Abstract

Studies of social capital usually emphasize its prosocial, deviance-reducing effects. This article instead explores its negative potential. The authors focus on the relationship between different forms of community-level social capital and tax avoidance by wealthy Americans, using data from the Panama Papers leaks to analyze the residential communities of Americans who engaged in offshore tax avoidance. The analysis demonstrates, first, that communities with more civic organizations are more likely to have tax avoiders. This finding suggests that civic organizations may promote cohesion among wealthy elites, producing insular attitudes and deviance. Second, income inequality correlates with tax avoidance, indicating that highly unequal communities have more insular elites. Finally, more patriotic communities have lower tax avoidance. These findings empirically establish the concept of “negative social capital” and advance the distinction between bridging (or cross-group) social capital, which lowers deviance, and bonding (or within-group) social capital, which is actually associated with greater elite deviance.

Sociologists have long argued that social capital, which refers to community connectedness and cohesion, can have both positive prosocial impacts on society and negative, antisocial implications (Fukuyama 2001; Portes 1998; Putnam 2000). Putnam (2007) specified two central forms of social capital that can lead to these outcomes. Bridging social capital refers to connectedness across social boundaries, such as class or ethnicity, and such connectedness generally presents advantages to broader society (e.g., by producing more engaged and committed citizens). Bonding social capital refers to connectedness within a social group (e.g., by people who share the same class or ethnic background). Bonding social capital may sometimes advantage community members but it can also harm the broader community by promoting insular norms, resulting in “negative social capital” (Portes 1998; Warren 2008). Although the dual nature of social capital has been widely acknowledged, empirical studies tend to focus almost exclusively on its prosocial function (Portes 1998; Warren 2008). In this study, we empirically analyze the association between social capital and a mostly overlooked deviant behavior: tax avoidance by wealthy elites. By studying this important and timely phenomenon, we hope to shed new light on the antisocial dimensions of social capital.

We use the Panama Papers leaked by the International Consortium of Investigative Journalists (ICIJ) in 2016, which revealed thousands of individuals who held shell companies in tax havens. The leak sparked a worldwide interest, revealing a parade of high-profile figures who held offshore shell companies, including among others, the king of Saudi Arabia; former prime ministers and presidents from Argentina, Italy, and Iceland; and athletes such as Lionel Messi and Tiger Woods (Chittum 2016; Martinez 2016). Beyond exploring the vices of politicians and celebrities, the leaks provided a rare opportunity for scholars to learn more about tax havens and their public perception. 1 We draw on data from the Panama Papers to analyze the relationship between community-level social capital and the readiness of wealthy elites to engage in offshore tax avoidance.

Specifically, we use the Panama Papers leaks to analyze the social capital of communities where U.S. tax avoiders live. We extracted 2,732 unique residential addresses of U.S.-based persons who have used offshore shell companies and geolocated them in census tracts. 2 Using data from the American Community Survey (ACS) and other sources, we focus on three community characteristics that have been shown to capture elements of social capital: civic organizations, economic inequality, and patriotic behavior.

Our findings show that social capital is in fact significantly associated with offshore tax avoidance. However, our exploratory correlational analysis did not find the simple negative association between social capital and tax avoidance that the literature might lead us to expect. In fact, different aspects of social capital show different relationships with tax avoidance. First, we found that tracts with a higher number of civic organizations have higher levels of tax avoidance, even when controlling for other factors. This challenges previous literature from de Tocqueville ([1835] 2003) to Putnam (1993, 2000), which argues that civic organizations promote trust and cooperation between members of a community and spill over into broader society (i.e., promoting bridging social capital). We propose that civic organizations may in some cases facilitate elite socialization (Cousin and Chauvin 2017; Mills 1956) and thereby contribute to the formation of insular norms through bonding social capital. This hypothesis is bolstered by evidence showing that this relationship is driven by nonreligious organizations and is stronger in tracts with smaller numbers of immigrants. Income inequality in a community is also positively associated with tax avoidance, which could be because large income gaps preclude the emergence of bridging social capital. Finally, we find that community-level patriotic behavior, captured by compliance with the U.S. census and military service (Abascal and Centeno 2017), is associated with lower levels of tax avoidance. This supports the hypothesis that patriotism operates as bridging social capital at the community level (Szreter and Woolcock 2004) and is thus associated with lower deviance by elites.

Before proceeding, we should clarify our terminology. Tax avoidance refers to the use of legal means to avoid paying taxes, and tax evasion refers to illegal means. The individuals mentioned in the leaks have owned or used shell companies, which are companies without active business operations that are often used to conceal ownership and move funds discreetly (Martinez 2016). Therefore, if a person or firm appears on the list it does not automatically mean that they engaged in any illegal activities. 3 However, at least some of the people mentioned in the leaks did commit illegal tax evasion: two Americans have already been convicted of tax-related crimes in the wake of the Panama Papers, and other investigations are under way in the United States and elsewhere (Fitzgibbon 2021). As our data do not allow us to distinguish between legal and illegal behaviors, we use the cautious term tax avoidance throughout the text.

Social Capital: An Antidote to Deviance?

Social capital refers to the degree of connectedness in society and the benefits that connectedness produces, including trust and cooperation (Abascal and Baldassari 2015; Coleman 1988; Portes 1998; Portes and Vickstrom 2011; Putnam 2000). According to Coleman (1988), social capital consists of (1) groupwide obligations, expectations, and trust; (2) a constant flow of information among group members; and (3) the enforcement of social norms (pp. 101–105). We focus on social capital as a characteristic of communities and set aside conceptualizations that treat it as an individual resource (e.g., Bourdieu 1985).

The traditional approach to social capital treats it as a powerful antidote to crime and deviance, meaning violation of social norms (Putnam 1993, 2000; Sampson, Raudenbush, and Earls 1997). A dense social network leads to frequent and intense interactions that provide group members with constant reminders of social norms and exposes them to the judging eyes of others. This social monitoring facilitates cooperation and reduces opportunism (Putnam 2000:18–19). The benefits of group-level social capital extend to all community members, regardless of their individual attitudes or connectedness. As Putnam (2000) noted, If the crime rate in my neighborhood is lowered by neighbors keeping an eye on one another’s homes, I benefit even if I personally spend most of my time on the road and never even nod to another resident on the street. (p. 17)

These positive effects are expected to flow over to broader society and produce more cooperative, trusting and rule-following citizens. Indeed, scholars have found associations between social capital and a range of positive outcomes in education, crime rates, economic growth, health, and well-being (Abascal and Baldassari 2015; Portes 1998; Putnam 2000; Sampson et al. 1997; Slemrod 1998; Wilkinson and Pickett 2009).

