Abstract

Researchers and policymakers often suggest that housing instability harms well-being across multiple domains. But housing instability can be operationalized in various ways, and whether all forms are equally detrimental—and whether each form causes disadvantage or merely reflects it—is unknown. Using National Longitudinal Survey of Youth 1997 data, the authors advance theoretical and empirical understandings of housing instability in three ways. First, they document the prevalence and (lack of) overlap between multiple dimensions of instability. Second, using methods that carefully attend to selection, the authors investigate which forms of instability appear to affect employment, health, and family structure. Finally, they investigate disparities by race/ethnicity, gender, and class background. The findings are mixed. Some forms of instability appear consequential for some outcomes, but not all. The authors find some variation by race/ethnicity, gender, and class. They conclude that housing instability may be a mechanism of inequality, but not one that can be treated as monolithic.

As millions of Americans faced difficulty finding and affording housing during the Great Recession and the COVID-19 pandemic, researchers and policymakers focused attention on housing instability as a prominent social problem. Interest in housing as a dimension of stratification is well founded. Rates of housing instability are closely tied to existing inequalities, with lower socioeconomic status adults and adults of color at highest risk (Cox et al. 2019; Heflin 2017; Rugh and Massey 2010), and a rapidly expanding research literature has improved our understanding of the social causes of various forms of housing instability (DeLuca and Rosen 2022). Increasingly, however, scholars, policymakers, housing advocates, and journalists alike have suggested that housing instability is not only a social problem in itself but may also be a causal mechanism that further disadvantages the adults who experience it (Badger, Miller, and Parlapiano 2023; Desmond 2016; The White House 2024). Maryland Governor Wes Moore, for example, recently stated, “Housing insecurity is the number one driver of poverty in [Maryland]” (Cox 2024). How the concept of housing instability is operationalized in research varies, however. As a result, what exactly this term means in the public discourse and how much evidence there is to support claims of a causal link between housing instability experiences and subsequent well-being is unclear.

In this study, we examine whether there is plausible evidence that housing instability writ large does in fact causally shape subsequent well-being for American adults. Using data from the National Longitudinal Survey of Youth 1997 (NLSY97) for adults aged 18 to 40 years, we investigate multiple facets of housing instability. Using methods that attend to potential selection into housing instability, we examine which, if any, of these forms of housing instability appear to affect adults’ subsequent well-being across three dimensions suggested by prior qualitative research: employment, health, and family structure.

This study makes three main contributions to our understanding of the housing instability experienced by American adults. First, we explore the utility of a broad conception of “housing instability.” We document the prevalence of multiple dimensions of instability—residential mobility, feeling like one lacks a permanent residence, living in temporary accommodations, and being behind on the rent or mortgage—in a nationally representative sample of adults aged 18 to 40 years, and we consider the extent to which these measures of housing instability reflect distinct vs. overlapping experiences. We find little overlap between these measures of housing instability, underscoring the need to examine these measures individually to understand which (if any) predict future well-being.

Second, we provide evidence of the causal effects of these different forms of housing instability on adults’ outcomes across three domains: employment, health, and family structure. Although prior research focuses disproportionately on health outcomes, qualitative research suggests that housing instability may also affect employment, earnings, and child coresidence (Desmond 2016; Edin and Shaefer 2015; Western 2018). We ask whether housing instability may be consequential for multiple dimensions of adult life and how its consequences may vary across these dimensions. Moreover, although more research has examined the link between housing instability and health, much of our knowledge in this area comes from correlational studies that may not fully account for selection into housing instability. Using multiple methods and attending carefully to selection, we provide the most rigorous evidence to date of which of our four dimensions of housing instability may be causally linked to adult employment, health, and family structure.

Finally, we advance knowledge about the link between housing instability and racial, gender, and class inequality. Both race and intergenerational wealth play prominent roles in patterning housing access in the United States, and recent evidence reveals that women and men differ in their housing instability experiences as well (Hepburn, Louis, and Desmond 2020; Moses and Janosko 2019). We examine how the prevalence and potential consequences of different forms of housing instability may vary by race/ethnicity, gender, and class background to better understand the role of housing instability as a potential driver of inequality.

Defining Housing Instability

We focus on housing instability, which we define as the absence of or tenuous hold on a stable place to call home. This definition encompasses a variety of different situations, including living in temporary accommodations, making frequent moves, and being at risk for losing one’s home because of nonpayment of rent or mortgage. Housing stability plays a unique role in structuring adults’ lives; qualitative research reveals that being stably housed allows adults to create a secure “homeplace” to anchor their life and social relationships and is critical for adults’ abilities to access social programs and build economic security (Burton and Clark 2005).

To date, most research on the consequences of housing instability for adults focuses on two specific forms of housing loss: eviction and foreclosure. Eviction, foreclosure, and the threat of housing loss from eviction or foreclosure are consistently associated with worse economic and employment outcomes and physical and mental health (Fowler et al. 2015; Hatch and Yun 2021; Kahlmeter, Olof, and Brännström 2018; Murphy, Zemore, and Mulia 2014; Tsai 2015; Vasquez-Vera et al. 2017). Moreover, much of this research uses methods that adjust for selection into housing loss or exploit natural experiments, providing compelling evidence that these housing loss events have causal effects on adult well-being (Collinson et al. 2022; Desmond and Gershenson 2016; Desmond and Kimbro 2015; Desmond and Shollenberger 2015; Herkenhoff and Ohanian 2019; Humphries et al. 2019).

The robust public and academic conversation around eviction and foreclosure has advanced knowledge of these critical indicators of housing instability. However, housing loss via eviction or foreclosure reflects one specific, acute form of housing instability and represents only a small portion of the overall housing instability that adults face (Burgard, Seefeldt, and Zelner 2012; DeLuca and Rosen 2022). Moreover, as we describe later, knowledge of the potential causal impacts of other forms of housing instability remains limited. Adults may experience a range of forms of housing insecurity, and although these forms overlap somewhat, this overlap is far from perfect, with different measures capturing different populations (Cox et al. 2017). For example, housing affordability is one measure of housing instability that has received substantial attention in recent years, and one we attend to in this study, but focusing solely on this metric would miss a substantial share of the housing-unstable population (Routhier 2019). 1

We adopt a broad conception of housing instability that captures its multidimensional nature and considers how different dimensions may, or may not, vary in their impacts on adult well-being. We focus on four distinct, though potentially overlapping, measures of housing instability: residential hypermobility, feeling like you do not have a permanent residence, living in temporary accommodations such as a hotel or group home, and being late on the rent or mortgage. Although these measures, described further later, do not encompass every form that housing instability that adults can experience, they do capture multiple dimensions of housing instability, from physical instability to subjective feelings of not being permanently housed. Moreover, these measures closely align with housing instability measures currently recommended by Children’s HealthWatch and employed by Epic Systems, the largest electronic health records provider, in their social determinants of health screener (Children’s HealthWatch 2025; Epic Systems 2022; LeLaurin et al. 2023). 2 Accordingly, evaluating the strength of evidence that these various forms of housing instability directly impact subsequent well-being is of not just sociological relevance but also practical relevance for practitioners.

We document the prevalence of each of these measures in a nationally representative sample of adults and demonstrate empirically the importance of distinguishing between them. In the following section, we describe why we anticipate that these different forms of housing instability may each affect future adult well-being and how they may vary in their effects.

How Housing Instability May Affect Adult Well-Being

A large literature links housing instability to negative child outcomes across a range of domains—including academic, behavioral, and health—from early childhood into young adulthood (Clark 2018; Gold 2020; Haynie and South 2005; Mollborn, Lawrence, and Root 2018; Pribesh and Downey 1999; Vogel, Porter, and McCuddy 2017; Ziol-Guest and McKenna 2014). Many of the mechanisms through which housing instability is hypothesized to shape child well-being, like family stress or disruptions in social support networks, may also shape the well-being of adults. Yet the connection between housing instability and adult well-being remains less well understood. We examine the association between different types of housing instability and adult outcomes across three domains: employment, health, and family life. To motivate this analysis, in this section we describe three potential mechanisms that prior research suggests may contribute to these associations: increased stress levels, reduced access to resources, and changes in daily routines and relationships.

