Abstract

Rental housing has been regarded as the new ‘frontier for financialisation’ since the 2007 financial crisis. But research examining financialisation of de-commodified rental housing is limited and is primarily focused on stock acquisitions by financial investors and the enabling role of either national or local governments. This critically overlooks the emergence of the financialised production of social rented housing, the interplay between levels of government (particularly with the regional level), and the leading role of the state in these processes. By combining a political sociology approach to policy instruments with a housing system studies perspective, the paper investigates how Italy, through the interplay between national, regional (Lombardy) and local (Milan) governments, led the financialisation of its social rented housing production. Through analyses of six decades of financial-legislative changes in the housing system regarding production/provision, finance and land supply, it identifies a three-stage journey towards financialisation: (1) the rise and fall of publicly-owned rental social housing (1950s to 1990s); (2) the regionalisation and marketisation of the sector up to the late 2000s; and (3) the upward transfer from the first local-scale experiment with the real estate mutual investment fund in Milan to the creation of a national-scale System of Funds for the production of social rented housing. The study shows that the re-commodification of housing and land initiated in the 1980s were intertwined and a conditio-sine-qua-non for financialisation; that the state played a crafting—rather than solely enabling—role in this process; and that trans-scalar legislative–financial innovations transformed social rented housing into a liquid asset class.

Introduction

Since 2010, Italy has been witnessing a return to the production of social rented housing (SRH hereafter) with 2.4 million sqm planned to be built by 2020 (FHS, 2016) and an unprecedented proliferation of private and non-profit SRH providers. Extensive SRH production and the involvement of the non-profit sector are not typical of familistic 1 welfare regimes and residualist housing systems such as the Italian one (Arbaci, 2019). Rather, it is a feature of universalist housing systems developed by social-democratic and corporatist welfare states (e.g., Scandinavian and Central European countries). Is this a path change in response to the housing affordability crisis?

We argue that this return to SRH production is not part of a system’s de-commodification process but the result of the state-led marketisation of the sector and the subsequent penetration of capital from the financial markets. This developed through a new financial infrastructure created by the national government called the ‘Integrated System of Funds’ (Sistema Integrato di Fondi, SIF hereafter). The SIF has channelled about 2.3 billion euros into the SRH sector since 2009, supported by legislative reconfigurations of housing and planning at local, regional and national levels. In fact, this process cannot be understood in isolation from the interplay with local/regional financial-legislative innovations introduced in Lombardy and Milan (the Italian financial centre), which have been fundamental for the development of this instrument and its national governance. The SIF is a fund of ‘real-estate mutual investment funds’ (REIMFs hereafter) that characterises the ‘Italian way’ to housing financialisation.

Despite the residualisation of the SRH sector, the Italian case represents a relevant example of financialisation of rental housing, since it sheds light on the unexplored financialising dynamics affecting production and its role within the new round of financialisation of de-commodified rental housing that emerged during the 2010s across Europe and the US with a shift in rental housing financialisation from predatory equity logics to long-term and less-risky investment strategies (Wijburg et al., 2018). Studies on financialisation have only recently broadened attention from owner-occupation/mortgage securitisation to rental sectors regarded as the new ‘frontier for financialisation’ after the 2007 financial crisis (Fields, 2017). But scholarship on the financialisation of de-commodified rental housing remains limited and is primarily focused on stock acquisitions/enhancement by financial investors, overlooking capital investment that fuels rental housing production and associated urban processes. Despite the emphasis on the role of the state in enabling housing financialisation (Aalbers, 2016), the role of its distinct institutional arrangements also requires further investigation. In particular, the analytical emphasis on either the local or national scale is dominant in existing literature and overshadows the interplay between scales and how different levels of government (particularly the neglected intermediate regional level) work in articulation to open up local real estate to financial markets.

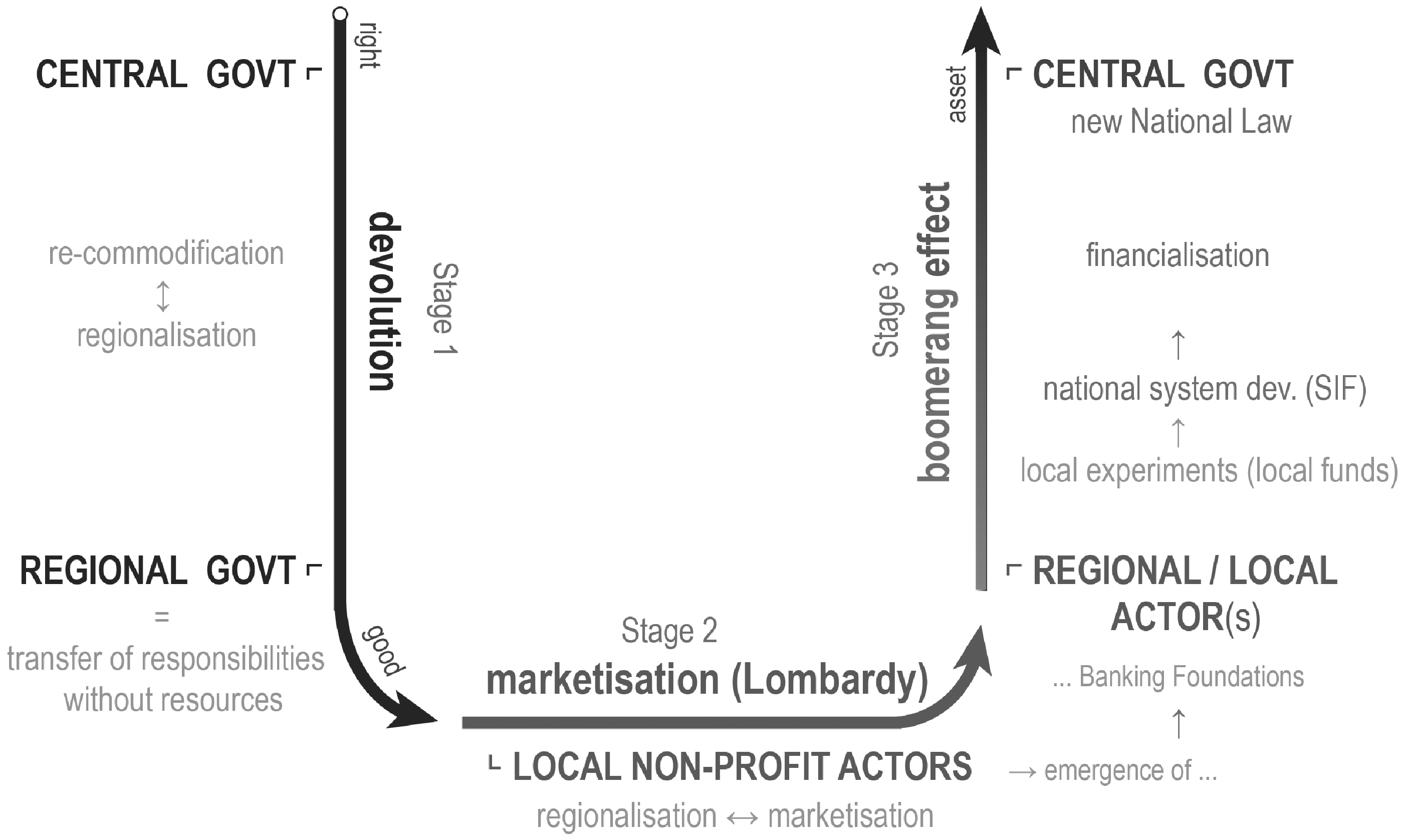

This paper aims to fill these gaps by investigating the evolution of the Italian SRH sector post-WWII to identify the mechanisms that paved the way to the financialisation of SRH production. Through analyses of changes at national, regional (Lombardy) and local levels (Milan) of (1) financial-legislative frameworks that transformed the housing system regarding (2) housing production/provision, (3) finance and (4) land supply, it identifies three key periods (Figure 1). Stage 1 (1950s–1990s) comprises the rise and fall of public SRH production with the devolution of housing responsibilities from national to regional governments. Stage 2 (1990s–2000s) entails a regionalisation process that accompanied the marketisation of the SRH sector, drawing on the Lombardy case. Stage 3 (early 2000s onwards) incorporates legislative–financial innovations that led to the financialisation of the SRH sector, first at the regional levels with the emergence of new financial actors (banking foundation) and then at the national level with the establishment of the SIF that resulted from what we describe as a ‘soft re-centralisation’ of financialised SRH production.

