Abstract

Aligning private finance with the Sustainable Development Goals (SDGs) promises to close the multi-trillion-dollar SDG ‘financing gap’ while unlocking trillions more in market opportunities. This article explores the processes mobilised for this alignment in Indonesia, an emerging country exemplified as a site where such opportunities are profuse. We do so through assessing modalities of planning, prototyping and building project pipelines designed to facilitate market development for green and SDG bonds. As these types of bonds are supposedly used only to finance socially and environmentally beneficial projects, they are placed at the forefront of innovations to align financial returns with sustainable development outcomes. To make sense of what these forms of innovative finance do, we weave scholarship on the financialisation of development and on (shifting) governance practices surrounding the development project, together with empirical material gathered from SDG finance events, document analysis and semi-structured interviews. We argue that the processes shaping market development for green and SDG bonds functionally iterate upon and extend an open-ended project of making development legible to capital: to see and act on the SDGs as an investable proposition. This legibility rests upon and engenders standard(ising) techniques to define what counts as ‘green’ and ‘sustainable’ in ways that (in)visibilise impacts, promising – albeit speculatively – the realisation of social, environmental and financial goals. Here, the SDGs provide the institutional locus to enliven this promise, erasing the unevenness of finance-oriented development and legitimising capitalist modes of ‘seeing’ and ‘doing’ development around this promissory imaginary.

Introduction

There is apparently a persistent financial gap that stands in the way of the Sustainable Development Goals (SDGs), a set of global goals agreed in 2015 by United Nations member states to serve as ‘the blueprint to achieve a better and more sustainable future for all’ (United Nations, 2023). In developing countries, the gap is estimated to be US$ 2.5 trillion per year pre-COVID-19 pandemic, which was projected to have risen to US$ 4.2 trillion in 2020 alone (OECD, 2020). What comes with this yawning gap, though, is a supposedly greater market opportunity waiting to be ‘unlocked’, for which ‘intelligent’ and ‘innovative’ development finance is essential given the limits of public funding and conventional approaches (Development Committee, 2015). 1 Money is not the central issue here, with only 1% of wealth in global capital markets needed to close the SDG financing gap (Steiner, 2018). Accessing this wealth for the SDGs, however, is premised on correcting the misalignment between the SDGs and public and private finance (Development Committee, 2015; United Nations, 2015).

Policy propositions to correct this misalignment permeate through key agendas for financing the SDGs: the United Nations Addis Ababa Action Agenda on Financing for Development, the Secretary-General Strategy for Financing the 2030 Agenda and the multilateral development banks’ From Billions to Trillions: Transforming Development Finance (Development Committee, 2015; Guterres, 2019; United Nations, 2015). These agendas stipulate that (re)allocating private capital towards the SDGs hinges on, in part, ‘appropriate incentives’ and ‘transparent, stable and predictable investment climates’ (United Nations, 2015: para 5, 36), given that ‘private resources move in directions determined by risk-reward considerations’ (Development Committee, 2015: 3). Consistent with this framing, the Organisation for Economic Cooperation and Development (OECD) conceives of SDG alignment as: … a means to mobilise resources for the implementation of the 2030 agenda and a value proposition to preserve the long-term value of assets by doing no harm and contributing solutions to sustainable development challenges, thereby reducing risks and enhancing resilience of the global financial system (OECD, UNDP, and Ministère de l’Europe et des Affaires étrangères 2020: 4, emphasis added).

Development interventions, in this context, ought to purposefully design, test, and iterate projects and financing arrangements for bankability alongside sustainability (UNDP, 2018). Indeed, bankability – the balance between revenue generation and risk – is now a watchword in SDG finance circles, framed as essential to bring SDG finance at scale (See Guterres, 2019; OECD, UNDP, and Ministère de l’Europe et des Affaires étrangères, 2020; World Bank, 2019).

In this article, we explore the alignment being drawn between finance and sustainable development in an emerging country context: Indonesia. We ask what processes are mobilised for this alignment? What part do the SDGs play in these processes? When placed in context, what can they tell us about contemporary ways of seeing and doing development? We grapple with these questions by assessing modalities of planning, prototyping and building project pipelines intended to facilitate market development for green and SDG bonds: fixed income debt instruments valorised as innovative means to narrow the SDG financing gap (See OECD, 2021; United Nations Global Compact and UNEP Finance Initiative, 2019). Although these bonds are structured in much the same way as conventional bonds, their proceeds are earmarked for projects considered more ‘future proof’ in the face of imminent and longer-term socioecological risks (Jones et al., 2020; Tripathy, 2017). In promising financial returns alongside resilient and sustainable outcomes, these bonds are viewed as instruments of SDG alignment (OECD, UNDP, and Ministère de l’Europe et des Affaires étrangères, 2020).

Indonesia is an emblematic case study for a number of reasons. The country is said to face an immense SDG financing gap, estimated to be at US$ 4.7 trillion (United Nations Indonesia, 2021). It is a pioneer of sustainable finance in the region and has assumed global leadership in innovative financing to bridge this gap, notably through its G20 presidency (OJK, 2015; Setyowati, 2020). It is also profiled as a key prospective sustainable investment destination (AlphaBeta, 2017; Climate Bonds Initiative, 2022). Since the advent of the SDGs, numerous initiatives ostensibly aiming to design and scale up bankable project pipelines, and instruments to finance these projects, have proliferated. 2 This includes SDG Indonesia One, a blended finance facility established within the state-owned enterprise PT Sarana Multi Infrastruktur (hereafter PT SMI) to mobilise SDG-aligned finance for infrastructure development. Moreover, Indonesia is reputed as ‘one of the savviest emerging market sovereign borrowers’ (Davis, 2020), on account of a reform programme to accelerate capital market deepening under Finance Minister Sri Mulyani (Office of Assistant to Deputy Cabinet Secretary for State Documents and Translation, 2022; Samboh and Wirayani, 2016). In 2019, Indonesia was the largest source of green bond issuance in the Association of Southeast Asian Nations (ASEAN) region (Climate Bonds Initiative, 2019), and in 2021, it became the first Southeast Asian nation to issue a sovereign SDG bond (UNDP 2021).

These initiatives reflect an evolving development financing landscape that is increasingly shaped by interventions to create markets for sustainable finance, within Indonesia and elsewhere (Hayati et al., 2020; Mawdsley, 2018a). PT SMI, for example, positions itself as a ‘market maker’ and an ‘ecosystem enabler,’ where it works within an ‘ecosystem’ of regulators, project owners, donors and financiers in testing innovative financing solutions with an eye to finetuning policies and regulations and developing the ‘right’ financial/environmental market knowledge needed for sustainable finance to grow (Dalel, 2020). This embrace of the iterative nature of market development corresponds well with the shift ‘from planning for outcomes to planning for uncertainty’ shaping capital markets across Southeast Asia, where ‘it is the promissory – if not speculative – future of finance that finds expression in variegated market designs’ (Rethel, 2018: 186, 191 emphasis in original).