First, prior research demonstrates that residential mobility, lacking a permanent residence, living in temporary housing, and being behind on the rent or mortgage may each increase stress. Frequent moves require repeatedly finding new housing, a process that can be challenging, especially for adults with housing histories marred by instability (Desmond 2016; Harvey et al. 2019; Reosti 2021). For adults in temporary housing or who lack a permanent home, reliance on organizations, friends, or family members for housing can also be stressful (Desmond 2012a; Dordick 1997; Harvey 2022). Additionally, the financial pressure associated with falling behind on one’s rent or mortgage and the threat of housing loss that this debt entails contribute to anxiety and stress (Vasquez-Vera et al. 2017).

The stress induced by housing instability may affect adults’ health, employment, and family life. Stress can harm mental health, and, if adults turn to unhealthy behaviors such as substance use or unhealthy diets to cope with stress, it may also negatively affect physical health (Kushel and Moore 2023; Stahre et al. 2015). The stress of housing instability can negatively affect romantic and parenting relationships (Furstenberg 2014), which could result in family separation and nonresidence with one’s children. Stress may also impair work performance, resulting in decreased work hours and earnings or even job loss, or distract adults from job searches.

Second, qualitative research highlights how frequent moves and living in temporary quarters directly complicate efforts to access resources that could support employment or improve health (Desmond 2016:63, 216; Edin and Shaefer 2015:55, 100). For example, without reliable contact information and documentation of their address, housing-unstable adults may struggle to access public supports, such as libraries, which could facilitate their job search. Frequent moves or living in temporary housing can result in lost paperwork and paperwork sent to incorrect addresses, stymieing adults’ abilities to navigate administrative requirements to access public benefits, such as medical coverage. Housing instability can also be time consuming. When making frequent moves or living in temporary housing, time spent searching for housing and managing housing needs may divert time from job searches, work hours, and health-improving behaviors, such as exercise and preventive care.

Third, housing instability can disrupt adults’ daily routines and relationships, with potential implications for health, employment, and child coresidence. Frequent moves can lead adults away from their current institutional supports, such as medical facilities, and make accessing care challenging. Moves between neighborhoods also require adults to integrate themselves into a new community (Ludwig et al. 2008:154), which may affect emotional well-being and access to social support. Moreover, if moving between neighborhoods alters work commutes, tardiness and absence from work may increase.

Living in temporary or unstable residences may pose particular challenges to coresiding with children. Some shelters and temporary facilities explicitly disallow child coresidence. Additionally, parents who move frequently or live in temporary housing may choose, or be encouraged by family or child welfare authorities, to have their children live with another parent or a relative who can provide more stable, adequate housing (Dunifon 2018; Edin and Shaefer 2015:74; Pittman 2014). Research on criminal justice system involved adults finds that transitional housing and homeless shelter residence negatively affect family relationships and, particularly, the likelihood that parents coreside with their children (Laub and Sampson 2006; Western and Smith 2018).

In sum, we expect that different forms of housing instability may shape adult outcomes across multiple domains: health, employment, and family structure. Compared with employment and family structure, the association between housing instability and health is most commonly studied. Researchers have linked housing instability to poorer self-rated health (Bhat et al. 2022; Hatch and Yun 2021; Stahre et al. 2015; Yun and Hatch 2025), health care access (Duchon, Weitzman, and Shinn 1999; Kushel et al. 2006; Reid, Vittinghoff, and Kushel 2008), lower birth weight among pregnant mothers (Carrion et al. 2015), insufficient sleep (Liu et al. 2014), poorer health behaviors (German, Davey, and Latkin 2007; Margolis et al. 2006; Murphy et al. 2014; Stahre et al. 2015), and greater incidence of depression and anxiety (Bossarte et al. 2013; Davey-Rothwell, German, and Latkin 2008; Suglia, Duarte, and Sandel 2011). However, because more disadvantaged individuals are more likely to experience housing instability, it remains unclear whether the associations between housing instability and negative outcomes are causal or merely correlational (Garboden, Leventhal, and Newman 2017). Some evidence suggests a causal relationship with health outcomes. Clark, Kusunoki, and Barber (2022) used individual fixed effects in a sample of women aged 18 to 19 years in Michigan to show that frequent moves are negatively associated with contraceptive use. Likewise, multiple studies find that some measures of housing instability are associated with worse health outcomes, even after controlling for previous health (Bhat et al. 2022; Burgard et al. 2012).

We extend prior research by examining whether there is evidence that housing instability has plausibly causal effects on adults’ future well-being across multiple domains. As described earlier, there is strong reason to expect causal effects of housing instability on adult well-being, but much of this evidence stems from qualitative studies, studies of particular populations such as formerly incarcerated adults, or correlational studies. We extend this research by using a nationally representative sample of adults and multiple methods to explore the evidence for a causal relationship between different forms of housing instability and adult health, employment, and child nonresidence, net of selection into housing instability. We also explore how the relationship between housing instability and adult outcomes varies depending on the measure of instability used and the specific outcome examined.

Differences by Class Background, Race and Ethnicity, and Gender

Given the strong link in the United States between parents’ socioeconomic status and their children’s life outcomes (Ermisch, Jantti, and Smeeding 2012), we expect disparities in housing instability by class background. Class background may also structure whether and how housing instability affects other forms of well-being. Economically advantaged support networks may help adults weather periods of housing instability; for example, well-off kin could help adults reestablish housing stability quickly or provide financial and other supports to mitigate any negative effects of housing instability (Schmidt 2025). Previous research demonstrates that extended family resources affect adults’ housing outcomes (Hall and Crowder 2011; Sharp, Whitehead, and Hall 2020).

Racial discrimination, past and present, has produced large disparities in housing access, leaving Black and Hispanic households uniquely vulnerable to housing instability (Desmond 2012b; Goetz 2013; Korver-Glenn 2021; Rugh and Massey 2010). Compared with White households, Black and Hispanic households have higher scores on composite indices of housing instability (Bhat et al. 2022; Cox et al. 2017) and disproportionately experience many forms of housing instability, including eviction (Desmond 2012b), foreclosure (Hall, Crowder, and Spring 2015), homelessness 3 (Olivet et al. 2021), residential mobility (Ihrke and Faber 2012), and falling behind on housing bills (Heflin 2017; Sharp and Hall 2014). Given these disparities, a link between housing instability and adult well-being could reinforce existing racial inequalities.

There is also reason to suspect the effects of housing instability may vary by race and ethnicity, though which groups should be most disadvantaged remains an open question. Housing discrimination (Pager and Shepherd 2008) could exacerbate the challenges of housing instability. For example, Black and Hispanic adults experiencing frequent moves might move between higher poverty neighborhoods and have fewer housing options open to them than their White counterparts, which may worsen the impacts of housing instability. On the other hand, if Black or Hispanic adults tend to experience more disadvantageous housing in general than White adults, the added disadvantage of housing instability may have a relatively smaller effect (see Fomby and Cherlin 2007). Compared with White adults, Black and Hispanic adults face heightened risk for many housing and neighborhood disadvantages, from lead exposure to neighborhood disinvestment and violence (Muller, Sampson, and Winter 2018; Sharkey 2013), conditions that could obscure the harms of housing instability.

Variation in kin support may also contribute to differential effects of housing instability. Compared with their White counterparts, economically vulnerable Black adults are less likely to have access to financial support from extended family (Heflin and Pattillo 2006; Sarkisian and Gerstel 2004). The absence of financial support from better off kin could leave them vulnerable to negative effects from housing instability. In contrast, Black and Hispanic families may have greater access to nonfinancial support, including a temporary place to stay and transportation (Hogan, Hao, and Parish 1990; Sarkisian and Gerstel 2004). Such in-kind support could lessen the harms of housing instability for Black and Hispanic adults compared with White adults.