Putnam (2000, 2007) and others have pointed out two distinct forms of social capital. Bridging social capital connects individuals across groups. Through interactions and institutions, it spreads social norms to broader society, promoting prosocial behaviors and attitudes. Patriotism constitutes a particularly potent subtype of bridging social capital that includes trust and cooperative attitudes vis-à-vis the nation-state (see Abascal and Centeno 2017; Szreter and Woolcock 2004). 4 Bonding social capital, meanwhile, connects individuals within bounded social groups such as social classes or ethnic groups. It may lead to the adoption of broader trust and social norms in some cases but does not necessarily do so (Warren 2008).

Some scholars challenge the optimistic view of social capital, invoking the potential perils of bonding social capital (Warren 2008). They argue that social capital may also encourage elitism and insularity. The term negative social capital (Portes 1998), for example, refers to situations in which strong in-group solidarity comes at the detriment of the rest of society. As Fukuyama (2001) noted, “Both the Ku Klux Klan and the Mafia achieve co-operative ends on the basis of shared norms, and therefore have social capital, but they also produce abundant negative externalities for the larger society in which they are embedded” (p. 8). Ethnic groups may also produce negative social capital: in a society made up of internally cohesive ethnic groups, it is difficult to achieve a sense of overarching solidarity and shared rules (Fukuyama 2001; Henrich 2020; Wimmer 2018). Beyond criminal organizations and ethnic communities, elites provide another example of the negative potential of bonding social capital. Cohesive elites are more likely to pursue their interests as a class, which often comes at the expense of the rest of society (Domhoff 1967; Khan 2012; Mills 1956; Warren 2008; Winters 2011). Well-connected, cohesive elites are also likely to develop their own set of norms and pay less heed to the rules of society (DiMaggio and Garip 2012). Bonding social capital, then, can also promote antisocial behaviors. For such negative social capital to emerge, there is no need for the subgroup to be explicitly hostile or predatory vis-à-vis broader society: it suffices that its norms differ from those of the rest of society.

Although the double-edged nature of social capital is generally acknowledged in theory (e.g., DiMaggio and Garip 2012; Fukuyama 2001; Portes 1998), in practice most studies emphasize its positive aspects (e.g., Putnam 2000) and do not empirically examine its negative potential. In this study, we use prevalent measures of social capital to investigate its relationship with an important antisocial phenomenon: tax avoidance by wealthy U.S. elites.

Social Capital and Tax Avoidance

Tax avoidance (and its counterpart tax compliance) is a highly appropriate setting for the study of social capital and deviance because paying taxes is a prime example of norm-following behavior that serves the greater good. Tax obligations pose an individual cost for public benefit. Traditionally, economists assumed that tax compliance was a function of tax rates and fear of being caught and punished (Clotfelter 1983; Poterba 2001). Although tax obligations are enforced through occasional audits, scholars have more recently shown that the decision to pay, or to avoid paying, taxes is strongly influenced by social and psychological factors, including a sense of duty, norm adherence, and peer influence (Luttmer and Singhal 2014). Thus, actual levels of tax compliance are much higher than the levels expected on the basis of fear of punishment alone (Alm and Gomez 2008; Alm and Torgler 2006; Kogler et al. 2013; Torgler and Schneider 2009).

Scholars have used the term tax morale to describe the “nonpecuniary motivations for tax compliance as well as factors that fall outside the standard, expected utility framework” (Luttmer and Singhal 2014:150). Luttmer and Singhal (2014) listed three main factors that shape tax morale and, through it, tax avoidance: institutions, values, and social context. All three are intertwined with community social capital. Additionally, existing literature has identified several individual-level predictors of tax morale that are potentially connected to social capital. Such predictors include respondents’ trust in others and in state institutions, adherence to norms, national pride, political engagement, and religiosity (Alm and Gomez 2008; Konrad and Qari 2012; Lefebvre et al. 2015; Scholz and Pinney 1995; Slemrod 1998; Torgler and Schneider 2009). To some extent, these factors reflect durable individual attitudes. However, they are also very likely to be affected by social context, namely the degree of connectedness and cohesion in respondents’ communities of residence. From that perspective, tax avoidance constitutes a form of social deviance, especially in high-compliance countries such as the United States.

Elite tax avoidance offers a particularly promising case for studying the relationship between tax avoidance and social capital because elites serve as a bounded group on the one hand, and a group deeply invested in the state and its infrastructure on the other. Wealthy Americans often emphasize hard work and prudence in their self-legitimizing discourses (Khan 2011; Sherman 2018). This demonstrates adherence to broader social norms associated with the middle class. Wealthy elites are also often politically engaged and socially influential (Cook, Page, and Moskowitz 2014), suggesting a sense of responsibility vis-à-vis broader society. On the other hand, cohesive elites are known to adopt alternative norms that are indifferent to the general good (Farrell 2020; Khan 2011; Mears 2020). This may be particularly pertinent in domains such as taxation, where elite preferences and interests may diverge from the rest of society (Winters 2011). Thus, social capital among elites can potentially carry both bridging and bonding functions, promoting either elite tax compliance or elite tax avoidance.

Our study builds on earlier sociological work that has demonstrated the role of community-centered social capital in elites’ decision making. Young et al. (2016) showed that American millionaires’ residential choices are less affected by state-level tax rates than popular debates suggest. The authors interpreted this finding as indicating wealthy elites’ “embeddedness” in their local communities, stating that they possess “place-specific social capital” (p. 424; see also Young 2017). In other words, social capital may help keep high earning elites in their communities even when they stand to reduce their tax burden by moving away. Our study takes the problem of elites, taxes, and social capital a step further, investigating multiple unexamined aspects of elite embeddedness.

Elite tax avoidance is also important because of its economic consequences. A substantial proportion of the world’s total financial wealth, around eight percent by some estimates, is held in offshore tax havens such as the British Virgin Islands, the Cayman Islands, Bermuda, and Switzerland, mostly by the ultrarich (Alstadsæter, Johannesen and Zucman 2018, 2019; Harrington 2016; Zucman 2015). As a growing share of the United States’ wealth is concentrated in the hands of the top 0.1 percent (Atkinson, Piketty, and Saez 2011), the importance of their tax receipts is increasing, making this a crucial policy question. Although scholars have explored the wealth management industry behind tax havens (Harrington 2016; Shaxson 2011), there is still a lack of understanding of the social dynamics that govern their use. Existing literature on the community determinants of crime and deviance, meanwhile, tends to focus on low-income and marginalized communities (e.g., Sampson et al. 1997). Expanding our understanding of the relationship between social capital and elite deviance is of great importance.

