Abstract

A majority of people in developing countries lack access to formal finance and rely on community-organised groups. These savings and credit associations (SCAs) face challenges in overcoming well-known collective action problems. SCA financial products can be understood as a common pool resource. Drawing on Ostrom’s (1990) design principles for self-governing local institutions, we investigate the conditions under which SCAs can achieve sustainability. Using a qualitative methodology, data were collected by examining administrative records and interviewing stakeholders from three SCAs in the Philippines. Our results indicate that adherence to the design principles is positively associated with SCA sustainability. We find that pre-existing social connections are not a necessary condition for initial adherence to the design principles but social capital may play an important role in sustainability overall. These findings contribute to our understanding of how governance design can boost the sustainability of informal groups and enhance financial inclusion among the poor.

Keywords

Introduction

The goal of reaching Universal Financial Access by 2020 was motivated by the expected benefits like reducing poverty and income inequality (Burgess & Pande, 2005; Karlan & Morduch, 2010; Levine, 2005; World Bank, 2018); so, why do 1.7 billion adults remain ‘unbanked’ (Demirgüç-Kunt et al., 2018, p. 4)? Despite government and donor assistance, supply-side constraints remain problematic. Formal providers are often unable to reach lower-income populations due to high transaction costs, information asymmetries and difficulties in designing profitable products for complex and varied needs (Besley, 1995; Stiglitz & Weiss, 1981). In their place, groups of individuals have been providing basic financial services among themselves.

Such groups are commonly referred to as savings and credit associations (SCAs), self-help groups (SHGs) and village savings and loans associations (VSLAs). They offer members some element of a core financial service: saving, loans or insurance. They are distinct from other forms of financial institutions in their localised, autonomous and self-governing nature, as well as their smaller scale and independence from formal legal, fiscal and financial authorities. They typically do not involve external capital (unlike group lending programmes) or subsidies, and are managed and sustained internally. SCAs vary by group size, meeting frequency, contribution amount and loan allocation method.

Many low-income and rural populations depend on such community-based institutions to meet their daily financial needs. One-quarter of adults in developing economies who saved in the past 12 months reported doing so through semi-formal institutions like SCAs (Demirgüç-Kunt et al., 2017). SCAs are the sole point of financial access for many (Demirgüç-Kunt & Klapper, 2012). One international non-governmental organisation (NGO) reports that they have supported 351,000 VSLAs covering more than 7 million members over 51 countries since 1991 (Care, 2019, p. 16). Where formal institutions are unwilling or unable to serve, SCAs can mobilise scarce and otherwise idle capital (Bouman & Hospes, 1994); protect and discipline savings (Dupas & Robinson, 2013; Gugerty, 2007); and fund larger spending on durable goods or productive investments (Besley et al., 1993). Involvement in SCAs can serve as insurance mechanisms (Klonner, 2003), and support food security (Beaman et al., 2014; Ksoll et al., 2016).

SCAs evidently play a crucial role in the financial lives of lower-income households. But they are challenging to run. Well-documented problems include default, embezzlement, conflict and administrative overburden (Ardener, 1964; Bouman, 1995; Edwards, 2010; Geertz, 1962). SCAs are critiqued for their ‘low reliability’, ‘risks of fraud and collapse’ and an ‘inability to offer long terms’ for value creation (Ledgerwood, 2013, p. 68). A survey of rotating savings and credit associations (ROSCAs) in urban Benin found them to be inherently unstable (McNabb et al., 2019). However, successful cases have also been recorded. There is merit in gaining a better theoretical understanding of the conditions that account for the variations in their success and failure to inform financial access strategies. This article therefore asks: under what conditions do SCAs achieve sustainability in financial service provision?

Research into community-based and informal finance groups has explored participant characteristics (Levenson & Besley, 1996), behaviour and preferences (Dupas & Robinson, 2013), and how local savings groups might support wider developments like financial digitalisation (Mehmood et al., 2019). We are interested in analysing the design and performance of the group itself. Understanding how institutional design affects group performance can move us closer to systematically reproducing the conditions for longer-lived SCAs, and therefore how to expand reliable and sustained financial access.

This article makes two contributions to the scholarly literature on SCAs. First, it aims to address a gap in our understanding of SCA sustainability by developing an analytical framework that draws on Elinor Ostrom’s design principles for local self-governance. Second, it tests the implications of this framework with a novel data set gathered from local savings groups in the Philippines.

The second section discusses the literature on SCAs and their sustainability in greater depth. We demonstrate how Ostrom’s design principles for local governance can be applied to SCAs, to address potential collective action failures that might lead to savings group breakdown. Our framework motivates the hypothesis that greater adherence to the design principles promotes greater sustainability. The third section explains the study design and case study context. The fourth section present results and the finding that adherence to the design principles is positively associated with sustainability. In the fifth section we discuss a second finding that pre-existing social connections appear not to be a requirement for initial adherence to the design principles. Successful self-governing arrangements can be set up largely from scratch and run well while social connections are formed among the group. These findings will be of interest to policymakers aiming to deliver sustained financial inclusion among poor communities. The seventh section concludes the article.

Scholarly Context

Understanding Savings and Credit Associations as a Collective Action Problem

Groups of individuals sharing a common interest may find themselves in a social dilemma. Individuals face the incentive to behave independently to maximise their short-term self-interest at the expense of the common goal. If each individual behaves in such a manner, the result would jointly leave all participants worse off than if they cooperated. However, no individual has the incentive to change their strategy to cooperate, given the predicted choices of others to defect. Such social dilemmas are commonly understood as public good or collective action problems (Olson, 1965). They have been modelled as prisoner dilemmas (Dawes, 1975) and as problems of shirking (Alchian & Demsetz, 1972), freeriding (Grossman & Hart, 1980) and moral hazard (Holmstrom, 1982).

With respect to common pool resources (CPRs), Ostrom (1990) termed them problems of provision and appropriation. Because of the jointness of supply, if each individual prefers to freeride on the contributions of others, joint benefits like the maintenance of resources may be underprovided. The problem of appropriation occurs when subtractable common resources are overused or destroyed because participants seek to maximise their personal benefit over others. The ensuing result is the notorious ‘tragedy of the commons’ (Hardin, 1968). Ultimately, the challenge of collective action is to overcome short-term selfish interests and achieve ‘mutually beneficial cooperative ways of getting things done’ (Ostrom & Ahn, 2009, p. 20). These aspects of CPR governance can be seen to apply to SCAs, which require management of a shared and limited pool of financial capital.

Cooperation is central to SCAs. Individuals form groups to achieve a shared goal: to provide financial services among themselves. However, the ability to enjoy individual benefits from these services requires the sustained cooperation of enough members. Each individual’s choices affect others’ abilities to benefit from the system. Group funds must be sufficient for members to be able to access credit when needed. This relies on adequate member contributions. If members choose to freeride by contributing very little sums or none at all, productive use of the common fund will be severely hampered. For example, Beninese ROSCAs surveyed by Dagnelie (2008) list problems like irregular payments and unequal pots as a common cause of group failure. SCA evaluations mention complaints about individuals who do not contribute regularly (Bermudez & Matuszeski, 2010). In many groups, taking loans is also considered a form of ‘contribution’ because of the eventual interest added to the overall fund. As such, members who do not take loans but share in the increased dividends can be considered freeriders (Edwards, 2010).

SCAs also grapple with adverse selection and moral hazard. Individuals may renege on their loan repayments, or riskier members may request for larger loans or earlier pots to increase the benefits of defaulting (van den Brink & Chavas, 1997). Enforcement of obligations and repayments are commonly cited problems, sometimes leading to group collapse (Anderson et al., 2009; Bauchet & Larsen, 2018; Bouman, 1995; Handa & Kirton, 1999). As Ostrom (1990, p. 33) observed, problems of appropriation and provision are ‘intimately bound together’: if overuse, crowding and default become severe, members will not be motivated to contribute to the common fund. Overuse and large-scale defaults may result in the eventual depletion of funds and grievous loss of monies (Karlan & Morduch, 2010).

The literature also highlights the importance of social capital in governing CPRs. Social capital can be understood as ‘features of social life – networks, norms, and trust – that enable participants to act together more effectively to pursue shared objectives’ (Putnam, 1995, pp. 664–665). Putnam raises the importance of ‘joining’ to social capital, contrasting the act of making a donation with the very different type of participation that joining a group involves. This aspect is clearly relevant to SCAs, which are voluntary, require an active decision to join and usually require some degree of face-to-face activity and participation to stay in the group. Ostrom links the concept directly with local governance arrangements: ‘crafting institutions … is one form of investing in social capital’ (Ostrom, 1994, p. 529). Assumptions of trust, a key aspect of social capital, are built in to Ostrom’s (1994) formal modelling of a farmers’ association aiming to build an irrigation scheme. In their seminal work on savings groups, Besley et al. (1993) draw on earlier anthropological literature to formalise the costs of violating rules through social sanctions (e.g., discomfort, loss of face and ostracism). Such social sanctions are assumed to prevent defaults and maintain the viability of savings groups (Anderson et al., 2009).

