Abstract

An innovative approach to mitigating climate change beyond the international negotiations and hard-law approaches is governing by disclosure – the acquisition and dissemination of information to influence the behavior of particular actors. This paper analyzes the institutionalization of carbon disclosure as an organizational field, focusing in particular on the role of governance entrepreneurs in this process. The emergence of carbon disclosure is scrutinized along four distinct stages of transnational institutionalization: start-up; competition and growth; convergence and consolidation; integration into international public policy. For each phase, the role and relevance of governance entrepreneurs is analyzed. The article finds that during the first stage, entrepreneurs mainly acts as innovators and “out-of-the-box” thinkers; in stage 2, entrepreneurs can be characterized as flexible adaptors and opportunity seekers, while in stage 3, the role of meta-governors in dominant. Finally, the last stage, entrepreneurs acts as connectors and bridge-builder between the transnational sphere of carbon disclosure and the wider international governance arena.

Keywords

Introduction

The international community is not on track to meet its global climate change mitigation targets. The emissions gap between the greenhouse gases (GHG) reduction pledges made by countries party to the United Nations Framework Convention on Climate Change (UNFCCC), the nationally determined contributions (NDCs) under the Paris Agreement, and the emissions pathway necessary to limit climate change within the range of 2℃ above pre-industrial levels is widening (UNEP, 2016). Acknowledging the need to close this ambition gap, scholars and practitioners are discussing additional and alternative measures beyond national mitigation policies. In this context, one of the most innovative approaches to mitigating climate change beyond the international negotiations and hard-law approaches is governing by disclosure – the acquisition and dissemination of information to influence the behavior of particular actors in a desired direction (Gupta, 2010). The idea of disclosure in the area of global environmental governance has developed from its beginnings as generic environmental disclosure to its current application to the field of climate change in the form of carbon disclosure. In this process, an organizational field has emerged in which organizations fulfil partially overlapping, partially complementary functions.

Research analyzing the overall governance architecture of climate change has to date mainly utilized structural explanations for the emergence and dynamics of institutionalization (Abbott et al., 2016; Biermann et al., 2009; Keohane and Victor, 2011). Abbott et al. (2016) apply an organizational ecology perspective to analyze the proliferation of private transnational regulatory organizations in the climate governance field. In contrast, this article analyzes the institutionalization of climate change disclosure as an organizational field from the perspective of governance entrepreneurs and entrepreneurship. The guiding question is: how does the role and relevance of governance entrepreneurship change from phase to phase in the institutionalization process? The empirical focus is on carbon disclosure and accounting as a sub-domain of climate change governance. The envisaged contribution of this article is two-fold: first, the article introduces a novel heuristic model of transnational institutionalization along four stages that could help to better understand the emergence and development of organizational fields. And second, the article suggests widening the application of the policy entrepreneur concept to the field of governance, analyzing the role of governance entrepreneurs (both individual and organizational) in innovating governance along the four-stage model of institutionalization.

I proceed as follows: 1 section ‘Analytical framework: Governance entrepreneurs and the four stages of transnational institutionalization’ sets out to discuss the concept of governance entrepreneurs/entrepreneurship and introduces a model of transnational institutionalization along 4 distinct stages. Section ‘The institutionalization of carbon disclosure’ introduces the empirical domain of carbon disclosure before it engages with an analysis of the institutionalization process and organizational field dynamics across all fours stages with reference to a number of empirical examples, including the US-based non-governmental organization CERES (Coalition for Environmentally Responsible Economies), the GHG Protocol, CDP (formerly the Carbon Disclosure Project), the Investor Network on Climate Risk (INCR), the Global Reporting Initiative (GRI), the Carbon Disclosure Standards Board (CDSB) and the UN Principles for Sustainable Investment (PRI), highlighting in particular the role of governance entrepreneurs and entrepreneurship in each stage. Section ‘Conclusions: The role of governance entrepreneurs in institutionalizing transnational governance’ concludes with a reflection on the lessons learned and future research in this field.

Analytical framework: Governance entrepreneurs and the four stages of transnational institutionalization

This section engages with conceptual and definitional issues concerning governance entrepreneurs/entrepreneurship and introduces a model of transnational institutionalization along four distinct stages.