Research Hypotheses

We focus on the relationship between prominent indicators of social capital and elite tax avoidance. We assume that social capital indicators associated with increased tax avoidance capture bonding social capital and, conversely, that indicators associated with lower tax avoidance capture bridging social capital. Some indicators are unequivocally bridging or bonding and we expect them to be negatively or positively associated with tax avoidance, respectively. Other indicators, however, can be either bridging or bonding. We examine the canonical predictor of social capital, civic organizations, and the predictor that is arguably most pertinent to harboring elite wealth, economic inequality. Both these characteristics can function as either bonding or bridging social capital. We also investigate patriotic behavior as a predictor that is most likely to represent bridging social capital. In selecting these three predictors, we made sure to cover the three arenas that shape tax avoidance (Luttmer and Singhal 2014): institutions (i.e., organizations), values (i.e., patriotism), and social context (i.e., economic inequality).

First, we examine civic organizations, including religious and nonreligious organizations, as they are often seen as the prototypical component of bridging social capital. Putnam (2000) famously argued that a decades-long decline in civic organizations since the 1960s contributed to a loss of general trust by Americans. Putnam drew on the classic work of de Tocqueville ([1835] 2003), who viewed civic associations as an arena where community members and more broadly citizens interact and cooperate in a rational manner. According to social capital theory (Portes 1998; Putnam 2000), civic organizations boost bridging social capital, making community members more trusting, cooperative and compliant not only in their relations with one another but also in relation to society overall. A higher density of social organizations (such as bowling clubs or churches) may thus depress tax avoidance by fostering more frequent and intense interactions between community members, thereby increasing the spread and/or enforcement of social norms such as tax compliance. This leads to the expectation that communities with higher numbers of civic and religious organizations will show lower levels of tax avoidance through the use of offshore companies (Hypothesis 1a).

An alternative perspective on civic organizations, meanwhile, emphasizes their potential to strengthen bonds among those who are alike and thereby contribute to insularity. Civic organizations are often a site for elite socialization (Cousin and Chauvin 2017; DiMaggio 1982; Farrell 2020). Wealthy Americans are disproportionately active in political organizations (Cook et al. 2014), and it is plausible that they are overrepresented in other kinds of organizations as well. This suggests that civic organizations may contribute to in-group (bonding) social capital among the rich while lowering out-group (bridging) connections to broader society. Thus, a high density of civic organizations in a community may also encourage the development of insular elite norms, facilitate the spread of tax avoidance strategies, or broker professional contacts that facilitate greater tax haven use. The potential of civic organizations to promote bonding social capital leads to the hypothesis that tracts with higher numbers of civic organizations will show higher rates of tax avoidance (Hypothesis 1b).

There are several ways in which bonding civic organizations may increase tax avoidance. Elite clubs and golf courses may offer opportunities for elite bonding, but religious and ethnic organizations may also be associated with increased tax avoidance as norms and knowledge are shared among wealthy members of religious or ethnic communities (Fukuyama 2001; cf. Hien 2021; Portes 1998; Warren 2008). If civic organizations promote bonding social capital, leading to greater tax avoidance (Hypothesis 1b), it is important to investigate whether such a correlation is particularly high in religious or ethnic communities.

Another indicator of community-level social capital that may be relevant for global elites who use offshore tax havens is income inequality. Elite tax avoidance by definition removes the resources of the wealthy from national communities that are, on average, poorer than those elites. Examining income inequality on the community level allows us to assess whether the local aspects of economic inequality might be related to this decision. We again test two competing hypotheses connecting community-level income inequality and elite tax avoidance. One approach posits that socioeconomically diverse communities would be characterized by higher levels of bridging social capital. When people of different socioeconomic levels share a neighborhood, they are forced into constant contact and, potentially, are forced to cooperate over local issues. According to the contact hypothesis (Allport 1954), this kind of interaction should reduce prejudice and foster a cross-class sense of connectedness. Indeed, numerous studies have demonstrated the negative impact of residential segregation on poor Americans and pointed out the higher public efficacy in socioeconomically diverse neighborhoods (Reardon and Bischoff 2011; Sampson et al. 1997). Sherman (2018) argued that wealthy families that live in poorer neighborhoods engage in downward comparisons with their neighbors, leading them to appreciate their economic fortune and sport more prosocial attitudes. Wealthy families living in wealthy neighborhoods, in contrast, engage in upward comparisons, leading them to consume more as part of a status competition. Thus, there are several potential mechanisms by which communities with a higher level of income inequality will show lower rates of tax avoidance (Hypothesis 2a): wealthy individuals may come in direct contact with less resourced individuals, increasing their empathy and reducing their desire to withhold taxes from their community. Proximity to less resourced neighbors engender such empathy simply by noticing less expensive homes, worse infrastructure, or worse-funded public institutions. Conversely, those who live in more economically homogenous areas may be less aware of such plights, and more comfortable shielding their own funds from taxation.

An alternative approach suggests that residential proximity does not in itself create solidarity across social classes (i.e., bridging social capital). On the contrary, large income gaps would enhance the tendency of different social classes to follow different social norms (see Lamont 1992), lowering the potential for the enforcement of community-wide norms. Inequality is generally known to reduce trust and cooperation (Xu and Marandola 2023). Specifically, conflicts of interest rooted in economic differences may inhibit civic cooperation and create an antagonistic environment. Indeed, high income inequality in a community is associated with lower levels of trust, higher rates of violence and worse health outcomes (Portes and Vickstrom 2011; Wilkinson and Pickett 2009). The deleterious effect of inequality on bridging social capital is expected to be particularly strong for wealthy elites, who may be distrustful vis-à-vis their less affluent neighbors. From this perspective, wealthy individuals will become more aware of their neighbors’ circumstances by proximity but rather than inducing feelings of empathy or care, proximity will induce fear, repugnance, or anxiety and thus additional resource hoarding. This leads us to expect that communities with higher income inequality would exhibit higher rates of offshore tax avoidance (Hypothesis 2b).

Finally, to complement community characteristics that potentially carry multiple forms of social capital, we include the most unambiguous form of social capital that is commonly associated with tax compliance: patriotism, which we treat as a form of bridging social capital (Gangl, Torgler, and Kirchler 2016; Konrad and Qari 2012). Because we want to capture patriotism as a form of social capital and not a proxy for partisanship (Bonikowski 2016), we focus on patriotic behavior rather than ideals. We follow Abascal and Centeno (2017) in operationalizing patriotic behavior using military service and census participation. We choose these behaviors over political donations and voting, the other two patriotic behaviors examined by Abascal and Centeno, as they are less explicitly political. We measure military service using the percentage of veterans in the community, which indicates residents’ willingness to voluntarily engage in pro-nation-state behaviors (Abascal and Centeno 2017). Military service is arguably a strong indicator of patriotic behavior as it involves joining a total institution. Yet military service is also highly associated with socioeconomic status (Bachman et al. 2000). We therefore also include a second measure: census mail-in response rate, which requires less effort than military service, but is a less skewed measure capturing community members’ level of voluntary compliance with nation-state institutions (Abascal and Centeno 2017). It is an indicator of voluntary compliance because citizens are requested to mail in their census forms, but there is no penalty for neglecting to do so. The potential mechanism here is that observing higher levels of patriotic behavior that requires some sacrifice will induce greater feelings of belonging, solidarity, and prosocial behavior. Communities with higher shares of veterans (Hypothesis 3) and higher rates of census response (Hypothesis 4) would then exhibit greater trust in institutions, including tax authorities, leading us to expect that these measures will be negatively associated with community-level elite tax avoidance (Konrad and Qari 2012; cf. Szreter and Woolcock 2004).