In this context, what undergirds market development for green and SDG bonds is not so much an innovative endeavour as a recursive iteration of a high-modernist, technocratic-capitalist mode of seeing and doing development: to see and act on the SDGs as an investable proposition. In seeking to align the SDGs with the goals of finance, the development of green and SDG bonds rests upon and engenders categorical logics and technical expertise that Scott ([1998] 2020) posits as markers of high modernism, insofar as they produce abstractions to make the proposition of rendering the SDGs investable seem plausible and necessary (see also Harvey, 1989). As will be illustrated, market development for green and SDG bonds abstracts what is of little interest to finance capital. It engages in simplifications to authorise what counts as green and sustainable in ways that (in)visibilise impacts, promising – albeit speculatively – social, environmental and financial gains. Crucially, given that ‘for capitalists, simplification must pay (Scott ([1998] 2020: 8),’ this shapes the interventions that are imagined (their forms and scale) and financed.

In what follows, we proceed by setting the scene for our inquiry, weaving together current official discourse and practice around unlocking SDG finance with scholarship on the financialisation of development, and (changing) practices of simplification and legibility surrounding the development project. We then outline our methodological considerations in Materials and methods section. In Plans, prototypes and project pipelines: Aligning private finance with the SDGs section, we trace three vignettes to represent various processes of simplification in the market development for green and SDG bonds in Indonesia. Foregrounding the role of the SDGs, we consider the promise and limits of these simplifications in The promise and limits of ‘innovative’ debt financing for the SDGs in Indonesia section. The final section concludes.

The SDGs, financialisation and (sustainable) development that capital can ‘see’

The SDGs: An investable proposition

Writing on trends in development policy and practice that were unfolding in the lead up to the SDGs, Emma Mawdsley (2018a: 265) suggests that we are witnessing ‘a deepening nexus between financial logics, instruments and actors, and “intentional” development: that is, the ideologies, programmes and practices of the “mainstream” international development community.’ She attributes this financialisation-development nexus to a confluence of factors beyond the SDGs, including changing geographies of foreign aid and development cooperation, and of wealth, poverty and inequality (Mawdsley, 2017; 2018a). In this particular conjuncture, however, the SDGs provide a ‘legitimating veneer to the development industry's current work to create investment opportunities in “frontier” economies’ (Mawdsley, 2018b: 193). Indonesia is such a frontier – a site of discoveries and opportunities – with its vast natural resources, rising middle class (consumer base) and large working population (labour force) (IMA Asia, 2016).

In this deepening nexus, a key narrative goes that as the custodian of large pools of finance capital, only the private sector can bring SDG finance at scale, and that, given the right conditions, ‘large-scale capital eagerly awaits the right kinds of projects’ (Cohen et al., 2021: 2). Proffered as a prize for the private sector, the SDGs are said to harbour a US$ 12 trillion per annum business opportunity in four sectors alone – food, cities, energy and materials and health and well-being – with developing countries accounting for more than half the value of SDG business opportunities (AlphaBeta, 2017; Guterres, 2019; OECD, UNDP, and Ministère de l’Europe et des Affaires Étrangères, 2020).

3

Yet, underinvestment in these sites of immense possibilities remains prevalent. This, as the Addis Ababa Action Agenda on Financing for Development makes explicit, is attributed, in part, to: an insufficient number of well-prepared investable projects, along with private sector incentive structures that are not necessarily appropriate for investing in many long-term projects, and risk perceptions of investors (United Nations 2015: para 47).

Put simply, it is not a lack of money, but a lack of investable projects with the right risk-reward profile and appropriate incentives that hinder private sector participation in financing the SDGs (See also Development Committee, 2015; Nassiry et al., 2016). The assumption, then, is that unlocking finance for the SDGs hinges on growing the availability of investable projects.

Nothing perhaps expresses this more clearly than the increasing purchase of ‘bankability’ and ‘scalability’ to complement ‘sustainability’ in interventions designed to align private finance with the SDGs (Guterres, 2019; OECD, UNDP, and Ministère de l’Europe et des Affaires étrangères, 2020). Many development institutions operating within and across national borders are now busily involved in seeking and marketing bankable and scalable development interventions, including innovative financing instruments, to attract finance capital (See Climate Bonds Initiative, 2022; Joint SDG Fund, 2023; OECD, 2020; UNCTAD, 2017; 2018; United Nations Indonesia, 2021; UN DESA, 2022b). The aim is not only to make development interventions sufficiently bankable (and therefore investable), but also replicable or transferable from one context to another (and therefore scalable) (UNDP, 2018).

The making of such interventions, it has long been noted, necessarily depends on a categorical logic to figure subjects, objects and relationships ‘that capital can see’ to make them amenable to financial calculation and management (Robertson, 2006: 367; see also Gabor and Brooks, 2017; Hilbrandt and Grubbauer, 2020; Sullivan, 2018). With regard to this way of seeing, a key debate emerging within the broad ambit of financialisation in conservation and development centres on the translation and integration of social and environmental ‘externalities’ into categories of manageable risk. Risk, writes Bracking (2019: 710), ‘benefits from being already central to the lexicon of finance capitalism.’ Tripathy's (2017) ethnographic research on green bonds standards is illustrative of this, demonstrating how the practice of labelling projects as green revolves around the identification and management of green risks. In this endeavour, environmental uncertainties are translated into material risks that can be valued and incorporated into financial decisions and management (e.g. how climate may affect the future value of projects/assets) (Tripathy, 2017; see also Schmidt and Matthews, 2018). This translation, as Jen Christiansen (following Jen Beckert) argues in their study on marine conservation ‘blended finance’, forms fictional expectations, ‘in the sense that no serious truth claims can be made regarding events that lie in the future’ but nevertheless shapes investors’ expectations (Beckert as cited in Christiansen, 2021: 95).

The notion of bankability informs such states of expectation. Whether an investment is bankable depends on the calculation of risks to assure investors that the proposed investment is safe, which goes beyond the features of the investment alone (Nassiry et al., 2016). It is equally shaped by a set of ‘enabling conditions’ – the appropriate legal and regulatory framework, creditworthiness, perceived credibility and institutional capacity – determining the probability of the investment to meet its social, environmental and financial goals (Nassiry et al., 2016). In other words, the bankability of an investment demands simplifications that stabilise the fluid dynamism of social, environmental and political milieus to make investments safe under conditions of uncertainty.

In the case of green bonds, their production, value and sale similarly rest on (speculative) modes of abstraction that are sufficiently credible to convince participants to engage in new markets (Bracking, 2015; 2019). Here, standards bring such credibility, ‘making perceived greenness visible’ (van Veelen, 2021: 135, emphasis in original; see also Bracking, 2015). This is accomplished through what Perkins (2021: 2045) calls ‘a lenient zone of qualification,’ which ‘establishes broad protocols over process but has permitted a high degree of decentralised regulatory plasticity with regard to the meaning of green.’ For instance, the Green Bonds Principles – a voluntary process guideline on green bond issuance – focuses (as expected) only on process, where greenness is ascertained through whether issuers possess the right governance arrangements with regard to project selection, use and management of proceeds and reporting (International Capital Market Association, 2021). The establishment of greenness, as such, is once-removed from the objects of investments. Finance, then, does not necessarily land where the most significant environmental or social contribution could be made. Rather, where finance lands hinges on how greenness or sustainability comes to be defined, valued and accepted within a particular green/sustainable economy that is being assembled (Asiyanbi, 2018; 2021; van Veelen, 2021).

