Abstract

In March 2021, the American Rescue Plan substantially increased the maximum per-child child tax credit (CTC). However, research has yet to explore educational investments associated with the CTC. Thus, the authors leverage a probability-based panel survey of CTC-eligible families across 49 states to examine how parents’ investments in tutoring and college savings relate to the degree to which parents believe that their children will have better lives than they did. Through mediation models, the authors find that even though families that used the CTC for tutoring and college savings perceived an impact, intentions were related only to increased optimism through actions for college savings. Moreover, through their moderation models, the authors find that the direct effects of using the CTC for college savings on increased optimism were significant only for lower income families and that converting savings plans into actions was substantially more common among families with previous savings experiences.

In 2020 and 2021, Congress passed a series of bills to mitigate the economic impacts wrought by the coronavirus disease 2019 (COVID-19) pandemic. Via direct payments to adults, forgivable loans to small businesses, emergency health care funding, and relief funding for state and local governments, the federal government issued more than $1 trillion in pandemic-related stimulus aid (U.S. Department of the Treasury n.d.). A substantial portion of this government relief funding, authorized largely through the American Rescue Plan, targeted supports to children and their families, including more than $189 billion to K–12 education and $76 billion to higher education (Jordan 2022). Schooling-focused debates persist over the impacts of pandemic-induced instructional disruptions on student learning (e.g., Goldhaber et al. 2022) and the sufficiency of the federal fiscal response to these disruptions (e.g., Gordon and Reber 2022). However, the federal fiscal response to the pandemic’s impacts on children was pursued not only through supporting schools but through supporting families as well.

One of the federal government’s major family support initiatives was a temporary expansion of the child tax credit (CTC). Originally legislated as part of the Taxpayer Relief Act of 1997, the CTC granted tax credits to families with children up to 16 years old (Hamilton et al. 2021). Originally a $400 credit per child, subsequent legislation increased the maximum credit to $2,000 (Hamilton et al. 2021). In March 2021, however, the American Rescue Plan increased the maximum per-child CTC to $3,000 for children 6 to 17 years old and to $3,600 for children younger than 6. This credit was fully refundable, meaning that households could receive the credit regardless of whether they had any tax liability. Additional changes included increasing the income phase-out threshold to $150,000 for married parents and $112,500 for single parents, expanding eligibility for very low income families, and changing a portion of its distribution to be allocated to recipients on a monthly basis rather than as a lump sum payment following tax filing (Hamilton et al. 2021).

Despite broad-based public support (Hamilton et al. 2021) 1 and significant evidence of the efficacy of the expanded CTC on a range of child and family outcomes (Curran 2021), including reductions in family hardships (Collyer et al. 2022), the expansion has proved to be short lived. Fall 2021 efforts to extend the expanded CTC through the Build Back Better Act ultimately fell short of necessary support in the Senate after being passed by the House of Representatives in November 2021 (Library of Congress 2022). Thus, the CTC ended in 2021. Despite myriad evidence finding no indication that the expanded CTC would significantly reduce employment and labor participation (Ananat et al. 2022; Lourie et al. 2022; Hamilton et al. 2021), 2 some detractors, including Senator Joe Manchin of West Virginia, opined that an expanded CTC would reduce recipient employment incentives (Adamczyk 2022).

The failure to extend the CTC is underscored by significant evidence as to its impact on child outcomes. Perhaps the most cited benefit of the expanded CTC is its effects on child poverty. One report estimated the decline in the number of children living in poverty due to the CTC to be as high as 3.8 million while the credit was active (Center on Poverty and Social Policy at Columbia University 2022; Parolin, Collyer, and Curran 2022). These figures expectedly reversed following the program’s expiration: in January 2022, 3.7 million more children were identified in poverty, a 41 percent month-over-month increase, from 12.1 percent to 17 percent. Black and Latino child populations experienced even larger increases in their respective poverty rates. Were the expanded CTC to be extended, it is estimated to reduce long-term child poverty by 34 percent and deep child poverty by 39 percent (Corinth et al. 2021).

In addition to addressing child poverty, the CTC can also be used to address social mobility through educational investments, such as tutoring and college savings. Given the strong relationship between poverty and child development (Gibson-Davis et al. 2022), these types of investments may be most salient for CTC recipients. Moreover, tutoring and college savings are especially important in the aftermath of COVID-19, as tutoring is frequently cited as a remedy to pandemic-induced learning disruptions (e.g., Kraft and Falken 2021), while national data from fall 2020 demonstrate large college enrollment gaps among low-income students (Hanover 2020). Nevertheless, research has yet to explore the degree to which parents intended to use the CTC for these types of investments, how these intentions relate to subsequent actions, and ultimately, how these actions relate to optimism about social mobility prospects.

To fill this gap in the research, we leverage a novel panel survey of CTC-eligible families across 49 states to examine how parents’ short-term investments in child tutoring and long-term investments in college savings relate to the degree to which parents believe that their children will have better lives than they did, a core tenet of what is often referred to as the “American dream.” In examining education-related CTC intentions and uses we seek to extend the body of evidence regarding the CTC’s effect on children by identifying pathways through which the CTC may alter parents’ optimism regarding their children’s future outcomes.