The findings of the paper contribute to three key debates. First, the trans-scalar journey towards the financialisation of SRH in Italy shows that re-commodification processes in housing and land, often studied separately, are intertwined and are the conditio-sine-qua-non for the housing financialisation that started in the 1980s. Moreover, the financialisation of land has been indispensable for a viable financialisation of SRH production and, hence, for a new round of financialisation of rental housing based on long-term/relatively low-risk investments. Second, in contrast with existing scholarship, the analysis demonstrates that the state across its different levels of government (including the regional one) has led, rather than simply enabled, the financialisation of SRH. Third, whilst the transformation of SRH into a liquid financial asset class has been acknowledged as the culmination of the financialisation process (as it connects local real estate to global financial markets), we argue that such a transformation, far from limited to the operations of finance, should be seen in relation to wider changes within institutional settings; that is, the multilevel, public–private governance action in distinct and apparently detached policy fields that contributes to liberate capital entrapped in rental housing from its spatial fixity.

The approach employed here departs from classic functionalist perspectives focused on explicit policy objectives. Using a political sociology approach to policy instruments (Lascoumes and Le Galès, 2009), it focuses on the implicit modes of regulation of technical instruments that constitute policy- and law-making processes altering the housing and land supply systems. This political sociology approach has been combined with an outlook stemming from comparative housing studies (Arbaci, 2019) that sees housing as a system weaving the supply (land, provision and production) with the tenure policy system, thus providing an innovative perspective on financialisation research. In this perspective, the particular focus on SRH, a key tenure that defines the universalist/residualist nature of a welfare regime/housing system, offers a crucial angle to investigate the state’s action within housing financialisation and the wider process of a housing system’s de/re-commodification.

The research thus mostly uses longitudinal policy analyses of national/regional legislation and regulations and local policies (reports, plans and private–public agreements), complemented with semi-structured interviews (fifty-seven during 2013–2018) with policymakers, housing providers, tenant unions and community groups as part of a broader research on the changing regional housing and planning/land-use systems in Lombardy. The paper focuses on the case of Lombardy and Milan not only because of their key roles in the development of the national-scale SIF but also because the financialisation of SRH was concentrated in the Northern Regions, where 73% of SIF investments and over 80% of new SRH units are located (CDP, 2014). Critically, neoliberalisation and financialisation in Italy are spatially uneven and unfolding primarily in these regions (Vettoretto, 2019).

The paper starts with a discussion of literature focused on the three debates relevant to this research on financialisation and the role of the state. The second section contextualises the Italian case and explores the three stages of the state-led financialisation of SRH in Italy. The conclusion reflects on and discusses the key findings and contributions of the study.

Three debates on the financialisation of rented housing

Scholarship on housing financialisation has focused mostly on owner occupation and mortgage securitisation (Aalbers, 2008; Gotham, 2009; Wainwright, 2009). Attention has only recently been paid to financialising dynamics affecting the rental housing sectors, especially after the 2007 financial crisis (Fields, 2017, 2018). Research initially brought to light acquisitions of former de-commodified rental stocks by private equity and hedge funds oriented towards short-term predatory equity in countries such as Germany, the UK and the USA (Bernt et al., 2017; Beswick et al., 2016; Fields and Uffer, 2014). But in the 2010s, new interest for mid-/long-term investment strategies emerged among real estate investment trusts/funds seeking less volatile income streams in rental housing, which Wijburg et al. (2018) called financialisation 2.0. Simultaneously, a small but no less important scholarship has started to examine the financialisation of de-commodified rental housing providers, such as housing associations in the Netherlands and in London (Aalbers et al., 2017; Wainwright and Manville, 2017). This paper joins these burgeoning scholarships by filling gaps in the SRH segment regarding both: (1) local/regional-scale studies addressing the transition from the first to the second round of rental housing financialisation, and (2) studies exploring the financialised production of new SRH stocks and its actors, rather than just acquisitions/enhancement of existing de-commodified stocks. In so doing, it embraces three major debates on housing financialisation.

First, the re-commodification–financialisation nexus in housing. The re-commodification of (European) housing systems—a shift in the conception of housing from a right to a good (individual commodity) and to an asset (financial commodity) entailing the state’s withdrawal from this welfare pillar and the transition towards marketised arrangements of the SRH sector — has been extensively explored since the 1990s (Kemeny, 1995; Lowe, 2011). This process has recently regained attention within the housing financialisation debate (Forrest and Hirayama, 2015; Rolnik, 2013) as part of the wider neoliberal turn in urban production (Pinson and Journel, 2016). Despite a consensus that housing re-commodification has created new markets for financial investors, the nexus between these two processes remains unclear and empirically under-investigated, in particular how their interplay led to profound changes in housing and land supply. The perspective from housing studies adopted in this paper can help to further this understanding as it relates the tenure policy system and the supply system (land, provision and production). Moreover, changes in the SRH sector offer a fundamental angle to examine this nexus between de/re-commodification and financialisation of the wider housing system since the redistributive degree of a housing system (along the universalism/residualism spectrum) largely depends on the scale of de-commodification of rental housing and its interplay with the other tenures (see Kemeny’s concept of unitary and dualist rental systems).

Second, the role of the state in housing financialisation. Research has shown that context-specific and evolving institutional arrangements (Lapavistas, 2013), as well as the nature/organisation of housing systems (Fernandez, 2016), are of critical importance in understanding the way financialisation unfolds in different countries. But comparative research has primarily been focused on the relationship between global financial markets and more or less permeable national housing systems (ibidem), while studies on the state’s role in the financialisation of housing/urban production has looked at either local governments (Beswick and Penny, 2018; Weber, 2010) or national ones (Wijburg, 2019). Single-scale analyses have thus provided important but partial insights into the phenomenon (see critique in French et al., 2011). Although scholars have acknowledged the crucial influence of trans-scalar processes of financial intermediation in urban production (Halbert and Attuyer, 2016), there is limited understanding of the role and interplay of different levels of government. Moreover, the state has mostly been seen as enabler/facilitator, and its crafting role in shaping financial infrastructures and instruments has been overlooked. By combining the analytical approach focused on policy instruments—tested recently in the study of the financialisation of urban production (Sanfelici and Halbert, 2019)—with a novel trans-scalar perspective, the paper innovatively explores the interplay and distribution of power among different levels of government (in particular, the ‘hinge function’ of neglected intermediate levels) and their intertwining roles, not just as mediators but as active participants in housing financialisation within specific national contexts. In so doing, it also adds to the debate on state financialisation, whereas the Italian case reflects the generalised post-Keynesian tendency of governments to practise ‘statecraft’ by relying on financial innovation (Lagna, 2016: 167).

