Abstract

As financial advice migrates online, “finfluencers” are democratizing access to financial knowledge, challenging the historically male-dominated advisory landscape. This mixed-methods study explores how gender shapes the creation and consumption of finfluencer content. Qualitative analysis reveals gendered advice patterns: Men emphasize quantitative aspects, whereas women incorporate narratives and personal stories. Experimental surveys uncover subconscious same-gender preferences in advice receptivity, contrasting with stated desires for gender-neutral guidance. These implicit affinities persist even when advice content is anonymized and gender-balanced. Paradoxically, finfluencers introduce diverse voices and challenge traditional norms yet also subtly cater to gendered perspectives. The research highlights the complex role of gender in the digital financial advice market, where expanding inclusivity coexists with enduring biases. Findings offer insights for developing more equitable and empowering financial education in the digital age while revealing the subconscious factors shaping the emerging finfluencer discourse.

The emergence of social media is transforming how people understand personal finances, familiarizing millions to a new type of financial advice-givers, known colloquially as “finfluencers.” 1 These individuals share their insights, money tips, and investment strategies through popular online platforms such as Instagram, TikTok, and YouTube, setting themselves apart from traditional financial advisors. As social media opens access to content creation and dissemination, finfluencers represent a more diverse range of voices in a domain historically dominated by older, affluent, White men (Crosthwaite et al. 2022; Crosthwaite, Knight and Marsh 2019; Hayes and Ben-Shmuel forthcoming; White et al. 2019). Indeed, their presence marks a significant shift toward a more inclusive and accessible array of financial knowledge that challenges traditional gatekeeping and norms.

In an era of financialization that emphasizes self-reliance, financial literacy and access to financial advice play critical roles in individuals’ ability to make wise decisions and accumulate wealth. Although some individuals still rely on paid practitioners, many are now turning to finfluencers for free guidance on social media. Indeed, reports indicate that over a quarter of Gen-Z and one-fifth of Millennials now get most of their financial advice from social media, with a majority taking action based on what they find online (NAPFA 2021). The accessibility of these platforms has allowed finfluencers to gain rapid traction, collectively attracting many millions of followers, although the quality of their counseling may be questionable (Manfredo 2022). More significantly, finfluencers tend to be far more diverse than the licensed professionals they are disrupting. For instance, whereas over three-quarters of certified financial planners today are still White men, women dominate social media influencing overall (Devos, Eggermont, and Vandenbosch 2022). 2 Financial influencing follows suit, with women of color like Tiffany Aliche (@thebudgetnista) and Dasha Kennedy (@thebrokeblackgirl) each commanding hundreds of thousands of followers. In fact, 10 out of the 18 “2023 Finfluencers to Watch” list put out by financial media firm TheStreet were women, and 10 were non-White (Button 2023). 3 For the first time, financial advice from a range of voices and perspectives, and not just that canonized by the financial services sector, is being widely disseminated.

This provides an opportunity to study how financial advice is constructed and shared in a more democratized, digital age (cf. Chang 2005). Importantly, it allows for new examination of how gender may manifest in this traditionally masculine domain. In the past, most financial advice has followed similar professional norms and scripts regardless of an advisor’s own gender (Crosthwaite et al. 2019, 2022; d’Astous, Gemmo, and Michaud 2013; Robb and Woodyard 2011). Such developments prompt critical questions about the gendering of financial advice and its consumption: Are financial narratives inherently gendered, and if so, how does this influence the way individuals across different gender identities engage with and apply the financial guidance they encounter? This inquiry is vital for understanding the dynamics of today’s financial advice, where traditional barriers are being dismantled and new patterns of influence and engagement are emerging. 4

Contemporary research shows the persistence of gendered patterns in financial literacy, advice seeking, and advisory preferences. Women still report lower financial literacy and confidence in managing money compared to men (Lusardi and Mitchell 2014; Robb and Woodyard 2011). They also tend to favor receiving financial advice from women, perhaps sensing greater empathy from shared experiences in navigating traditionally male-dominated financial spaces (Baeckström, Marsh, and Silvester 2021; Newcomb and Rabow 1999; Stendardi, Graham, and O’Reilly 2006). However, surveys also find that both men and women claim they desire unbiased, gender-neutral counseling regardless of any perceived differences in needs (Hartford Funds 2022). This points to a potential disconnect between stated preferences and unconscious gender biases, which studies confirm can covertly shape financial behaviors and decisions (Klein, Shtudiner, and Zwilling 2021). 5 Indeed, a large body of research points to implicit preferences as powerful drivers of actual behavior (Greenwald, McGhee, and Schwartz 1998) even when individuals report otherwise egalitarian views (Nosek, Banaji, and Greenwald 2002). This research, therefore, aims to explore both (1) the presence of gendered patterns in financial advice giving by finfluencers online and (2) audiences’ implicit biases in its consumption—contributing empirically and theoretically to scholarship on gender, social media, and personal finance.

To investigate these questions, we employ a mixed-methods approach, combining qualitative content analysis of finfluencer posts followed by a series of quantitative studies.

The first phase is a qualitative content analysis, confirming that women and men finfluencers do tend to differentiate their content through both overt and subtle means. We find, for instance, that women finfluencers frequently employ storytelling and narratives of empowerment aimed at inspiring and engaging their audiences (see also Hayes and Ben-Shmuel forthcoming). They emphasize, for example, budgeting, saving, and reducing debt—areas stereotypically associated more with women’s financial roles (see Newcomb and Rabow 1999; Sesini, Manzi, and Lozza 2023). In contrast, men finfluencers are more likely to focus their messaging on wealth accumulation, risk-taking, and investing prowess—building on certain masculine themes in finance (see Boggio et al. 2017; Crosthwaite et al. 2019). By employing different styles and focuses, finfluencers are not just providing rote financial advice; they are also shaping the narrative around personal finance in ways that reflect and reinforce gender-specific perspectives and experiences. Our work here builds on previous research that reveals gendered self-presentation strategies and discourse propagated among influencers in fashion and other lifestyle verticals (Abidin 2016; Duffy and Hund 2015); however, this is the first empirical examination to reveal similar patterns in the domain of financial advice—one often heralded as rational, objective, universal, and thus, gender-neutral (e.g., d’Astous et al. 2022). 6

In the next phase, we use a quantitative approach and look to those receiving finfluencer advice. Here, we find that a majority of both men and women in an initial survey express a view that financial advice ought to be gender-neutral. This aligns with previous surveys conducted by the financial services industry (e.g., Hartford Funds 2022). However, in a subsequent study that experimentally exposed respondents to anonymized finfluencer posts that were stripped of any gender-identifying information, we find a strong implicit preference for same-gender content. Importantly, a follow-up study asked a new group of respondents directly whether the same anonymized posts exhibited any gender bias, where the modal response among both sexes was that the content was gender-neutral. These findings highlight a paradox: Individuals assert a belief in gender-neutral financial advice and struggle to recognize gender biases in such advice, yet they demonstrate a subconscious inclination toward content received from finfluencers of their own gender.

The presence of gendered financial advice from finfluencers along with this conflict between stated beliefs and subconscious preferences underscore the need to address and understand underlying biases in how traditional financial advice is given and received. Our findings contribute broadly to scholarship on gender performativity in digital spaces and have particular relevance for policy and education initiatives aiming to advance financial literacy and inclusion. Our findings point to the complexity of financial advising as a cultural practice, revealing that even within spaces touted for their objectivity, gendered practices pervade, shaping both the content produced and its reception. This insight not only contributes to our understanding of financial discourse but also suggests that achieving genuine inclusivity in financial education requires addressing these deeply ingrained biases, encouraging a reevaluation of what constitutes effective and equitable financial advice. By shedding light on hidden drivers of advice preference, this work also highlights the prominent role of gender in economic behavior and decision-making more broadly.

Although other ascribed characteristics, such as the race or family background of finfluencers and their audiences, are important to explore, the present research concentrates on gender in particular given the substantial precedents establishing such differences specifically in financial literacy and confidence with financial matters (Chen and Volpe 2002; Lusardi and Mitchell 2014; Rink, Walle, and Klasen 2021; Robb and Woodyard 2011). These well-documented gaps point to gender as a strong predictor for shaping financial advice reception and warrant closer examination. Additionally, initial exploration of our corpus of finfluencer posts suggests a deliberate gendered positioning in their content strategies, more so than race or other demographic features. This study’s intent is, therefore, not to posit gender as the sole or primary factor driving financial advice biases or preferences but, rather, to provide foundational evidence as a springboard for more nuanced and intersectional analyses of financial advice content and engagement both online and offline.

