Abstract

The Affordable Care Act (ACA) greatly expanded access to health care. The number of uninsured individuals in the United States is at its lowest since the first surveys were conducted on insurance status in 1972.1,2 This legislation and its associated expansion in coverage has the potential to improve underutilization of appropriate health care by lowering or eliminating cost sharing for recommended but underused medical services. 3 Large national randomized studies have demonstrated a reduction in appropriate or needed medical services as consumers’ out-of-pocket expenses for those services increased. 4 Increased costs can particularly affect use of preventive care5–8 and prescribed medications.9,10 Legislation that lowers the cost of underused, evidence-based preventive services may be particularly beneficial, as these services aim to diagnose and address illnesses before they become more harmful or more expensive to manage and treat.

Despite this recent expansion in access to health insurance, consumers still face barriers to using their insurance plans to obtain needed care. 11 Some people are covered by plans that do not provide adequate financial protection from risk, relative to their incomes. 12 High deductibles or out-of-pocket costs associated with health care utilization among the insured also may dissuade consumers from accessing health care. 12 Many individuals, including those with insurance and those with chronic conditions requiring ongoing care, still report that they have delayed seeking medical services due to fears about the high costs of health care.13–15

Under the ACA, preventive care is covered without cost sharing for the insured. 1 However, individuals who are unaware of this complete coverage may opt to delay or avoid preventive care as a result of the assumed cost, waiting to seek care until their illness is severe and requires advanced medical care. Consequences of such delay may include missed opportunities to appropriately address chronic conditions such as heart disease, cancer, and diabetes, which were responsible for approximately half of all American deaths in 2010. 16 Low health insurance literacy is a widespread characteristic of the population in the United States and can lead to a misunderstanding of the financial and health implications of health insurance plans.17,18 Individuals with low health insurance literacy may be less likely to use preventive services and to delay or avoid preventive care due to cost. 19 Numeracy, which is a component of health insurance literacy, is also important to understanding and using health insurance. 20 A proficient level of numeracy is necessary for making informed decisions about health care planning (e.g., for chronic conditions) 21 and appropriate use of preventive services like colorectal cancer screenings and mammography.22,23

Consumers’ anxiety and distress as a result of medical costs, referred to as increased financial toxicity, also may affect their health care utilization.24,25 Financial toxicity has been studied in the context of cancer because of the significant costs associated with cancer treatment 26 and has been related to cancer patients’ treatment decisions. 27 Though general medical expenses may not be as expensive as some cancer-related costs, 26 many costs add significant burden to consumers28–30 and are rising even among privately insured patients.31,32 Little is known about the relation between financial toxicity as a result of general medical expenses and health care utilization for prevention of disease and treatment of emerging or chronic conditions among the general population.

Consumers’ tendency to seek more or less medical care, measured on a minimizer-maximizer scale, may also affect their utilization of needed medical services. 33 Health care “maximizers” are consumers that are more likely to seek medical care even for minor problems, whereas “minimizers” may prefer to avoid medical care until it is absolutely necessary. Gaining insight into consumers’ preexisting utilization biases is an important step in developing a better understanding of why individuals may delay or avoid seeking care.

To better ensure consumers’ access to needed health care services for both prevention of disease and treatment of emerging or chronic conditions, research should explore the characteristics of those who delay or avoid seeking health care services due to cost, particularly those who report a delay in preventive care due to cost. In this study, we examined the characteristics of individuals who reported delaying or avoiding seeking care in the past 12 months. Our primary hypotheses were that those with higher perceived financial toxicity from health care, those who are more likely to minimize seeking health care, those with lower numeracy skills, and those with lower health insurance knowledge would be more likely to report avoiding or delaying care due to cost. Additionally, we hypothesized that those who were unaware that preventive care is covered with no out-of-pocket costs to consumers would be more likely to report avoiding or delaying seeking preventive care due to cost.