On this point, Rethel's Debordian view of capital market development in Southeast Asia is deeply relevant. 4 Rethel (2018: 191) argues that financialisation, to a considerable extent, is not about outcomes per se, but about facilitating process that sustains, and is sustained by, ‘the promissory future of finance.’ This is mediated through the re-enactment, circulation and validation of specific forms of knowledge to legitimate capital market development (Rethel, 2018). Routine, standardised valuation of greenness and sustainability that accompanies the issuance of thematic bonds is one means through which such knowledge travels. Standardised valuation, some suggest, is therefore significant not so much for the way it influences the attributes and outcomes of projects to be financed, but for the way it legitimates the market development they promote (Hilbrandt and Grubbauer, 2020). It helps form, in short, a legible terrain where capital would land.

Simplification and legibility: On the recursion of high modernism

The valuation and standardisation techniques deployed to align private finance with the SDGs are characteristic of the high modernist ideology that Scott ([1998] 2020: 4) describes in Seeing Like a State as ‘a faith that borrowed, as it were, the legitimacy of science and technology.’ Like the high modern schemes detailed in Seeing Like a State, forging such an alignment is inevitably schematic, in which careful planning is needed to constitute a field of intervention that makes commensurate social, environmental and financial goals (Scott [1998] 2020). Thus, as aforementioned, environmental concerns become subsumed in the financial grammar as categories of green risk, the management of which necessitates specific technical expertise that transcends context. There is, then, a continuity between the work to align private finance with the SDGs and the high modern schemes of Scott's critique, in terms of the concern to delimit and discipline the logics and techniques of governance. In this light, what of innovation? The post-2015 development landscape is awash with innovations purportedly aiming to do development differently (UNDP 2018). As the UNDP puts it, ‘[t]he sheer scope of the SDGs requires us to invest in disrupting old ways of working, to imagine, design and test new forms of infrastructures and platforms’ (UNDP, 2018: 8).

Indeed, many development interventions no longer embody the archetypal forms (or styles) of seeing and governing that Scott critiques (see Johns, 2019; Li, 2005). Approaches to bring SDG finance at scale seem to deviate from high modernist tendencies, favouring experimentation over rigid planning: to ‘innovate, test and iterate to find the most effective interventions’ (UNDP, 2018:28). The proliferation of financing labs dedicated to designing and testing innovative instruments to scale up SDG finance is expressive of this. 5 The connotation of the ‘lab’ suggests a kind of change that Scott ([1998] 2020) advocates as an antidote to high modernist planning: to design in, rather than ignore, more experiential, open-ended knowledge into policy and practice. The leeway afforded in the implementation of the SDGs also seems to eschew top-down, homogenising tendencies of high modern planning (Biermann et al., 2017). These circumstances share some resemblance with what Johns (2019: 853; 863) stylises as a shift from planning to prototyping insofar as they engender the ‘possibilities being worked up iteratively and inductively,’ a shift that demands attention to the ‘politics of prototypical technique, rather than… the politics of the master plan.’

While attention to the politics of prototypical technique is certainly needed, there are at least two things that can potentially become lost in juxtaposing ‘planning’ with ‘prototyping’. First, prototypical techniques are not new. A prototype is ‘the first example of something… from which all later forms are developed’ (Cambridge Dictionary, 2023). Pilot projects – long-existing and ubiquitous forms of development interventions – are, for all intents and purposes, prototypes: experimental objects designed to be ‘tested’ and reworked (Li, 2007; Massarella et al., 2018). Thematic bonds, too, are objects from which all later forms are developed (Bracking, 2019). Second, and relatedly, this juxtaposition renders the relationship between planning and prototyping less thinkable. Recall, however, that Scott ([1998] 2020), writing on scientific forestry, conveys that a planned environment such as monocropping provides a legible terrain with which to conduct experimentation ‘that could be codified and taught’ to further advance scientific forestry (Scott [1998] 2020: 20). In the case of green and SDG bonds, their production, sale and replication cannot proceed without planning to standardise what is eligible for green/SDG financing (Lazarova, 2016; OECD, 2021), itself a project of legibility at a global scale. Planning and prototyping, in this instance, provisionally co-shape and reinforce one another in attempts to produce interventions that could be categorised, learned and replicated within and across scales.

This aspiration to standardise greenness and sustainability is resolutely high modernist, but this does not mean it is not iterative. It is necessarily so because simplification and legibility are prone to failures and contradictions: they rarely do what they ought (Scott [1998], 2020; see also Blomley, 2008). These failures and contradictions are themselves productive grounds for interventions, feeding what Li (2005) calls the ‘general problematic of “improvement”:’ a continuing effort to rectify the deficiencies of development interventions. But interventions to remedy the undesirable consequences of high modernist schemes are often recursive, in the sense that they are thought out within the bounds, and therefore distil and reinscribe (at least partially), a narrow set of objectives and optics (Li, 2005; Scott, [1998] 2020). Li's (2007: 231) account of a World Bank village development programme in Indonesia, for example, shows that while the project sought to understand village life from the ‘bottom-up’, the resultant diagnosis and interventions remained the purview of experts who saw poverty through a lens that excluded many political-social matters ‘from the program's knowable, technical domain.’ In contemporary tech-based climate governance, Leiter and Petersmann's (2022) inquiry into prototypical techniques demonstrates the ways in which high modernist tendencies remain pronounced in innovations for climate challenges, many of which claim to attend to local context while aspiring for universal application. Troubled with experimental failures emerging from valuation techniques that sought commensurability across difference, the financialisation of development, too, builds on earlier iterations of commodification and financialisation of socionatures (See Bracking, 2019; Robertson, 2006; Sullivan, 2018; Tripathy, 2017). As Bracking (2019: 724, emphasis added) puts it, ‘[c]oncepts of carbon, greenness, resilience and insurance-based accounting, each loosely derived from the phases of a deepening financialisation, come together and correlate in acts of contingent becoming.’ These contiguous phases of deepening financialisation reify a polity where capitalism is reproduced – time and again – through the project of social and ecological repair (Cohen et al., 2021). These examples alert us to look beyond binary prisms such as ‘planning’ and ‘prototyping’, and to refrain from distinguishing too sharply and too readily between what is old and new.