The Case: Offshore Tax Avoidance

The term tax havens usually refers to jurisdictions that offer favorable legal regimes for moving and holding funds, such as the Cayman Islands, Jersey, or Luxembourg. With the help of specialized professionals, economic elites transfer money to these jurisdictions and register legal entities that hold these funds (Harrington 2016; Martinez 2016). The main advantage is confidentiality. With an offshore account, one can hide wealth from tax authorities or anyone else. Not all offshoring is used for tax avoidance, but it is a key avenue for tax avoidance by economic elites (Alstadsæter et al. 2019; Zucman 2015). Zucman (2015) estimated that the total global offshore wealth was at least $7.6 trillion, and about $200 billion is lost in tax revenue globally each year. Despite their importance, offshore havens have been understudied because of the difficulty of obtaining precise data.

Unlike simpler tax avoidance behaviors such as concealing income or manipulating the timing of gifts, offshoring funds requires substantial expertise and legal work. It therefore leaves a paper trail that can serve as a basis for analysis. The offshore wealth held by Americans is low by international standards; for example, in 2007 it was equal to 7.3 percent of the nation’s gross domestic product, lower than the European average of 12.8 percent (Alstadsæter et al. 2018). Still, Zucman (2015) estimated that approximately $35 billion is lost to the Internal Revenue Service annually. Focusing on the United States allows us to study tax avoidance in a country with high tax compliance, where strategies such as the use of offshore tax havens are stigmatized by most members of society (Torgler and Schneider 2009:241). The relative rarity of tax avoidance in the United States allows us to analyze it as a case of elite deviance.

Until now, it has not been possible to directly examine the relationship between community context and tax behavior like tax haven use. Scholars have mostly relied on surveys that asked individual respondents about their tax morale (i.e., declared attitudes) and, in some cases, their tax behavior (e.g., Alm and Gomez 2008; Halla 2012). 5 The reliance on surveys means that the units of analysis were individuals and not communities, making it difficult to detect community effects (see, however, Torgler and Schneider’s [2007] comparison of large political units within European nations). More crucially, existing analyses of tax compliance relied on self-reported attitudes and behaviors. Self-reporting is susceptible to social desirability bias, which becomes especially problematic when trying to understand deviant behavior that respondents may be wary of disclosing. In the present study, in contrast, we analyze tax avoidance in situ, using data on behavior of tax haven use that allow us to establish variation across communities.

Data and Variables

Data

To study offshore tax avoidance, we use a unique, original dataset based on leaked data on offshore wealth held by Americans. The data were released by ICIJ and include the “Panama Papers,” “Paradise Papers,” “Bahamas Leaks,” and “Offshore Leaks.” The files contain multiple data sources from different time periods between 2010 and 2016 covering a wide range of jurisdictions. For example, the Paradise Papers, leaked in 2016, came from two firms and 19 government corporate registries (ICIJ n.d.). Leaked data provide a unique opportunity to analyze the use of offshore havens as they allow us to overcome the problems of underreporting and social desirability bias that hinder the study of such stigmatized practices. Scholars have used these data to explore tax lawyers’ ethical responsibilities (Field 2017) and the effects of leaks on firm success (O’Donovan et al. 2019), but to the best of our knowledge this is the first examination of private individuals who offshore wealth. We use these data to identify 2,732 unique residential addresses of tax avoiders in the United States, and to analyze the characteristics of the census tracts where they are located, drawing on data from the ACS and other sources.

After downloading the full dataset from the ICIJ website, we excluded non-U.S. addresses from the files, leaving 4,110 individual records. We extracted residential addresses of individuals who use tax havens, geocoded them using the Google Maps application programming interface, and located them in census tracts. The procedure followed an institutional review board–approved protocol. The algorithm failed to geocode 14 cases, leaving 4,096 addresses. Some addresses were labeled “residential,” but most were ambiguously labeled “registered address.” These addresses are mostly the “on file” addresses used internally by the service providers whose data were leaked (on the basis of personal correspondence with the ICIJ). Although some of the individuals identified in the leaks may have multiple residences, the fact that these were the only residential addresses on file for the purposes of mailing, billing, and record keeping, increase the likelihood that these are their primary residential addresses. To purge the file of potential nonresidential addresses, we followed an iterative approach in which we sequentially excluded name fields with words such as LLP, LLC, Trust, and so on, and then examined the data until we no longer found such words. Then we used Google Maps to search all addresses that appeared potentially nonresidential (e.g., including the word suite) and eliminated those that appeared nonresidential. In particularly ambiguous cases, we searched the building name for its Web site online to see whether it was an apartment or office building. We deleted individuals with the same address so that any family with multiple individuals living together were collapsed into a single address-observation (as such, “individuals” in this article should be interpreted as individual households). For individuals with multiple addresses for which no primary address was indicated, we used the “mailing” address assuming individuals opt to receive mail where they reside. Finally, we used Stata’s matchit string matching package (Raffo 2020) on both the name and address fields, deleting any duplicate names or addresses, and hand-checking ambiguous cases. The final dataset includes 2,732 unique residential addresses of tax avoiders in the United States.

Despite potential biases associated with who ends up appearing in the leaks, there are two reasons to believe the data are not overly biased with regard to residential community characteristics, the only form of bias consequential for this analysis. First, the dataset aggregates four different leaks that are composed of many different data sources. The aggregation of multiple sources reduces the potential spatial bias introduced by any single source. Second, there are observations in 49 of 50 U.S. states (all but North Dakota), as well as Washington, D.C., indicating that observations are not spatially concentrated around a handful of firms or individuals. To suspect bias relating to community characteristics, we would have to believe that certain community characteristics correlate with the likelihood of an individual appearing in a leak without limiting the leak to a handful of specific communities. Keeping this in mind, as well as the absence of other nonbiased data on elite tax avoidance behavior (Piquero and Benson 2004; Simpson 2011), the leaked data serve as an appropriate, if imperfect, source for measuring the spatial distribution of elite tax avoidance in the United States.