Methods

Participants were recruited via Amazon Mechanical Turk (MTurk) in May 2017. MTurk is an online service through which users can complete studies posted by researchers in exchange for payment. In this study, participants answered a 77-item survey and were paid $ 0.50 on the survey’s completion. MTurk may have some distinct advantages over other in-person convenience sampling methods as participants are more likely to be similar to those in the general US population. 34 Previous research has also demonstrated that data collected from MTurk are as valid as those obtained using traditional data collection methods.35,36

Measures

Delaying or Avoiding Care Due to Cost

Participants were asked to indicate whether they had delayed or avoided any care due to cost in the past 12 months with a single item (one of our primary outcomes). They were then shown a list of six health care services common among both men and women across various ages (well visit, doctor visit when one is sick, cholesterol check, flu shot, purchasing prescription drugs, obtaining bloodwork at a laboratory) and indicated whether they had delayed or avoided those specific services due to cost. Each of the six services were categorized a priori as preventive care (well visit, cholesterol check, flu shot, selected because they are relevant across gender, across many age ranges, and/or are typically recommended at frequent intervals) or nonpreventive care (doctor visit when one is sick, purchasing prescription drugs, obtaining blood labs). Participants were considered to have delayed or avoided preventive care if they reported delay or avoidance of at least one of the three preventive services, and delay or avoidance of nonpreventive care if they reported delaying or avoiding at least one of the three nonpreventive services.

Financial Toxicity

Consumers’ anxiety and distress as a result of medical costs was measured using a modified version of the Comprehensive Score for Financial Toxicity (COST),37,38 a validated 11-item measure that asks about medical expenses and corresponding stress that individuals may experience. Because the COST measure was originally developed for cancer patients, the items included in our survey were edited to remove any mention of cancer and instead refer to general medical expenses. In doing so, we aimed to examine anxiety and distress a result of medical expenses more broadly. For example, the statement, “My cancer or treatment has reduced my satisfaction with my present financial situation” was edited to read, “My medical expenses have reduced my satisfaction with my present financial situation.” Items are scored numerically from 0 to 4, and an overall financial toxicity score is calculated through the summation of all 11 items. A lower COST score indicates greater financial toxicity. COST scores that were measured using the unedited construct were found to correlate with income, psychosocial distress, and measures of health-related quality of life. 38 Scores also exhibited strong internal consistency (Cronbach α of 0.92). 38

Medical Minimizer-Maximizer Scale

Participants’ predisposition to over- or underutilize medical care was estimated using the medical minimizer-maximizer scale. 33 This recently validated measure includes 10 items scored on a Likert scale from 1 to 7, and an overall minimizer-maximizer value is calculated by averaging the 10 individual item scores. For each participant, a greater score on the minimizer-maximizer scale indicates a preference toward seeking health care at a greater frequency than those scoring lower on the scale. This scale has been shown to predict self-reported health care utilization and was found to be distinct from distrust in medicine, health care access, and health status. 33 Given the novelty of this measure, we were interested in testing the association between minimizer-maximizer tendencies and delay or avoidance of care. Knowing that this measure has correlated with self-reported utilization in prior studies, we hypothesized that a tendency to underuse health care may also relate to avoidance of care due to cost, even after controlling for anxiety due to cost.

Health Insurance Knowledge

Participants’ general knowledge of health insurance was measured as a percentage of correct responses to eight true/false questions about important health insurance terms that were developed, tested, and modified from our previous work.39–41 If participants were insured, their specific understanding that preventive services are covered without cost sharing under the ACA was measured with a single yes/no item that asked whether the participants’ insurance covered the full cost of a yearly checkup or well visit. This measure has not been formally validated, but has demonstrated internal consistency in our previous work (Cronbach α ranges from 0.69 to 0.72).39,40 We hypothesized that knowledge of preventive care coverage without costs to consumers would inversely relate to a delay or avoidance of preventive care due to cost. We also examined whether broader health insurance knowledge related to a delay or avoidance of both preventive and nonpreventive care.

Subjective Numeracy

Participants’ numeracy was measured using the Subjective Numeracy Scale, 42 a validated 8-item scale that asks participants to rate their numerical ability and preference for the presentation of statistical information. Total scores can range from 1 to 6. An individual is determined to have greater subjective numeracy if he or she has a higher subjective numeracy score. The Subjective Numeracy Scale has been found to correlate with multiple objective measures of numeracy, while also being less stressful and frustrating for participants. 42 The scale exhibits internal consistency (Cronbach α of 0.82). 42 We hypothesized that lower numeracy would relate to higher avoidance of care due to cost based on past findings.22,23