Policy change has frequently been explained by highlighting the key role specific advocates of change, referred to in the literature as policy entrepreneurs (as an equivalent to entrepreneurs in the business world). In the words of Mintrom and Norman (2009: 650), ‘Policy entrepreneurs distinguish themselves through their desire to significantly change current ways of doing things in their area of interest’. This definition can easily be broadened to include innovations that cannot narrowly be conceived as public policies, but belong to the wider set of governance mechanisms (Jordan and Huitema, 2014). Organizational field theory (discussed above) has also identified the key role of entrepreneurial actors and behavior, i.e. institutional entrepreneurs and entrepreneurship, in changing organizations and organizational fields (see e.g. Greenwood and Suddaby, 2006; Lawrence and Phillips, 2004). In the words of Waldron and colleagues (Waldron et al., 2015: 132): ‘Institutional entrepreneurs are actors who create new or transform established institutions in ways that diverge from the status quo.’ Taking these definitions into account but going beyond them, I suggest using the term governance entrepreneur to denote those individuals, groups of individuals and organizations that meet the above descriptions but aim at changing governance rather than policies or institutions (narrowly understood as public regulations and rule systems). The term governance entrepreneur is different from the concept of policy entrepreneur in the following ways: first, governance is a broader field of activity, providing consequently a broader space for entrepreneurial activities; second, actors in governance are more diverse, and consequently, governance entrepreneurs are often from fields beyond public policy; third, innovation in the field of governance might be harder to evaluate due to the often soft nature of private initiatives. While these differences exist, I argue that sufficient similarities remain that enable the analyst to utilize the entrepreneurship concept to learn about governance innovation and institutional change. 2

In the introduction to this special issue, Boasson and Huitema (2017) introduce two key characteristics of entrepreneurship that help to determine whether or not an actor/organization acts entrepreneurial. First, entrepreneurship includes acts that are targeted at ‘enhancing governance influence by altering distribution of authority and information’ (Boasson and Huitema, 2017). And second, entrepreneurship includes acts ‘aimed at altering or diffusing norms and cognitive frameworks, worldviews or institutional logics’ (Boasson and Huitema, 2017). In this context, the authors highlight the role of positive and negative framing in changing ideas and approaches. As I will discuss in more detail below, governance entrepreneurs in the organizational field of carbon disclosure employ in particular the latter approach.

It is to the concept of organizational fields that I turn to now. Institutional analysis has repeatedly shown that the international arena is increasingly institutionalized, showing a high degree of international organization. In this context, scholars have for example analyzed the increasing legalization of world politics (Goldstein et al., 2001), its broad institutional similarity across national cultures (Meyer et al., 1997) and emerging strategies to increase coherence amid institutional diversity, for example, through orchestration (Abbott et al., 2016). The transnational realm is no different from the international. Increasing institutionalization is a key feature of transboundary relations that involve non-state actors next to governmental actors. While the concept of (transnational) institutionalization is broad, the perspective of organizational fields enables us to analyze the process of institutionalization at the level of distinct issue areas and policy-fields. In DiMaggio and Powell’s classic definition (1983: 145), organizational fields are made up by ‘those organizations that, in the aggregate, constitute a recognized area of institutional life’. This broad understanding will guide the analysis of carbon disclosure as an emerging organizational field.

The discussion will now turn to a model of the institutionalization process in transnational governance. 3 At the end of this process stands the fully matured organizational field. The relevance of institutionalization relates to two main observations. First, high levels of institutionalization of governance mechanisms correlate with positive measurements of problem-solving effectiveness (Beisheim and Liese, 2014). In other words, high levels of institutionalization lead to better performance. And second, the level of institutionalization might serve as a proxy for the degree of change of a given governance system. In the case of carbon disclosure, the possibly high level of institutionalization might signify that relevant parts of the economic sub-system have started to change into a more sustainable direction. The model I propose here to analyze the institutionalization process in transnational carbon disclosure governance has four stages. The stages are conceptually separate, but in reality they will occur simultaneously to some degree. It is also important to note that while the different stages represent distinct stages of institutionalization in the transnational realm, they do not represent a strict sequence. An issue area (such as carbon disclosure) moves towards transnational organization through a number of distinct stages. If all four stages can be observed, this can be interpreted as a high level of institutionalization and a mature organizational field.

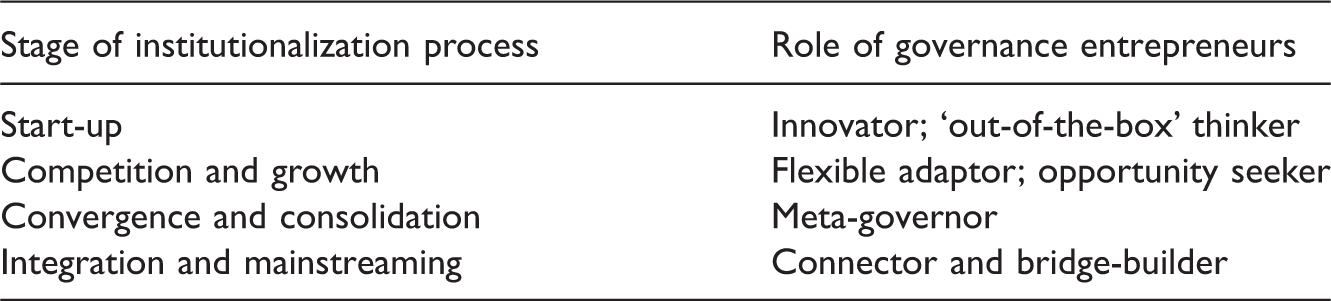

The start-up phase is characterized by an experimental mode of operation, high uncertainties and the risk of failure. New ideas and institutional innovations are developed by governance entrepreneurs, change agents that aim at systemic solutions to pressing societal problems. New governance arrangements are developed and tested in a social niche that provides some protection against the powerful interests of the status-quo actors in the field.