Finfluencers: Social Media and the Changing Discourse of Financial Advice

The rapid evolution of social media over the past decade has profoundly impacted communication and knowledge sharing globally. Platforms such as TikTok, Instagram, Twitter/X, and YouTube have connected billions of users worldwide, providing new tools and platforms for content creation and building communities around shared interests (Hemsley and Mason 2013). With social media’s expansion, a new category of internet celebrity has emerged—so-called “influencers” who leverage these platforms to build devoted followings in their domains of knowledge or interest (Abidin 2016). Whereas fame and authority were previously concentrated among elite figures such as celebrities and credentialed experts, ordinary individuals are now able to accrue large audiences by producing engaging content online. By cultivating perceptions of authenticity and an intimate, para-social relationship with their followers, influencers have become trusted voices on subjects even where they lack traditional qualifications (Bond 2016; Djafarova and Trofimenko 2019). Across the internet, influencers have amassed many tens of millions of subscribers and garnered billions of views. Their content spans an incredibly diverse range of topics, from beauty, fashion, and lifestyle to gaming, technology, and more (Hudders, De Jans, and De Veirman 2021). As a result, media scholars argue that influencers represent a paradigm shift in knowledge production and credibility in the digital age (Watkins 2022). Their resonance with niche communities grants them power to shape opinions, trends, and even policy issues among devoted followers.

One subset gaining popularity is the finfluencers—that is, financial influencers. Ranging from investment professionals showcasing market insights to everyday investors sharing budgeting tips, finfluencers produce financially focused content as bite-sized posts or tweets. They tend to adopt an informal,  ), and humor to make the material relatable. This contrasts sharply with the technical financial jargon and dense numbers that have traditionally dominated the field. By simplifying money management principles for mass consumption, finfluencers have helped democratize financial literacy and make concepts such as saving, investing, taxes, and debt more accessible and approachable. This represents a shift in who controls financial discourse given that finfluencers exhibit greater diversity in age, gender, race/ethnicity, and socioeconomic background compared to the traditional demographic of older, White, male advisors that has prevailed for decades (White et al. 2019).

), and humor to make the material relatable. This contrasts sharply with the technical financial jargon and dense numbers that have traditionally dominated the field. By simplifying money management principles for mass consumption, finfluencers have helped democratize financial literacy and make concepts such as saving, investing, taxes, and debt more accessible and approachable. This represents a shift in who controls financial discourse given that finfluencers exhibit greater diversity in age, gender, race/ethnicity, and socioeconomic background compared to the traditional demographic of older, White, male advisors that has prevailed for decades (White et al. 2019).

Research shows that influencers across many domains adopt gendered self-presentation techniques to shape their personal brands in line with cultural norms and expectations and to attract ever-larger follower bases (Abidin 2016; Duffy and Hund 2015). For instance, studies reveal that female lifestyle and fashion influencers tend to emphasize traits such as warmth, vulnerability, caretaking, and intimacy to resonate with their predominantly female audiences (Duffy and Hund 2015; Lokithasan et al. 2019). In contrast, male influencers in domains such as gaming and technology are more likely to highlight expertise, competition, and risk-taking (Lokithasan et al. 2019). These divergent self-branding strategies underscore how influencers tacitly integrate gender norms into their content approaches based on social expectations and their personal preferences and assumed target demographics.

An open question exists whether finfluencers similarly engage in gendered financial advice positioning and content strategies. Finfluencers do exhibit far greater diversity compared to traditional financial advisors; however, it is not immediately clear if this variety influences the nature of their guidance due to finance’s unique position as seemingly rational and its self-conception as an impartial discipline. We thus see three potential scenarios emerge in this context, ranging from the perpetuation of superficial gender tropes seen in other influencer domains, to deeper integration of gender assumptions into the financial content, to actively minimizing gender distinctions:

Superficial gendering

Finfluencers may employ gendered aesthetics and visual elements, but men and women will still give practically similar financial advice. This would suggest a surface-level differentiation but without substantively changing the core guidance. The underlying advice remains consistent in message and tone even as the outward presentation aligns with target demographics along gendered lines.

Implicitly gendered content

Finfluencers may directly integrate gendered perspectives and framings into the actual messaging and meaning of the financial advice itself, leading to qualitatively different insights from and for men versus women. Even if the top-level guidance on saving, investing, taxes, and so on, appears similar, the rhetorical packaging used to engage audiences and bring the advice to life embeds distinctly gendered assumptions and worldviews.

Universal approach

Finfluencers may avoid gender segmentation entirely, focusing on broadly applicable advice to maximize follower base, albeit with a risk of overgeneralization. The emphasis would be on commonalities and universal principles that apply across demographics. However, this could come at the expense of providing tailored insights that address financial situations faced disproportionately by specific communities.

By examining the strategies employed by finfluencers, we can gain insights into how modern financial advice is constructed and potentially transformed in the digital age. This shifting landscape carries tremendous practical import because it can motivate the economic decisions and outcomes of millions of individuals. A recent industry survey reports that over 60 percent of all American investors received at least some of their financial advice from social media in 2021, compared to just one-quarter who counseled a financial professional (Evans 2021)—a figure even more pronounced among the younger Millennial and Gen-Z cohorts. The impact of finfluencers on decision-making, especially among younger, digitally savvy audiences, calls for a critical evaluation of their content in shaping financial attitudes, perceptions, and behaviors.

In the next section, therefore, we also consider the consumption of finfluencer content. Just as gender socialization may shape the construction and dissemination of advice, so too might it influence receptivity and interpretation by audiences.

Gender Imbalances in Financial Engagement

Despite progress toward equality in recent decades, there remain noticeable disparities in how men and women engage with and benefit from financial guidance. Research consistently shows a gender gap in financial literacy and confidence even when controlling for things such as income, educational attainment, and marital status (Bradley 2021; Hasler and Lusardi 2017; Lusardi and Mitchell 2014; Robb and Woodyard 2011). This disparity starts early, with high school and university-age girls already exhibiting lower financial literacy scores than their male peers (Amagir et al. 2020; Chen and Volpe 2002; Mandell 2008). Scholars point to wide-ranging cultural conditioning into traditional roles that shape economic behaviors and attitudes in gendered ways (Sotiropoulos and d’Astous 2013). These norms and expectations contribute to differences in financial socialization, with, for example, parents placing greater emphasis on their sons to develop financial acumen and independence at a young age—in contrast to daughters who receive more financial assistance but less hands-on education in money matters from parents (Newcomb and Rabow 1999; see also Fonseca et al. 2012).

Gender disparities in literacy and confidence also appear to extend into financial advice-seeking contexts. Women report greater satisfaction when receiving financial advice from women advisors, perceiving them as more understanding and relatable, whereas women who obtain their advice from male advisors report feeling less knowledgeable, take fewer risks, and are more anxious about their investments (Baeckström et al. 2021). A substantial body of research underscores how seeing one’s own gender reflected in a particular field improves participation and engagement. For example, studies show that girls are more likely to pursue careers in STEM when exposed to female role models and mentors (Young, Young, and Paufler 2017), and women scientists likewise emphasize the importance of seeing other women in leadership roles in normalizing such educational paths for themselves (Drury, Siy, and Cheryan 2011). Similarly, having access to female financial advisors could provide women with relatable perspectives and shared experiences that inform better financial decision-making. Yet the financial advisory field remains heavily male-dominated. Recent industry demographics disclose less than one-quarter of certified financial planners are women, as are only 17 percent of financial advisors registered in the UK—a low level that has not budged since 2005 (Croxson et al. 2019). 7 This lack of diversity limits the narratives and financial subjectivities available to women seeking guidance (see Lai 2017).