Materials and methods

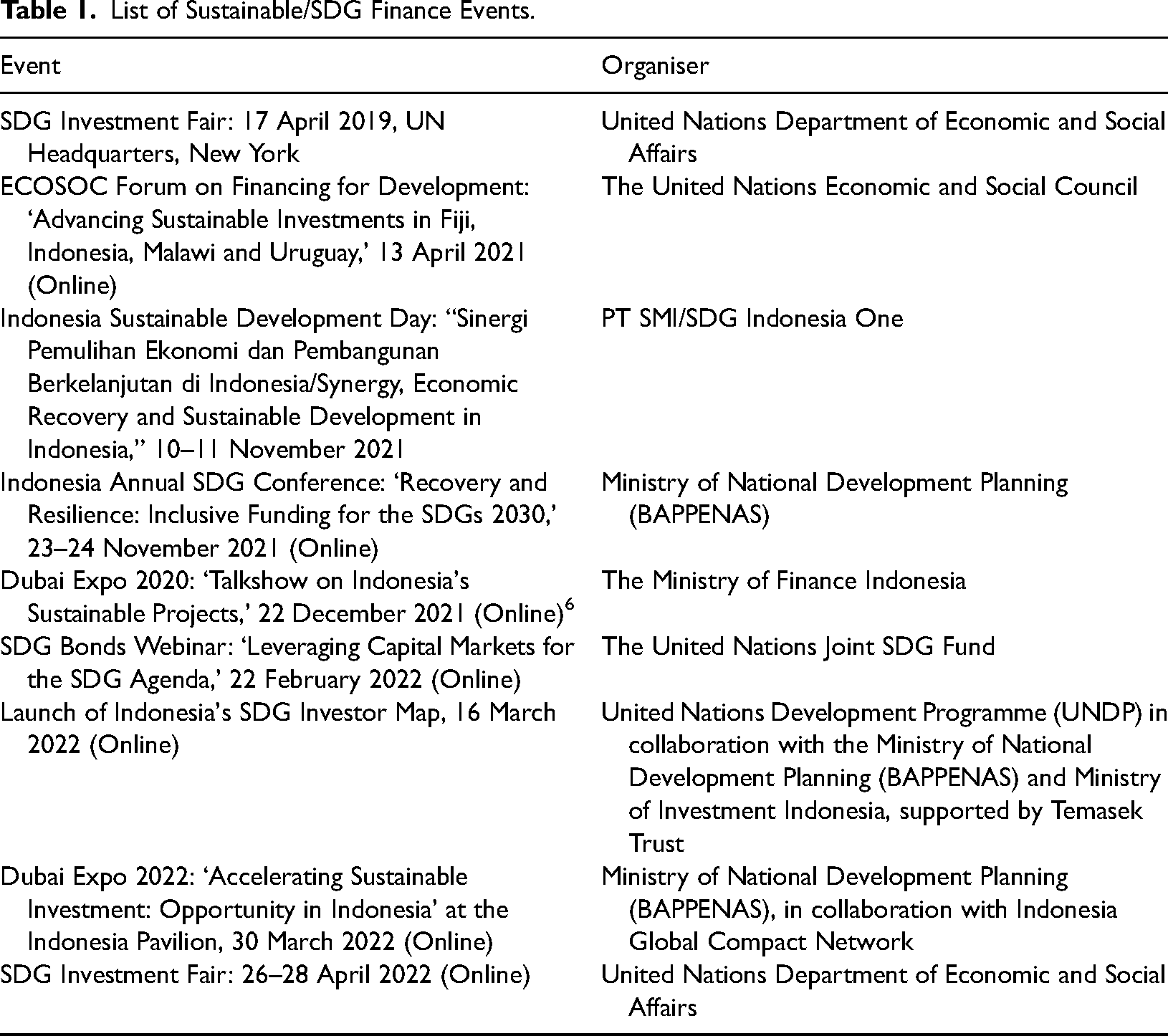

With specific reference to market development for green and SDG bonds in Indonesia, this article sketches a picture of the legible terrain regarded as essential for SDG-private finance alignment. By exploring processes of simplification and legibility mobilised for this alignment, we aim to better understand the ways in which the SDGs help shape contemporary ways of ‘seeing' and ‘doing' development. Empirically, we draw on observations from professional sustainable and SDG finance events where Indonesia is a host or participant, including conferences, policy dialogues and trade/investment fairs. Detailed notes were taken of the events, including the (ritualised) order, speakers and content of these events, as well as promotional material often interspersed between individual keynotes and panel discussions. We pay particular attention to the discourse articulating what innovative sustainable finance means, and what prospects and practices the alignment between finance and sustainable development enlivens. Other than Indonesia Sustainable Development Day and Indonesia Annual SDG Conference, all events are outward-facing, intended primarily for external audiences. These events convey a frictionless image of Indonesia as a sustainable investment destination, where knowledge of the ‘enabling environment’ is circulated; new market opportunities are shared; and measures Indonesia has taken to incentivise investments – tax incentives, adherence to international ‘best practices’, various government guarantees for low-carbon development and so on – are showcased. It is notable, for example, that during the 2021 Dubai Expo, the highly contentious Omnibus Law on Job Creation was promoted as one that ‘simplifies bureaucracy while still putting forward the environmental aspect through a risk-based business license’, smoothing over concerns of the law's regressive nature in social and environmental terms (Harianja, 2020; Suntoro, 2021). Notwithstanding some overlaps, the more inward-facing events (in Bahasa Indonesia) go beyond the focus on marketing Indonesia as a commercial enclosure towards emphasising the state's aspiration to escape the ‘middle income trap’ – an ambition frequently articulated to the notion of sovereignty and the promise of prosperity and fairness – enfolding domestic audiences in the promissory future of finance-led development. This speaks to the ways in which Indonesia differentially addresses domestic and international investors. These proceedings, to borrow from Rethel (2018: 195), are sites where a particular view of, and approach to, sustainable development ‘seeking to meld commercial and ethical concerns is instantiated and legitimated’ (see also Leivestad and Nyqvist, 2017). All events were accessed online, and all, except one, were held virtually due to the COVID-19 pandemic (Table 1).

List of Sustainable/SDG Finance Events.

We complement these observations with a close reading of official documents, given the centrality of ‘documentary practices’ in constituting and implementing rules and standards, and legitimising interventions (Hull, 2012). We focus on the documents specifically produced for the issuance of SDG and green bonds, as well as those that underpin Indonesia's capital market development. These include Indonesia's medium-term development plans 2015–2019, 2020–2024 (Rencana Pembangunan Jangka Menengah/RPJMN, 2015–2019, 2020–2024); Financial Services Master Plans (in particular, the Sustainable Finance Roadmaps contained therein) 2015–2019 and 2020–2024; feasibility studies for bond issuances; legal documents relevant to capital market development; and ex-ante and ex post evaluation documents designed to show impact legibility of SDG and green bonds (including green sharia-compliant bonds or sukuk). In our reading, we pay attention to aesthetics and genres, looking at and through documents to discern meanings and intents around the objects they are designed for (Hull, 2012). We ask what and who these forms of documentation serve and how do they problematise, envision and act on sustainable development. Lastly, we carried out seven semi-structured interviews, each between 60 and 90 minutes long, with those familiar or directly engaged with the production and issuance of thematic bonds in Indonesia, to further clarify the role of the SDGs in shaping sustainable development that capital can see.

Noting the swathe of activities and instruments intended to unlock private finance for development in Indonesia, we purposefully trace three vignettes from the materials we have gathered to comprehensively illustrate the entwined processes through which development is made legible to capital. First, we scan the master plans intended to create a legible terrain, in which a ‘a common language’ is being defined to globalise green and SDG bond markets. Second, we consider the production of a ‘prototype’ – Indonesia's first corporate green bond – on this emergent terrain and how this pioneering experiment helps shape the contours of this terrain. Third, we look at the ways in which bankable project pipelines, which are needed to grow the green/SDG bond markets, are built or found. Here, pipelines refer to a list of projects or assets ‘typically presented as a sequence of proposed investment opportunities overtime’ (e.g., planned renewable energy projects across the Indonesian archipelago in the next decade) (OECD, 2018). They are, quite literally, simplifications that capital can see: indicative maps of risk-return profiles of projects/assets, including the estimated cost, the land needed or already acquired, implementation schedule, government guarantees, projected returns and so on (see BAPPENAS, 2019).