Studies examining how the association between housing instability and adult well-being varies by race have produced mixed results. Using National Longitudinal Study of Adolescent to Adult Health data, Hatch and Yun (2021) found a stronger initial negative association between eviction and health for White adults than non-White adults but a stronger long-term association for non-White adults. Using data from the Midlife in the United States study, Bhat et al. (2022) found a stronger association between housing instability and chronic health conditions for Black adults than White adults. Stein, Le, and Gelberg (2000) found that homeless Black women in Los Angeles report worse birth outcomes than their White or Hispanic counterparts. We build on this literature by asking how the association between different measures of housing instability and health, employment, and family outcomes may differ for White, Black, and Hispanic adults in a nationally representative sample. Understanding variation in these associations is key to unpacking housing instability as a mechanism of racial inequality.

Prior evidence suggests that men and women also differ in their experiences of housing instability. For instance, men make up a majority of the homeless population (Moses and Janosko 2019), but women disproportionately experience eviction and are more exposed to risky mortgage lending that leaves them vulnerable to foreclosure (Baker 2014; Hepburn et al. 2020). We extend this research by asking how adult women and men differ in their exposure to different forms of housing instability.

In addition to potential gender differences in rates of housing instability, the impacts of housing instability may also vary by gender. For example, some evidence suggests that residential mobility is more negatively associated with psychological well-being for women than men (Davey-Rothwell et al. 2008; Magdol 2002). These differences may stem from women’s disproportionate burdens from housework and childcare, which may compound the stress of moving, as well as gender differences in vulnerability to move-related stress (Magdol 2002). If women experience greater stress from other forms of housing instability, lacking a permanent residence, living in temporary housing, and falling behind on housing bills may also negatively affect women more than men. These associations may not only be stronger for health, but also for employment and family outcomes, which can likewise be affected by stress.

On the other hand, the association between housing instability and child noncoresidence may be weaker for women than for men. Because mothers are more likely to be custodial parents, fathers’ coresidence may depend more on their ability to maintain a positive relationship with the child’s mother, which may be negatively affected by the stress and uncertainty of housing instability. Moreover, some forms of temporary housing, such as emergency shelters, more often accommodate mothers with coresident children than fathers, meaning that women may be more able than men to maintain coresidence with minor children during periods of housing instability.

Data

We use data from the NLSY97, which surveyed a nationally representative sample of 8,984 12- to 16-year-olds living in the United States in 1997. Respondents were interviewed annually from 1997 through 2011 and biennially after. We use data through the 2019 survey year, when respondents were aged 34 to 40 years. 4 In our sample, we include all respondent waves when respondents were 18 years or older, a total of 119,030 person-years from 8,841 respondents. During the earlier years of adulthood that are captured by our data (18-40 years), adults are particularly vulnerable to housing instability; for instance, at these ages, migration rates are higher (Benetsky, Burd, and Rapino 2015), and adults are more likely to be renters, a status associated with higher risk for housing unaffordability (Joint Center for Housing Studies 2024). Because residential mobility peaks around 23 years of age (Benetsky et al. 2015), we also ran all analyses on person-years in which respondents are 25 to 40 years old and found that these models reproduce all the significant results shown in Tables 4 to 7.

Measures of Housing Instability

The NLSY97 data allow us to examine four time-varying measures of housing instability. First, we consider residential mobility using an annualized measure of the number of different addresses at which the respondent reports living for at least one month since their last interview, adjusted for the amount of time that has passed between survey dates. Because the reasons for residential mobility vary and a single move may not indicate the lack of a stable home (Garboden et al. 2017), we focus on experiences of hypermobility, as frequent moves may be destabilizing and harmful to adult well-being. Informed by previous research (Cutts et al. 2011; Murdoch et al. 2022; Sandel et al. 2018), we consider individuals who moved two or more times in the prior year (the top 4th percentile in our sample) to be hypermobile. 5 Second, our measure of having no permanent residence provides novel insight into respondents’ self-perceptions of unstable housing. We create this measure from respondents’ answers to two questions asking whether they consider their current place of residence (regardless of type) to be temporary or permanent and, if temporary, whether they have some other place that they consider their permanent residence. This variable is set equal to one if a respondent indicates that they consider neither their current place of residence nor any other to be their permanent residence. Third, a binary variable indicates whether the individual currently lives in temporary housing—on the street or in a hotel, a motel, a boarding house, an emergency shelter, a rehabilitation facility or group home, or a hospital—on the date of their interview. Finally, we capture housing unaffordability with a binary variable indicating whether the respondent reports having been late on their rent or mortgage by more than 60 days in the past 12 months.

Outcome Measures

We consider four outcome measures, which capture adult well-being in different domains. Our first outcome is the number of weeks the adult was employed in the last calendar year. Our second is labor income (total wages and salary) in the prior calendar year, adjusted for inflation to 2018 dollars. Our third outcome is child noncoresidence. This measure takes on a value of 1 if the adult has biological minor children who live outside their household and a value of 0 if not. 6 Our final outcome is an indicator for poor health, created from an ordinal measure of self-reported general health on a five-point scale. This measure takes on a value of 1 for individuals who rated their general health as “poor” (1.02 percent of responses) or “fair” (9.36 percent of responses) at the date of interview and 0 for those who rated their health as “good,” “very good,” or “excellent.” 7

Methods

We use individual fixed-effect models to estimate within-adult change in each outcome over time. We use ordinary least squares (OLS) to predict weeks employed and income and logit models to predict child noncoresidence and poor self-rated health. Our fixed-effect models estimate how changes in housing instability status are associated with changes in each outcome. Because each adult serves as their own control, fixed-effect models eliminate potential confounding from time-invariant characteristics that vary between adults. Therefore, we do not control for fixed characteristics such as race or gender. To examine whether the effects of housing instability may vary across groups, we also run fixed-effect models separately by race/ethnicity (White, Black, and Hispanic), gender, and parental education level (whether either of the respondents’ residential parents or guardians completed more than 12th grade as of the 1997 survey), using postestimation tests to determine whether coefficients differ significantly across groups. To avoid the pitfalls of comparing logit coefficients across models (Mood 2010), we use OLS models for all outcomes when making subgroup comparisons.

In our fixed-effect models, we control for time-varying characteristics that are associated with both housing instability and our outcomes of interest. In all models we control for age, highest degree completed, current student status, history of criminal justice system interaction (conviction history, incarceration history, and current incarceration), disability status, hard drug use, marital status, whether the respondent has any biological minor children, urban residence, and region of residence. Age is operationalized with a series of indicator variables, one for each age (18-40 years) reflected in our sample. Educational attainment is captured by highest degree completed to date: no diploma or degree (reference), high school diploma, some college, college degree, or graduate or professional degree. We include an indicator to identify current students. Criminal justice system history is captured with time-varying indicators for whether a respondent has ever been convicted of a crime, has ever been incarcerated, or is currently incarcerated at the interview date. Disability is captured by an indicator set equal to one if respondents indicate that their health limits their ability to work or the amount of work they can do. Hard drug use is operationalized as a dummy variable set equal to one if the respondent reports that they used any drug or substance (other than alcohol or marijuana) not prescribed by a doctor to get high or achieve an altered state since the last interview. Parent status is captured by an indicator identifying respondents with at least one biological minor child. We also control for census region of residence (Northeast, North Central, South, or Midwest) and whether the respondent is living in a census-designated urban area.

In models of child noncoresidence and poor self-rated health, we also control for current labor income, and in models predicting child noncoresidence, we control for child age with a set of variables indicating whether the respondent has any biological children aged 0 to 5, 6 to 10, or 11 to 17 years at the date of each interview. We use multiple imputation for item-specific missingness on control variables, but we do not impute missing values for outcome or housing instability measures. 8 Descriptive statistics for our outcome and control variables are shown in Table A1 in the Appendix.

