Abstract

Utility-scale renewable electricity generation is essential to decarbonisation as well as to ensuring affordable and secure electricity supplies around the world. Yet thus far there has been limited critical thinking dedicated to the complexities behind the finance and ownership of this new infrastructure and how national and local stakeholders should participate in and benefit from its development, particularly in contexts of high inequality in low- and middle-income countries. As the global renewable energy industry becomes increasingly consolidated and financialised, evidence from a number of countries suggests that despite the pro-environmental outcomes of utility-scale renewable electricity generation, the processes and institutions that procure and finance it have often failed to include or benefit individuals and communities living in the national and local vicinity. This paper therefore sets two key competing objectives of renewable electricity generation in context: as a predictable, long-term revenue stream for investors, and as a mechanism for socio-economic development and community empowerment. Building on scholarship from human geography, development studies and sustainability transitions, my analysis takes forward understandings of the role of finance in utility-scale renewable electricity generation as a key aspect of the political economy of the energy transition. In exploring the evolution of renewable electricity as a new and rapidly emerging asset class I consider how its development is increasingly determined by the frameworks and logics of finance and investment. Drawing on examples from South Africa and Mexico, I address the following questions: What are the evolving configurations and processes of finance and investment in utility-scale renewable electricity generation? How have they been facilitated? And what tensions have arisen from their implementation at the national and local level?

Introduction

Recent years have seen the rapid growth of electricity generation from renewable energy, which by 2018 generated an estimated 13% of the world’s electricity (UNEP/BNEF, 2019: 20). Yet while renewable energy is essential to climate change mitigation as well as to ensuring affordable and secure electricity supplies around the world (UNDESA, 2020), there has been limited critical academic thinking dedicated to the complexities behind its ownership. Similarly, there has been limited analysis into how national and local stakeholders should participate in and benefit from its development, particularly in contexts of socio-economic, political and spatial inequality in low- and middle-income countries (LMICs). As the global renewable energy industry becomes increasingly consolidated and financialised, evidence from a number of countries suggests that despite the pro-environmental outcomes of large-scale renewable energy projects, the mechanisms and institutions that procure and finance it have often failed to adequately account for, or benefit individuals and communities living in the national and local vicinity. Such a failure has resulted in tensions and resistance by trade unions, local communities and Indigenous peoples (Dunlap, 2018; Marais et al., 2017).

In this paper I focus on grid-connected, utility-scale renewable electricity generation. Of a total of $272.9 billion of global renewable energy investment in 2018, 86.5% of it was for utility-scale projects dominated by onshore and offshore wind, solar photovoltaics (PV), and to a lesser extent, concentrated solar power and small-scale hydro (less than 50 MW) 1 (UNEP/BNEF, 2019: 38). A significant proportion of this generation has been procured under renewable energy auctions, developed by independent power producers (IPPs) and paid for by a complex interaction of public and private sources of finance and investment under structures of project finance.

In keeping with the theme of this special issue on electricity capital ( Luke and Huber, 2021 ), I investigate two competing objectives of utility-scale renewable energy. The first, embraced in particular by the finance industry, sees renewable electricity generation as a predictable, long-term revenue stream for investors (BloombergNEF, 2020). The second, of priority for non-governmental organisations, local communities, trade unions and some local and national government departments, sees this development as a potential mechanism for community empowerment and socio-economic development (Halsey et al., 2019). While these two competing objectives represent tensions or even incompatibilities between global processes of procurement and finance on the one hand and localised, territorial realities on the other, thus far there has been limited in-depth, qualitative research dedicated to understanding them, particularly in contexts of high inequality in LMICs.

As I explore, South Africa and Mexico serve as poignant illustrations of how such tensions have manifested in specific national and sub-national circumstances, and between which there are significant points of comparison. Both are in the top 10 developing nations for clean energy asset finance and regional leaders in renewable energy deployment in sub-Saharan Africa and Latin America and the Caribbean respectively (BloombergNEF, 2020: 29). Both have undertaken regulatory reforms of their state-owned electricity sectors in recent years in order to introduce auction programmes for the procurement of renewable electricity generation from IPPs. While both countries are members of the G20 group of the world’s largest emerging economies they also have high levels of socio-economic, political and spatial inequality, which play a key part in the tensions inherent in utility-scale renewable electricity projects. Not least, because these projects require large tracts of land, in both countries the most competitive resources are often located in remote and rural areas, of which the majority populations are socio-economically and politically marginalised. As discussed below, evidence thus far suggests that these populations are the least likely to benefit from these new developments.

Drawing on scholarship from human geography, development studies and sustainability transitions, I take forward research on the political economy of the energy transition which has identified tensions and trade-offs between the development of renewable energy infrastructure on the one hand and the need to ensure equitable participation in the process and distribution of the benefits on the other. However, this literature has yet to establish a critical and in-depth knowledge base on the relationship between evolving modes of finance and investment, and the socio-economic impacts of this infrastructure, including the extent to which national and local actors are included in or excluded from such development. There is therefore far greater scope to engage with renewable electricity as a new and rapidly emerging asset class, including how its development and deployment is increasingly determined by the priorities and logics of finance and investment, particularly in contexts of inequality, poverty and marginalisation.

In expanding on these themes, I offer a theoretical and empirical counterpoint to the many techno-economic studies on energy finance which conceptualise finance as external to the system rather than inextricably bound up with it. In so doing I seek to generate a critical understanding of the complex and differentiated roles of public, private, national and international sources of finance and investment at play in utility-scale renewable energy projects. Situating this infrastructure within the context of its inseparable and co-evolving relationship with the finance that supports and shapes it, I ask the following overarching questions: What are the evolving configurations and processes of finance and investment in utility-scale renewable electricity generation? How have they been facilitated? And what tensions have arisen from their implementation at the national and local level?

This paper draws from an extensive desk-based analysis of academic and grey literature, including industry-specific publications such as Recharge News, Renewables Now, ESI-Africa and Engineering News; company reports from the renewable energy industry; national policy and planning documents from South Africa and Mexico; reports and data by international energy institutions such as IRENA, REN21, the International Energy Agency (IEA) and the Organisation for Economic Co-operation and Development (OECD); and loan and investment data from development finance institutions and the Bloomberg New Energy Finance database. My research is also informed by field work in South Africa between 2015 and 2017 and participant observation at meetings and webinars of industry and finance, including at the Africa Energy Forum in London 2015, the South African Windaba in 2016, and the online Africa Utility Week in May 2020. Interviews are not cited in the interests of participant and commercial confidentiality.

A methodological challenge to this research is that the landscape of renewable electricity capital is one of a heterogeneous and constantly evolving set of actors, reflecting the complex and shifting nature of transnational flows of finance and investment (Grimes and Sun, 2014). Indeed, beyond publicly available data from development finance institutions, it can be difficult to access and disaggregate all of the actors and configurations of finance and investment involved in utility-scale projects. Deals are not always disclosed, data may not be complete and the various different ways in which money is being recycled in the sector is not always captured (OECD/IEA, 2018). While this inevitably places restrictions on the analysis, such a reality also reflects one of the findings of this research, that the opaque and shifting nature of project ownership can make attributing responsibility for it much harder.

The structure of this paper is as follows: the next section establishes the analytical framing on the role of finance in the energy transition. A later section provides a contextual exploration of the global trends and processes for the procurement and finance of renewable electricity generation. This exploration includes the emergence of IPPs, the design of renewable energy auction programmes, the evolution of accompanying structures of project finance and the determining influence of investor risk as a highly negotiated concept. The penultimate section explores how these global processes have interacted with territorial realities in South Africa and Mexico and their subsequent contribution to structural inequalities and local conflicts. The final section concludes with a research agenda for future thinking on this complex multi-scalar issue.

On the energy transition and the role of finance

Given the multi-faceted nature of electricity which, as a subset of energy, is at once a natural resource, a technology, a networked infrastructure, a basic service and a financial asset, the framing of this paper is necessarily inter-disciplinary. Mindful of broader questions of political economy, power and politics in energy transitions which are by their nature messy, non-linear and conflict-ridden (Baker et al., 2014; Bridge and Gailing, 2020), electricity can be seen as a site of struggle, over its procurement, finance and ownership and the allocation of its benefits, and interactions between incumbent configurations of political, social and economic power and technological change (Gentle, 2009; McDonald, 2016). As I explore, this struggle includes political resistance against renewable energy IPPs; social conflict between local communities and Indigenous peoples, and institutions of the state, corporate entities and flows of finance and investment; and movements of protest and resistance against new forms of enclosure and land appropriation (Avila-Calero, 2017).

