 56.5% of households choose the ‘as and when possible’ option. This is possible for the Kurichya tribe as they enjoy being in the good books of the lenders.

Mode of Repayment to Informal Source of Finance (Percentage).

Need for Informal Finance

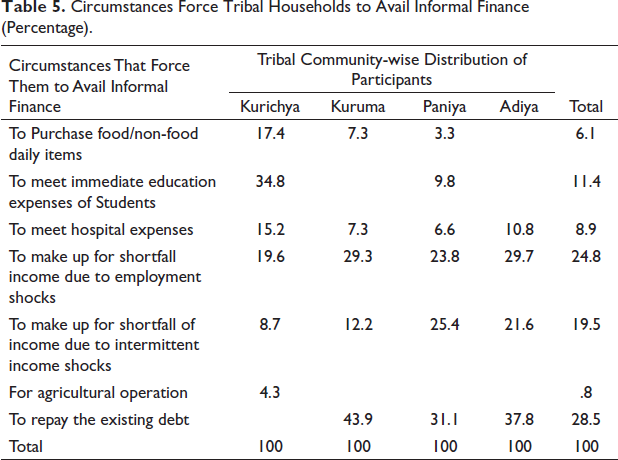

It is found that majority of tribal households (28.5%) rely on the informal source of credit mainly for repaying their existing debt, whereas 24.8% of tribal households seek informal credit to adjust for the occasional shortfall in income. It is reported that 11% of tribal households take credit from informal sources to meet the educational expenses of their children. Tribal community-wise distribution of the circumstances that force tribal households to avail of informal finance indicates that among the Kurichya tribal households, the largest demand for informal credit is for meeting education expenses, while among the Kuruma, it is for meeting the past debt obligations. Among the Paniya and Adiya, informal finance is sought mainly due to income and employment shocks, respectively (Table 5).

Circumstances Force Tribal Households to Avail Informal Finance (Percentage).

It is evident that as soon as anyone from the household falls ill or their income falls below their expectations, they tend to seek credit from other people. Their struggle to make both ends meet gets derailed when unexpected setbacks come their way. Hospitalisation and the loss of workdays due to illness were the major setbacks that added to the trials and tribulations of tribal life. Participant 92, a Kurichya tribal woman working as a helper in a vegetable processing shop says:

My family consisting of my bedridden husband, my in-laws and three children live on the meagre income which I get from this job. If I fall ill and am hospitalized for a while, our entire life will be derailed. We need help at this moment, and we do not seek credit to build mansions or to send our children for any professional degrees. If nothing caters to this tiny need for credit, development does not mean anything to us. For us, development means fulfilment of our daily requirements…nothing less nothing more

Consequences of the Dependence on Informal Finance

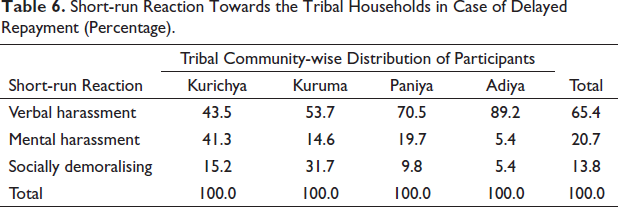

The repercussions of the excessive dependence on informal sources of finance turn out to be gruesome for all, irrespective of social and economic identities. People who access informal finance start facing problems when they are default on repayment. We first present the immediate repercussions in the event of credit not being repaid by the tribal households. It is understood that informal financial providers such as indigenous moneylenders use different tactics to pressurise their customers to repay loans with exorbitant interest. It is revealed from the study that most informal financial suppliers verbally abuse the customers who make default in repayment. Data show that 65.4% of tribal households appear to be the victims of verbal harassment of the moneylenders. Agents of informal financiers also resort to not merely social demoralising but mental harassment as well toward the tribal households (Table 6).

Short-run Reaction Towards the Tribal Households in Case of Delayed Repayment (Percentage).