Because housing instability may be both a cause and a consequence of each well-being measure we consider, each model includes a one-period lagged version of the housing instability measure, reflecting the respondents’ housing instability experiences in the period preceding the year in which outcomes are measured, and a one-period lead version of the housing instability measure, reflecting the respondents’ housing instability experiences in the period following the year in which outcomes are measured. We use the lagged and lead versions of our housing instability measures to think through the causal ordering of the relationship between housing instability and other forms of well-being.

Because some housing instability and outcome variables are measured at the date of the current interview (i.e., no permanent residence, temporary housing, child noncoresidence, poor health), while others reflect experiences over the past 12 months (i.e., residential mobility, housing unaffordability, labor income, weeks employed), the inclusion of lagged housing instability variables ensures that models always include measures of housing instability experiences that occurred prior to measurement of the outcome variable. 9 We focus our results discussion on the coefficients on housing measures that precede outcome variable measurement.

Our inclusion of lead measures of housing instability, on the other hand, allows us to test whether future housing instability is significantly associated with present outcomes. If so, that may suggest either that the outcome in question shapes future housing instability independent of fixed individual characteristics and the time-varying controls included in the model (e.g., a decline in health may affect ability to pay the rent or mortgage on time) or that some unobserved time-varying confounder may drive the relationship between housing instability and the outcome being considered. As such, the inclusion of lead measures of housing instability can be thought of as akin to a placebo test.

As in other observational studies, the validity of our fixed-effect models depends on the assumption that our control variables capture all time-varying differences between housing-unstable and housing-stable adults that are relevant to the outcome of interest. We attend to this assumption with our inclusion of lead measures of housing instability and robustness checks to examine the percentage bias that would invalidate our results, but potential time-varying confounding remains a threat to causal inference.

Results

Descriptive Results

Table 1 describes the prevalence of each measure of housing instability. The top panel reveals that 4.33 percent of young adults moved two or more times in the past year, with White non-Hispanic adults reporting hypermobility most often (4.75 percent) and Hispanic adults least often (3.28 percent). This finding is consistent with prior research showing greater levels of residential mobility among White American households (Evans and Chapman 2024; Mateyka 2015). Women have a higher rate of hypermobility (4.60 percent) than men (4.07 percent), and adults whose parents completed some higher education have higher rates (4.64 percent) than adults whose parents completed high school or less (3.98 percent).

Prevalence of Housing Instability.

Note: Analyses are weighted to be representative of the cohort of 12- to 17-year-olds living in the United States in 1997. The National Longitudinal Survey of Youth 1997 has asked respondents about being late on the mortgage or rent only since 2007. HS = high school.

About 1.17 percent of young adults feel that they have no permanent residence, and 0.43 percent are living in temporary housing. Black non-Hispanic adults have the highest rates of not having a permanent residence (1.74 percent) and living in temporary housing (0.53 percent), and White and Hispanic adults have lower rates (1.07 percent lack a permanent residence and 0.36 percent and 0.46 percent, respectively, live in temporary housing). Men are more likely to lack a permanent residence than women (1.54 percent vs. 0.79 percent) and are somewhat more likely to live in temporary housing (0.45 percent vs. 0.41 percent). Adults whose parents had no more than a high school education have higher rates of not having a permanent residence (1.39 percent) and living in temporary housing (0.47 percent) than adults whose parents completed more education (0.94 percent, 0.37 percent).

On our measure of housing unaffordability, being more than 60 days late on the rent or mortgage sometime in the past year, Black adults again report the highest prevalence (3.00 percent), followed by Hispanic (2.31 percent) and White adults (2.22 percent). Unlike other measures of housing instability, women report higher rates of housing unaffordability (2.71 percent) than men (1.92 percent). Adults whose parents completed no more than high school have higher rates of housing unaffordability (2.86 percent) than adults whose parents completed more education (1.79 percent).

Although each measure of housing instability is relatively rare on an annual basis, the bottom panel of Table 1 indicates that the cumulative prevalence of each of these experiences across all years from age 18 through 2019 (when young adults were aged 34–40 years) is far higher. Looking at the number of times an adult experienced each form of housing instability, conditional on experiencing it once, we see that the median young adult who experiences each form of housing insecurity experiences it just once over this period, but the mean number is higher, showing that a minority of young adults experience repeated occurrences.

By 2019, 36.02 percent of young adults have experienced two or moves within a year, with White adults reporting the highest rates (38.45 percent), followed by Black adults (31.84 percent) and Hispanic adults (29.26 percent). Among adults who ever experience hypermobility, White adults report a greater mean number of hypermobility experiences (1.64) than Black and Hispanic adults (1.50 for both). A greater share of women (37.85 percent) than men (34.33 percent) ever experience hypermobility, and women who experience hypermobility experience it somewhat more often (1.65 times) compared with men who experience hypermobility (1.55 times). Finally, adults whose parents completed no more than high school were less likely to ever experience hypermobility (32.84 percent) than those whose parents had more education (38.95 percent), but there is little difference in the average frequency of hypermobility among those who experienced it.

By 2019, nearly one in nine young adults has identified themselves as having no permanent residence during in at least one interview since turning 18. Black adults have the highest rates of having ever lacked a permanent residence (13.96 percent), compared with Hispanic (10.40 percent), and White (9.94 percent) adults. Black adults who ever report having no permanent residence do so an average of 1.53 times, compared with just 1.26 times for White adults and 1.22 times for Hispanic adults. About 12.68 percent of men have lacked a permanent residence, compared with 8.32 percent of women, and men who lack a permanent residence report this state an average of 1.41 times, compared with 1.15 times for women. Among adults whose parents completed high school or less, 12.08 percent have ever been without a permanent residence, but just 8.88 percent of adults whose parents completed more education have. Likewise, among adults who ever report having no permanent residence, adults whose parents completed more than high school reported having no permanent residence more frequently on average (1.36 times) than adults whose parents have less education (1.26 times).

Temporary housing residence remains the least common form of housing instability; just 4.04 percent of respondents lived in temporary housing (at the time of their survey) at some point by 2019. Black adults are most likely to have lived in a temporary residence (5.70 percent) and White adults the least (3.55 percent). However, Hispanic adults who ever live in temporary housing do so an average of 1.46 times, more than either their White (1.36 times) or Black (1.30 times) counterparts. Men are more likely to have been observed in a temporary residence (4.36 percent) than women (3.71 percent), but women who ever experience temporary housing do so more times on average than men (1.48 vs. 1.36 times). Similarly, adults whose parents completed high school or less are more likely to have ever lived in temporary housing (4.56 percent) than adults whose parents completed more education (3.38 percent), but conditional on having ever lived in temporary housing, they experience this state fewer times on average (1.37 times) than adults whose parents have higher levels of education (1.48 times).

The cumulative prevalence of housing unaffordability is higher; 11.48 percent of all adults have reported being late on the mortgage or rent at least once by 2019. Again, Black adults report this most often (16.29 percent) and White adults least often (10.74 percent), though we see relatively little variation by race/ethnicity in the mean number of reports of late rent or mortgage among those who have ever been late. A greater share of women has ever been late on the rent or mortgage (13.19 percent) than men (9.87 percent). Women also report a higher mean number of years with late rent or mortgage (1.53 years) than men (1.39 years), conditional on ever being late. Adults whose parents completed high school or less are also more likely to have ever been late on the rent or mortgage (14.15 percent) than adults whose parents completed more education (9.05 percent), though there is little difference in the mean number of years that an adult reports being late on the mortgage or rent conditional on ever being late.

Notably, correlations between the four different housing instability measures we consider are quite low (see Table 2). Temporary housing and no permanent residence are the most highly correlated, with a correlation coefficient of just 0.0774 across all person-years in which respondents are 18 years or older. Moreover, Cronbach’s α coefficient for a scale measure created from these four variables is just 0.1058, further emphasizing how little overlap there is between these point-in-time measures of housing instability.

Correlations between Housing Instability Measures, across All Person-Years Age 18 Years and Older.

