Abstract

This research aims to analyse the Working Capital Management affects financial performance in Indian manufacturing sector. This research employs secondary data for data collecting from BSE, which comprises 20-year financial data from 2003 to 2022 using the sample of 419 companies. The study used descriptive statistics, random effects, and fixed effect models to define the sample and evaluate the influence of working capital management on manufacturing industry. Findings suggested that working capital management proxies have a major impact on the financial performance of the company. Proxy of CCC indicates that negative and significant impact of GOP, NPM, and NPR. The coefficient of ICP indicates that negative and significant relation between firm performances. In addition, we discovered a statistically significant inverse relationship between APP and GOP and NPM and NPR, suggesting that the more quickly a company in our sample pays its bills, the less profit it generates. The above table demonstrates that RCP has a positive and significant alliance with GOP. To the best of the author’s knowledge, this paper provides the study to examine the WCM’s effect for firm’s performance and contributes valuable insights on this company’s investors and managers.

Introduction

Corporate finance is a crucial aspect of any business organization. The decisions made by financial managers have a significant impact on the total profit of a company as well as the benefits to various stakeholders (Lefebvre, 2022). Working capital financing plays a crucial role in organizations’ liquidity management, allowing the firm to meet its day-to-day requirements without interruption. This affects not only the firm’s liquidity management but also its profit (Alkadmani & Nobanee, 2020). In essence, it is a managerial aspect in which financial managers determine the number of current assets and liabilities. Managers maintain contact with the risk minimization strategies and, as a result, implement a variety of routine operational softnesses that keep organizations on the safe side and in connection with the profit maximization strategies. Inadequate management of working capital is a significant reason for the failure of most small businesses in both developed and developing nations (Mardones, 2022). For a business to be successful, it is essential to have a thorough comprehension of working capital. As it directly affects the firm’s profitability and liquidity, it is regarded as equal to the management of fixed capital, even though it deals with current liabilities and current assets in every respect (Kayani et al., 2020).

The academics have conducted a large amount of research on topic of working capital management (WCM) and its impact on the performance of corporations (Ahmad et al., 2022). The great majority of academics found significant links between the management of working capital and the achievement of business goals. Most of the methods managers use to assess working capital are not based on well-established financial principles but on more subjective criteria or models. Working capital is defined as funds immediately available for use within an organization (Wang et al., 2020). In consideration of the conflicting results of prior research, a knowledge gap must be filled in order to gain a better understanding of WCM and how it affects a company’s profitability. The establishment of more exact tools for analysing a firm’s financial performance is acknowledged as a crucial pillar of modern economic research (Busch et al., 2022). Financial performance extent is essential for any business because it enables managers to determine the degree to which corporate objectives are being met; it aids managers in making decisions and implementing them; and it provides detailed information about the firm’s financial position and shareholder wealth creation (Agyemang et al., 2019).

However, accounting performance indicators such as gross operating profit (GOP), NPM, and NPR have been criticized for failing to represent an organization’s total cost of capital effectively. This means that accounting income cannot be used to accurately measure corporate success or interpret firm performance values (Ilham, 2020). Because GOP, NPM, and NPR are disregarded as prospective indicators of a manufacturing company’s performance, a significant gap exists. This leads to new discussion and the creation of a research gap. Financial managers spend a lot of time trying to figure out what drives working capital and how much of it they should have on hand at any one time (Faria et al., 2022). Making money at the expense of the company’s liquidity may have a detrimental effect on the company’s capacity to maintain its financial stability. As a result, the balance between the objectives of the two companies is necessary. In this connection, working capital cannot be kept at a minimum in the absence of operational limitations. In order to sustain future revenues and sales, businesses must optimize and safeguard their working capital. Different scholars have worked upon this topic worldwide by employing different sectors of data. Therefore, there is a shortage in the emerging countries under specific field notably on vehicle sector, if any of studies have been done is out to date (Vuong, 2022).

Investing decisions may also be influenced by this data. After conducting a study of WCM, the organization’s management may adopt a variety of activities. Regulatory agencies will work with nonfinancial sectors. These findings might help other firms improve their WCM operations. WCM in the automobile industry will improve as a result of this study, according to the findings. In this regard, students, scholars, accountants, financial managers, and policymakers in emerging economies should all benefit from an economic conceptual framework. According to the findings, producers calculate their profitability using a variety of methods. Thus, managing a company’s working capital is another way to evaluate how well it is doing.