My focus on the political economy of the energy transition represents a critical move away from the long-standing literature on the socio-technical or low-carbon transition which has been analytical as well as prescriptive in policy terms. Under frameworks of transitions management, the multi-level perspective and strategic niche management this literature has dedicated significant exploration to how socio-technical change in systems such as electricity can happen, including via interactions between ‘niches’, ‘regimes’ and ‘landscapes’(Markard et al., 2012; Smith et al., 2010; Verbong and Geels, 2007). A key criticism of this literature is that its geographical focus has been informed disproportionately by the experience of countries in Europe and North America. Moreover, it makes implicit and unquestioned assumptions about the democratic nature of state power, national infrastructure development, levels of energy access and national capacities for technological innovation. Such assumptions do not readily apply to contexts of inequality and poverty in LMICs and political structures shaped by post-colonial path dependencies.

In parallel to scholarship on the political economy of the energy transition, a related critical body of literature has emerged in recent years from human geography and development studies, which broadly speaking can be categorised as ‘energy transitions in the global South’ (Castán-Broto et al., 2018). This literature puts forward a diversity of socially, culturally, politically and spatially aware analyses from a variety of geographical settings (e.g. Baptista and Plananska, 2017; Hansen et al., 2018; Osunmuyiwa et al., 2017; Rignall, 2015). Studies from within this field have also emphasised the significance of the need for any energy transition to be pro-poor (Ahlborg, 2017; Ockwell and Byrne, 2016), and criticised the concept of the energy transition in LMICs altogether as a project based on the import of foreign finance and technologies with little regard for local context (Simmet, 2018).

Meanwhile, notions of the ‘just transition’ that merge the urgent need for a global low-carbon shift that upholds the norms of socio-economic justice have been put forward by academia (Newell and Mulvaney, 2013; Swilling et al., 2016), civil society and trade unions (PCS, 2016) and some government departments, including in South Africa (National Planning Commission, Republic of South Africa, 2019). The essence of any theoretical and applied understanding of the just transition is that systems of production and consumption should be reconfigured to avoid resource depletion, environmental degradation and the perpetuation or creation of socio-economic inequalities. In this way the concept challenges implicit assumptions that ‘radical green niches’ will be automatically accompanied by socio-economic co-benefits and seeks to address the livelihood and other socio-economic or environmental losses that may accompany any transition to sustainability.

While these recent contributions have given a more critical understanding to the role of power relations and the distributional complexities of the energy transition, more analysis is needed in order to understand the significance of capital flows and financial forces in shaping renewable energy pathways. This includes the way in which finance, labour, state-capital relations, socio-economic welfare and civil conflict may interact with the introduction of new technological and infrastructural configurations of electricity, particularly in contexts of high socio-economic and political inequality. Despite the significance of understanding national processes of decision-making in the electricity sector, including regulation, planning and procurement, there are evident limits to this nationally bounded focus in an increasingly financialised and globally interdependent world. Greater exploration is therefore needed, of the multi-scalar interactions between rapidly evolving capital flows and configurations on the one hand and on the other, the embedded nature of electricity within a specific national and/or sub-national context including systems of law and governance and socio-cultural structures.

In order to better understand the recent emergence of renewable electricity generation as a relatively new and rapidly expanding physical and financial asset and a growing commodity within financial markets, I further draw from the literature on financialisation. A literature which, with its origins in Marxist heterodox economics, is now a well-established research stream within economic geography (Ioannou and Wójcik, 2019) and development studies (Bracking, 2016; Mawdsley, 2018). While definitions of financialisation can be ‘rather fluid’ (Furlong, 2019: 574) and subject to a growing and sometimes conflicting diversity of theoretical and empirical interpretations (Christophers, 2015; Fine, 2013; Lapavitsas, 2011), an over-cited but useful descriptor is provided by Epstein (2005: 3) who refers to ‘the increasing role of financial motives, financial markets, financial actors and financial institutions in the operation of the domestic and international economies’. More recently, Christophers (2015: 187) has summarised it as ‘the growing penetration of financial logics into our daily life-world, or finance’s increasing dominance of processes and outcomes of capital accumulation’.

A key feature of financialisation is the proliferation of finance capital and financial markets in the global economy and many national economies since 1970s, not least in countries with highly developed capital markets including the US and UK but also many emerging markets, including Mexico and South Africa (Karwowski and Stockhammer, 2017). At a national level, these developments have resulted in the financial sector taking up a large or dominant share of GDP as compared to other productive sectors, and the incorporation of national economies and firms into global circuits of financial capital as an indicator of economic maturity (Mawdsley, 2018).

Processes of financialisation have resulted in the increasing transformation of physical objects into speculative assets (Leyshon and Thrift, 2007), including in this case utility-scale renewable energy projects. As Schmidt and Matthews (2018: 152) elaborate, ‘infrastructure is a site where financial products (i.e. loans, bonds, securities) meet the material mobilization of “nature”’. Yet despite the considerable literature on infrastructure financialisation in general (e.g. Crow-Miller et al., 2017; Furlong, 2019), there are minimal studies to date on renewable energy as a new and emerging asset class. In light of this, Castree and Christophers (2015: 379) have called for analysts and policy-makers to understand how the financing of new infrastructure in the context of anthropogenic climate change currently functions, so that it can be shaped ‘to realise important non-economic goals’.

A nascent body of research that responds to this call includes US-centric analyses on the impatience of venture capital in the clean tech bubble in Silicon Valley in the 2000s and the subsequent move to ‘software-centric cleantech’ (Knuth, 2018) and the growing influence of conglomerate ownership on solar PV manufacturers in the 1980s (Jerneck, 2017). Despite these important contributions there are few studies on the links between renewable energy and finance in contexts of inequality in LMICs. Exceptions include Harrison and Popke (2018), who explore how processes of electricity sector liberalisation and procurement mechanisms for renewable energy from IPPs in the islands of the Caribbean have created dominant roles for IFIs and new networks of foreign-owned corporations and their shareholders; Kennedy (2018), who examines the contradictory outcomes of the influx of foreign investment into Indonesia’s solar PV sector; and Baker (2015a) who in unpacking the evolving role of finance in South Africa’s renewable energy sector finds a contradiction between the short-term nature of capital gains and demands for project ‘bankability’ on the one hand and the unique and potentially progressive requirements for community ownership and economic development on the other.

My analysis makes the following contributions to the literatures discussed above. First, while recent research has examined the complex nature of project finance for infrastructure and the multiple cascading contracts it involves (Ashton et al., 2012; O’Neill, 2019) such research has focussed on high-income economies with limited exploration of its more recent application to renewable electricity projects more specifically. Second, given that both the literature on the energy transition and the majority of studies of financialisation are focussed within national boundaries, there is therefore far greater scope to understand the cross-boundary nature of financial flows and foreign markets and its interaction with renewable energy systems (Christophers, 2015). Third, by examining interactions between public and private sources of finance and the key role of the former in leveraging the latter, I contribute to research on the shifting nature of development finance in recent decades, following Mawdsley’s finding of ‘a distinctive acceleration and deepening of the financialisation-development nexus’ (Mawdsley, 2018: 265). This ‘re-configuration of parts of the “developing world” as the risky frontiers of profitable investment’ (Mawdsley, 2018: 271), now sees development finance institutions (DFIs) providing ‘the institutional and material basis for capital penetration, financialisation, market development and a more orderly set of practices for the management of risk to capital’ (Carroll and Jarvis, 2014: 535).