Given the time-limited nature of the expanded CTC, we are not able to observe objective, long-term social mobility outcomes. Nevertheless, on the basis of an expectancy-value theory of educational achievement—in which parents expectations of their children influence parents’ behaviors that ultimately influence children’s beliefs and behaviors (Wigfield and Eccles 2000)—research has demonstrated a consistent relationship between positive parental expectations and educational achievements (see, e.g., Neuenschwander et al. 2007). Thus, given the strong relationship between educational achievements and social mobility (Card 1999), subjective social mobility predictions in this context can serve as an important factor in predicting future social mobility. Here, subjective social mobility predictions, operationalized as parents’ optimism about their children’s social mobility prospects, can help us understand the degree to which educational investments may be associated with upward social mobility in the future. Beyond serving as a predictor of a child’s future social mobility, parents’ optimism about future social mobility prospects may be related to more immediate positive effects, such as positive parenting behaviors and youth motivational beliefs (Simpkins, Fredricks, and Eccles 2012). Furthermore, parents’ optimism about future social mobility prospects may also be related to more general senses of optimism, which has been found to have a profound impact on their children’s psychological and physical health, social connections, and overall well-being (Carver and Scheier 2014).

Understanding the link between parental optimism and CTC-funded investments in children can help improve our understanding of how the expanded CTC operated in family education decisions and, more broadly, further our understanding of the benefits of the CTC for low-income children and youth. Here, increased optimism may represent the long-term reach of the expanded CTC in its ability to affect children’s social mobility outcomes through educational investments that are often made by higher income families. At the same time, it is possible that making educational investments with the CTC may not be enough to move the needle in parental optimism; rather parents may view these investments as ways of “catching up” but not necessarily “getting ahead.” Given inequities in access to educational resources, this may be especially salient in educational investments. Moreover, even if the CTC generated additional educational investments that increase social mobility prospects overall, additional limitations can arise if disparities are found in investment plans, actions, and outcomes.

To effectively demonstrate both the promise and limitations associated with the CTC and educational investments, we employ a path model to examine how CTC uses and perceived impacts explain the relationship between CTC intentions and parental optimism (mediation), as well as how these relationships may vary across socioeconomic disparities and structural constraints (moderation). In particular, we examine how lower family income and lack of previous college savings alter relationships among CTC plans and actions, as well as their relationships with optimism. In examining actual uses of the CTC in our follow-up survey, administered immediately after the CTC payments ended, we observe a substantial gap between intentions and uses, but the overall patterns across indicators of race/ethnicity and income persist. Furthermore, through mediation models we find that even though families that used the CTC for tutoring and college savings perceived an impact, intentions were only related to increased optimism through actions for college savings. Moreover, through our moderation models, we find that the direct effects of using the CTC for college savings on increased optimism were only significant for lower income families and that converting savings plans into actions were substantially larger for families with previous savings experience.

Conceptual Framework and Expectations

Leveraging income data from birth cohorts from 1940 to 1984, Chetty et al. (2017) demonstrated that the “American dream” of social mobility—children earning more than their parents—was true for 90 percent of the children born in 1950, but that this rate fell to 50 percent for children born in 1980; this change was largely an artifact of unequal distributions across income groups. As education is often one of the strongest predictors of income (Card 1999), it is unsurprising that social mobility is strongest in areas with good schools (Chetty et al. 2014). Therefore, families who do not live in areas with good schools, many of whom are low income, may consider tutoring as a pathway to social mobility. Furthermore, as the financial costs of college can limit postsecondary opportunities, families may also consider college savings as a pathway to social mobility. When considering Graham’s (2017) recent work on pursuit of the American Dream, the trends associated with upward social mobility often translate into optimism, especially in relation to how parents perceive the social mobility prospects of their children. Thus, we conceptualize that investing in both tutoring and college savings will increase parents’ optimism about their children’s social mobility prospects.

In addition to broad notions of educational investments and optimism about social mobility prospects, it is also important to consider the ways in which low-income families make these investments, especially in the context of unconditional cash transfers that resemble the CTC. In Amorim’s (2021) recent study on the Alaska dividend, she demonstrated that low- and middle-income parents often use cash transfers to “catch up” to high-income parents by increasing child investments in areas like school expenses, extracurricular lessons, recreation, clothing, and electronics. As noted by Amorim, this confirms previous studies on unconditional cash transfers, demonstrating that when given the opportunity, low-income parents do tend to make short-term investments in their children’s education (see, e.g., Duncan, Huston, and Weisner’s [2007] study on the New Hope antipoverty experiment and Halpern-Meekin et al.’s [2015] study on the earned income tax credit [EITC] ). Although Amorim did not explore long-term investments, such as college savings, Nichols and Rothstein’s (2017) review of the EITC summarizes the positive effects of the EITC on both school performance and college enrollment.

Additionally, it is important to consider the relationships between intentions and actions with regard to educational investments, especially in the context of low-income families. Although the relationship between intentions and actions can be thought of as a process, such as those outlined in the transtheoretical model of change (see Prochaska, DiClemente, and Norcross 1992) and later applied to savings contributions (Gutter, Hayhoe, and Wang 2007), the CTC represents a different prospect to recipients. Instead of going through a decision-making process with current sources of income, CTC recipients are contemplating what to do with new sources of income across a range of spending categories. Here, initial intentions that are not later acted upon may reflect a need to invest in other areas. This may be especially prevalent among low-income households, who are more likely to experience income shocks and other unexpected hardships, especially during the pandemic (Enriquez and Goldstein 2020). In this regard, Amorim (2021) observed difficulties in maintaining child investments in the long run for low- and middle-income dividend recipients, which may point to the inability for low-income families to translate investment intentions into behaviors.

Finally, previous college savings experiences may also relate to the ability to convert investment intentions into actions, as these experiences may indicate that parents have access to investment tools, such as tax-advantaged college savings accounts, that can provide a concrete mechanism for parents to invest in their children’s future education. Indeed, research on individual development accounts has demonstrated that previously banked participants had more frequent deposits and higher amounts of savings (Grinstein-Weiss et al. 2010). More recent research has demonstrated that individuals with access to formal savings mechanisms (e.g., child savings accounts) are more likely to save for their children’s education than those without (Ansong et al. 2021; Elliott and Beverly 2011).