Participant Characteristics

Participants answered questions about their age, gender, race, education, medical history, household income, and current health insurance status. Items from validated measures and/or national surveys were used when available.43–48

Data Analysis

Analyses were conducted using SPSS Version 23. Descriptive statistics for the participants were calculated and are presented in Table 1. Chi-square tests were used for categorical variables; in the event of small cell counts, Fisher’s exact test was used. T tests or Wilcoxon rank sum as appropriate were employed for mean differences between continuous variables in Tables 1 to 3. Separate logistic regression models examined the impact of each of our predictor variables (financial toxicity, minimizing/maximizing tendencies, subjective numeracy, health insurance knowledge, knowledge of preventive care coverage) on each of the three outcomes of interest (delaying/avoiding any care, delaying/avoiding preventive care, delaying/avoiding nonpreventive care). All models except for those with knowledge of preventive care coverage as the outcome controlled for the presence of any chronic conditions (any v. none), insurance status (insured v. uninsured), and income (less than $25,000, $25,000 to $49,999, $50,000 to $74,999, $75,000, or more). The knowledge of preventive care coverage models did not control for insurance status because that question was only asked of those who had insurance. We controlled for the potential confounding effects of insurance status and income because a lower income and lack of insurance may increase the relative out-of-pocket costs of care to consumers, and thereby potentially associate with varying levels of care utilization. 3 Similarly, we controlled for chronic conditions to avoid potential confounding, as the presence of chronic conditions is associated with increased use of health care services.49,50

Participant Characteristics (N = 470), Including Bivariate Analyses Examining Delaying/Avoiding Any Care due to Cost

One participant in the “did not delay” group did not answer age question and one participant in the “delay” group did not answer the age question.

One participant in the “did not delay” group did not answer the gender question. P value is for difference between Male and Female. Other was treated as missing for this analysis.

One participant in the “did not delay” group did not answer the income question (n = 258).

Three participants from the “delay” group and four from the “did not delay” group did not complete the minimizer-maximizer scale.

One participant in the “did not delay” group and three participants in the “did not delay” group did not complete the subjective numeracy measure fully.

Eight participants in the “delay” group and six participants in the “did not delay” group did not complete the financial toxicity measure.

Between delayed and did not delay.

Bivariate Analyses Examining Those Who Delayed or Avoided Preventive Care due to Cost Versus Those Who Did Not

Six participants from the “delay” group and eight participants from the “did not delay” group did not complete financial toxicity measure.

Three participants from the “delay” group and four participants from the “did not delay” group did not complete the minimizer/maximizer scale.

One participant from the “delay” group and three participants from the “did not delay” group did not complete the subjective numeracy measure.

Twelve people indicated that they looked up responses to some items; they were excluded from analyses with knowledge as an independent variable.

This analysis includes only insured participants, as the relevant survey item was only asked if participants were insured.