Global processes: From liberalisation to financialisation

Procuring renewable energy

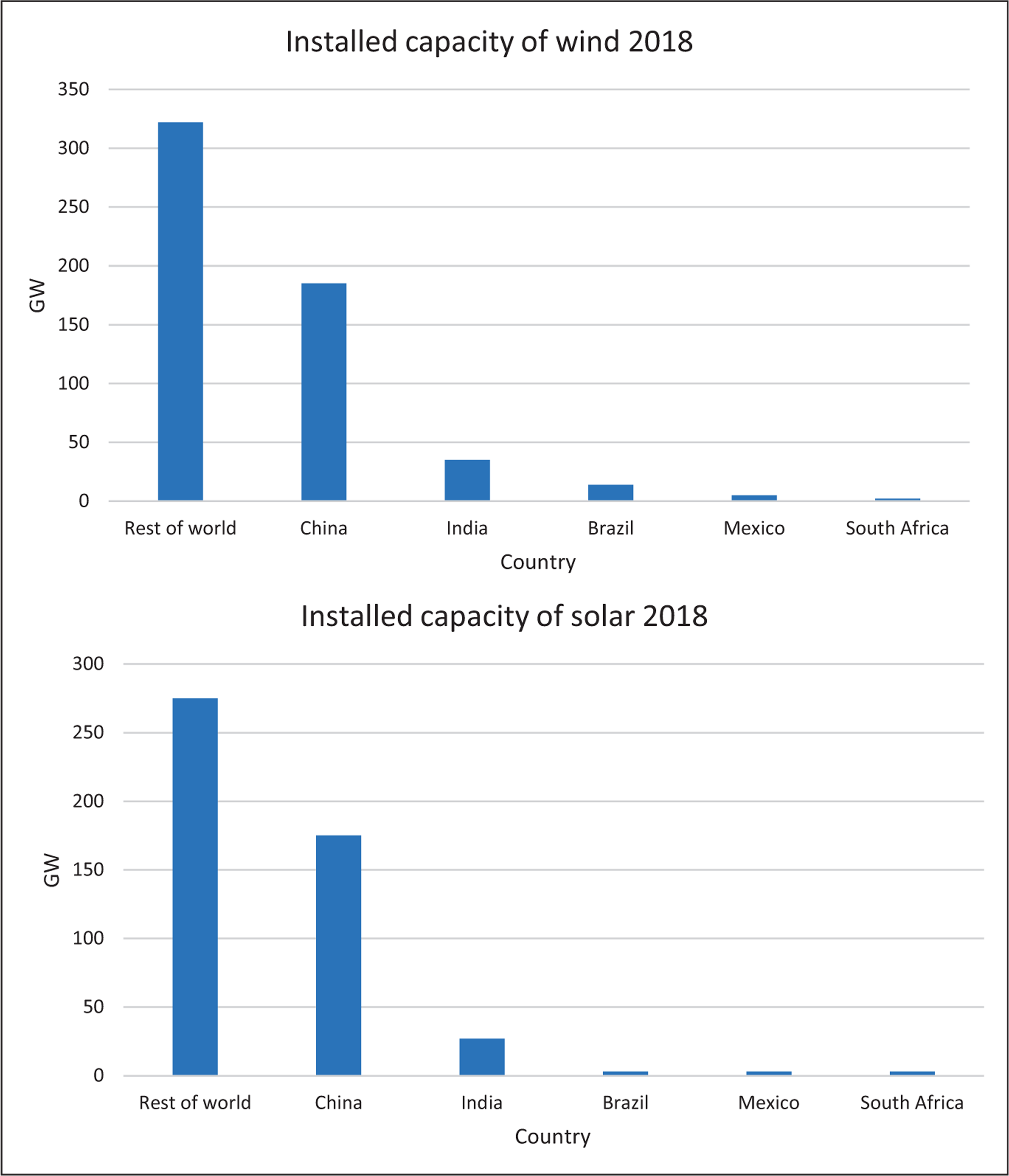

Since 2015 investment commitments for renewable energy have exceeded those of conventional energy such as coal and gas. In 2018 global investment in new capacity stood at $272.9 billion (UNEP/BNEF, 2019: 20) of which developing countries, dominated by China, India and Brazil, accounted for 54% and China for 33% (UNEP/BNEF, 2019: 22–23). While in global terms, Latin America (excluding Brazil) and sub-Saharan Africa represent a relatively small percentage of renewable energy investment and installed capacity to date (Figure 1(a) and (b)), this paper raises important questions regarding how the growth of such investment may continue to play out in these regions.

(a) Global installed capacity of wind, 2018. (b) Global installed capacity of solar, 2018. Source: IRENA (2019a).

Unlike large thermal sources of electricity generation which are often financed by public institutions, and nuclear energy which relies almost entirely on state-backed finance, private sources provide 90% of global renewable energy investment, of which the majority for solar PV and onshore wind (IRENA and CPI, 2018: 12). Much of this investment goes to IPPs, electricity generation projects that are privately developed, constructed, operated and owned with a dominant proportion of private finance (Eberhard et al., 2016). A significant proportion of this investment has been facilitated by market-based renewable energy auctions, or tenders with competitive bidding programmes, 2 which in the last decade have replaced state-determined subsidies and feed-in tariffs as the preferred regulatory mechanism for the procurement of utility-scale, renewable electricity generation (Hochberg and Poudineh, 2018). Between 2005 and 2019 the number of countries implementing renewable energy auctions grew from six to 100 (IRENA, 2019b) and by 2022 auctions are expected to procure half of new renewable capacity globally (OECD/IEA, 2018: 51). These auctions have developed in parallel with the privatisation of public sector capital investment and the internationalisation of investment in large infrastructure.

IPPs and renewable energy auctions have emerged out of long-standing and often ideologically driven shifts over how electricity should be governed. These shifts, sometimes referred to as the ‘regulatory pendulum’ in electricity governance (Hall et al., 2013), can be summarised into two opposing positions: between those arguing for a state-owned monopoly with central planning, and those for a liberalised market with an independent regulator (Baker et al., 2021). In the case of the latter, a liberalised electricity sector is perceived as competitive and efficient, and a state-owned one as over-subsidised, resistant to innovation and subject to the political demands of consumers and interest groups such as trade unions (Carreón-Rodríguez et al., 2007; Harraway, 2014). Proponents of liberalisation tend to assume that markets have a natural ability to facilitate a low-carbon energy transition through renewable energy IPPs, while a state-owned monopoly will remain controlled by carbon-intensive incumbents. Those in favour of state-ownership meanwhile see electricity as a public good, with accompanying assumptions that a state-controlled utility will act in the public interest, while a liberalised market and IPPs will simply prioritise the interests of corporate elites with limited concern for low-income consumers (NUMSA, 2014).

In the first half of the twentieth century the electricity sector, in countries where it was established, was generally a state-owned vertically integrated monopoly. But by the 1980s and 1990s and in keeping with the neo-liberal economic orthodoxy of the time, the ‘standard model’ of power sector reform had become highly influential across the globe. In developing countries this model was promoted by the World Bank and related consultants and in turn endorsed by other multi-lateral lending institutions as part of loan and debt relief conditionalities under structural adjustment programmes. The model, which was informed by the experiences of a small group of countries including the UK, USA, Norway and Chile, followed general assumptions that public ownership resulted in poor technical performance and was unable to meet the high levels of investment required by the electricity sector (Gratwick and Eberhard, 2008). The model’s proponents therefore prescribed the unbundling of state-owned utilities into private transmission, generation and distribution companies, including a significant role for wholesale markets and ultimately, retail competition (Sen, 2014).

However following repeated failings of its implementation in developing countries, the model has been subject to numerous criticisms, including for the generalised assumptions that it made about the nature of electricity access, state capacity and the national ability to attract investment, regardless of country context (Eberhard and Godhino, 2017; Sen, 2014). That said, many principles of liberalisation remain influential. Since then, various forms of ‘hybrid power markets’ have developed, in which vertically integrated, state-owned utilities remain as the dominant player and the single buyer of electricity but IPPs contribute a certain amount of generation capacity, selling their output to a government off-taker, often the utility, or a corporate buyer under a power purchase agreement (Eberhard et al., 2016). Renewable energy auctions play a key role in these hybrid power markets, including in South Africa and Mexico as I discuss below.

Auctions follow a market-based framework under which IPPs submit a bid with a price per unit below a certain tariff cap at which they would sell the electricity generated by their project to the grid. Auctions are usually held under a series of bidding rounds which set the total volume of generation capacity that can be awarded. The project that meets the qualifying criteria at the lowest price wins the bid. The nature of these qualifying criteria however can vary depending on the country or region. For instance, while South Africa’s auction programme includes criteria for socio-economic development and community ownership, Mexico’s is assessed on price alone (see ‘Territorial realities: South Africa and Mexico’ section). A further variation is that while in South Africa capacity is specified by technology type, in Mexico it is technology neutral. While auctions in some countries place restrictions on the volume of projects or MW allocations that can be awarded to individual companies under each round, others do not. In Mexico for example, the lack of restrictions has resulted in a small number of large companies being awarded majority control of the market including Italy’s Enel Green Power, US SunPower, China’s Jinko Solar and Spain’s Acciona (Yaneva et al., 2018).

The financial and technical principles of auction programmes are now well-documented, including by industry, regulators and practitioners (cf. Eberhard et al., 2016; Norton Rose Fulbright., 2017). However, and as evidenced in ‘Territorial realities: South Africa and Mexico’ section, the financial, contractual and regulatory blueprints currently in circulation (e.g. Abrams, 2017) have tended to overlook the importance of the socio-economic, political and cultural context of the locality in which they are operating. Indeed, the significant challenges that such a context can pose to the implementation of renewable energy auction programmes and the utility-scale projects they facilitate have often been underestimated by project developers, regulators and/or governments. Consequently, socio-economic development criteria such as those in South Africa can be perceived as an investment risk by developers for imposing constraints that drive up the cost of capital, reduce profit and discourage or even deter investment (IRENA, 2017: 38). Moreover, the competitive nature of auction programmes tends to create huge barriers to entry for smaller players including community energy companies which are unable to meet the high financial and transaction costs of participation, such as feasibility studies, qualification arrangements, deposits or bonds, or to absorb the heavy risks and losses incurred by an unsuccessful bid.

Yet as a result of this competitiveness, a significant decrease in the electricity tariffs submitted by project bidders has taken place, particularly over the last five years (OECD/IEA, 2018: 51) and in many countries, Mexico and South Africa included, electricity generated from wind and solar PV is now on a par with or cheaper than that generated by conventional technologies such as coal and gas (IRENA, 2018a). These decreasing tariffs have been assisted by the relatively cheap costs of capital in the last decade due to low global interest rates, particularly in mature markets (UNEP/BNEF, 2019: 42). The cost of capital is a significant consideration given that the majority cost of a wind or solar PV project derives from the upfront expenditure on project construction, unlike thermal and nuclear power plants of which the costs are spread throughout the project’s operation, including fluctuating fuel costs.

