Abstract

The authors examine the historical origins of Germany’s 1,032 largest fortunes. The innovation of this research is to link a rich list from 2019 with rich lists from 1913 and genealogical data provided in Wikidata. The authors find a remarkable historical continuity of large fortunes despite two world wars, the Great Depression, regime changes, and different currency reforms. One third of the companies associated with today’s largest fortunes were founded before World War I. About 8 percent of today’s fortunes can be traced back to fortunes on rich lists from 1913. Regression analyses show that these entrenched fortunes rank on average higher on the rich list than fortunes of younger origin. Network analyses indicate that some of today’s largest fortunes are intertwined through marital lines, hinting at social closure at the top. These findings indicate that the accumulation and perpetuation of fortunes over many generations is an important feature of top wealth in Germany.

Most countries are confronted with historically high levels of wealth inequality and an extreme concentration of economic power in the hands of a very small minority at the top of the wealth distribution (Chancel et al. 2022). Whereas macro-level research documenting country differences in the level of wealth concentration (measured, e.g., as the top 1 percent wealth share) and the development of wealth concentration is increasing (e.g., Albers, Bartels, and Schularick 2022; Piketty 2014), much less is known about the development of individual fortunes and the individuals and families at the very top of the wealth distribution (Baselgia and Martínez 2022). However, it is important to know more about the small group (e.g., the richest 0.01 percent) at the center of wealth concentration to better understand wealth inequality.

We argue that the historical origin of today’s top fortunes is a characteristic worth examining in order to grasp the structure of top wealth. First, the origins of fortunes are likely to be related to economic processes. If a considerable share of top fortunes persists over decades by perpetuating wealth within the family, this could guarantee continuity and long-term stability of capital investment but also harm the economy by an inefficient distribution of financial capital or poor management (Beckert 2022; Morck, Stangeland, and Yeung 2000). Second, the analysis of the historical origins of fortunes informs us about processes of social closure of the wealth elite. If large fortunes are perpetuated within the family, the wealth elite is not regularly transformed through new entrants. The lack of social mobility among the wealth elite, in turn, carries the risk of causing the elite to drift away from the wider society, hampering their understanding of social realities and threatening social cohesion (Toft and Hansen 2022). Third, the historical origins of top fortunes are likely to be related to the extent to which power structures of the wealth elite are consolidated (Starr 2019). Large fortunes give their owners political and economic power (Gilens and Page 2014; Starr 2019). It can be assumed that the older the fortunes, the higher the likelihood of the entrenchment of power. Last, the historical origins of top fortunes are closely linked to popular attitudes toward the rich. There is growing literature on the “deservingness of the rich” highlighting the historical origin of wealth as a central criterion (Rowlingson and Connor 2011). According to this literature, fortunes that are attributed to family background rather than competence and hard work are less likely to be perceived as deserved. Thus, the widespread meritocratic ideology justifies wealth concentration if access to top wealth positions does not depend on the family background but is based on the equality of opportunity (Beckert 2008).

But how can we conceptualize and measure the historical origins of top fortunes? Origins have often been conceptualized as the dichotomy of inherited versus self-made wealth. Whereas “self-made” signifies that fortunes originate in individuals’ own efforts and success, “inherited” indicates that the origin of the fortune can be traced back to ancestors, highlighting the role of the family background. This conceptualization of historical origins is widely applied and has been found useful to explain social closure and mobility within the wealth elite (Hansen 2014; Korom, Lutter, and Beckert 2017) but also to better understand economic processes (Morck et al. 2000).

In this study, we propose to further develop the concept of historical origins of top fortunes by incorporating the concept of entrenchment (Starr 2019). According to Starr (2019), entrenched features of a society could be, for example, institutions, rules, interests, or beliefs. Entrenched features are characterized as being long lasting and very difficult or even impossible to change (p. xi). They resist stress, defy pressure, and overcome opposition (Starr 2019:1). It is important to observe these features because a “society’s entrenched features—the foundational features that are hardest to change—shape what kind of society it is” (Starr 2019:xii). We propose that in societies characterized by high levels of wealth concentration, the historical origin of top fortunes is an important aspect of the economic elite’s entrenchment. The long-term perpetuation of wealth within the family (enabled, for example, by rules such as primogeniture) is a way of entrenching the social and political order (Starr 2019:36). At the micro-level, large fortunes may be more or less entrenched in family lines. We argue that a good indication of the entrenchment of a fortune within a family is whether it has survived economic and social upheavals such as economic depression, regime changes, and wars (Starr 2019:4).

To shed light on the historical origins of today’s top fortunes in Germany, we first examine the founding dates of the companies associated with those fortunes. We then identify a group of what we call “entrenched fortunes”. We operationalize entrenched fortunes as a subgroup of today’s fortunes that date back to the beginning of the twentieth century. Thus, they have successfully coped with the social, economic, and political upheavals of the past century. Thereafter, to understand the relevance of entrenched fortunes for today’s wealth structure, we examine how these fortunes dating back over 100 years differ from fortunes of younger origin. Last, we examine in an exploratory way if the entrenched fortunes are connected to fortunes of younger origins through family lines. Thus, we ask whether the entrenched wealth elite seals itself off from the rest of the wealth elite.

Our analyses are based on a German journalistic rich list from 2019 (Manager Magazin), which contains the 1,032 largest German fortunes. Rich lists, in contrast to survey or tax data, have the advantage of providing real names of families or individuals and focus on the very top of the wealth distribution. These names can be used to augment the list with publicly available information. To identify the share of entrenched fortunes, we link today’s rich list with rich lists from the beginning of the twentieth century (Martin 1913). We then compare these entrenched fortunes with the more recently established ones on today’s rich list by means of frequency tables and ordinary least squares regressions. To explore to what extent the entrenched fortunes are intertwined with fortunes with more recent origins, we draw kinship webs. To this end, we link the rich lists with Wikidata, a collaboratively edited multilingual knowledge graph, and scrape the genealogical data on all those individuals in the rich list that we can identify.