On the basis of this research, we construct conceptual models (Figures 1 and 2) in which CTC plans, actions, and perceived impact are directly and indirectly related to parents’ optimism about their children’s social mobility prospects. We make the following hypotheses:

Converting investment plans into actions: First, we explore the relationship between CTC plans and actions. The ability to convert plans into actions represents one of the first steps in improving optimism about a child’s social mobility prospects. Although we expect plans to be strongly related to actions, we recognize that family characteristics and previous experiences may moderate these relationships.

Hypothesis 1: Planned uses will have a positive direct effect on actual use, and that these effects will be larger for short-term, as opposed to long-term, investments.

Hypothesis 1a: These effects will be larger for higher income families and families with history of previous savings and investments. In this sense, the CTC may widen, rather than narrow, opportunity gaps.

Perceiving the impact of the CTC: Next, we explore the relationship among CTC plans, actions, and perceived impact. The ability for plans and actions to relate to perceived impact is especially important when considering optimism about a child’s social mobility outcomes. When we account for actual use, we would not expect the direct relationship between planned uses and perceived impact to be significant, as this may represent unfulfilled plans. However, we would expect planned uses to be indirectly related to perceived impact through actual use, as this represents the conversion of plans into actions. Moreover, we expect that families with previous college savings experiences might perceive a larger impact of the CTC, as they may be more likely to convert their plans into actions.

Hypothesis 2: Actual use will have a positive direct effect on perceived impact for both short- and long-term investments.

Hypothesis 3: Planned uses will not have a significant direct effect on perceived impact for either short- or long-term investments.

Hypothesis 3a: Planned uses will have a positive indirect effect on perceived impact through actual use for both short- and long-term investments.

Hypothesis 3ai: For long-term investments, these effects will be larger for families with higher incomes and a history of previous investments.

Increasing optimism: Finally, we explore the relationships among CTC plans, actions, perceived impact, and optimism. The ability for plans, actions, and perceived impact to relate to optimism provides an understanding of how parents perceive CTC investments to relate to social mobility and the ability of their children to achieve the “American Dream.” To understand this phenomenon, we simultaneously explore the direct relationship between CTC use and optimism, as well as the indirect relationship between CTC use and optimism through perceived impact, which represents the conversion of actions into impact. Similarly, we explore the direct and indirect effects of CTC plans. When we account for actual use and perceived impact, again, we would not expect the direct relationship between planned uses and optimism to be positive, but rather negative, as this could represent unfulfilled plans. However, we would expect planned uses to be indirectly related to perceived impact through actual use, as this represents the conversion of plans into actions and perceived impacts. Moreover, as the CTC will represent a larger proportion of a lower income household’s finances, we might expect that the relationship between educational investments to be larger for these families. Furthermore, as families with previous college savings experiences may be more likely to convert their plans into actions, we might expect the relationships among educational investments and optimism to be larger for these families.

Hypothesis 4: Perceived impact will have a positive direct effect on optimism for both short- and long-term investments.

Hypothesis 5: Actual use will have a positive direct effect on optimism for both short- and long-term investments.

Hypothesis 5a: Actual use will have a positive indirect effect on optimism through perceived impact for both short- and long-term investments.

Hypothesis 6: Planned uses will have a negative direct effect on optimism for both short- and long-term investments.

Hypothesis 6a: Planned uses will have a positive indirect effect on optimism through actual use and perceived impact for both short- and long-term investments.

Hypothesis 6ai: For long-term investments, these indirect effects will be larger for families with lower incomes and a history of previous college savings experiences.

Theoretical model: short-term investments.

Theoretical model: long-term investments.

Data and Sample

The data for this study come from a two-wave panel survey of CTC-eligible households (i.e., parents of tax dependent children younger than 18 years) who were drawn from an online, probability-based panel administered by NORC/AmeriSpeak. 3 The survey was administered at two points in time, with wave 1 being administered immediately before the first CTC payments were sent out (July 8–13, 2021) and wave 2 being administered soon after the final payments were sent out (December 27, 2021, to January 14, 2022). 4 The survey asked a variety of questions about households’ experience with and perceptions of the CTC, as well as questions about socio-demographic characteristics and household well-being indicators. 5 The survey took a median of 15 minutes to complete, and participants were offered a cash equivalent incentive of $5 for completing each survey wave.

The survey sample includes U.S. adults who were aged 18 to 65 years, had household incomes less than $150,000 (the threshold for maximum credit eligibility), and responded to both waves of the survey. Overall, the response rate to both waves of the survey was 8.4 percent, which included 1,209 CTC-eligible respondents. However, our final sample has two additional restrictions. First, we restrict our sample to only those households who reported both expecting to receive the CTC and actually receiving the CTC (n = 732). We do this because the purpose of our study is to explore the relationship between planned and actual uses of the CTC and parents’ perceptions of their children’s future, and we only asked about planned and actual CTC uses for those that expected to receive the CTC (in wave 1) and actually received the CTC (in wave 2). Second, we restrict our sample to only those who provided responses to all our key indicators (e.g., measures of CTC use, parents’ optimism), which resulted in a final analytical sample size of 632.

Table A1 in the Appendix presents the descriptive statistics for this sample. Roughly two thirds of the sample had more than one child, were between the ages of 30 and 44 years, and were female. Almost 80 percent were unmarried, and 37 percent had a bachelor’s degree or higher. The median respondent reported a 2020 household income of between $50,000 and $74,999. 6

Measures

Optimism about Social Mobility

Participants were asked how likely it was that “Your child will have a better life than you did.” Participants selected responses from a four-point, Likert-type scale: “very unlikely,” “somewhat unlikely,” “somewhat likely,” and “very likely.”