Financing renewable energy

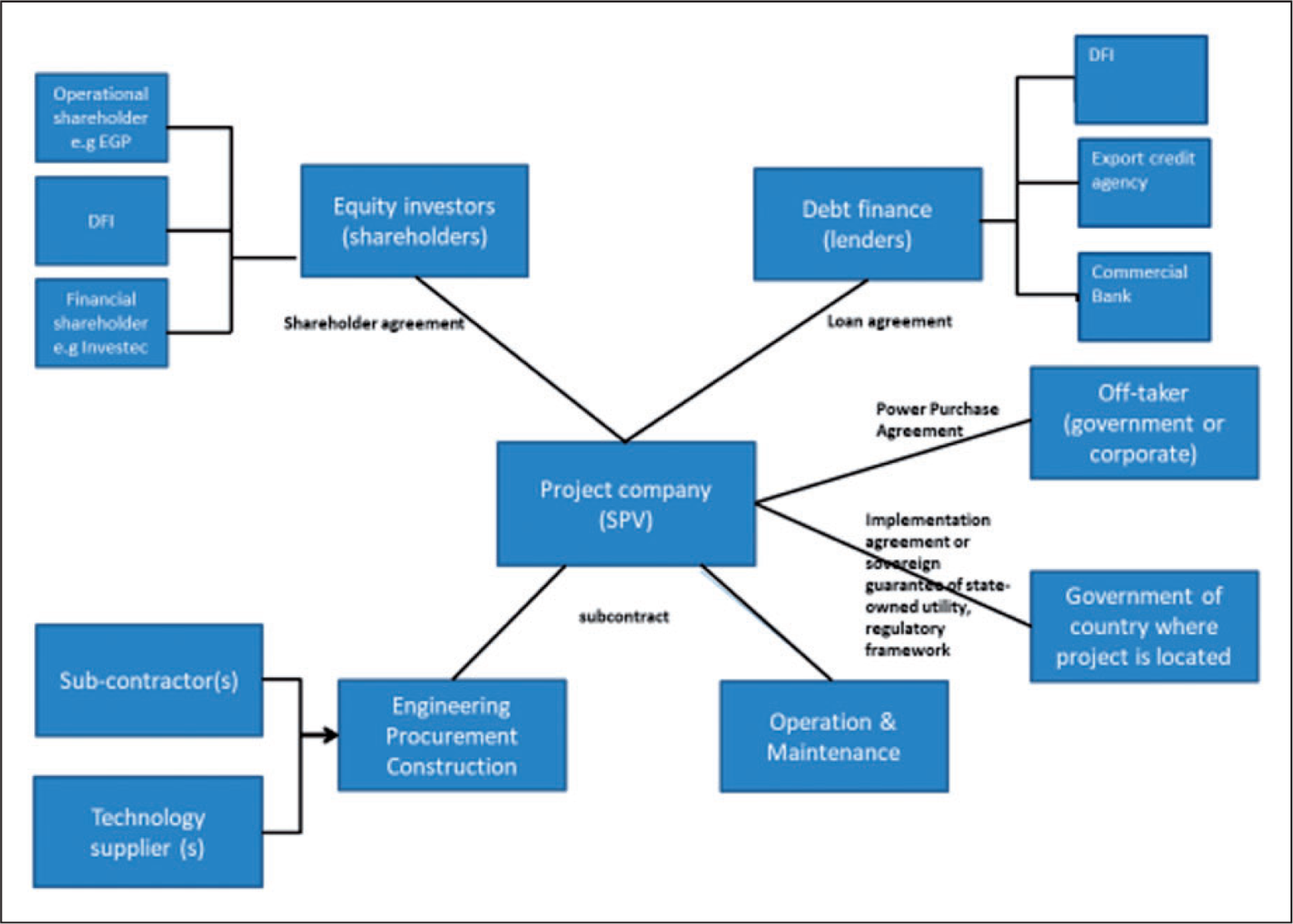

Project finance emerged in 1980s as a mechanism for long-term, capital-intensive financing for privately generated electricity generation projects (see Figure 2; Baker, 2015b; Yescombe, 2013: 9–11). The greatest contribution of project finance now goes to utility-scale renewable electricity generation which is growing in importance in emerging markets such as South Africa and Mexico, where what investors deem as ‘supportive policies and contractual structures that guarantee predictable long-term cash flows’, e.g. auctions, are now in place (OECD/IEA, 2018: 125). As the OECD/IEA (2018: 120) further explains: ‘project finance is generally used in the case of complex and large projects where the industry may be relatively less mature, but financiers have a high level of understanding of the government policy that underpins the business model’.

Example of project finance structure for a renewable electricity project. Source: Author’s own.

The design of renewable energy auction programmes and corresponding structures of project finance have co-evolved to become increasingly sophisticated, complex and opaque, in parallel with the evolution of utility-scale renewable energy as a highly competitive industry that favours economies of scale in the supply chain and large global corporate players. Since 2010 in particular these developments have been accompanied by significant decreases in the costs of technology and operation and maintenance, and in turn decreased investment risk and decreased costs of capital. Within the last five years a rapid consolidation of the global renewable energy industry has taken place with significant corporate mergers and acquisitions leading to restructuring processes and subsequent job losses (Renewables Now, 2018).

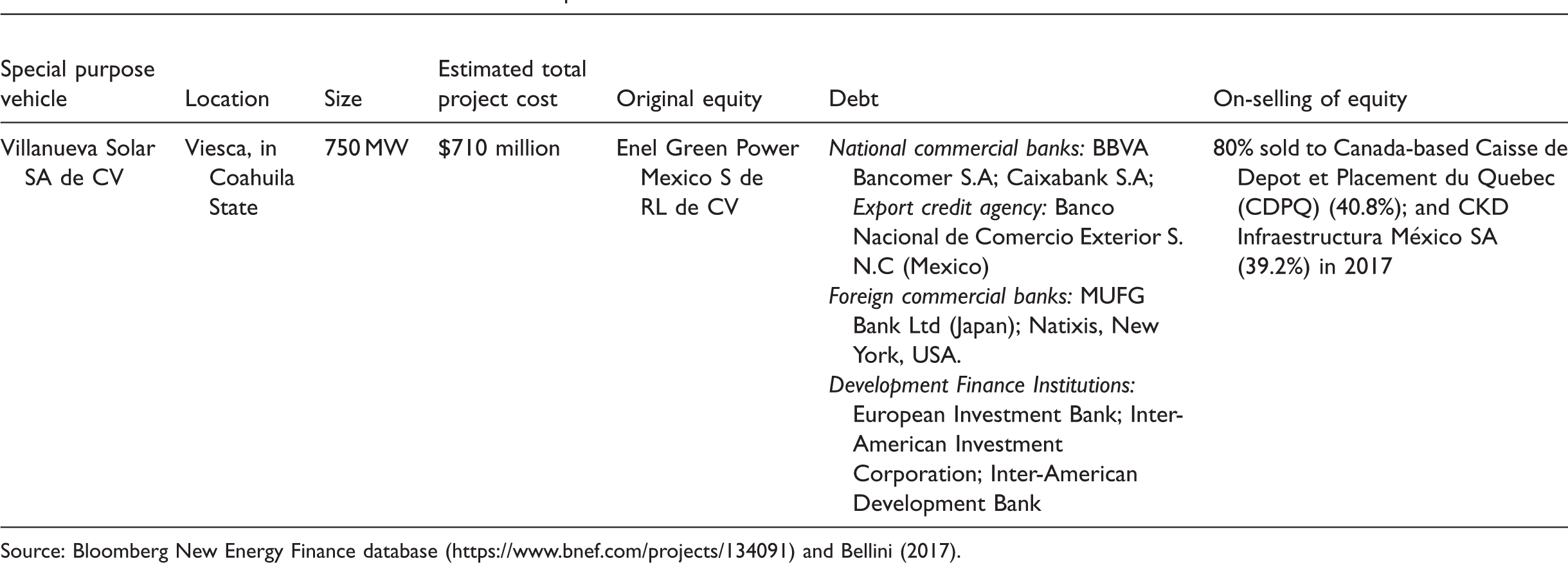

Despite national and regional variations, the global renewable energy market is now dominated by fewer and bigger developers with strong balance sheets, operating within highly globalised production networks (Knight, 2018) involving major original equipment manufacturers and engineering, procurement and construction companies (EPC), such as Nordex-Acciona, Siemens-Gamesa, Vestas and Goldwind. As the technologies for utility-scale renewable electricity generation have grown in size and become more efficient, so has project size, particularly in the case of offshore wind in Europe and China, and onshore wind and solar PV in emerging markets. Two key examples of the latter include Mexico’s 424 MW Reynosa 1 wind farm and 750 MW Villanueva solar PV plant (see Table 1). A key reason for this growth in scale is because larger projects offer higher returns, which lower the cost of capital and help project developers to negotiate better terms for debt financing (OECD/IEA, 2018: 52). 3

Financial structure of Enel Villanueva solar PV plant in Mexico.