The rest of the article is organized as follows: The ‘Review of Literature’ section discusses the past studies on WCM. The section ‘Research Methodology’ discusses the empirical model and variables. The ‘Empirical Results’ section presents results and discussion and the section ‘Conclusion’ concludes.

Review of Literature

Poor techniques of WCM hinder company ability to function successfully. The management of working capital is consequently a primary issue for CEOs. The majority of the research on WCM has been on the performance and profitability of WCM-using companies. Repeatedly, research demonstrates substantial correlation between successful WCM practices and enhanced corporate profitability (Lefebvre, 2022). Thus, depending on the industry and the environment in which an organization works, there are a range of connections between WCM strategies and company performance. According to Akbar et al. (2021), after-global-financial-crisis WCM policies of majority of organizations suggest that short-term financial goals are prioritized above long-term ones. According to the GMM approach, a concave connection exists between WCM practices and firm performance. Accounts payable turnover is the period required for suppliers to receive payment for the things acquired (Arcuri & Pisani, 2021). To achieve these goals, it is essential that each component be well managed to optimize working capital. WCM is therefore a managerial concern (Akbar et al., 2021). A crucial aspect of effective WCM for any business is ensuring that short-term obligations are thus fulfilled on schedule and long-term assets are adequately insured.

Using the current ratio, you can determine if an asset has enough money to cover its current liabilities, which are obligations due soon. Ilham (2020) says the company got a return on its assets, and a high current ratio shows its profits are also high. Investors might expect a high rate of return if earnings are high. Stock returns are improved by the current ratio. The current ratio is calculated by dividing CA by CL. Warrad (2014) found that current constraints on stock returns had a small but positive effect, while Alkadmani and Nobanee (2020) found that current rationing did not impact stock returns. This research will determine how WCM affects firm performance when the quality of governance acts as a moderator. The study’s findings will be useful to the nonfinancial sector investors and managers in developing and emerging countries.

Collection time is inversely related to the number of days before payment is due in the short-run activities. In this connection, there are several types of accounts that the company or organisation may give its consumers. Successful receivables management means being paid more quickly once sales are made. In return, the customers have a responsibility to treat organisation that provides the goods or services with respect. Reduce the amount of clients who are behind on their payments. Customers that owe money are those who have done business with company but have not yet paid for products or services they got. Account holder management’s major goal is to reduce the time it takes from the time a bid is submitted to the time an instalment is accepted. (Mielcarz et al., 2018)

SG is an increase in sales that happens over the course of a year or on an irregular basis, according to Mukti and Milikan (2015). Managers use a variety of methods to figure out how much working capital they need. A concave connection exists between WCM practices and firm performance. Accounts payable turnover is the period required for suppliers to receive payment for things acquired. Businesses with strong sales growth will need to make more investments in different kinds of assets, whether they are fixed assets or current assets. Hantono (2018) says that the company can figure out how much funds it will make by predicting how much sales will go up. One way to measure the company’s sales growth from one year to the next is to use the sales growth ratio. Sales growth ratios have an effect on profitability, and profitability has an impact on company operational performance.

Mardones (2022) in general, firm profitability is a useful metric since it considers the interests of shareholders. Based on the value of shareholders, FP may be used as an indicator of the company’s overall success. Because GOP, NPM, and NPR are not taken into account as ways to measure how well a manufacturing company is doing, there is a big gap. This leads to new discussion and creation of a research gap. As a financial theory tool, GOP has been widely utilized to explain many aspects of economics. GOP has been examined extensively by a broad spectrum of scholars, including psychologists (Muhtadi, 2019; Singhal et al., 2016). According to Perera and Priyashantha (2018), GOP is defined as the sum of equity and liabilities multiplied by total assets. As it directly affects the firm’s profitability and liquidity, it is regarded as no less than management of fixed capital, despite the fact that it deals exclusively with current liabilities and assets. As a result, balance between objectives of two companies is necessary. Company GOP is equal to the market value multiplied by cost of replacing its assets. It is possible to resell company’s property for profit if GOP is larger than one as opposed to one. Businesses with higher GOP values, according to Fitriani, (2020), perform better over the time than those with lower GOP values, which are likely to do significantly worse.

Contrary to numerous studies conducted in various countries in the past, these results contradicted their conclusions. Consequently, it is pertinent and intriguing to investigate the nature of the relationship between WCM and the profitability of Indian manufacturing companies.