Explanatory and Control Variables

After geocoding the leaked data, we aggregated observations of tax haven users into counts within census tracts, combining them with data from the 2009–2013 ACS five-year estimates and other sources. Because of their small size—69 percent of them have fewer than 5,000 inhabitants—census tracts have long been used to operationalize residential context (Sharkey and Faber 2014) with flows of social information and some degree of shared norms, and are therefore suitable spatial units for analyzing communities. We chose 2009–2013 ACS estimates and other 2010 covariates to provide community characteristics that are roughly contemporaneous with known residence dates of tax avoiders, as almost all observations were current within six years of 2010. Some observations from the leaked documents had “valid until” dates, which we understood as the most recent date the address listed was a known residence. Most observations, however, did not have such a date, which we assumed meant the address was valid at the time of each respective leak. The leaks spanned from 2010 to 2016, meaning that all were within six years of 2010. We performed a robustness check on the main analysis excluding the 406 addresses that were marked not valid within six years of 2010 and coefficients had the same directions and levels of statistical significance.

To measure the number of civic organizations in a tract we use the National Neighborhood Data Archive, which aggregates both nonreligious organizations such as social clubs and ethnic organizations and religious organizations such as churches and temples (Finlay et al. 2020). We operationalize income inequality using the tract-level Gini income coefficient: the higher the value, the more economically unequal. 6 Finally, we use percentage veterans in a tract and the tract response rate for the 2010 census, which captures the percentage of households that mailed back a completed census form of all households that received such a form, as measures of patriotism. Variable descriptive statistics are presented in Table 1.

Tract Descriptive Statistics.

We also use several control variables: percentage of individuals older than 25 years with a bachelor’s degree, proportion foreign born, proportion White, proportion of individuals older than 45 years, whether a tract is in a census metropolitan statistical area (to distinguish between urban and nonurban tracts), tract population, and (logged) median household income. Of these control variables, the racial and nativity composition of a tract may reflect aspects of its social capital. However, interpreting these variables raises significant challenges. Namely, unlike patriotism and civic organizations, which shape communities in ways that are more consistent across individuals (see discussion of Putnam 2000 above), nativity and race have dramatically different implications for community members with different attributes. In other words, the meaning of a community that is 80 percent foreign born is very different for its foreign-born residents and its native-born residents. As we do not have access to the race and nativity of the tax avoiders in this study, we include these variables as controls but do not assign hypotheses about their potential role in community social capital. Hypothetically, a similar concern can be raised about tract economic inequality, however we assume that individuals who use international tax shelters are closer to the top of the income distribution. Crucially, we offset (zero-inflated) count models by the number of high earners (>$200,000), essentially modeling the rate of avoiders per high earners, and include that variable as a control in other models used as robustness checks.

Methods

We use zero-inflated negative binomial (ZINB) regression to address the central problem with using leaked data to model counts: a high proportion of zero counts. A common challenge when dealing with data that have a large number of zeros (as is common with leaked data) is telling apart “true zeros”—in our case, tracts that actually have no tax avoiders—from excess zeros, which are tracts where tax avoiders are simply absent from the data. ZINB assumes two disparate processes for producing zeros and estimates them simultaneously. One process, estimated by a logistic function, determines which units have excess zeros. The other, estimated using a negative binomial distribution, estimates the count model beyond excess zeros. In interpreting the ZINB, we focus only on the negative binomial portion because we view the process producing excess zeros—the unknown process by which some tracts with tax avoiders were left out of the leak—as irrelevant for understanding the theoretical relationship between community factors and tax avoidance. As the process by which some tracts are left out of the data leaks is unknown, we include all available independent variables and controls in both portions of the model.

We ran tract-level ZINB models to test each of our hypotheses, including tract-level controls and state fixed effects. State fixed effects control for unobserved time-invariant state characteristics, such as state laws and culture, allowing us to estimate the relationship between community-level factors and tax avoidance without concern over the different contexts in which tracts are nested. We then ran one model testing all hypotheses together to examine whether the inclusion of some hypotheses influence findings about others. To further investigate the role of civic organizations, we also examined each organization type separately—religious and nonreligious—as well as the interaction terms between nonreligious organizations and proportion foreign born in a tract.

As a robustness check, we also estimated the model with all hypotheses using a multilevel random effects ordered logit with a transformed dependent variable, and a simple multivariate linear regression as a useful baseline (Appendix A). These models are less suitable than ZINB because they do not address the problem of excess zeros. As the variance of tax avoider count is greater than its mean, we chose the negative binomial distribution over Poisson. However, we also ran the Poisson model for robustness (Appendix A). All alternative models support our main findings.

As a cross-sectional correlational analysis, our method cannot establish causality and is prone to questions of selection. For example, if we find that tracts with a greater number of civic organizations are prone to a greater number of tax avoiders it may be because the bonding social capital presented by organizations induces resident elites to shelter their wealth, or it might be that elites who already shelter wealth, more so than other elites, desire to live in tracts that have the sort of bonding social capital that civic organizations present. This analysis cannot untangle the processes behind how tax avoiders find themselves in tracts with certain characteristics, but it can characterize the tracts in which elite tax avoiders live.

Results

Only a small share of all communities in the United States were home to tax avoiders listed in the ICIJ leaks: the 2,732 addresses in our data were concentrated in 2,216 tracts, out of a total of 57,650 tracts with at least one high-earning household for which complete information is available. Figure 1 compares the distributions of tracts with no tax avoiders, those with one tax avoider, and those with multiple tax avoiders across key characteristics.

Distribution of tract characteristics.

The figure demonstrates that communities without any tax avoiders (represented by the gray bars) are systematically different from communities with one tax avoider (blue bars) and those with multiple avoiders (red bars). Specifically, communities with tax avoiders appear, on average, to have higher economic inequality, fewer veterans, more residents earning more than $200,000, and higher numbers with bachelor’s degrees. They also appear to have slightly more civic organizations and higher variability in census participation, but these differences are less pronounced. These, however, are simply bivariate associations. To better understand the relationship between social capital and tax avoidance on the community level we next turn to multivariate statistical models.

To investigate the relationship between community-level characteristics, in particular the role of social capital, and economic elites’ tax avoidance, Table 2 presents tract-level ZINB tax avoider count models of our four hypotheses (with logistic functions for modeling excess zeros). The ZINB model is offset by the number of high earners in the tract, reflecting the assumption that offshore tax avoidance is pursued in tracts that contain higher income households. Models 1 to 4 correspond to hypotheses 1 to 4, respectively, controlling for additional community variables as well as state fixed effects. Model 5 incorporates all four explanatory variables with the same controls to examine how their coefficients change.

Tract-Level Zero-Inflated Negative Binomial Count Models of Tax Avoiders.

Note: Values in parentheses are standard errors. AIC = Akaike information criterion; BIC = Bayesian information criterion.

p < .05. **p < .01. ***p < .001.