Empirical testing, however, suggests a nuanced role for social capital as an explanatory variable of SCA performance. Handa and Kirton (1999) find that ROSCAs with greater social connections were more likely to experience problems than ROSCAs that offered payments to their leader and used random pot allocation methods. Dagnelie (2008) tests a wider range of variables, including group membership, social capital and institutional design. Rather than groups with high social capital, he finds that groups that elect committees, screen members and enforce important sanctions are more likely to survive. In their study of ROSCAs in Taiwan, Bauchet and Larsen (2018) find that member characteristics and group composition with regard to social connectedness were not associated with group survival. While McNabb et al. (2019) find that groups started among family were more likely to be sustainable than those started with family and friends, their analysis also suggests that institutional design such as the presence of written rules, repeated cycles and sanctions have a more important role to play in ROSCA sustainability. The empirical evidence points to distinct roles played by social capital and the broader set of institutional design features in explaining SCA performance; we now turn our attention to the latter.

Analysing Sustainability in the Context of Collective Action Problems

In the presence of collective action problems, classic theory implies that individuals will be trapped in an inevitable cycle of destruction, but could be saved by the coordination of external agencies that can enforce cooperation (Hardin, 1968; Olson, 1965). This might explain why SCAs are often overlooked in favour of market- or government-based solutions. A competing scholarly outlook gives prominence to the existence of community-based institutions successfully managing small-scale CPR systems without external governance (Baland & Platteau, 1996; Ostrom, 1990). Likewise, the presence of user-managed SCAs defies unambiguously pessimistic predictions.

Empirical studies have measured sustainability outcomes and covariates in diverse ways. The operationalisation of sustainability has included single-reported cases of non-repayment (McNabb et al., 2019), experience of problems in the group (Handa & Kirton, 1999) and the collapse of groups (Bauchet & Larsen, 2018; Dagnelie, 2008). While significant, instances of default are not synonymous with unsustainability in accumulating SCAs; conversely, the achievement of sustainability cannot be equated simply with the avoidance of default.

We argue that sustainability can be framed as a question of how some SCAs manage to overcome cooperation problems and maintain collective action in ensuring the ongoing provision of core financial services. This conceptualization is different from the narrower one of individual defaults and the broader one of group collapse in previous studies. Our framing recognises that SCAs may continue to be robust even in the face of individual defaults, periods of declining contributions in lean times and membership change. At the same time, groups may not be sustainable even if they have yet to collapse, if they are not functioning adequately enough to enable continued access to their financial services.

An Institutional Approach to Explaining Sustainability

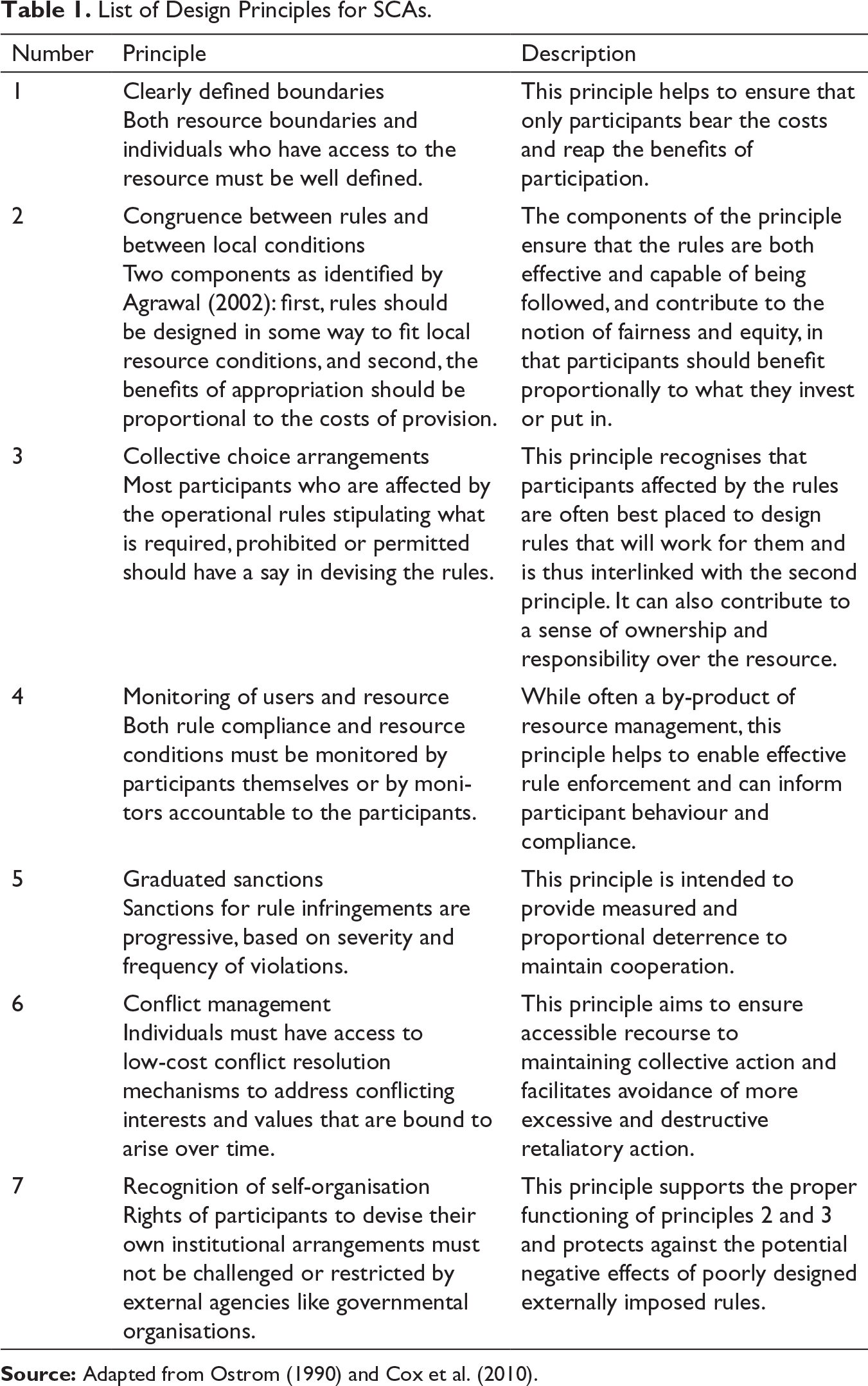

List of Design Principles for SCAs.

The design principles serve to shape individual incentives and behaviours. Rather than being rational, self-interested and calculating, individuals in social situations are boundedly rational, norm adopting and learning. Mutually reinforcing notions of trust and reciprocity are in effect: individuals choose to cooperate when they trust that others will cooperate. As more individuals build reputations as trustworthy reciprocators, levels of overall trust are enhanced, and further cooperation is more likely to occur. Institutions are the rules and codes of conduct used within a community that ‘potentially reduce uncertainty, mediate self-interest and facilitate collective action’ (Ostrom & Cox, 2010, p. 5). Institutions enable the conditions by which trust, reputation and reciprocity norms can develop and mature to sustain cooperation among groups of individuals. Current SCA models assume that members cooperate based on individualised cost–benefit calculations. However, the ability of groups to devise institutional arrangements to engender cooperation should not be overlooked.

Ostrom’s design principles are uniquely adaptable towards developing a general theory of sustainability in SCAs, where groups face comparable problems of cooperation, and where an extensive array of specific group rules to ‘suit a particular environment, purpose, preference or emergency’ (Bouman, 1995, p. 382) requires a level of abstraction. Informed by these design principles and empirical evidence discussed earlier, we propose the following hypothesis: The greater the adherence to Ostrom’s design principles, the greater the sustainability of the SCA.

Study Setting and Method

Testing this hypothesis lends itself well to a qualitative approach. Qualitative methods can generate richer, contextualised and sometimes unexpected observations on the way SCAs and other self-governed institutions operate (Benda, 2013; McMorran et al., 2014; Ostrom, 2010). The study applies a comparative analysis to three SCAs in the Philippines. The Philippines Development Plan 2017–2022 includes access to finance as a priority goal (National Economic and Development Authority, 2017). Despite the well-known studies on savings behaviours by Ashraf et al. (2006) and Giné et al. (2010) that were based in the Philippines, academic research on SCAs in the Philippines remains relatively scant with a few exceptions (Boonyabancha & Kerr, 2018; Quinones & Seibel, 2000).