It is apparent that the psychological impact of verbal and mental harassment is impinging on the socio-economic life of the tribal people. Verbal abuse takes many forms such as yelling, put-downs, name calls and belittling behaviours. Participant 32, a coolie worker hailing from Paniya community in the market go-down, narrates his painful experience:

We are often abused by ‘other state money lenders’ who visit us every Sunday morning. It is highly humiliating, especially when we are abused in the presence of our relatives, in-laws, and children. Abuse is the first form of attack on us when we delay the repayment of dues. For everyone Sunday morning is awesome, but for us it is awful. Moneylenders knock at our doors every Sunday morning to get their dues back. Unless paid or sought any time for repayment, they start abusing us. Verbal abuse always demotivates us, depresses us, and tends to withdraw us from productive work. The edifice of the so-called financial structure that is said to have been developed to serve us utterly fails to come to our rescue

Credit Denial in Case of Default in Repayment

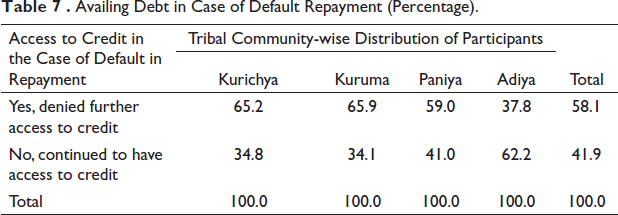

Default in repayment normally happens in the case of poor and low-income tribal households. From the discussion with the suppliers of informal finance, it is understood that they lent money to tribal households knowing that there would be a default in repayment. But, in some cases, if default occurs they would cease to lend to such borrowers fearing that further lending might lead to increased backlog in payment. In this study, we enquired whether the tribal households are denied credit at any time following default in the payment of the first loan. Unsurprisingly, 58% reported that they had been denied further credit by their lenders in case of default in repayment of the first loan. It is seen that among the Kurichya and Kuruma tribal communities, nearly 65% of households opined that they had been denied credit by their informal financiers following default in repayment (Table 7).

Availing Debt in Case of Default Repayment (Percentage).

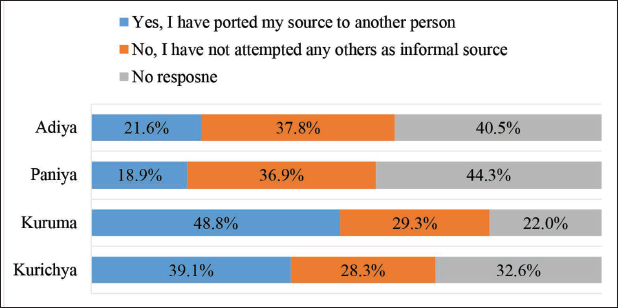

Seeking Credit from Other Sources (Porting Credit) in Case of Denial of Credit

Having presented the possibility of denial of credit following default in repayment, it is important to know the alternative sources from where they can get credit to meet their requirements in subsequent times. Households from the Kuruma community (48.8%) reported that they would port their credit in case of denial by the existing supplier of informal finance (Figure 2). Among the Kurichya, nearly 40% opined that they would port credit to other sources like relatives, and any other moneylenders. But it is important to note that in the case of Adiya and Paniya tribes, only 21.6% and 18.9%, respectively, reported the possibility of porting credit to other sources. This shows that even in the case of denial of credit, households from these communities tend to be loyal to their existing credit suppliers.

Sources of Credit in the Case of Denial of Debt from the Existing Sources of Finance (Percentage).

Unlike the forward tribal communities, porting credit appears to be not easy for backward tribal communities like Paniya. For porting to be successful, there must be an array of choices of informal financiers or formal institutions. But, given the choice constraints, porting of credit continues to be a problem for the backward tribal communities, and hence, they continue to maintain their ties with the existing informal financier despite the problems that come up. Participant 53, a casual labourer from the Paniya community, responds to this issue:

For us, village money lenders and the other lenders are the sole sources of immediate credit needs. We have no other choice compared to these informal sources. We always maintain our ties with them even though they abuse us, humiliate us or at times physically assault us. Left with no alternatives, we have been at the mercy of the village money lenders. There is no question of porting of our credit sources under these circumstances