Planned Use

In wave 1, the CTC was described to respondents in the following manner: In early 2021, the federal government temporarily expanded the existing Child Tax Credit. If you are a parent, between July and December, 2021, you should receive $300 per month for each child age 0 to 5 and $250 per month for each child age 6 to 17.

Participants who expected to receive the CTC were then asked if they planned on using it for a variety of purposes. Pertaining to this study, participants were asked (“yes” or “no”) if they planned on using the CTC for “Hiring or spending more on tutors for your children” and “Starting/growing a college fund for your children.”

Actual Use

In wave 2, participants who reported receiving the CTC were asked a similar question to their planned CTC use in wave 1: “You said you received the expanded Child Tax Credit payments. How did you use these payments?” Response options to the actual use question also included options for tutoring and college funds.

Perceived Impact

CTC recipients were asked how much they agreed or disagreed with the following statements: “The Child Tax Credit payments allowed me to afford more or better tutoring for my child(ren)” and “The Child Tax Credit payments allowed me to save more for my child(ren)’s future education.” Participants selected responses from a five-point, Likert-type scale: “strongly agree,” “somewhat agree,” “neither agree nor disagree,” “somewhat disagree,” and “strongly disagree.”

Previous Investments

In wave 1, participants were also asked if they were currently saving for their children’s future education.

Income

Participants were asked to provide the total pretax income that their household received from all sources, such as wages, Social Security, pensions, annuities, or side jobs for 2020. A binary indicator was created from this measure (0 = $0–$59,999, 1 = ≥$60,000) to reflect the median household income of CTC respondents in wave 1 who also responded in wave 2.

Methods

To explore the relationships among CTC investments, use, perceived impact, and optimism, as well as how these relationships differ across family characteristics, we used a path-analysis approach. Path analysis allows the significance and strength of multiple hypothesized structural relationships to be simultaneously tested with mediating and moderating effects. Specifically, we used a multistep process in our analytic approach using Mplus (version 8).

First, we conduct a single-group path analysis to understand the mediating role of CTC use and perceived impact on the relationships between planned use and optimism (when controlling for previous optimism) for both short-term (tutoring) and long-term (college saving) investments. Second, we conduct a multigroup path analyses to understand the moderating effects of income and previous investments. Because of subsample size limitations, this is conducted for long-term investments only. To test moderating effects, structural paths are constrained, one at a time, to be equal across groups (Bowen and Guo 2011). Because models with new parameter constraints are nested within previous less restrictive models, χ2 difference tests can be used to determine whether more restrictive models have significantly poorer fit (Bowen and Guo 2011). If more restrictive models have worse levels of fit, then previous less restrictive models, in which parameters are allowed to vary across groups, are retained (Bowen and Guo 2011). The parameters that are allowed to vary across groups demonstrate a moderating effect of the group (Bowen and Guo 2011). 7 Within these models, we used a mean and variance-adjusted weighted least squares estimator, which involves both diagonal and full weight matrices to compute standard errors and is robust to non-normal distributions within our data. In doing so, we used a probit link function. Descriptive statistics for our sample can be found in Table 1.

Descriptive Statistics.