Finally, the conceptualisation of how financialisation in urban production is enacted. Gotham (2009), building on Harvey’s (1985) work, identified the unlocking mechanism for solving the spatial fixity of capital invested in real estate as a culminating step in housing financialisation. However, while such a mechanism was examined in relation to homeownership mortgage securitisation, it remains almost unexplored in relation to rental housing. By reconstructing the trans-scalar journey that led to the financialisation of the Italian SRH sector, the paper contributes to a deeper understanding of how the ‘creation of liquidity out of spatial fixity’ (Gotham, 2009: 355) works in this segment by expanding on financialising instruments and infrastructures for mid-/long-term investments by real-estate investment funds/companies as well as on the structural preconditions that make SRH a liquid asset class.

A trans-scalar journey to the financialisation of the Italian SRH sector

As in other Southern-European familistic welfare states, the Italian housing system has fostered owner occupation as the predominant tenure, keeping the SRH sector small and residual within a dualist rental system. Recent data shows that over 71% of households own their homes, 18% are tenants (ISTAT, 2011), and less than 4% of the total housing stock is public SRH (Consiglio dei Ministri, 2009), which is half of the EU average (IZA et al., 2013).SRH here refers to fully or partially de-commodified rental accommodations (thus rents below market rates) for low- and middle-low income groups, mostly (co-)subsidised by the state with direct/indirect incentives and produced/promoted by local governments, regional public companies or, more recently, by non-profit and private actors. Eligibility criteria is means-tested on income, needs and medical conditions, but non-profit/private providers of quasi-market SRH can select tenants with incomes above those set by local government periodic ranking lists.

In the Italian housing system, the dominance of owner occupation is systemic and path dependent, a legacy of Catholic social policies that view (social) housing as a family rather than state responsibility and owner occupation as a key political-economic instrument to boost employment and economic growth, ensure political stability and provide a primary source of social protection for families (Allen et al., 2004).

This unbalance between owner occupation and rent has sharpened since housing re-commodification resumed in the 1980s. The private rental sector shrank due to the boost of homeownership through tax incentives combined with the drop in mortgage interest rates associated with the liberalisation of the credit market (Camera dei Deputati, 1999), while the abolition of rent control triggered over a 105% rent increase between the 1990s and the 2000s (Cittalia, 2010) and a staggering loss of affordable rental stock. SRH has also been significantly reduced due to the privatisation of public stock through the Right-to-Buy scheme and the national government’s withdrawal from public production (Mugnano, 2017). These changes are intertwined with the process of regionalisation and devolution of responsibilities for SRH provision to regional and local governments, which adopted different approaches to housing re-commodification.

The recent wave of large SRH production is, thus, atypical of the Italian familistic welfare regime. As we will show, rather than a de-commodification process, this stems from the financialisation of SRH production in Italy. The following analysis traces this three-stage ‘journey’ that starts with the decline of the public production/provision of SRH, followed by the marketisation of the sector at the regional level—a crucial shift towards the financialisation of SRH in Italy—and concludes with the creation of the SIF at the national level.

Stage 1: From centralisation to devolution: the rise-and-fall of housing de-commodification

The rise

SHR provision by the national government expanded significantly in post-WWII. Coupled with the strengthening of rent control and an increase in the public land bank, this expansion was part of a broader process of de-commodification of the Italian housing and land systems, echoing the path followed by the corporatist welfare states in Central Europe (e.g., Germany and France), though more residualist in scale and scope.

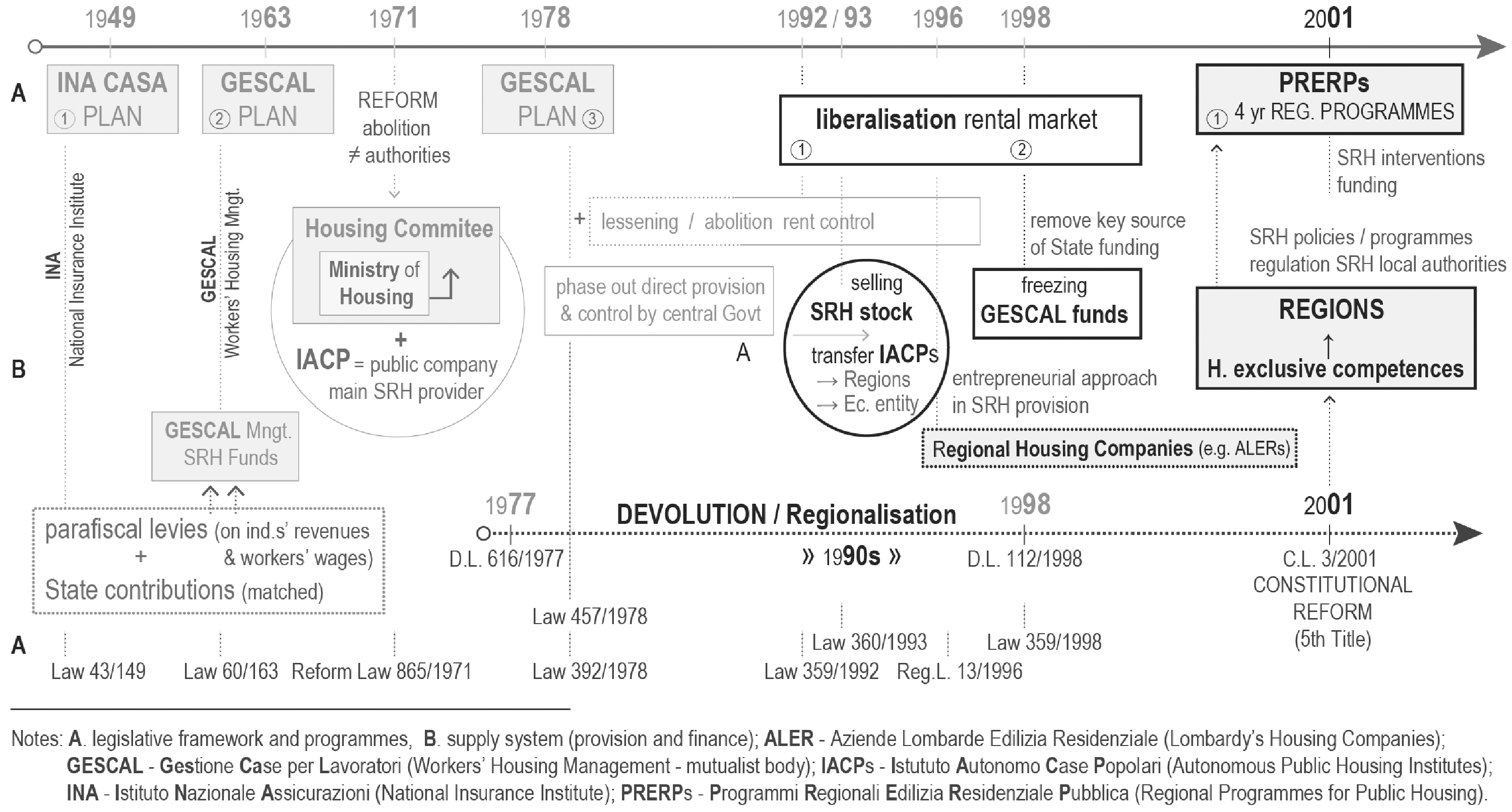

The centralisation of the planning and coordination of SRH provision by the national government was a gradual process, whose legislative path only came to an end in the early 1970s (Figure 2, left). First, the Law 865/1971 established the Residential Housing Committee, a coordination entity of Ministries with responsibilities in SRH policy. Next, the provision of SRH was concentrated under a single institutional body (IACP-Istituti Autonomi Case Popolari; Autonomous Public Housing Institutes) in order to abolish the multiplicity of public authorities operating in the sector (Minelli, 2004). This simplification process made IACPs the main local entities tasked with the production and management of SRH stock.