This study uniquely contributes to the literature on top wealth. By building a dataset on the basis of rich lists from the beginning of the twentieth century, rich lists from today, and genealogical data we generate descriptive knowledge about the largest fortunes in Germany, complementing prior research on top wealth in China, Norway, Switzerland, and the United States (e.g., Baselgia and Martínez 2022; Kaplan and Rauh 2013; Korom et al. 2017; Lu, Fan, and Fu 2021; Toft and Hansen 2022). Germany is an especially interesting case to study the historical origins of today’s top fortunes. This is not only because it ranks fourth regarding the number of billionaires in the Forbes billionaires list for 2022 but also because Germany has experienced several historical events over the past century that have led to major societal, political, economic, and legal upheavals (Albers et al. 2022). We show that despite the turbulent events during the twentieth century, many of today’s fortunes have been formed by past generations. In particular, more than one third of the companies associated with Germany’s largest fortunes were founded before World War I. Eight percent of today’s fortunes descend from fortunes held by the same families at the beginning of the twentieth century. Furthermore, this study adds to the literatures on the role of the family for top wealth reproduction. Assessing the family intertwining of fortunes, we identified one large kinship web linking some of today’s entrenched fortunes through marital and kinship lines to each other but also to fortunes of younger origin.

Previous Research on the Historical Origins of Large Fortunes

The Role of the Family

Social scientists mostly agree that inheritance is an important determinant of top wealth in modern industrial societies (Beckert 2008; Bessière and Gollac 2023; Hansen 2014; Keister and Lee 2017; Medeiros and de Souza 2015; Piketty 2014). This stream of literature argues that the family establishes the basis for the long-term continuity of top fortunes through direct intergenerational asset transfers (Farrell 1993). Therefore, studying the historical origins of large fortunes goes along with studying family relations.

In this study, we use a broad concept of family as an area of social life spanning several households and multiple generations. Following Close (1985), family “refers to that area of social life covering and circumscribed by kinship (blood or consanguineal relationships) and marriage (conjugal and other affinal relationships)” (p. 9).

Theories on inherited advantage argue that capitalist societies offer wealthy families plenty of channels to “hoard opportunities” and perpetuate their fortunes over generations (Beckert 2022; Hansen and Toft 2021; Tilly 1998). Accordingly, this stream of literature suggests low intergenerational mobility at the top of the wealth distribution (Medeiros and de Souza 2015; Toft and Hansen 2022). Low mobility at the top seems to hold also in the long run as, for example, Barone and Mocetti (2020:1864) provided evidence for wealth inheritance over six generations, indicating the existence of a “glass floor” protecting descendants of the super-rich from losing their fortunes.

However, there seem to be country differences in the relevance of inheritance for the accumulation of large fortunes. Using the Forbes billionaires rich lists from 1996 to 2015, Freund and Oliver (2016) showed that German fortunes are more than twice as likely to be inherited than those in the United States, indicating a less dynamic composition of the German super-rich. Still, prior research also finds evidence for the central role of long-term wealth perpetuation within families in the United States. Using the annual American Forbes 400 rich lists (1982–2013), Korom et al. (2017) showed that although entrepreneurship is increasingly important for being listed, heirs are more likely to remain listed in the long-term. Other European countries are similar to Germany in their share of inherited wealth (Freund and Oliver 2016). For example, for the case of Switzerland, Baselgia and Martínez (2022) showed that inheritance is still the main factor for making it to the top of the wealth distribution and that mobility at the top is very low.

Besides direct intergenerational wealth transfers, the family might also play a role in the perpetuation of wealth by spinning a web of kinship ties. Zeitlin and Ratcliff (2014) stressed that “freely intermarrying families, not individuals, are the constitutive units of classes, especially of the dominant class” (p. 7). Schumpeter (1972:13), too, thought of the family as the relevant unit of class analysis because class membership stems from the membership in a given clan or lineage. Therefore, studying kinship webs helps not only to examine the historical origins of large fortunes but also the internal integration of a social class connected to the largest fortunes. Moreover, the analysis of kinship webs helps examine how fortunes of different historical origins are intertwined by family lines.

Families at the top of the wealth distribution may perpetuate their fortunes by means of social closure and economic alliance building (Farrell 1993; Zeitlin 1974). Within families, the kinship network can be used to coordinate economic interests by placing family members in specific positions in the economy, politics, and society. And indeed, according to previous findings, individuals with a kinship tie to another individual on the Forbes 400 rich list are substantially wealthier than those without ties (Korom et al. 2017). Moreover, Toft and Hansen (2022) showed in the case of Norway that parental wealth transfers and a family context of ownership and control of large economic assets were beneficial for accumulating large fortunes. But families might also create strategic alliances through marriages and thereby connect fortunes. This was, for example, common practice within the German nobility (Hurwich 1998). Even though most super-rich individuals today probably do not enter into marriage for purely strategic reasons, marital homogamy has been found to be especially prevalent in the upper strata (Benton and Keister 2017; Mare 2011; Toft and Hansen 2022; Toft and Jarness 2021).

The Role of Political and Social Circumstances

The development of wealth concentration depends on political and social circumstances. For example, wars have been found to be a central wealth equalizing factor because of war-related physical destruction of domestic capital assets, lack of investment capital, and a fall in relative asset prices (Piketty and Saez 2014). But other societal, political, and economic upheavals are related to the development of wealth concentration and top wealth, too. For instance, 2021 marked the year of the largest increase in billionaires’ share of global wealth, indicating that the super-rich benefited remarkably from the COVID-19 pandemic (Chancel et al. 2022). But country-specific shocks can also shape the conditions for wealth accumulation at the top (Albers et al. 2022). Because we focus on Germany, we provide a brief summary of the German historical context. We further discuss the relationship between historical events and the perpetuation of individual fortunes at the top of the wealth distribution.