To be sure, traditional financial advice has long endorsed masculine subjects and subjectivities, dating back centuries. As Crosthwaite et al. (2019, 2022) illustrate through their deep analysis of early financial advice texts, framing finance as a means to masculine empowerment and alternative selfhoods has been a persistent undercurrent throughout its history. Despite doubts about its practical usefulness, the rhetoric of financial advice used from the seventeenth th century through today has naturalized financial participation as a domain largely of maleness and whiteness. As they explain, It is not simply significant that such texts are overwhelmingly written by white men, but also that they typically project an implied reader who is likewise white and male. . . . [T]o be invested (both financially and emotionally) in the stock market is simultaneously to be invested in a particular conception of subjectivity—in this case, a subjectivity that is forcefully and decidedly male. (Crosthwaite et al. 2019:670, 682)

This cultural conditioning over time has tacitly shaped prevailing norms and assumptions about who constitutes a financial subject and the type and content of advice they should receive. 8

And yet, both public perception and the finance profession’s self-image largely paint a different picture. They often perceive and promote financial advice as being neutral, unbiased, and objective. This discrepancy is significant because it suggests a practical disconnect between the implicitly gendered nature of financial advice—as identified by the aforementioned research—and the prevailing societal and professional belief in its neutrality.

Outwardly, men and women still often perceive the domain of financial advice to be impartial, in part due to the accepted narrative that financial decisions ought to be rational, that is, based on coherent analysis and mathematical evaluation of figures and tables and seemingly devoid of social or cultural influences. Even behavioral finance, which acknowledges the psychological faults in economic decision-making, often frames these deviations from rationality as universally human rather than varying by gender (Sent and van Staveren 2019). Taken together, this approach promotes the belief of finance as a field governed by universal principles equally relevant to everyone irrespective of gender (see d’Astous et al. 2022). 9 However, this broad perspective inadvertently conceals the historical and current gender biases that permeate the field. For instance, a 2022 survey by Hartford Financial found that a majority of both male and female respondents, across all ages, preferred financial advice that was neutral and not tailored to any specific gender. They desired such impartiality even while acknowledging that men and women might have different financial needs (Hartford Funds 2022). This paradoxical stance exemplifies the conflict between what people say they want (stated preferences) and what their actions suggest they actually value (revealed preferences) in the context of financial advice and decision-making.

A large body of research informs us that implicit biases are powerful drivers of behaviors and decisions even when explicit views appear egalitarian (Greenwald et al. 1998; Staats 2016). These biases reflect associations outside conscious awareness that develop from repeated cultural exposure and social experience—and can diverge markedly from stated attitudes. For instance, although overt racism has declined in the United States, experiments using implicit association tests consistently uncover enduring racial prejudices that influence an array of interpersonal behaviors and judgments about others (e.g., Oswald et al. 2013). As an example, most individuals today report that race should not factor into political candidate evaluations. Yet experiments demonstrate that when a candidate’s race is made salient, both White and Black participants exhibit implicit biases in favor of their own racial group (Greenwald et al. 2009; Hahn and Gawronski 2019).

Gender biases similarly permeate tacit judgments and actions in a range of contexts (Rudman and Goodwin 2004). Studies find that stereotypes associating men with science and women with arts subjects shape academic interest and performances even when controlling for ability (Nosek and Smyth 2011). Hiring experiments also reveal persistent pro-male undercurrents among both male and female evaluators, influencing employment and compensation decisions (Reuben, Sapienza, and Zingales 2014). This body of work reveals how unintentional but implicit attitudes and stereotypes develop through ongoing exposure to cultural messaging and social dynamics.

A similar phenomenon may shape financial advice contexts: Although surveys find both men and women state a preference for gender-neutral financial guidance, unconscious gender biases likely still permeate judgments and receptivity when advice is received. Consequently, a critical next step is to investigate whether implicit gender biases factor into the consumption and interpretation of financial advice even among those professing a desire for neutrality. Unpacking this potential divergence is key to understanding how modern financial advice is engaged with by diverse audiences.

Empirical Strategy

The unprecedented availability of finfluencer posts on social media represents a significant advance in research on financial advice. Unlike traditional financial advisors, whose guidance often occurs in private, one-on-one settings, finfluencers share their insights publicly, creating a large, accessible body of content. The public nature of their advice further allows for a systematic analysis of patterns in their messaging, a task that was previously challenging due to the private and highly regulated nature of traditional financial advising (cf. Clarke 2000). And although public figures such as Dave Ramsey, Suze Orman, and Jim Cramer, among others, have certainly provided guidance to a mass audience through various media, their messaging often adheres to a generic, one-size-fits-all approach (Faulkner 2017). Consequently, the present shift from private to public advisory spaces opens up new possibilities for empirical research—finfluencers make visible what was previously obscured when it came to examining gender bias in the giving and receiving of financial guidance.

Our research approach is built around two phases. First, we conducted a qualitative analysis to explore if and in what ways women and men finfluencers tailor their content. To achieve this, we closely reviewed and categorized 621 finfluencer posts, identifying key themes and patterns.

The second phase of our study focused on understanding how audiences respond to the content produced by men and women finfluencers through a three-step quantitative analysis. First, we conducted a short survey to collect data on participants’ preferences for either gender-specific or gender-neutral advice. This step aimed to capture stated preferences toward the gendered framing of financial guidance, establishing a baseline and to see if we could replicate the findings of the Hartford Funds (2022) study. Following this, we conducted a study with a fresh cohort of participants who were shown a series of anonymized finfluencer posts—equally divided between male and female creators. These posts, chosen based on their strong gender-coded messaging identified in the qualitative analysis, were modified to remove any clues about the creators’ identities. Participants evaluated the content of these posts across several criteria, such as relatability, practicality, quality, and their willingness to follow and share the advice given. This stage was designed to reveal any biases affecting the valuation and perception of financial advice independent of the finfluencer’s gender. Lastly, we asked a new sample of participants to review the same selection of anonymized finfluencer posts as previously described, explicitly asking them to categorize each post as masculine, feminine, or gender-neutral. This provides a direct test of whether audiences can consciously recognize the presence of gendered messaging in finfluencer content.

By triangulating explicit appraisals with implicit reactions, our tiered methodology provides a nuanced test of how gendered financial advice is both tacitly received and overtly perceived by audiences.

Qualitative Study

Our content analysis unfolded over a span of more than two years, from March 2020 to December 2022, incorporating extensive participant observation. Initially, we adopted a digital ethnographic method, dedicating up to two hours daily for the first eight weeks to immerse ourselves in, engage with, and record a variety of finfluencer content (see Abidin and de Seta 2020). This immersion helped us to familiarize ourselves with the ecosystem and informed the development of our sampling strategy: We strategically selected 20 male and 20 female finfluencers with substantial followings (i.e., over 10,000 followers) on Instagram and TikTok. When a finfluencer maintained active profiles on both Instagram and TikTok, we prioritized collecting their content from Instagram for consistency. In curating our final sample, we established several key inclusion criteria to maintain the integrity and focus of our analysis. First, we required that each finfluencer’s account be associated with an individual creator rather than a larger company or brand. This criterion excluded accounts linked to major financial institutions or media outlets (e.g., Ellevest, Financial Diet) but allowed for a diversity of individual finfluencer backgrounds, niches, and advice styles. Second, we sought out influencers who consistently posted content directly related to personal finance rather than those for whom financial topics were a secondary or occasional focus. This helped ensure the relevance and richness of our data for examining gendered patterns in financial advice. Third, we looked to media mentions and industry lists highlighting top finfluencers to identify potential candidates. This external validation helped corroborate the prominence and impact of the voices in our sample. Through this purposive sampling process, we could effectively zero in on the key players and discourses shaping this space (see Appendix in the supplemental material). Although not exhaustive, this sample captures a rich cross-section of the dynamics animating the finfluencer space.

To assess finfluencer gender, we considered both self-identification and characterizations in social media posts and popular media sources (e.g., use of pronouns, outward appearance, explicit references to gender identity). Although relying on external ascriptions is not without limitations, this strategy aligns with our focus on the social construction and perception of gender in this domain. Importantly, we did not encounter any instances of contradiction between finfluencers’ self-identification and their media characterizations.

For our analysis, we chose 18 post dates from each finfluencer, creating a total potential set of 720 posts. This number was chosen to balance depth and breadth, providing a robust corpus for discerning gendered patterns while remaining manageable for close qualitative analysis. To construct our sample, we utilized two selection logics: First, we chose posts from nine randomly selected dates distributed across our more than two-year observation period. Second, we selected posts from nine dates corresponding to major financial market events, such as the onset of the COVID-19 pandemic and the Russian invasion of Ukraine. This approach ensured our data set reflected both the day-to-day cadence of finfluencer content and their commentary during moments of acute financial upheaval. In 99 cases, a finfluencer in our set did not post on one of the analysis dates, leaving us with a final analytic sample of 621 social media posts.