If we instead consider individuals’ cumulative housing instability experiences across all survey years, we see some increase in both the interitem correlations and Cronbach’s α coefficient, but correlations remain relatively weak, ranging from 0.0197 to 0.1597 (Table 3). The strongest correlation is between hypermobility and ever living in temporary housing (r = 0.1597). Compared with Cronbach’s α coefficient for our point-in-time measures, Cronbach’s α coefficient for these four cumulative versions of our housing instability measures is higher but still only 0.2972. The increase in correlation when considering cumulative versions of our four housing instability measures suggests that individuals may experience different forms of housing instability at different points in time. However, the correlations remain modest even across years, indicating that it is generally not the same individuals experiencing all of these differing dimensions of housing instability.

Correlations between Cumulative Housing Instability Experiences by 2019.

Fixed-Effect Models

Tables 4 to 7 report the results from fixed-effect models of our four outcome measures, with each table using a different measure of housing instability to predict these outcomes. To help readers distinguish which coefficients are measured temporally prior to outcome variables, we have highlighted in black boxes the coefficients on housing measures that precede outcome variable measurement in Tables 4 to 7. We focus our interpretation primarily on these coefficients, but we also briefly discuss the relationships we observe between current measures of well-being and subsequent housing instability.

Individual Fixed-Effects Models: Hypermobility (Two or More Moves in Past Year).

Note: Primary coefficients of interest are highlighted in black boxes. Labor income and weeks employed in the past year are modeled using OLS, while noncoresident children and poor health are modeled using logistic regression. Values in parentheses are standard errors. Coefficients are not shown for age, highest degree completed, current student status, conviction history, incarceration history, current incarceration, disability, hard drug use, marital status, parent status, urban residence, region of residence, labor income in the past year (for models of noncoresident children and health), and child ages (for model of noncoresident children). OLS = ordinary least squares.

p < .10. *p < .05. **p < .01. ***p < .001.

Individual Fixed-Effects Models: No Permanent Residence.

Note: Primary coefficients of interest are highlighted in black boxes. Labor income and weeks employed in the past year are modeled using OLS, while noncoresident children and poor health are modeled using logistic regression. Values in parentheses are standard errors. Coefficients are not shown for age, highest degree completed, current student status, conviction history, incarceration history, current incarceration, disability, hard drug use, marital status, parent status, urban residence, region of residence, labor income in the past year (for models of noncoresident children and health), and child ages (for model of noncoresident children). OLS = ordinary least squares.

p < .05. ***p < .001.

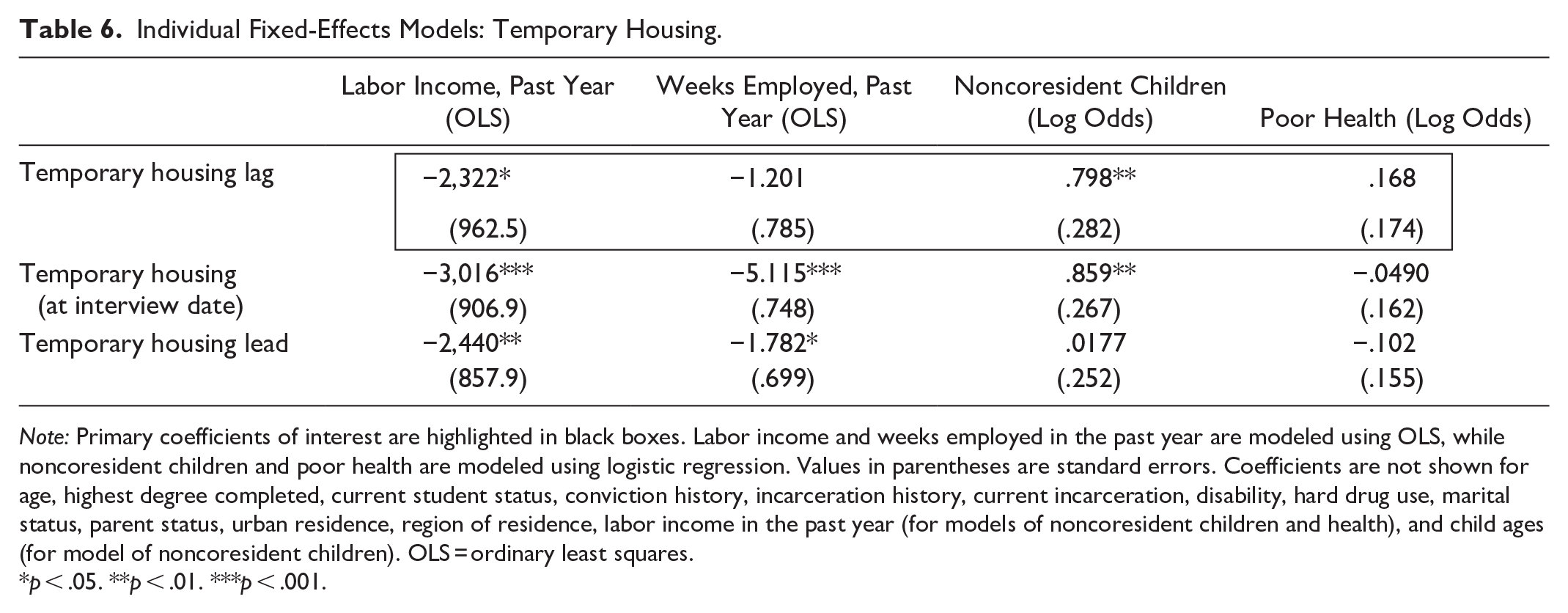

Individual Fixed-Effects Models: Temporary Housing.

Note: Primary coefficients of interest are highlighted in black boxes. Labor income and weeks employed in the past year are modeled using OLS, while noncoresident children and poor health are modeled using logistic regression. Values in parentheses are standard errors. Coefficients are not shown for age, highest degree completed, current student status, conviction history, incarceration history, current incarceration, disability, hard drug use, marital status, parent status, urban residence, region of residence, labor income in the past year (for models of noncoresident children and health), and child ages (for model of noncoresident children). OLS = ordinary least squares.

p < .05. **p < .01. ***p < .001.

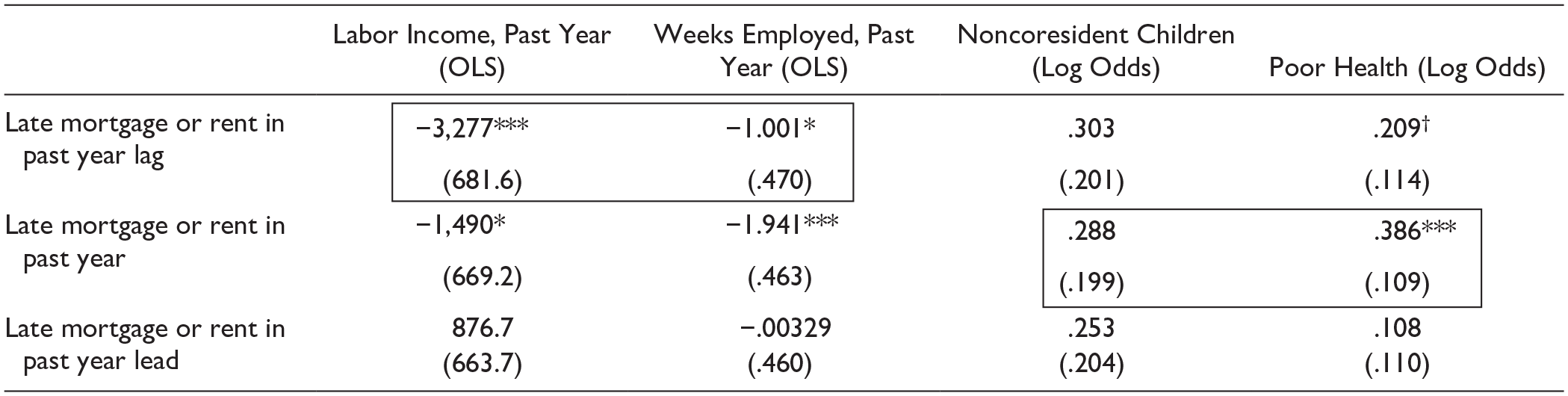

Individual Fixed-Effects Models: Mortgage or Rent >60 Days Late in Past Year.