Research Methodology

In this section, we will discuss the technique that was used for the study. It provides a description of the research design, the specifications of the model, the definition and measurement of the variables included in the model, estimation methodologies, sources of data, and tools for the analysis of data.

Data Source

Using the sample of 419 companies, we obtained firm-specific data from the yearly financial statements of listed companies operating in the Indian manufacturing sector using the CMIE Prowess database for 2003–2022. In this study, the firm’s performance is the dependent variable measured using GOP, NPM, and NPR. The independent variables are the cash conversion cycle, inventory conversion period, receivables collection period, account payables period, debtor’s turnover ratio, and inventory turnover period. Firm size, sales growth, debt-equity ratio, current ratio, and cash flow were the control variables sourced from the individual firms’ financial statements.

Model Specification

The study used these models to explain the importance of the observed variations among the firms and the desired impacts of the selected variables inside the sampled organizations over time. Following Sharma and Kumar (2011), Amin and Islam (2014), Yazdanfar and Ohuman (2014), Tutino and Pompili (2018), Alvarez et al. (2021), Diwei et al. (2022), Garg and Meentu (2022), Shukla et al. (2022), and Sinha and Vodwal (2022), the following static panel models were adopted:

Fixed Effect Model

where

Random Effect Model

where

Definition and Measurement of the Variables

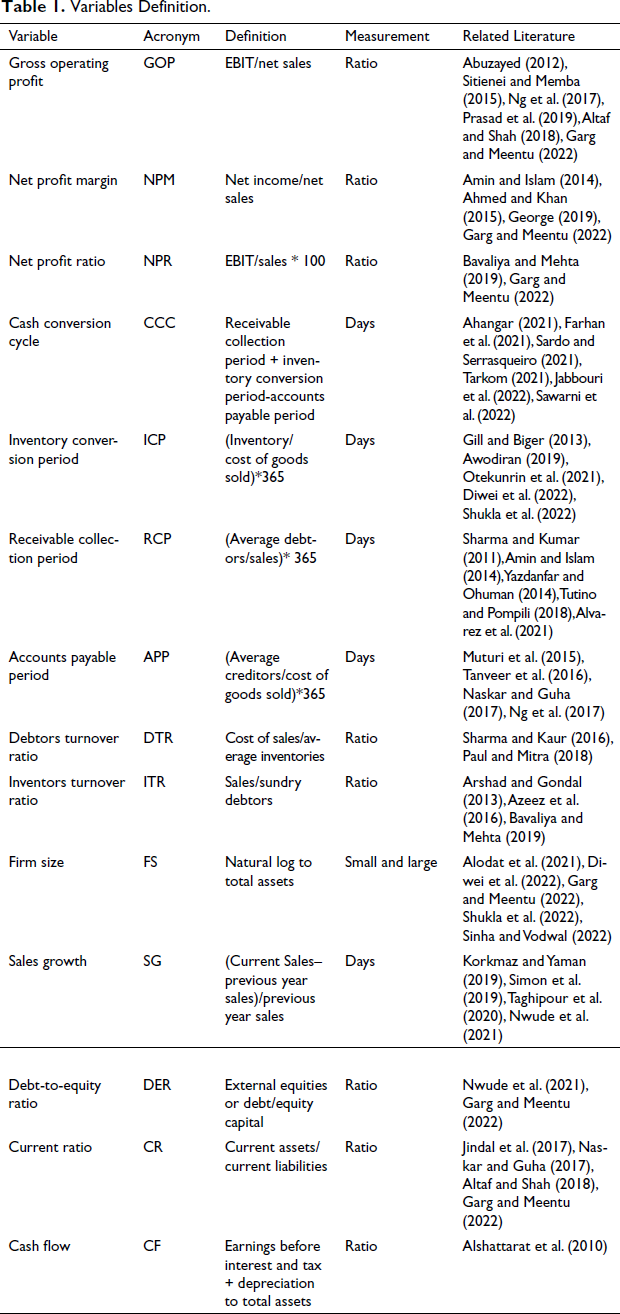

Table 1 indicates how the variables are defined and measured.

Variables Definition.

Empirical Results

This section contains the article’s findings and analysis. Following the presentation of descriptive statistics are analyses of correlation and panel regression, as well as a discussion of the results.