In the following section, we present our qualitative findings on the gendered nature of finfluencer content. First, we outline the overarching patterns and thematic differences observed across male and female finfluencers, highlighting how their communication strategies and focus areas diverge. Then, we dive deeper into these themes, providing specific examples of posts from our data that exemplify these gendered patterns. Finally, we discuss how these differences in framing and rhetoric reveal broader assumptions and orientations toward financial topics that are shaped by gender. Through this progression, we aim to provide a rich and nuanced understanding of how gender influences the creation and presentation of financial advice in the finfluencer space

Qualitative Findings

Our analysis of finfluencer posts reveals that both genders employ distinct communication strategies—some aligning with patterns that reflect wider trends observed across online content domains. For instance, men often employed primary colors with larger, bolder fonts; women used more tertiary colors and pastels and a variety of decorative fonts and styles (see Hudders and deJans 2022). This supports the presence of superficial or aesthetic gendering of some finfluencer posts.

But we also observed a notable gendering in the deeper layers of the content and its meaning. Differences emerged around the discussion of empowerment, financial independence, and inclusivity, themes predominantly found in posts by women finfluencers. A striking example from one is “A Man is Not a Financial Plan!” (@investdiva), a proclamation of self-sufficiency. Furthermore, women finfluencers more readily addressed the interplay between financial well-being and mental health. For instance, one post stated, “Money and mental health go hand in hand . . . Get the help you need. Don’t be ashamed to reach out. And know that your mental health is the ultimate investment” (@clobaremoneycoach). These insights reveal how women finfluencers leverage social media not just to share financial advice but also to engage with broader feminist issues, positioning themselves as both knowledgeable authorities and passionate advocates.

To be sure, contrasts between men and women appeared even when covering otherwise the same financial topics. Men, for instance, often framed real estate primarily as an investment asset, whereas women emphasized the personal goal of homeownership. Additionally, male finfluencers tended to dive into the specifics of investment vehicles such as cryptocurrency, stocks, and bonds, focusing on their strategic aspects. In contrast, female finfluencers approached investments more conceptually, emphasizing their role in a diversified portfolio for providing security now and facilitating a comfortable future. To this point, although finfluencers of both genders described market volatility as something to look out for, their responses differed markedly. Men often associated volatility with excitement (one even calling it an “adrenaline rush”), viewing price swings as an opportunity for tactical advantage. Women, however, were more likely to discuss volatility in terms of its emotional toll (e.g., as “stressful” or “anxiety-inducing”), promoting strategies of endurance rather than immediate action.

These differences not only highlight the unique perspectives each gender brings to financial advice but also underscore how these views shape their online persona and influence the guidance they offer. Interestingly, our coding also uncovered more subtle thematic differences that on the surface might seem neutral but could significantly influence follower attitudes. Men, for example, frequently cited specific financial metrics or figures—returns, prices, percentages—emphasizing the quantitative aspects of finance. Women, in contrast, while also engaging with traditional financial advice tropes, tended to weave narratives around financial decisions, connecting them to personal stories or broader life goals. For instance, budgeting and saving tips were often couched in personal stories about specific spending temptations resisted. Similarly, retirement planning revolved around securing time for family or hobbies rather than hitting numeric wealth targets. Such rhetorical and framing divergence suggests gendered assumptions and orientations deeply penetrate financial messaging even where the broader subject matter or practical substance of the advice itself aligns. Nuanced differences such as these can greatly affect how followers perceive and interact with financial advice—they reflect not only the distinct digital identities cultivated by finfluencers but also potentially how their audiences assimilate and apply the guidance into their own lived financial realities.

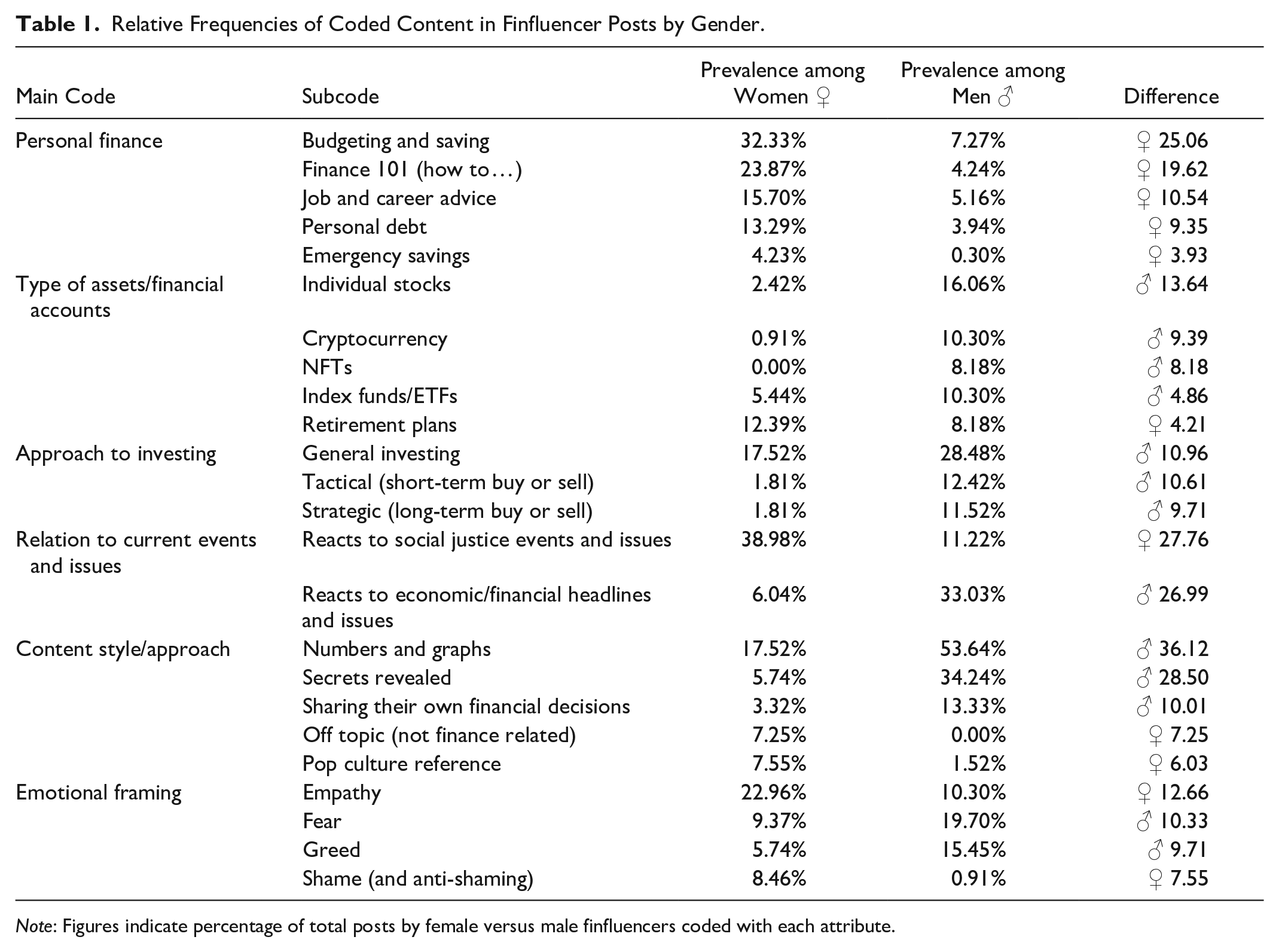

To more systematically identify divergent themes and content in the financial advice, we employed a comparative indexing methodology that enumerated the relative frequency of codes across finfluencers by gender. To validly categorize certain rhetorical features or topics as predominantly male- or female-focused required establishing these empirically rather than presuming stereotypical associations a priori (see Table 1). We stylized such patterns as male-prevalent or female-prevalent only after demonstrating that they repeatedly clustered in our data. We find that many differences in framing and usage carry substantive meaning regarding perspectives on finance itself—they exhibit distinct gendered assumptions, objectives, and self-conceptions around money. As scholars such as Brown (1987) argue, rhetoric reveals reality. But rather than reifying divisive stereotypes through coding, our analysis unpacks how financial engagement gets socially constructed to resonate more effectively across gender lines. 10

Relative Frequencies of Coded Content in Finfluencer Posts by Gender.