Plans, prototypes and project pipelines: Aligning private finance with the SDGs

Plans: Developing a common language

Creating ‘an environment conducive to innovation’ is a key objective of the Indonesian Financial Services Master Plans (2015–2019; 2021–2025) (OJK, 2021a: 37). It also features in Indonesia's medium-term development plans, SDG action plans and the SDG roadmap, all of which are national translations of the SDGs (BAPPENAS, 2015; 2017; 2020; 2021; OJK, 2014; 2015; 2021a; 2021b). In the Indonesian context, the financialisation-development nexus thus materialises through the articulation between national development ambitions and capital market development, with the premise that the latter would provide a substantial source of financing for the realisation of the former (BAPPENAS, 2017; 2020; OJK, 2021b).

With reference to green and SDG bond markets, their emergence and growth are intertwined with the creation of a common language and best practice by those who populate and animate the sustainable finance landscape, or ‘ecosystem’ as it is referred to in official discourse (OJK, 2021b). As the Chair of the Indonesian Financial Services Authority or Otoritas Jasa Keuangan (hereafter OJK) puts it, an understanding on what constitutes sustainable finance and projects, one that is internationally shared, is needed to form scalable innovative financial products (Santoso, 2021). There are at least two notable developments towards the establishment of this common language.

One is the enactment of a regulation on the issuance of green bonds: POJK No. 60/2017 (OJK, 2017). This is an output of the first phase of the Sustainable Finance Roadmap, a part of the more-encompassing Financial Services Master Plan 2015–2019. To be legible to international finance, the regulation reproduces much of what is laid out in the Green Bond Principles, with the exception that 30% of the green bond's proceeds can be used outside of ‘green’ purposes (OJK, 2017). In essence, it sets out the procedures and terms on the issuance of green bonds, from project selection (including a list of eligible sectors for financing) to annual reporting and sanctions in cases of unmet obligations (OJK, 2017). Greenness, in this instance, is established by disclosing categories of projects; intended environmental targets; the process and method through which the issuer identifies and manages social and environmental risks; and a summary of opinion of the green bond framework by an environmental expert (OJK, 2017: Art 7.a). Reporting on the use of proceeds is mandatory, but it does not need to specify whether the intended environmental targets are met (OJK, 2017: Art 10–11).

The second is the Indonesia Green Taxonomy, launched in 2022, a part of the second phase of the Sustainable Finance Roadmap. A key aim is to encourage innovation in green financial products and services, including green bonds, by providing ‘an overview on the classification of sectors/subsectors that have been scientifically categorised as green, to avoid greenwashing practices’ (OJK, 2022b: 11, emphasis added). The taxonomy is based on the Indonesia Standard Industrial Classification (Klassifikasi Buku Lapangan Usaha), a substantial part of which refers to the International Standard Industrial Classification of all Economic Activities published by the United Nations Statistics Division (UNSD), presumably to promote interoperability (OJK, 2022b). It is also benchmarked against other green taxonomies, notably those of China, European Union and ASEAN (OJK, 2022b). Green classification in the taxonomy refers to activities that ‘do no significant harm, apply minimum safeguard, provide positive impact to the environment and align with the environmental objective of the taxonomy’, with yellow signifying no significant harm and red being harmful (OJK, 2022b: 14). This classification, however, is subject to adjustment. The taxonomy is posed as a living document to accommodate ‘diverse approaches in determining green criteria thresholds’ and ‘new business activities, changes in standards and policies, as well as scientific development and technological advancement’ (OJK, 2022b: 11–12).

There are at least three things worth noting with regard to how greenness is constituted through these policy and regulatory designs. One is that the design of Indonesia's sustainable finance ecosystem, and the boundaries and rules governing this ecosystem, is considerably shaped by the financial services industry (OJK, 2022b). This is an industry known for its perfunctory and patchy engagement with sustainability. The integration of social and environmental assessments ‘for big scale and high-risk’ loans and investments, for example, has long been mandated in the 1998 amendments to the 1992 Banking Law (Government of Indonesia, UU 10/1998). Still, decades later, these assessments rarely take place, and when they do, such assessments are often done in a cursory manner (Setyowati, 2020). Increasing industry competencies on sustainability is itself a key objective of the Sustainable Finance Roadmaps (OJK, 2014; 2021b; Interview 6 23 March 2022). Yet, in 2021, OJK established a Sustainable Finance Taskforce, comprising only of representatives from banks, capital markets and non-bank financial institutions, to further the development of Indonesia's sustainable finance ecosystem (OJK, 2022a). In playing a key part in the design of policies and regulations governing its own conduct, the financial services industry may well construct ‘a world of finance that seeks to reconstitute (claims of) ‘the social’ and ‘the environmental’ in its own image’ (Asiyanbi, 2021: 9).

The second, relatedly, concerns the reproduction of a utilitarian view of ‘the environment’. Although the green taxonomy is cast as a living document, it fixes an understanding of the environment, and its relation to the notion of sustainable development. Here, ‘the environment’ (including the resources contained within it) is couched in terms of its utility to ‘continuously support the economy in a sustainable manner,’ understood as ‘economic capital assets’ (OJK, 2022b: 13). Environmental (and social) concerns are conceived of as credit risks in need of ‘identification, measurement, mitigation, supervision and monitoring processes’ (OJK, 2022b: 20).

The third concerns the aesthetic of an objective scientific order. The database that forms the taxonomy is accompanied by an appendix disclosing the process of its making: from the conceptual framework setting out the objectives of standardisation to analyses of plans, policies, regulations and international commitments informing the classification of green, yellow and red, all of which received ministerial assessment and confirmation (OJK, 2022b). But it would be negligent to infer objectivity from this seemingly rigorous assessment. A closer look at the database itself reveals a much more arbitrary and cobbled picture. It is curious, for example, that ‘activities of government agencies in the fields of mining, electricity, water and gas’ and ‘tobacco plantation’ fall automatically into the green classification, which means no further qualification of greenness is necessary (OJK, 2022b). All these speak to the ways in which planning constructs a legible terrain – a field of intervention – that is conducive to certain kinds of ‘prototyping’, as exemplified in the issuance of Indonesia's first corporate green bond ‘prototype’ below.

Prototypes: Reinscribing conventions

Indonesia's first corporate green bond – worth IDR 500 billion (approximately US$33.7 million) – was issued in 2018 by PT SMI, a state-owned infrastructure financing facility under the Ministry of Finance (PT SMI, 2018a). At the time, ‘there were no benchmarks for the issuance of green bonds in Indonesia’ and OJK's green bond regulation ‘had not been tested’ (World Bank, 2018). Through this pioneering role, PT SMI considers itself to be an ‘ecosystem enabler’ in helping to build industry ‘know-how’ on green bond issuance (PT SMI, 2019b). In the issuance process, it did everything a credible issuer would do in keeping with international best practice. It established a Green Bond Framework, with the World Bank providing financial and environmental expertise in its design (World Bank, 2018). The framework is compliant with OJK's green bond regulation, and consistent with the Green Bond Principles and the ASEAN Green Bond Standard (PT SMI, 2018b). The framework solicited a second party opinion from CICERO – Centre for International Climate and Environmental Research – who rated it ‘medium green’ based on PT SMI's ‘sound approach to green financing for business activities that protect and/or improve the quality or function of the environment’ (CICERO, 2018: 2). And it has since produced annual reports on the use of proceeds to bondholders (PT SMI, 2019a; 2020a; 2021a).