Social Support to Resist the Actions of Informal Financiers

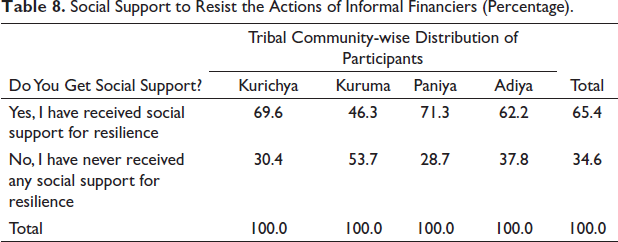

As the tribal communities are not able to repay loans within the stipulated time, there would be bad responses from credit suppliers which make tribal households more vulnerable. Data show that there exists a strong social coherence among the tribal communities, that is, they have a good social connection due to their settlement life. The study reveals that 65.4% of households reported having received social support to resist the actions of informal financiers (Table 8). Among the Paniya tribes, 71.3% of households get social support to resist the actions of informal financiers. The reason for this highest social support that the Paniya tribe receives is only because they live in settlements or colonies. But this type of social bondage is slightly less in the case of Kuruma tribal community.

Social Support to Resist the Actions of Informal Financiers (Percentage).

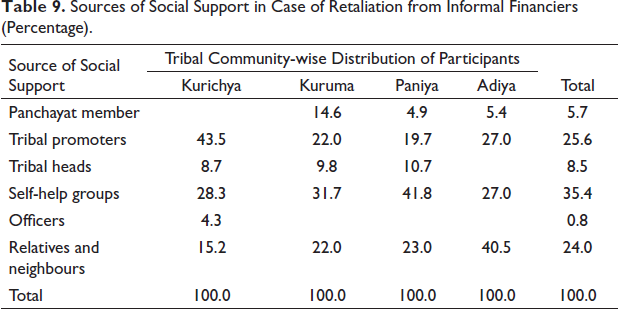

Next, we look at the different sources of social support that the tribal households receive to resist against the actions of suppliers of finance. These sources mainly include SHGs, tribal heads, relatives and neighbours. It can be seen from the data that more than 35% of tribal households receive support from SHGs and 25.6% from tribal promoters, and 24% from relatives and neighbours. Among the Kurichya, the majority (more than 40%) receive support from tribal promoters but in the case of Paniya, 41.8% of households receive support from the members of SHGs. It is disheartening to know that only 4.3% of the Kurichya tribal households opine that they receive support from tribal officers (other than the tribal promoters). All other households from other tribal communities opine that they never get any support from tribal officers to resist the untoward retaliation from the creditors in times of default in the repayment (Table 9).

Sources of Social Support in Case of Retaliation from Informal Financiers (Percentage).

Since informal lending does not fall under the legitimate framework, legally, the borrowers are unable to move against any atrocities meted out to them by the financiers. In earlier times, tribal heads used to come across such problems, and an amicable solution could be found in the interest of both parties. Now, the tribal heads have been replaced by the democratically elected local self-government members who intermediate between the borrowers and the lenders. Sometimes, neighbours and relatives also come to the rescue of borrowers from the clutches of moneylenders. A tribal promoter whom we met had to say this:

Many a times, we have to be the mediator in many informal debt settlements between the borrowers and the lenders. We lay down the legal implications of illegal lending at exorbitant interest rates if the moneylenders continue to stick on to their argument. However, there is a limit to this. Moneylenders cannot rotate their money if it gets blocked by some borrowers. Their presence is indispensable for the tribal people as well, especially in the absence of formal financial institutions that completely suits their credit requirements. Therefore, we find it extremely difficult to strike a solution between the competing positions of both the lender and the borrower. As both need each other, the tie-up between the village moneylender and the low-income tribal people has become so integrated that even some upheavals due to disputes arising out of default in repayment hardly break the connection forever