During the past century, Germany has experienced historical events with tremendous societal, political, economic, and legal upheavals, such as five different forms of government, three currency conversions, two world wars, and the separation and unification of Germany. These developments are accompanied by a strong decline in wealth inequality, caused mainly by tax increases and direct effects of the two world wars (e.g., the influx of displaced people and substantial capital destruction) (Albers et al. 2022). Between 1895 and 2018, the wealth share of the top 1 percent halved, from almost 50 percent to 27 percent. Nearly all of this decline occurred between 1914 and 1952. In the postwar period, the wealth share of the top 1 percent increased only marginally (Albers et al. 2022).

Furthermore, the economic persecution of Jews shaped wealth inequality in Germany. In 1933, the approximately 550,000 Jews living in Germany owned about 16 billion Reichsmark. It is estimated that they were able to save about a quarter of their assets abroad. The other three quarters of Jewish wealth were appropriated by companies, private persons, social organizations, and institutions of the Nazi administration (Drecoll 2009). This expropriation of Jewish assets radicalized and institutionalized especially after the pogrom night of 1938 (Ritschl 2019). A considerable share of today’s German wealth is based on the economic events during the Nazi era. Some companies profited massively from the expansion of the armaments industry or from the “Aryanization” of Jewish companies (Windolf and Marx 2022).

Another peculiarity of Germany is its division after World War II. Because of its economic system, West Germany offered better conditions for the accumulation and perpetuation of fortunes compared with East Germany, where most private ownership was destroyed. Until today, large regional economic discrepancies between East Germany and West Germany persist as a result of the 40-year separation. In 2018, West German households were on average more than twice as rich as Eastern households. These wealth discrepancies are especially pronounced at the top: whereas the average household of the top 1 percent in eastern Germany owns 3 million euros, their western counterparts own 12 million euros (Albers et al. 2022).

These macro-level developments in wealth concentration also have implications for wealth accumulation and preservation at the individual level. One fundamental sociological aspect of wealth at the individual level is social mobility. Although German history has offered plenty of challenges to the perpetuation of individual fortunes, it could be possible that the group at the very top of the wealth distribution consists to a large extent of the same families over time. In contrast, Schumpeter (1972) argued that “each class resembles a hotel or an omnibus, always full, but always of different people” (p. 126). Staying with the metaphor of a hotel, we can see that macroeconomic events have caused the number of beds in the five-star hotel for the super-rich to change over time. But are there families that manage to move into the hotel permanently? Or is there indeed, as Schumpeter suggested, mobility within the hotel of the super-rich? Because economic historians have shown that the great macro-level equalization of wealth occurred after 1914, it is worth studying to what extent Germany’s five-star hotel today welcomes the descendants of its 1914 guests. Just as to what extent their guests are old acquaintances matters for the atmosphere in a hotel, it matters for society to what extent the top wealth strata comprises entrenched fortunes.

Conceptualizing and Measuring the Historical Origins of Large Fortunes

Most prior research on the origins of top wealth distinguished between inherited and self-made wealth (Baselgia and Martínez 2022; Freund and Oliver 2016; Hansen 2014; Kaplan and Rauh 2013; Korom et al. 2017). Although this dichotomous approach has been criticized because inheriting wealth does not necessarily preclude active entrepreneurship and hard work, and because the term self-made undermines the fact that self-made wealth holders largely benefit from inherited privilege such as race, gender, or economic background (Miller and Lapham 2012; Sherman 2021; Tsigos and Daly 2020), it has been found useful to analyze social mobility and closure at the top of the wealth distribution.

To further disaggregate the binary categorization, prior research added, for example, the categories “inherited a modest business and built it into a much larger one” (Kaplan and Rauh 2013) or “through marriage” (Baselgia and Martínez 2022). Furthermore, previous research started to use the founding dates of companies or the ownership generation as a proxy for the historical origins of fortunes. This provides a long-term perspective on the historical origins of top fortunes. Using founding dates rather than the ownership generation allows to better analyze the historical context of origin. For example, information that a significant share of fortunes is held by the fifth generation and information that a significant share of fortunes is based on companies founded during World War II provide two different perspectives on the structure of top wealth.

However, we must bear in mind that the founding date of a fortune-generating company does not necessarily equal the year of origin of the respective fortune. The accumulation of large fortunes is rather characterized by “the big jump and the accumulation of advantages” according to Mills (2000:110). Individuals have to acquire a strategic position that opens up an opportunity to make a big jump (i.e., to accumulate a large amount of wealth within a short period). After the big jump, the individual can transform this wealth into a large fortune by benefiting from the accumulation of advantages. The more money, the higher the accumulation potential (Piketty 2014). However, it might be that the big jump does not occur in the first generation, but only in one of the following generations. Thus, the accumulation of a top fortune might be the result of intergenerational effort. Therefore, using founding dates or the ownership generation is only an approximate measure of the historical origin of the fortune.

We propose to incorporate the concept of entrenchment (Starr 2019) in the conceptualization of the historical origin of today’s top wealth. As defined in the introduction, entrenchment means the capability to be stress resistant and to withstand pressure to change. Accordingly, we define entrenched fortunes as fortunes that have survived economic and social upheavals such as economic depression, regime changes, and wars. Empirically, we measure entrenchment of the economic elite by identifying the share of fortunes descending from the beginning of the twentieth century. This means that today’s entrenched fortunes originate from top fortunes in the period before the start of the great wealth equalizing (1914). For example, a fortune that can be traced back to a simple craft store founded in 1913 does not count as entrenched, but a fortune that is connected to a brewery family that held a considerable fortune already in 1913 counts as entrenched. Thus, in our operationalization, entrenchment means that the fortune has been perpetuated over more than the past 100 years.