The second stage, competition and growth, is characterized by an increase in the number and scope of governance arrangements. Individual arrangements act largely independent of each other as interactions are uncoordinated and driven by a competitive logic. The initial innovation is further developed and smaller variations occur, reflecting the diverging interests of stakeholders involved.

In the third distinct phase of convergence and consolidation, arrangements start to converge in terms of their core norms, organizational principles and external communication. While the different processes that contribute to policy convergence are less important in this context, convergence should not be understood as leading to a predefined end-point (all arrangements look the same), but rather highlights the procedural character of convergence. Policy convergence is defined ‘as any increase in the similarity between one or more characteristics of a certain policy (e.g. the exact policy settings) or in the similarity of the policy repertoire in a certain field (such as environmental policy) across a given set of political jurisdictions (such as states) over a given period of time’ (Holzinger et al., 2008: 556). Convergence of governance arrangements in the environmental field has been analyzed from two different perspectives: one line of research has observed the gradual convergence of transnational rule-making organizations in terms of their internal organizational structures, decision-making procedures and overarching discourses (Cadman, 2011; Dingwerth and Pattberg, 2009). On this account, an organizational field of transnational rule-making is emerging that compels individual organizations to become more similar over time (through the mechanisms of isomorphism and professional networks). A second line of research has focused on convergence in terms of concrete policies and content, not on institutional aspects (Bartley, 2007; Overdevest, 2010; Smith and Fischlein, 2010).

In addition, the third stage of transnational institutionalization is also characterized by the emergence of meta-governance (Jessop, 1997). On this account, generic rules are developed with a view towards streamlining divergent policies and practices by predominantly public meta-governance organizations (Brunsson et al., 2012). From this perspective, meta-governance has been defined as ‘creating the frameworks and rules of the game within which private forms of governance need to pursue their activities’ (Derkx and Glasbergen, 2014: 42). Increasingly, meta-governance by private transnational actors is acknowledged. A well-known example of private transnational meta-governance in the environmental field is the ISEAL alliance (Derkx and Glasbergen, 2014; Loconto and Fouilleux, 2014), an organization that has develop a standard for developing sustainability standards (such as those administered by the Marine Stewardship Council or Fair Trade International). Meta-governance has also been observed in the field of labor standards (e.g. Fransen, 2015).

The fourth stage of institutionalization is characterized on the one hand by the integration of transnational governance arrangements (or parts thereof) into existing international public policy arrangements, and on the other hand by the emergence of new international institutions that attempt to (re)integrate transnational governance into the public realm (Pattberg, 2006). This re-integration might lead to better coordination and overall effectiveness; however, the political appropriation of private standards by public actors might also lead to decreased effectiveness as the underlying market-driven logic of transnational institutions is weakened. At each stage described above, governance entrepreneurs will play an important, albeit different, role. The next section will analyze the role and relevance of governance entrepreneurs/entrepreneurship along the four stages of institutionalization.

The institutionalization of carbon disclosure

What is carbon disclosure?

The terms carbon disclosure, carbon accounting and carbon reporting are often used interchangeably; however, as they display slight definitional differences, a brief discussion of each term seems appropriate. A recent review of the literature on carbon accounting (Stechemesser and Guenther, 2012) has counted no less than 129 publications between 1998 and 2011, with a visible increase in annual publications from 2008 onwards (20 and more paper published per year). Carbon accounting and related terms such as carbon reporting, accounting for emissions and Greenhouse Gas Accounting are defined in various ways, offering both narrow and broad conceptualizations. Based on the review of available literature, Stechemesser and Guenther (2012: 25) summarize the common denominator of carbon accounting as the ‘measuring, collation, assessment and communication of GHG emissions emitted by a source or sequestered in a sink and the monetary valuation of GHG emissions (as assets and liabilities) to provide this information to internal or external audiences’. This broad definition consequently covers various mandatory or voluntary processes (e.g. estimation, measurements, monitoring, reporting, verification and auditing) of calculating emissions and removals of GHGs (including but not limited to carbon dioxide (CO2)) to the atmosphere at various spatial scales (e.g. national, regional, individual, organizational) with a broad range of purposes including compliance, reporting and disclosure (Ascui and Lovell, 2011).

Carbon reporting is a narrower term (Haigh and Shapiro, 2012), denoting the (voluntary or mandatory) reporting of carbon emissions and carbon footprints by companies. Here, the debate has focused on questions concerning the information requirements of the addressees of carbon reporting and the specific methods of reporting (e.g. Kyoto Protocol’s reference manual, the British PAS 2050 standard or the Greenhouse Gas Protocol (GHG Protocol) Standards).