Note: Primary coefficients of interest are highlighted in black boxes. Labor income and weeks employed in the past year are modeled using OLS, while noncoresident children and poor health are modeled using logistic regression. Values in parentheses are standard errors. Coefficients are not shown for age, highest degree completed, current student status, conviction history, incarceration history, current incarceration, disability, hard drug use, marital status, parent status, urban residence, region of residence, labor income in the past year (for models of noncoresident children and health), and child ages (for model of noncoresident children). OLS = ordinary least squares.

p < .10. *p < .05. ***p < .001.

Table 4 reports the results from models examining the relationship between hypermobility and our adult well-being outcomes. We find that hypermobility, defined as two or more moves in the past year, is significantly associated with lower income, fewer weeks of employment, and child noncoresidence, but has no statistically significant relationship with poor health. 10 Income is lower by $1,094 and adults work about half a week less, on average, in the year after they report making two or more moves. For child noncoresidence, hypermobility in the prior year is associated with 42 percent higher odds of living apart from your biological minor child (e0.347 = 1.415).

We also ran models using alternative versions of our hypermobility measure that used >1 move or ≥90th percentile (1.2 moves) in the past year as the threshold for defining hypermobility. Results are largely consistent between models using these three different thresholds for defining hypermobility. Coefficient magnitudes almost universally increase as the number of moves used to define hypermobility increases, and standard errors uniformly increase as the number of respondents falling into the hypermobile category decreases. Accordingly, there is some slight variation in statistical significance levels of coefficients across different hypermobility thresholds and outcomes, but results are substantively consistent across the three operationalizations of hypermobility.

Table 5 shows that not having a permanent residence is significantly associated with fewer weeks of employment but does not have a significant association with income, odds of residing separately from biological minor children, or poor health in the following year. Adults work about three fewer weeks, on average, in the year after they report having no permanent residence.

Table 6 displays results from models that include temporary housing residence. We find that temporary housing is significantly predictive of subsequent income and noncoresidence with biological children. Income is lower by $2,322 on average in the survey year following temporary residence. The odds of noncoresidence with one’s children are more than twice as large in the survey year following temporary housing residence (e0.798 = 2.221). Perhaps unsurprisingly, current income and weeks of employment are negatively associated with future temporary housing residence.

Finally, Table 7 displays results from models that incorporate the housing unaffordability measure. The results indicate that having been late on the rent or mortgage payments in the past year has a significant association with income and weeks worked in the next year, as well as poor self-rated health. Having been late on the mortgage or rent is associated with a decrease of $3,277 in income and one fewer week worked in the following year and is associated with a 47 percent increase in the odds of having poor health (e0.386 = 1.471).

Looking across Tables 4 to 7, we see that each of our measures of housing instability is predictive of poorer labor market outcomes in the subsequent period, but only hypermobility and housing unaffordability are associated with decreases in both income and weeks employed. The likelihood of not residing with one’s biological children, on the other hand, only increases following hypermobility and living in temporary housing. Finally, being late on one’s mortgage or rent is the only measure that is significantly predictive of worse health in the following period. 11

We also see some evidence of the circularity of these relationships, particularly in the relationship between housing instability and labor market outcomes. Hypermobility in the past year (Table 4), being late on a mortgage or rent payment in the past year (Table 7), and living in temporary housing at the interview date (Table 6) are significantly and negatively associated with both income and weeks worked in the past year, but the causal ordering (if any) is unclear given that these are all measured contemporaneously. Likewise, lacking a permanent residence and living in temporary housing at the interview date are each associated with child noncoresidence in the same wave, and lacking a permanent residence is associated with increased odds of being in poor health in the same wave.

The only housing instability indicator with significant lead coefficients across multiple outcomes is temporary housing: income and employment are both significantly and negatively associated with future temporary housing (Table 6), suggesting that employment-related shocks may increase the likelihood of subsequent temporary housing residence. With the exception of weeks employed and hypermobility in the subsequent year, the lead coefficients of other housing instability measures are not statistically significant, which suggests that the relationships between prior housing instability and current well-being in other models are not primarily driven by some unobserved time-varying confounder.

Race-Specific Models

Next, we discuss the results of race-specific fixed-effect models, which follow the same model specifications as in Tables 4 to 7 but are run separately by race/ethnicity. Tables A2 to A5 in Appendix I display coefficients on measures of each form of housing instability measured prior to the outcome. We focus our discussion on statistically significant differences in the coefficients across the race-stratified models, identified using postestimation tests.

Table A2 indicates that hypermobility, living in temporary housing, and late mortgage or rent payments are predictive of lower labor market income for all racial/ethnic groups. Although the precise magnitude and significance of these associations vary, postestimation tests reveal that the differences between these coefficients are not statistically significant. 12

Although temporary housing did not appear predictive of weeks employed over the subsequent year in Table 6, Table A3 indicates that living in temporary housing is associated with working 3.4 weeks fewer for White adults (p < .01). In contrast, late mortgage or rent payment has a significant negative association with weeks employed for Black adults but not White adults, 13 and the coefficient in the model for Black adults is more than twice as large as it was in the pooled-race fixed-effects model (Table 7). Mirroring the main results in Tables 4 and 5, both hypermobility and having no permanent residence are negatively associated with weeks worked for all racial/ethnic groups, and these coefficients are not significantly different from one another.

Table A4 indicates that hypermobility and temporary housing are both associated with lower probability of residing with one’s minor children across races, as they were in the main models in Tables 4 and 6, although there is again variation in the exact magnitude and significance of these associations. 14 Although hypermobility is associated with significantly lower probability of residing with one’s biological children in the following year for both Black and White respondents, the relationship is about three times stronger for Black adults than White adults (difference significant at p < .10). Additionally, although the association between having no permanent residence and child noncoresidence was not significant in the race-pooled models (Table 5), this association is significant and positive for in the model for Hispanic adults only.

Finally, Table A5 shows that having been late on the mortgage or rent in the prior year is associated with an increase in the probability of poor health in the next year across races/ethnicities, with no statistically significant differences in the coefficients across the race-stratified models. 15 Additionally, the relationship between temporary housing and health was not significant in the pooled model (Table 6), but the race-stratified models show that temporary housing is predictive of poor health for Hispanic adults, but not Black or White adults.

Overall, housing instability appears to be consequential for subsequent well-being across racial and ethnic groups, but we find some evidence that these impacts may vary. The effects of temporary housing on employment appear greatest for White adults, the effects of late mortgage or rent payment on employment appear to be greater for Black adults than White adults, and Hispanic adults seem to be uniquely disadvantaged in the association between not having a permanent residence and subsequent child noncoresidence and the association between temporary housing and subsequent poor health. No single racial/ethnic group appears to be consistently more disadvantaged by housing instability, however.

Gender-Specific Models

The gender-specific fixed-effect models suggest that many of the labor market consequences of housing instability may be larger for men (Tables A6 and A7 in Appendix II). Being late on the mortgage or rent, for example, is associated with lower income for both men and women in the following year, but the relationship magnitude is more than three times larger for men. Likewise, having no permanent residence predicts fewer weeks worked for both men and women (although this association is not significant for women), but the coefficient is nearly four times as large for men. Other differences between men and women are not statistically significant but are suggestive of potentially larger housing instability consequences for men. For example, gender-specific models reveal a significant relationship between having no permanent residence and subsequent income for men (p < 0.1), with men earning $1,355 less on average in the period after they report having no permanent residence, despite there being no significant relationship between no permanent residence and income in the pooled model. Similarly, hypermobility is associated with fewer weeks worked for men and women, but the association is only significant for men.