Note: Figures indicate percentage of total posts by female versus male finfluencers coded with each attribute.

Additionally, we leverage the relative differences in frequency we uncovered to identify and select the most “gendered” posts from among our sample to be used in the quantitative phase that follows.

In the following, we provide some illustrative examples of the most divergent codes.

Numbers and graphs

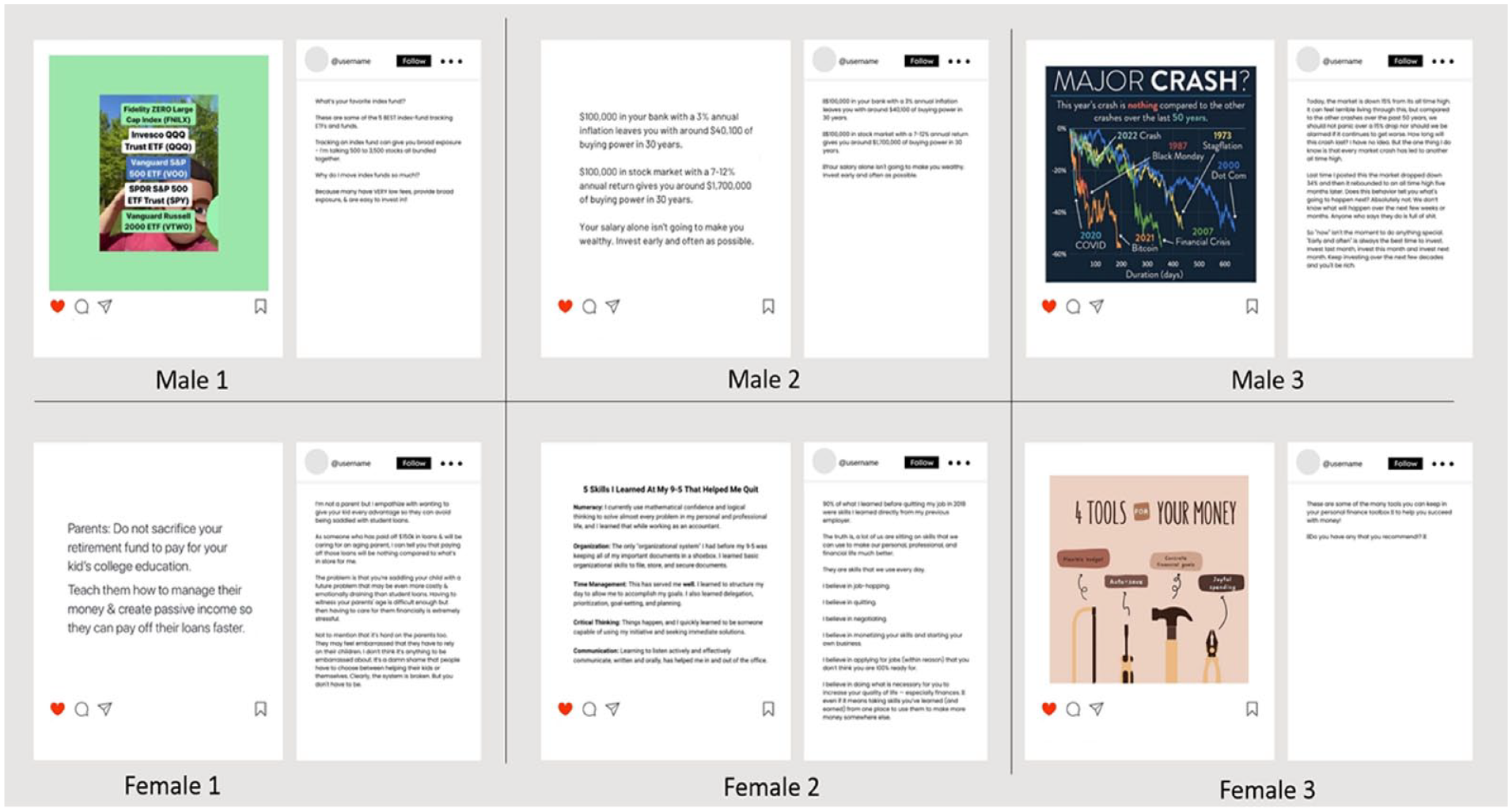

Numbers, figures, charts, and graphs showed up much more frequently in men’s posts than in women’s. A common trope was to depict a price chart of some stock or investment going up or down over time along with some commentary (see e.g., Figure 1, panel Male 3). Other common examples included numerical examples or specific figures in the form of dollar amounts, time frames, interest rates, or rates of return (among others): Becoming a millionaire is a simple math equation. . . . Invest $100/m for 55 years, Invest $200/m for 46 years, Invest $500/m for 35 years, Invest $1,000/m for 27 years, Invest $2,500/m for 17 years. There is no ‘luck’ involved. You either invest the amount you need to or you don’t. (@budgetdog) $100,000 in your bank with a 3% annual inflation leaves you with around $40,100 of buying power in 30 years. $100,000 in stock market with a 7-12% annual return gives you around $1,700,000 of buying power in 30 years. Your salary alone isn’t going to make you wealthy. Invest early and often as possible. (@calltoleap)

Anonymized finfluencer posts for Studies 2 and 3.

Secrets revealed

Some posts were framed as sort of letting people in on a little-known secret, often touted as a way to profit from exploiting that secret. This tactic was more prevalent among male finfluencers: So you want to know how to make money during a stock market crash/pullback? Trust me, I’m not making anything up. You can do this with a little thing called SPREADS. . . . That’s right a lot of retail investors actually don’t know how to do this. I’m actually going to be talking about this in my FREE webinar this Thursday. (@calltoleap) Here’s what they don’t want you to know about your retirement: you can go from unsecured account to a secured account. In an unsecured account you can actually lose money – the market goes down, you lose money. A secured account you can’t lose AT ALL. So if you have a 401(k), TSP, or 403(b), you better make sure you go from that unsecured account to a secured account before you lose. (@rorykdouglas)

Reacting to short-term swings and headlines

Male finfluencers were more likely to identify headlines or market events as short-term trading opportunities, with specific recommendations made for their followers. For instance, in March 2020, as the effects of the COVID-19 pandemic began to become more obvious, the following post was made by @wall_street_trapper: Through every crisis there’s always an opportunity. Now isn’t the time to panic, it’s time to research: ZOOM & VISA are 2 great businesses to have during these times. In lockdown, people will work from home and use video communications to still be able to meet with colleagues. Zoom has just donated its services to in-home schools for this time. People won’t be going in public and order everything online on credit cards. While people sit home, Visa is the most used card of all financial services.

Men were also more likely to respond to company-specific news headlines like earnings calls: Chipotle stock is up almost 13% today because they crushed their earnings, guided to higher growth, and just bought back $200M of their stock. And some analysts are calling for a $2,800 price target. (@austinhankwitz)

Individual stocks or tickers

Men posted about individual stocks or tickers much more than women. This theme already appears in some of the previous examples, with ticker symbols on social media posts often denoted by the “$” for easier searching online.