A third relevant conceptualization is carbon disclosure. The idea of carbon disclosure is to ‘translate corporate carbon profiles into assessments of risks and market opportunities with clear financial implications for firms and investors. Indeed, this constitutes the central logic behind the carbon disclosure movement’ (Kolk et al., 2008: 228–229). Here, the focus is less on the overall process and methodology but rather on the broader societal purpose of reporting and accounting. Carbon disclosure is increasingly understood as an instance of informational governance, i.e. governance through information (Soma et al., 2016). More specifically, carbon disclosure uses mechanisms of transparency and accountability to influence behavior of target actors.

Within the broader debate on transparency and accountability (Biermann and Gupta, 2011; Gupta and Mason, 2016), Mitchell (2011) has distinguished transparency of governance from transparency for governance. While the former refers to policies and institutions designed to allow a polity to control the decision-makers, the latter can be defined as ‘the acquisition and dissemination of information to influence the behaviour of particular actors’ (Mitchell, 2011: 1882). Further, we can distinguish disclosure-based transparency and education-based transparency (Mitchell, 2011: 1885). While education-based transparency seeks to correct a situation in which actors lack complete and accurate information about a given situation and thus fail to recognize their true interests, disclosure-based transparency attempts to overcome situations of information asymmetry. Once crucial information is made public, there is an expectation that power asymmetries are rectified and the playing field between actors is leveled (Mitchell, 2011: 1885).

In the case of climate governance by disclosure, for-profit actors (e.g. institutional investors) different from the information-holders (companies) call for disclosure of emissions data that can lead to a new strategic situation in which change in behavior becomes the self-interest of the targeted actors. Recent studies on carbon disclosure have, among other things, scrutinized the relation between risk exposure and sustainable performance (Elijido-Ten, 2017), analyzed the differences between mandatory versus voluntary disclosure initiatives (Matisoff, 2013), assessed the political contestations inherent in carbon disclosure (Knox Hayes and Levy, 2014), questioned the ability of disclosure to empower (Dingwerth and Eichinger, 2010), and explored the limits of carbon disclosure as a governance mechanism (Harmes, 2011). Few studies have however approached carbon disclosure from an organizational field perspective (for a general reconstruction, see MacLeod and Park, 2011).

Analysis and discussion

The following sections analyzes the process of institutionalization in the domain of carbon disclosure, a sub-field of the broader climate change governance domain with specific focus on the role of governance entrepreneurs. The aim of this section is two-fold: first, to provide a plausibility probe for the assumptions about the four stages of institutionalization as outlined above; and second, to better understand the role of governance entrepreneurs/entrepreneurship in each stage. 4

Start-up stage: The coalition for environmentally responsible economies

The CERES emerged in 1989 when a group of responsible institutional investors (organized in the Social Investment Forum, SIF) and US-American environmental organizations jointly published the so called Valdez Principles, utilizing the huge public outrage around the Exxon Valdez oil spill (of 24 March 1989). Within this group, participants started discussing the possibility of using the power of investors (i.e. shareholder resolutions and structural pressure of divestment) to influence company behavior. The innovative idea behind CERES was to engage companies in an ongoing dialogue resulting in the endorsement of a set of core environmental principles (these so-called Valdez principles have been renamed CERES principles in 1993) that would establish long-term corporate commitment to continual progress in environmental performance.

CERES developed a 10-point Corporate Code of Conduct that establishes ‘an environmental ethic with criteria by which investors and others can assess the environmental performance of companies’ (CERES, 2002a: 31). The pivotal commitment is the obligation on the part of companies to report regularly about the state and the improvement of their environmental behavior. The code of conduct consequently popularized the idea of periodic environmental reporting, but also contributed to a stronger awareness of the financial consequences of environmental misbehavior of corporations.

The original idea for CERES emerged at a board meeting of the SIF in 1988. It had become evident that most of SIF’s clients considered environmental performance a key issue for investment decisions, but serving those clients proved difficult because of information shortage on the overall environmental performance of companies. The idea of periodic environmental reporting therefore emerged as a suitable way to provide social responsible investors with the necessary information, setting in motion a transformative process in which companies would gradually change their unsustainable practices into more sustainable ones, driven by public scrutiny and investor pressure. Referring to some of the broader contextual factors that enabled the novel idea of environmental reporting to emerge, Joan Bavaria, a founding CERES member, recalls: [the need for principles and reporting] arose just as an information revolution was starting to race around the world. We senses that this was a real revolution, with implications for our economy, environment and culture…. (cited in Pattberg, 2007: 163) [t]he vision of CERES’ organizers was for firms to release to the public ‘consistent and comparable’ environmental data similar to what is used by investors for analysis of corporate financial performance.