Results

Converting Investment Plans into Actions

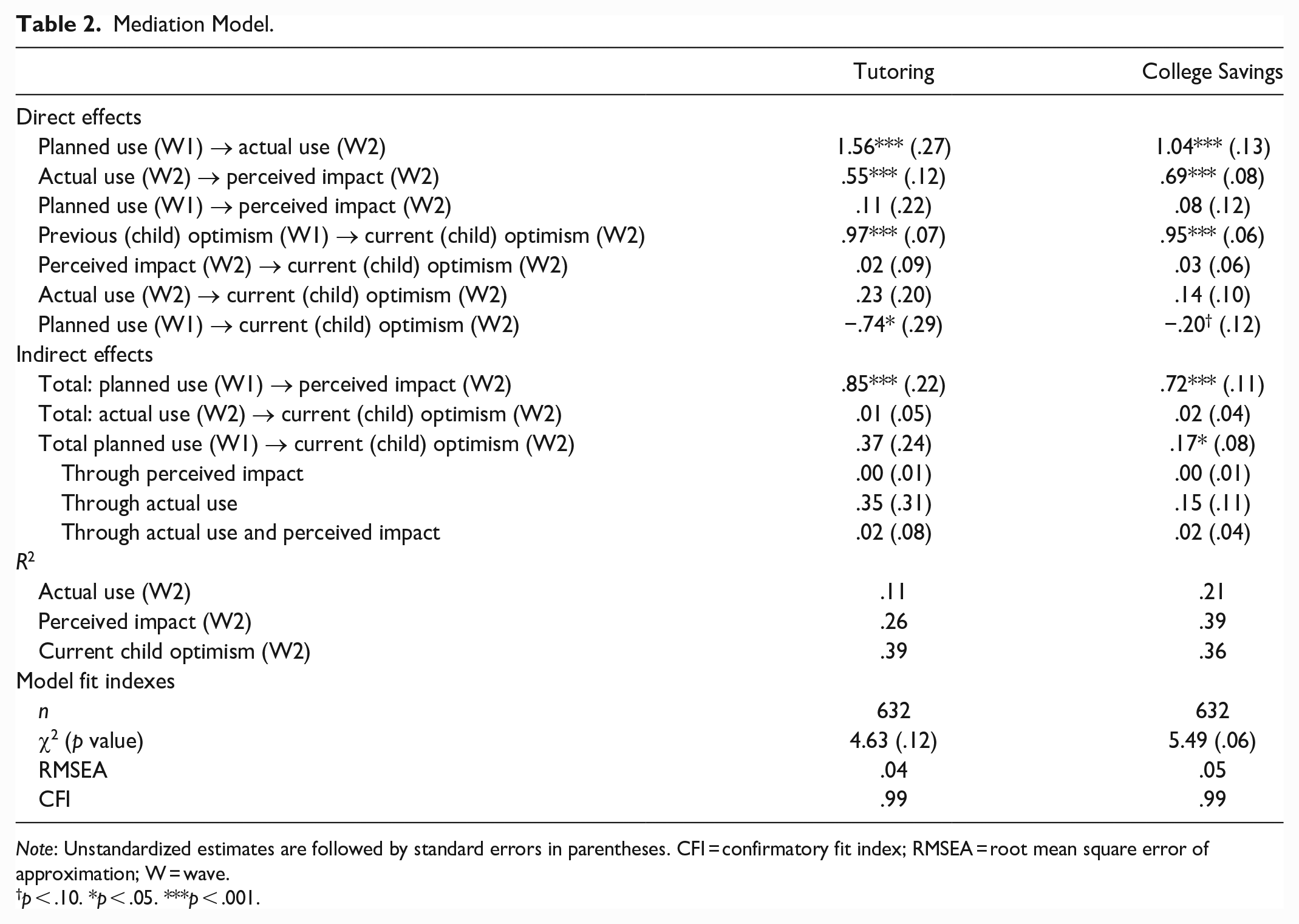

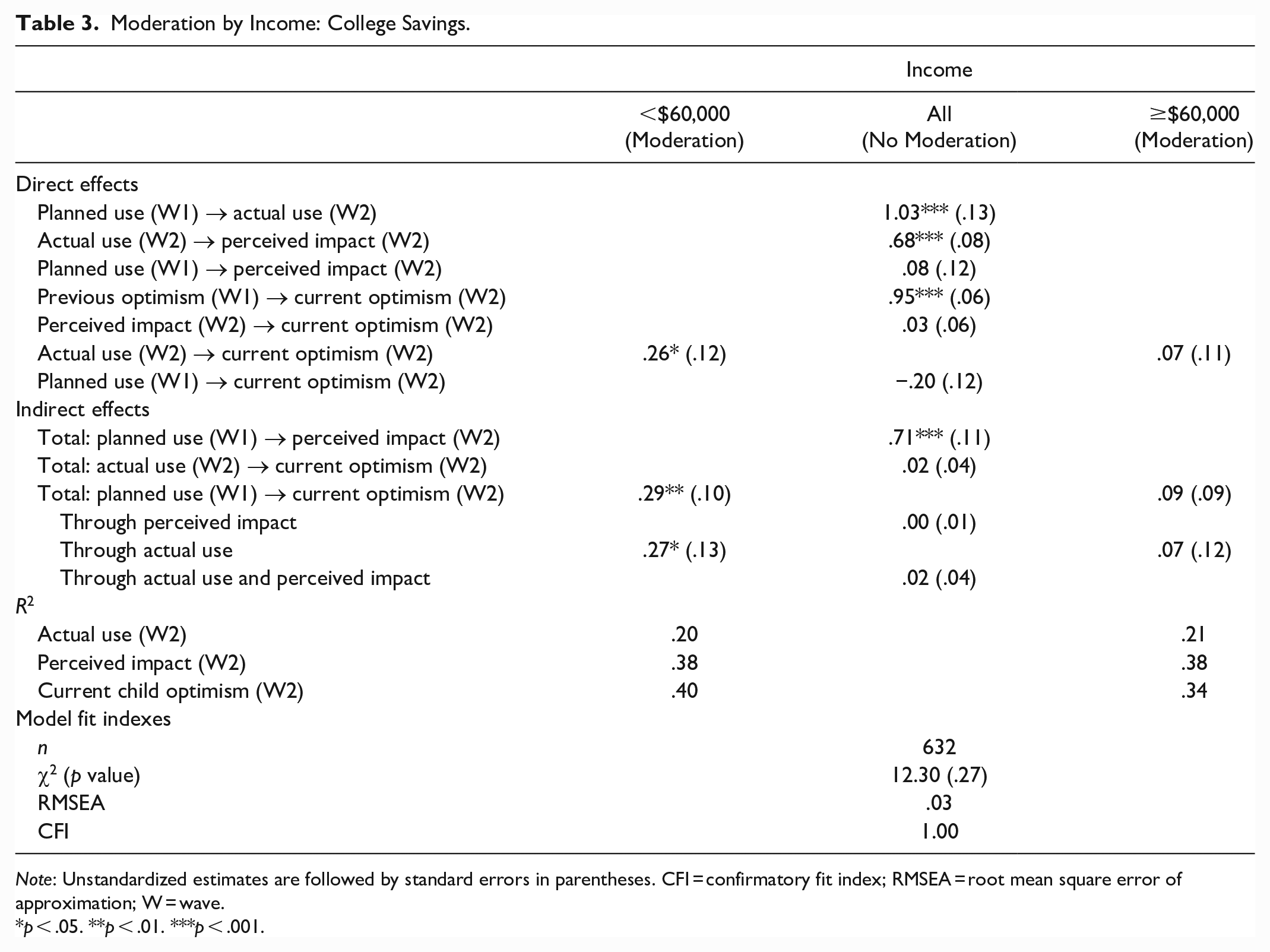

Mediation results for both short- and long-term child investments can be found in Table 2, while moderation results for long-term child investments can be found in Tables 3 and 4. Our findings confirm our first study hypothesis concerning investment actions, as we find that that planned uses have a positive direct effect on actual use (hypothesis 1) and that these effects are larger for short-term (tutoring: z = 1.56, p < .001), as opposed to long-term (saving: z = 1.04, p < .001), investments (Table 2). Our findings also partially confirm our moderation hypothesis concerning investment actions (hypothesis 1a), as we find a larger effect for those with previous college savings (z = 1.10, p < .001) than those without previous college savings (z = 0.56, p < .01) (Table 3).