I feel like a kid in a candy store . . . over the next few weeks, we have a window of opportunity to buy investments at a discounted price . . . in February, Tesla ($TSLA) stock was trading at $835, the stock is now worth $445 . . . now is the time to buy. (@theinvestingtutor) Things aren’t so bad when you zoom out: Return Over the Last Year • NVIDIA (NVDA):+70% • Alphabet (GOOGL):+38% • Microsoft (MSFT):+31% • Berkshire Hathaway (BRK.B):+30% • Apple (AAPL):+16% • S&P 500 (SPY):+14% • Meta Platforms (FB/META):+13%

(@tickstocks)

(@tickstocks)

Job and career advice

Women finfluencers were much more likely to give advice on career management and the job search. An individual’s career path and job-related decisions (e.g., salary negotiations, job changes, upskilling) have significant and direct implications for their income, benefits, and overall financial security. In this sense, career advice is inherently financial advice because it shapes one’s earning potential and economic resources (Gallen and Wasserman 2021). This is especially true for women, who more often face gender gaps and distinct challenges in the workplace that can substantially impact their financial trajectories (Thomas et al. 2021). An example of a post coded with this theme includes the following: PSA: Recruiters can see when you apply to a bunch of different roles at their company. Do your research and apply to 1-3 roles that best fit your skills and career objectives—not 100 different roles just because. (@babeonabudgetblog)

She continues in the post’s caption, “Tailor your resume to the job(s) you’re applying to, and make sure to use keywords from the actual job description(s). Once you’ve done that, try to find the recruiter on LinkedIn and let them know you’ve applied! I promise you, this approach will be more fruitful.” Other advice focused more on salary negotiation or how to ask for a raise. For instance, I know there’s a voice in your head that whispers “am I really worthy enough to negotiate? Am I deserving enough?” Yes, yes you are. Companies EXPECT you to negotiate, and they’re purposefully offering you LESS than what you’re worth and what they’re willing to offer with the expectation that you will negotiate. So, take this as your sign. (@herfirst100k)

Empathy, empowerment, and (anti-)shame

Empathy is frequently used by both men and women, but women in particular, to demonstrate that they too have been in challenging situations, relate with their followers, and encourage them by making suggestions for how to move forward. Nearly one-quarter of posts by female finfluencers were framed using empathy for their audience, supporting their financial challenges and recognizing potential shame surrounding past practices. Pieces of advice were often illustrated by personal, authentic examples where shame is openly addressed rather than implied. This approach often challenged followers to acknowledge their lack of financial literacy as an opportunity to learn and grow rather than be chastened. Some examples include the following: [D]on’t be scared to admit you’re wrong & change your mind. It’s actually quite liberating once you start. Putting up a facade that you know everything is actually quite exhausting. Try saying “Oh I didn’t know that. Can you tell me more?” You’ll learn so much! (@Delyannethemoneycoach) Remember, it’s ok to make money mistakes. It’s ok to make mistakes in general. The key is to learn from them, and hopefully you can learn from mine. (@your.richbff) The irony of all of this is that you’re not actually bad at money. You just haven’t been given the tools to really succeed. Imagine what it would feel like to believe you’re GOOD with money. (@ellyce.fulmore)

Budgeting and saving

These two closely related pieces of financial advice are a focus of one-third of female finfluencer posts compared to only 7 percent of the male posts we analyzed. This advice often took the form of straightforward tips coupled with words of encouragement to stick with a budget or savings plan once in place. Others offer more detailed advice, even going line by line through followers’ budgets on occasion to show weak spots and recommend corrections.

Plan out your weekly spending & saving goals and review your past week spending/saving habits. This may be difficult at first but it will help in the long run and build your financial confidence. (@myfabfinance) There are three reasons I see budgets fail: 1)They aren’t rooted in purpose, 2)They were unrealistic from the jump, 3)They don’t account for the unpredictable. (@moneywithkatie)

Personal debt

In addition to student loans, which prominently featured in the posts of female finfluencers, personal debt was a broad topic that they addressed (as opposed to just 3 percent of the male creators). This advice ranged from taking advantage of student loan relief programs to prioritizing paying off high-interest debts and refinancing loans. The most common theme, however, was to motivate oneself to begin repaying personal debt with the goal of eventually eliminating it altogether.

3 years ago I had $222,000 worth of student loan debt and no idea how I was going to pay it off. 3 years later I’m almost debt free and own a small business. A lot can change in a short amount of your time–you just need to start. . . . Seriously though, just start. (@babeonabudgetblog)

Quantitative Studies

Our qualitative analysis reveals that male and female finfluencers differentiate their financial advice online in various ways that both confirm broader stereotypes and take subtler forms, such as the use of numbers and figures versus an emphasis on budgeting and saving. These insights are crucial for understanding the gendered presentation of financial advice online. However, they leave open questions regarding audience responses to such content and one’s likelihood to engage with varied advice.

Respondents for all three quantitative studies were recruited using Amazon’s Mechanical Turk (AMT) platform, an online labor market that is commonly used in social science research for data collection. In general, researchers find that AMT samples faithfully reproduce established findings on many social science outcomes despite the fact that these samples are not representative along certain demographic dimensions—in that they tend to be younger, more female, more liberal, and more educated than the general U.S. population (Berinsky, Huber, and Lenz 2012; Hargittai and Shaw 2020). Still, AMT samples are found to be just as effective but more diverse than classroom- or laboratory-sourced samples (Hauser and Schwarz 2016). To be sure, AMT samples have been shown to produce quite reliable data for high-quality sociological research (Schilke and Rossman 2018; Weinberg et al. 2014). Respondents who participated in one study were excluded from being recruited into another and were compensated at approximately the pro-rata U.S. federal minimum wage. To increase subject pool reliability, respondents were restricted to American adults who received a positive rating on AMT of 95 percent or greater over 500 or more tasks. Incomplete responses or those who failed an attention check question or reCAPTCHA were removed.

Study 1 Methods

For the first study, we recruited a sample of 180 respondents (median age = 40; median income = $40,000–$49,999; 55 percent female; 68 percent with a four-year+ degree; 81 percent White; 57 percent married), to whom we asked: “When it comes to the content of financial advice, would you prefer it to be gender-specific or gender-neutral?” Option choices were (a) “Gender-specific: Tailored advice considering gender-specific financial challenges and opportunities” or (b) “Gender-neutral: Universal advice applicable to all, regardless of gender.” 11

Study 1 Findings

Seventy-five percent (135) of all responses selected gender-neutral, a significant majority that also replicates Harford’s 2022 industry survey. When segmented by respondent sex, there was a notable difference, with men showing a stronger preference for neutral advice. Although a significant 65 percent of women still selected gender-neutral, more than 88 percent of men did.

Study 2 Methods

In our second quantitative study, we looked for implicit bias among respondents. For each gender category. we chose the three still image posts and one video post that featured the highest concentration of codes found to be distinctively male-prevalent or female-prevalent in our qualitative analysis. 12 For example, male-oriented posts heavily emphasized content related to numbers/graphs, revealing “secrets,” and reacting to market headlines, whereas female-oriented posts foregrounded themes such as empathy, personal debt, career advice, and financial basics. By selecting posts that epitomized the most salient gendered content features, we could create a focused stimulus set to cleanly test the impact of these features on audience reception.

To further isolate the effect of content on audience perceptions, we anonymized the selected posts by extracting the text and visual content and reembedding it in a generic social media frame, removing any explicit cues about the content creator’s gender or identity. This enabled us to assess how the gendered themes and rhetoric itself shaped audience reactions independent of the finfluencer’s personal characteristics (see Figure 1).

Our exemplar posts were displayed in random order to an analytic sample of 634 respondents, of whom 50 percent were male and 50 percent female (purposefully seeking an equal gender balance for this task; median age = 41; median income = $50,000–$59,999; 61 percent with a four-year+ degree; 80 percent White; 53% married).

Respondents were asked to carefully consider each finfluencer post and then assess them using a 5-point Likert scale (from “strongly disagree” to “strongly agree”) developed around the following five question items as an indicator of overall respondent favorability:

I believe this is good advice.

I would follow this advice.

I trust this advice.

I find this advice relatable to me.

I would share this advice with my friends/family.

To test for internal consistency and be sure that our index is reliable when averaging across these five assessment items, we calculated Cronbach’s alpha, which was found to be α > 0.92 for each post displayed. This is a very high level of scale reliability (a common heuristic is that α > 0.70 is acceptable and α > 0.80 is good), so averaging across response items will concentrate the signal and reduce noise (Tavakol and Dennick 2011).