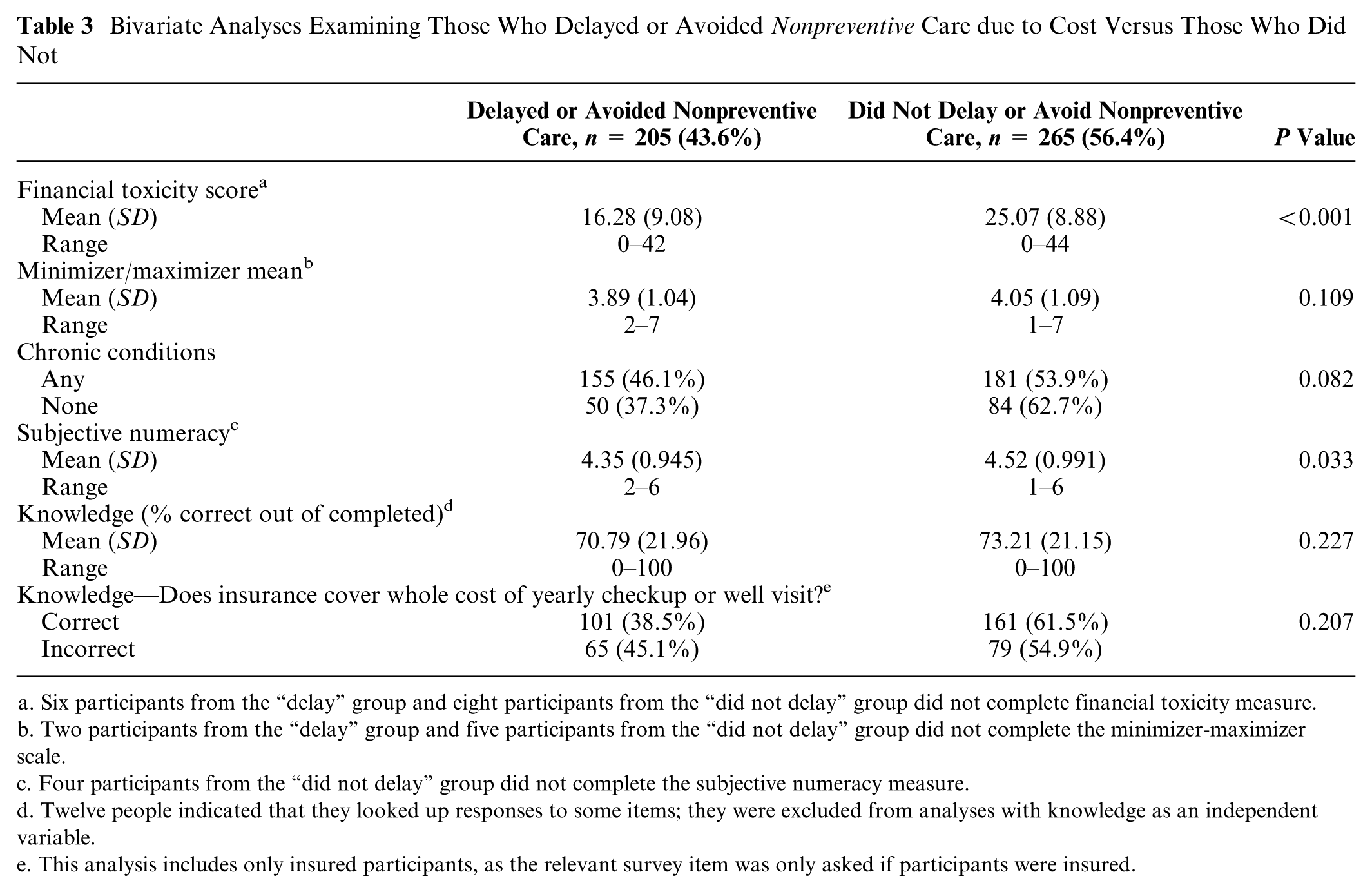

Bivariate Analyses Examining Those Who Delayed or Avoided Nonpreventive Care due to Cost Versus Those Who Did Not

Six participants from the “delay” group and eight participants from the “did not delay” group did not complete financial toxicity measure.

Two participants from the “delay” group and five participants from the “did not delay” group did not complete the minimizer-maximizer scale.

Four participants from the “did not delay” group did not complete the subjective numeracy measure.

Twelve people indicated that they looked up responses to some items; they were excluded from analyses with knowledge as an independent variable.

This analysis includes only insured participants, as the relevant survey item was only asked if participants were insured.

Of 518 participants enrolled, 470 participants responded correctly to two questions assessing their attention to the survey. Data from the 48 individuals that failed one or both attention-check questions were excluded. In addition, if participants responded that they had looked up answers to any of the questions in the survey (N = 12), those individuals’ responses to only the knowledge-based questions were excluded, and were therefore not included in analyses involving health insurance knowledge. Their remaining responses were not excluded and remained in other analyses. Finally, one individual did not complete the survey item regarding income, a control in our multivariable analyses, and was therefore excluded from all multivariable analyses

Results

Summary statistics for the 470 included observations are displayed in Table 1. The mean age of participants was 39 years (SD = 13.2, range 20–98) and over half were female (61.2%). Most identified as Caucasian only (80.9%) and non-Hispanic (94.7%). About half (56%) had earned a 4-year college degree or more. Most (86.4%) participants had health insurance, and a majority (71.5%) had at least one chronic health condition. The demographics of the population sampled on MTurk are fairly representative of the US population 51 and of other MTurk studies,34,52 though our sample was, on average, more educated as compared to the US population and there were fewer individuals who identified as Hispanic.