However, if the additionality – and indeed the innovative element – of a green bond is that it can unlock cheaper, long-term capital to environmentally beneficial projects that would otherwise not be financed (Jones et al., 2020), then no additionality was realised through the issuance of PT SMI's green bond. In this case, all of the bond's proceeds were used to refinance existing projects (PT SMI, 2021a; 2020; 2019). In addition, while acquiring a green label incurred additional cost and time, investors remained primarily motivated by financial returns (Syahruzad, 2021). Given market conditions, the green bond had to offer comparable returns to conventional bonds to attract investors, with 7.55% and 7.80% interest rates paid by PT SMI, to mature over 3 and 5 years, respectively (Amanda, 2019; World Bank, 2018). This echoes a recent market survey among securities companies and investment banks in Indonesia: that ‘investors’ decisions are primarily influenced by the rating of the bond, reputation of issuers, the tenor of the bond (prefer short tenors), guarantor, and the coupon rate’ (Wijaya et al., 2021: 2).

Even if the bond had provided cheaper, longer-term capital, as is the case with Indonesia's sovereign SDG bond (Ministry of Finance, 2021), this may not necessarily lead to the realisation of environmental objectives. Consider the expert-based valuation designed to appraise sustainability credentials. In this appraisal, sustainability itself is ambiguously translated and valued. CICERO's grading methodology, for example, assigns shades of green based on ‘exposure to climate risks,’ with dark green being the least exposed (CICERO, 2018: 6). Exposure to climate risks, here, is neither quantified nor linked to specific environmental outcomes. Rather, it is assessed through PT SMI's existing governance arrangements on risk identification and management, monitoring, reporting mechanisms and so on (CICERO, 2018). The same goes for the second party opinion provided by CICERO to Indonesia's SDGs Government Securities Framework, which is based on, among other things, Indonesia's ‘capacity for anticipating and assessing adverse social risks when selecting eligible green and social projects’ (CICERO, 2021: 5). This effectively means that the designation of greenness or assessment of social benefits and risks are based on the issuers’ risk profile, not the projects themselves (Bracking 2019). In practice, this produces an abstract, if not nominal, accountability: one that provides investors with a green or social stamp, while distancing them from the actual environmental and/or social outcomes of their investments.

When quantification of (estimated) outcomes is performed, it too produces reductive specifications. For example, one of the three eligible projects PT SMI refinanced through its green bond proceeds was the Greater Jakarta Light Rail Transit (LRT), which it claimed would contribute to SDGs 1 (no poverty); 3 (health and well-being); 5 (gender equality); 8 (decent work and economic growth); 9 (industry, innovation and infrastructure); 10 (reduced inequality); 11 (sustainable production and consumption) and 13 (climate action) (Syahruzad 2021). In its annual green bond reporting, however, its estimated environmental impacts are confined only to ‘greenhouse gas emissions avoided (carbon dioxide equivalent)’ and ‘energy savings’ (PT SMI, 2021a; 2020; 2019a). No other environmental or social impacts are disclosed. The review report by an ‘environmental expert’ appended to each annual report is similarly reductive, generally only reporting on whether the project selection and allocation of proceeds remain consistent with the Green Bond Principles and reaffirming the positive environmental impacts already disclosed by PT SMI (PT SMI, 2021a; 2020; 2019a). This impact legibility erases possible tensions among the many goals the project claims to advance. The development of the Greater Jakarta LRT is not without controversy, with concerns raised over evictions during land acquisition and transit-induced gentrification associated with commercial and residential developments (Embu, 2018; Jakarta Legal Aid Institute, 2017). Yet, the risk of reinforcing old and creating new socio-economic boundaries in the city landscape is overlooked.

But invisibilising risks/impacts that can unsettle the promise of a triple bottom line is inherent in innovating or ‘prototyping’ for market success. By issuing Indonesia's first corporate green bond, PT SMI aimed to not only raise finance but to help develop the market, drawing lessons from the process to bring back ‘to the ecosystem’ and fostering the knowledge industries needed for green bonds to grow (Dalel, 2020). Other issuances of differently denominated thematic bonds by the government of Indonesia are concerned largely with gauging investors’ needs – how investors in different markets view sustainability and its relation to risks and returns – which is necessary ‘if Indonesia wants to ensure that the issuance of these instruments will gain success in the market’ (Interview 3 26 November 2021). Here, it is typical for the issuer to organise (global) roadshows (or non-deal investor updates) to showcase, and solicit feedback on, the bonds on offer, as the Ministry of Finance did for the SDG bond, green bonds and green sukuk (Islamic Sustainable Finance & Investment, 2019; Ministry of Finance, 2021). The lessons gleaned from these issuances also generally centre around further ‘deepening’ the market: how to construct the right incentives for issuers, given the additional cost of establishing greenness; how to ensure interoperability between international standards; how to do proper reporting; how to build the ‘right expertise’ and so forth (Syahruzad, 2021).

Financial innovations for the SDGs, then, do not change conventions. Instead, they iteratively reinscribe conventions, emphasising and transposing the logic and techniques of finance – such as credit ratings and risk-return ratio – in the production and sale of green and SDG bonds. In so doing, they circulate, reproduce and reify technical, financialised interventions that erase the unevenness of capital market development, but that create internationally recognisable forms of credibility, irrespective of outcomes (Rethel, 2018).

Financial returns to bondholders, though, are assured. By and large, this means that green or SDG bonds’ underlying projects (or assets) have to be bankable. The availability of bankable project pipelines – at the right volume and scale – is key to scaling up innovations like SDG and green bonds (Climate Bonds Initiative, 2022), a discussion we now turn to.

Project pipelines: Seeing bankability

In his opening remark to a session during the 2019 SDG Investment Fair, James Zhan (2019), Director of Investment and Enterprise at the UN Conference on Trade and Development (UNCTAD), pointed out that it is the difficulty of finding bankable project pipelines that inhibits the ‘good will’ of the private sector to invest in the SDGs and ‘the political will’ of governments to achieve the SDGs. What this implied, however, is that irrespective of good will, green or sustainable qualities are, by themselves, inadequate to unlock private finance for the SDGs. Indeed, as President of Global Capital Finance Juergen Moessner (2019) plainly stated during the session, ‘for something to be investible, there has to be a return.’ He applauded Arifin Rudiyanto, the Indonesian Deputy Minister for Maritime and Natural Resources Affairs, for Indonesia's well-prepared project pipelines (presented minutes earlier), but pointed to a ‘missing link’ in the effort to attract private finance: ‘that it is always presented from a need basis,’ which ‘from an investor point of view is not that relevant’ (Moessner, 2019). What matters is the prospect of a reliable revenue stream. Everything else, including the project's contribution to the SDGs, is ‘qualitative enhancement’ (Moessner, 2019).