Data and Methods

Data

Obtaining reliable data is a major challenge in the study of elites, particularly for the super-rich. Although sampling techniques have improved in the last decade leading to a more successful collection of data via questionnaires (Schröder et al. 2019), super-rich samples in large national surveys still do not capture the largest fortunes. Population surveys suffer from nonresponse bias, which appears to be especially high in European countries, Germany in particular (Bach, Thiemann, and Zucco 2019). As an alternative to tax register or survey data, various authors have made use of international or national rich lists, usually generated by journalistic estimates (e.g., Baselgia and Martínez 2022; Freund and Oliver 2016; Korom et al. 2017). These rich lists have the advantage of providing real names and company names, which can be used to find more information on the origins of the fortunes. Using national rich lists adds the value of examining a larger share of the wealthiest individuals and families in more detail. They thus represent an alternative data source for identifying and exploring large fortunes and their owners.

We use a rich list published by the Manager Magazin, a German monthly business magazine. Since 2010, the Manager Magazin has annually published a list of the largest 500 German fortunes. From 2000 to 2009 they published the 300 wealthiest Germans. It was only in 2018 and 2019 that the Manager Magazin published rich lists including the 1,001 largest fortunes in Germany as well as a list of the 31 richest German clans (families with an unknown or very high number of family members owning the fortune jointly). The readership of the Manager Magazin and the rich lists comprises business and political leaders, the financial community, family business elites, and the general population.

The net wealth of the rich list entries is estimated by journalists. Their estimation is based on research in archives and registers as well as conversations with wealth managers, lawyers, bankers, and listed individuals themselves (Manager Magazin 2019). The value of shares is estimated according to the closing prices on September 13, 2019, and the values of unlisted companies are estimated according to their turnover, profitability, and market position. Net wealth comprises land and real estate holdings, interests, shares, and art objects. Because determining “a precise value for these assets can involve more art than science” (Raub, Johnson, and Newcomb 2010:134), it is important to acknowledge that the exact figures for estimated wealth are probably inaccurate. However, the included individuals and families clearly belong to the German wealth elite and the ranks of entries in the list are most likely accurate. We make use of the rich list in 2019 containing 1,001 entries and the clan list from the same year containing 31 clans. Each entry is one fortune, which can be held either by an individual or by a group of individuals or families. Bach et al. (2019) estimated that each entry represents about four households; thus the list covers about 0.01 percent of German households (Albers et al. 2022).

In addition to the existing variables and information included in the Manager Magazin rich list, we augment with information about the individuals and families. 1 The original lists contain the name of individuals or the family, the name and location of the company, the worth of the fortune (in billion euros), the rank in the rich lists, and if the fortune is related to a family foundation (included as dummy variable; 1 = yes, 0 = no) or a company foundation (included as dummy variable; 1 = yes, 0 = no). Further variables generated for this study are the foundation year of the company, and three dummy variables (1 = yes, 0 = no) indicating if the family was part of the nobility, if the company has already been sold, and if the family has ancestors who were listed on a rich list from the beginning of the twentieth century. The last mentioned variable indicates if a fortune is entrenched. To identify entrenched fortunes we manually linked today’s rich list with the rich lists published by Martin (1913).

Rudolf Martin, a former Prussian official of the Reichsamts des Innern (interior ministry), published rich lists for almost all German states from 1912 to 1914. The almanac Jahrbücher des Vermögens und Einkommens der Millionäre list the names, addresses, income, and wealth of millionaires in nearly all states of the German Empire (Gajek 2014). These lists have been used by (economic) historians to document wealth concentration but also to describe the social structure of top wealth in Wilhelmine Germany (e.g., Augustine 1994).

To exploratively examine if families owning entrenched fortunes are intertwined through family and marriage ties with families owning fortunes of younger origin, we reconcile the individuals of the rich lists with Wikidata (https://www.wikidata.org). Wikidata is a collaboratively edited multilingual knowledge graph. Whereas the free online encyclopedia Wikipedia consists of unstructured articles about various topics or objects including individuals, Wikidata contains structured information. Each Wikidata page refers to one item, for example, a topic, an object, or a person. The information about the item is recorded as statements that are built by pairing a property with a value. To understand the structure of Wikidata, let us look at one example. In 1913, Bertha Krupp von Bohlen und Halbach was the richest individual in the Kingdom of Prussia. The Krupp family was one of Germany’s leading industrial dynasties of the nineteenth and twentieth centuries. Bertha Krupp is included in Wikidata as the item Q66505 (https://www.wikidata.org/wiki/Q66505). To store the information that she is human, an editor added a statement to the item Q66505 by pairing the property “instant of” (P31) with the value “human” (Q5). Because the value “human” has its own Wikidata page, it is possible to link Bertha Krupp to other humans. In the same way, information on her family members can be stored. For example, through the properties “father” (P22) and “mother” (P25), Bertha Krupp is linked to her father Friedrich Alfred Krupp (Q61543) and her mother Margarethe Krupp (Q109468). Thus, on the basis of the genealogical information stored in Wikidata, we can draw kinship networks.

Wikidata does not include all individuals on the rich lists (see Table 1 for an overview of the number of observations). We were able to identify 439 individuals on the rich lists from 2019. For some entries, we could identify more than one individual; for many entries, we could not identify any individual. Some super-rich families try everything to avoid appearing in the public sphere, making it even more difficult to research the names of individual family members. For each of the 439 individuals, we scraped all ancestors until the nineteenth century. At least one family tie was included for 193 individuals in Wikidata. We compared the list of ancestors with Rudolf Martin’s rich lists from 1913 and identified 76 individuals from these lists as ancestors. We have to acknowledge that the identified individuals are not a random sample of the rich lists but are biased toward nobility and other factors affecting inclusion in Wikidata. Furthermore, missing information on family ties is clearly not random. For example, because of the public interest in the German nobility and the importance of lineage for the nobility, it is more likely for noble persons to have family ties included in their Wikidata entries. Therefore, we do not seek to draw general conclusions about the marital strategies of super-rich families but rather use the data to exploratively examine if there is any evidence that entrenched fortunes are linked to fortunes of younger origin through marriage ties.