Descriptive Statistics

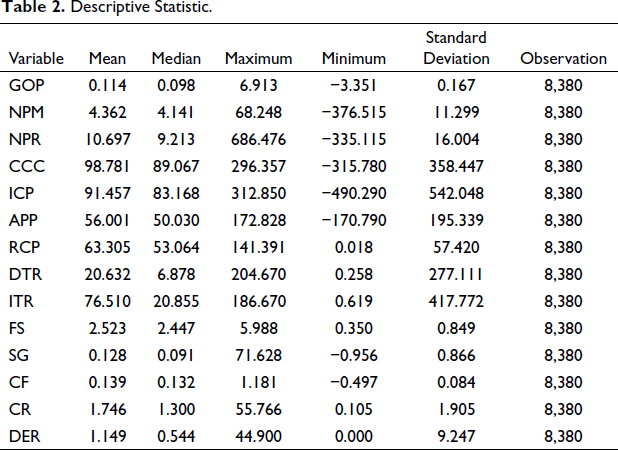

According to Table 2, the variables relevant to the study are presented in descriptive statistics. A mean provides an overview of a collection of values by determining their averages. As a measure of how values are spread around the mean, the standard deviation is used. A variable’s range can be determined by its minimum and maximum values. It is determined that there are a total of 8,380 observations. It is clear from Table 2 that all the different variables had positive average values, often known as means. The dependent variables, GOP, NPM, and NPR had a respective mean of 0.114, 4.362, and 10.697 that was greater than their respective standard deviations (0.167, 11.299, and 16.004), indicating less variability around the means. The mean values of CCC, ICP, APP, RCP, DTR, and ITR are 98.781, 91.457, 56.001, 63.305, 20.632, and 76.510, respectively, and their standard deviations are 358.447, 542.048, 195.339, 57.420, 277.111, and 417.772, respectively, over the sample period, with minimum values of –315.780, –490.290, –170.790, 0.018, 0.258, and 0.619 and maximum values of 296.357, 312.850, 172.828, 141.391, 204.670, and 186.670, respectively, indicated the range of the variables. For the Firm Size (FS), Sales Growth (SG), Cash Flow (CF), Current Ratio (CR), and Debt Equity Ratio (DER) the mean values are 2.523, 0.128, 0.139, 1.746, and 1.49, which are greater than their standard deviations (0.849, 0.866, 0.084, 1.905, and 9.247), respectively, over the sample period, with minimum values of 0.350, –0.956, –0.497, 0.015, and 000 and maximum values of 5.988, 71.628, 1.181, 55.766, and 44.900, respectively, indicating the range of the variables.

Descriptive Statistic.

Correlation Matrix

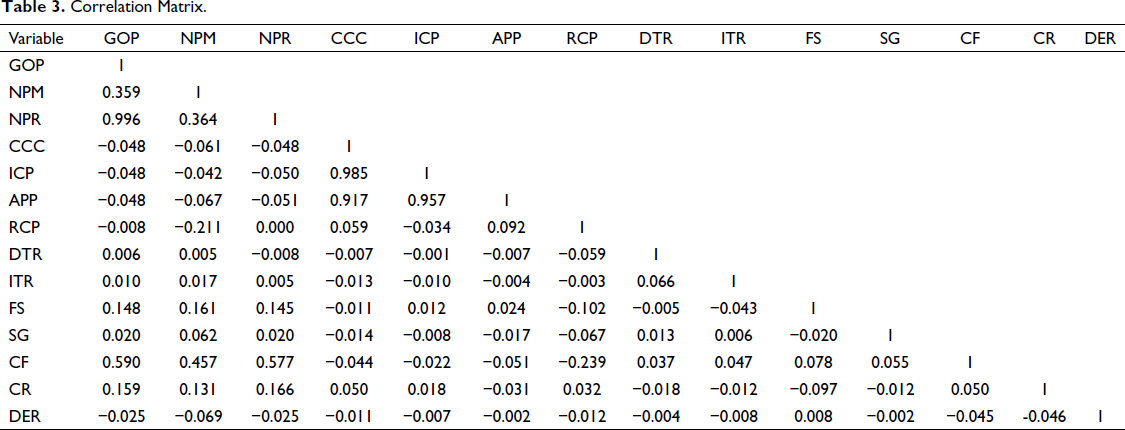

Table 3 of correlation matrix indicates that majorly, there is a positive correlation between independent variables. Further, the table indicated negative relationship between some variables. Table 3 indicated that CCC has positive correlation with ICP and APP, with values 0.985 and 0.917. The table indicated that no value of r is higher than 0.800, which is why there is no chance of multicollinearity in data.

Correlation Matrix.