This kind of exchange, not uncommon in SDG finance gatherings, help shape and validate ‘intentional’ development oriented around growing bankable project pipelines (UN DESA, 2018; 2019; 2021; 2022a). In Indonesia, increasing bankable projects – ‘transforming needs into opportunities’ – is institutionalised as a development objective in its own right (Martini as cited in Ministry of Finance, 2018). In 2018, SDG Indonesia One – a financing platform managed by PT SMI – was launched to support the attainment of the SDGs through infrastructure financing (Ministry of Finance, 2018). It functions as a blended finance platform, where it manages public and private funds to be channelled through project development, de-risking, financing and an SDG equity fund, providing ‘integrated project financing (end-to-end financing) from the initial stage of project development to financing through equity investment’ (PT SMI, 2019b: 42).

In and of itself, the appointment of PT SMI as the implementing agency of SDG Indonesia One raises the platform's legibility to financiers. It is a state-owned enterprise closely associated with the Ministry of Finance, with a track record of managing funds from various sources, accreditation with the Green Climate Fund and ‘investment grade’ credit rating (AAA domestically and BBB/Stable internationally) (ADB, 2022b; Fitch Ratings, 2021; PT SMI, 2021b). PT SMI, in other words, is seen as a credible partner to donors and investors. Many who have pledged money to SDG Indonesia One have previously worked with PT SMI, such as the International Finance Corporation (IFC), Agence Française de Développement (AFD) and Deutsche Investitions- und Entwicklungsgesellschaft (DEG) (ADB, 2022b).

A significant proportion of the money pledged to SDG Indonesia One is earmarked for project development (PT SMI, 2018a; 2021b). This is because ‘designing an optimal risk-sharing protocol at the project development phase is at the crux of ensuring bankability’ (Rana, 2017). In 2021, technical assistance for project development used up 85% of total funds realised (PT SMI, 2021b). A key aim in the disbursement of loans from the Asian Development Bank (ADB) to SDG Indonesia One, for example, is to reduce ‘credit risk in projects to a level that is sufficient to attract commercial lenders’ (ADB, 2022b: 5). Note, however, that much of this capital is redistributed through loans by PT SMI. Access to it is therefore based on the ability of (sub)projects and (sub)borrowers to service the loan (ADB, 2022b). As the loan agreement stipulates: PT SMI shall not make any Subloans… unless such Qualified Enterprise has at its disposal… adequate working capital, and other resources which are required by such Qualified Enterprise for the carrying out of its Qualified Subproject in respect of which the Subloan is to be made (ADB 2022a: article 3.03).

That most of the funds committed to SDG Indonesia One come in the form of loans, which are then disbursed in the form of subloans, means that ‘the ability of the project to repay is the most important criterion’ (Interview 2 27 October 2021). As noted in our interviews, the ‘risk appetite’ of PT SMI is conservative. As a state-owned business entity it simply cannot finance small-scale projects, which is a challenge for SDG-oriented projects as ‘their bankability is typically low’ (Interview 1 9 October 2021) and ‘not always big scale’ (Interview 3 26 November 2021). The requirement for bankability does not mean social, environmental and governance risks go unaccounted in project development. In 2018, PT SMI instituted a comprehensive risk management framework to measure and manage a whole host of risks, from legal risk and reputational risk to social and environmental risks in an attempt to comprehensively balance risk and return for the company (PT SMI, 2018a). However, ‘all risks are assessed in relation to the potential or possibility of default’ (Interview 2 27 October 2021).

The fact that creditworthiness is a key criterion to access finance supposedly allocated for ‘de-risking’ raises the question of whether, and to what extent, investment opportunities are being ‘de-risked’ in frontier and emerging economies. In the case of the ADB loan to PT SMI for SDG Indonesia One, ‘project development’ is less about building projects than finding already bankable projects to finance. As an interviewee notes, SDG Indonesia One is basically ‘a matchmaking platform to connect investors with relevant projects’ but the difficulty of getting projects that match the risk appetite of both PT SMI and donors means that ‘the number of pipelines is quite small’ (Interview 1 9 October 2021). This is especially because bankability alone is inadequate to attract big finance, it has to be the right scale and ‘what exists today does not respond to the needs of small and medium enterprises or projects’ (Interview 3 26 November 2021).

Just as importantly, it is questionable whether the work to align private finance with the SDGs can accelerate the flow of finance to the implementation of these goals. In SDG Indonesia One, the capital that is unlocked is typically far less than what is pledged by partners, precisely because of the limited availability of the right projects. In 2021, for example, US$ 3.22 billion was pledged to the platform, of which only US$ 230 million was realised (PT SMI, 2021b). This raises the key concern that (re)producing (chains of) debt to finance global goals that aspire to leave no one behind would instead exacerbate inequalities and vulnerabilities, while eclipsing any alternative agenda for reparation and redistribution (Perry, 2021).

The promise and limits of ‘innovative’ debt financing for the SDGs in Indonesia

What role do the SDGs play in the planning, prototyping and building of project pipelines we describe above? And what do they tell us about contemporary ways of seeing and doing development? Quite obviously, these processes are built on a simplification: that private finance is the linchpin without which progress on the SDGs cannot be made. This simplification breeds another simplification: that unlocking private finance requires an expression of sustainable development that is legible to capital. Interventions to align private finance with the SDGs are buoyed by, and reproduce, a promise of social, environmental and financial returns on investment. Here, social and environmental concerns are refracted through a financial lens: as categories of risks amenable to technical interventions. Yet, the considerable amount of work to make development legible to capital and make Indonesia legible as a sustainable investment destination has done little to unlock capital for the SDGs. Nor has it necessarily contributed to better sustainability outcomes. Here, to borrow from Ferguson (2005: 379), ‘capital does not “flow”… it hops’ across space towards the most bankable, largest and most scalable projects, ‘neatly skipping over most of what lies in between’ (see also Anantharajah and Setyowati, 2022). And so, it is the promise, not certainty, of ‘doing well by doing good’ that gives the financialisation-development nexus movement.

Still, the simplifications produced and reproduced in the processes we describe are not inconsequential. The alignment between finance and the SDGs enacted in and through green and SDG bonds obscures potential conflicts between social, environmental and financial goals. Just as importantly, such an alignment effectively (and affectively) erases the structural inequities and unsustainability in the logic around, and pursuit of, capital market development to finance sustainable development (cf. Garcìa Lamarca and Ullström, 2022). Causes of poverty, inequities and unsustainability unconnected to the problematique of ‘closing the SDG financing gap’ go largely unheeded, including the ways in which finance – even that which is labelled green and social – has been found to intensify said problems (Colven, 2022; Bigger and Millington 2020).