In analyzing the results in Table 2, we examine only the negative binomial portion of the models, which is presented at the top of the table. 7 Model 1 shows that the greater the number of civic organizations in a tract, the higher the predicted count of tax avoiders. Specifically, holding all other variables constant with an offset for high earners, and controlling for state fixed effects, the expected number of tax avoiders increases by a factor of 1.01 (exponentiating 0.010) for each additional organization within a tract. This positive and statistically significant association indicates that civic organizations promote bonding rather than bridging social capital, increasing elite deviance (namely, offshore tax avoidance) rather than reducing it. This lends preliminary support to Hypothesis 1b over Hypothesis 1a.

Model 2 shows that higher levels of community-level economic inequality are also associated with higher tax avoider counts. Specifically, a one-unit increase in the income Gini coefficient predicts an increase in the number of tax avoiders in a tract by a factor of 1.017 (exponentiating 0.017), holding covariates constant and accounting for state fixed effects. This positive association lends support to the hypothesis that economic inequality (or socioeconomic heterogeneity) in a tract is likewise associated with bonding rather than bridging social capital in the context of elite tax avoidance (Hypothesis 2b). Wealthy elites residing in more unequal (or less homogenous) communities are more likely to engage in offshore tax avoidance.

Models 3 and 4 tested the hypothesized negative association between patriotic behaviors and elite deviance. In these two models, neither the share of veterans nor census participation was statistically significantly correlated with tax avoidance. Model 5 in Table 2 combines all four measures of social capital, assessing how they interact with one another. When all measures are included, the level of census participation in a tract becomes statistically significant, suggesting it may capture bridging social capital after all, lending support to Hypothesis 4. Civic organizations and income inequality maintain statistically significant associations with the predicted number of tax avoiders, in the original directions. Model 5 estimates that each additional civic organization in a tract is associated with an increase in the predicted number of tax avoiders by a factor of 1.009, while an increase in tract Gini coefficient is associated with an increase by a factor of 1.02. A percentage point increase in census participation is now statistically significantly associated with a decrease in predicted number of tax avoiders by a factor of 0.952. According to the five models’ Bayesian information criteria, model 5 fits the data the best; its conclusions are therefore warranted. 8 Census participation captures bridging social capital in the context of elite tax avoidance, civic organizations and income inequality capture bonding social capital. Beyond testing our original hypotheses, Table 2 also provides insight into other community correlates of tax avoidance through the models’ controls. It shows that all else being equal, smaller tracts with a higher proportion of foreign-born residents have more tax avoiders on average.

To provide a better sense of the magnitude of coefficients, Figure 2 plots the predicted number of tax avoiders (and their corresponding 95 percent confidence intervals) at different observed levels of the four main independent variables. All predictions are based on model 5 in Table 2, and all fix every variable except the focal variable at its mean. For ease of interpretation, the expected predicted probability of being an excessive zero in the ZINB model is also fixed at its mean, such that the graph captures the variable’s role in the count portion of the ZINB model but not its role in the logistic portion. 9

Predicted number of tract tax avoiders at different levels of civic organizations, census participation, Gini coefficient, and percentage veterans, with 95 percent confidence intervals.

Figure 2 shows that the predicted number of tax avoiders increases with higher numbers of civic organizations and lower census participation rates, reflecting the variables’ positive and negative coefficients (respectively) in Table 2. These predictions are conservative as point estimates are likely downwardly biased. 10 Keeping that in mind, the observed ranges of organizations and census participation appear to have similar associations with tax avoider count, as both predict between 0.02 and 0.15 tax avoiders in the tract. Additionally, Figure 2 shows that income inequality does not show a linear relationship with tax avoidance, as the predicted number of tax avoiders first increases and then falls as tract Gini coefficient increases. Percentage veterans, while not significantly correlated with the count of tax avoiders, shows a more linear relationship. However, neither Gini coefficient nor percentage veterans predicts as high a number of tax avoiders as civic organizations and census participation, hovering around 0.04 throughout their respective ranges.

To provide a more concrete characterization of communities with tax avoiders, we examined the 10 census tracts with the greatest number of avoiders. These tracts had between five and nine tax avoiders identified in the Panama Papers. Nine of the top 10 tracts were in California (mostly around Los Angeles) or New York (Manhattan), with the tenth in Texas (Houston). As expected, these tracts were relatively wealthy (an average median household income of $125,000) and highly unequal (a Gini coefficient of 0.52). Each of these tracts had at least one country club, alumni club, or golf course, and their census mail-in rates were relatively high (76 percent).