Our research was conducted in partnership with the Center for Community Transformation (CCT); a local NGO whose social development programmes include assistance for SCAs in financially excluded communities. CCT often collaborates with local authorities to promote SCAs and additionally offers technical support in designing group rules and financial records. Their aim is for local groups to operate autonomously. CCT began SCA operations in Cebu province in 2011. The province provides a range of groups with a variety of outcomes, characteristics and contexts. Undertaking interviews allows us to explore the lived experiences of group members, while administrative data shed light on the operations and sustainability of the groups.

Case Selection

Three SCA groups were selected following preliminary discussions with CCT. Case selection aimed for variation in the outcome variable across cases and controlling for other explanatory variables by choosing two similar cases. In all groups, all members contributed weekly to the group fund, which accumulated and was not rotated. Existing groups were assumed more likely to be sustainable at the outset. Failed groups, which staff suspected to have broken down rather than come to an agreed closure, were assumed more likely to represent a negative outcome. The first two cases were selected as largely similar cases with suspected different outcomes on the dependent variable (George & Bennett, 2005; Mahoney & Goertz, 2004).

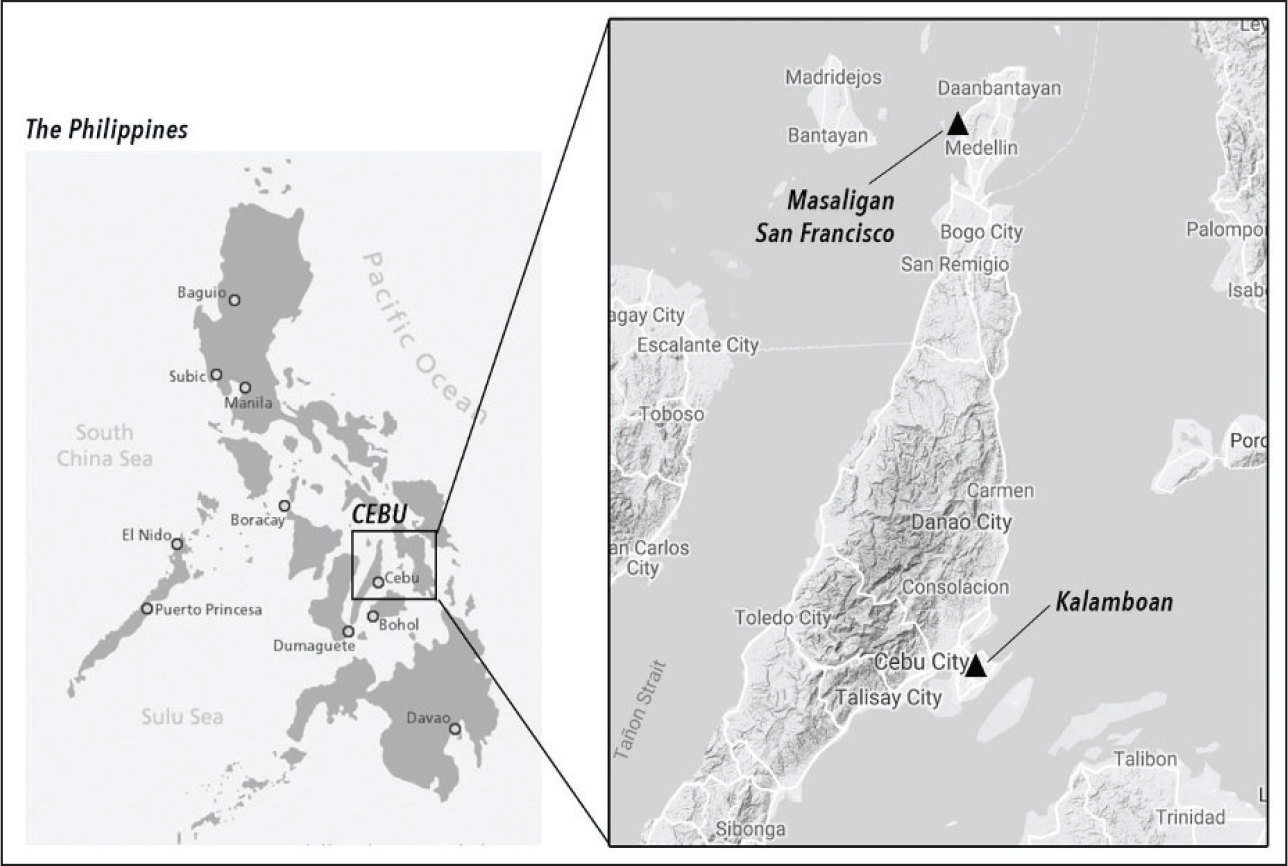

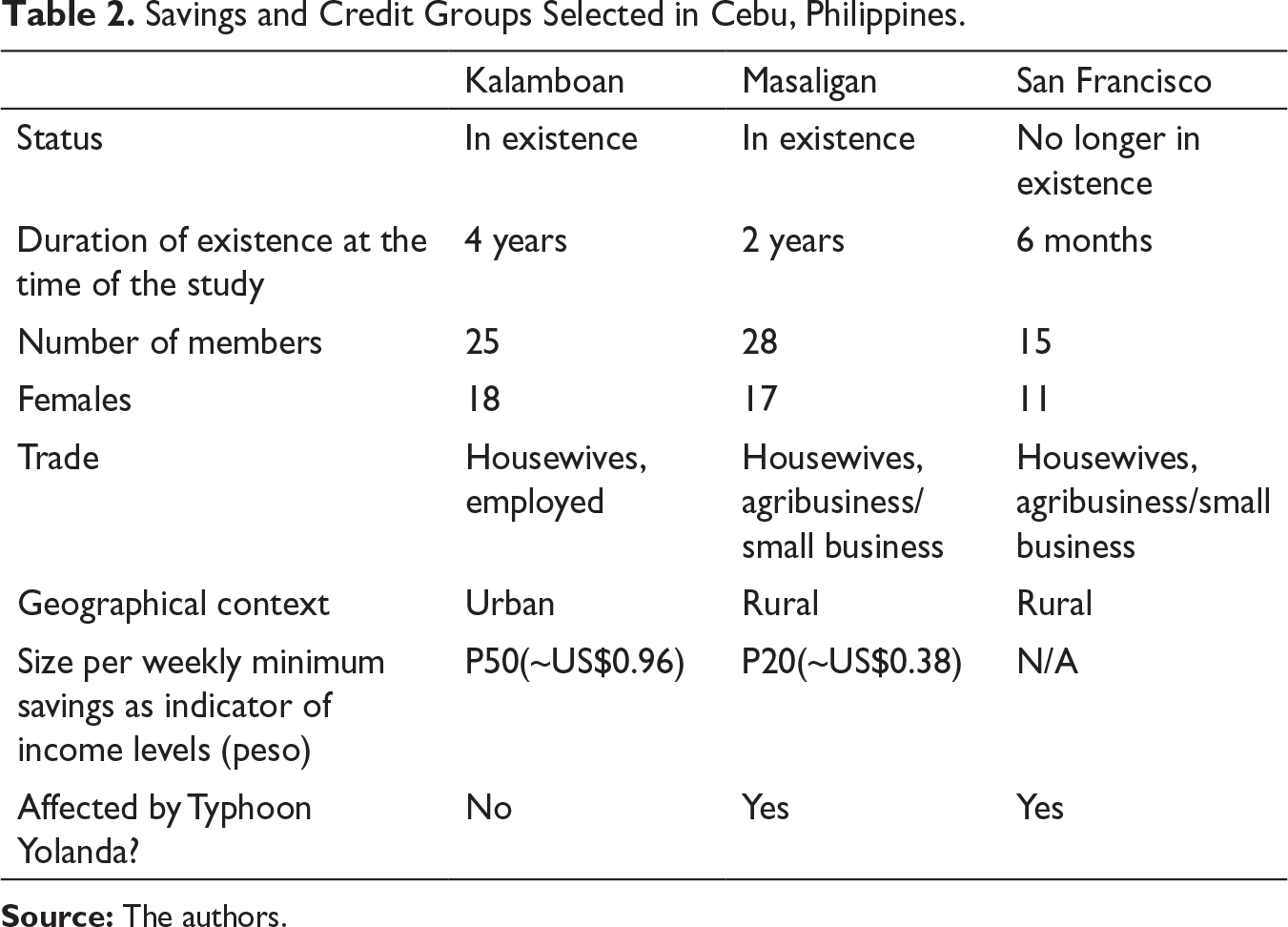

Both groups, named Masaligan and San Francisco, were located off the coast of Medellin, Cebu, in a small rural residential area (see Figure 1). Known colloquially as ‘Yolanda Homes’, the community was built to resettle households devastated in late 2013 by Typhoon Yolanda. As part of the initiative of the National Housing Authority (NHA), each housing block was encouraged to form an SCA with the assistance of CCT. Masaligan and San Francisco formed soon after resettlement in 2017 among members who did not know each other well or at all. Both groups consisted of a heterogeneous mix of gender, age and income-generating activities, although the average member tended to be very low-income, middle-aged, female and micro-entrepreneurs in the agricultural sector (see Table 2 for group characteristics). Both groups were created as savings-only groups. Masaligan continues to provide basic financial services to date, while San Francisco broke down after 6 months.