Overview of Number of Individuals in Network Analysis.

Analytic Strategy

The aim of this study is to shed light on the historical origins of Germany’s largest fortunes. To this end, we first descriptively examine the founding dates of the companies associated with the fortunes as a proxy for the age of the fortunes. Second, by linking today’s rich list with a rich list from the beginning of the twentieth century, we identify a group of entrenched fortunes that date back more than 100 years and, therefore, survived tremendous political and economic upheavals. To understand the role of these entrenched fortunes in today’s society, we examine to what extent entrenched fortunes differ from more recently established fortunes in terms of geographical variation, their position within the wealth distribution, and further characteristics. To this end, we study these characteristics descriptively and run ordinary least squares regressions. The dependent variable is the rank in the rich list, taking values between 1 and 1,001 (we exclude the separate clan list). Higher values indicate lower ranks. Our predictor variable is a dummy variable indicating if the fortune is entrenched (i.e., today’s fortune can be linked via family lines to fortunes listed in Rudolf Martin’s rich list from 1913) or not (reference category). We control for different characteristics of the fortunes (see Table 2 for descriptive statistics of the variables). Finally, to further scrutinize how the entrenched fortunes relate to fortunes with younger origins and to examine social closure within the top wealth strata, we draw and analyze kinship webs covering individuals and their family members who are connected to the largest fortunes today.

Descriptive Statistics of Variables in the Regression Model.

Note: For the regression analysis, we do not use the separate clan list. Thus, the number of observations reduces to 1,001, and the share of entrenched fortunes reduces to 6.5 percent.

Results

Founding Dates of the Largest Fortunes

To examine the age structure of the largest fortunes, Figure 1 shows the number of fortunes as well as the combined wealth by founding date. 368 of the 1,032 fortunes date back to before World War I. This does not mean that those families were already rich at the beginning of the twentieth century but that the companies or predecessors of today’s companies already existed. The black coloring shows the share of the combined wealth attributed to entrenched fortunes. It becomes apparent that the combined wealth of companies founded before World War I does not descend, for the most part, from the largest fortunes at the beginning of the twentieth century. These findings highlight that large fortunes are often the result of wealth accumulation across more than one generation.

Number of fortunes and combined wealth by founding date of company.

Figure 1 also shows that about half of the companies were founded after World War II. Looking at the combined wealth, it is striking that the total value of the fortunes dating back before World War I is larger than the total value of the fortunes founded after World War II, despite the smaller number of fortunes. This again highlights that today’s fortunes are substantially shaped by past generations. To provide further insights into the relevance of the past for today’s largest fortunes, we now look in more detail at the entrenched fortunes.

Entrenched Fortunes

About 8 percent of today’s 1,032 largest fortunes can be traced back to fortunes at the beginning of the twentieth century. In other words, the ancestors of 82 families mentioned on today’s rich list were already included in a rich list in 1913. If we only look at the largest 500 fortunes, the share of entrenched fortunes increases to 10 percent. Table 3 shows 10 of these entrenched fortunes. It becomes apparent that today’s entrenched fortunes are not possessed by individual persons but rather by families (i.e., today’s rich list includes only the family names), whereas in 1913 specific individuals could be identified. Today, the entrenched fortunes are often dispersed across an unknown number of family members. The entrenched fortunes are rooted in companies from different sectors. The list includes biotech companies such as Sartorius, a pharmaceutical and laboratory equipment supplier, companies in the food industry such as the German multinational company Dr. Oetker, famous for their baking powder and cake mixes, or the brewery Spaten-Franziskaner-Bräu, and engineering companies such as Robert Bosch or Voith. These families have been able to perpetuate and amplify their fortunes across many generations resulting in very high ranks in today’s rich list.

Entrenched Fortunes.

To understand the role of entrenched fortunes, it is helpful to examine how they differ from more recently established ones. Table 4 compares these two groups of fortunes. Whereas membership of the nobility plays hardly any role in the nonentrenched fortunes (1 percent), more than one third (35 percent) of the entrenched fortunes are connected to the nobility. Entrenched fortunes are a little more often connected to a sale of the business. Interestingly, entrenched fortunes are less often to be connected to a family foundation or company foundation. Do entrenched fortunes also differ from the rest of the fortunes in terms of regional distribution?

Characteristics of the wealthy elite.

The geographical variation of today’s largest fortunes in Germany is depicted in Figure 2. The circles represent the fortunes. To better highlight the differences between entrenched fortunes and the remainder, the panel on the left depicts only those entries that have ancestors on the rich list in 1913 (entrenched fortunes) and the panel on the right depicts the remaining entries. The size of the circle indicates the amount of wealth in billion euros. The color of the circle indicates if the family is part of the German nobility. Strikingly, the figure shows that Germany’s largest fortunes are concentrated in the western states of Germany and in particular in the Rhineland and southern Germany.

Geographical variation of today’s largest fortunes in Germany.

Figure 2 (left panel) indicates again that many of the entrenched fortunes are connected to the nobility, highlighting the long-lasting influence of the German nobility and landed wealth. Interestingly, noble and non-noble fortunes cluster in different regions, probably because of differences in the sources of wealth (e.g., land ownership versus industrial wealth). Comparing the two maps, it becomes apparent that there are hardly any entrenched fortunes on the territories of the former German Democratic Republic including Berlin, highlighting the consequences of political regime changes. Other than that, the regional distribution of entrenched fortunes does not seem to differ greatly from the other fortunes.