Bivariate analyses indicate individuals who delayed or avoided any medical care, compared to those who did not delay or avoid care, were more likely to be younger (mean age 36.38 v. 40.74, P = 0.003), female (49.8% of women v. 37.0% of men, P = 0.007), uninsured (68.8% of uninsured v. 41.1% of insured, P < 0.001), health care minimizers (mean score 3.75 v. 4.16, P < 0.001), experience greater financial toxicity (mean score 15.80 v. 25.64, P < 0.001), and have lower subjective numeracy (4.34 vs. 4.55, P = 0.001; Table 1).

Individuals who delayed/avoided preventive care, compared to those who did not delay/avoid preventive care, were more likely to experience greater financial toxicity (mean score 15.64 v. 24.12, P < 0.001), had lower subjective numeracy (mean score 4.35 v. 4.52, P = 0.009), had less general knowledge about health insurance (mean score 67.42% v. 74.58%, P < 0.001), and were less likely to know that preventive care is covered at no out-of-pocket cost (23.7% v. 42.4%, P < 0.001; Table 2). Individuals who delayed or avoided nonpreventive care, compared to those who did not delay or avoid nonpreventive care, were more likely to experience greater financial toxicity (mean score 16.28 v. 25.07, P < 0.001), and have lower subjective numeracy (mean score 4.35 v. 4.52, P = 0.033; Table 3).