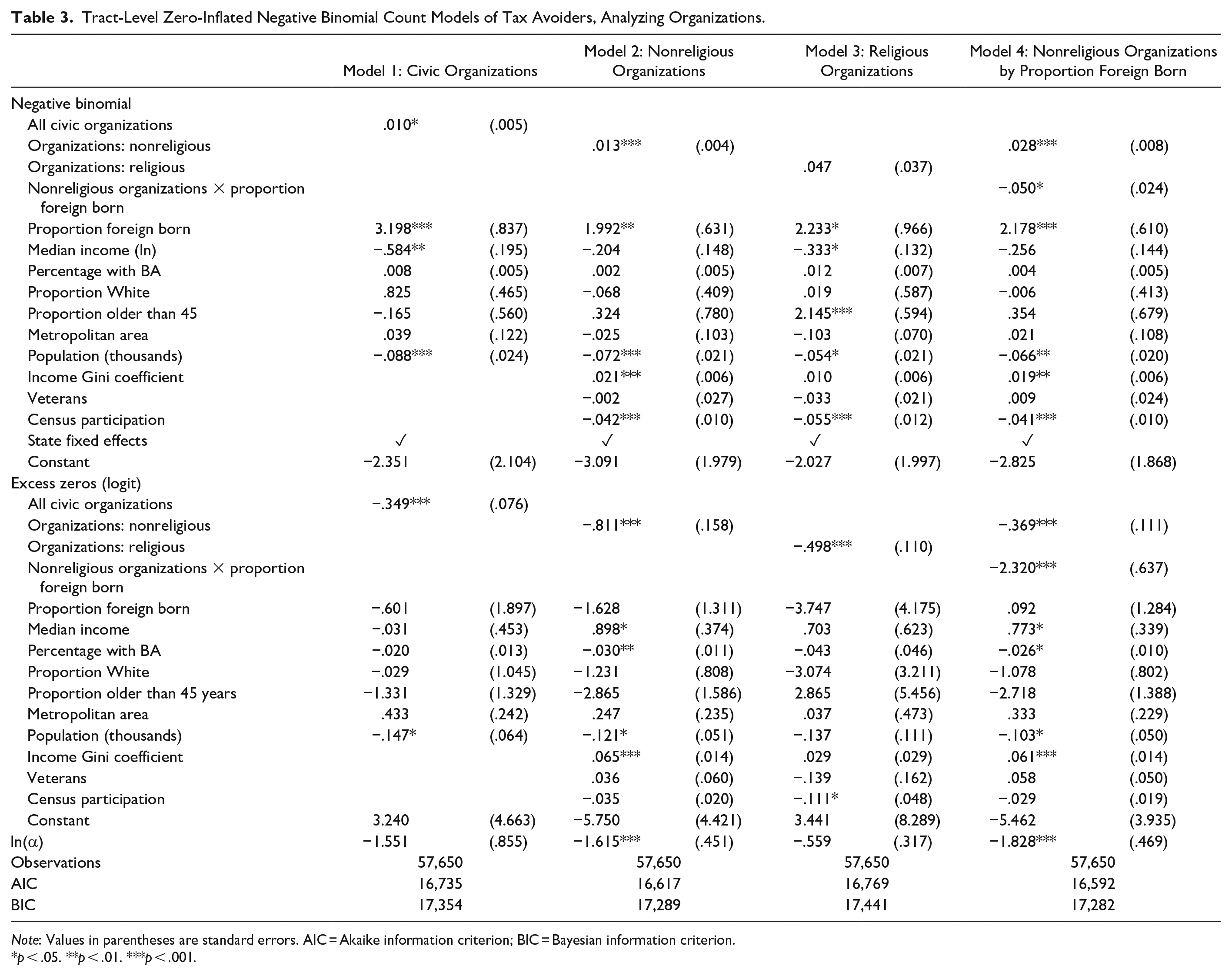

In our analysis, civic organizations and census participation are the two most meaningful community-level predictors of elite tax avoidance. Civic organizations are often viewed as the epitome of social capital (Putnam 2000; see de Tocqueville [1835] 2003), making our findings surprising. However, there are numerous types of civic organizations, including ethnic associations, churches, elite clubs, and others. It is therefore important to understand more precisely what types of organizations are associated with elite tax avoidance. Indeed, it is particularly important to investigate the potential role of ethnic organizations given the large and robust coefficient for proportion foreign born in the models in Table 2. In a secondary analysis (Table 3), we explore whether the relationship between civic organizations and elite tax avoidance is driven by religious organizations and whether this relationship is stronger in immigrant-heavy communities.

Tract-Level Zero-Inflated Negative Binomial Count Models of Tax Avoiders, Analyzing Organizations.

Note: Values in parentheses are standard errors. AIC = Akaike information criterion; BIC = Bayesian information criterion.

p < .05. **p < .01. ***p < .001.

Model 1 in Table 3 reproduces model 5 from Table 2 to provide the baseline findings about the relationship between organizations and tax avoidance. In models 2 and 3, we separate the aggregate civic organizations variable into nonreligious (e.g., social clubs and ethnic organizations) and religious (e.g., churches and shrines) organizations. 11 Models 2 and 3 demonstrate that the relationship between civic organizations and elite tax avoidance is driven entirely by nonreligious organizations. Religious organizations alone are not significantly associated with tax avoidance, and the association between nonreligious organizations and tax avoidance is larger than the association between all organizations and tax avoidance.

Accordingly, model 4 focuses on nonreligious organizations. We explore whether the association between civic organizations and tax avoidance is particularly strong in immigrant-heavy communities. Model 4 demonstrates a weak negative interaction between nonreligious civic organizations and the proportion of foreign-born residents on the one hand, and tax avoidance on the other. In other words, civic organizations show a stronger association with tax avoidance in tracts with lower proportions of foreign-born residents. This suggests that the relationship between civic organizations and tax avoidance is not driven by organizations that cater to immigrant or ethnic populations. It lends further support to the assumption that the explanatory mechanism is elite socialization.

Taken together, Table 3 demonstrates that nonreligious civic organizations drive the association between civic organizations and tax avoidance, and that these nonreligious organizations are not more likely to appear in tracts with a greater proportion foreign born, given similar numbers of high earners. This lends additional support to Hypothesis 1b: tax avoidance is higher in tracts with large concentrations of civic organizations. The absence of positive correlations between organizations and religion or immigration reinforces the suspicion that this is explained by the elite socialization (or bonding social capital) that such organizations facilitate.

Conclusion

Social capital has been a central concept in sociology since the 1990s. Although most scholars focus on its prosocial aspects (Coleman 1988; Putnam 2000), we set out to explore how different aspects of social capital relate to antisocial behavior. Specifically, we investigate the relationship between common measures of social capital and a pernicious type of antisocial behavior: tax avoidance by wealthy elites. We draw on Putnam’s (2007) distinction between bridging social capital, which connects individuals across groups and generally yields prosocial outcomes for broader society, and bonding social capital, which connects people within groups and may yield antisocial outcomes for the broader group (see Warren 2008).

Our analysis produced three main findings. First, communities with a higher number of civic organizations (specifically nonreligious organizations) tend to have higher numbers of tax avoiders. We speculate that civic organizations may operate as a site for elite sociality that produces bonding social capital, increasing the chances of antisocial behavior. This surprising finding challenges the standard view in the literature, which treats such organizations as a source of bridging social capital and an antidote to deviance and insularity (Putnam 2000). Second, we find that communities with higher income inequality are also more likely to host tax avoiders, though this relationship is not linear and less substantive than that between organizations and elite tax avoidance. We hypothesize that this could reflect the eroding effect of socioeconomic inequality on bridging social capital in a community (Xu and Marandola 2023). Finally, we find that patriotic behavior (Abascal and Centeno 2017) as measured by census participation is negatively associated with elite tax avoidance. This bolsters the hypothesis that at least some patriotic behaviors constitute a form of bridging social capital, which is in turn associated with lower elite deviance (Konrad and Qari 2012; Putnam 2000; Szreter and Woolcock 2004) at the community level.

Our research makes three main contributions to the literatures on social capital, elites, and tax avoidance. Our main contribution is the empirical demonstration that some forms of social capital are positively associated with antisocial behaviors. Until now, scholars have theorized about “negative” or “bad” social capital (Fukuyama 2001; Portes 1998; Warren 2008) without investigating it empirically. We show that civic organizations, a canonical indicator of social capital, are positively associated with elite tax avoidance. Social capital may thus coincide with antisocial behavior, at least for elites. This unexpected finding highlights the dual nature of social capital, which captures within-group (bonding) as well as across-group (bridging) solidarity (Putnam 2000). By paying attention to this crucial distinction, social scientists may be able to better predict the impact of different forms of social capital. Another contribution to the measurement of social capital is the role of patriotic behavior. Earlier works have studied patriotic behaviors (Abascal and Centeno 2017) or theorized an institution-oriented social capital (Szreter and Woolcock 2004). We show that patriotism, even patriotism that is exercised in the privacy of individuals’ homes (census participation), is negatively correlated with tax avoidance in a way that is indicative of bridging social capital.