Trans-scalar periodisation of the re-commodification and financialisation of SRH since the 1980s.

Stage 1, evolution of legislative frameworks and SRH supply, 1950s–1990s.

Simultaneously, the national government took a lead in the provision and production of SRH. It established the National Insurance Institute for Home Management (Gestione INA-Casa, Istituto Nazionale Assicurazioni 2 ) which gave rise to the largest public intervention in the SRH sector (State Law 43/1949), with two national seven-year programmes (1949 and 1956). However, a more structured state action started in the 1960s, when a new institutional mutualist body for Workers’ Housing Management (GesCaL, Gestione Casa Lavoratori) replaced the INA-Casa management and introduced two ten-year programmes in 1963 (Law 60/1963) and 1978 (Law 457/1978) that completed this expansionary phase.

Both the centralisation of public finance and expansion of public land have been crucial in the housing de-commodification process. A dedicated GesCaL Fund was structured as a workers’ mutualist institution financed through para-fiscal levies on both employee salaries and employer paid wages. Although the fund aimed to deliver homes to blue-collar and key workers, its scope was progressively extended to other low-waged professional categories (though they did not contribute to the fund); in this way, this mutualist, corporatist institution de facto became the National government’s key tool for direct intervention in the SRH sector.

In the early 1960s, the national government also introduced a new master-planning instrument for local governments to earmark between 40% and 70% of any new residential development for SRH (Piani Edilizia Economica Popolare, Subsidised Public Housing Plans; Law 167/1962). This instrument thus enabled the expansion of SRH stock and, simultaneously, promoted a process of de-commodification of land by eminent domain (compulsory purchasing of private land below market price) that contributed to the broader expansion of the public land bank.

The fall

This expansionist period ended in the late 1980s. Public disinvestment in the SRH sector went hand-in-hand with a broader re-commodification of the housing system, initiated in the late1970s with the lessening of rent control (Law 392/1978; Allen et al., 2004) and later amplified by the devolution of housing responsibilities to regional governments. These processes reflected the incremental withdrawal of the national government from the housing system as a whole.

The expansion of SRH was halted and the national government withdrew from public production and funding following the phase of industrial restructuring of the 1980s and the subsequent fiscal crisis (Figure 2, right). Two main measures accelerated the disinvestment and shrinking of the sector: the progressive freeze of the GesCaL Fund and the introduction of the Right-to-Buy scheme (Law 560/1993). This phase of decline was associated with the devolution of responsibilities to regional governments regarding the SRH stock and the regulation of local IACPs. Although the regionalisation of the SRH sector was ‘set in stone’ in the 2000s (Constitutional Law 3/2001), it began in the late-1970s (Decree Law 616/1977) and received a crucial impulse during the 1990s (Decree Law 112/1998).

The decline of the public production of SRH and its residualisation was part of, and a driver for, the wider recommodification of the housing system since the 1980s. While market rent prices started to rise (Cittalia, 2010) after the abolition of rent control (Law 359/1992; Law 431/1998), the Right-to-Buy scheme substantially reduced the size of SRH stock and its weight within the overall rental sector from its inception in 1993. This dynamic is deep-seated in the longstanding political project to promote owner occupation, characteristic of the Italian housing system. The sale of more than 120,000 SRH homes in the first ten years (Consiglio dei Ministri, 2009) was instrumental to the national increase in mortgage-driven owner occupation, a process supported through the mortgage tax deduction for primary residency and the liberalisation of the credit market (and inherent lowering of interest rates; Camera dei Deputati, 1999).

Meanwhile, the gradual freeze of the GesCaL Fund—with the halt of social security contributions to the fund in 1998—removed the key source of public funding for SRH production. The national government instead allocated gradually decreasing funding for local urban regeneration programmes for the refurbishment of the SRH stock and restructuring of the sector (Cremaschi, 2001; Ombuen et al., 2000). These urban programmes—under the coordination of wider regional plans, such as the Regional Programme for Public Housing (PRERPs, Programmi Regionali Edilizia Residenziale Pubblica) in Lombardy—concluded the expansionist phase of the SRH, including public land acquisitions by eminent domain.

The halt in the state’s direct provision, production and funding of SRH coincided with the unfolding of a broader process of divestiture, leasing and financial valuation of public property/land assets especially from the defence sector (Artioli, 2016; Ponzini and Vani, 2012), triggered by complex and discontinuous law-making processes that started in the 1980s (Gastaldi, 2015) and involved the creation of the state’s Asset Management Agency (Agenzia del Demanio) in 1999.