Source: Bloomberg New Energy Finance database (https://www.bnef.com/projects/134091) and Bellini (2017).

As outlined in Figure 2 project finance for renewable electricity generation typically involves the establishment of a special purpose vehicle (SPV) or a limited company, set up for the sole purpose of developing, operating and owning the project. The nature of this structure means that risks are allocated among the various consortia involved in the SPV and are largely held off the balance sheet of the parent companies involved (IEA/OECD, 2018: 119).

As Figure 2 further illustrates, once established the SPV enters into contracts with the companies or consortia that undertake the EPC and operation and maintenance of the project, as well as the power purchase agreement with the off-taker, which may be a state-owned utility or a corporate buyer depending on the national regulatory framework. In the case of South Africa, the state-owned utility Eskom is the sole off-taker while in Mexico, projects sell either to the state utility Comisión Federal de Electricidad (CFE) or to a corporate buyer which must have a nominal ownership in the project, e.g. Spanish utility Iberdrola and Mexican cement company Cemex (Yaneva et al., 2018). Utility-scale projects typically have fixed price contracts for their electricity generation via a legally binding power purchase agreement which lasts for 15 years in Mexico and 20 in South Africa, thereby generating a long-term, predictable cash flow for investors. The SPV also enters into an implementation agreement or state-backed guarantee with the host government which guarantees payment to the project company in the event of the off-taker default. This sovereign guarantee is nearly always required by lenders and investors for projects in developing countries and forms a key part of reducing the project's investment risk, as discussed below.

Debt financiers, or ‘lenders’, provide finance-based debt on fixed loan terms on the project’s future cash flow and have no or limited recourse to the liability of the parent companies involved in the SPV. Debt is often provided by a national commercial bank, for example Standard Bank in South Africa and Banco Santander in Mexico or a combination of national commercial banks acting in syndication with each other in larger projects. Public finance from multilateral, regional, bi-lateral and/or national development finance institutions (DFIs) and/or export credit agencies (ECAs) may also be involved in the debt syndicate (see Tables 1 and 2). This public finance may be provided at concessional interest rates depending on perceived investment risks related to the country, the project and the technology in question (IRENA and CPI, 2018; see Table 3). Risk mitigation instruments, for instance from the World Bank’s Multilateral Investment Guarantee Agency (MIGA) may also be included in the debt syndicate in order to help address some of the risks outlined in Table 3. Lenders are the first to receive financial revenues generated by the project and are not liable for any losses the project may make. They therefore take a lower level of risk than equity investors.

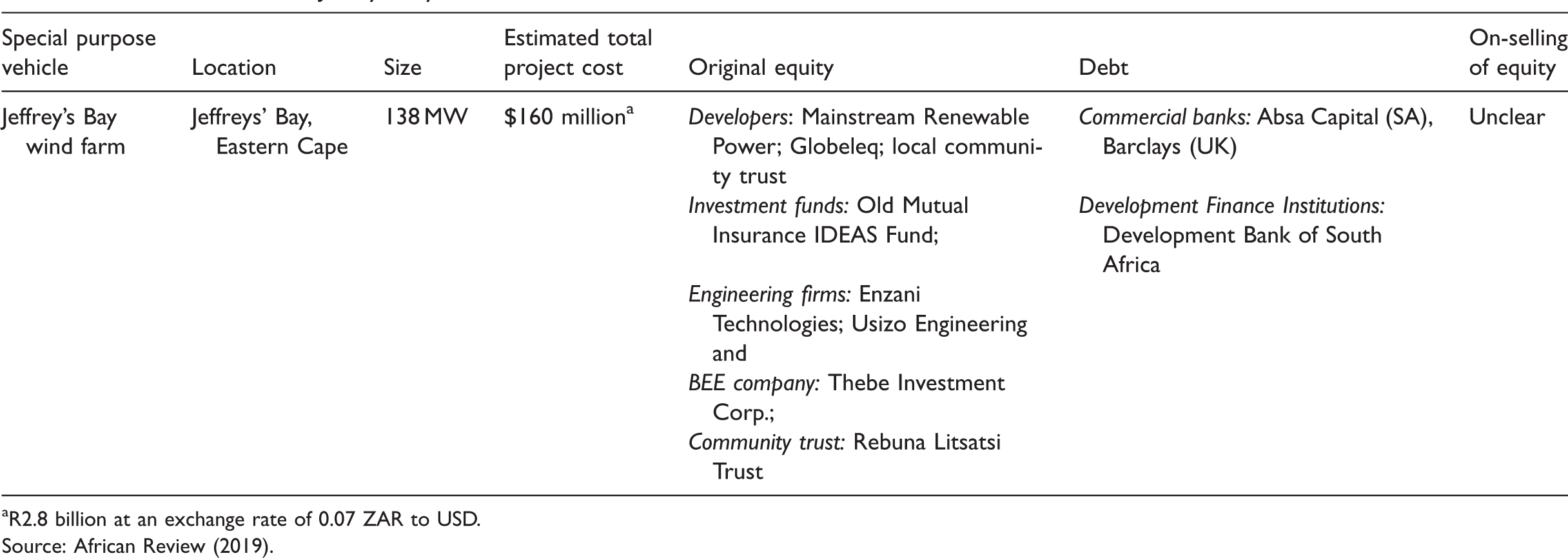

Financial structure of Jeffreys’ Bay wind farm in South Africa.

aR2.8 billion at an exchange rate of 0.07 ZAR to USD.

Source: African Review (2019).

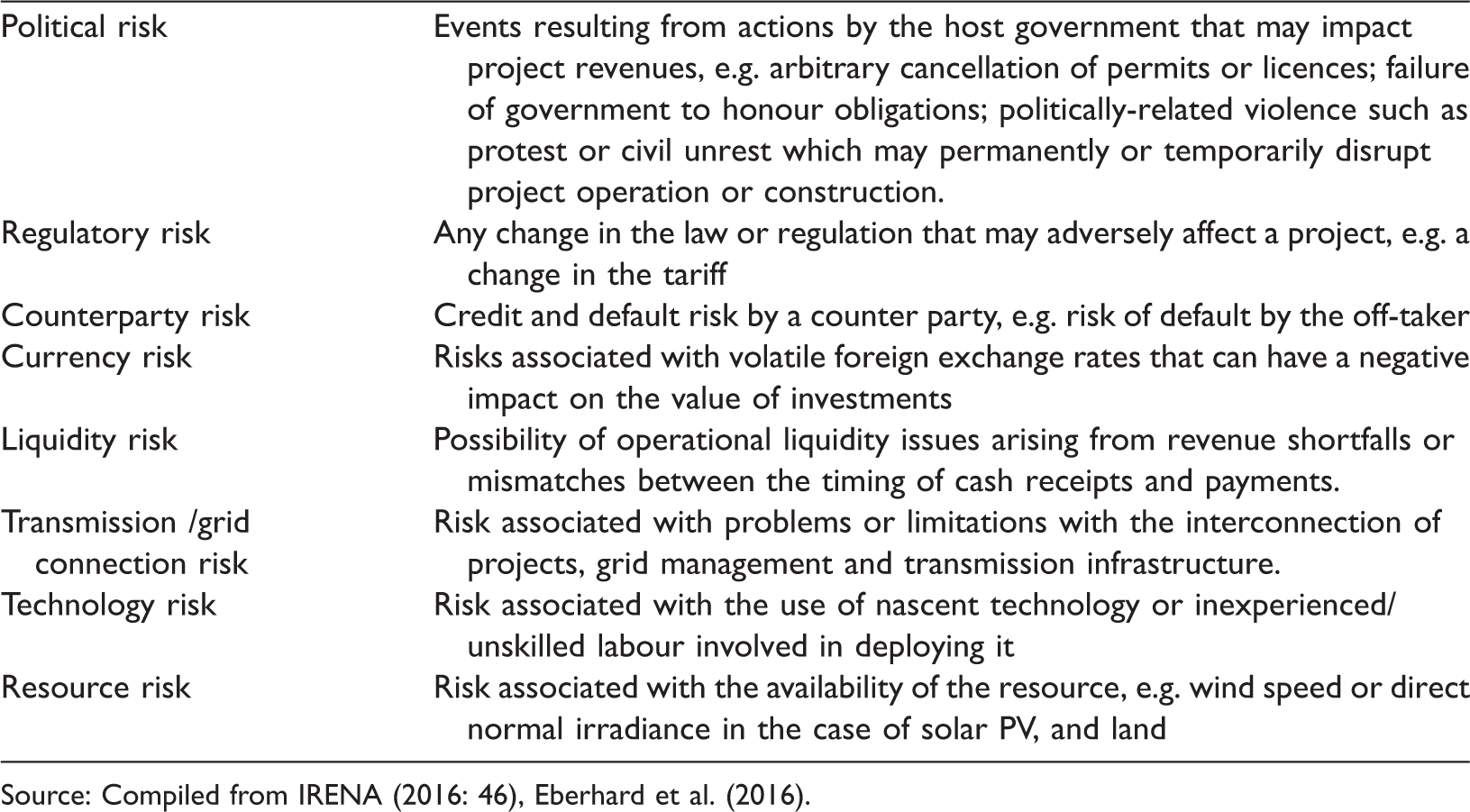

Types of risk in renewable energy project finance.