This way of seeing manifests in a set of governance practices that share fundamental features with what Scott ([1998] 2020) describes as high modern. The planning, prototyping and building of project pipelines we describe are collectively concerned with a rather narrow, and shallow, technical project of (in)visibilising impacts for the issuance and growth of debt financing in the name of sustainable development. They are enacted through, and actively reinforce, technical expertise that links a set of managerial practices to anticipated, albeit uncertain, outcomes. Greenness, as we have shown, is appraised through the degree to which bond issuers possess the necessary governance arrangements to deliver on their sustainability promises. Such an appraisal generates only knowledge required to legitimate green and SDG bond markets, which inevitably neglects contextual conditions that may unsettle the legibility it seeks to produce, as was briefly illustrated by the Greater Jakarta LRT example. Like other high modern schematics, thematic bond standards and the green taxonomy disassociate what counts as green from the specificities of contexts in Indonesia, striving instead to build a ‘common language’ to globalise green capital markets.

In all these, the SDGs help to give reason, consolidate and legitimise what Merry (2019) might describe as an emergent global ‘infrastructure of measurement’ determining the allocation and use of interest-bearing debt finance through a tenuous, decontextualised understanding of greenness or sustainability (see also Tan, 2022). The long list of SDG targets and indicators, as Asiyanbi (2021: 8) points out, is ‘readily transferable’ as a template for sustainable investment standards and reporting. This infrastructure is built on the codification of private (self-regulating) systems of governance such as the Green Bond Principles in national policies and regulations, as we have shown through Indonesia's green bond regulation. An infrastructure where a focus on procedure means that, in practice, what becomes green, sustainable or SDG-oriented is ‘epistemologically separable’ from its actual contribution to social and ecological outcomes (Bracking, 2015: 2347).

What these high modernist tendencies reveal is that the politics of prototypical techniques that Johns (2019) draws to our attention cannot be separated from the politics of planning. A green or SDG bond is essentially a planned prototype. While a legible terrain is needed for its issuance, it is formative in reinforcing a particular kind of legibility to grow green/SDG bond markets. Planning and prototyping, then, co-shape one another to produce and reproduce a particular way of seeing. As interventions designed to promote markets-in-the-making, plans, prototypes and project pipelines are subject to different (re)configurations to test what would help green/SDG bond markets grow within and across time and space.

In a development landscape teeming with innovations claiming to disrupt the ways in which development is imagined and pursued, greater scrutiny is needed to question the proclaimed shift between old and new ways of seeing and doing, the logics on which they are built and that they in turn recast. This means going beyond contrasting frames of continuity and change or planning and prototyping. As Li (2005: 383) reminds us, ‘vast schemes to improve the human condition continue to be designed and implemented, but many do not take the highly visible form Scott identifies as “high modern”.’ Still, these schemes can reinscribe, reproduce, and in some cases amplify predominant logics and techniques, even in ostensibly steering away from them (Li, 2005). Green and social finance, as many argue, are deeply implicated in reinscribing, reproducing and amplifying capitalist ways of doing development, closing off other political possibilities (Garcìa-Lamarca and Ullström, 2022; Rosenman, 2019). Such critical engagement with innovation in the literature on the SDGs, however, is notably absent. This is a gross oversight, particularly given the discourse on innovation and transformation – of doing development differently – that is pronounced in the SDGs. In making sense of what SDG-oriented innovations – financial and non-financial – do in the present context, there is a clear need to pay attention to recursive schemes. That is to say, when new modalities of governance actually operate to embed, albeit reworked, earlier discourses and practices.

Conclusion

In exploring market-making processes for green and SDG bonds, we have illustrated that the alignment between private finance and the SDGs is shaped by simplifications that capital can see. Here, legibility to capital – that fixes and stabilises – is writ large as a precondition for these forms of innovative financing to take shape. As such, innovative financing for the SDGs (re)forms, and is formed through, an emergent mode of ‘doing’ development informed largely through a singular, categorical logic: that anything can, and should, be valued through its relation to capital. If only there is a common language with which we can make these values visible and show impact, the logic goes, then surely we can unlock and leverage private finance for social, environmental and financial gains. The work of planning, prototyping and building project pipelines we have explored reproduces this promise, iterating once more an open-ended project of making development legible to capital. Yet, despite growing financial logics and techniques shaping ‘intentional’ development, there are limits to what can be made bankable, or be made valuable in financial terms. Their productive effects, then, are tied less to the capital they generate, and more to the ways in which they shape how sustainable development is seen and pursued: as an investable proposition still waiting to be accomplished.

In referring to planning, prototyping and building project pipelines as mutually reinforcing and recursive processes, we have shown how innovative financing for the SDGs rests upon practices that cannot be adequately understood as planning or prototyping, change or continuity. Newly configured practices, in this instance, rework and give stability to long-existing capitalist ways of seeing and doing development, this time legitimated through the SDGs. Here, the risk of deepening debt capital markets in a country that has suffered from speculative capital flows goes unheeded (Rethel, 2020).

Our study leaves open and opens up several questions worth exploring to think through contemporary dynamics surrounding financialisation and development in Indonesia. Just as planning or prototyping – if seen as binary concepts – imperfectly captures these dynamics, so too do categories such as ‘sovereign’ and ‘corporate’ or ‘public’ and ‘private’. PT SMI, while corporate in form and function, is fully state-owned. Its corporate interests, therefore, are virtually indistinguishable from those of the state. In this light, more research is needed to understand the differences, and growing convergence, among varied forms and sources of capital – public, private, Islamic or ‘blended’ – and their risk-return expectations, particularly considering the rise of state capitalism in redefining the global D/development regime (Alami et al., 2021). Related to this, there is a need to nuance the relationship between financialisation and state-led developmentalism taking shape in Indonesia (Pangestu, 2020; Warburton 2018). While Indonesia has done much to usher foreign investors into the country, it has also pursued domestic market deepening of retail bonds and sukuk (denominated in Rupiah) to reduce its reliance on international financing (Rethel 2020). This paradox can, for instance, be better understood through more in-depth, situated and sustained engagement with what Kaur (2020: 246) calls the ‘bonds of investment – bond in a double sense of affective ties and financial instruments – that lock cultural nationalism and capitalist growth in a state of mutual indebtedness.’ How do discourses change/remain the same in how the state attempts to make development legible to its international and domestic constituencies? How does it engage with or intervene in financial networks and flows across the globe? Exploring these questions is pertinent if we are to better comprehend the (changing) forms and flow of finance, the power relations that shape them, and the concrete manifestations of the growing entanglement between financialisation and development in Indonesia and elsewhere.

Highlights

We explore market-making processes for ‘innovative’ development finance in Indonesia: Green and SDG bonds.

These processes form a legible terrain for financialising development: to see, and act on, the SDGs as investable propositions.

They deploy standardisation techniques to establish qualities of ‘greenness’ and ‘sustainability’ that are disassociated from outcomes and contexts.

In so doing, these processes do not necessarily unlock new sources of finance or contribute to social and environmental goals.

These ‘innovative’ means, however, succeed in reinscribing capitalist modes of ‘seeing’ and ‘doing’ development, foreclosing other possibilities.

Footnotes

Acknowledgements

We thank Tatiana Acevedo-Guerrero, Marie Petersmann, Thomas Biffin, Ann Prijosusilo, the editor Rosemary Collard and three anonymous reviewers for their helpful comments and feedback, and to the interviewees for taking the time to participate in this research.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the H2020 European Research Council (grant number 788001).