Stage 2: From the regionalisation of housing policy to the marketisation of SRH

Regionalisation

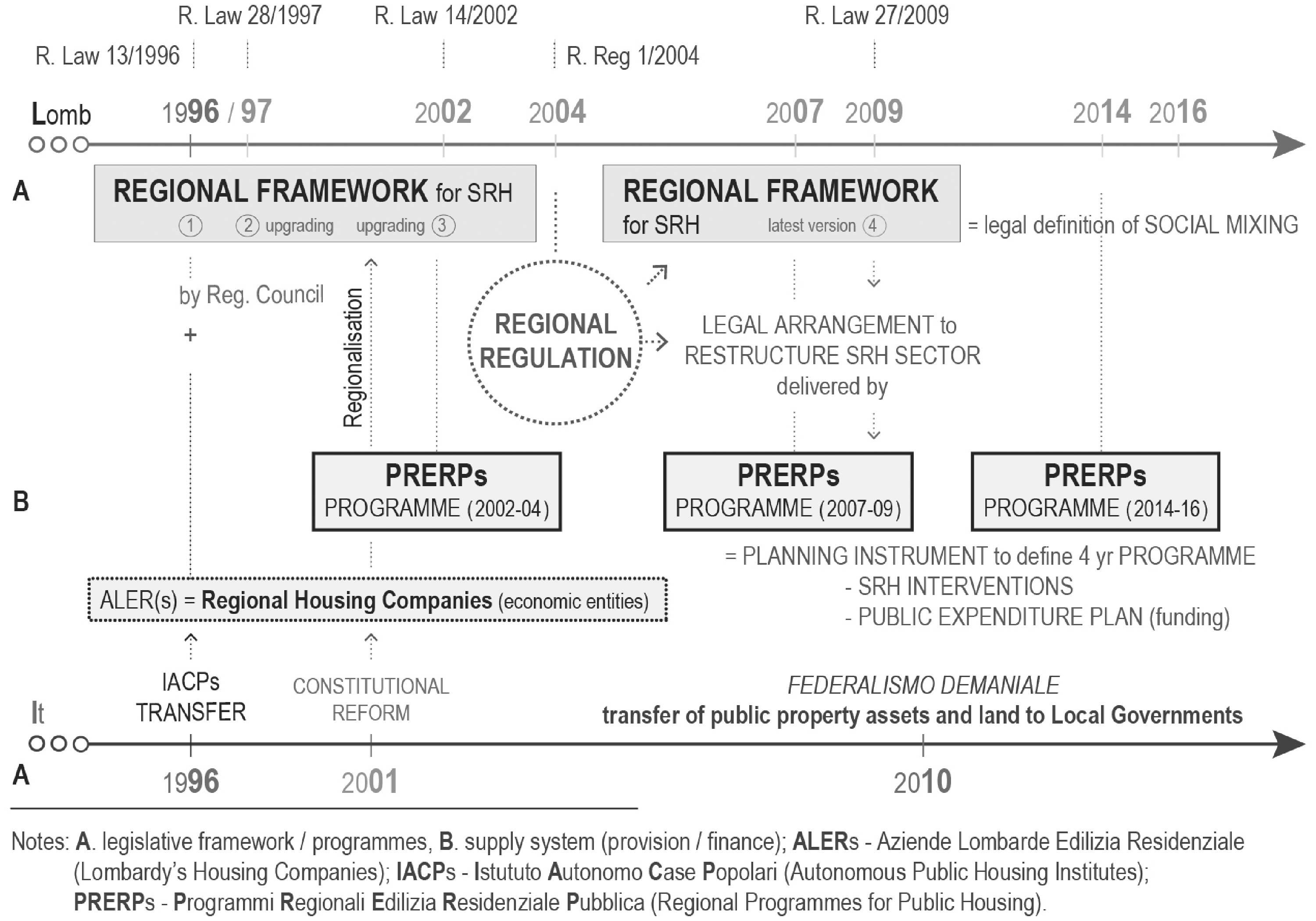

Parallel to the regionalisation of Italian social policies (Kazepov, 2009), the devolution process required regional governments to define their legislative frameworks and paths for the re-commodification of their SRH sectors. But following Italy’s fiscal crisis throughout the 1980s and the end of the expansionary phase of the welfare state, the regionalisation of SRH policy and of the planning system was characterised by a ‘devolution without resources’ which brought about a progressive, yet regionally uneven, marketisation of the sector. Among those regions that opened the SRH supply to private and non-profit providers, Lombardy pursued the strongest marketisation of the SRH sector.

In Lombardy (Figure 3, left), the law-making process leading up to the regionalisation of SRH policy started in 1996 (Regional Law 13/1996) and resulted in a comprehensive legislation in 2009 (Regional Law 27/2009). SRH became a ‘service of general interest’, according to the legislative definition by the national government (Article 1 of Ministerial Decree 22/04/2008) and consistent with the European Economic Community Treaty on state aids. Two aspects of this definition were crucial for the marketisation of the sector: (a) SRH can be equally provided by the public and private sector (including non-profit providers); and (b) SRH was turned into a ‘planning standard’ entailing prescriptive planning contributions in the form of land or residential units. In most of the cases analysed, however, these contributions have been re-arranged through public–private negotiations, weakening their statutory nature in favour of a more flexible system.

Stage 2, evolution of legislative frameworks and SRH supply, 1990s–2010s.

This legislative transition led to the increasing involvement of new providers from both the private and non-profit sector responsible for the production and management of SRH. Within the regional framework of PRERPs, urban regeneration programmes acted as laboratories to experiment with public–private partnerships and shaped the governance of the SRH sector at the local scale. Local governments played a key role in crafting public–private governance settings: in this experimental phase, they acted as SRH providers and offered a variety of incentives—in particular the free allocation of public land as leverage—to attract private investments into the SRH production.

The three PRERPs that developed from 2002 to 2016 collectively saw a drastic reduction of national government funding from around 1.2 billion to less than 0.15 billion (Regione Lombardia, 2014). Up until 2011, the Regional government introduced within this framework a transitional co-funding scheme to boost SRH production, in which regional subsidies matched provider investments according to the tenure-mixing arrangements of new developments. The residualisation of national government funding was intended to attract private investments into the local SRH sector and thus replace public funding with financial resources emerging from market dynamics.

Crucial to the substitution of public funding with private investments was the fact that the regionalisation of the SRH sector developed alongside the regionalisation of the planning system, which led in Lombardy to a broader re-commodification of the land system. Since the mid-2000s, the regional legislative framework (Regional Law 12/2005)—which introduced the new definition of SRH as a ‘planning standard’—replaced the old regulatory approach to land-use planning with a more flexible, negotiation-based and growth-oriented system. Confronted with the erosion of public funding for the SRH sector, local governments were pushed to engage in public–private negotiations to boost SRH production. Local governments had to rely on (a) planning gains that required developers to transfer shares of the new stock to local governments for SRH purposes in exchange for planning permissions or (b) free transfer or free lease of public land as incentives to support SRH providers. SRH production became conditional on urban growth.

In this context, the mobilisation of public land (as undeveloped plots, brownfield sites or disused properties) became ‘the’ public leverage for local governments to lead public–private negotiations in the SRH sector and promote urban growth in general. It was part of the re-commodification of public shares of property/land assets initiated in the 1980s and accelerated under the increasing pressure of EU restrictions on national public-debt management (and consequent budgetary constraints for local governments; Besussi, 2016). This process of divestiture and land re-commodification expanded during the 1990s and the 2000s with the creation of new financialising instruments for the financial valuation and sale of public property/land assets at the national level, such as REIMFs (Law 86/1994; Law 503/1995; Decree Law 58/1998) and ‘special purpose vehicles’ for the securitisation of public property/land assets (Decree Law 351/2001; Law 296/2006).

As shown later, the ongoing reorganisation of the planning and land systems that began in the 1990s was fundamental for creating the conditions for the financialisation of housing; initiated by the national government, it was de facto operationalised through regional legislation. Furthermore, in the aftermath of the financial crisis, the introduction of the Valuation and Sale Plan (Piano di Valorizzazione e Alienazione Immobiliare; Decree Law 112/2008) expedited the selling of public property/land assets by local governments to meet the imposed budgetary constraints.

Marketisation

According to the new legislative definition of SRH, Lombardy’s legislation established a variety of quasi-market rental contracts as alternatives to the traditional, subsidised rental contract for publicly owned SRH (Figure 3, right). These new quasi-market contracts were intended to target middle-class groups, commonly not entitled to publicly owned SRH but unable to afford market rents. They were presented as a tool for social-mixing programmes (Regional Regulation 1/2004; Belotti, 2017); however, according to legislative requirements of financial sustainability, social and functional mixing became a rhetoric discourse (Bricocoli and Cucca, 2016) to legitimise social-engineering arrangements that aggregated groups and services/functions with different solvency capacities aimed to secure the financial viability of SRH.In this quasi-market setting, SRH was transformed into a viable asset. In May 2016, the Director of Lombardy General Directorate for Housing confirmed the use of social-mixing programmes as an instrument to increase the financial viability of new SRH developments: ‘When you make investments—which do not regard publicly-owned housing, to be clear—the provision of diversified rental contracts that target different groups becomes a viability condition for long-term investments. I mean “diversified” not just with reference to groups, but also regarding mix of functions that are part of the investment. When you implement a residential development, the new accommodations are intended for different tenancies: from student to temporary housing, from quasi-market rental contracts to a minimal share (at most 10-15%) of subsidised rental contracts for publicly owned SRH, and including housing-related functions that make your investment viable. […]. This is what I gathered from these initiatives; Cenni di Cambiamento, Borgo Sostenibile and other SRH developments seem to me designed in this way.’