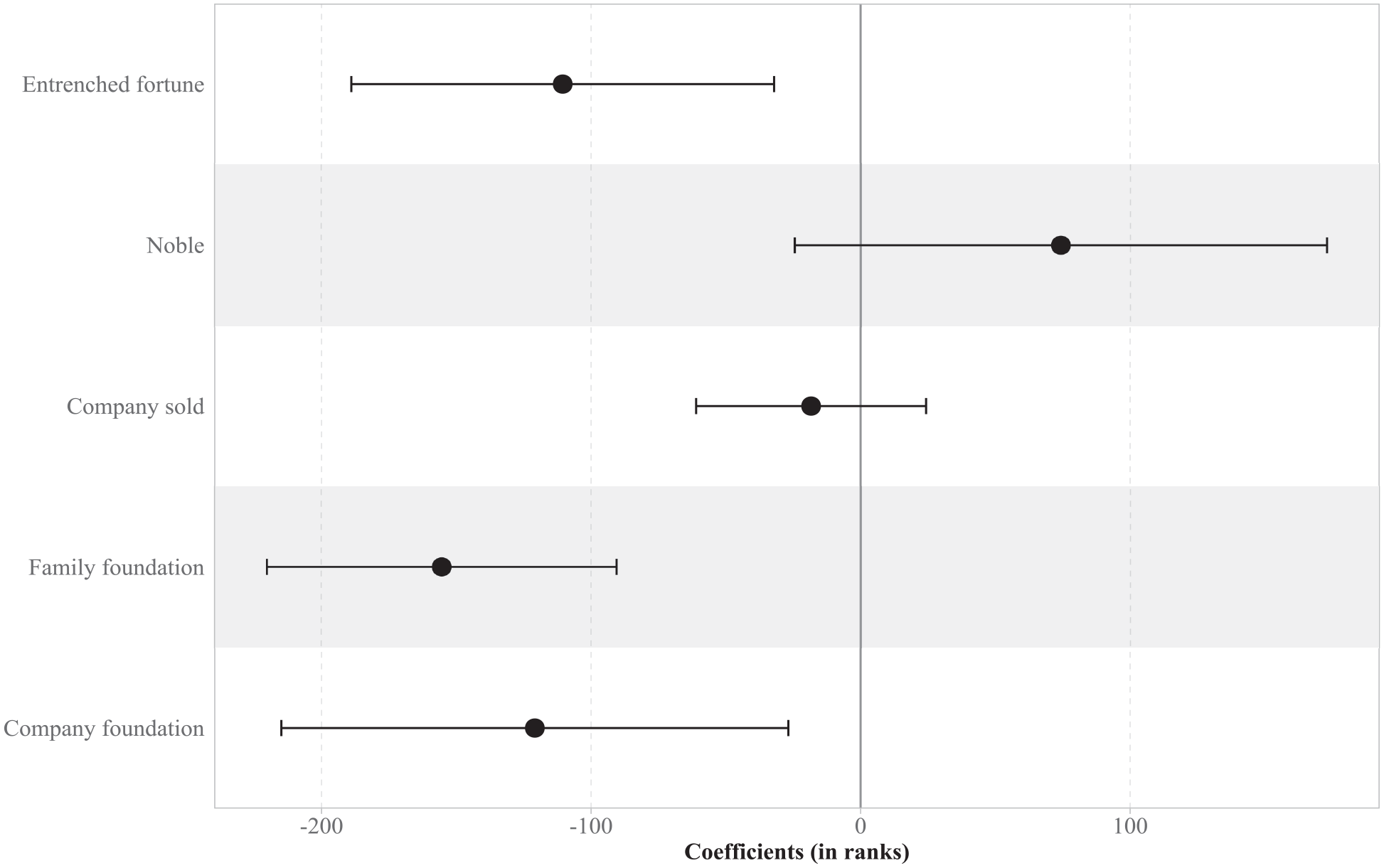

To examine if the entrenched fortunes differ from the other fortunes regarding their position within the wealth distribution, we estimated a multivariable regression with the rank of fortunes in the rich list as dependent variable (see Figure 3). 2 The predictor variable is a dummy variable indicating whether the fortune is entrenched. Adjusted for the other variables in the model, entrenched fortunes are on average listed 111 ranks higher than nonentrenched fortunes. This result is in line with Mills’s (2000) “accumulation of advantages” hypotheses.

Regression results.

In the following, we interpret the control variables. Controlling a family foundation or a company foundation is significantly related to the rank: fortunes connected to a family foundation are on average 155 ranks above fortunes without a family foundation and fortunes with a company foundation are listed on average 121 ranks higher than fortunes without a company foundation. The association between having a foundation and the level of wealth suggests that sophisticated wealth management tools are used to perpetuate fortunes (Beckert 2022). The causality, however, is unclear. Either larger fortunes provide more opportunities to establish a foundation or having a foundation helps accumulate larger fortunes, for example, because of tax benefits (Tait 2019). The ranks of fortunes are not significantly related to being held by members of the nobility versus nonmembers. Importantly, this nonsignificant correlation does not indicate whether noble families are more likely to perpetuate their wealth, only that the value of fortunes held by noble families does not seem to differ from that of non-noble families. The sale of a company is also not significantly linked to the rank in the rich list. However, to understand the long-term consequences of company sales and diversification of wealth portfolios, one would need to have longitudinal information on the development of the value of fortunes before and after the sale.

Kinship Webs

We now turn from the analysis of fortunes to the analysis of the individuals and families owning these fortunes and exploratively examine how the largest German fortunes are connected by kinship relations. Analyzing kinship webs alongside vertical wealth transmissions is crucial because it provides a broader understanding of the dynamics of wealth concentration and social closure at the top. By examining how fortunes are not only related to the past, but also how they are intertwined among each other, we gain insights into the internal integration of the wealth elite.