Savings and Credit Groups Selected in Cebu, Philippines.

A third SCA, Kalamboan, was selected as a group that differed from Masaligan and San Francisco in many respects. It self-organised in 2015, came under the umbrella of CCT in mid-2017 and continues to provide financial services to its members. It provides loans as well as savings. The group is part of a small community living in the dumpsite of the urban Lapu-Lapu City. Kalamboan consists of neighbours who have lived closely together in the community for many years. The community was not affected by Typhoon Yolanda. Members are typically middle-aged housewives or men employed at the adjacent waste processing facility. As urban residents, members possess higher income levels than those of Masaligan and San Francisco, but they are still well below the poverty line and excluded from formal financial services.

Data Collection

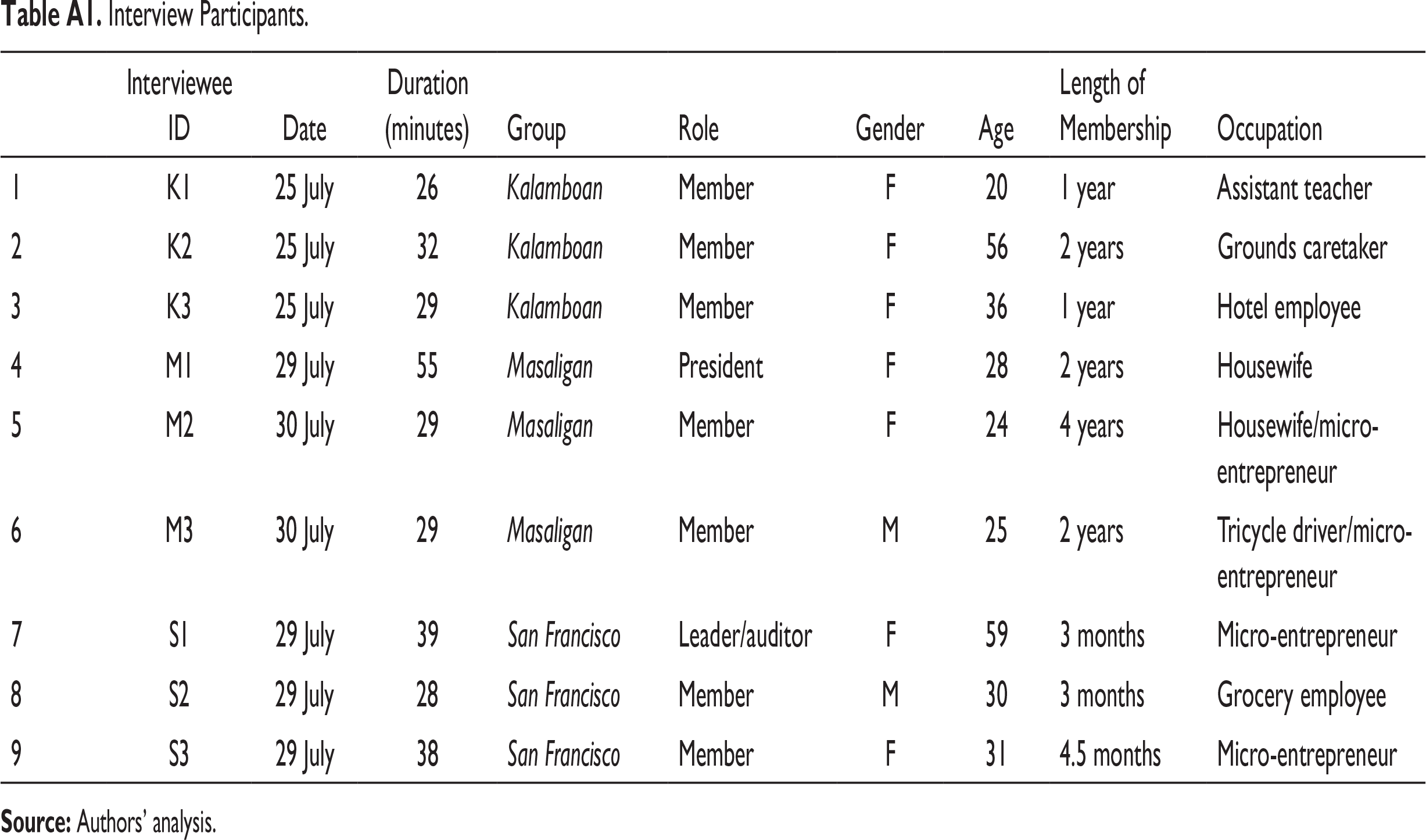

Written group constitutions and financial records (where available) were gathered and combined with semi-structured, face-to-face interviews conducted with group members. 1 Interviews lasted for an average of 35 minutes each and were transcribed to English from Tagalog, English and Cebuano (depending on the interviewee). Group constitutions provide information on formal rules. Financial records set out the type and take up of financial services. Interviews generate insights on lived experiences and group functioning in practice. The combination of data sources allows for triangulation between primary and the secondary sources. This was expected to be especially helpful where formal written rules do not reflect actual rules in practice. Conversely, secondary sources can be useful checks to address the possible error in self-reported information. Nine members took part in interviews, three per group. Interviews asked first about group practices and then individual participation and perceptions of those practices (Charmaz, 2001). One group leader from each group was purposively selected as a valuable source of information on the history and operation of their group. The remaining two members of each group were randomly selected to avoid selection bias. 2 These structured, private interviews enabled reviewing and cross-checking answers across participants to form a coherent picture of group practices, and also created room for greater openness and uncovering of practices and perceptions that may not be discerned by all. As the interviews were in large part concerned with factual knowledge or common experiences, this process, along with the ability to triangulate information with the secondary sources, and the relative homogeneity of group members, ensured that complete and accurate information was sufficiently achieved or that saturation was reached (Guest et al., 2006).