3

Against this background, for the first time, capital from the credit market started to flow into the SRH sector. Boosted by the regional transitional co-funding scheme, SRH providers significantly increased their propensity to act as risk-taking investors in order to compensate for the gradual withdrawal of public funding (Belotti, 2017). Especially non-profit actors often had to rely on bank loans to co-finance the remaining share of construction costs, thus experiencing unprecedented levels of indebtedness. Since the 2000s, in Milan, ALER went far beyond by developing a high-risk debt-led investment strategy; it created an arms-length real estate investment company, which borrowed over 145 million euros to finance failed investments in land acquisition and property development that jeopardised its financial stability (Regione Lombardia, 2015). In July 2016, a Regional Councillor and member of the Inquire Committee on ALER’s insolvency in Milan, emphasised the ease with which ALER borrowed several million euros to co-finance regeneration programmes and new SRH developments in Milan (boosted by the regional co-funding scheme), while relying on derivative products and creating a new financial arms-length real-estate investment company. ‘In most cases, loans were taken out, let’s say, to get the state’s funding to co-finance ALER’s interventions in different neighbourhoods. […]. But that’s only part of it! For instance, what I discovered as a member of the Inquire Committee […] is that a thirty-million bank loan has been taken out to create ALER’s pension fund. This happened in 2011’.

Stage 3: The ‘upward transfer’: from local experiment(s) in Lombardy to the financialisation of the Italian SRH sector

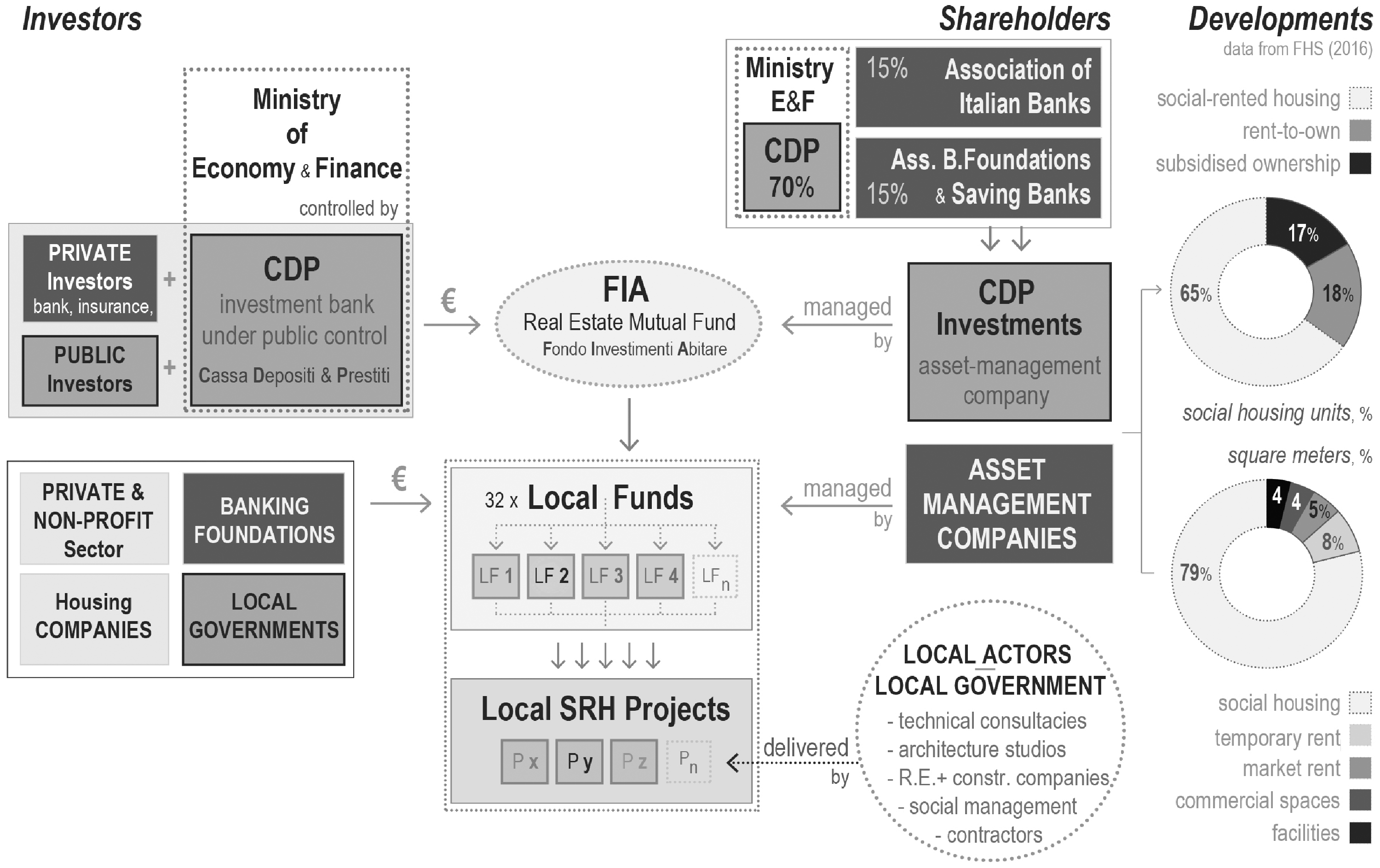

After the national government’s withdrawal from funding SRH production and the transfer of legislative responsibilities to regional governments, local public and non-profit actors in Lombardy and other northern regions undertook tasks of SRH production/provision under a new marketised and debt-driven framework, with local governments playing a new role of mobilisation and coordination. Against the backdrop of this ‘downward transfer’ from the national to the regional/local levels, an experimentation of REIMF for the production of SRH took place in Milan. These local financial innovations, in turn, inspired a national law-making process that led to the implementation of the SIF across Italian regions, a financial initiative coordinated by the national government-controlled bank Cassa Depositi Prestiti (CDP hereafter). This return to the scene of the national government to foster the financialised production of SRH nationwide represented a trans-scalar ‘upward transfer’ of the decision-making and infrastructure design process.

Local experiment(s)

During the marketisation of the SRH sector in Lombardy, Milan became the testing ground of new public–private governance and housing finance arrangements. Both were tested in two local pilot developments that opened the sector to financial markets with the creation of a pioneering financialising instrument. This experimental phase laid the ground for the financialisation of the Italian SRH sector.

Stage 3, evolution of legislative frameworks and SRH supply, 2000s–2010s.