Nonetheless, we are unable to establish causality. Because of the nature of the data on real-world tax haven use, we could not design a study that assesses the causal link between different facets of social capital and tax avoidance. In other words, we do not know whether communities with more civic organizations (or fewer census participators) produce bonding social capital that promotes antisocial behaviors or whether individuals who avoid taxes are more likely to join civic organizations or avoid completing the census. Future research could advance the state of knowledge by examining comparable phenomena in which causal relationships can be established. Our key finding regarding the association between civic organizations and elite tax avoidance raises another question: are tax avoiders actually members of such organizations? The present design does not provide an answer to this question. However, Putnam (2000:17) has convincingly argued that individuals in well-connected communities may reap the benefits of reduced deviance even if they do not themselves contribute to social connectedness. By the same token, individuals in communities with insular, bonding social capital such as elite social clubs may be more disposed toward antisocial behavior even if they themselves are not members of such organizations.

A second contribution pertains to the study of elites. Scholars have long had an interest in intraelite cohesion and cooperation (Domhoff 1967; Khan 2012; Mills 1956) but have seldom used the framework of social capital. 12 By explicitly connecting social capital with elite deviance, we expand the analytic toolbox of the literature on elites, which already examines the role of socialization in elites’ views and habits (Farrell 2020; Khan 2011; Lamont 1992; Mears 2020). Our findings raise the possibility that where elite cohesion is higher—because of a tight network of organizations or deep socioeconomic divides—elite members may be more likely to engage in deviance. More broadly, they direct our attention to local community factors that are correlated with elite norms and behavior (see Sherman 2018). Thus, scholars of elites should pay attention to elite socialization within community contexts when making sense of their socialization.

One key study that has connected social capital and tax avoidance focused on millionaire migration. Young et al. (2016) pointed to local social capital (e.g., business contacts)as a potential factor that depresses elite tax avoidance by lowering elites’ willingness to move. Because of its beneficial effect for a broader community, this hypothesized social capital (which the authors conceptualize as “embeddedness”) should be considered bridging social capital. Our study fine-tunes the relationship between social capital and elites’ tax compliance. We found that some facets of social capital have a bridging function, connecting elites to the broader community, whereas other facets may actually constitute bonding social capital associated with insular attitudes. Place and community matter for the rich, but not in a monolithic manner. Some communities also have “antisocial capital” that is associated with elite insularity.

Finally, this study contributes to the literature on tax avoidance by empirically demonstrating the role of community context using direct community measures. Recent scholarship has found that tax avoidance is a social phenomenon influenced by trust, a sense of duty, and adherence to norms (Alm and Gomez 2008; Luttmer and Singhal 2014). However, existing studies tend to measure these social elements on an individual level, and typically use either self-reports of tax avoidance or weaker versions of avoidance, such as shifting the timing of gifts. By using community-level measurements and investigating a more severe tax-avoiding behavior, we bolster the argument that tax avoidance is deeply embedded within a social context. Community context is key for understanding tax avoidance and other deviant behaviors, not just through its positive characteristics but also through the potential for antisocial capital.

Footnotes

Appendix

Comparing Alternative Estimates.

| ZINB | ZIP | Multiple Regression | Ordered Logit | |||||

|---|---|---|---|---|---|---|---|---|

| Negative binomial/main | ||||||||

| Civic organizations | .009*** | (.002) | .008*** | (.001) | .007*** | (.002) | .063*** | (.014) |

| Income inequality | .020** | (.006) | .021*** | (.006) | .001 | (.000) | .034*** | (.005) |

| Veterans | −.008 | (.027) | −.003 | (.024) | −.000 | (.000) | −.021* | (.009) |

| Census participation | −.049*** | (.010) | −.047*** | (.010) | −.002*** | (.000) | −.028*** | (.005) |

| Percentage with BA | .007 | (.005) | .005 | (.005) | .000* | (.000) | .033*** | (.002) |

| Proportion foreign born | 1.830** | (.630) | 1.844** | (.661) | .180*** | (.017) | 3.128*** | (.293) |

| Proportion White | −.215 | (.395) | −.147 | (.427) | .063*** | (.007) | .969*** | (.185) |

| Proportion older than 45 years | .823 | (.758) | .733 | (.670) | .063*** | (.014) | 2.143*** | (.309) |

| Metropolitan area | −.023 | (.106) | .012 | (.110) | −.004 | (.002) | −.138* | (.064) |

| Population (thousands) | −.076*** | (.021) | −.073** | (.022) | −.004*** | (.001) | .090*** | (.013) |

| Median income (ln) | −.283 | (.151) | −.273 | (.158) | −.015 | (.009) | .502*** | (.108) |

| High earners | .001*** | (.000) | .001*** | (.000) | ||||

| State fixed effects | ✓ | ✓ | ✓ | ✓ | ||||

| Constant | −2.167 | (1.909) | −2.316 | (1.894) | .160 | (.110) | ||

| Excess zeros (logit) | ||||||||

| Civic organizations | −.336*** | (.047) | −.299*** | (.036) | ||||

| Income inequality | .055*** | (.013) | .051*** | (.012) | ||||

| Veterans | .019 | (.066) | .026 | (.052) | ||||

| Census participation | −.044* | (.021) | −.037* | (.018) | ||||

| Percentage with BA | −.026* | (.011) | −.025* | (.010) | ||||

| Proportion foreign born | −2.729 | (1.412) | −2.454 | (1.299) | ||||

| Proportion White | −2.120* | (.876) | −1.781* | (.823) | ||||

| Proportion older than 45 | −1.807 | (1.736) | −1.664 | (1.381) | ||||

| Metropolitan area | .287 | (.255) | .319 | (.229) | ||||

| Population (thousands) | −.149* | (.061) | −.122* | (.054) | ||||

| Median income (ln) | .473 | (.358) | .403 | (.336) | ||||

| Constant | .540 | (3.995) | .576 | (3.620) | ||||

| ln(α) | −1.727** | (.543) | ||||||

| cut1 | 12.844*** | (1.349) | ||||||

| cut2 | 14.971*** | (1.348) | ||||||

| Observations | 57,650 | 57,650 | 57,650 | 57,650 | ||||

| AIC | 16,662 | 16,670 | 3,441 | 15,940 | ||||

| BIC | 17,334 | 17,333 | 4,006 | 16,514 | ||||

Note: Values in parentheses are standard errors. AIC = Akaike information criterion; BIC = Bayesian information criterion; ZINB = zero-inflated negative binomial model; ZIP = Poisson distribution zero-inflated model.

p < 0.05. **p < .01. ***p < .001.

Acknowledgements

We are grateful to the two anonymous reviewers for their helpful comments. We also thank Jere Behrman, Julia Behrman, Dafna Gelbgiser, Mauro Guillén, Efrat Herzberg, Rami Kaplan, Annette Lareau, Lilach Lurie, John MacDonald, Erez Maggor, Erez Marantz, Isaac Martin, Hyunjoon Park, Isaac Sasson, Leslie Sebba, Talia Shiff, David Weisburd, and Xi Song for useful comments and suggestions.