Gender-specific models of biological child noncoresidence, on the other hand, provide some evidence that the consequences of housing instability may be more pronounced for women (Table A8). Hypermobility is positively and significantly associated with child noncoresidence in the next wave for both men and women, but the coefficient on temporary housing is more than three times larger for women compared with men (difference significant at p < 0.01), and the relationship is statistically insignificant for men. Likewise, late mortgage or rent payment is associated with an increase in the probability of living apart from one’s biological child(ren) in the subsequent survey wave only for women, though the difference in the coefficients for men versus women is not significant.

Finally, gender-specific models of poor health reveal that temporary housing, which had not been predictive of subsequent wave health in the pooled models, is associated with higher odds of poor health for men, but not for women (Table A9). These models reveal no other significant differences by gender, however.

Class-Stratified Models

The class-stratified fixed-effect models (Appendix III) suggest that the effects of different forms of housing instability vary by parents’ educational attainment, but the group most disadvantaged varies by form of housing instability and outcome. Adults whose parents had more than a high school education appear more disadvantaged in labor market outcomes (Tables A10 and A11), potentially reflecting their generally greater advantage in the absence of housing instability. The coefficient on hypermobility in the model of labor income is more than five times larger and only significant for adults whose parents had more than a high school education. Likewise, the coefficient on temporary housing in the model of weeks employed is negative and significant only for adults whose parents have higher levels of education. Although there is variation in the magnitude and significance of other coefficients related to labor market outcomes on the basis of parents’ education level, these differences are not statistically significant.

For child noncoresidence, we see evidence that adults whose parents have lower levels of education may be more disadvantaged by housing instability (Table A12). Hypermobility and late mortgage or rent payment each only have significant relationships with child noncoresidence for adults whose parents completed high school or less, and these coefficients are significantly different than those for adults whose parents completed more than high school. In contrast, hypermobility is only predictive of poor health for adults whose parents have higher levels of education (Table A13).

Robustness Checks

We also ran models that predict each outcome weighted by inverse probability of treatment weights (IPTW) (Appendix IV). These weights give more (or less) weight to adults whose characteristics make them less (or more) likely to experience housing instability. The IPTW approach seeks to address potential confounding by creating a pseudopopulation in which housing instability is independent of prior characteristics. It is an increasingly common method of estimating plausibly causal effects (e.g., Levy 2022), though it is subject to standard caveats about no unobserved confounders. All significant results shown in Tables 4 to 7 hold in the IPTW models (Table A14) except for the significant association between late mortgage or rent payment and weeks employed (Table 7).

As an additional robustness check, we use the konfound package in Stata to quantify the percentage bias necessary to invalidate inferences from a Rubin causal model framework (Xu et al. 2019) (Appendix V). These sensitivity analyses reveal what proportion of observed cases would need to be replaced with cases for which there is an effect of 0 to invalidate the statistically significant relationships of interest shown in Tables 4 to 7. Tables A15 to A18 display the threshold for the minimum percent of the estimate that would have to be attributable to bias to invalidate the estimates for the primary coefficients of interest (i.e., those highlighted in black boxes) in Tables 4 to 7.

The sensitivity analysis reveals that more than 33 percent of the estimate would need to be attributable to bias to invalidate most of the significant findings from Tables 4 to 7. The relationships most susceptible to bias are those between temporary housing and income (19 percent of the estimate would need to be attributable to bias to invalidate the inference) and late mortgage or rent payment and weeks worked (8 percent of the estimate would need to be due to bias to invalidate the inference).

Finally, we ran Granger (1969) causality test models in which we include lagged outcome variable measures that precede measurement of the lagged housing instability measures. Granger causality posits that if past values of x are significant predictors of y even when past values of the y have been included in the model, then x exerts a causal influence on y. Most of the significant findings we present in Tables 4 to 7 hold when we use a Granger causality test approach. However, these robustness checks suggest that our findings related to labor market outcomes may be less reliable: weeks employed is not significantly associated with hypermobility or no permanent residence, and income is not significantly associated with temporary housing residence when we use Granger causality test models. These latter two findings were also ones highlighted as less robust by our sensitivity analysis.

Conclusion

This research adds new evidence to the growing public conversation around housing instability. We broaden the conversation beyond eviction and housing affordability by creating nationally representative estimates of the scale of exposure to various forms of housing instability. Although housing instability is relatively rare on an annual basis, its cumulative prevalence over early adulthood is striking. Since turning 18, about 11 percent of young adults have felt as if they do not have a permanent residence, and more than 12 percent have been more than 60 days late on their rent or mortgage.

Our descriptive results underscore the sharp disparities in housing instability by race and ethnicity; Black adults are far more likely than White adults to feel that they lack a permanent residence, live in temporary housing, and be late on their rent or mortgage, on both an annual basis and cumulatively across young adulthood. We also find large disparities by class background, with adults whose parents completed high school or less having higher rates of these forms of housing instability than adults whose parents completed more education. These disparities are striking but perhaps unsurprising given the role of race, class, and the intersection of the two in structuring housing opportunities in the United States (Hall and Crowder 2011; Korver-Glenn 2018; Pais 2017). Additionally, we find that women and men often experience different types of housing instability. Men have higher rates of feeling they lack a permanent residence, while women have higher rates of falling behind on the rent or mortgage.

Understanding whether the relationship between housing instability and other forms of well-being is causal or merely correlational is of crucial importance for correctly identifying contemporary drivers of inequality in the United States. We meaningfully advance this literature by carefully testing for evidence of a causal relationship between various forms of housing instability and multiple measures of adult well-being in a nationally representative sample. We interrogated the strength of these potentially causal relationships using a variety of methods, including individual fixed-effect models with lagged and lead measures of housing insecurity, inverse probability of treatment weighted models, sensitivity analyses, and Granger causality tests.

We find that the answer to the question of whether housing instability appears to influence subsequent adult well-being depends in large part on what type of housing insecurity and form of well-being are considered. We find strong evidence that a consistent residence serves as a foundation for family stability. Residential mobility and living in temporary arrangements, such as shelters or group homes, each predict subsequent child noncoresidence. This finding is consistent with our expectations based on qualitative work showing that parents who struggle to maintain stable, safe housing may send their children to another household out of concern for their well-being (Rhodes and DeLuca 2013). We also find that each of our measures of housing instability predicts poorer labor market outcomes in the subsequent period, whether reduced weeks employed (no permanent residence), labor income (temporary housing), or both (hypermobility and late mortgage or rent). Meanwhile, being late on the rent or mortgage predicts poor self-rated health. Together, these findings highlight the importance of considering multiple forms of housing insecurity, as each seems to have distinct impacts on adult well-being.

Our findings add to evidence that different measures of housing instability capture different populations (Bhat et al. 2022; Cox et al. 2017; Routhier 2019), but they highlight the limits of combining all available measures of housing insecurity into a single index or scale and of conceptualizing “housing instability” as a single concept with consistent impacts on adult well-being. In addition to our findings that different forms of housing instability seem to have different impacts on forms of adult well-being, we find little correlation between our different measures of housing instability. Importantly, even measures that seem to reflect similar concepts can have little overlap and may have different effects on well-being. For instance, we find that subjective feelings of lacking a permanent residence have relatively little overlap with living in temporary housing, suggesting that many of those who appear to be living in unstable circumstances to a researcher (e.g., in shelters, motels) either do not perceive their current circumstances as unstable or think of themselves as having alternative homes to return to, while some individuals who appear to be stably housed (e.g., in an apartment) may not actually consider themselves as such. Although researchers working on indices and scales of housing instability have greatly advanced our understanding of the scope of housing instability, as a single concept, we caution against using such amalgamated measures to understand the effects of housing instability, as combining multiple forms of housing instability into a single measure may obscure the impacts of each type and the potential mechanisms at play.