Variables and Content Analysis

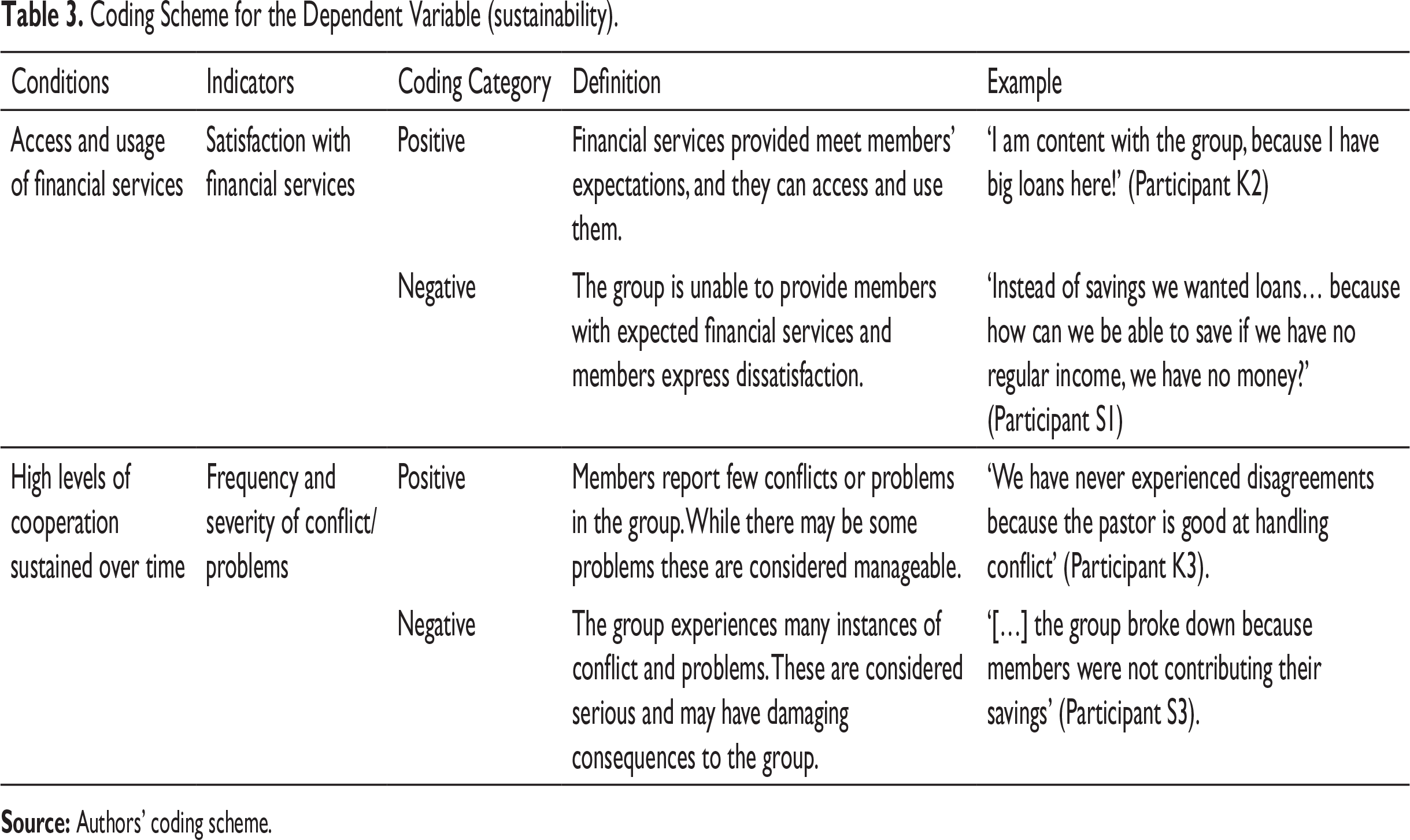

Coding Scheme for the Dependent Variable (sustainability).

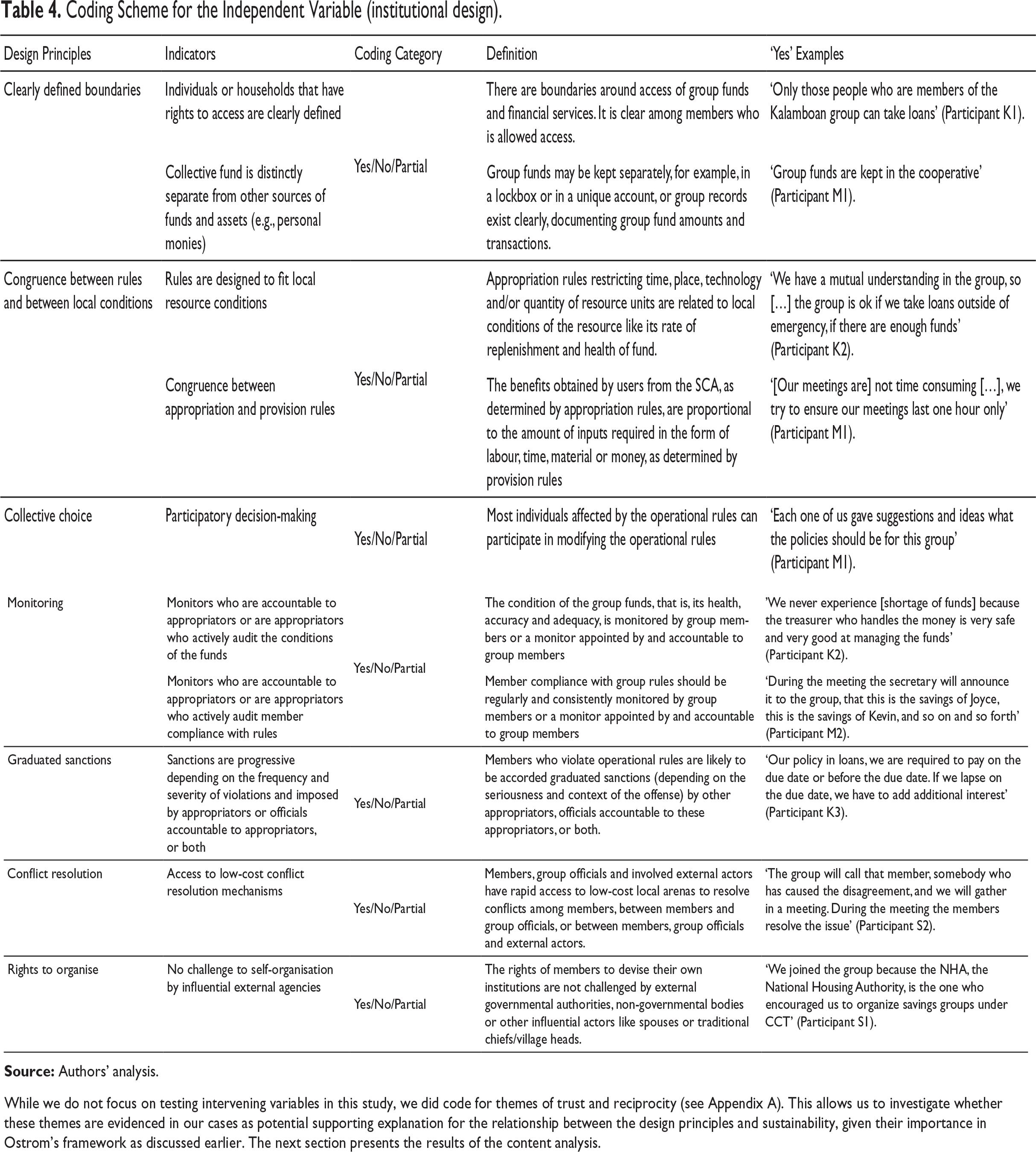

Coding Scheme for the Independent Variable (institutional design).