While at the beginning the very idea of engaging with corporations was contested, CERES proved the added value of this strategy and became a governance entrepreneur in its own right. The entrepreneurial role and innovative potential of CERES can be illustrated by its attempt to frame climate change as a business risk.

5

Framing has been identified by the editors of this special issue as a key strategy of entrepreneurs that do not target authoritative decision-making but rather aim for normative change. Boasson and Huitema (2017) write: ‘The purpose [of framing] will be to promote ideas, methods or measures that are new within the setting they are performed’. This is precisely what we observe in relation to CERES attempt to re-frame climate change as a business strategy. As part of this framing strategy, CERES has produced and commissioned a range of studies that highlight climate change as a risk for business and investors. For example, in a 2002 report CERES (2002b: 2) states: [T]he bottom line […] is straightforward: climate change represents a potential multi-billion dollar risk to a wide variety of U.S. businesses and industries. It should, therefore, command the same level of attention and urgency as any other business risk of this magnitude.

In a study from 2010 (CERES, 2010), the climate change proxy voting of 46 mutual funds in the US is analyzed and found to have grown from 14% votes in support in 2004 to nearly 27% in support in 2009. When looking at the specific motions (resolved clauses) asking boards for action, it is interesting to note that not only relatively undemanding requests – such as producing a report on climate-related risks – were supported, but also far more demanding request. For example, resolutions asking the board to adopt quantitative GHG reduction goals received 38% support in 2009 (CERES, 2010: 11). More recent data from 2015 shows that 95 companies have received climate-related motions from members of the CERES-organized INCR, often reaching majorities from the shareholders. One concrete example is the motion directed at BP to report annually on carbon asset risk mitigation, accepted with 98.3% of the vote. The motions (CERES, 2016) demand the Company to ensure that routine annual reporting from 2016 includes further information about: ongoing operational emissions management; asset portfolio resilience to the International Energy Agency’s (IEA’s) scenarios; low-carbon energy research and development (R&D) and investment strategies; relevant strategic key performance indicators (KPIs) and executive incentives; and public policy positions relating to climate change.

Competition and growth: The Greenhouse Gas Protocol, the Carbon Disclosure Project and the Investors Network on Climate Risk (INCR)

The second stage of transnational institutionalization is characterized by competition among various schemes (often catering to divergent interests) and the overall growth of the governance innovation niche. Consequently, this section discusses the emergence and subsequent competition among three organizations related to the field of carbon accounting. The GHG Protocol, the CDP and the INCR.

The GHG Protocol is a widely used accounting tool for government and business leaders to understand, quantify and manage GHG emission. The GHG Protocol emerged out of collaboration between the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD). Both organizations recognized that a global and unified standard for corporate carbon and GHG disclosure and reporting would become a key necessity in light of evolving climate change policy. In collaboration with large corporate partners such as British Petroleum and General Motors, WRI published a report called ‘Safe Climate, Sound Business’ (WRI, 1998) that identified the need for standardized measurement of corporate GHG emissions as a key step towards more effective climate change policies.

Similar initiatives were underway at the WBCSD. In late 1997, WRI senior managers met with WBCSD officials and an agreement was reached to launch an NGO-business partnership to address standardized methods for GHG accounting. A steering group was set up in 1998, comprised of members from environmental groups and industry (e.g. WWF, Pew Centre, Norsk Hydro and Shell, among others) to guide the multi-stakeholder standards development process.

Four years after these beginnings, the first generation of standards, the Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard (the so called Corporate Standard) was finally published in 2001. 6 Since then the GHG Protocol has developed a total of four standards, including a set of calculation tools to assist companies in disclosing their GHG emissions.

In more detail, the Corporate Standard provides concrete standards and guidance for companies and other organizations preparing a GHG emissions inventory. It covers the accounting and reporting of the six GHG covered by the Kyoto Protocol – CO2, methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), and sulphur hexafluoride (SF6). It was designed to help companies prepare a GHG inventory at lower costs by simplifying reporting requirements; to provide business with information that can be used to build an effective strategy to manage and reduce GHG emissions (including investors); and to increase consistency and transparency in GHG accounting and reporting among various companies and private programs.

CDP, formerly the Carbon Disclosure Project, is a London-based independent non-profit organization representing, as of 2016, 827 institutional investors with an investment base of more than $100 trillion (CDP, 2016). In 2003, it issued its first CDP questionnaire that asked companies to disclose their past and future carbon emissions. CDP has followed up with annual questionnaires to companies requiring disclosure of their carbon emissions. The required disclosure stimulates information sharing about climate change and the related business risks between companies and stakeholders. The CDP ambition to drive sustainable economies is based on the assumption that information disclosure will motivate and facilitate meaningful dialogue among business actors, investors and the wider public and ultimately trigger substantial corporate responses to climate change. In the words of Kolk et al. (2008: 724–725): The CDP represents a voluntary effort to develop standardized reporting procedures for firms concerning their climate-related activities, in a form intended to complement annual financial accounts and provide information relevant to investors.