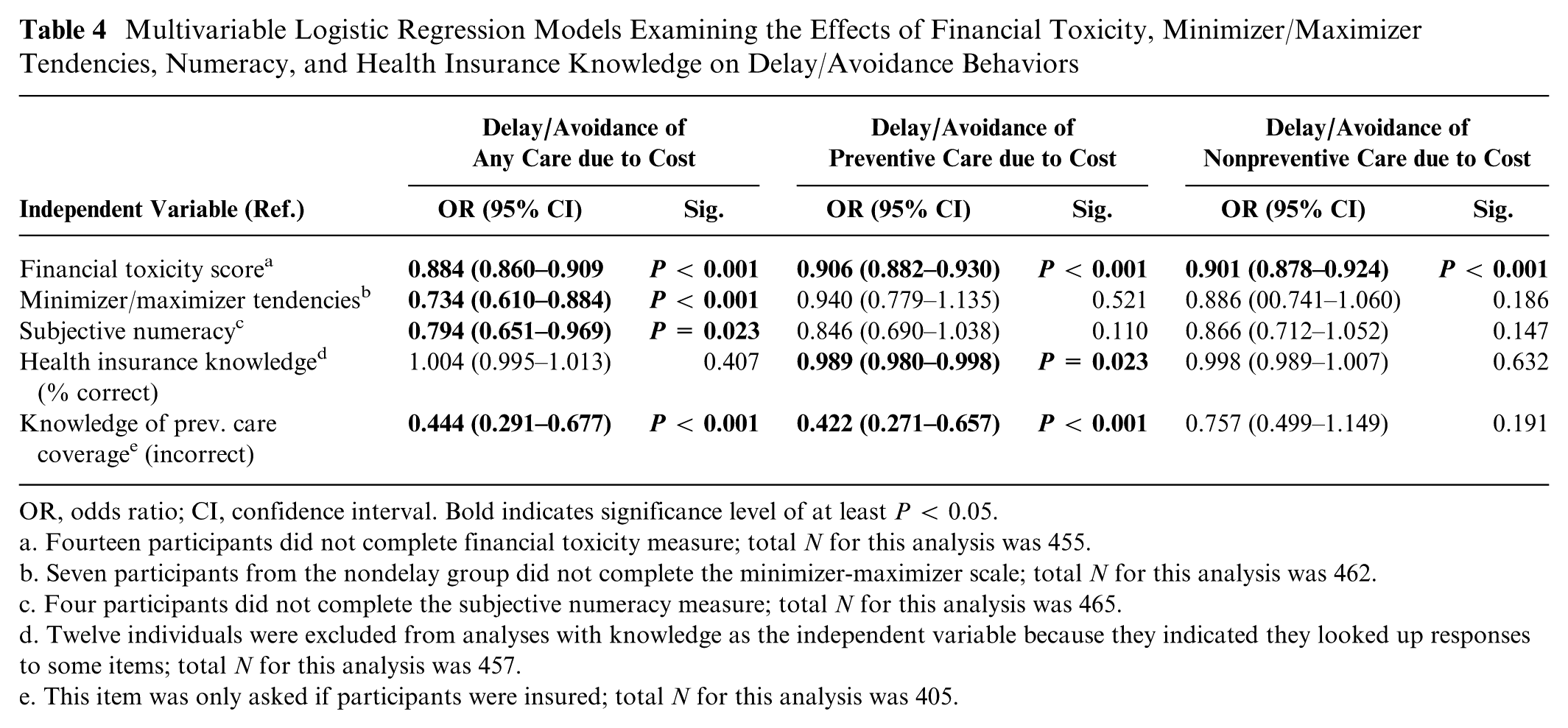

Multivariable analyses (Table 4) found that individuals were more likely to delay/avoid any care if they experienced greater financial toxicity (meaning a lower financial toxicity score) (odds ratio [OR] = 0.884; P < 0.001; 95% confidence interval [CI] = 0.860–0.909), exhibited minimizing tendencies (OR = 0.734; P < 0.001; CI = 0.610–0.884), had lower subjective numeracy (OR = 0.796; P = 0.023; CI = 0.651–0.969), and did not know that preventive care is covered at no out-of-pocket cost (OR = 0.444; P < 0.001; CI = 0.291–0.677). Individuals were more likely to delay/avoid preventive care if they experienced greater financial toxicity (OR = 0.906; P < 0.001; CI = 0.882–0.930), had lower health insurance knowledge (OR = 0.989; P < 0.023; CI = 0.980–0.998), and did not know that preventive care is covered at no out-of-pocket cost (OR = 0.422; P < 0.001; CI = 0.271–0.657). Individuals were more likely to delay/avoid nonpreventive care if they experienced greater financial toxicity (OR = 0.901; P < 0.001; CI = 0.878–0.924).

Multivariable Logistic Regression Models Examining the Effects of Financial Toxicity, Minimizer/Maximizer Tendencies, Numeracy, and Health Insurance Knowledge on Delay/Avoidance Behaviors

OR, odds ratio; CI, confidence interval. Bold indicates significance level of at least P < 0.05.

Fourteen participants did not complete financial toxicity measure; total N for this analysis was 455.

Seven participants from the nondelay group did not complete the minimizer-maximizer scale; total N for this analysis was 462.

Four participants did not complete the subjective numeracy measure; total N for this analysis was 465.

Twelve individuals were excluded from analyses with knowledge as the independent variable because they indicated they looked up responses to some items; total N for this analysis was 457.

This item was only asked if participants were insured; total N for this analysis was 405.

Discussion

This study examined the characteristics of individuals who reported delaying or avoiding health care due to cost in the last 12 months. To our knowledge, this study is one of the first to explore the role of financial toxicity and medical minimizer-maximizer tendencies as they relate to delay and avoidance of health care. Findings suggest that increased financial toxicity may lead individuals to delay or avoid both preventive and nonpreventive care. Lower health insurance knowledge, and specifically lower knowledge about preventive care coverage, may lead consumers to avoid preventive care due to perceived costs. Greater minimizing tendencies and lower subjective numeracy may relate to delaying or avoiding care due to costs. This work provides a step toward a deeper understanding of the underlying reasons individuals may be more likely to delay or avoid health care services due to costs.

In this study, many participants indicated that they delayed care due to cost, even though most were insured, consistent with previous work.12,13 Approximately 45% of respondents noted that they had delayed or avoided any care due to cost in the last 12 months, despite the fact that 86% of individuals in this sample were insured. Of respondents with insurance (N = 406), over one third did not know that their insurance covered the whole cost of a yearly checkup or well visit. Low health insurance literacy has been associated with lower knowledge about specific preventive services such as colorectal cancer screening 53 and may relate to less access to needed care. 54 Higher health insurance literacy may improve appropriate health care utilization. 17 Interactive web-based or in-person programs may be able to help educate consumers and increase their confidence using insurance to seek needed care.18,40 For example, clinical or community-based education, especially for those newly insured, may better encourage preventive care behaviors by directly addressing this knowledge gap.