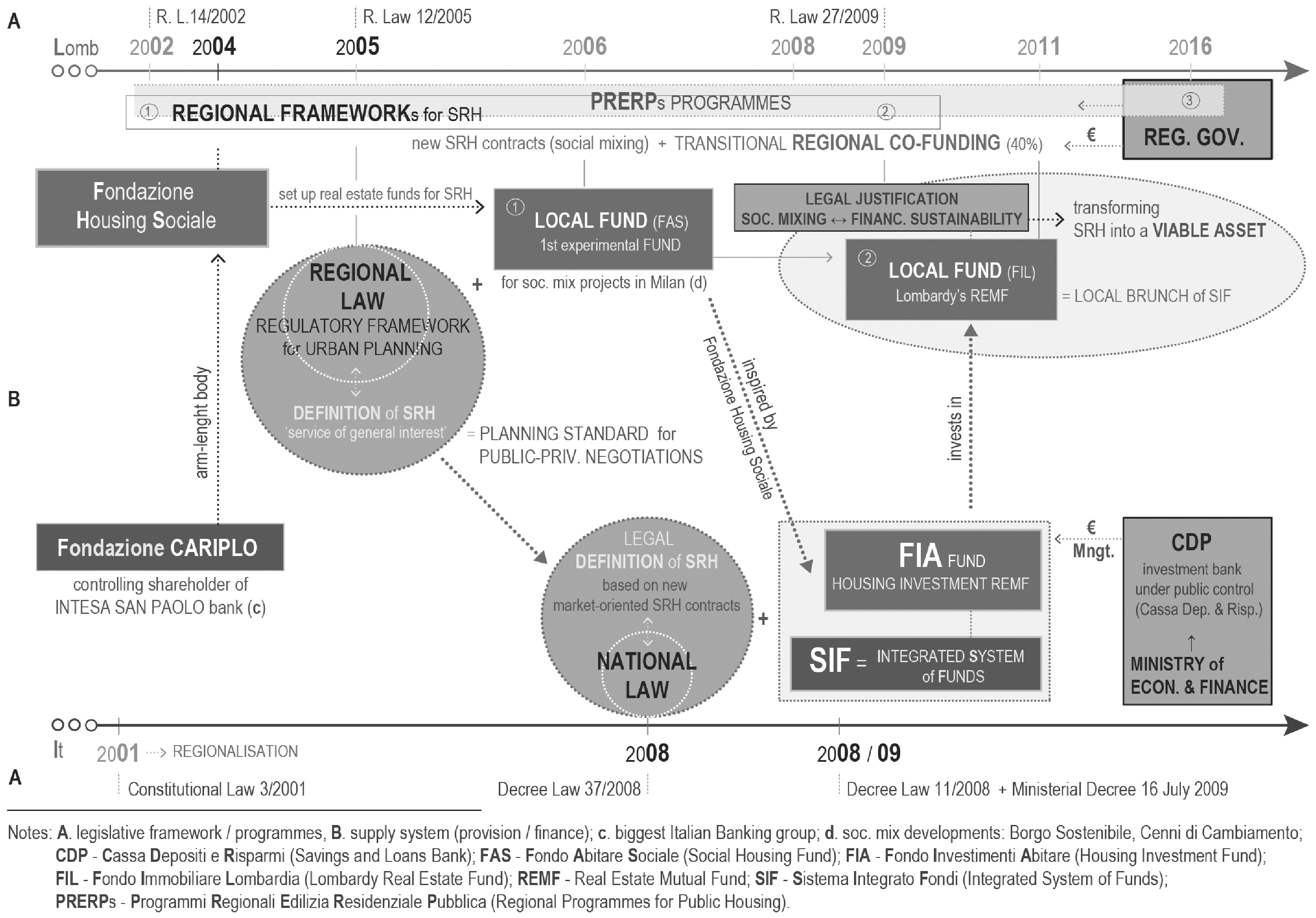

Owing to Lombardy’s regional planning legislation and the re-definition of SRH set in the mid-2000s, Milan’s local government unlocked forty-six plots of public land for ‘services of general interest’ (Communal Deliberation 26/2005) as part of a large-scale local plan for SRH production and renewal (Figure 4, left). The local plan became ‘the’ public leverage, within the scope of the PRERPs, to mobilise new non-profit actors, experiment with public–private partnerships and promote new financial solutions for the SRH sector at the local level. In July 2016, Milan’s head of the Housing Department explained the impact of the regional definition of SRH that anticipated its legislative definition at the national level: ‘What did the former Regional Head of Housing Department and the former Local Head of Housing Department invent? Building on Article 9, Comma 1, of the Regional Law 12/2005 […], they said: SRH should be a “service of general interest”. […] Dear Local governments, that “basket of functions” regarding SRH is thus a “service for the city”; you can now implement SRH on plots of land formerly allocated for public green areas, thus becoming a planning standard. […]. We are saying that the City Council will promote new SRH, not by economic contribution, but by “land contribution.”’

In 2005, Milan’s local government signed a protocol agreement with the Fondazione Housing Sociale to develop new SRH stock financed through a new ‘real-estate ethical fund’ (Fondo Abitare Sociale), an experimental financial instrument that anticipated the SIF. Further policy resolutions (Communal Deliberation 22/2008; Managerial Determination 69/2008; Managerial Determination 114/2008) formalised a free ninety-year land lease of three public plots to Polaris, the asset management company of the fund and a 48% subsidiary of Fondazione Cariplo. During the 2010s, Polaris financed and developed the first two pilot projects in Milan (Cenni di Cambiamento and Borgo Sostenibile that included about 450 SRH units), the testing ground of these pioneering legislative–financial arrangements.

The financialisation of SRH in Italy

The local experiments led by Fondazione Housing Sociale, regarded as a success story, inspired the national government to introduce a new legislative framework (Decree Law 112/2008; Ministerial Decree July 16th 2009) for the establishment of the SIF, a closed-end fund of funds dedicated to attract capital from financial markets for the provision/production of SRH across Italy (Figure 4, right). The financialisation of the SRH sector thus resulted from the intersection of financial and legislative competences provided at different scales by financial actors and the state. Moreover, it embodied a trans-scalar shift from a local-scale experiment to a national-scale law-making process, whereby the banking foundation acquired significant influence in shaping the national legislative framework (ACRI, 2018; Ferri and Rizzica, 2016). In March 2017, a manager of Fondazione Housing Sociale explained the role of these pilot projects. ‘The Decree Law 12/2008, which included both the definition of SRH and the know-how about real-estate ethical funds, draws upon the governance experiment led by the Lombardy Regional government. So, the law comes before the single project. But, it is true that these projects had already been put forward, international competitions of ideas launched, and the machine was already in motion prior the law: these are concrete signs to what otherwise would have been just a debate on procedures and funding scheme.’

The structure of the SIF.

In 2011, CDP provided the first stimulus to the SIF: its initial capital injection in the first closing (one billion euros) opened the door to inward investments from financial markets, whereby banks and insurance groups contributed with additional capital after the second closing (about 44% of a total of 2.28 billion euros in subscriptions (MIT, 2015). Capital from global financial markets, for the first time, flowed into the Italian SRH sector.

The SIF transformed SRH into a new liquid asset class. Institutional investors invested into REIMFs as financial products (that is, an investee per se) on the exclusive base of their investment portfolio, net asset value and rating risk. Investments were no longer funnelled into a concrete localised SRH development with specific features; instead, they flowed into the SIF as an abstract de-spatialised source of mid- or long-term financial returns per se, which promised annual target yields of about 3% above the Italian National Statistics Institute’s consumer price index. In contrast to traditional credit schemes or investments to finance urban production, capital invested in REIMFs, although equally blocked for a fixed time and non-rescindable, is, however, always transferable to third parties and, as such, liquid.

The implementation of the SIF and penetration of financial flows into the sector also paved the way to a large private acquisition of land by the REIMFs for SRH, including the intake of real estate developments under construction from companies going bankrupt. This suggests the emergence of financialising dynamics affecting land provision in combination with the financialisation of the SRH sector.