Impact of WCM of GOP

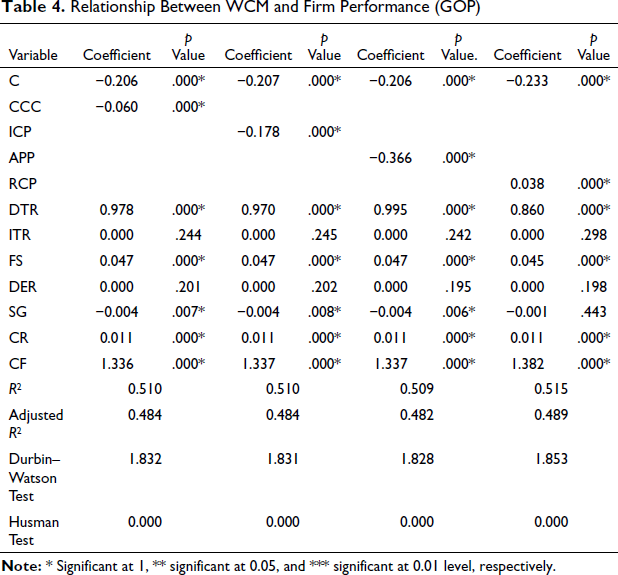

Table 4 displays the results of GOP using two models: Random Effect Model and Fixed Effect Model. In Table 4, fixed effect model is the best-fitted model. The findings reported in this section are derived from the fixed effects model, which successfully accomplished the study’s objectives about the influence of WCM on GOP.

Relationship Between WCM and Firm Performance (GOP)

Findings show that manufacturing sector should have proper management of cash regarding speedy collection. Proxy of CCC indicates that negative and significant impact of GOP. To put it another way, profitability will suffer if there is a longer gap between cash receipts and payments. However, increasing the number of days required for the cash conversion cycle will delay the receipt of incoming funds. As a result, there is an imbalance in cash holdings and limited availability of liquidity. The coefficient of ICP indicates that negative and significant relation between firm performances. According to this study, increasing the number of days inventory is kept means less money is made. Additionally, if it takes longer to sell the stock, it will cut into profits. The ratio of accounts payable to total revenue (GOP) tends to be negative. This trend suggests that successful businesses are taking longer to settle their bills. This indicates that companies are delaying payments to their debtors to meet their immediate working capital requirements. The above table demonstrates that RCP has a positive and significant alliance with GOP at 1% of significance level. Similarly, the outcome of reveals that the DTR of the company as an independent variable has a positive and significant impact on firm performance. Similarly, the outcome reveals that size of company, current ratio, and cash flow as a control variable has positive and significant effect on firm’s performance, while the coefficient of sales growth has negative and significant impact of firm performance.

Impact of WCM of Net Profit Margin

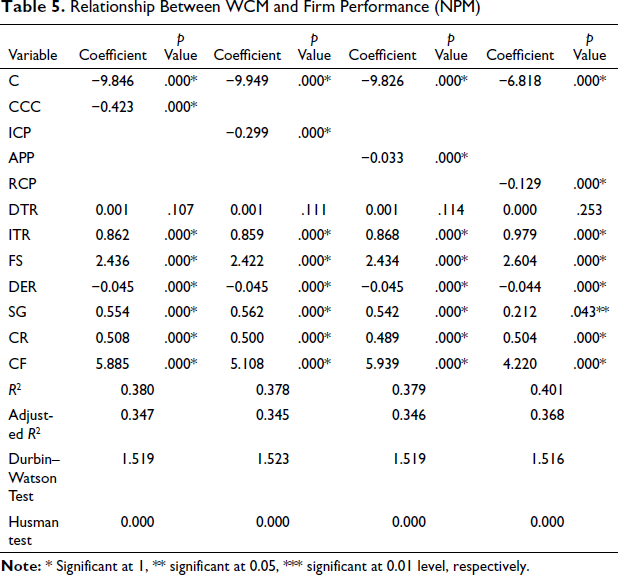

Table 5 displays the results of net profit margin using two models: Random Effect Model, and Fixed Effect Model. Table 5 displays the outcomes of a Hausman test performed to determine which model (fixed or random) should be used for the subsequent round of regression analysis. The results of an investigation into the influence that the management of working capital has on the net profit margin (NPM) are presented in Table 5. This investigation was carried out using a fixed effects model.