In 2015, some 5500 companies report to the CDP, making it the world’s largest database on corporate environmental information. CDP also offers an evaluation of the quality of carbon disclosure. The Carbon Disclosure Leadership Index (CDLI) provides information on the quality of carbon disclosure for carbon-intensive and non-carbon-intensive sectors and makes disclosure statements comparable across industries. In addition to the annual disclosure request, CDP has diversified its operations. For example, the creation of the Corporate Supply Chain Program widens CDP’s focus to encompass the emissions resulting from a company’s supply chain and the risks and opportunities in relation to climate change. 8 Furthermore, CDP also offers disclosure tools for cities to manage their carbon emissions.

While the business community has responded positively to the CDP – among the FT Global 50, some 40 companies regularly respond to the CDP questionnaire – the voluntary nature of the arrangement has prompted a number of critiques. First, transnational companies are given the flexibility to choose which region they include in their emission disclosure. For example, some transnational corporations have chosen to disclose information on their carbon emissions deriving from their activities in developed countries exclusively while neglecting emergent markets. Most companies place a disclaimer in their answer that the information they are disclosing does not include their activities in some developing countries. Second, the output of the arrangement (i.e. the emissions data) is intended for global use, but a majority of the institutional investors are based either in Europe or in the North America. Institutional investors from other world regions are not explicitly excluded from participation, their non-participation, however, suggests that they lack the capacity to do so.

The establishment of an institutionalized framework for reporting carbon emissions of companies, and since 2013 also cities, through the CDP and the GHG Protocol has been accompanied by a parallel institutionalization of the investor-side of the carbon disclosure equation. As a result, a number of parallel approaches towards carbon disclosure are emerging, a clear indicator of institutionalization.

The INCR was launched officially in 2003, following the successful Institutional Investors Summit on Climate Change held at the United Nations headquarters in New York. INCR is a network of institutional investors and financial institutions that aims at promoting better understanding of the financial risks and investment opportunities posed by climate change. The entrepreneurial agent behind INCR is CERES. While CERES can be considered an entrepreneur in the field of institutional investor support for carbon disclosure as well, their activities could also be interpreted as an attempt to solidify the emerging field in order to secure influence. On this account, CERES has become a structurally powerful actor in the field of carbon disclosure and reporting, particularly in the US.

INCR’s membership has grown steadily from 10 investors managing approximately $600 billion in assets in 2003 to more than 70 investors managing close to $7 trillion in assets. Members include asset managers, state and city treasurers and comptrollers, public and labor pension funds, foundations and other institutional investors. INCR uses the collective power of investors to promote improved disclosure and corporate governance practices on the business risks and opportunities posed by climate change.

INCR has mainly worked on two fronts: first, by targeting public actors such as the US Securities and Exchange Commission; and second, by targeting corporations directly. INCR’s main tool for achieving these goals is the INCR action plan, originally developed in 2003, and renewed in 2005 and 2008. The plan calls on institutional investors, fund managers, financial advisors and companies to take a range of measures to address the financial risks of climate change (Pattberg, 2012). In addition, the plan also establishes a commitment of the INCR members themselves, including the commitments to manage their investments accordingly, to engage companies, investors, and to support policy action.

INCR also measures progress against the action plan as a tool for changing investor behavior. In a 2008 report, INCR reviews the progress made towards the 2005 action plan and concludes that ‘even with this impressive progress by INCR and its members, there is still much to be done’ (INCR, 2008: 2). Among other issues, the report criticizes that too few investors are realizing the substantial gains to be made in the clean technology sector, urges that major mutual funds should pay more attention to climate change and calls for companies to further improve their disclosure of climate related risks.

In sum, the examples of the GHG Protocol, CDP and INCR illustrate how the generic idea of environmental disclosure that has been pioneered by CERES in the early 1990 s is further detailed, interpreted and implemented in diverse ways. The result is a proliferation of similar initiatives that perform like-functions that is characteristic of the second phase of transnational institutionalization. Examples from other environmental domains include the proliferation of forest and marine fisheries and aquaculture certification schemes that followed the initial innovation of certification in the early 1990 s (see Kalfagianni and Pattberg, 2013; Visseren-Hamakers and Pattberg, 2013). Governance entrepreneurs are vital in this phase as they copy and adapt generic ideas to specific contexts, thereby furthering the growth of the institutional field. In particular, competition among emerging organizations pressures entrepreneurs to further innovate.

Convergence, consolidation and meta-governance: The Global Reporting Initiative and the Climate Disclosure Standards Board

The third stage of transnational institutionalization is characterized by the emergence of meta-governance in a given governance arena. Therefore, in this section, I take a closer look at two organizations that engage in meta-governance in the field of carbon disclosure: the GRI and the CDSB.