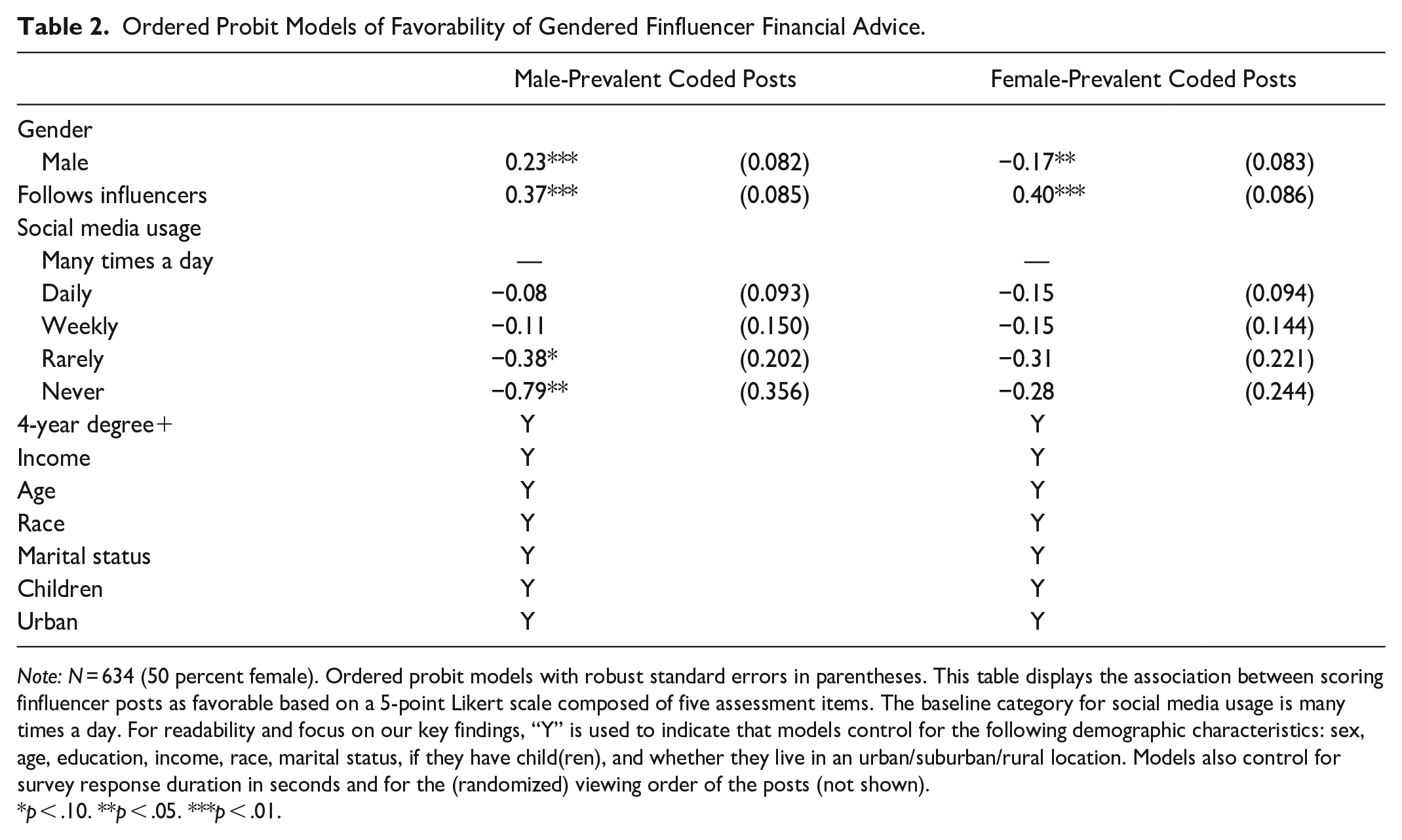

Based on this index, we estimate ordered probit models, which is an appropriate methodology for analyzing ordinal data based on agreement or personal attitudes, where the “distances” between choices are subjective and nonequidistant (and for which linear regression models are inappropriate; Daykin and Moffatt 2002). Positive coefficients thus correspond with higher overall favorability: better advice (i.e., higher perceived quality), advice that they would more likely follow themselves, more trusted advice, more relatable advice, and advice they would more likely share.

Study 2 Findings

We segment our analysis to focus on those posts that most strongly exemplified female-prevalent and male-prevalent codes based on our comparative indexing described previously. This allows us to better isolate the influence of gendered messaging on audience reactions.

Here, we see clear evidence of implicit gender biases in the assessment of financial advice posts (see Table 2). The positive and significant coefficient for “male” under the male-prevalent coded column indicates that men in our sample rate posts exhibiting more masculine rhetoric more favorably across the attitudinal index captured by our dependent variable. Conversely, the negative and significant coefficient for “male” under the female-prevalent coded column indicates that female respondents view posts containing feminine content or rhetorical patterns more positively. Together, this suggests meaningful preference divergence by gender identity. If reactions were truly neutral, we would expect the respondent gender to be nonsignificant in both models.

Ordered Probit Models of Favorability of Gendered Finfluencer Financial Advice.

Note: N = 634 (50 percent female). Ordered probit models with robust standard errors in parentheses. This table displays the association between scoring finfluencer posts as favorable based on a 5-point Likert scale composed of five assessment items. The baseline category for social media usage is many times a day. For readability and focus on our key findings, “Y” is used to indicate that models control for the following demographic characteristics: sex, age, education, income, race, marital status, if they have child(ren), and whether they live in an urban/suburban/rural location. Models also control for survey response duration in seconds and for the (randomized) viewing order of the posts (not shown).

p < .10. **p < .05. ***p < .01.

These gender preferences persist even when controlling for various demographic factors, social media usage, and influencer following habits. This implies that the tacit gender coding within the financial advice content itself is likely driving the differences in reception by men and women. Irrespective of platform familiarity or general engagement with influencers, the subtle integration of masculine versus feminine themes, assumptions, figures of speech, and messaging frames appears to resonate differently across gender identity lines. It is worth noting that these patterns remain consistent when focusing solely on the three static posts from each category, excluding the video content that might unintentionally hint at the finfluencer’s identity, suggesting the robustness of these gendered preferences across different types of content presentation.

Study 3 Methods

In addition to evaluating the finfluencer posts, we also asked respondents at the end of the survey what they thought the study was about. Several respondents indicated they thought the study was about financial advice and social media, but not one respondent indicated gender or anything close to it—suggesting that study respondents were not consciously aware of their preference for same-gendered financial advice.

Pursuing this, we conducted a brief follow-up study using a new sample (N = 296; 51 percent female; median age = 40; median income = $50,000–$59,000; 60 percent with four-year+ education; 76 percent White; 49 percent married) in which we asked respondents to explicitly evaluate the gender tilt of each post’s content. They viewed the same still image posts as previously described in randomized order but were asked, “How would you best describe the content of this post: masculine; feminine; or neither/gender-neutral?”

Study 3 Findings

Our analysis revealed a striking consensus among respondents: The modal response for each post was gender-neutral by both male and female participants. This uniformity suggests a widespread perception that the financial advice presented through social media posts is devoid of gender bias irrespective of the respondent’s gender. This observation, which aligns with people’s stated preferences for neutral advice in Study 1, is particularly intriguing when juxtaposed with the findings from Study 2, which identified distinct gender preferences in the consumption of financial advice. Despite these implicit preferences, individuals, on average, do not seem to consciously perceive or acknowledge the gendered framing of the advice they encounter on social media platforms.

Although it is important to consider the possibility of social desirability bias in any study involving self-reported gender perceptions, there are some compelling reasons to believe that such bias did not significantly influence our results or their interpretation. First, the consistency of the gender-neutral modal response across both male and female participants suggests that this pattern is not merely a reflection of one gender group’s heightened sensitivity to bias perceptions. If social desirability were a major factor, we might expect to see greater divergence between men’s and women’s responses given that previous research has shown that women tend to exhibit stronger social desirability tendencies in gender-related contexts (Dalton and Ortegren 2011). Second, the fact that participants in Study 2 implicitly responded to the gendered patterns in the content despite not explicitly recognizing them in Study 3 suggests that the “neutrality illusion” is a genuine perceptual phenomenon rather than a mere artifact of self-presentation. If participants were, in fact, aware of the gendered nature of the content but deliberately suppressed this perception in their Study 3 responses, it is unlikely that they would have shown such clear implicit preferences in Study 2.

Discussion and Conclusions

The popularity of finfluencers on social media platforms has dramatically transformed the landscape of financial advice, making it more public and accessible than ever before (Hayes and Ben-Shmuel forthcoming). Indeed, millions of individuals globally are now engaging with finfluencers, turning to platforms such as Instagram, TikTok, and YouTube for insights into investing, budgeting, and financial planning. According to data from the global financial firm Nartallo (2021), at the end of 2021, the hashtag #FinTok on TikTok had over 500 million views and #investing over 3.7 billion. On Instagram, #financialfreedom appears in more than 10 million posts and #investing in nearly 12 million—just a small indicator of the vast and ever-expanding universe of financial guidance available to the online public (Nartallo 2021). This burgeoning interest underscores a significant change in how financial advice is sought and disseminated, with social media emerging as a key player in the democratization of financial knowledge.