Source: Compiled from IRENA (2016: 46), Eberhard et al. (2016).

The equity shareholding of the SPV refers to the consortium of investors who hold a share in the ownership of the asset. Typically this consortium includes the renewable energy project developer(s) who often hold the majority share, and financial investors such as private equity infrastructure funds. Some concessional finance from a DFI or ECA may also be present within an equity shareholding depending on the technology, the country and other conditions. In the case of South Africa and Mexico, key players in the equity shareholding include major European companies and utilities; national industrial companies; institutional investors; and dedicated renewable energy investment vehicles (see Tables 1 and 2). Equity investors are the last to receive cash flows generated by the project and are therefore far more dependent on the project’s success than debt financiers. Because they carry greater risk, they therefore expect to generate higher returns through the project revenue stream (IRENA, 2016).

While the financing of a renewable electricity generation project was previously structured on the basis of a 70:30 debt to equity ratio of the capital cost of the project, it is now more often structured on an average ratio of 80:20 (OECD/IEA, 2018). In simple terms, the higher the proportion of debt there is in a project finance arrangement, the lower the average cost of capital, the lower the tariff and the cheaper the project. In essence, as the renewable energy sector has matured, so has it become a more viable prospect for developers and investors.

From renewable energy finance to the financialisation of renewable energy

The role of development finance in facilitating processes of financialisation discussed in the ‘On the energy transition and the role of finance’ section is also evident within project finance configurations for renewable energy. While in previous decades development finance was disbursed largely in the form of grants and loans, the nature of this sector is now such that it operates in partnership with institutions ‘which are themselves increasingly governed by financial logics’ (Mawdsley, 2018: 267) including SPVs, venture capital, hedge funds, sovereign wealth funds, credit ratings agencies and global accountancy firms (Sinclair, 2008). While private sources provide 90% of global renewable energy investment (IRENA and CPI, 2018), public finance plays a very significant role in leveraging and de-risking this investment, particularly within debt syndicates in project finance (see Figure 2, Tables 1 and 2). However, the nature of these arrangements varies according to the national setting. In South Africa for example, development finance has played a much greater role than the global average, and in some years has been more dominant than sources of private investment. Development finance in Mexico meanwhile has been more in line with the global average, standing at 10% of all energy investment in 2018 (Global Climate Scope Website, 2019).

Debt from DFIs leverages the participation of commercial banks through grants, concessional and non-concessional loans and risk mitigation instruments, particularly in countries with a limited track record of renewable energy infrastructure development and where the investment climate may otherwise deter commercial banks and private investors. In addition to their mobilisation role in project finance, significant technical assistance has also been given by bi-lateral and multi-lateral donors for the design and implementation of policies to promote renewable energy markets, e.g. auction programmes and related regulatory reform and fiscal incentives (Baker, 2015b; IRENA and CPI, 2018: 28).

Perceptions and definitions of investment risk (see Table 3) and related commercial priorities for ‘bankability’ hold a fundamental influence over the terms and structures of project finance, the setting of the cost of capital and the internal rate of return of the project (IRENA, 2016; Yescombe, 2013). For lenders and investors, the higher the risk the higher the anticipated return, which inevitably increases the cost of capital. If the cost of capital is too high, it may become too expensive to borrow and prove prohibitive to the viability of a project. While investment risks are deemed higher in LMICs than they are in more established renewable energy markets such as the US and Europe, so are the returns. Yet rather than the neutral and technical entity that risk is often presented as by commercial banks, investors and project developers, its definition and how it is allocated is highly subjective and contested. There are multiple considerations in defining risk, the emphasis of which can shift depending on the concerns and priorities of the moment, the technology and national socio-economic and political conditions (Baker, 2015a). Table 3 summarises common definitions of project risk, of which some examples are outlined in the ‘Territorial realities: South Africa and Mexico’ section.

As the project finance industry has evolved in recent decades, so too has a highly professionalised industry of intermediaries such as lawyers and technical advisors who charge high fees to negotiate the terms of investment risk on behalf of their clients, e.g. the lender, the shareholders, and the off-taker or the government department responsible for the PPA or host government agreement as illustrated in Figure 2. As Baker (2015b: 339) surmises, renewable energy development is ‘conducted by private actors who proliferate behind a cloak of contractual opacity that encourages extraordinary risk taking’ which helps to shield principal actors in project finance transactions ‘from the consequences of their risky behaviour’.

The process of the financialisation of a renewable electricity generation project comes about through the development of a secondary market, which sees a proportion of the equity shareholdings and/or debt finance within the SPV being refinanced or on-sold just before or after project construction. These sales are often to entities such as insurance companies, pension funds and dedicated infrastructure investment firms for whom the project will generate a long-term, stable and predictable cash flow. Following Schmidt and Matthews (2018: 152), investments in utility-scale renewable energy projects ‘are increasingly entangled with circuits of global finance both as capital is raised and as debts and securities are traded’. As a result, recent years have seen an explosion in new renewable energy business models and financing vehicles, including the rise and fall of the YieldCo, defined as ‘a company that owns assets that generate predictable cash flow’ (Varadarajan, 2016) but which was linked to bankruptcies of the developers SunEdison and Abengoa in 2016, both of which affected the sustainability of projects in South Africa (Renewables Now, 2018). With many renewable energy companies, infrastructure investors and investment vehicles now listed on global stock exchanges, there is also a growing international market for green bonds which are used to refinance a project after construction, including in South Africa and Mexico (Ngwenya and Simatele, 2020; Yaneva et al., 2018: 26).

The nature of this on-selling goes to the tensions at the heart of this research. On the one hand the finance industry claims that a secondary market frees up capital for further investment into renewable energy elsewhere (Wroblewska, 2015) and that institutional investors have a crucial role to play in scaling up renewable energy investment as the largest potential source of private capital (IRENA, 2016: 12). Yet the opposing view counters that the nature of this market creates a disconnect between the ownership of the project and the responsibility for it (Bryan and Rafferty, 2006: 75). As Furlong (2019: 574) discusses, ‘while capital may abandon a set of infrastructures, people-especially low-income people- often cannot’. In a similar argument Lohmann and Hildyard (2014: 78–79) explain how ‘equity funds rarely become linked with any given community for more than a few years’, … resulting in ‘the disembedding of capital from specific local commons and its re-embedding in social and political networks of power located elsewhere’. How these tensions between the international mobility of renewable electricity capital and the static nature of local commons are playing out in South Africa and Mexico is now discussed.

Territorial realities: South Africa and Mexico

Both South Africa and Mexico have been shaped by their own unique histories of colonialism and structures of socio-economic, political and spatial inequality. South Africa’s apartheid legacy has resulted in severe inequality along racial divisions despite recent attempts at the redistribution of land and legislation for black economic empowerment (Harvey, 2015), while a key feature of Mexico’s inequality has been the marginalisation of Indigenous peoples who hold a strong collective identity and deep cultural relationship to their land and territory (Avila-Calero, 2017). In Mexico, 70% of Indigenous peoples are poor and 40% of speakers of Indigenous languages live in extreme poverty, lacking access to the basic services of water, health, education and electricity (CONEVAL, 2016).

Alongside such inequality, both countries are members of the G20 group of the world’s largest emerging economies and have sophisticated financial markets. South Africa’s Johannesburg Stock Exchange is the largest and oldest on the continent and Mexico’s stock exchange, La Bolsa Mexicana de Valores, is Latin America’s second largest after São Paulo. Both countries are regional leaders in renewable energy deployment in sub-Saharan Africa and Latin America and the Caribbean respectively and in recent years have undertaken complex regulatory reforms of their electricity sectors along the lines discussed in ‘Procuring renewable energy’ section in order to enable the introduction of auction programmes for utility-scale renewable electricity and generation by IPPs.

In South Africa these reforms included amendments to the country’s Electricity Generation Act in order to allow for the introduction of the renewable energy independent power producers’ programme (RE IPPPP), launched in 2011. Under RE IPPPP, successful projects sell power to the state-controlled monopoly electricity utility Eskom, which otherwise continues to dominate generation, transmission and distribution in the country (Baker et al., 2015). In Mexico, changes were made to the constitution in order to permit the introduction of the country’s Ley de la Industria Eléctrica (the Electricity Industry Law) in 2014 in addition to other relevant laws and amendments, thereby creating a wholesale electricity market of far greater complexity than South Africa’s.