The idea of carbon disclosure is part of the wider discourse and practice of environmental and sustainability reporting. Going back to the time of shareholder campaigns against corporate engagement in the South African Apartheid regime, social activism in cooperation (rather than in confrontation) with companies quickly became a prime choice for many activists during the late 1980 s (Bendell, 2000). In 1989, CERES was the first organization to issue a corporate code of conduct that included a commitment to ongoing disclosure and reporting on environmentally sensitive issues (Pattberg, 2007: 151–190). This idea of non-financial disclosure and reporting was later labeled sustainability reporting and successfully institutionalized in the GRI in 1997.

The GRI has been set up as a multi-stakeholder initiative to provide a framework for corporations to report on their sustainability performance. The organization was initially organized as a joint project of CERES and the Tellus Institute, a leading North American think tank in the field of sustainability politics, supported by the United Nations Environment Program. A key entrepreneur in this context has been Bob Massie, former president of CERES and first chair of the GRI from 1997. GRI now includes several hundred members from various regions and sectors of society. In contrast to other transnational governance arrangements, where a private governance scheme emerged as a result of the absence of international standards, the GRI was initiated in response to the proliferation of different reporting standards that inhibited a comparison between sustainability reports of individual companies. It therefore serves as a prime example of convergence and consolidation in the field of sustainability reporting as it serves the purpose of meta-governance. On this account, meta-governance can be interpreted as the result of entrepreneurial strategies reacting to a change in the wider organizational context, in this case the proliferation of competing reporting schemes.

First led by a steering committee of governance entrepreneurs in the field of sustainability reporting, the GRI became an independent organization in 2002 (see Dingwerth, 2008). Since then, GRI’s goal has been to make ‘reporting on economic, social and environmental performance as routine and comparable as financial reporting’ (GRI, 2003: 4). As its main instrument to achieve this goal, the GRI is developing and advertising its Sustainability Reporting Guidelines. A first version of these guidelines was developed in 2000 and refined several times (the current generation of guidelines is labeled G4). The aim of the guidelines is to enable report users – rating agencies, investors, and shareholders, but also employees, consumers or local communities – to evaluate a company’s performance and to compare it to that of its competitors with a view towards integrating this additional information into decision-making. This specific approach, governance by disclosure and comparison, has been highly influential in the establishment and institutionalization of the CDP and other carbon disclosure initiatives.

Recently, scholars have begun to study the role of international organizations and other actors as orchestrators of transnational governance (Abbott et al., 2016). The main argument here is that organizations utilize intermediaries (such as the GRI) to affect behavior of target actors (such as corporations). In the context of this discussion, orchestration can be seen a further indication of increased institutionalization.

The CDSB is an explicit attempt to provide meta-governance to an area that is marked by bottom-up diversity. The CDP, the GHG Protocol, the INCR and other organizations offer frameworks for reporting corporate GHG emissions. In the words of CDSB board member Richard Samans (CDSB, 2013): Consistent and comprehensive disclosure frameworks are important to the incentives shareholders provide to corporate managers to deploy capital efficiently. The World Economic Forum is pleased to be part of this ground breaking cooperation to establish a generally accepted corporate carbon disclosure framework that will make life easier for companies and investors. It is a good example of leadership by the private sector and civil society on a critical global challenge.

In the context of our discussion of institutionalization at the transnational level, the CDSB is a very good illustration of the stage of convergence and meta-governance. In this case, meta-governance through the CDSB is driven by the interests of key players that would gain from increased cooperation and mutual recognition. On the board of the CDSB, the CDP, CERES, the GHG Protocol and the Climate Registry are represented, among others. It is the explicit goal of the CDSB not to develop a new and alternative standard, but to merely harmonize what is already out there. Whether this behavior is still covered by the concept of governance entrepreneurship or rather by vested interests and strategic behavior is an interesting question beyond the scope of this article.

Harmonization through meta-governance is also observable in environmental domains beyond carbon disclosure. For example, the ISEAL Alliance has become the standard setter for developing transnational multi-stakeholder standards (through the ISEAL Code of Good Practices), including those of the FSC, MSC, fair-trade International and others.

Integration into international public policy: The UN Principles for Responsible Investment and the ISO 14064 Standard

The fourth stage in the institutionalization of transnational governance is the integration into international regulatory frameworks that further mainstream and streamline transnational initiatives. Two concrete examples illustrate this development: the Principles for Responsible Investment Initiative (PRI) and the International Organization for Standardization’s 14064-I standard. 9

The PRI is an international network of investors working together with the aim to implement the six Principles for Responsible Investment across the investment industry. 10 Its goal is to understand the implications of sustainability for investors and support signatories to incorporate these issues into their investment decisions. In implementing the principles, signatories hope to contribute to the development of a more sustainable global financial system. As of December 2017, the PRI has approximately 1700 signatories from over 50 countries, representing 62 US $ trillion in assets.