Interest Rate and Borrowing from Informal Finance by the Tribal Households

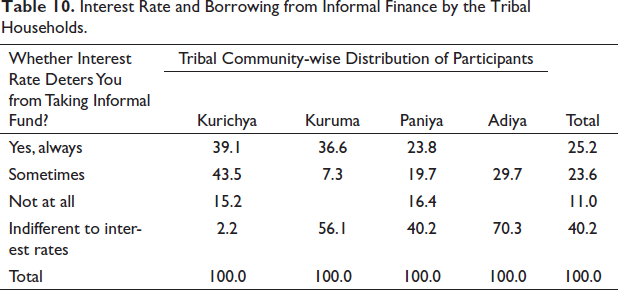

We have looked into the possibility of interest rate becoming a factor that keeps the tribal households away from approaching informal financiers for loans. The study shows that 40.2% of households are indifferent to the interest rates when they attempt to avail credit from any source of finance, especially informal finance. It can be seen that 11% of households never regard interest rate as a determining factor of their demand for credit from the informal financiers. Among the Kurichya tribal households, only 39.1% consider the interest rate while demanding credit from any source and 40.2% of Paniya households are completely indifferent towards the interest rate when deciding on their demand for informal sources of credit (Table 10).

Interest Rate and Borrowing from Informal Finance by the Tribal Households.

In the case of tribal communities, the cost of credit does not appear to be the determining factor for demanding informal credit. Participant 156, from Kuruma community, who lives by collecting forest produce from deep forests, narrates how she relates the cost of credit to the need.

We are unmindful about the interest rate at which we borrow particularly when we desperately need money from any source. It is not the cost that matters when we are in dire need of money, but what matters most is whether we get it or not. I think for plainsmen also the same thing applies. However, plainsmen enjoy wide choices of credit.

Discussion

It is true that in India, financial access has increased with the nationalisation of banks and the establishment of regional rural banks and co-operative banks (Chavan, 2008). In Kerala, the penetration of banking has been quite substantial compared to the national trend. In the tribal belt as well, banks have established branches keeping in mind the banking needs of the poor and marginalised people. The presence of banks in the tribal areas in Kerala is evident from the fact that close to 100% of tribal households have been declared banking included (Kumar, 2013). However, accessing bank accounts either due to the pressure from banks (supply-driven financial inclusion) or due to own demand from the customer (demand-driven financial inclusion) does not suffice to make the people financially included or banking included. It boils down to the fact that equipping tribal communities with financial literacy and skills while also considering the establishment of small banking and credit unions in underserved areas would strengthen the existing supply and demand-side strategies being adopted in tribal areas to address the issues pertaining to the financial access of the tribal communities. Along with supplying bank accounts, it is important that banks should cater to the credit needs of the people. However, this study reveals that the tribal communities, despite having been included in the banking system by way of securing an account, are more dependent on informal sources for credit, which, interalia, makes them persistently impoverished.

This obviously points towards the fact that a mere banking inclusion does not appear to be helpful in relieving tribal households from the unlawful clutches of the informal financiers. As long as they remain under the mercy of informal financiers, it is unlikely to bring about tangible and constructive changes in the life of the tribal households. Unlike the previous studies dealing with the problems that arise out of access to the informal finance, this study has attempted to unfold the real story related to the repercussions that emanate from the excess reliance of tribal communities on the informal credit. This study presents different sources of informal finance including those which have never been addressed appropriately and comprehensively by other studies. For instance, the present study delves deep into sources like relatives, friends, neighbours, social groups and contractors. It is interesting to note that friends, relatives, and neighbours together account for almost 55% informal credit by the tribal communities in the present study. This proclaims the extent to which the social and relational capital come to the rescue of tribals when they find themselves in dire need of credit, albeit these sources do not appear to be sufficient in addressing their credit requirements. On top of all these, it has been found that majority of tribal households do not consider interest rate as a factor that deters them from availing credit from the informal financial sources, pointing to the irrational behaviour of tribal credit seekers. In fact, this corroborates the theoretical underpinning that often low-income and socially disadvantaged segments of society particularly the tribal people do not exhibit any rational behaviour in seeking credit from different sources. The so-called rationality assumption (Mujabi et al., 2021) in the demand for credit finds no evidence when it comes to the case of tribal people as shown in the present study. It is evident that credit market behaviour exhibited by tribal communities is often driven by ‘bounded rationality’ rather than rationality as such (Kim, 2021).