Our analysis aims to identify connections between today’s wealthiest individuals and their ancestors by examining family ties documented in Wikidata. To this end, we considered parents, children, relatives, and spouses as family members of the super-rich. Figure 4 depicts the comprehensive family networks, which encompass a total of 20,387 individuals. This figure comprises 76 individuals from the rich list in 1913, 193 individuals from the rich list in 2019, and 20,118 family members. Out of these 193 individuals, 26 possess entrenched fortunes, while 167 individuals have accumulated their wealth more recently.

Kinship webs of the German super-rich.

Figure 4 indicates that there exists one large family network including 15 individuals on today’s rich list (7 with entrenched fortunes and 8 with nonentrenched fortunes) and 46 individuals on the rich list from 1913. However, the figure also indicates that for most individuals Wikidata does not contain much information on their relatives. This applies, for instance, to Daniel Terberger, a business heir, who is linked only to his wife and two children in Wikidata. On the other hand, Karl Friedrich, Prince of Hohenzollern’s parents, siblings, spouses, and children are indicated, which might result from the public interest in and visibility of aristocracy.

Figure 5 zooms in on the largest kinship network, showing only the shortest paths between the rich individuals in 2019 (entrenched fortunes in blue, others in red, both labeled) and 1913 (depicted in yellow). In other words, we keep all rich individuals (1913 and 2019) but only the family members who connect the rich individuals. The smaller gray circles represent these family members. The ties between individuals indicate family relationships (spouses, children-parent, or other relatives).

Largest kinship web.

Let us look at how the fortunes in the largest family network are connected via family lines (see Figure 5). The graph illustrates that a small part of the German super-rich is strongly interconnected, both intra- and intergenerationally. In particular, we are interested in how entrenched fortunes are connected to fortunes of younger origins. In other words, is there evidence that members of the entrenched wealth elite close themselves off from the rest of the wealth elite? We find a few examples showing the opposite, namely family ties between the entrenched wealth elite and those with more recently established fortunes. For instance, Til Schweiger, actor and movie director, who does not stem from an old business family or aristocracy, is connected to fortunes from more than a century ago. His connection to entrenched fortunes comes through his daughter’s intimate relationship with the son of Frédéric Prince of Anhalt. The latter, in turn, was adopted by Marie Auguste Princess of Anhalt, who belongs to the noble Askanian family. Even though this connection seems to be arbitrary, we argue that Til Schweiger’s fame and wealth provided him and his daughter with social networks, enabling them to connect with the wealthy, aristocratic family of Anhalt. Til Schweiger is also connected to Albert Darboven, a business heir listed on the rich list of 2019, through Darboven’s marriage to Edda Princess of Anhalt. Besides families that have only recently joined the wealth elite, the kinship network also includes families who have accumulated their fortunes after World War II. For instance, Daniel Terberger is the chairman of the board of directors of the family business KATAG AG, a fashion service provider. Through his marriage to the Duchess Elisabeth Marie in Bavaria he is loosely connected to different families who were already rich at the beginning of the twentieth century. Another example is Albert Brenninkmeijer, the heir to the chain of fashion retail clothing stores C&A. Brenninkmeijer is married to Princess Carolina, the niece of Queen Beatrix of the Netherlands.

Thus, we can see various family linkages between aristocratic and entrepreneurial wealth. Because many family relations of the super-rich are not included in Wikidata, these networks of super-rich families through family ties are potentially much larger. Although the kinship webs should be interpreted cautiously because of the high amount of missing information on Wikidata, the identified kinship web hints at marital strategies as a mechanism of social closure within the wealth elite. Importantly, this seems to be the case not only for the nobility. Furthermore, it seems that the entrenched wealth elite does not close themselves off from the fortunes of younger generations.

Overall, these findings highlight the potential of kinship webs for understanding the wealth elite and their wealth reproduction. The existence of family linkages among the wealth elite implies the potential for the transmission and consolidation of wealth across generations because members of kinship networks are likely to exchange their resources (Farrell 1993). Furthermore, the identification of family connections between the entrenched wealth elite and individuals with more recently accumulated fortunes challenges the notion of complete isolation among the entrenched wealth elite.

Summary and Conclusion

Despite growing academic and public interest in wealth concentration, we know only little about the largest privately held fortunes. We contribute to the nascent literature on top wealth (e.g., Baselgia and Martínez 2022; Freund and Oliver 2016; Korom et al. 2017; Lu et al. 2021; Toft and Hansen 2022) by generating a novel dataset on the 1,032 largest fortunes in Germany 2019 and by examining the historical origins of today’s top wealth in three steps.

Step one was to examine the founding dates of the companies associated with the fortunes as a proxy of their year of origin. We showed that more than one third of Germany’s largest fortunes are associated with companies founded before World War I. Although foundation dates rarely coincide with the “big jump” (Mills 2000) of a fortune, many of today’s largest fortunes have a long history. We speculate that many of today’s fortunes are a result of wealth accumulation across more than one generation and benefited from the “accumulation of advantages” (Mills 2000) over generations.

In a second step we identified and analyzed fortunes that descend directly from the largest fortunes at the beginning of the twentieth century. Eight percent of today’s top 1,032 fortunes are entrenched, that is, they can be traced back to large fortunes held by the same family from 1912 to 1914. Because of its turbulent twentieth century, Germany is a particularly interesting case. We find evidence for a historical continuity of large fortunes despite two world wars, the Great Depression, regime changes, and different currency reforms. Moreover, entrenched fortunes differ from the fortunes of younger origin in terms of being part of the nobility, regional distribution, and their ranks in today’s rich list.