The outcome of Mexico’s reforms built on earlier though largely unsuccessful attempts to liberalise the sector initiated in 1992 (Carreón-Rodríguez et al., 2007). Such attempts however eventually led to the introduction of a limited number of IPPs, which generated electricity either for own use or for sale to the CFE. This development was then followed by an expanding coalition of national and international corporate and financial interests in the wind industry in the 2000s, pushing for the remaining barriers to the independent production of wind to be removed. Binding targets for renewable energy were introduced in 2008, and by 2012, 1.2 GW of wind farms had been built in the isthmus of Tehuantepec, of which the majority for self-supply (Boyer and Howe, 2019: chap 2). In 2016 the national auction programme for the procurement of utility-scale electricity from renewables and other generation was eventually launched (OECD/IEA, 2017).

Auctions in both countries gained international praise and recognition and facilitated the involvement of many of the world’s largest renewable energy developers, EPCs and technology suppliers. While the contribution that renewable electricity from IPPs currently makes to overall generation capacity in both countries is minimal, it is predicted to increase: wind and solar PV is set to constitute 14% of Mexico’s generation capacity by 2024 (OECD/IEA, 2017), and 25% of South Africa’s by 2030 (Department of Energy, Republic of South Africa, 2018).

By March 2019 South Africa’s RE IPPPP had secured $14.8 billion 4 in investment commitments and procured 6.4 GW of generation capacity from 92 utility-scale IPPs under five bidding rounds (IPP Office, Republic of South Africa, 2019). Yet despite an unprecedented take off in 2011, RE IPPPP stalled between 2015 and 2018 for reasons which include political opposition and a refusal by the state-owned monopoly utility Eskom to sign power purchase agreements of projects awarded under the fourth bidding round. Eskom justified this move by arguing that it would make a loss from having to purchase energy from IPPs. The utility’s opposition has been supported by some trade unions and factions from government and business associated with former president Jacob Zuma, protesting against what they see as the ‘capitalist capture of renewable energy’ and arguing that renewable energy will undermine jobs in the coal industry (Cloete, 2018). It was not until April 2018, following the inauguration of President Cyril Ramaphosa that the outstanding power purchase agreements were signed.

By comparison, and in part due to the already existing presence of a wind industry in the country, Mexico’s auction programme developed much more rapidly under three tendering processes initiated in 2016. The country has now attracted $6 billion of investment commitments for the 5 GW of renewable electricity generation procured thus far. By 2017 Mexico had joined the top 10 countries of renewable energy investment (UNEP/BNEF, 2018: 20) and the results of its third power auction in 2017 broke records, with average wind contracts agreed at $18.60 per MWh, and solar at $20.80 per MWh (UNEP/BNEF, 2018: 40). Yet in a comparable story to South Africa, Mexico’s auction programme has also now stalled due to political challenges following the voting in of president Andrés Manuel López Obrador of the centre left National Regeneration Movement (MORENA) in late 2018. In a move unanticipated by the renewable energy industry and even by some government departments, in early 2019 López Obrador announced the suspension of the programme and his intention to hand control of the electricity sector back to the former state-owned utility the Comisión Federal de Electricidad. He justified this move on the basis that private companies were supplying the market with high costs (Bellini and Zarco, 2019).

This high-level political opposition to utility-scale renewable electricity generation and privately generated power in both countries comes back to the concept of energy as a site of struggle and to the ideological debate over whether electricity should be owned and governed by a state monopoly or a liberalised market discussed in the ‘Procuring renewable energy’ section. It further serves as an example of political, regulatory and counterparty risk discussed above. This political struggle has been paralleled by failures to adequately benefit and include local communities in the vicinity of renewable energy projects in South Africa, and in the case of Mexico increased inequalities and violent civil resistance of which the latter has challenged the viability of the renewable energy projects under development.

Auction design has differed between each country. Under South Africa’s RE IPPPP, project companies not only have to submit a bid below a set tariff cap at which they will sell electricity to the state-owned utility Eskom but also demonstrate how the project will meet certain socio-economic criteria. The evaluation of the bid is allocated 70% on the tariff and 30% on socio-economic development criteria, with the winning projects meeting the requirements at the lowest price. These socio-economic criteria include the participation of black-owned companies in the equity shareholding as part of the country’s black economic empowerment legislation introduced to address socio-economic marginalisation in the post-apartheid era. A further requirement is that local communities located within a 50 km radius of the project must be structured into the equity from a minimum shareholding of 2.5%. This shareholding is then managed by a legally established community trust, which is responsible for representing the local community and managing a dividend of about 1.5% of projected revenue (Baker and Wlokas, 2015).

Despite the progressive potential of these criteria, evidence thus far suggests that there have been a number of flaws in the implementation of the community trusts. First, revenue will only flow to the community after the project’s debt has been paid off, usually in about year 15 of project operation (Baker and Wlokas, 2015). In addition, many project trusts have been established by project developers with minimal or no consultation with the community concerned. Project companies have also been allowed to dictate local community empowerment targets to local residents during the bidding process (Nkoana, 2018) but have then failed to deliver on the targets they set. As the majority of projects are situated in rural areas with high rates of poverty and unemployment, this has challenged the already limited planning capacity of municipal and provincial governments (Wlokas, 2015). For this reason, in many instances poor management of the process has resulted in a ‘tyranny of participation’, which has reinforced ‘the control of powerful stakeholders over vulnerable communities’ (Nkoana, 2018).

Conflicts have also taken place within the trusts over how the expected revenue streams should be allocated and spent within the community (Wlokas et al., 2017). This, in addition to the problematic process of identifying who qualifies as a community member within the 50 km radius in light of the mobile nature of young residents in particular who migrate to cities for the purpose of employment (Wlokas et al., 2017). While in some regions there are multiple IPPs in close proximity which has resulted in overlaps between the 50 km radiuses, many trusts still operate in isolation from each other (McEwan, 2017). The promise of local jobs in the vicinity of many of the sites has also created false hope for many community members given that the majority of the employment potential for unskilled workers for a wind or solar plant lies in the construction phase of approximately two years. After this, operation and maintenance depends on only a small core of highly trained specialists who are generally recruited from elsewhere.

In Mexico by comparison, bids are assessed primarily on the tariff submitted, through a process that was specifically designed to encourage low prices. As discussed in the ‘Financing renewable energy’ section, projects procured under the auction sell either to the state utility, the CFE, or from the third bidding round onwards, to a corporate buyer which must have a nominal ownership in the project. Generators of renewable energy will also receive clean energy certificates for 20 years which do not expire and can be purchased and sold, thereby serving as an additional incentive for developers. Unlike in South Africa, there is no specific requirement for community equity ownership and project developers have minimal formal responsibility for local community development beyond social and environmental impact assessments. In a similar story to that of South Africa, some local community members have gained employment during project construction but the potential for permanent work in renewable energy is limited. While the IEA referred to Mexico’s renewable energy auction as ‘one of the most ambitious, comprehensive, well-developed reforms undertaken in the world since the 1990s’ (OECD/IEA, 2017: 13), the long-term social sustainability of the projects has since come under question (Radowitz, 2017; REN21, 2017).

A key reason for this is because utility-scale renewable energy projects in Mexico are being built disproportionately in Indigenous territories, with high poverty rates and marginalisation and where people have centuries-long cultural and spiritual ties to the land. Notably in the ‘wind corridor’ in the Isthmus of Tehuantepec in Oaxaca between the Pacific and the Atlantic oceans covering an area of 1200 km2, and in the states of Yucatán for solar PV and Puebla for small hydroelectricity (Avila-Calero, 2017; Boyer and Howe, 2019). There are now 31 wind farms in operation in Oaxaca (Government of Oaxaca, 2020), the third poorest state in Mexico and in which there has been the greatest level of civil unrest against utility-scale renewable energy projects. These are projects that were built before the start of the auction programme, as well as those facilitated by it, many of which have been developed by a small number of large international companies, or subsidiaries thereof who have been awarded majority control of the market as discussed in the ‘‘Procuring renewable energy’ section (Yaneva et al., 2018).

However, the extent to which Indigenous communities have benefited from the projects to date has been limited and rarely evenly distributed, with notable negative impacts including conflicts over land tenure and corruption (Boyer and Howe, 2019). In the case that the project will affect an Indigenous community, it is the Mexican state that holds responsibility for gaining the community’s consent (Baker, 2015b). The country’s renewable energy auction process draws on domestic legislation and international standards on the rights of Indigenous peoples and in particular the mechanism of ‘free, prior and informed consent’ (FPIC). FPIC, which originates in international human rights law as set out in the United Nations Declaration on the Rights of Indigenous Peoples (UNDRIP), has in recent years been incorporated into environmental and social lending safeguards of the World Bank’s private sector lending arm, the International Finance Corporate, other DFIs and Equator Principles Banks. For this reason, DFIs have played an important role in setting up consultations (Baker, 2015b).