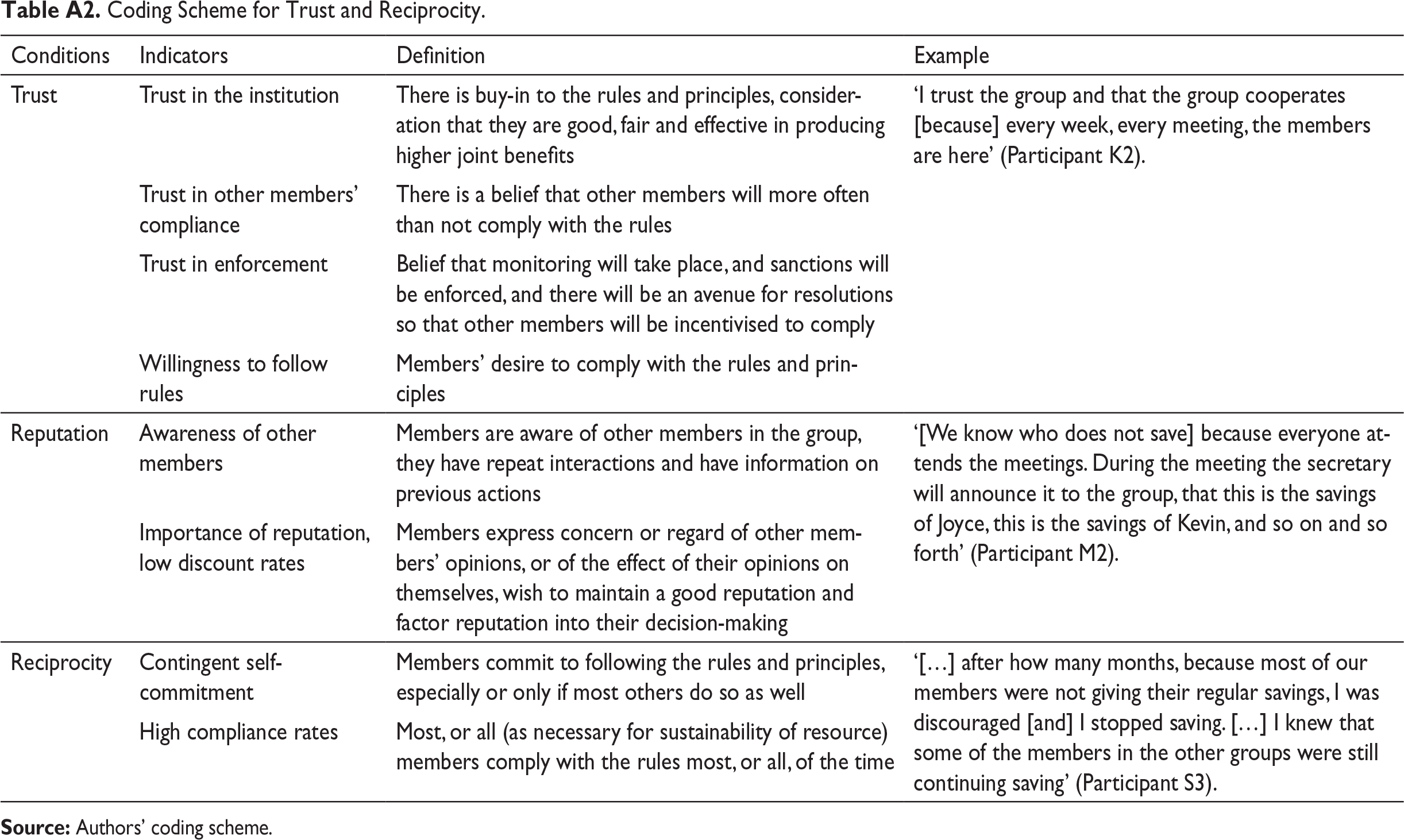

While we do not focus on testing intervening variables in this study, we did code for themes of trust and reciprocity (see Appendix A). This allows us to investigate whether these themes are evidenced in our cases as potential supporting explanation for the relationship between the design principles and sustainability, given their importance in Ostrom’s framework as discussed earlier. The next section presents the results of the content analysis.

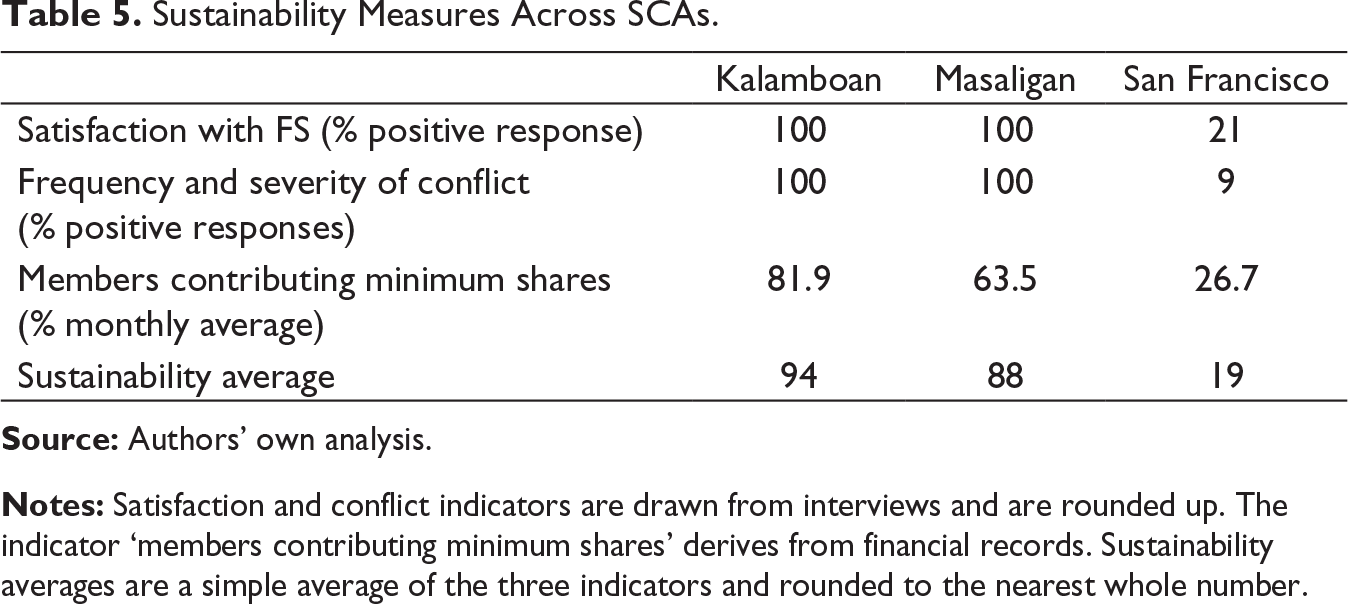

Sustainability Measures Across SCAs.

Notes: Satisfaction and conflict indicators are drawn from interviews and are rounded up. The indicator ‘members contributing minimum shares’ derives from financial records. Sustainability averages are a simple average of the three indicators and rounded to the nearest whole number.

Results

Sustainability

Results clearly show that members of both Masaligan and Kalamboan were highly satisfied with their group services, despite differences in levels of provision. For example, a member of Kalamboan explained their confidence in the continued sustainability of the group, demonstrating satisfaction and a positive opinion of access to loans:

This group keeps going because we have plans for the future, and if ever we have needs, we can easily borrow from the savings, from the group fund. (Participant K2)

On the other hand, when asked whether members of Masaligan wished they were able to take more than emergency loans from the group, a member affirmed their content with the savings as the core provision:

It was a group decision [not to provide loans outside of emergencies]. In this group we learn about the discipline of savings, so if we have emergencies, we learn how to prioritize our expenses and not spend it on unnecessary things. (Participant M1)

In San Francisco, some members were satisfied purely with a savings service, but others sought credit for micro-enterprise investment and were immensely dissatisfied. This was frequently a source of serious disagreement and conflict. High levels of non-cooperation were detrimental to the functioning of the group. As of the last available report, only 4 of the 15 members were attending the meetings, and the total fund amounted to just ₱450 (approximately US$8.6). This adds up to a low sustainability assessment (see Table 5).

Masaligan and Kalamboan reported few concerns of serious problems or conflict. Unlike previous studies that presumed single instances of rule violations or disagreements as indicators of unsustainability, members in this case seemed to have a different perception of what they considered as problematic for the group. A revealing example was shared by a member who mentioned instances of rule violations that did not seem to warrant concern: ‘There are members who have not been saving weekly, but not for a long time… one month’ (Participant M1). The two groups seemed to consider approximate compliance as satisfactory, as long as overall group cohesion was maintained. This was further supported by analysis of their financial records, which showed that on average, approximately 82% and 64% of members in Kalamboan and Masaligan, respectively, contributed their minimum shares monthly. In summary, both Masaligan and Kalamboan are recorded as much more sustainable than San Francisco was, with Kalamboan displaying slightly higher levels of sustainability.