In the last step, we exploratively analyzed to what extent today’s largest fortunes are intertwined by family relationships and if the entrenched wealth elite closes itself off from the younger wealth elite. To this end, we studied kinship webs. We identified a large kinship web connecting 15 of today’s largest fortunes. This kinship web revealed marriage ties between the entrenched wealth elite and the rest of the wealth elite, providing evidence against the closure of the entrenched wealth elite. However, social closure tendencies of the total wealth elite became apparent. The marriage ties at the very top of the wealth distribution are clearly not random and are remarkable considering that we look at Germany’s top 0.01 percent of households. Because of the high amount of missing information on genealogical data, we can only provide first insights into marital homogamy at the very top of Germany’s wealth distribution and cannot specify its extent.

Our findings contribute to different current scholarly discussions on wealth inequality and top wealth ownership. First, the literature on wealth inequality is engaged in estimating the persistence of wealth across generations (Barone and Mocetti 2020; Clark and Cummins 2015; Hällsten and Kolk 2023). We add to this literature by focusing on the very top of the wealth distribution. By identifying the share of today’s top fortunes which survived for more than 100 years in a country marked by multiple social and economic crises, we emphasize the persistence of wealth at the very top. This is in line with prior literature showing that social persistence is largest at the top of society (Barone and Mocetti 2020; Hällsten and Kolk 2023).

Second, the literature discusses the role of the family for the long-term perpetuation of large fortunes (Beckert 2022; Bessière and Gollac 2023; Hällsten and Kolk 2023; Hällsten and Pfeffer 2017; Mare 2011; O’Brien 2023). Social stratification research has long focused on the individual and the nuclear family when explaining the stratification of life chances in society. We highlight that not only the nuclear family but the extended kinship web might be relevant for wealth preservation. As indicated by prior research, these kinship webs often serve as mechanisms for social closure and economic alliance building among the wealth elite (Chung, Lee, and Zhu 2021; Farrell 1993; Zeitlin 1974). The identification of kinship webs spun through marriages relates to prior research showing that marital homogamy is still an important mechanism of social closure today (Toft and Hansen 2022; Toft and Jarness 2021). Whereas prior studies impressively showed how elite families are intertwined through marriages in the Nineteenth and twentieth centuries by examining local elites (Farrell 1993; O’Brien 2023), this study showed that also today a country’s wealth elite is partly connected through complex kinship webs. Future research could build upon our findings and examine the consequences of these kinship webs. For example, are members of a dense kinship web of top wealth holders indeed more likely to have descendants who are also at the top of the wealth distribution? Thus, whereas this study aimed at describing today’s fortunes, future research could start from the past and test the role of kinship webs as a mechanism of wealth perpetuation quantitatively.

Last, research on the reproduction of top wealth is confronted with at least two problems related to data. One problem concerns the measurement of the wealth elite, a group which is commonly referred to as a hard-to-reach population. The other problem concerns the measurement of wealth reproduction because long-term data on family wealth is rare. In recent years, innovative datasets and methods have been developed. Some studies use surnames to estimate long-term social mobility at the top (Barone and Mocetti 2020; Clark and Cummins 2015), others use rich lists to estimate top wealth shares (Bach et al. 2019), again others manually generate datasets on local elites (O’Brien 2023). We used yet two other innovative approaches to study elites and wealth reproduction. First, we link rich lists from two successive centuries to identify the share of families who were already part of the wealth elite 100 years ago. Second, we use genealogical data to draw kinship webs. Using genealogical data stored in Wikidata, a free collaborative, multilingual database, enables researchers to study the kinship web of different kinds of elites. Drawing kinship webs uncovers hidden family relationships between seemingly unrelated families and puts these relationships to the foreground of the study of family wealth. Our study highlighted that today’s wealth elite consists not only of isolated families but that some families are embedded in large kinship webs, potentially contributing to durable inequality (Beckert 2022; O’Brien 2023).

This study comes with some limitations. The high amount of missing information on individuals and their family ties in Wikidata prevent an exact measurement of social closure at the very top of the wealth distribution. Furthermore, although rich lists, in contrast to survey or register data, have the big advantage of providing names that can be used to augment the data with publicly available information our dataset of the largest 1,032 fortunes comes with some caveats. Today’s rich list might be biased toward entrepreneurs because public records of companies are the most important source of information for wealth estimates. To acknowledge the uncertainty entailed in the wealth estimates, we only use ranks rather than the wealth estimates in our regressions. However, if fortunes consisting of diversified portfolios are systematically missing from the list, our estimates of the share of entrenched fortunes are likely to be biased.

In this study we highlighted that the accumulation and perpetuation of fortunes over many generations is an important feature of top wealth in Germany. One threat resulting from the perpetuation of fortunes in the hands of a few families is social closure at the top (Beckert 2022). Our study indicated that Germany’s top wealth strata are not as open as Schumpeter’s omnibus or hotel metaphor suggested. As other scholars have argued, the lack of new entries in the wealth elite carries the risk of the elite drifting away from the wider society, threatening social cohesion (Toft and Hansen 2022). Furthermore, the entrenched wealth elite identified in this study clashes with meritocratic principles. This could lead to social tensions: the broader population might perceive the super-rich as not deserving of their fortunes if they are based on their family background instead of competence (Rowlingson and Connor 2011). Yet another societal consequence of the persistence of fortunes might be entrenched power structures (Starr 2019). Further empirical research on the consequences of entrenched fortunes for society is urgently needed to assess these propositions.

Footnotes

Appendix

Acknowledgements

We thank the research group Economic Sociology at the Max Planck Institute for Societies and, in particular, Lukas Arndt, Jens Beckert, and Isabell Stamm for helpful comments on earlier versions of this article and Johanna Liebe for excellent research assistance.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is supported by the German Research Foundation (DFG), grant number BE 2053/11-1.