Similarly, physicians and other health care professionals may be able to play a role in helping their patients learn how best to seek needed care that is also affordable. During clinical visits, members of a patient’s care team could initiate conversations with patients about payment and costs in the context of their care, in order to alleviate cost-related anxiety. Once cost enters the discussion, doctors and patients are often able to brainstorm money-saving strategies that may lower costs, 55 though these opportunities for discussion are often missed in the current health care setting. 56 Brief conversations may help providers tentatively characterize the financial situation of their patients, and thereby better integrate care needs given any financial strains that exist. This type of care that treats the patient holistically and focuses on the capacity of the patient to manage his/her health is often called “minimally disruptive medicine.” 57 It can help provide realistic treatment options tailored to the realities of patients’ lives. Conversations incorporating cost and capacity may be increasingly important for those with reduced financial or physical resources, as they are more likely to report experiencing greater disruption in care. 58 Should similar findings regarding a relationship between greater financial toxicity and delay or avoidance of care hold in a larger prospective study, they may have more complex implications that relate to the structure of our overall health care system.

Finally, an awareness of individuals’ minimizer-maximizer tendencies and numeracy skills may help inform the ways providers discuss care. For example, providers may need to carefully and appropriately emphasize when it is of the utmost importance to seek care or to adjust a care plan for those patients who appear to be health care “minimizers.” If a patient has a maximizer tendency, reassurance, decision support tools, and phone or Internet-based resources could improve the individual’s self-efficacy and chronic disease self-management and thereby help “maximizers” avoid consumption of unnecessary care. Similar communication strategies may also be important for patients with lower numeracy skills.

Lower compared to higher patient numeracy skills may lead to a lack of comprehension, appreciation of, and/or appropriate reactions to the probabilistic nature of diseases and benefits of preventive and nonpreventive treatments including risk assessment.59,60 For patients with lower numeracy skills, providers may need to emphasize what appear to be the most effective treatment plans in plain language without numerical jargon and to stress the importance of prevention. Targeted and/or tailored messaging may be particularly important for primary care and emergency care physicians, who work as the first-line providers addressing emerging problems and helping to manage chronic conditions.

These findings should be interpreted given study limitations. Preventive and nonpreventive care delay or avoidance were measured using responses to six common types of care, but these examples were not all-encompassing. The examples of preventive and nonpreventive delay/avoidance behaviors we provided may not have fully captured the services that individuals delayed or avoided. Furthermore, participants were asked if they had foregone lab work as one of the nonpreventive delay/avoidance behavior examples, but we did not distinguish between screening and diagnostic lab work. In addition, the financial toxicity measure was originally validated for cancer patients, and to our knowledge, the present research represents the first time it has been used in the context of the general population. By using a modified COST measure, our aim was to capture anxiety and distress as a result of the burden of general medical expenses. However, given that this measure was validated in the cancer patient population, the participants in our experiment may have interpreted and responded to these items differently if they were thinking about a routine office visit rather than the significant financial burdens more similar to those experienced by cancer patients. Health insurance knowledge was estimated using a measure we previously developed and tested,39,40 but it has not been formally validated. Though research has shown that MTurk may have an advantage over convenience sampling, 34 respondents were better educated, more likely to be female, and less likely to report being Hispanic than we would expect from a national sample. Finally, this work was not an exhaustive exploration of characteristics that may affect health care avoidance due to cost. Examining further characteristics may benefit policy makers who aim to ensure appropriate access to care for consumers.

Despite increased access to health insurance, patients face barriers to using their insurance to obtain needed care. Financial distress, minimizing tendencies, subjective numeracy, and varying levels of health insurance literacy are important factors influencing delay or avoidance of care. Characteristics may affect preventive or nonpreventive care utilization differently, but some, such as financial toxicity, may be predictors of delay or avoidance for both types of care. Findings underscore the continued need for education about health insurance. They can also support interventions that encourage discussion about the role that health care costs play in consumers’ health care decision making to facilitate appropriate health care seeking behaviors.

Footnotes

Funding and Support:

This research was supported in part by the 2017 Summer Research Program of the Institute for Public Health at Washington University in St. Louis, funded by the Global Health Center at the Institute for Public Health, and the Children’s Discovery Institute of Washington University and St. Louis Children’s Hospital. It was also supported in part by the Barnes Jewish Hospital Foundation and Siteman Cancer Center.

Declaration of Conflicting Interests:

MCP has a research contract (2017-2019) from Merck Sharpe & Dohme, on a topic unrelated to the content of this manuscript.