Unrestricted number of borrowings that can be made with informal financiers has been found to be a factor for excess reliance of tribes on the informal finance for credit. Here, again, it is quite interesting to note that forward tribal communities borrow more frequently from informal financiers as they are considered to be more credit-worthy in the eyes of credit suppliers compared to the backward tribal communities. Further, it could be observed that flexibility in repayment has been allowed only in the case of forward tribal communities. They have been found to be enjoying the rule ‘as and when possible’ in the case of repayment, which shows that the economic and social status of tribal households play a key role in dictating the terms of credit even in the case of informal finance. The study has found that default in repayment usually invites uncivilised behaviour from the part of the informal financiers. They resort to verbal abusing which is the first reaction from the creditor when the debtor defaults on repayments, and verbal abusing in different forms is extremely demoralising for the tribes. Default in repayment often ends up in credit denial which forces the tribal households to go for what is called credit porting. Again, credit porting has been found to be a luxury for only the forward tribes. Here, again the backward tribes are at a disadvantage. The study shows that the social support plays a crucial role in tackling the issues created by informal financiers.

Conclusion

Caught up in severe economic hardships owing to many socio-economic factors and the growing reluctance towards availing formal finance, Tribal communities under this study appear to be mainly depending on informal sources for loans. Most of the tribal households repeatedly borrow from informal sources mainly to repay the existing debt and to meet educational expenses. The tribal communities who do not repay the loans on time experience verbal harassment from the informal lenders.

As the study reveals, excess reliance on informal finance has adverse repercussions on the socio-economic life of people especially when weaker communities like tribes are exposed to such conditions. It is true that informal finance often comes to the rescue of people especially when formal banking institutions find it extremely difficult to offer a helping hand. Nevertheless, if informal finance operates as is happening elsewhere in India, it will surely turn out to be detrimental to the social and economic interests of people like the tribes. Undoubtedly, this aggravates their vulnerability, and they will be pushed to abject poverty and economic impoverishment. Therefore, the need of the hour is to bring informal finance under the strict surveillance of the government machinery, if the alternative source of the formal system cannot substitute it so as to cater to the genuine credit needs of the people.

The intertribal variation reflected in the differences in the attitude of forward and backward tribal communities towards informal finance makes it obvious that the policies towards tribal development need to be revamped in accordance with the financial needs of the tribal communities. The forward tribal communities, namely, Kurichya and Kuruma, aided by their economic and social empowerment compared to the backward tribes, are found to be dealing with issues of informal finance in a more sophisticated manner. Informal financiers keep on extending credit to them despite periodical default in repayment. This points towards the necessity of economically and socially empowering tribal communities so as to make them creditworthy not only in the eyes of informal financiers but also formal financial institutions. It calls for tailoring institutional (formal) credit solutions suitable to the credit needs and socio-economic conditions of the weaker segments of the society. Policymakers and government need to pay more attention to enhancing the livelihood avenues through interventionist attempts. In short, the problem of excess reliance on informal finance and its repercussions can be resolved by adopting a supply-side cum demand-side strategy. On the demand side, equipping the tribes with skills and knowledge in using financial instruments and institutions through the well-planned financial literacy campaign can also help in emancipating tribes from exploitative hands of informal financiers. On the supply side, the policymakers can think of establishing kiosk-based small banking and credit unions backed by formal banks in financially ill served areas. In terms of the limitation of the study, it has considered only four accessible tribal communities which reside in colonies and in areas close to forests, but excluded very primitive tribal communities, which reside in deep forest, and do not have any connection and interaction with the mainstream. Future studies may include perspectives of informal moneylenders. It is also important to explore how to break the cycle of borrowing. As some borrowed to meet educational expenses, it is useful to look at whether government educational benefits and services are delivered to these communities and their adequacy. To conclude, innovative strategies are needed to address both demand- and supply-related issues so that the exploitation of tribal people and communities can be ended and prevented.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.