In early 2005, former United Nations Secretary-General Kofi Annan (an example of a governance entrepreneur at the UN level) invited a group of the world’s largest institutional investors to join a process to establish the Principles for Responsible Investment. Developed with the contributions of a multi-stakeholder group including the global investment industry, intergovernmental organizations, civil society and academia, PRI is an investor-led coalition in partnership with the United Nations Environmental Programme Finance Initiative and the United Nations Global Compact. The two latter organizations are themselves joint ventures between the UN and business actors. While they act largely independent of the UN decision-making (through the UN General Assembly and the ECOSOC), they supply the idea of responsible investment principles with the legitimacy of the UN system. This is a good illustration of the fourth stage of transnational organization, in which transnational rules become (re)integrated into public policy framework, at least partially.

Furthermore, principle 3 asks investors to seek appropriate disclosure on environmental and social issues from the companies that they invest in, referring to disclosure tools such as the GRI.

The second example illustrates how transnational regulations are incorporated into international (or in this case hybrid) institutions. In 2006, the International Organization for Standardization (ISO) adopted the GHG Protocol’s Corporate Standard as the basis for its ISO 14064-I: Specification with Guidance at the Organization Level for Quantification and Reporting of Greenhouse Gas Emissions and Removals. This observation highlights the role of the GHG Protocol’s Corporate Standard as the international standard for corporate and organizational GHG accounting and reporting.

Similar developments have been reported from other environmental governance domains. For example, the federal government of Mexico has incorporated parts of the international Forest Stewardship Council Principles and Indicators into its reformulated 1996 forest law (Pattberg, 2005). In sum, the two examples discussed above clearly show that the fourth stage of transnational organization has been reached in the field of carbon disclosure and reporting. In this last stage, entrepreneurship might appear less relevant than compared with the earlier phases as fundamental principles have already been established and the ‘business model’ of carbon disclosure has been proven. However, the entrepreneurial element is visible in the role of Kofi Annan, for example, who seized the opportunity to introduce the idea of responsible investment into the United Nations context.

Conclusions: The role of governance entrepreneurs in institutionalizing transnational governance

Dominant roles of governance entrepreneurs in each stage of the institutionalization process of carbon disclosure.

In addition to understanding the role and relevance of governance entrepreneurs in the four stages of institutionalization of the carbon disclosure organizational field, there are three more general observations that stand out. First, entrepreneurial approaches play a considerable role in the early stages of institutionalization, in particular in the experimental start-up phase, where investments are risky and the return on investment uncertain. At this stage, entrepreneurial behavior is aided by broader contextual ‘windows of opportunity’ that enable risky ideas to take hold in a volatile environment. The huge public outrage around the Exxon Valdez oil spill, paired with proven strategies of divestment in South Africa and a technological revolution at the horizon (e.g. world wide web) enabled the idea of periodic environmental reporting to take hold in business circles beyond the few ‘green’ pioneers. Entrepreneurship was able to re-frame climate change into a business risk and over time to institutionalize climate change risk awareness as the new normal (e.g. visible in the recent majority of shareholder votes in favor of a climate risk strategy of ExxonMobil).

Second, organizations that have been governance entrepreneurs might evolve into status-quo agents once the institutionalization process has reached the meta-governance phase. Rather than pushing for more innovation, organizations might chose to protect what has been achieved. The result is often a quest for harmonization (benefitting some actors not others) and a general slowing down of entrepreneurial activities. In other words, entrepreneurs develop into powerful agents, often with new vested interests to be protected.

Finally third, entrepreneurship as a bottom-up strategy to overcome (real or perceived) governance failures does not necessarily lead to institutional fragmentation (Biermann et al., 2009). At the fourth stage, actors (often international organizations) provide steering functions that result in a balance between functional differentiation and conflictive fragmentation. Governance entrepreneurship therefore contributes to institutional complexity but not to dis-integration or conflictive overlaps that might undermine the overall governance effectiveness of an organizational field.

While these findings are first steps into the largely unknown terrain of governance entrepreneurship as a driver of transnational institutionalization, a number of questions remain unanswered and should therefore guide future research in this area. First, does the four-stage model of transnational institutionalization also apply to other sub-fields of environmental governance and beyond? Second, what resources explain the effectiveness of entrepreneurial strategies along the four stages (in other words, are some resources more important at a certain stage)? Third, at what point can we observe (or even predict) an organizational field to tip from an entrepreneurial mode into a more stable ‘normality’ (a development that is already partially visible in phase four of the institutionalization process)? And fourth, under what conditions does entrepreneurship develop into status-quo behavior that has the potential to stall further innovations towards the sustainability transition? Hopefully, future research will help answering these questions, thereby contributing to a much-needed theory of transnational organization.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.