Relationship Between WCM and Firm Performance (NPM)

The CCC is shown to have a coefficient value of –0.423, which indicates that a one-day increase in CCC will cause a fall in NPM of 0.423 units, with this finding being statistically significant at the 1% level. The coefficient value for ICP is negative (–0. 299) and significant at a 1% level. In other words, raising ICP by one-day results in a 0.299 NPM decrease. As a result, this study came to the conclusion that APP had a significantly negative impact on profitability (NPM). When performing APP, it showed a coefficient value of –0.033, meaning that when APP increases by one day, NPM will fall by 0.033 units. At a 1% level, the result is significant. As a result, this study concluded that APP has a negative, significant impact on profitability (NPM). The RCP is also shown with a coefficient value of –0.129, which indicates that the NPM will fall by 0.129 units if the RCP is allowed to increase from one day to the following while all other independent variables are held constant. This finding is statistically significant at the 1% level. Other variables are significant in firm performance except for DTR.

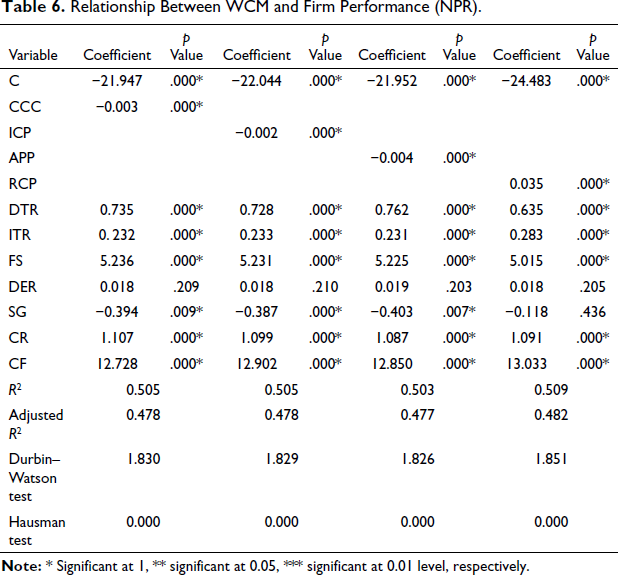

Impact of WCM of Net Profit Ratio

The R-square value in this research is approximately 0.509%. This suggests that CCC, ICP, APP, RCP, DTR, ITR, FS, DER, SG, CR, and CF contributed to 50.90% of the variance in profitability. However, other variables not included in this analysis explain 49.10% of the variance in profitability. Table 6 compares the outcomes of the REM and the FEM for the net profit ratio. Results from the fixed effects model, which were used to determine the influence of WCM on the net profit ratio (NPR), are presented in Table 6.

Relationship Between WCM and Firm Performance (NPR).

Table 6 summarizes the expected overall profitability of WCM. The coefficient value of –0.003 suggests a more significant negative effect of CCC on profitability (NPR). The outcomes also demonstrate the firm’s capability to control the structures of current assets and liabilities and to determine the ideal value of such things as current liabilities, inventory, receivables, and cash.

Additionally, CCC is viewed as a measure of the organization’s ability to use its current assets to service its current debt, ensuring that the firm has sufficient resources to finish its operation, and maintain high levels of inventory conversion to cash and maximum profitability. The data shows a negative relationship (–0.004) between NPR and ICP, suggesting that the selected companies have low asset and product turnover. Profitability is highly sensitive to variations in inventory turnover. As a result, the company’s inventory policy must be carefully considered. In addition, we discovered a statistically significant inverse relationship between APP (–0.004) and NPR, suggesting that the more quickly a company in our sample pays its bills, the less profit it generates. If the company can collect on its accounts receivable, as the RCP suggests, it will boost its financial performance. Except for DER, other criteria are relevant in explaining a company’s success.

Conclusion

This research looked at the factors that influence a firm’s profitability, specifically impact of WCM, using data from Indian Manufacturing period from 2003 to 2022. Ratios used as a proxy for WCM in publicly listed and nonlisted firms operating in India were calculated using data from manufacturing sector financial annual reports spanning the years 2003–2022. The results indicate that the CCC, ICP, APP, and RCP as proxies for WCM have a significant impact GOP, NPM, and NPR as predictors of firm performance. The findings of study bridging the gap of literature by stating WCM and sales growth are vital indicators of manufacturing sector firm performance. The scope of study is limited to 419 listed manufacturing firms and two nonlisted enterprises. The research was limited to secondary data acquired from all of BSE’s respective yearly financial reports.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.