Interestingly, these dynamics blossomed since 2011 in parallel with the rapid succession of several austerity measures (Gastaldi, 2015; Gastaldi and Camerin, 2014), that sped up the broader divestiture of public property/land assets initiated in the 1980s. As a result, the process of re-commodification of land intensified in scale and pace, while opening the door to capital flows. This intensive law-making process was entwined with the so-called federalismo demaniale, the transfer of state owned property assets—especially from the defence sector—to local governments (Decree Law 86/2010; National Law 98/2013), thus furthering the mobilisation and sale of local public property/land assets to meet budgetary constraints and attract capital into local real estate sectors (including SRH) to promote urban growth. In May 2016, Milan’s Head of the Planning Department described how this mechanism worked in Milan during the initial implementation of the new planning legislative framework in the 2010s (Regional Law 12/2005): ‘If you look at the new Milan Plan, there are areas of urban transformation that concern military sites, industrial brownfields and railyards. […] The building index in these areas is 35% for real estate market—which, because of the “functional non-differentiation”, can be any type of function—and 35% for SRH. Out of the three large military sites that are now “starting” as areas of urban transformation, one has been bought by the CDP (Caserma Mameli), another one by the Ministry of Finance’s REIMF (Caserma di Baggio). So, in short, their investments have to meet this type of regulatory arrangements.’

This dynamic indicates that the trans-scalar shift in SRH financialisation has been intertwined with an analogous trans-scalar shift in the financialisation of land. In both domains, although with new guises and under a new marketised paradigm, the national government re-asserted its legislative capacity and, albeit indirectly, its functions of coordination and financial stimulus, playing a leading role in the transformation of SRH into a liquid asset class. ‘soft re-centralisation’ dynamics were thus crucial for the expansion of the financialisation of housing.

Conclusion

The paper traces changes in the Italian housing system that underpinned the transformation of SHR from right to good and ultimately to liquid asset. It identifies three key stages of this journey and unpacks the changes in legislative/policy frameworks, housing production/provision, finance and land supply that paved the way to financialisation. Critical in this process was the interplay among levels of government and, specifically, what we have described as a ‘soft re-centralisation’ of financialised SRH production. The findings offer a number of contributions to three debates on the financialisation of housing.

First, the research advances the understanding of the housing re-commodification–financialisation nexus. It shows that re-commodification was a conditio-sine-qua-non to housing financialisation. Both the national government’s withdrawal from the sector and the marketisation process at a regional scale were preconditions to making SRH a financial asset class. Critical to this process was the concurrent re-commodification of land supply, in particular through the halt in land purchasing by local governments, the regional re-commodification of the planning system, and the national law-making process for the divestiture and financial mobilisation of public property/land assets. Although the transformation of land into a liquid financial asset has been examined in the case of Milan (Kaika and Ruggiero, 2016; Savini and Aalbers, 2016), the crucial relationship between housing and land financialisation has been overlooked by existing literature which tends to treat the two spheres separately. As this paper shows, it was the mutually constitutive relationship between housing and land re-commodification that paved the way to housing financialisation, and (public) land was a crucial lever to attract global financial investments into SRH. This relationship was also fundamental in the new round of rental housing financialisation (Wijburg et al., 2018), since the shift towards a flexible land-use regime and the mobilisation of the state’s land/property assets were indispensable in guaranteeing the prospects for steady income streams from the financialised production of SRH and, then, for the financialisation of the overall rental sector.

The analysis of the re-commodification–financialisation nexus in the Italian case challenges the view that financialisation of rental housing emerged as a response to the global financial crisis (Fields, 2018). Rather, the financialisation of former de-commodified rental housing and the new interest for mid- and long-term investment strategies (as in the case of the SIF) must be seen against the backdrop of changes in the Italian residualist housing and land systems that started before the global financial crisis and evolved through it and independently from it. Also, far from expressing an interest broadening from owner-occupation to rental housing, it indicates a growing pervasiveness of finance that expands in scope and scale within the whole housing system, a critical sphere for capital accumulation in capitalist societies. A question warranting further research is whether and how the re-commodification–financialisation nexus plays out in universalist housing systems such as those of the social-democratic and corporatist welfare states of Central and Northern Europe.

Second, the research further reframes the state’s role in housing financialisation. Whilst the state’s crucial presence behind financialising dynamics in European countries’ housing systems has already been acknowledged (Aalbers, 2016), it is mostly seen as an enabler of financialisation. This research exposes the state’s persistent centrality in crafting the financialisation of SRH, which can arguably be considered as a form of state-led financialisation.

This could only be revealed by a trans-scalar research approach that disentangled the multilevel architecture of the state. Although the national government withdrew from SRH production/provision, the state did not lessen its control on the sector. In Lombardy, regional and local governments continued to steer SRH production/provision within a new marketised framework and created the financial–legislative conditions to turn SRH into a viable asset class. Moreover, beyond recognising the active role of local governments in boosting housing financialisation—in line with Beswick and Penny’s (2018) research on London boroughs—and revealing the hinge function of the regional level (overlooked in the literature), the analysis exposed the persistent hierarchical prominence of the national government. Despite the influence of the banking foundation on (the law-making process underpinning) the SIF, it was the national government that led the development of such financial infrastructure, crafted the legislative frame for SRH production/provision, and (albeit indirectly) channelled financial resources towards SRH through the national government controlled bank (CDP).

Importantly, SHR financialisation was crafted through a non-linear and complex interplay among levels of government. Although the ‘devolution without resources’ from the national to regional governments (downward transfer) paved the way to the marketisation of SHR and local/regional financial–legislative experiments in Lombardy and Milan, these in turn influenced the national government’s development of the SIF (upward transfer). This ‘soft re-centralisation’ effectively gave the national government the capacity to steer global capital flows penetrating local real estate, contradicting the dominant assumption of its hollowing out. Devolution in SRH policy was not a deregulation process, but a re-regulation process characterised by a transformation/re-distribution of regulative powers.

Finally, the research expands the understanding of how capital invested into rental housing is liberated from its ‘spatial fixity’ (Gotham, 2009). Distinguishing between financing mechanisms and financialising dynamics is paramount for conceptualising housing financialisation. The involvement of financing instruments—such as public funds (e.g., GesCaL Fund) or bank loans to finance SRH production—does not per se indicate financialising dynamics. These require specific conditions and instruments that make SRH a liquid asset, overcoming the spatial immobility of capital invested in rental housing. The SIF played a key role in ensuring these conditions by packaging pools of new SRH developments into REIMFs. Financial investors conceive REIMFs as sources of measurable yields regardless of each localised SRH development’s features; ‘magic boxes’ where capital can be invested to benefit from a stable annual income stream with maximised return after a fixed time.

This financialising mechanism, however, cannot be reduced solely to a financial device. Given the aspatial nature of REIMFs, both stable local governance and the state’s guarantees are crucial for investors’ confidence and investment viability. Moreover, a wider mobilisation of ‘backing’ policy instruments is required. In Lombardy, for example, social-mixing policies were key in aggregating socioeconomic groups with different solvency capacities acting as a social-engineering device to mitigate investment risk. Understanding financial intermediation thus requires refining the policy instrument approach recently employed to examine the financialisation of urban production (Sanfelici and Halbert, 2019) by looking beyond the mere action of financial policy instruments to unpack their interplay with other policy fields, apparently tangent but de facto implicated in financialisation. The point here is not solely to stress the importance of public policies as preconditions for financialisation (Bernt et al., 2017) but to recognise their enduring functional role for financial extraction.

Footnotes

Acknowledgements

The authors are grateful to the interviewees, and to Dr Juliana Martins, the City Governance and Planning Research Group (Bartlett School of Planning) and the anonymous reviewers for their invaluable comments.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.