Adherence to Design Principles

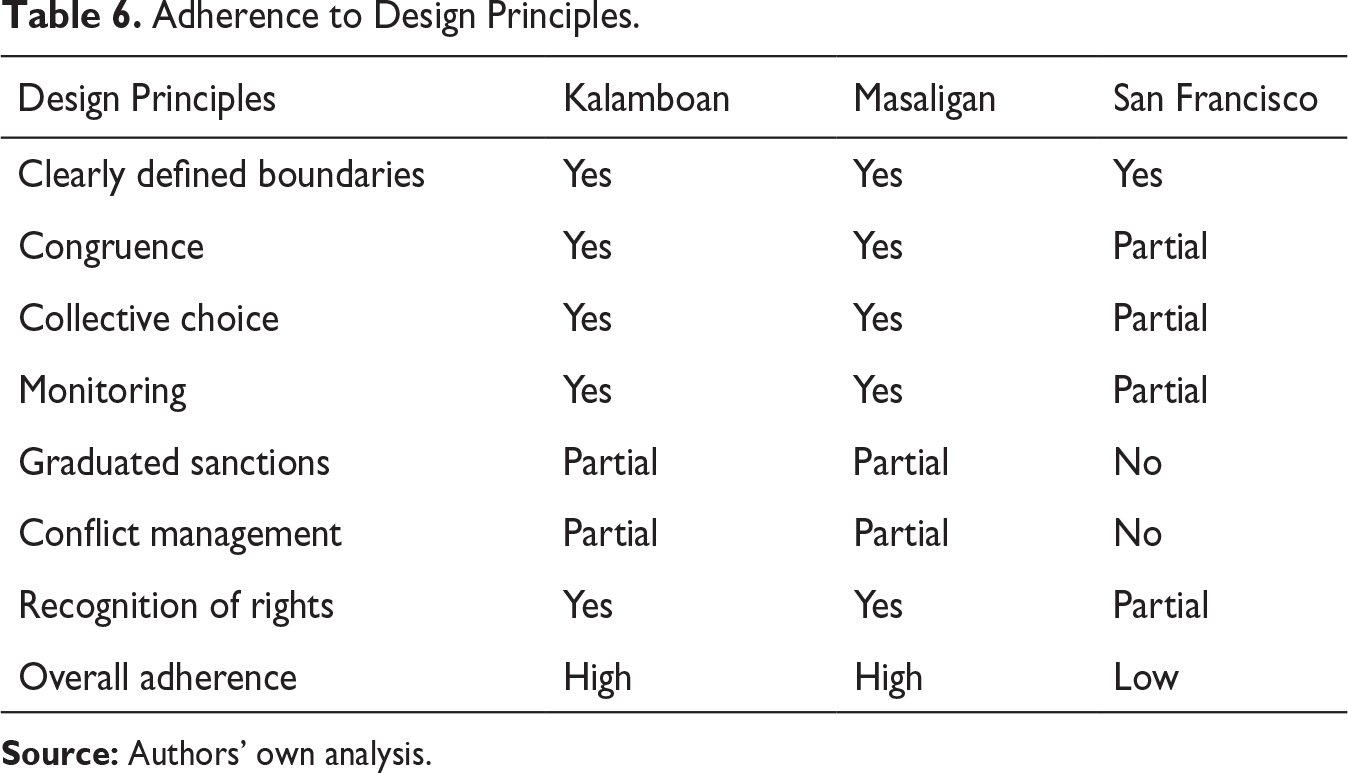

All three groups had clearly defined boundaries (principle 1) for users and resources. Only members were allowed to access the group services and funds. Kalamboan members had to be ‘residents in [their] village and Filipino citizen[s]’ (Kalamboan Constitution). Financial records drew ‘boundary lines’ around users and resources by listing members and demarcating the total amount in the funds.

Congruence (principle 2) requires that rules of appropriation and provision fit local conditions of the resource system. This was met in Masaligan and Kalamboan but not in San Francisco. Kalamboan’s contribution shares were larger, and loans could be taken for flexible purposes. As they were in high demand, loans were capped at ₱3,000 and to be returned within 1 or 2 months with interest. In Masaligan, contributions and the overall pot were smaller, and accordingly, loans were only allowed for medical emergencies. They were, however, provided under more flexible terms, and members ensured there were always available funds for such needs:

With the approval of members, loans can be borrowed without interest. But they must be returned immediately so other members can also borrow. During share-out, members must leave 1 share (20 Pesos) for maintaining the balance of the fund. (Masaligan Constitution)

In contrast, San Francisco suggested a lack of congruence. Some members in the group wished to borrow, while others simply demanded the savings commitment. Despite the potential efficiency gains from negative sorting on present bias (Cassidy & Fafchamps, 2018), the group was unable to design corresponding rules for the appropriation of loans. This relates to the second condition of the congruence principle: that there should be congruence between the benefits of appropriation and costs of provision. For members in San Francisco that wished to borrow, fund contributions were considered an unfair cost without proportional benefits:

We wanted loans because how can we have additional capital to start up a business if we put up savings? It is hard for us to put regular savings every week because we have no regular income. (Participant S1)

Comparatively, members of Masaligan and Kalamboan perceived few or no costs in the SCA. Meetings and savings contributions were understood as part of the eventual benefits, alongside intrinsic and social benefits. Masaligan meetings were kept to less than 1 hour to reduce transaction costs.

Collective choice (principle 3) appeared to be met by all three groups: the groups determined their own policies through a process of voting during meetings, and group officers were appointed through an election. However, formal rules for participation may be undermined by power dynamics or external forces (Cleaver, 1999). This seemed to be the case to a minor extent in Masaligan and more seriously in San Francisco. Masaligan’s meetings had been rearranged to suit the needs of local CCT staff. As a result, attendance and contributions dropped from nearly 90% compliance to 29% in the summer of 2019. Members swiftly moved to reschedule meetings at the original times, reflecting a genuine ability to participate in and control the decision-making process; hence, the ‘Yes’ rating on collective choice for Masaligan (see Table 6). External interference in San Francisco’s policymaking process was of a more serious nature. Members felt constrained in the design of their group policies by the stipulation of NHA that groups needed to be formed per housing block. Members were largely prevented from formulating loan procedures by local CCT officers, who advised against it:

The group wanted to avail loans. We were not able to, CCT told us that we would not be able to avail loans […] So I decided not to continue […]. (Participant S1)Adherence to Design Principles.

While NHA or CCT may not have imposed rules overtly on San Francisco, their outsized influence and interference in the group’s decision-making process impeded the genuine realization of collective choice.

A high level of monitoring (principle 4) took place through group meetings in Kalamboan and Masaligan. Transactions were only permitted during weekly meetings so that members could monitor both fund movements and member compliance. Handling of the funds and group records was delegated to elected officials, and members monitored them by requiring transactions to be announced out loud and verifying records against personal passbooks. In Masaligan, funds were deposited to a cooperative and receipts filed. The Kalamboan treasurer was appointed to monitor loan disbursal and ensure that funds are sufficient to meet various loan requests. The importance of this monitoring role was evident in the following example:

We had an experience when the treasurer had his vacation for one month. The group still continued [but] during that one month, no loans could be taken, and I kept the money in my room, in the box with a key. (Participant K2)

The monitoring principle was only partially met in San Francisco. Transactions did not occur in group meetings; instead, a group ‘auditor’ was appointed to collect contributions from house to house before the meeting date. When the auditor left the group after 3 months, there was no replacement to continue the monitoring activities. Further, group records were kept by local CCT officers, who were neither members nor accountable to the members. The contrast between successful monitoring in Masaligan and less functional monitoring in San Francisco is encapsulated by the following observations from group members:

[We know who does not save] because everyone attends the meetings. During the meeting the secretary will announce it to the group, that this is the savings of J—-, this is the savings of K—-, and so on and so forth. (Participant M2) […] at first we had a leader to monitor the members, A—–, the one who is collecting the savings. But since she left the group there was nobody to monitor the members to save. (Participant S1)

Graduated sanctions (principle 5) were applied in Masaligan and Kalamboan. In Kalamboan.

Loans [which] are not yet repaid by the due date […] will be renewed with […] interest. No [further] loans can be taken [by members] if [they have] remaining balances due. (Kalamboan Constitution)

Members of Masaligan, who wished to drop out of the group, would not be permitted to withdraw their savings until the date of share-out. These sanctions were naturally progressive as the lengthier and larger the rule violation, the costlier the punishment.

3

However, none of the groups had sanctions for missing meetings or fund contributions. Masaligan’s formal rules stipulated that members had to make up for any missed contributions the following week but this rule was rarely enforced. Neither was it considered a ‘punishment’ as it was no more than the original agreement asked. As a member of Masaligan explained:

We are not imposing [monetary] penalties because [the defaulting members] will [find it] more difficult to save if we have penalties. So, we agreed in the group not to impose penalties, but we make sure we can put our regular savings. (Participant M1)

Weekly meetings were a low-cost forum for conflict resolution (principle 6). In all three groups, elected officials were expected to manage and resolve conflicts. CCT staff were also expected to help manage conflicts between officials and members. However, there did not seem to be any mechanism in place to resolve disputes between CCT and NHA officials and group officials and members in all three groups. The principle is also subject to the same concerns as those with collective decision-making. While a mechanism may exist in technicality, these processes may not translate to reality, for example, where power dynamics prevent their actual utilization. This was the case in San Francisco where interviewees reported they felt unable to air their concerns among the group and in fact never did so; for this reason, adherence is coded ‘no’ in the San Francisco group (see Table 6). The converse is true in Masaligan, where formal mechanisms for conflict resolution did not exist between group members and CCT officials, yet some conflicts were resolved, in practice, through informal means. In Kalamboan, all participants reported that group conflicts were rare as the group leader was adept in resolving any disagreements, confirming to a certain extent the operation of formal mechanisms in practice. No instances of conflict between group members and CCT officials in Kalamboan were reported, and it was thus not possible to observe whether in practice there were informal processes capable of resolving them. As such, overall, a ‘partial’ rating is provided for both Masaligan and Kalamboan.

Finally, the groups’ rights to organise (principle 7) were not challenged by any external authorities; indeed, Masaligan and San Francisco were actively encouraged to do so:

We joined the group because the NHA, the National Housing Authority, is the one who encouraged us to organize savings groups under CCT. […] The NHA told us that there should be a savings group in every unit. (Participant S2)

However, external agencies (NHA and CCT) may have undermined the capability and autonomy, especially of San Francisco to devise its own institutions during its formative stage, which appear to have had lasting implications. As evinced in principle 3 and as a member described:

The group was not united on the proposed policy. Because the policy of CCT is different from the [desire] of the savings group […] We did not try to change the policy as we were no longer interested in staying in the group. (Participant S1)

Does Adherence to Institutional Design Principles Support Sustainability Outcomes?