We find evidence of heterogeneity by gender, by race/ethnicity, and by class background. Our results suggest that the labor market consequences of housing instability are generally larger for men than for women, across multiple measures of housing instability. Labor force attachment and work experience from early adulthood shape lifetime earnings and employment opportunities (Lewis and Gluskin 2018), so the negative impacts of housing instability likely have long-term implications for these men. Temporary housing residence, likewise, appears to be detrimental for subsequent health for men but not for women, but the consequences of housing instability for child noncoresidence are generally larger for women than for men. We do not find consistent evidence that any one racial or ethnic group is more disadvantaged by housing instability than other groups. However, because Black adults and, to a lesser extent, Hispanic adults are both more likely to experience most forms of housing instability, our findings that these experiences disadvantage adults across racial and ethnic groups contribute evidence that housing instability may be an important driver of racial and ethnic inequality. Finally, class-stratified models reveal that housing instability appears more harmful for labor market outcomes for adults whose parents have higher levels of education, but it may be more likely to result in child noncoresidence for adults whose parents have lower levels of education.

Together, our measures reflect multiple dimensions of housing instability and align closely with those currently in use by medical professionals as social determinants of health (Children’s HealthWatch 2025; LeLaurin et al. 2023), but our data prevent us from including all potential measures. For instance, we include one important measure of housing unaffordability, being behind on one’s rent or mortgage (Bhat et al. 2022; Burgard et al. 2012; March et al. 2011; Vasquez-Vera et al. 2017), but the NLSY97 data do not allow us to consistently calculate housing cost burden (whether the household spends more than 30 percent of their income on housing), which is the most common measure of housing affordability. Likewise, the NLSY97 public data do not include consistent measures of eviction or foreclosure, or of housing and neighborhood quality, two other important dimensions of housing needs (Cox et al. 2019; DeLuca and Rosen 2022; Routhier 2019). Future research should examine how these measures may or may not overlap with the measures we have examined here.

Additionally, we find high cumulative prevalence of different forms of housing instability, raising questions about how these fit into the early adult life course. For instance, future work should consider how the prevalence and frequency of different forms of housing instability may change over time and in response to common life events, such as college graduation and marriage or separation. This work should pay particular attention to the unique role of hypermobility. Unlike our other measures of housing instability, hypermobility is most common for White adults and for adults whose parents have higher levels of education. Although this descriptive finding is consistent with prior research that finds higher rates of residential mobility among White Americans (Evans and Chapman 2024), our finding that hypermobility appears to lead to subsequent disadvantage across groups raises interesting questions about what exactly drives hypermobility and how it differs from other forms of housing instability.

We consider this study an important first step toward building a robust and reliable literature investigating the consequences of different housing insecurity experiences from a causal perspective, but it is only a first step. Given that housing insecurity is often itself a symptom of other disadvantages and challenges individuals are already facing, our goal has been to explore the strength of evidence for any plausibly causal relationship between housing instability and subsequent measures of well-being once we carefully consider the time ordering of these experiences. Although our robustness checks strengthen our confidence in our results, our methods cannot perfectly address all forms of unobserved confounding.

Moreover, our analyses capture effects in the subsequent period, but more research is needed to understand the timing of the effects of housing instability. In our analyses, the precise length of the lag between the housing instability measure and the outcome measure varies depending on the measure and the annual or biennial structure of the NLSY survey; longer gaps between the housing instability experience and measurement of the outcome may limit our ability to identify relationships between these variables. Future research should consider whether there may be delayed or lingering effects. We hope that having established evidence that some forms of housing instability do appear to influence some measures of adult well-being in the subsequent period lays the groundwork for future work that will more carefully attend to how long such effects may persist and whether they are more meaningful and/or destabilizing at some periods of life.

We have not examined the mechanisms that are most likely to link particular forms of housing instability to particular measures of adult well-being, but identifying such mechanisms is crucial for improving our theoretical understanding of different forms of housing instability and their effects. Future research should also seek to uncover the reasons for variation in the impacts of different forms of inequality, as well as the implications of these differences for inequality. Examining additional outcome measures may also contribute to our understanding of mechanisms. We selected outcome measures to reflect three key domains of well-being—employment, health, and family life—but future research should examine additional measures and specific components of our measures of interest (e.g., distinguishing between mental health, access to public benefits, and use of health care, in addition to our measure of overall health). Although further research is still needed, our hope is that this study contributes to an increasingly robust conversation around the variety of ways housing instability, in its many forms, may influence adults’ subsequent well-being, as well as an increase in causally focused research in this area moving forward.

Supplemental Material

sj-docx-1-srd-10.1177_23780231251347047 – Supplemental material for Cause or Consequence? Evaluating the Evidence for Housing Instability as a Predictor of Adult Well-Being

Supplemental material, sj-docx-1-srd-10.1177_23780231251347047 for Cause or Consequence? Evaluating the Evidence for Housing Instability as a Predictor of Adult Well-Being by Brielle Bryan and Hope Harvey in Socius

Footnotes

Acknowledgements

The authors are listed in alphabetical order. We gratefully acknowledge excellent research assistance from Fang-Yu Yeh and Soleste Starr, as well as support from the University of Kentucky United in True Racial Equity Research Priority Area and a Rice University Social Sciences Research Institute Seed Money Grant.

Supplemental Material

Supplemental material for this article is available online.

1

Routhier (2019:243) found that 18 percent of urban renter households experienced crowding, poor physical conditions, or forced moves without also experiencing unaffordability. Likewise, ![]() :4) showed that only 8 percent of adults in the Midlife in the United States Study missed a rent or mortgage payment, but a total of 14 percent reported at least one of the housing instability experiences they measure (doubling up, missed a rent or mortgage payment, threatened with eviction or foreclosure, lost home, or experienced homelessness).

:4) showed that only 8 percent of adults in the Midlife in the United States Study missed a rent or mortgage payment, but a total of 14 percent reported at least one of the housing instability experiences they measure (doubling up, missed a rent or mortgage payment, threatened with eviction or foreclosure, lost home, or experienced homelessness).

2

Children’s HealthWatch uses the following three measures to screen for housing instability: (1) being behind on the rent or mortgage at some point in the past 12 months; (2) moving two or more times in the past 12 months; and (3) currently living or ever having lived in “a shelter, motel, temporary or transitional living situation, scattered site housing, or [having] no steady place to sleep at night” (Sandel et al. 2018). Epic Systems’ health instability screening questions include: (1) having been unable to pay mortgage or rent on time at some point in the past 12 months, (2) having lived in three or more places in the past 12 months, and (3) not having a steady place to sleep or sleeping in a shelter at any point in the past 12 months (![]() ).

).

3

Hispanic adults’ use of homeless services varies across communities. However, Hispanic households experience high rates of housing challenges, and underrepresentation in homelessness services may largely reflect difficulties accessing services (Aiken, Reina, and Culhane 2021).

4

Although 2021 survey year data are now available, we exclude them from our analysis because of the extreme upheavals to housing, health, work, and family coresidence caused by the COVID-19 pandemic.

5

Because residential mobility peaks in early adulthood and declines thereafter, our hypermobility threshold of two moves in the past year corresponds to the 94th percentile for move frequency for ages 18 through 25 years, the 97th percentile for ages 26 to 30 years, and the 99th percentile at ages 31 through 40 years.

6

We control for whether respondents have any biological children in all models.

7

Note that these percentages do not align with the proportion shown for poor health in ![]() in the Appendix, because we use survey weights when calculating the summary statistics displayed in Table A1.

in the Appendix, because we use survey weights when calculating the summary statistics displayed in Table A1.

8

We produced 10 imputed datasets with the chained equations method in Stata MI commands. Results using casewise deletion are substantively consistent with our main results, but standard errors are larger and significance sometimes changes accordingly.

9

Once NLSY97 data collection becomes biennial in 2011, there is a larger gap between measurement of housing instability and outcome for some combinations of variables, particularly for housing instability measures recorded at each survey date (i.e., no permanent residence, temporary housing) when combined without outcomes also measured at each survey date (i.e., child noncoresidence, health). In these later survey years, these particular lagged housing instability measures now reflect instability that was experienced two years prior to the measurement of the outcome. We expect that these gaps between measurement of “treatment” and outcome will introduce greater noise in our estimates, making it harder to identify a relationship between these particular housing instability measures and these particular outcomes, but they should not introduce bias.

10