Mediation Model.

Note: Unstandardized estimates are followed by standard errors in parentheses. CFI = confirmatory fit index; RMSEA = root mean square error of approximation; W = wave.

p < .10. *p < .05. ***p < .001.

Moderation by Income: College Savings.

Note: Unstandardized estimates are followed by standard errors in parentheses. CFI = confirmatory fit index; RMSEA = root mean square error of approximation; W = wave.

p < .05. **p < .01. ***p < .001.

Moderation by Previous Activity: College Savings.

Note: Unstandardized estimates are followed by standard errors in parentheses. CFI = confirmatory fit index; RMSEA = root mean square error of approximation; W = wave.

p < .10. *p < .05. **p < .01. ***p < .001.

Perceiving the Impact of the CTC

Our findings confirm our second and third study hypotheses, concerning perceived impact of the CTC (hypotheses 2 and 3), as we find that that actual use, but not planned uses, have a positive direct effect on perceived impact of the CTC for both short-term (tutoring: z = 0.55, p < .001) and long-term (saving: z = 0.69, p < .001) investments (Table 2). Our findings also confirm our mediation hypothesis concerning perceived impact of the CTC (hypothesis 3a), as we find that that planned use has a positive indirect effect on perceived impact through actual use for both short-term (tutoring: z = 0.85, p < .001) and long-term (saving: z = 0.72, p < .001) investments (Table 2). Similar to the moderation effect in investment actions, our findings confirm our moderated mediation hypothesis concerning perceived impact of the CTC (hypothesis 3ai), as we find a larger indirect effect for those with previous college savings (z = 0.79, p < .001) than those without previous college savings (z = 0.40, p < .05) (Table 4).

Increasing Optimism

Our findings do not confirm our fourth study hypothesis concerning optimism (hypothesis 4), as we do not find that perceived impact has a positive direct effect on optimism for either short- or long-term investments. Our findings also do not confirm our fifth study hypothesis (hypothesis 5), as we do not find that actual use has a positive direct effect on optimism for either short- or long-term investments. However, we detect marginally different models for income, finding a significant positive direct effect of actual use on increased optimism for households making less than $60,000 (savings: z = 0.26, p < .05) and no significant effect for families making $60,000 or more (Table 3). As there was no direct effect of perceived impact on optimism, it is unsurprising that the indirect effects on optimism involving perceived impact were also not observed. As such, our findings did not confirm hypothesis 5a.

Additionally, our findings confirm our sixth study hypothesis concerning optimism (hypothesis 6), as we find that planned uses had a significant negative direct effect on optimism for both short-term (tutoring: z = −0.74, p < .05) and long-term (savings: z = −0.20, p < .010) investments (Table 2). Our findings partially confirm our mediation hypothesis concerning planned uses and increased optimism (hypothesis 6a), as we find that planned uses had a positive indirect effect on optimism overall for long-term investments (saving: z = 0.17, p < .05) (Table 2). Finally, our findings confirm our moderated mediation hypothesis concerning planned uses and optimism (hypothesis 6ai), as we find that the overall indirect effects of planned uses on optimism (saving: z = 0.29, p < .01), as well as the specific indirect effects through actual use (saving: z = 0.27, p < .05) are significant only for families making less than $60,000 (Table 3). At the same time, we find that the overall indirect effects of planned uses on optimism are larger for families with previous savings (z = 0.17, p < .05), as opposed to families without previous savings (z = 0.09, p < .10) (Table 4).

Robustness Checks

Alternatively, given the hardships associated with the pandemic (Grinstein-Weiss et al. 2021), it is possible that unexpected household “shocks” may influence our results. For example, shocks may explain why wave 1 planned uses were negatively associated with wave 2 optimism. In this regard, we run a series of robustness checks with job, income, housing, and transportation shocks included in multivariate regression models that predict child optimism and include the same variables from our path analyses. However, shocks were not significantly associated with child optimism in these models, nor did the relationship between wave 1 planned uses and wave 2 optimism alter in their presence. We therefore can infer that shocks are not likely driving this particular relationship in our models. Nevertheless, as other potential confounders cannot be ruled out, these findings should be interpreted with caution.

Discussion

In this two-wave survey of American parents before and after the monthly CTC payments in 2022, we observed several significant trends. Some of these findings are fairly intuitive. For example, a greater proportion of families used the CTC for college savings than tutoring, which resembles the differences in their prevalence in the general population. Beyond these differences, the overall proportions are worthy to note: nearly two fifths (39.7 percent) of respondents planned on using the CTC for college savings and nearly one fifth (19.0 percent) of respondents actually used it for college savings. Although this demonstrates relatively high rates of using the CTC for long-term educational investments, it also demonstrates high rates of unfulfilled plans. Here, it is important to note that families were more likely to use the money as they originally intended when the payoff was imminent (e.g., tutoring), as opposed to distant (e.g., college savings). Furthermore, those with previous child college savings were more likely to actualize their savings intentions than those without. Moreover, parents who spent the CTC on tutoring and college savings agreed that the CTC made affording these things easier. Perhaps most important, these findings suggest that by reducing cost barriers to educational investments, unconditional cash support programs like the CTC can broaden access to social mobility.

Given the variation in use across race/ethnicity and income groups, the CTC can also be seen as increasing social and economic equity. For example, the proportion of Black families and, to a lesser extent, Hispanic families that planned to and actually used the CTC for tutoring far surpassed the proportion of White families: whereas 11.5 percent of Black families and 5.3 percent of Hispanic families used the CTC for tutoring, only 1.3 percent of White families used the CTC for tutoring. Similar trends were observed for college savings: whereas 36.5 percent of Black families and 23.7 percent of Hispanic families used the CTC for college savings, only 14.5 percent of White families used the CTC for college savings. Black and Hispanic families also had greater perceived impacts from the CTC in these investment areas. Moreover, the racial differences in college savings cannot be explained by income alone, as a lower proportion of low-income families used the CTC for college savings than higher income families.