Large-scale wind development in Mexico has often been highly divisive and deepened inequalities. Land tenure reform introduced in 1992 which allowed Indigenous rural communities to sell, rent and subdivide previously communal land served to encourage agribusiness, forestry and more recently the development of large-scale wind farms. For this reason, Avila-Calero (2017: 993) argues that renewable energy project development has contributed to ‘the enclosure of communal lands, the private appropriation of benefits, and the lack of democratic procedures’. Similarly, Baker (2015b: 11) has documented that subsidiary companies acting on behalf of wind farm developers have put pressure on rural farmers ‘to sign long-term leases to communally-owned land’, the terms of which have been highly favourable to the developer at the expense of the lessor. In many cases the affected farmers are not native speakers of Spanish and, lacking in representation are in no position to decipher the legal language which make up these contracts. Such contracts have played a key role in reducing the nature of investment risk discussed above. The nature of land reform and the contracts that have ensued have also contributed to divisions between communities who own land and have been able to profit from renting it out to the project developer, and those who do not and are thereby denied opportunity for any socio-economic gain (Boyer and Howe, 2019).

There has also been resistance against such developments, including community blockades and extensive protests, resulting in protracted litigation (Baker, 2015b; Boyer and Howe, 2019). Dunlap (2018) for instance describes how wind energy developments in the Isthmus of Tehuantepec have resulted in ‘violent social divisions’ between the police and demonstrators protesting against the dispossession of land, community, sacred sites and cultural traditions facilitated by locally recruited private security services. Yet as Avila-Calero (2017: 1000) explains, the resistance is rarely against wind power per se, but rather against the way in which it is carried out, or in other words, ‘against land grabbing and its impacts over local communities’. Such resistance has resulted in construction delays or even acted as a deterrent to continued project development and serves as a key example of political risk summarised in Table 3.

As this section has discussed, utility-scale electricity in both countries has been enabled by procurement mechanisms and financial arrangements that have contributed to existing relations of inequality and nationally specific pathways of historical marginalisation. The broader implications of these examples for renewable development elsewhere evokes Rignall’s (2015: 554) finding that energy transitions ‘are not only about energy, or even geography, they are about how power infuses the relationships between energy, politics, and the spatial transformations associated with transition’.

Conclusion

Utility-scale renewable electricity is at once a tool of climate change mitigation, a new and rapidly expanding infrastructural and technological sector embedded within specific localities, and an emerging asset class that is subject to the priorities and interests of transnational capital. In this paper I have set two key competing objectives of utility-scale renewable electricity projects in context: as a predictable, long-term revenue stream for investors, and as a mechanism for socio-economic development and community empowerment. In so doing I have unearthed key tensions within the design and implementation of utility-scale renewable energy procurement programmes in South Africa and Mexico; the finance and ownership configurations they facilitate; the extent to which the socio-economic benefits of these new technologies and infrastructures are being distributed to local institutions, communities and individuals; and the conflict and struggles that have ensued. As I have identified, key tensions exist in the design of auction programmes as the dominant procurement mechanism for renewable electricity generation, between the competition involved in winning a successful bid with the cheapest electricity generation possible on the one hand, and the collaboration required to ensure the realisation of socio-economic benefits, local acceptance and the inclusion of local stakeholders on the other. With this in mind I now offer the following four conclusions.

First, this paper has laid the ground for deeper empirical and theoretical research into the need to think critically about the role of finance in the energy transition. Such thinking should include how the potentially diverse risks and rewards of utility-scale renewable energy procurement programmes and the projects they facilitate have been negotiated and allocated, and the extent to which current structures could be reformed to more equitable and sustainable ends. A far greater understanding of the complex and differentiated configurations of finance and investment that shape the development of associated infrastructures and technologies is needed, not least in terms of the implications this has for local ownership, inclusion and socio-economic development. Further exploration is also needed into the way in which finance capitalism has been able to transform utility-scale renewable electricity infrastructure into new and diverse asset classes that can become increasingly divorced from their impacts at the local level through a growing secondary market and processes of financialisation.

Second, the co-evolution of renewable energy procurement, structures of finance, and the growth in size of utility-scale projects and their corresponding technologies is arguably moving towards an industry of ‘big technology, big infrastructure and big capital’ and a market dominated by an increasingly consolidated industry. Yet while this research has focused on the utility-scale, the nature of finance and ownership of emerging models of decentralised and distributed models of electricity is an important area for future research. As the cases of South Africa and Mexico have illustrated, while high-level political opposition and disagreement can play a key role in undermining or at least delaying regulatory and procurement processes for renewable energy, assumptions of simple binaries between public and private, and market and state in electricity governance require further unpacking. Not least, as the nature of project finance in both countries has demonstrated, subsidiaries of foreign companies from countries in which their own state is the majority shareholder (e.g. France’s EDF and Italy’s Enel Green Power) operate as private investors in the equity shareholding of SPVs in renewable energy projects elsewhere. Such shareholders have in turn benefitted from the leverage provided by development finance institutions, operating within equity shareholdings.

Third and further to the methodological challenges discussed in the ‘Introduction’ section, this research has significant implications for a far more interdisciplinary methodology for energy transitions research in order to achieve a greater understanding of the reach and influence of electricity capital between global processes and territorial realities. Such methodology could firstly include detailed quantitative analyses to unpack the national and international flows of finance involved in renewable electricity generation as an evolving financial asset, as well as critical policy analysis to further investigate the politics of the negotiation of electricity regulation and procurement processes that ultimately enable these assets to develop. But far more can be done to link this elite-level focus with methods from political ecology and anthropology in order to acquire greater insights into the localised impacts of renewable energy development. Recent examples of such methods include Rignall (2015) and Boyer and Howe (2019). In theoretical and methodological terms, such an approach implies a much more significant dialogue between political economy and political ecology. Moreover, ethnographic methods, while a significant tool for research at the community level, could also be used in elite settings in order to elicit a greater understanding of the operations and priorities of investors, developers and the highly professionalised industry of mediators involved in setting and negotiating the terms of risk that determine who gains and who loses from the energy transition. The involved and long-term nature of such research cannot be overlooked or underestimated.

Finally, this research raises critical questions regarding the governance and regulation of finance and electricity at multiple scales and the extent to which capital can disciplined so that it can be effectively channelled to community empowerment and local socio-economic outcomes. Following Castree and Christophers (2015: 379), if the financial sector can be seen as ‘an unelected government whose power is such that it needs to be carefully governed through a set of endogenous and exogenous norms, rules and institutions’, then it follows that auctions are an incentive shaped by governments, technical assistance and investor interests that enable financiers to craft ‘investment vehicles to help decarbonise the world’s current infrastructural assets’ (Christophers, 2015: 379). As the examples of South Africa and Mexico have illustrated, national and sub-national institutions of government, particularly in LMICs do not always hold the bargaining power, the capacity or the willingness to radically implement and shape these frameworks of renewable energy procurement and conditions of project development in the face of powerful, renewable energy majors and institutions of transnational capital. This raises the question over how marginalised communities can influence and benefit from development that may affect them profoundly and otherwise serve to perpetuate their marginalisation. As the development of utility-scale renewable energy across the globe continues apace, such questions demand greater theoretical and empirical prominence in the research on energy transitions.

Highlights

Utility-scale renewable electricity generation is essential to decarbonisation yet limited critical academic thinking has been dedicated its ownership. Despite the pro-environmental outcomes of utility-scale renewable energy, it has often failed to include or benefit local communities. Electricity is a site of ‘struggle’ between technological change and established configurations of political, social and economic power. Renewable electricity is a rapidly emerging asset class, increasingly determined by the frameworks and logics of finance and investment Two competing objectives of renewable electricity are a long-term revenue stream for investors and a mechanism of socio-economic development.

Footnotes

Acknowledgements

Thank you to the three anonymous reviewers and Leila Harris, the editor of this journal who gave me really helpful advice and comments on how to improve the argument of this paper; Nikki Luke and Mat Huber for inviting me to submit to this special issue and participate in the panel stream on Geographies of Electricity Capital at the AAG in April 2019 which gave me critical intellectual inputs, encouragement and further impetus to develop my thoughts into a published piece; and the following people for all their advice and valuable inputs into my thinking on this issue: Shalanda Baker, Sergio Oceransky, Holle Wlokas, Sarah Knuth, Andrew Hook, Chantal Naidoo, Jesse Burton and Hilton Trollip.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Some of the field work for this paper was funded by a project approved by the German Ministry for Environment and The Energy Research Centre of the University of Cape Town (2015) and the China Africa Research Initiative at Johns Hopkins University’s School of Advanced International Studies (SAIS-CARI) (2016). Further support for the writing of this paper was provided by a generous fellowship from Maria Sibylla Merian Centres Programme of the Federal Ministry of Education and Research Germany under the grant number 01 UK1824A.