The transition toward digital platforms for financial advice has not only broadened access but has also introduced a diverse range of voices and perspectives into the financial discourse. This shift, therefore, also provides a unique opportunity to explore the nuanced ways gender shapes the creation and reception of financial content. Our mixed-methods empirical research sheds light on the interplay between gender, communication styles, and audience engagement within the increasingly popular finfluencer domain.

Qualitative analysis of hundreds of finfluencer posts revealed that in addition to different aesthetic choices, both male and female finfluencers embed meaningfully distinct perspectives into their messaging. Men finfluencers tend to focus, for example, on quantitative aspects of finance, utilizing numbers and graphs to convey their messages, whereas women more often incorporate narratives and personal stories, connecting financial decisions to broader life goals and personal well-being. This divergence not only highlights gendered assumptions and orientations within financial messaging but also suggests that these differences extend to the very core of how financial advice is framed and understood. By embedding distinct perspectives into their content, finfluencers are not merely sharing financial advice; they are also shaping the discourse around personal finance and contributing to new financial subjectivities (Lai 2017), making it more relatable and accessible to a broader audience. This inclusivity is crucial in a financial landscape that has traditionally been exclusive and intimidating for many. It opens up new pathways for financial empowerment, encouraging individuals to engage with financial content that resonates with their own experiences and aspirations.

At the same time, our quantitative studies reveal a contradiction in how such gendered content is received by audiences. When directly asked, strong majorities assert a preference for impartial, universally relevant guidance. However, exposing participants to anonymized posts exhibiting what we coded as highly gendered themes uncovered unconscious affinity along identity lines—men gravitated toward content coded as more thematically masculine, and women favored more feminine posts. This discrepancy between stated and revealed preferences carries implications regarding deeply embedded socio-cognitive frames that shape knowledge consumption and credibility assessments around finance. Even without knowing the advisor’s gender, advice recipients may subconsciously favor approaches that align with the roles and behaviors they have internalized as appropriate or effective for their gender. Although individuals may genuinely express a desire for impartiality, they still operate based on embedded social perspectives that shape deeper affinities.

Respondents, furthermore, seemed unable to consciously detect gendered nuance in the financial advice on social media, or perhaps these differences are more understated than anticipated. As researchers, we had the benefit of closely following dozens of finfluencers over many months, meticulously analyzing hundreds of posts to discern tacit patterns that casual users could likely overlook. Our process granted a privileged vantage point to uncover themes that audiences themselves may struggle to identify. Still, people appear to pick up on indirect, gender-related cues in the advice itself, such as communication style, topics emphasized (e.g., budgeting vs. investing), or the approach to risk. These cues, although not explicitly revealing the gender of the advice giver, may align with recipients’ internalized expectations of gendered communication, leading to a subconscious preference for advice that “feels like” it comes from someone with a similar social identity.

The unconscious gender alignment we discovered appears paradoxical on its face, yet it may not be entirely problematic. Rather than stemming from exclusionary motives, these latent preferences could signify that integrating subtle diversity actually enhances relevance and trust for audiences. Financial messaging that resonates with internalized worldviews and lived experiences across gender lines may garner more trust and relatability even when the high-level guidance seems equivalent in substance. If so, this suggests strictly impartial communication risks adhering to dominant paradigms that have marginalized certain identities and perspectives.

To be sure, conventional financial advice from mainstream sources is often not as gender-neutral as often purported. Instead, it has long situated financial participation and competence as one of masculinity (Crosthwaite et al. 2022). Much advice directs individuals, regardless of who they are, to perform the same certain analyses, calculations, and estimations—and extant research shows that men, on average, perform objectively better than women on tasks relating to mathematics and applied numeracy skills net of educational attainment (Cook 2018). This pertains to a normative type of advice that prescribes what one should do to achieve the best possible financial outcomes, but this is not the only type of advice offered. Another type—informative advice—offers material that allows an individual to make informed decisions on their own. This type of financial guidance is frequently found online, in magazines such as Money or Kiplinger, and in the marketing materials of financial services companies. Boggio et al. (2017) looked at such marketing materials targeting novice investors in the United States, Holland, and Italy. They identified a prevalence of metaphors used in this material that stem from conceptual domains customarily associated with masculinity: war (e.g., “the market is a battlefield”), fitness/physical activity (“ride out a downturn”), games (“beat the market”), farming (“grow your wealth”), and the bodily senses (“taste success”). Their conclusion is that the language of typical investor communication may surreptitiously engender feelings of familiarity and belonging among men but create feelings of distance and exclusion among women (Boggio et al. 2017).

In light of these insights, the finfluencers appear to offer a compelling counterbalance to traditional financial advice paradigms, presenting a more inclusive and varied financial narrative that can engage a broader demographic. The diversity in communication styles and content focus between men and women finfluencers not only enriches the financial advice landscape but also challenges existing stereotypes about who financial advice is for and how it should be delivered (see Chang 2005). This evolution toward a more inclusive discourse has the potential to bridge gaps in financial literacy and empower individuals across the gender spectrum and beyond by providing access to advice that resonates more closely with their personal experiences and perspectives. Indeed, although not the focus of this article, the diversity of finfluencers extends beyond gender, encompassing important factors such as race, ethnicity, socioeconomic status, family background, and more—each layer adding depth to the financial narratives being shared. The intersectionality present within the finfluencer community can further enhance the relevance and accessibility of financial advice, making it more reflective of a broader range of lived experiences. More research is needed to explore these other aspects.

Additionally, the implicit gender biases in audience preferences for financial content highlight the complexity of financial education and engagement policy in the digital age. Although efforts to create gender-neutral financial education and advice are commendable, they should be balanced with an understanding of the subtle ways in which individuals relate to and act on this information. Addressing unconscious biases can lead to more effective financial communication strategies that cater to many needs and preferences, thereby enhancing financial inclusion and literacy.

To be sure, the gendered nature of financial advice may have inadvertent consequences for economic inequality. Our findings suggest that men tend to gravitate toward male-coded discourse emphasizing wealth accumulation and risk-taking, whereas women favor female-coded content prioritizing budgeting and saving. These divergent preferences could shape financial behaviors and outcomes, with women potentially adopting more conservative strategies that prioritize short-term stability over long-term growth (Charness and Gneezy 2012; Fonseca et al. 2012). Conversely, men’s exposure to content promoting investment and risk-taking may encourage financial behaviors that lead to higher returns but also greater volatility (Barber and Odean 2001). Over time, these gendered patterns might exacerbate the gender wealth gap because men may seek to accumulate wealth more rapidly and women’s financial growth may be constrained by a conservative focus on savings and security (Neelakantan and Chang 2010).

Moreover, the consistent exposure to different types of gendered advice may lead to divergent financial knowledge and skills. To counter potential disparities, financial educators and policymakers should strive to provide more balanced, inclusive guidance that empowers both men and women to engage in a full range of financial strategies (Lusardi and Mitchell 2014). By fostering a more equitable financial advice landscape, we can work toward reducing gender disparities in financial outcomes and promoting greater financial well-being for all.

Ultimately, our findings call for a more thoughtful approach to financial advice—one that acknowledges the inherent gender dynamics at play and leverages them to foster a more engaging, relatable, and inclusive financial discourse. As the digital landscape continues to evolve, so too should our strategies for financial education and empowerment, ensuring that they are responsive to the diverse realities of their audience while at the same time recognizing the potential for tacitly gendered financial messaging to reinforce stereotypes in financial contexts. By embracing the complexity and richness of gendered financial messaging, we can move toward a future where financial advice is not only widely accessible but also deeply resonant and empowering for all individuals regardless of gender.

Supplemental Material

sj-docx-1-srd-10.1177_23780231241267131 – Supplemental material for The Gendered Language of Financial Advice: Finfluencers, Framing, and Subconscious Preferences

Supplemental material, sj-docx-1-srd-10.1177_23780231241267131 for The Gendered Language of Financial Advice: Finfluencers, Framing, and Subconscious Preferences by Ambreen Tour Ben-Shmuel, Adam Hayes and Vanessa Drach in Socius

Footnotes

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.