These findings are similar to other research on CTC use patterns, which found that lower income CTC recipients were more likely to use the CTC on immediate or short-term needs such paying bills, paying down debt, and buying food, whereas higher income CTC recipients were more likely to use the CTC for longer term purposes like savings (Hamilton et al. 2021). This dynamic likely reflects the fact that low-income households have budgets that are almost entirely consumed by necessary expenses (Schanzenbach et al. 2016), whereas higher income households have relatively more budgetary slack that allows them more flexibility to save for long-term purposes such as college. Given this, it is not surprising that higher income households were more likely to report using the CTC for long-term child investments in our study, though it is interesting that Black and Hispanic households, who tend to have lower average incomes, report higher rates of using the CTC for college investments. This pattern, especially when considered alongside the higher rates of Black and Hispanic households using the CTC for tutoring, may indicate that Black and Hispanic households across the income spectrum disproportionately viewed the CTC as an opportunity to invest in their children.

However, we observed more complex relationships when exploring parental optimism regarding their children’s future that illuminate how nearly universal cash transfers, like the CTC, relate to social mobility outlooks. For example, planning to spend the money on tutoring or college savings in wave 1 was associated with overall declines in optimism in wave 2. As this finding could represent unfulfilled plans, there appears to be significant emotional consequences for not being able to invest in a child’s education as planned. Additionally, although we did not observe an overall direct effect of actual use and optimism, there were specific groups for whom optimism increased. For instance, parents making less than $60,000 per year who used the money on college savings had significant increases in optimism when controlling for wave 1 optimism, which was not the case for higher income households. Here, even though lower income parents had lower rates of planning to use and actually using the CTC for college savings, as seen in Table 1, when they were able to use it for college savings, their optimism increased, suggesting that the CTC could serve as a tool for accessing the American dream for those that are least likely to otherwise achieve it. Although the CTC represents a larger proportion of a lower income household’s finances, which may explain this trend, it is also important to note that many lower income households were disproportionally ineligible for the full CTC refunds in prior policy iterations (Curran and Collyer 2020). Overall, our finding that long-term (i.e., college savings) but not short-term (i.e., tutoring) educational investments were indirectly related to increased optimism may represent optimism’s relationship to “getting ahead” but not “catching up.”

Yet structural barriers, such as lack of a college savings accounts, could limit these trends, as we observe that parents who had already begun saving for their children’s education prior to the CTC were more likely to fulfill their plans of saving for college, which ultimately was associated with increased optimism. Finally, agreeing that the CTC made it easier to afford tutoring and college savings was not associated with gains in future optimism, suggesting that optimism is more about changes in actual behaviors, such as saving for college, rather than the mechanism that facilitates these behaviors. Ultimately, this trend may suggest limited political traction for the CTC and policies like it, as families, despite perceiving it to help them make investments in their children, did not attribute increased optimism to these perceptions.

These findings are limited by several factors. Most important, as our survey is based on self-reported behaviors of CTC recipients, we cannot verify these behaviors, nor can we ascertain the exact amount of the CTC that was allocated toward these self-reported behaviors. Future research should identify sources of administrative data that can help more fully understand CTC expenditure patterns. We also cannot observe long-term social mobility outcomes. Although parents’ optimism about their children’s social mobility prospects can be theoretically related to actual social mobility outcomes, it is possible these educational investments do not translate into future social mobility or, alternatively, that these investments do translate into future social mobility, but for some of these families, we do not observe increased optimism. Additionally, as we use a structural equation modeling framework to test hypothesized conceptual relationships, we recognize that we cannot control for selection bias, nor rule out all potential confounders. Finally, it is also important to note that although our study is adequately powered (0.79) to pick up moderate (root mean square error of approximation = 0.05) effect sizes (Moshagen and Erdfelder 2016), these estimates may differ for tests of group invariance. Future research should leverage Monte Carlo simulations to further explore power in these scenarios (Muthén and Muthén 2002).

Still, as one of the only in-depth investigations of the 2021 expanded CTC’s influence on child educational investments, this study carries several important implications. First, as parents with prior college savings were more likely to actualize their intentions, there is potential that similar future policies could exacerbate existing inequalities in wealth and education access unless structural barriers are addressed. As a result, universal educational savings accounts (Elliott and Beverly 2011) should be explored as a complementary policy measure. Second, it’s important to note that parents who intended to spend the money on child investments more often did. As research on their intended behaviors carries multiple limitations, including a possible social desirability bias (Bagozzi, Yi, and Nassen 1998), intentions are frequently dismissed in public policy conversations, as they are often deemed unable to predict actual behaviors. However, this study supports other work by Mendenhall et al. (2012) showing that benefit recipients’ predicted and actual expenditures of their refund are significantly related. As such, policy-makers should pay close attention to these trends. At the same time, future research should also consider what causes these plans to go unfulfilled at times.

Altogether, this research presents descriptive evidence that the expanded CTC allowed some families to make meaningful long-term investments in their children’s education but that the reach of the CTC in this regard was limited, as many families were not able to make these investments. Families who had hoped to use the funds on educational expenditures but were unable to actualize their intentions experienced declines in optimism about their children’s future. Nevertheless, low-income parents who were able to save experience increased optimism suggesting that this short-lived program allowed families to move closer to achieving the American dream, even if this progress was perhaps not as much as they had hoped for.