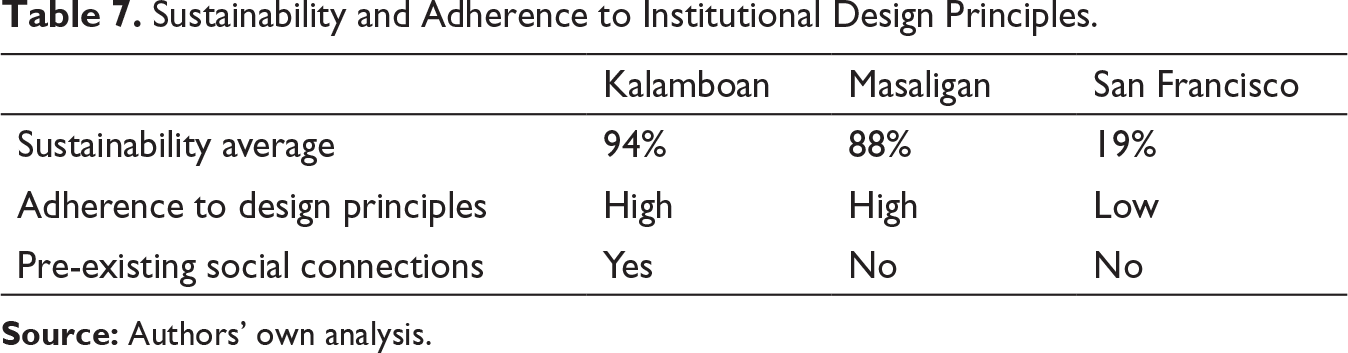

Sustainability and Adherence to Institutional Design Principles.

The institutional design principles enabled members of Masaligan and Kalamboan to cooperate, while trusting other members. The groups were able to design boundaries and rules that were beneficial to all members. When NHA and CCT tried to impose rules they presumed were appropriate for San Francisco, this had damaging consequences on the ability of the group to generate benefits for their particular circumstances. This in turn caused many members to ‘lose interest’. Genuine ownership over group rules matters. When asked why certain policies were followed, members of Masaligan and Kalamboan often simply stated ‘because it was decided by the group’. This attachment, alongside progressive sanctions, encouraged members to comply with rules. For example, where members of Kalamboan are withheld from the benefit of further loans if they have outstanding balances due:

I pay my loan every week so that I can avail another loan in the future. This is a good opportunity to save and borrow money, so I don’t feel comfortable breaking the rules, because of the benefits of the group. (Participant K1)

Trust and reciprocity are identified as key themes from interview participants in the two success cases. By being able to consistently monitor other’s behaviours, members of Masaligan and Kalamboan were able to build further trust that others were also cooperating. Members stated that they trusted in others because of their attendance at meetings, their history of compliance and transparency of records. Members themselves are able to build reputations as trustworthy reciprocators:

[Members trust me] because I already proved it. Every week, I pay my loans. Because it’s my obligation. (Participant K3)

The reverse was true of San Francisco, the least sustainable SCA. An influential group leader disagreed with the group rules on lending. Her perceived inability to change them led her to stop cooperating, and many members followed suit. The increasing lack of cooperation in the group resulted in rising levels of distrust among members. Even relatively compliant members responded negatively:

…after how many months, because most of our members were not giving their regular savings, I was discouraged [and] I stopped saving […] I could not enforce them, to tell them to save. (Participant S3)

Some studies have argued in favour of such trigger strategies—to cooperate if all players cooperate, otherwise defect forever (Gugerty, 2007)—rather than use progressive sanctions to elicit cooperation. The San Francisco case provides evidence to the contrary. When rule-abiding members also stopped cooperating completely, their own built reputations were destroyed. In line with Ostrom’s predictions, overall levels of trust depleted, ultimately crippling the group’s willingness to continue operating at all.

In summary, the analysis here demonstrates that institutional design principles directly influence the decision-making and behaviour of individual members, and support successful operations and sustainability. When SCAs lack such principles, members may find it difficult to cooperate and trust others to do the same.

Discussion

Kalamboan and Masaligan highlight the positive association between adherence to institutional design principles and sustainability. The groups are similar in many respects—size of group, proportion of female members and employment backgrounds. A key difference between them is that Masaligan members had experienced the devastation of Typhoon Yolanda and were subsequently, relocated to a new locality. The success of Masaligan suggests that pre-existing social connections appear not to be a necessary condition for constructing robust self-governing groups. Institutional design was able to sustain the group long enough for solidarity to accrue within and outside of group structures. Interviewees cited meetings as one of the most important aspects not just for monitoring and accessing services but also as a platform for building relationships and avoiding future conflict:

It would be insulting to just [access services] and leave. For me it is good that we attend the meeting so that we can … share with each other and learn more about the group. (Participant M1)

The experiences of San Francisco, however, highlight the challenges in making SCAs work long enough to build trust and relationships, which may have helped to supplement, or make up for deficiencies in, their institutional design. Future research might investigate further the conditions in which institutional design can interact with social capital to deliver sustainable SCAs.

Causal generalizations are limited in this small-n research design, but the trade-off is an ability to uncover rich data, refine the concept of sustainability, adapt the design principles to SCAs for the first time and gain insight into micro-level mechanisms of change. Future research could draw on the variables operationalised here to conduct large-n statistical analysis of causal effects, and qualitative studies could delve further into the relationships between the design principles and sustainability, for example, to understand better why two cases with ostensibly the same starting point (San Francisco and Masaligan) diverged in their self-governance early on. A further challenge is to investigate Ostrom’s eighth principle, not analysed here: the integration of SCAs into the larger financial system. Future research could also investigate whether older groups are able to achieve high levels of sustainability with lesser adherence to the design principles than younger groups—for example, because stronger foundations of trust and reputation (and social capital) built over time complement the institutional design principles. Signs of this are evident in the partial adherence of Masaligan and Kalamboan to graduated sanctions and formal conflict mechanisms, and the higher level of sustainability in Kalamboan (which is older and also reported pre-existing relationships). Longitudinal and panel research designs are needed to shed more light on the role of time in cementing the institutional principles, reciprocity and trust in SCAs.

Conclusions

SCAs are a key aspect of the financial lives of the poor. Yet there are gaps in our understanding of what accounts for sustainability in these self-governing, community-based organisations. This study provides an in-depth analysis of three SCAs located in Cebu, Philippines, and makes two contributions to the literature. First, we draw on Ostrom’s scholarship on governance of CPRs to create a framework of institutional design principles for local groups delivering microfinancial services. Sustainability of SCAs is deliberately defined more broadly than previous research and operationalised with novel indicators that better reflect the realities of SCAs on the ground. Our second contribution is to test the hypothesis arising from this framework using a new data set, which combines administrative data and interviews to better understand the lived experiences of SCA members and offers analytical leverage through careful case study selection. Our results show that adherence to Ostrom’s institutional design principles are positively associated with sustainability of SCAs.

We conclude that groups whose rules and practices embody the principles of clearly defined boundaries, recognition of local context, collective choice arrangements, monitoring, graduated sanctions, conflict resolution and rights of self-organisation report higher measures of sustainability. Further, our results indicate that while social capital is important in supporting sustainability, pre-existing social connections are not a necessary starting condition for SCA sustainability.

Our findings have practical implications for organisations promoting and engaging with SCAs, suggesting a more effective role for external agencies in creating an enabling environment for groups to independently craft sustainable institutions and recommending caution that their interventions do not unintentionally stymie these efforts. For example, looking ahead, more work is needed to understand the potential effects of mobile money technology for financial services. Linking SCAs to virtual cash boxes would allow members to save over the phone and avoid attending meetings. While this may be seen as safer than physical cash and time-saving, such an intervention may have unintended effects on the group’s institutional arrangements, such as their ability to monitor each other, build trust and relationships, and resolve conflict.

The findings will also be of interest to policymakers. The framework sets out a systematic approach to understanding the factors that affect sustainability. However, this approach is not an institutional blueprint, and local-level interpretations and applications of the principles will be important (Ostrom, 2010). Governments and donor agencies designing national financial inclusion strategies should look beyond formal service providers and consider local-level, user-owned and self-governed institutions as a low-cost, complementary approach to financial service access for all.

Interview Participants.

Coding Scheme for Trust and Reciprocity.

Footnotes

Acknowledgement

This research would not have been possible without the partnership and generosity of colleagues at the Centre for Community Transformation (CCT) and HOPE International. We are also grateful to the savings group members for inviting us to understand their experiences. The article has benefitted from the feedback of two anonymous reviewers; our thanks also go to Justin Fisher and Paolo Morini for their helpful suggestions.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.