Footnotes

Appendix

Descriptive Statistics and Comparison with U.S. Census Bureau Household Pulse Survey Data.

| Sample % | Household Pulse Survey % | |

|---|---|---|

| Number of children | ||

| 1 | 22.63 | 36.93 |

| 2 | 38.29 | 36.46 |

| ≥3 | 39.08 | 26.61 |

| Respondent age | ||

| 18–29 years | 8.54 | 13.38 |

| 30–44 years | 67.88 | 60.85 |

| 45–59 years | 21.52 | 23.41 |

| ≥60 years | 2.06 | 2.36 |

| Respondent gender | ||

| Male | 31.8 | 39.88 |

| Female | 68.2 | 60.12 |

| Marital status | ||

| Married | 78.45 | 63.15 |

| Not married | 21.55 | 36.85 |

| 2020 household income | ||

| <$25,000 | 11.45 | 17.69 |

| $25,000–$49,999 | 20.51 | 28.16 |

| $50,000–$74,999 | 24.96 | 20.15 |

| $75,000–$99,999 | 18.6 | 15.32 |

| ≥$100,000 | 24.48 | 18.67 |

| Educational attainment | ||

| Less than high school | 1.9 | 8.97 |

| High school graduate or equivalent | 12.97 | 31.91 |

| Some college/associate’s/technical degree | 38.29 | 33.06 |

| Bachelor’s degree | 29.11 | 15.45 |

| Graduate/professional degree | 17.72 | 10.6 |

| Observations | 632 | 9,742–9,762 |

Note: Observations for income (n = 629) and marital status (n = 631) are slightly lower than those for other variables because of missing data. The Household Pulse Survey data are from the week 41 survey (December 29, 2021, to January 10, 2022), which captures a similar time period to the our study’s wave 2 survey.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The Annie E. Casey Foundation and the Humanity Forward Foundation.

1

Fifty-seven percent of expected CTC recipients indicated support for a permanent expansion, relative to 17 percent opposed.

2

3

Funded and operated by NORC at the University of Chicago, AmeriSpeak is a probability-based panel designed to be representative of the U.S. household population. Randomly selected U.S. households are sampled using area probability and address-based sampling, with a known, nonzero probability of selection from the NORC National Sample Frame. These sampled households are then contacted by U.S. mail, telephone, and field interviewers (face to face). The panel provides sample coverage of approximately 97 percent of the U.S. household population. Those excluded from the sample include people with only Post Office box addresses, some addresses not listed in the U.S. Postal Service Delivery Sequence File, and some newly constructed dwellings. Although most AmeriSpeak households participate in surveys on the Web, non-Internet households can participate in AmeriSpeak surveys by telephone. Households without conventional Internet access but having Web access via smartphones are allowed to participate in AmeriSpeak surveys on the Web. AmeriSpeak panelists participate in NORC studies or studies conducted by NORC on behalf of governmental agencies, academic researchers, and media and commercial organizations.

4

Here, it is important to note that the postsurvey went out before the next “missed” payment. Thus, even though there was political opposition to an extension of the CTC at this time, families likely would not have experienced a change in household finances yet. Nevertheless, it is still possible that the changing political climate of the CTC may have had an unobserved impact on child optimism.

5

The survey also included a comparison group of respondents who were ineligible for the CTC (e.g., parents of adult children, nonparents). However, as CTC nonrecipients (regardless of eligibility) are not the focus of this study, we omit discussion of this comparison group. For more details on the study, see Hamilton et al. (2022). Instead, our focus lies in understanding how CTC recipients actualized intentions to subsequent use and how CTC use may have been related to parental optimism. Akin to a within-subject design (e.g., Charness, Gneezy, and Kuhn 2012), we compare CTC recipient responses over a two-wave survey panel. Traditional comparison groups composed of untreated (or otherwise treated) participants comport well with many other research designs but offer a less salient comparison in this scenario. For example, nonparents do not receive the CTC (nor, by extension, do they invest in their children’s tutoring or higher education savings, for example) and higher earning parents may differ from lower earning parents in systematic ways related to our areas of inquiry. Here, it is important to note that the CTC has a relatively high income phase-out threshold, beginning at $150,000 for married taxpayers filing jointly, such that nonrecipient parents (or parents who receive lower amounts of the CTC) may be substantially different from full CTC recipients. On the other hand, in our design we are not able to definitively rule out the effects of concurrent phenomena (whether pandemic related or other) on changes to CTC recipients’ translation of optimism through CTC intentions and uses. Although a few research designs may be better situated to rule out these potential confounders (e.g., a regression discontinuity design estimated at the income threshold cutoff for any CTC receipt), our data and sample size do not allow such an analysis.

6

![]() also includes a comparison of our sample of CTC recipients against CTC recipients in the U.S. Census Bureau’s Household Pulse Survey. Compared to the Household Pulse Survey data, our sample had more children, was more likely to be female, had higher incomes, and higher educational attainment. These differences are likely driven in part by fundamental differences in sample construction. Our study sample is individuals who both expected to receive the CTC and actually did so, and who responded to both waves of a longitudinal survey. The Household Pulse Survey sample is simply those who actually reported receiving the CTC in a single cross-sectional wave.

also includes a comparison of our sample of CTC recipients against CTC recipients in the U.S. Census Bureau’s Household Pulse Survey. Compared to the Household Pulse Survey data, our sample had more children, was more likely to be female, had higher incomes, and higher educational attainment. These differences are likely driven in part by fundamental differences in sample construction. Our study sample is individuals who both expected to receive the CTC and actually did so, and who responded to both waves of a longitudinal survey. The Household Pulse Survey sample is simply those who actually reported receiving the CTC in a single cross-sectional wave.

7

This process is conducted one parameter at a time to see which parameters vary the most across groups; then, starting with these parameters, new constraints are added one at a time to test differences against previous models.